Attached files

| file | filename |

|---|---|

| 8-K - FIRST M&F CORPORATION 8-K 2-6-2013 - FIRST M&F CORP/MS | form8k.htm |

| EX-99.1 - EXHIBIT 99.1 - FIRST M&F CORP/MS | ex99_1.htm |

EXHIBIT 99.2

Merger of Renasant Corporation

and First M&F Corporation

February 7, 2013

and First M&F Corporation

February 7, 2013

2

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation

Reform Act of 1995. Congress passed the Private Securities Litigation Act of 1995 in an effort to encourage corporations to

provide information about companies’ anticipated future financial performance. This act provides a safe harbor for such

disclosure, which protects the companies from unwarranted litigation if actual results are different from management

expectations. This release contains forward looking statements within the meaning of the Private Securities Litigation Reform

Act, and reflects management’s current views and estimates of future economic circumstances, industry conditions, company

performance, and financial results. These forward looking statements are subject to a number of factors and uncertainties which

could cause Renasant’s, M&F’s or the combined company’s actual results and experience to differ from the anticipated results

and expectations expressed in such forward looking statements. Forward looking statements speak only as of the date they are

made and neither Renasant nor M&F assumes any duty to update forward looking statements. In addition to factors previously

disclosed in Renasant’s and M&F’s reports filed with the SEC and those identified elsewhere in presentation, these forward-

looking statements include, but are not limited to, statements about (i) the expected benefits of the transaction between Renasant

and M&F and between Renasant Bank and Merchants and Farmers Bank, including future financial and operating results, cost

savings, enhanced revenues and the expected market position of the combined company that may be realized from the

transaction, and (ii) Renasant and M&F’s plans, objectives, expectations and intentions and other statements contained in this

presentation that are not historical facts. Other statements identified by words such as “expects,” “anticipates,” “intends,”

“plans,” “believes,” “seeks,” “estimates,” “targets,” “projects” or words of similar meaning generally are intended to identify

forward-looking statements. These statements are based upon the current beliefs and expectations of Renasant’s and M&F’s

management and are inherently subject to significant business, economic and competitive risks and uncertainties, many of

which are beyond their respective control. In addition, these forward-looking statements are subject to assumptions with respect

to future business strategies and decisions that are subject to change. Actual results may differ materially from those indicated

or implied in the forward-looking statements.

Reform Act of 1995. Congress passed the Private Securities Litigation Act of 1995 in an effort to encourage corporations to

provide information about companies’ anticipated future financial performance. This act provides a safe harbor for such

disclosure, which protects the companies from unwarranted litigation if actual results are different from management

expectations. This release contains forward looking statements within the meaning of the Private Securities Litigation Reform

Act, and reflects management’s current views and estimates of future economic circumstances, industry conditions, company

performance, and financial results. These forward looking statements are subject to a number of factors and uncertainties which

could cause Renasant’s, M&F’s or the combined company’s actual results and experience to differ from the anticipated results

and expectations expressed in such forward looking statements. Forward looking statements speak only as of the date they are

made and neither Renasant nor M&F assumes any duty to update forward looking statements. In addition to factors previously

disclosed in Renasant’s and M&F’s reports filed with the SEC and those identified elsewhere in presentation, these forward-

looking statements include, but are not limited to, statements about (i) the expected benefits of the transaction between Renasant

and M&F and between Renasant Bank and Merchants and Farmers Bank, including future financial and operating results, cost

savings, enhanced revenues and the expected market position of the combined company that may be realized from the

transaction, and (ii) Renasant and M&F’s plans, objectives, expectations and intentions and other statements contained in this

presentation that are not historical facts. Other statements identified by words such as “expects,” “anticipates,” “intends,”

“plans,” “believes,” “seeks,” “estimates,” “targets,” “projects” or words of similar meaning generally are intended to identify

forward-looking statements. These statements are based upon the current beliefs and expectations of Renasant’s and M&F’s

management and are inherently subject to significant business, economic and competitive risks and uncertainties, many of

which are beyond their respective control. In addition, these forward-looking statements are subject to assumptions with respect

to future business strategies and decisions that are subject to change. Actual results may differ materially from those indicated

or implied in the forward-looking statements.

