Attached files

| file | filename |

|---|---|

| 8-K - ZION BANCORPORATION 8-K 2-12-2013 - ZIONS BANCORPORATION, NATIONAL ASSOCIATION /UT/ | form_8k.htm |

February 11 - 14, 2013 Credit Suisse - 2013 Financial Services Forum

Forward-Looking Statements This presentation contains statements that relate to the projected or modeled performance or condition of Zions Bancorporation and elements of or affecting such performance or condition, including statements with respect to forecasts, opportunities, models, illustrations, scenarios, beliefs, plans, objectives, goals, guidance, expectations, anticipations or estimates, and similar matters. These statements constitute forward-looking information within the meaning of the Private Securities Litigation Reform Act. Actual facts, determinations, results or achievements may differ materially from the statements provided in this presentation since such statements involve significant known and unknown risks and uncertainties. Factors that might cause such differences include, but are not limited to: competitive pressures among financial institutions; economic, market and business conditions, either nationally, internationally, or locally in areas in which Zions Bancorporation conducts its operations, being less favorable than expected; changes in the interest rate environment reducing expected interest margins; changes in debt, equity and securities markets; adverse legislation or regulatory changes; and other factors described in Zions Bancorporation’s most recent annual and quarterly reports. In addition, the statements contained in this presentation are based on facts and circumstances as understood by management of the company on the date of this presentation, which may change in the future. Except as required by law, Zions Bancorporation disclaims any obligation to update any statements or to publicly announce the result of any revisions to any of the forward-looking statements included herein to reflect future events, developments, determinations or understandings. *

Overview Capital Capital Adequacy Allowance For Credit Losses Improvements to Profitability From Expected Capital Actions Profitability Net Interest Income Drivers Volume Rate/Spread Floors Cash/MBS Exposure Asset Sensitivity Fee Income and Non-interest Expense Financial Outlook Appendix Credit Quality Loans CDOs Agenda

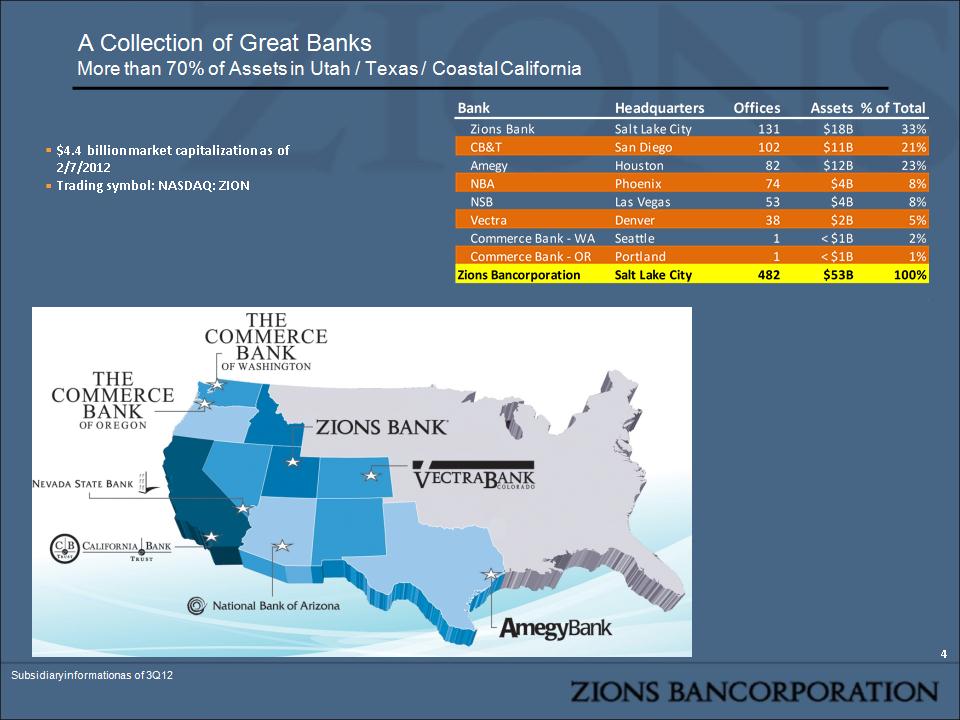

$4.4 billion market capitalization as of 2/7/2012 Trading symbol: NASDAQ: ZION A Collection of Great Banks More than 70% of Assets in Utah / Texas / Coastal California * Subsidiary information as of 3Q12

