Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - MALVERN BANCORP, INC. | t75514_8k.htm |

| EX-99.1 - EXHIBIT 99.1 - MALVERN BANCORP, INC. | ex99-1.htm |

EXHIBIT 99.2

|

M A L V E R N

Annual Meeting

February 7, 2013

|

|

M A L V E R N

Forward-Looking Statements

Certain comments in this presentation contain certain forward looking statements (as defined in the Securities Exchange Act of 1934 and the regulations hereunder). Forward looking statements are not historical facts but instead represent only the beliefs, expectations or opinions of Malvern Bancorp, Inc. and its management regarding future events, many of which, by their nature, are inherently uncertain. Forward looking statements may be identified by the use of such words as: “believe”, “expect”, “anticipate”, “intend”, “plan”, “estimate”, or words of similar meaning, or future or conditional terms such as “will”, “would”, “should”, “could”, “may”, “likely”, “probably”, or “possibly.” Forward looking statements include, but are not limited to, financial projections and estimates and their underlying assumptions; statements regarding plans, objectives and expectations with respect to future operations, products and services; and statements regarding future performance. Such statements are subject to certain risks, uncertainties and assumption, many of which are difficult to predict and generally are beyond the control of Malvern Bancorp, Inc. and its management, that could cause actual results to differ materially from those expressed in, or implied or projected by, forward looking statements. The following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed in the forward looking statements: (1) economic and competitive conditions which could affect the volume of loan originations, deposit flows and real estate values; (2) the levels of non-interest income and expense and the amount of loan losses; (3) competitive pressure among depository institutions increasing significantly; (4) changes in the interest rate environment causing reduced interest margins; (5) general economic conditions, either nationally or in the markets in which Malvern Bancorp, Inc. is or will be doing business, being less favorable than expected;(6) political and social unrest, including acts of war or terrorism; or (7) legislation or changes in regulatory requirements adversely affecting the business in which Malvern Bancorp, Inc. is engaged.

Malvern Bancorp, Inc. undertakes no obligation to update these forward looking statements to reflect events or circumstances that occur after the date on which such statements were made.

As used in this report, unless the context otherwise requires, the terms “we,” “our,” “us,” or the “Company” refer to Malvern Bancorp, Inc. and the term the “Bank” refers to Malvern Federal Savings Bank, a federally chartered savings bank and wholly owned subsidiary of the Company. In addition, unless the context otherwise requires, references to the operations of the Company include the operations of the Bank.

For a more detailed description of the factors that may affect Malvern Bancorp’s operating results or the outcomes described in these forward-looking statements, we refer you to our filings with the Securities and Exchange Commission, including our annual report on Form 10-K for the year ended September 30, 2012. Malvern Bancorp assumes no obligation to update the forward-looking statements made during this presentation. For more information, please visit our Web site www.malvernfederal.com.

2

|

|

M A L V E R N

Company Overview

|

|

M A L V E R N

Overview of Malvern Bancorp, Inc.

Malvern Federal Savings Bank, a federally chartered savings bank organized in 1887, is the wholly owned subsidiary of Malvern Bancorp, Inc.

On October 11, 2012, Malvern Bancorp, Inc. completed its second step conversion and became a fully public company, raising $36.4 million in gross proceeds.

Malvern Bancorp trades on the NASDAQ Global Market under the symbol MLVF.

Malvern Bancorp conducts its business from its headquarters and eight financial centers located in Chester and Delaware Counties, Pennsylvania.

As of September 30, 2012, we had $711.8 million in total assets, $457.0 million in net loans, $541.0 million in deposits and $62.6 million in shareholders’ equity.