3

|

Consideration:

|

100% stock (tax-free exchange)

Fixed exchange ratio of 0.6425x

|

|

Implied Price Per Share:

|

$12.35(1)

|

|

Aggregate Value:

|

$118.8 million(1)(2)

|

|

CDCI Preferred Stock and TARP Preferred

Warrant Treatment: |

$30.0 million CDCI to be redeemed in full prior to close

TARP warrants to be repurchased at close

Repurchase price to be negotiated with US Treasury

|

|

Board Seats:

|

Two current members from FMFC to be added to RNST’s board

of directors |

|

Ownership:

|

FMFC pro forma ownership will be approximately 20%

|

|

Required Approvals:

|

Customary regulatory approval, RNST and FMFC shareholder

approval |

|

Expected Closing:

|

Third quarter 2013

|

(1) Based on RNST’s 10 day average closing price as of February 4, 2013 of $19.22

(2) Does not include consideration to repurchase TARP warrants

4

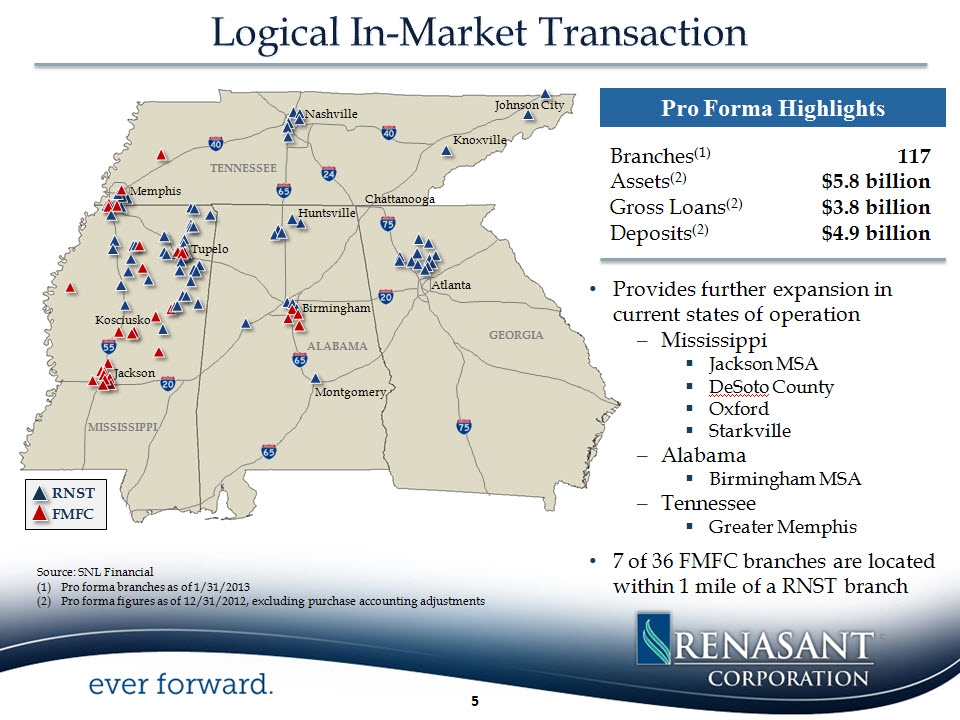

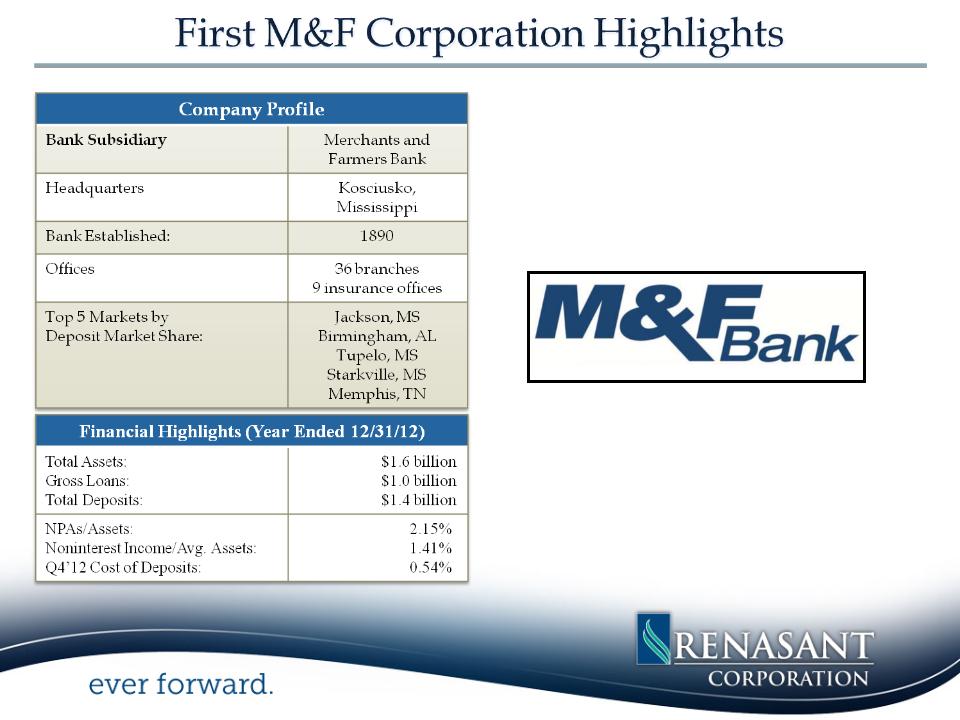