Awards: Nationally Recognized for Excellence Thirteen 2012 Greenwich Excellence Awards in Small Business and Middle Market Banking Including: Excellence: Overall Satisfaction Excellence: Likelihood to Recommend Excellence: Treasury Management Excellence: Financial Stability The Reputation Institute (cited in the American Banker): #2 Ranking Nationally Nationally Ranked in the Top 10 in Small Business Loan Originations 1 Top team of women bankers – American Banker Magazine2 * Greenwich.com; financial stability was based on responses from small business customers 1. Number of loans, SBA fiscal year ended September 30, 2012 2. One of five winning teams, 2012, Zions Bank

Overview Capital Capital Adequacy Allowance For Credit Losses Improvements to Profitability From Expected Capital Actions Profitability Net Interest Income Drivers Volume Rate/Spread Floors Cash/MBS Exposure Asset Sensitivity Fee Income and Non-interest Expense Financial Outlook Appendix Credit Quality Loans CDOs Agenda

Capital Levels are Strong Relative to Peers Source: SNL. Zion as of 4Q12; peers as of 3Q12. Loss absorbing capital defined to include tangible common equity, Basel III-qualifying non-common Tier 1 equity, and the allowance for credit losses *

Source: SNL. Zion as of 4Q12; peers as of 3Q12 CYN excluded from Reserve/NCO ratio due to ratio exceeding 2000% Annualized charge-off ratio. Reserves include loan loss reserve plus reserve for unfunded lending commitments. * Loan Loss Coverage is also Strong Comparatively

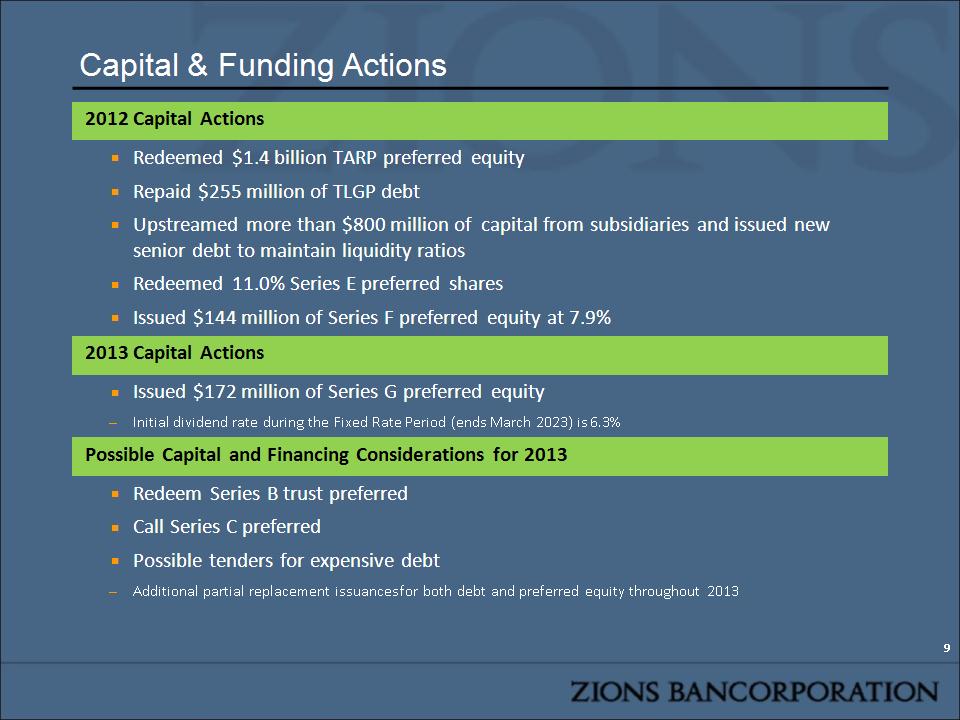

Capital & Funding Actions * 2012 Capital Actions Redeemed $1.4 billion TARP preferred equity Repaid $255 million of TLGP debt Upstreamed more than $800 million of capital from subsidiaries and issued new senior debt to maintain liquidity ratios Redeemed 11.0% Series E preferred shares Issued $144 million of Series F preferred equity at 7.9% 2013 Capital Actions Issued $172 million of Series G preferred equity Initial dividend rate during the Fixed Rate Period (ends March 2023) is 6.3% Possible Capital and Financing Considerations for 2013 Redeem Series B trust preferred Call Series C preferred Possible tenders for expensive debt Additional partial replacement issuances for both debt and preferred equity throughout 2013