4

|

|

M A L V E R N

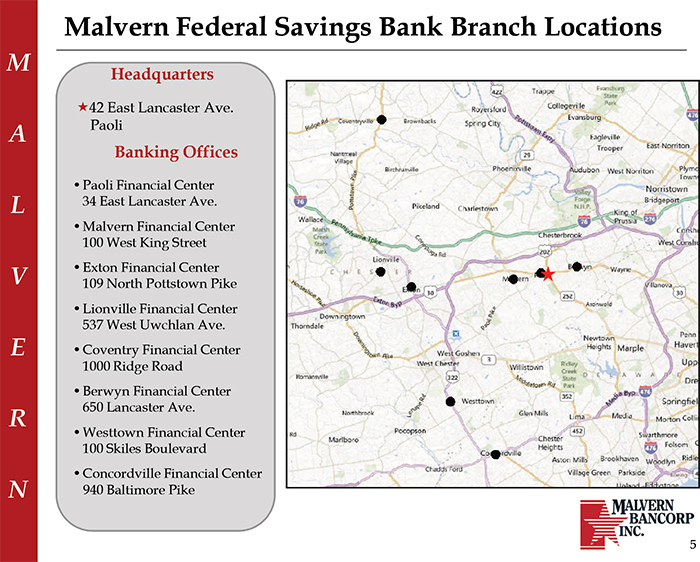

Malvern Federal Savings Bank Branch Locations

Headquarters

42 East Lancaster Ave.

Paoli

Banking Offices

• Paoli Financial Center 34 East Lancaster Ave.

• Malvern Financial Center 100 West King Street

• Exton Financial Center 109 North Pottstown Pike

• Lionville Financial Center 537 West Uwchlan Ave.

• Coventry Financial Center 1000 Ridge Road

• Berwyn Financial Center 650 Lancaster Ave.

• Westtown Financial Center 100 Skiles Boulevard

• Concordville Financial Center 940 Baltimore Pike

5

|

|

M A L V E R N

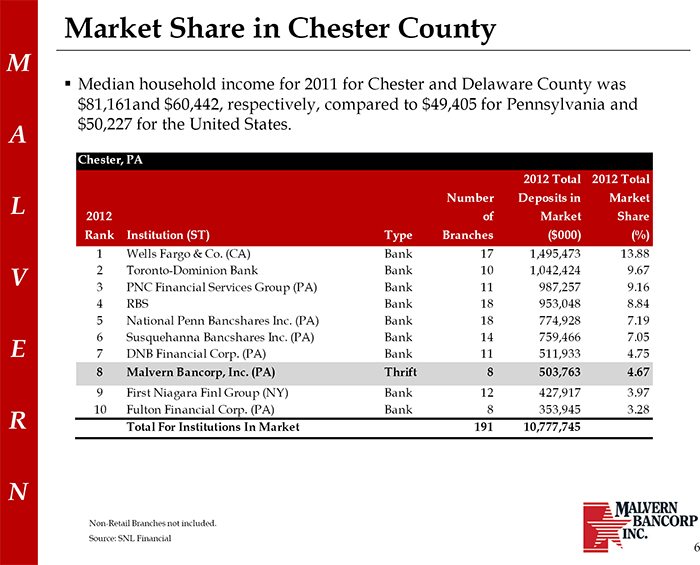

Market Share in Chester County

Median household income for 2011 for Chester and Delaware County was $81,161and $60,442, respectively, compared to $49,405 for Pennsylvania and $50,227 for the United States.

Chester, PA

2012 Total 2012 Total Number Deposits in Market 2012 of Market Share Rank Institution (ST) Type Branches ($000) (%)

1 Wells Fargo & Co. (CA) Bank 17 1,495,473 13.88

2 Toronto-Dominion Bank Bank 10 1,042,424 9.67

3 PNC Financial Services Group (PA) Bank 11 987,257 9.16

4 RBS Bank 18 953,048 8.84

5 National Penn Bancshares Inc. (PA) Bank 18 774,928 7.19

6 Susquehanna Bancshares Inc. (PA) Bank 14 759,466 7.05

7 DNB Financial Corp. (PA) Bank 11 511,933 4.75

8 Malvern Bancorp, Inc. (PA) Thrift 8 503,763 4.67

9 First Niagara Finl Group (NY) Bank 12 427,917 3.97

10 Fulton Financial Corp. (PA) Bank 8 353,945 3.28

Total For Institutions In Market 191 10,777,745

Non-Retail Branches not included.