þ Strategically advantageous

• Acquisition of 120+ year old bank with quality core customer base

– Combination of two 100+ year old institutions

• In-market transaction consistent with our acquisition philosophy

• Creates the 4th largest bank by pro forma deposit market share in Mississippi

– Strengthens position throughout existing footprint and provides entrance into new markets

• Enhances fee revenue businesses of insurance, mortgage, and wealth management

• Complementary cultures and strong ties to community

• Strong, stable deposits and earnings generation complement de novo and out-of-state market

expansion activities

expansion activities

þ Financially attractive

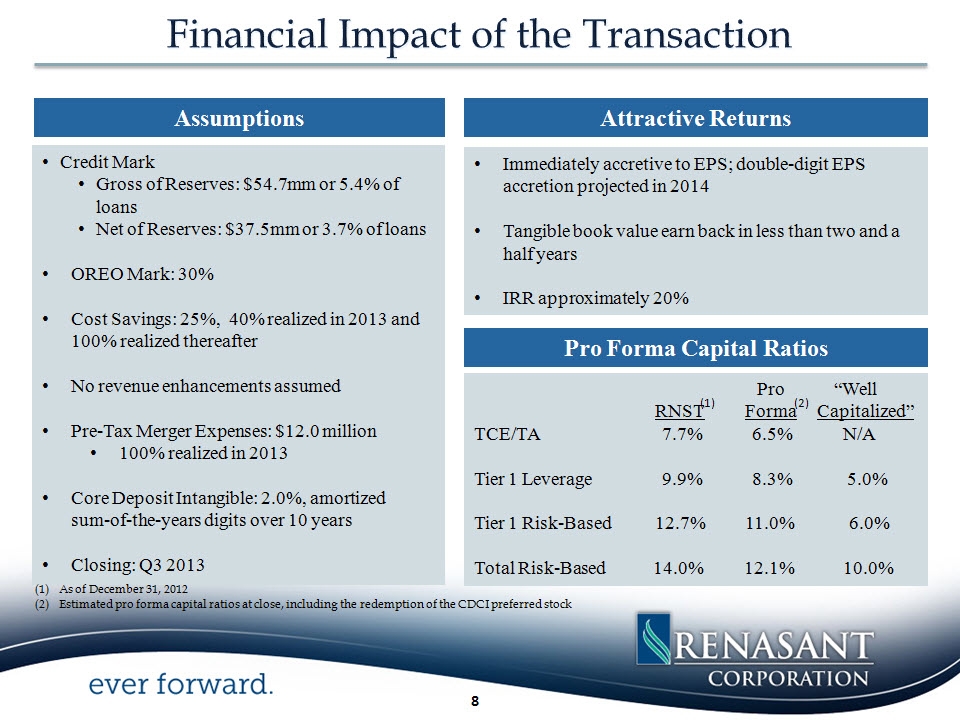

• Immediately accretive to EPS, double-digit EPS accretion projected in 2014

• Tangible book value earn back in approximately 2.5 years

• IRR approximately 20%

• Realization of significant expense synergies (25% of noninterest expense)