Callable Capital and Debt Maturity Profile * Currently Callable

Restructuring Capital Profile: Significant Potential Earnings Improvement Assumes no change to revenue and noninterest expense * Not updated for Basel III Notice of Proposed Rulemaking Key assumptions for medium-term target capital stack: preferred stock dividend: 6.5% (after tax); subordinated debt interest rate: 5.5% (pre-tax); senior debt interest rate: 4.5% (pre-tax). Rates are based upon current market conditions and do not reflect possible changes to ratings or other macro events. $2,500 $0 4Q12 RoT1C excludes net gains/losses on securities and securities impairment charges (OTTI).

Overview Capital Capital Adequacy Allowance For Credit Losses Improvements to Profitability From Expected Capital Actions Profitability Net Interest Income Drivers Volume Rate/Spread Floors Cash/MBS Exposure Asset Sensitivity Fee Income and Non-interest Expense Financial Outlook Appendix Credit Quality Loans CDOs Agenda

Loan Balance Trends Modest Overall Growth; Stronger Performance from Commercial & Industrial and Consumer Offset by Declines in Owner Occupied and Construction & Development * Indexed 4Q11 = 100 Source: company documents

Net Interest Income: Loan Balances vs. Commitments Favorable Trend in Commitments Source: company documents *

New Loan Spread Stabilizing Older 2009-2010 Vintage Loans Are Maturing and Are Generally Replaced at Lower Rates Cost of Interest Bearing Deposits Spread on Production: New Business * Source: Company documents as of 4Q12. Spreads are calculated using matched-maturity funds at transfer pricing rate

Cash Impact on Net Interest Margin is Significant The Result of a Disciplined Effort to Avoid Adding Assets with Duration Extension Risk * Core net interest income excludes items that are one time or non-recurring in nature such as regular and accelerated discount amortization on convertible sub debt and additional accretion of interest income on FDIC loans. “Impact : Cash” refers to the adverse impact on the NIM due to the total balance of cash held in interest-bearing accounts. The calculation assumes all cash is invested into loans at a 4.5% yield.

Source: SNL as of 4Q12. ZION w/Peer Median Securities NIM & RANIM is calculated assuming Zions had a median 22% securities as a percentage of earning assets, with a median yield of 2.6%. Risk adjusted NIM calculated as net interest income less net charge-offs divided by average earning assets. Synovus excluded due to large NCOs in 4Q attributable to asset sales. * Net Interest Margin Remains Strong Relative to Peers Despite Zions’ Large Cash Balance & Short Duration of Loan Portfolio

Securities & Cash Portfolio ZION has the Smallest Securities (and MBS) Portfolio vs. its Peers; Securities Duration is ~1.8 years Source: SNL. ZION as of 4Q12; peers as of 3Q12 MBS securities include resi mortgage pass-through investments that are not guaranteed by the U.S. Government Estimated option-adjusted duration of loan portfolio ~ 1.4 years Estimated option-adjusted duration of cash portfolio ~ 0.1 years Estimated option-adjusted duration of securities portfolio ~ 1.8 years *