Source: SNL Financial

6

|

|

M A L V E R N

Fiscal 2012 Review

Reduction in total nonperforming assets (“NPAs”) from $21.2 million at fiscal year-end 2011 to $14.3 million at fiscal year-end 2012. This represents a $6.9 million, or 32.5%, annual reduction in NPAs.

Improved operating results from a net loss of $6.1 million in fiscal 2011 to $2.0 million in net income in fiscal 2012. The primary reason for the $8.1 million improvement in our results of operations in fiscal 2012 compared to the prior fiscal year was a reduction in the provision of loan losses of $11.6 million, which was partially offset by a $4.2 million increase in income tax expense and a $2.2 million decrease in net interest income.

7

|

|

M A L V E R N

Fiscal 2013 Business Strategy

Our business strategy is focused on continuing to reduce the level of our non-performing assets, monitoring and overseeing our performing classified assets and troubled debt restructurings in an effort to limit the number of additional non-performing assets in future periods, complying with the provisions of the Supervisory Agreements until we are able to obtain relief from such agreements and conducting our traditional community-oriented banking business within these constraints.

Below are the highlights of our business strategy:

Improving Asset Quality Managing Our Loan Portfolio Increasing Capital

Obtaining Relief from the Supervisory Agreements So That We Can Grow Our Loan Portfolio and Resume Commercial Real Estate and Construction and Development Lending

Increasing Market Share Penetration

Increasing Our Core Deposits

Continuing to Provide Exceptional Customer Service

8

|

|

M A L V E R N

Financial Highlights

|

|

M A L V E R N

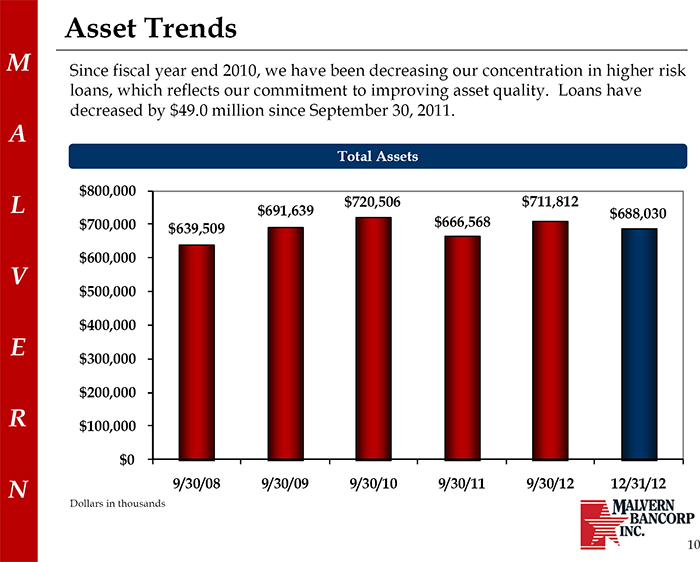

Asset Trends

Since fiscal year end 2010, we have been decreasing our concentration in higher risk loans, which reflects our commitment to improving asset quality. Loans have decreased by $49.0 million since September 30, 2011.