• Pro forma capital ratios above “well capitalized” guidelines

6

Extensive Credit Review

• Two tiered review conducted by Renasant’s senior

credit officers and loan review team

credit officers and loan review team

• Individually reviewed 84% of adversely classified

loans by volume, representing all relationships with

a balance greater than $100,000

loans by volume, representing all relationships with

a balance greater than $100,000

• Individually reviewed 100% of relationships with a

balance greater than $500,000

balance greater than $500,000

• Conducted review of underwriting policy and

procedure for smaller balance portfolios

procedure for smaller balance portfolios

• Reviewed 100% of OREO properties, including

physical inspection of over 80% of OREO by

volume

physical inspection of over 80% of OREO by

volume

Cumulative Losses and Credit Mark

Cumulative Losses Since 12/31/07(1): $118.2mm

Estimated Credit Mark (Loans & OREO) $62.5mm

Total Estimated Losses Through Cycle: $180.7mm

As % of 12/31/07 Gross Loan Balance(2): 14.8%

(1) Represents cumulative net charge-offs and OREO expenses through 12/31/12

(2) 12/31/07 gross loans held for investment of $1.2 billion

7

|

Implied Price Per Share:

|

$12.35(1)

|

|

Price / Tangible Book Value Per Share:

|

119%

|

|

Price / 2012 EPS:

|

23.1x

|

|

Price / 2013 EPS(2):

|

15.8x

|

|

Core Deposit Premium:

|

1.5%

|

(1) Based on RNST’s 10 day average closing price as of February 4, 2013 of $19.22 and an exchange ratio of 0.6425x

(2) Based on analyst estimate

9

9

Source: SNL Financial, Company documents

10

Source: SNL Financial, dates are those on which each transaction was announced

11

þ Strategically advantageous

• Acquisition of 120+ year old bank with quality core customer base

• In-market transaction consistent with our acquisition philosophy

• Creates the 4th largest bank by pro forma deposit market share in Mississippi

• Enhances fee revenue businesses of insurance, mortgage, and wealth management

• Complementary cultures and strong ties to community

• Strong, stable deposits and earnings generation complement de novo and out-of-state market

expansion activities

expansion activities

þ Financially attractive

• Immediately accretive to EPS, double-digit EPS accretion projected in 2014

• Tangible book value earn back in approximately 2.5 years

• IRR approximately 20%

• Realization of significant expense synergies (25% of noninterest expense)

