Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Chaparral Energy, Inc. | d432008d8k.htm |

$150mm Senior Notes

Add-On November 2012

$150mm Senior Notes Add-On

November 2012

Exhibit 99.1 |

2

22

2

This presentation contains "forward-looking statements" within the meaning of Section 27A of

the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934,

as amended. These forward-looking statements are subject to certain risks, trends and

uncertainties that could cause actual results to differ materially from those projected.

Among those risks, trends and uncertainties are our ability to find oil and natural gas reserves

that are economically recoverable, the volatility of oil and natural gas prices and significantly

depressed natural gas prices since the middle of 2008, the uncertain economic conditions in the

United States and globally, the decline in the values of our properties that have resulted in and

may in the future result in additional ceiling test write- downs, our ability to replace

reserves and sustain production, our estimate of the sufficiency of our existing capital sources,

our ability to raise additional capital to fund cash requirements for future operations, the

uncertainties involved in prospect development and property acquisitions or dispositions and in

projecting future rates of production or future reserves, the timing of development the oil spill

in the Gulf of Mexico on our present and future operations, the impact of government

regulation,

and

the

operating

hazards

attendant

to

the

oil

and

natural

gas

business.

In

particular,

careful consideration should be given to cautionary statements made in the various reports we

have filed with the Securities and Exchange Commission. We undertake no duty to update or

revise these

forward-looking statements.

expenditures

and

drilling

of

wells,

hurricanes

and

other

natural

disasters,

including

the

impact

of |

3

3

Presenters

Presenters

Mark Fischer, Chief Executive Officer

& President

Joe Evans, Chief Financial Officer

& Executive Vice President |

Chaparral Overview

Chaparral Overview

Founded in 1988, Based in Oklahoma City

Core areas —

Mid-Continent (Oklahoma) and Permian Basin (W. Texas)

Oil-weighted producer (64% oil; 36% gas); R/P ratio 18.6 years

Second largest oil producer in Oklahoma

Stable

1P

base

with

large

potential

upside

–

742

MMBoe

Near-term growth potential through drilling in

conventional & emerging plays ~

450,000 acres Long-term

growth

through

CO

2

EOR

–

74

fields

1

As of 12/31/11 using SEC methodology

Company Statistics

Production (Boe/d)

Proved Reserves (MMBoe)

1

Proved Reserves PV-10 ($mm)

1

TTM EBITDA ($mm)