Total Assets

$800,000 $720,506 $711,812 $691,639 $688,030 $700,000 $666,568 $639,509

$600,000 $500,000 $400,000 $300,000 $200,000 $100,000

$0

9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12

Dollars in thousands

10

|

|

M A L V E R N

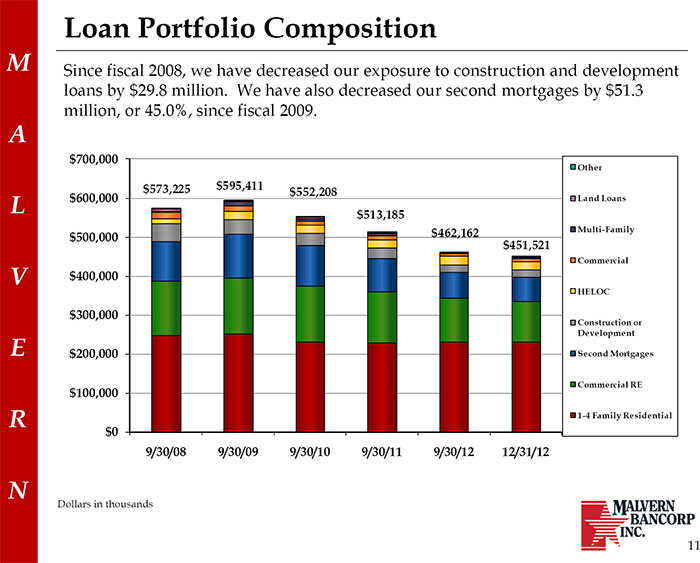

Loan Portfolio Composition

Since fiscal 2008, we have decreased our exposure to construction and development loans by $29.8 million. We have also decreased our second mortgages by $51.3 million, or 45.0%, since fiscal 2009.

$700,000

Other

$573,225 $595,411 $552,208

$600,000 Land Loans

$513,185

$462,162 Multi-Family

$500,000 $451,521

Commercial

$400,000

HELOC

$300,000

Construction or Development

$200,000 Second Mortgages

Commercial RE

$100,000

1-4 Family Residential

$0

9/30/08 9/30/09 9/30/10 9/30/11 9/30/12 12/31/12

Dollars in thousands

11

|

|

M A L V E R N

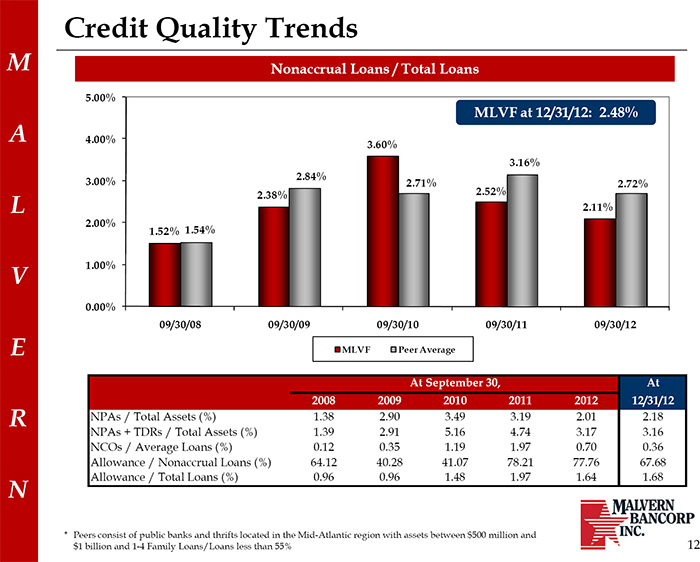

Credit Quality Trends

Nonaccrual Loans / Total Loans

5.00%

MLVF at 12/31/12: 2.48%

4.00%

3.60%

3.16% 2.84%

3.00% 2.71% 2.72% 2.38% 2.52% 2.11% 2.00% 1.52% 1.54%

1.00%

0.00%

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12

MLVF Peer Average

At September 30, At 2008 2009 2010 2011 2012 12/31/12

NPAs / Total Assets (%) 1.38 2.90 3.49 3.19 2.01 2.18 NPAs + TDRs / Total Assets (%) 1.39 2.91 5.16 4.74 3.17 3.16 NCOs / Average Loans (%) 0.12 0.35 1.19 1.97 0.70 0.36 Allowance / Nonaccrual Loans (%) 64.12 40.28 41.07 78.21 77.76 67.68 Allowance / Total Loans (%) 0.96 0.96 1.48 1.97 1.64 1.68

* Peers consist of public banks and thrifts located in the Mid-Atlantic region with assets between $500 million and 14 $1 billion and 1-4 Family Loans/Loans less than 55%