• Pro forma capital ratios above “well capitalized” guidelines

þ Low risk opportunity

• Extensive due diligence process completed

• Comprehensive review of loan and OREO portfolios

• Conservative credit mark

Appendix

13

Source: SNL Financial

14

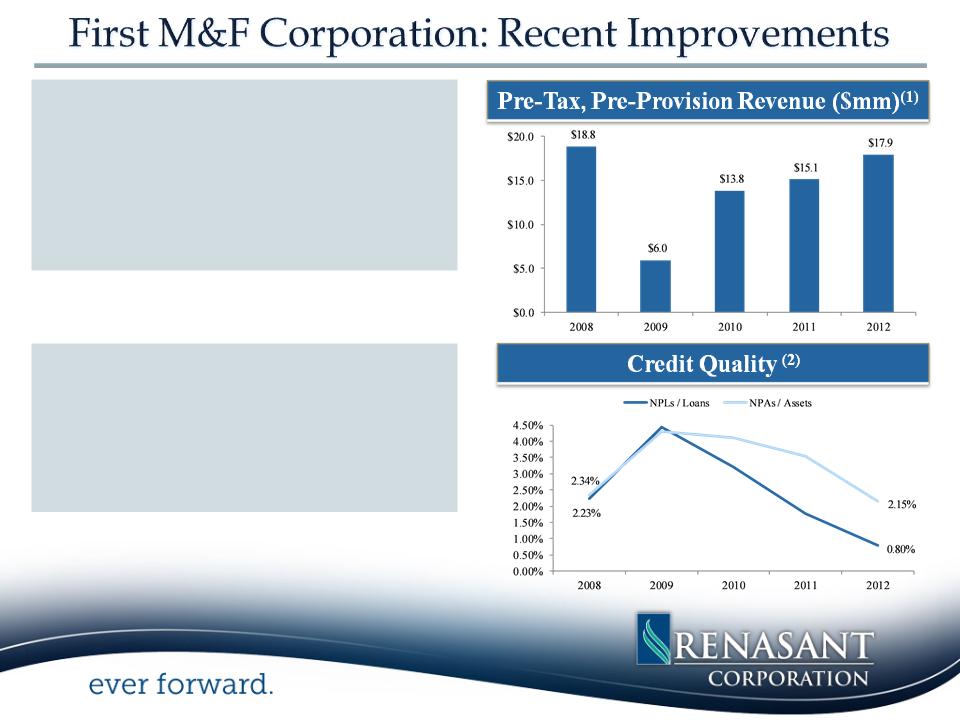

(1) In 2009, excludes $34.3 million goodwill impairment charge

(2) Nonperforming loans (NPLs) include loans 90 days past due and nonaccrual loans. Nonperforming

assets (NPAs) include NPLs and other real estate owned

assets (NPAs) include NPLs and other real estate owned

Source: SNL Financial, data as of 12/31/2012

• Increased Profitability

– Net income available to common

shareholders increased by 90% in 2012

shareholders increased by 90% in 2012

• Fee Income

– Mortgage banking revenue of $5.3 million

– Insurance revenues of $3.5 million

• Considerable Improvement in Asset Quality

– Nonperforming Loans/Loans at lowest

level since 2006 (0.80% of gross loans)

level since 2006 (0.80% of gross loans)

– 38% decrease in total nonperforming

assets in 2012 (to 2.15% of total assets)

assets in 2012 (to 2.15% of total assets)