4

4

~23,300

156.3

$2,309

$305

Q2, 2012 |

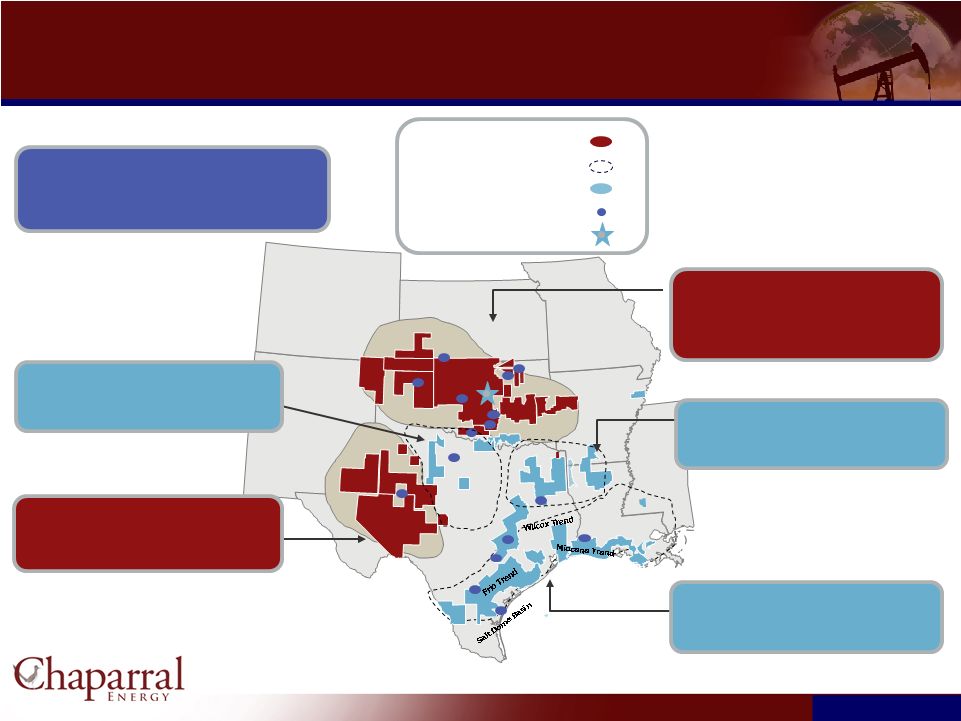

Operating Areas

Operating Areas

As of December 31, 2011 (SEC)

Val Verde

Basin

5

5

Sabine

Uplift

Midland

Basin

Delaware

Basin

Ouachita

Uplift

Arkoma

Basin

Fort

Worth

Basin

Anadarko

Woodford

Basin

OKC

Company Total

December

2011

proved

reserves

–

156.3

MMBoe

2011

average

daily

production

–

23.7

MBoe/d

Acreage (gross / net): 1,178,489 / 590,324

North Texas

Reserves: 3.9 MMBoe, 3% of total

Production: 0.5 Mboe/d, 2% of total

Permian Basin

Reserves: 19.3 MMBoe, 12% of total

Production: 3.6 MBoe/d, 15% of total

Core Area

Growth Area

Acreage

Field Offices

Headquarters

Mid-Continent

(Anadarko Basin & Central Oklahoma)

Reserves: 122.2 MMBoe, 78% of total

Production: 17.0 MBoe/d, 72% of total

Ark-La-Tex

Reserves: 7.2 MMBoe, 5% of total

Production: 1.3 MBoe/d, 6% of total

Gulf Coast

Reserves: 3.2 MMBoe, 2% of total

Production: 0.9 MBoe/d, 4% of total |

Strong Record of Reserve

and Production Growth Strong Record of Reserve and Production Growth

2003 –

2011 CAGR = 15%

2003 –

2011 CAGR = 16%

6

6

1)

Reserves as of December 31

for each year calculated

using flat SEC

pricing per the following:

6

6

Year-End SEC Reserves (MMBoe)

(1)

Annual Production (MMBoe)