12

|

|

M A L V E R N

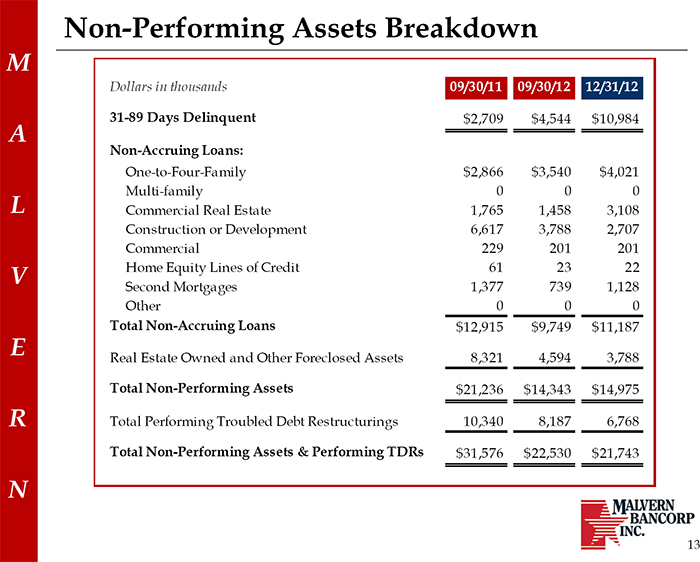

Non-Performing Assets Breakdown

Dollars in thousands 09/30/11 09/30/12 12/31/12

31-89 Days Delinquent $2,709 $4,544 $10,984

Non-Accruing Loans:

One-to-Four-Family $2,866 $3,540 $4,021 Multi-family 0 0 0 Commercial Real Estate 1,765 1,458 3,108 Construction or Development 6,617 3,788 2,707 Commercial 229 201 201 Home Equity Lines of Credit 61 23 22 Second Mortgages 1,377 739 1,128 Other 0 0 0

Total Non-Accruing Loans $12,915 $9,749 $11,187

Real Estate Owned and Other Foreclosed Assets 8,321 4,594 3,788

Total Non-Performing Assets $21,236 $14,343 $14,975

Total Performing Troubled Debt Restructurings 10,340 8,187 6,768

Total Non-Performing Assets & Performing TDRs $31,576 $22,530 $21,743

13

|

|

M A L V E R N

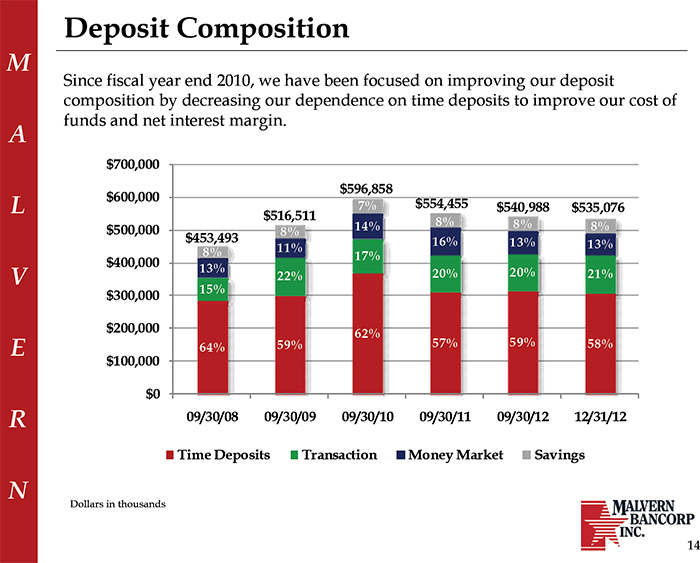

Deposit Composition

Since fiscal year end 2010, we have been focused on improving our deposit composition by decreasing our dependence on time deposits to improve our cost of funds and net interest margin.