15

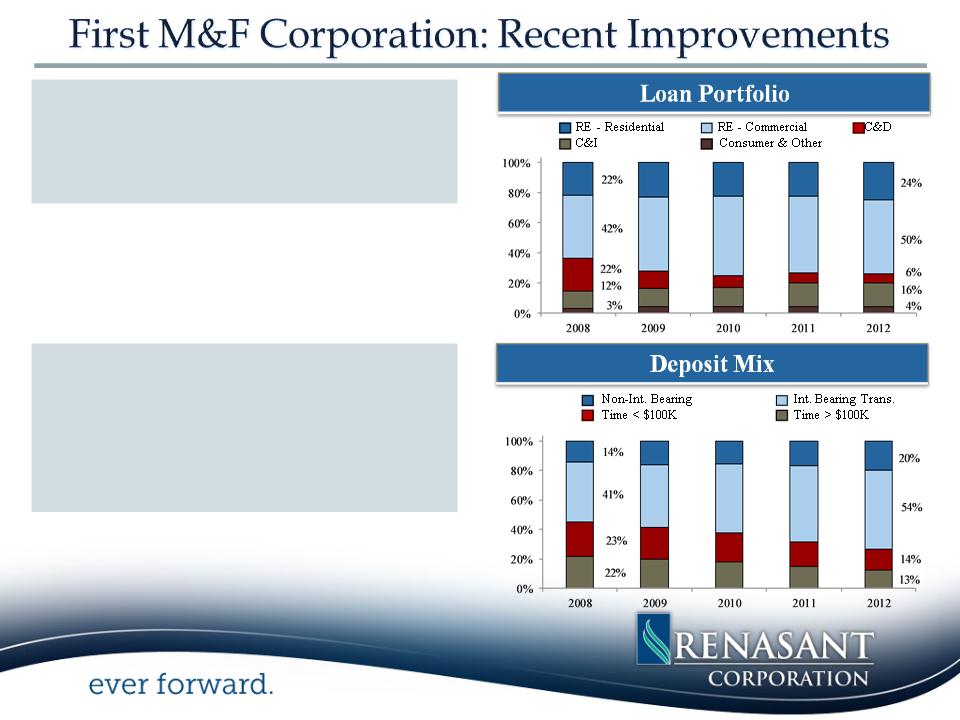

• Significant Remixing of Loan Portfolio

– C&D loans now represent 6% of the

portfolio, replaced by a greater

concentration of owner occupied CRE and

C&I loans

portfolio, replaced by a greater

concentration of owner occupied CRE and

C&I loans

• Shift in Deposit Mix

– Noninterest bearing deposits represent

20% of total deposits

20% of total deposits

– Decrease in time deposits to 27% of total

deposits

deposits

16

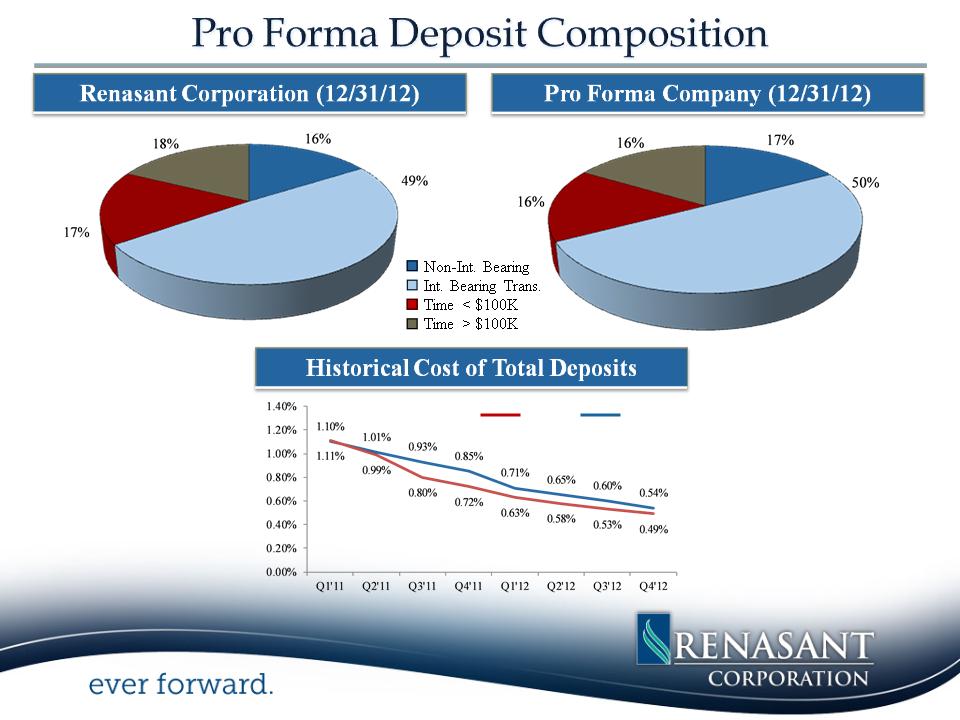

Source: SNL Financial, company earnings releases, data as of 12/31/2012

RNST FMFC

17

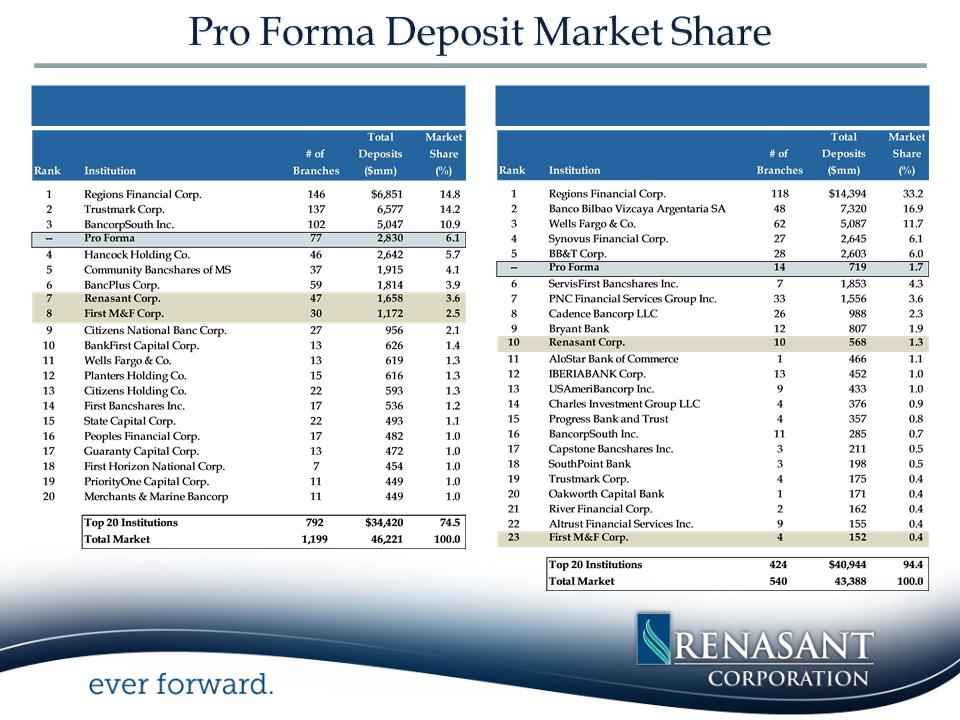

Source: SNL Financial

Deposit data as of 6/30/2012

(1)Represents deposit market share for the state of Mississippi