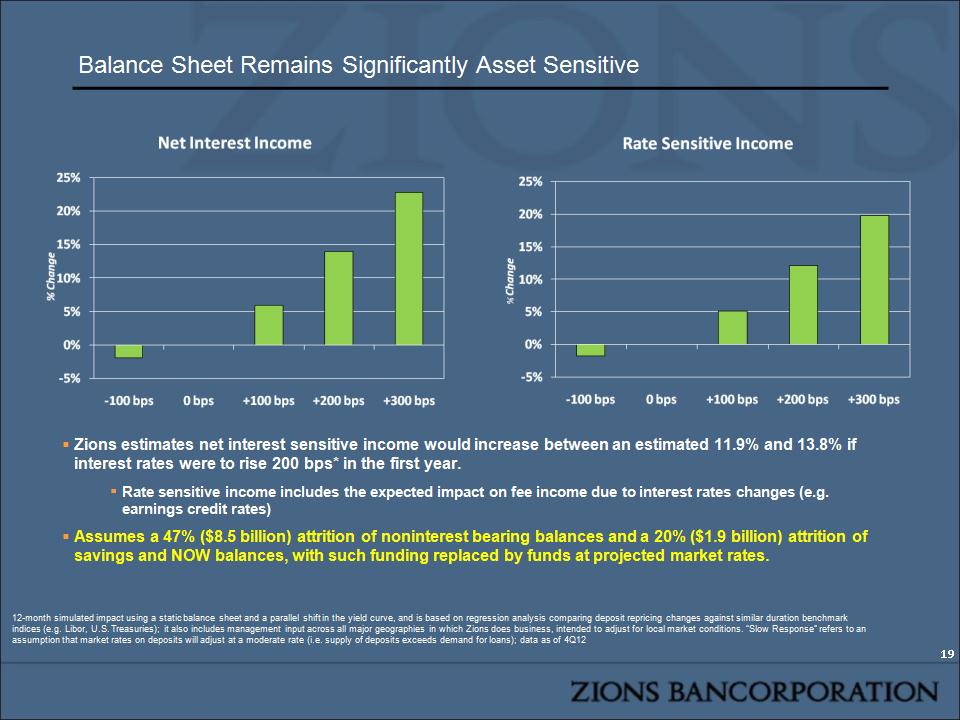

Balance Sheet Remains Significantly Asset Sensitive * Zions estimates net interest sensitive income would increase between an estimated 11.9% and 13.8% if interest rates were to rise 200 bps* in the first year. Rate sensitive income includes the expected impact on fee income due to interest rates changes (e.g. earnings credit rates) Assumes a 47% ($8.5 billion) attrition of noninterest bearing balances and a 20% ($1.9 billion) attrition of savings and NOW balances, with such funding replaced by funds at projected market rates. 12-month simulated impact using a static balance sheet and a parallel shift in the yield curve, and is based on regression analysis comparing deposit repricing changes against similar duration benchmark indices (e.g. Libor, U.S. Treasuries); it also includes management input across all major geographies in which Zions does business, intended to adjust for local market conditions. “Slow Response” refers to an assumption that market rates on deposits will adjust at a moderate rate (i.e. supply of deposits exceeds demand for loans); data as of 4Q12

Noninterest Income & Expense Trends * (In millions) Indexed as of 2Q11 * Credit category includes other real estate, credit related, and provision for unfunded lending commitment expenses. ** Regulatory & legal category includes legal & professional, FDIC premium and indemnification expenses. (In millions)

Consistently Profitable and Improving Earnings Quality High Cost Capital at Parent is the Primary Difference vs. Healthy Profitability at Subsidiaries * Source: Company documents (In millions)

Overview Capital Capital Adequacy Allowance For Credit Losses Improvements to Profitability From Expected Capital Actions Profitability Net Interest Income Drivers Volume Rate/Spread Floors Cash/MBS Exposure Asset Sensitivity Fee Income and Non-interest Expense Financial Outlook Appendix Credit Quality Loans CDOs Agenda

Topic Outlook Comment Loan Balances Stable to Moderately Higher Strong year-end growth not reversed in 1Q2013 Growth Driven Primarily by C&I and Consumer Core Net Interest Income Stabilizing - Slightly improving loan growth; Loan yield pressures moderating after mid-year Provision for Loan Losses Very Low Core Noninterest Income1 Stable to Moderately Higher Noninterest Expense Stable - Moderately Higher Salary Offset By Reduced Credit-Related NIE Preferred Dividends Mixed Rising moderately in the near term; expected to decline if Series C shares are called in 3Q13 Net Income Available to Common Increasing Excluding expenses related to possible tender for high cost debt and near-term increase in preferred dividend. One-Year Outlook Summary Vs. 4Q12 Results * Excludes gains / losses on securities (including OTTI) and other select items that are considered unlikely to recur on a consistent basis.