$700,000

$596,858 $600,000

7% $554,455 $540,988 $535,076 $516,511

14% 8% 8% 8% $500,000 8% $453,493 16% 13% 11% 13%

8% 17% $400,000

13% 20%

22% 20% 21% 15% $300,000

$200,000

62%

59% 57% 59% 58% 64% $100,000

$0

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12 12/31/12

Time Deposits Transaction Money Market Savings

Dollars in thousands

14

|

|

M A L V E R N

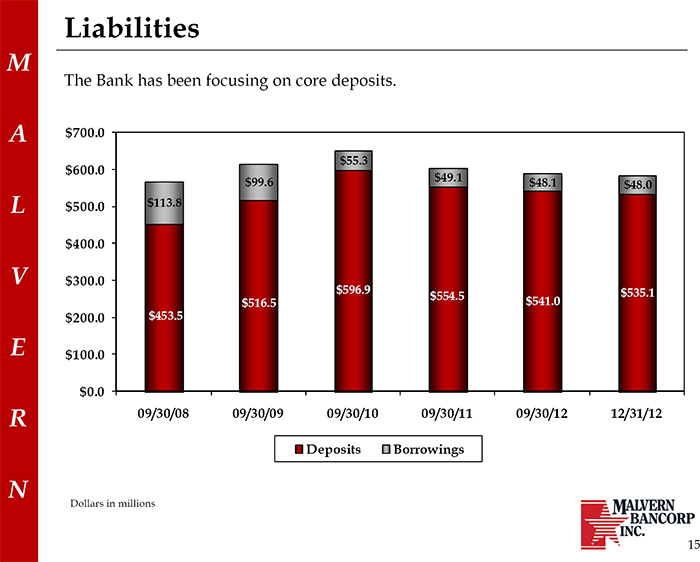

Liabilities

The Bank has been focusing on core deposits.

$700.0

$55.3 $600.0 $49.1 $99.6 $48.1 $48.0 $500.0 $113.8

$400.0

$300.0 $596.9 $535.1 $554.5 $516.5 $541.0 $200.0 $453.5

$100.0

$0.0

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12 12/31/12

Deposits Borrowings

Dollars in millions

15

|

|

M A L V E R N

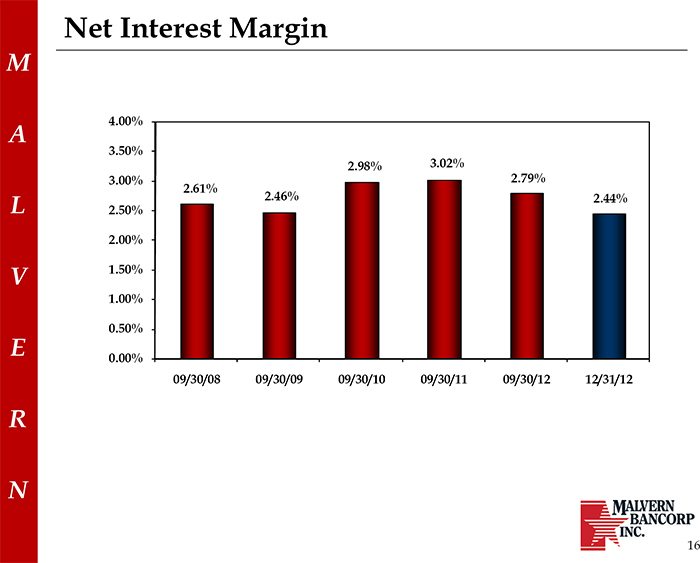

Net Interest Margin

4.00%

3.50%

2.98% 3.02%

3.00% 2.79% 2.61%

2.46% 2.44% 2.50%

2.00% 1.50% 1.00% 0.50%

0.00%

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12 12/31/12

16

|

|

M A L V E R N

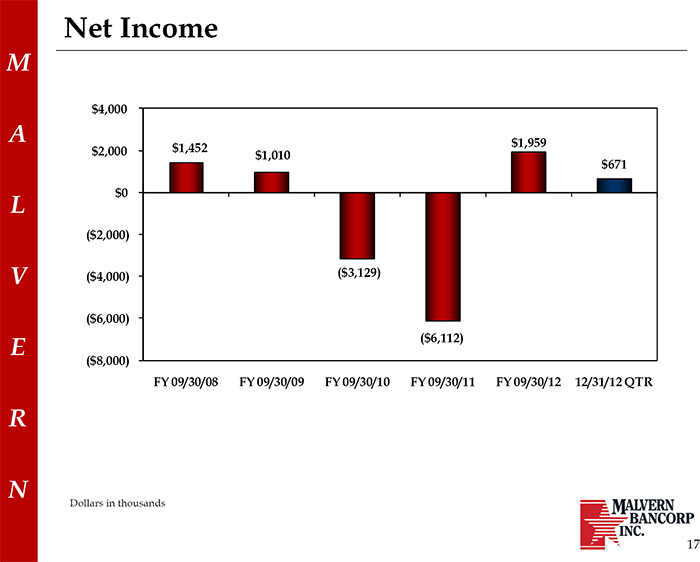

Net Income

$4,000

$1,959 $2,000 $1,452 $1,010 $671

$0

($2,000)