(2)Represents deposit market share for counties with RNST presence

17

Mississippi1

Alabama2

18

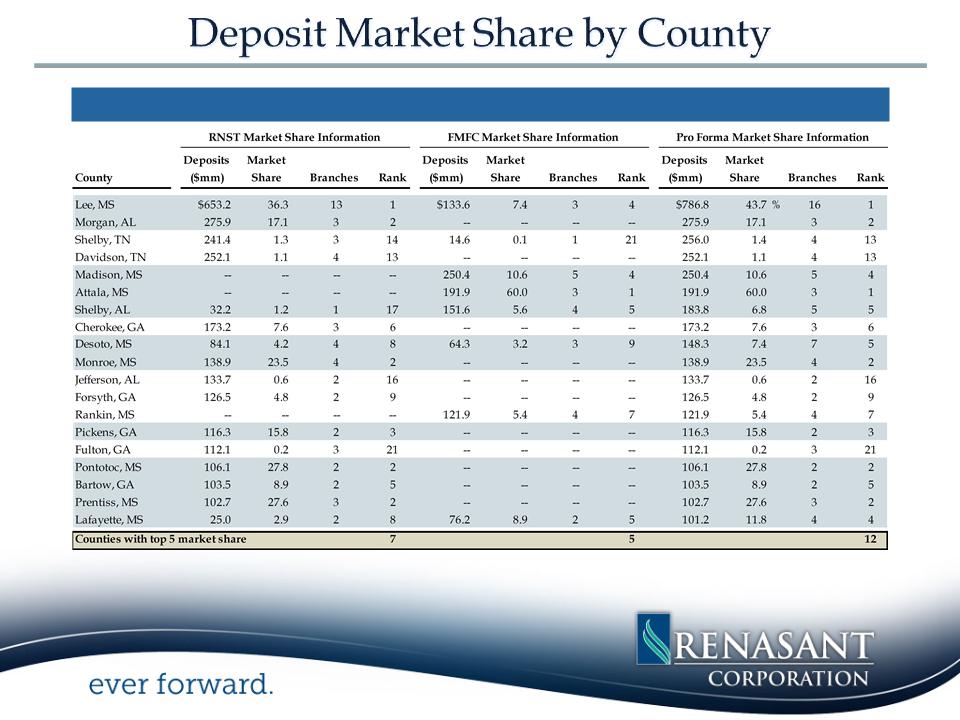

Counties with Top 5 Deposit Market Share

Source: SNL Financial, deposit data as of 6/30/2012

Includes counties with pro forma deposits greater than $100 million

Blue highlight denotes top 5 deposit market share

19

Renasant and M&F will be filing a joint proxy statement/prospectus, and other relevant documents concerning the merger

with the Securities and Exchange Commission (the “SEC”). This presentation does not constitute an offer to sell or the

solicitation of an offer to buy any securities or a solicitation of any vote or approval. INVESTORS ARE URGED TO READ