Overview Capital Capital Adequacy Allowance For Credit Losses Improvements to Profitability From Expected Capital Actions Profitability Net Interest Income Drivers Volume Rate/Spread Floors Cash/MBS Exposure Asset Sensitivity Fee Income and Non-interest Expense Financial Outlook Appendix Credit Quality Loans CDOs Agenda

Credit Quality is Improving and Losses are Better Than Peers For Zions, Net Charge-offs Have Returned to Pre-Crisis Levels Nonperforming ratio does not include accrual TDRs. Source: Company Documents & SNL Financial Net charge-off ratios annualized. * (In millions) (In millions)

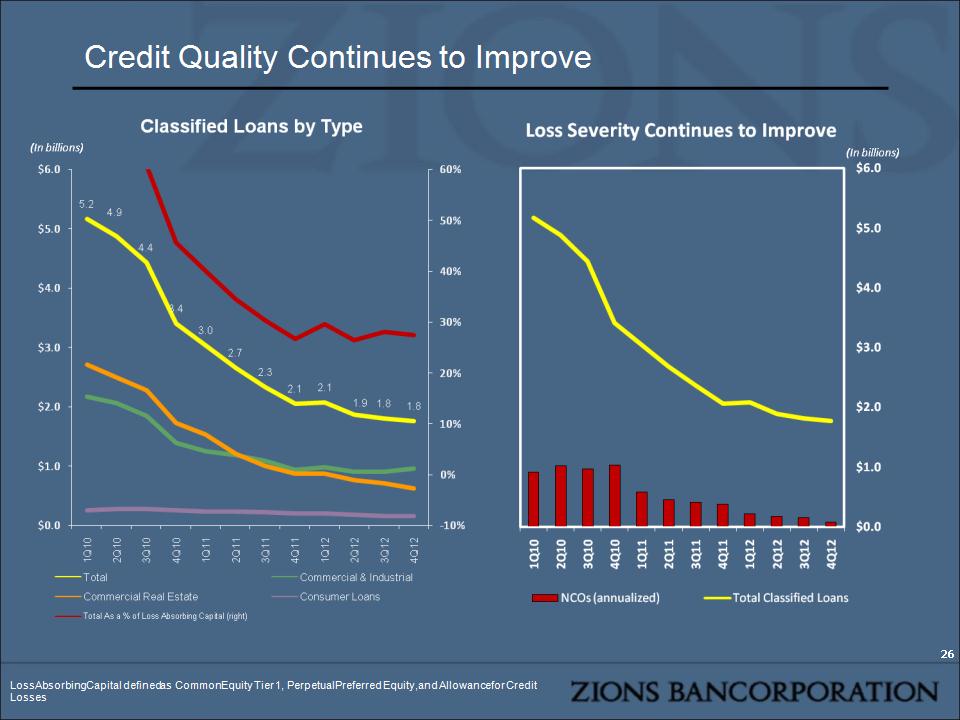

* Credit Quality Continues to Improve Loss Absorbing Capital defined as Common Equity Tier 1, Perpetual Preferred Equity, and Allowance for Credit Losses

(In billions) Weighted Average LTV = 60.2% Left - Sample data: As of 12/31/12; non-FDIC supported term loans > $500k balance; 76% of term loan dollars outstanding Right - As of 12/31/12; LTV’s were adjusted using PPR’s market level/property type value trend indices * Term CRE Metrics are Solid Percentage of loans within each bucket that are nonaccrual