($4,000) ($3,129)

($6,000)

($6,112)

($8,000)

FY 09/30/08 FY 09/30/09 FY 09/30/10 FY 09/30/11 FY 09/30/12 12/31/12 QTR

Dollars in thousands

17

|

|

M A L V E R N

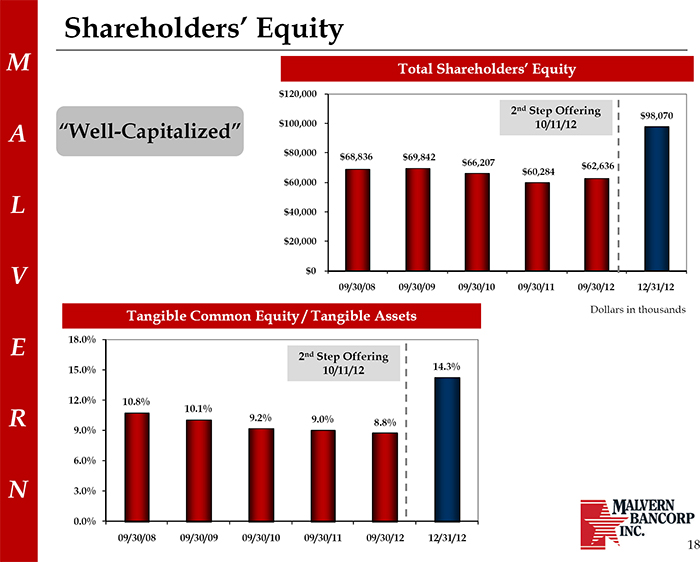

Shareholders’ Equity

Total Shareholders’ Equity

$120,000

2nd Step Offering $98,070

“Well-Capitalized” $100,000 10/11/12

$80,000 $68,836 $69,842 $66,207 $62,636 $60,284 $60,000

$40,000

$20,000

$0

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12 12/31/12

Dollars in thousands

Tangible Common Equity / Tangible Assets

18.0%

2nd Step Offering

15.0% 10/11/12 14.3%

12.0% 10.8%

10.1%

9.2% 9.0%

8.8% 9.0%

6.0%

3.0%

0.0%

15

09/30/08 09/30/09 09/30/10 09/30/11 09/30/12 12/31/12

18

|

|

M A L V E R N

Market Statistics

|

|

M A L V E R N

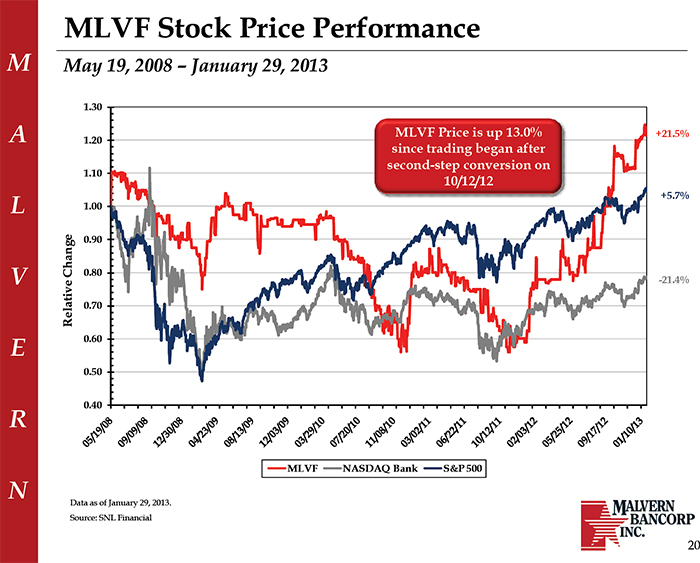

MLVF Stock Price Performance

May 19, 2008 – January 29, 2013

1.30

MLVF Price is up 13.0% +21.5%

1.20

since trading began after second-step conversion on

1.10

10/12/12

+5.7% 1.00

0.90

Change 0.80

-21.4%

Relative 0.70 0.60

0.50

0.40

MLVF NASDAQ Bank S&P 500

Data as of January 29, 2013.