THE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER DOCUMENTS TO BE FILED WITH THE SEC IN

CONNECTION WITH THE MERGER OR INCORPORATED BY REFERENCE IN THE JOINT PROXY

STATEMENT/PROSPECTUS BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT RENASANT,

M&F AND THE PROPOSED MERGER. When available, the joint proxy statement/prospectus will be mailed to shareholders

of both Renasant and M&F. Investors will also be able to obtain copies of the joint proxy statement/prospectus and other

relevant documents (when they become available) free of charge at the SEC’s Web site (www.sec.gov). In addition, documents

filed with the SEC by Renasant will be available free of charge from Mitchell Waycaster, Director of Investor Relations,

Renasant Corporation, 209 Troy Street, Tupelo, Mississippi 38804-4827, telephone: (662) 680-1215. Documents filed with the

SEC by M&F will be available free of charge from M&F by contacting John G. Copeland, Chief Financial Officer, First M&F

Corporation, 134 West Washington Street, Kosciusko, Mississippi 39090, telephone: (662) 289-8594.

with the Securities and Exchange Commission (the “SEC”). This presentation does not constitute an offer to sell or the

solicitation of an offer to buy any securities or a solicitation of any vote or approval. INVESTORS ARE URGED TO READ

THE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER DOCUMENTS TO BE FILED WITH THE SEC IN

CONNECTION WITH THE MERGER OR INCORPORATED BY REFERENCE IN THE JOINT PROXY

STATEMENT/PROSPECTUS BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT RENASANT,

M&F AND THE PROPOSED MERGER. When available, the joint proxy statement/prospectus will be mailed to shareholders

of both Renasant and M&F. Investors will also be able to obtain copies of the joint proxy statement/prospectus and other

relevant documents (when they become available) free of charge at the SEC’s Web site (www.sec.gov). In addition, documents

filed with the SEC by Renasant will be available free of charge from Mitchell Waycaster, Director of Investor Relations,

Renasant Corporation, 209 Troy Street, Tupelo, Mississippi 38804-4827, telephone: (662) 680-1215. Documents filed with the

SEC by M&F will be available free of charge from M&F by contacting John G. Copeland, Chief Financial Officer, First M&F

Corporation, 134 West Washington Street, Kosciusko, Mississippi 39090, telephone: (662) 289-8594.

Renasant, M&F and certain of their directors, executive officers and other members of management and

employees may be deemed to be participants in the solicitation of proxies from the shareholders of Renasant and M&F in

connection with the proposed merger. Information about the directors and executive officers of Renasant is included in the

proxy statement for its 2012 annual meeting of shareholders, which was filed with the SEC on March 8, 2012. Information

about the directors and executive officers of M&F is included in the proxy statement for its 2012 annual meeting of

shareholders, which was filed with the SEC on March 14, 2012. Additional information regarding the interests of such

participants and other persons who may be deemed participants in the transaction will be included in the joint proxy

statement/prospectus and the other relevant documents filed with the SEC when they become available.

employees may be deemed to be participants in the solicitation of proxies from the shareholders of Renasant and M&F in

connection with the proposed merger. Information about the directors and executive officers of Renasant is included in the

proxy statement for its 2012 annual meeting of shareholders, which was filed with the SEC on March 8, 2012. Information

about the directors and executive officers of M&F is included in the proxy statement for its 2012 annual meeting of

shareholders, which was filed with the SEC on March 14, 2012. Additional information regarding the interests of such

participants and other persons who may be deemed participants in the transaction will be included in the joint proxy

statement/prospectus and the other relevant documents filed with the SEC when they become available.

20

E. Robinson McGraw

Chairman

President and Chief Executive Officer

Kevin D. Chapman

Senior Executive Vice President and

Chief Financial Officer

209 TROY STREET

TUPELO, MS 38804-

4827

4827

PHONE: 1-800-680-

1601

1601

FACSIMILE: 1-662-

680-1234

680-1234

WWW.RENASANT.C

OM

OM

WWW.RENASANTBA

NK.COM

NK.COM