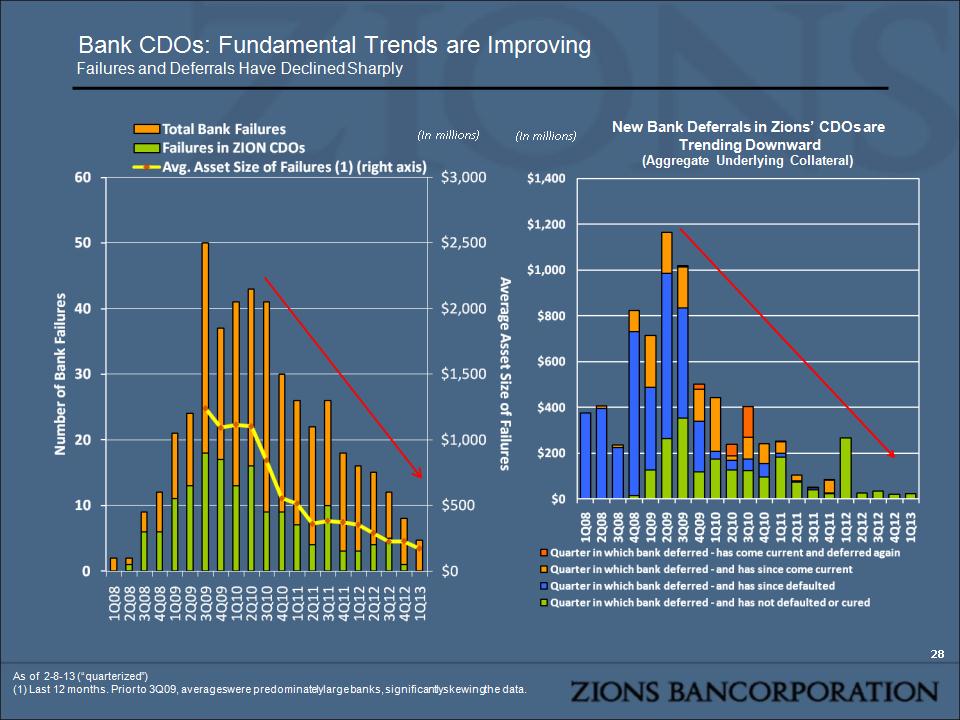

Bank CDOs: Fundamental Trends are Improving Failures and Deferrals Have Declined Sharply * As of 2-8-13 (“quarterized”) (1) Last 12 months. Prior to 3Q09, averages were predominately large banks, significantly skewing the data. New Bank Deferrals in Zions’ CDOs are Trending Downward (Aggregate Underlying Collateral) (In millions) (In millions)

Bank CDOs: Fundamental Trends are Improving Deferring Bank Re-performance has Increased * As of 2-8-13 (“quarterized”) * (In millions) Net of $220 million of re-deferrals from 8 banks Total underlying collateral supporting Zions’ bank CDOs: $17 billion Peak dollar value of deferring collateral: $3.5 billion (2Q11) Current deferring collateral: $2.3 billion

Bank CDOs: What To Expect Should the Environment Continue to Improve A Net Positive Impact to Tangible Common Equity per Share Prepayments Increase... As banks become more healthy and as Trust Preferred is considered to be a weaker form of capital, the more healthy banks are prepaying principal and interest Zions reviews evidence of prepayments as the basis for a change in the constant prepayment rate (CPR) assumption in the CDO valuation model, which assumption applies to future periods … Which May Trigger OTTI Due to Reduced Cash Flow to Junior Tranches Zions currently assumes a 10% CPR for small banks (<$15 billion in assets) for the 2013-2015 period, followed by a 3% CPR from 2016 through the maturity of the CDO. Cash flows from the underlying collateral is generally diverted to the senior tranches first. If the combined CPR speed assumptions are increased based upon market conditions, the reduction in underlying collateral in the CDO results in reduced overall cash flow to cover principal and interest payments to the junior tranches As a result, OTTI is taken on these junior tranches …Which Triggers Favorable AOCI , Gains on Previously Written-Down Securities Any OTTI taken on available-for-sale securities improves AOCI1 Additionally, because of the shorter expected time to receive cash flows in the senior tranches, the present value of the cash flows improves Some gains have been realized on senior tranches as payoffs exceeded amortized cost. This is similar to what happens when a loan pays off at a certain value, but had been previously charged down to an amount less than the payoff value. * Assumes other key variables, such as discount rates used to calculate the present value of cash flows remain stable compared to 4Q12.

What Happens if Things get Better? A Net Positive Impact to TCE/Share Bank & Ins. CDO Portfolio Scenario Assumptions Bank & Ins. CDO Portfolio Scenario Assumptions Bank & Ins. CDO Portfolio Scenario Assumptions Bank & Ins. CDO Portfolio Scenario Assumptions After-tax TCE per Share Impact After-tax TCE per Share Impact After-tax TCE per Share Impact After-tax TCE per Share Impact CPR Speed Spread Improves WA Spread to LIBOR From OTTI From AOCI Total Net %TCE/Share Base 10% -- 8.6% Scenario 1 13% 20% 6.9% $(0.02) $0.51 $0.50 2.4% Scenario 2 16% 40% 5.2% $(0.04) $1.14 $1.09 5.2% Scenario 3 19% 60% 3.4% $(0.08) $1.86 $1.78 8.5% * OTTI would be partially offset by securities gains from more senior tranches being paid down at par (Lockhart securities purchased at a discount) CPR Speed applied for 2013-2015 period, followed by a 3% CPR from 2016 through the maturity of the CDO (In millions)