Source: SNL Financial

20

|

|

M A L V E R N

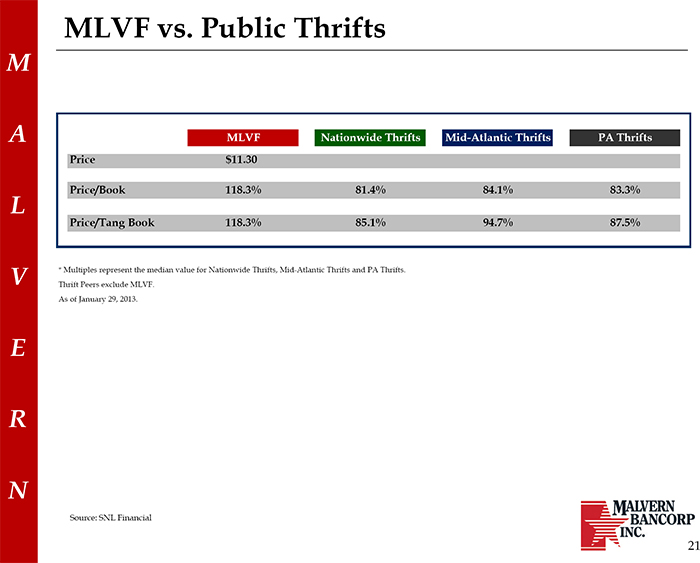

MLVF vs. Public Thrifts

MLVF Nationwide Thrifts Mid-Atlantic Thrifts PA Thrifts

Price $11.30

Price/Book 118.3% 81.4% 84.1% 83.3%

Price/Tang Book 118.3% 85.1% 94.7% 87.5%

* Multiples represent the median value for Nationwide Thrifts, Mid-Atlantic Thrifts and PA Thrifts.

Thrift Peers exclude MLVF.

As of January 29, 2013.

Source: SNL Financial

21

|

|

M A L V E R N

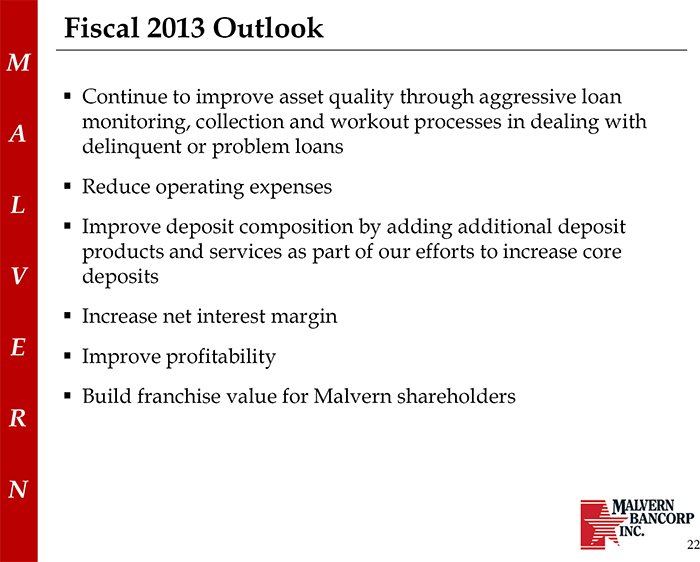

Fiscal 2013 Outlook

Continue to improve asset quality through aggressive loan monitoring, collection and workout processes in dealing with delinquent or problem loans

Reduce operating expenses

Improve deposit composition by adding additional deposit products and services as part of our efforts to increase core deposits

Increase net interest margin

Improve profitability

Build franchise value for Malvern shareholders

22

|

|

M A L V E R N

Questions?

|