Capital Structure Cost Savings Opportunities: 2013-2015 Capital Issue ($ in millions, except per share figures) Earliest Call or Maturity Date AFTER-Tax Rate Par Amount Out Book Amount Out Current Expense EPS Impact AFTER-Tax Replace-ment Cost Potential EPS Savings High Cost Issues High Cost Issues High Cost Issues High Cost Issues High Cost Issues High Cost Issues High Cost Issues High Cost Issues Series B Trust Preferred (8.0% rate) Currently Callable @ Par 4.9% $294 $294 $0.08 2.8% $0.03 Series C Preferred Stock (9.5% rate) 9/15/2013 @ Par 9.5% $798 $924 $0.41 5.6% (1) $0.17 Convert Sub Debt–5.65% May 2014 5/15/2014 (maturity) 16.2% $76 $58 $0.05 2.8% (2) $0.04 Senior Debt – 7.75% Sep 2014 9/23/2014 (maturity) 6.8% $500 $480 $0.17 2.8% $0.10 Convert Sub Debt–6.0% Sep 2015 9/15/2015 (maturity) 14.3% $195 $128 $0.10 2.8% (2) $0.07 Convert Sub Debt–5.5% Nov 2015 11/16/2015 (maturity) 13.4% $187 $122 $0.09 2.8% (2) $0.06 All amounts as of 4Q12; Sub debt after-tax rates are high due to the significant difference between book value and par, as well as the non-cash regular discount accretion. The table above does NOT include the effect of “accelerated” amortization expense, which occurs upon conversion. * Assumes $600 million is replaced with non-cumulative perpetual preferred at a dividend rate of 6.5%, while the remainder is replaced with senior debt at an after-tax rate of 2.8% Replacement cost assumes no reduction in volume (i.e. 100% replacement); however, some reduction in volume would be consistent with our medium-term target

Capital Structure Cost Savings Opportunities: 2013-2015 Capital Issue ($ in millions, except per share figures) Earliest Call or Maturity Date AFTER-Tax Rate Par Amount Out Book Amount Out Current Expense EPS Impact AFTER-Tax Replace-ment Cost Potential EPS Savings Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Additional Select Issues Outstanding Series A Preferred Stock (90D L+52 floater w/ 4.0% floor) Currently Callable @ Par 4.0% $60 $60 $0.01 NM NM Sub Debt–5.65% May 2014 5/15/2014 (maturity) 3.4% $30 $31 $0.01 2.8% (2) NM Sub Debt–6.0% Sep 2015 9/15/2015 (maturity) 3.5% $42 $45 $0.01 2.8% (2) NM Sub Debt–5.5% Nov 2015 11/16/2015 (maturity) 3.3% $62 $66 $0.01 2.8% (2) NM Senior Debt – 4.0% Jun 2016 6/20/2016 (maturity) 2.6% $198 $191 $0.03 2.8% NM Senior Debt – 4.5% Mar 2017 3/27/2017 (maturity) 3.4% $400 $384 $0.06 2.8% NM Series F Preferred Stock (7.9% rate) 6/15/2017 @ Par 7.9% $144 $144 $0.06 6.5% NM Series G Preferred Stock (6.3% fixed rate for 10 yrs, thereafter floating at 90D L+424 bps) 3/15/2023 @ Par 6.3% $172 $172 $0.06 6.5% NM All amounts as of 4Q12; Sub debt after-tax rates are high due to the significant difference between book value and par, as well as the non-cash regular discount accretion. The table above does NOT include the effect of “accelerated” amortization expense, which occurs upon conversion. * Assumes $600 million is replaced with non-cumulative perpetual preferred at a dividend rate of 6.5%, while the remainder is replaced with senior debt at an after-tax rate of 2.8% Replacement cost assumes no reduction in volume (i.e. 100% replacement); however, some reduction in volume would be consistent with our medium-term target