Chaparral’s reserve replacement ratio averaged 422% per year since 2003

Year

Oil

Gas

2007

$96.01

$6.80

2008

$44.60

$5.62

2009

$61.18

$3.87

2010

$79.43

$4.38

2011

$

96.19

$4.11 |

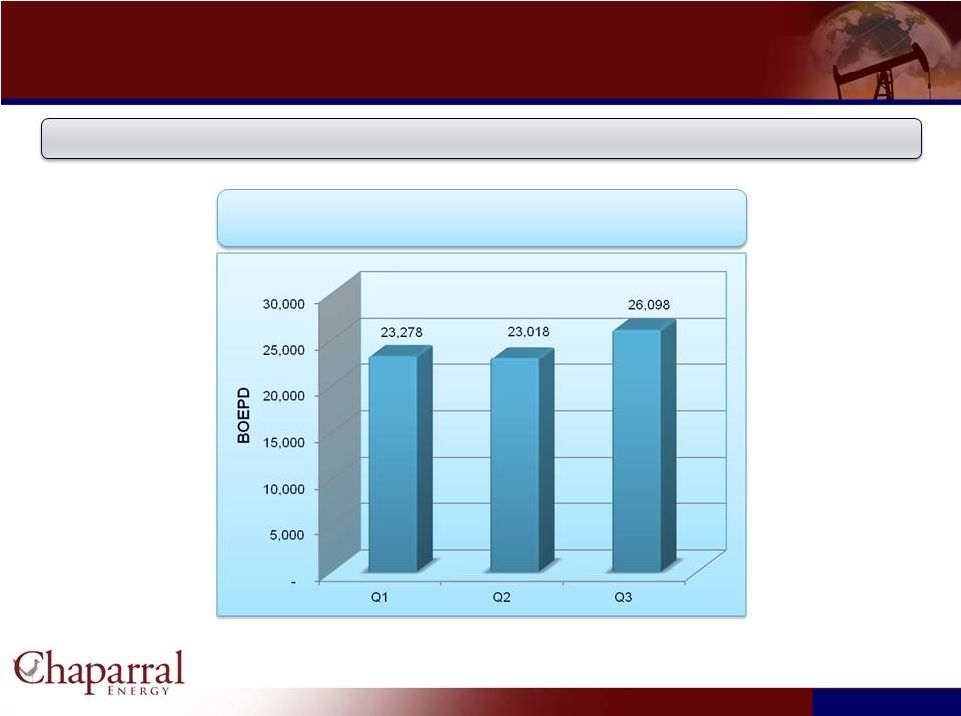

Current Production

- 2012

Current Production -

2012

7

7

7

7

2012 Production by Quarter

In the 3

rd

Quarter Chaparral increased production by 13.4% over the previous quarter

|

Financial Position to

Execute Strategy Financial Position to Execute Strategy

8

8

*Pro-Forma for $150mm Senior Notes Add-On and Increased Borrowing Base

Current Maturity Profile ($mm)

Liquidity ($mm)

Net Debt / EBITDA

Strong Financial Position

No senior note maturities before 2020

Hedge positions in place to secure cash flow

in near term

Budget CAPEX within free cash flow

(including divestiture proceeds) |

2012 Capital Budget ($ millions) 2012 Capital Budget ($ millions)

Key Drilling Areas

Northern OK Mississippi

Horizontal

$73

Anadarko Cleveland Sand

46

Anadarko Granite Wash

22

Marmaton

15

Bone Spring / Avalon

10

Hogshooter

7

Other

28

Total

$201

9

9

EOR Field

N. Burbank

$104

Panhandle Area

60

Other

3

Total

$168

*99% of Capital Program is Oil Focused

Component

2008

2009

2010

2011

2012

Budget

2012

Expanded

Budget

2012

%

Drilling

$168

$76

$196

$172

$131

$201

44%

EOR

24

14

36

86

127

168

37%

Enhancements

53

32

39

32

26

16

3%

Acquisitions

46

18

41

17

15

40

9%

Other (P&E,

Capitalized G&A, etc)

48

14

32

28

31

35

7%

Total

$339

$154

$344

$336

$330

$460

100% |

10

10

Conventional

drilling

(IRR:

50%

-

75%)

Anadarko Granite Wash

Anadarko Cleveland Sand

Unconventional

resource

play

drilling

(IRR:

35%

-

75%)

Northern Oklahoma Mississippi Play (“NOMP”): 260,000 net acres

Panhandle Marmaton: ~48,000 acres

Anadarko Woodford Shale: ~23,000 acres

Bone Spring/Avalon Shale: ~19,000 acres

Chaparral owns an inventory of 74 possible candidate

CO2-EOR

fields.

Proved reserves of 45.1 MMBoe from EOR designated fields as of

12/31/11

200+ MMBoe of total potential reserves

CO2

fields

exhibit

low-risk

and

stable

production.

IRR: 25% –

40%

Chaparral is Well Positioned for

Near–Term and Long–Term Growth

Near–Term Growth Drivers

Long–Term Growth Drivers

NOMP

CO

2

-EOR Fields |

Northern Oklahoma

Mississippi Play The Northern Oklahoma Mississippi Play (“NOMP”) is a

key near–term focus area for Chaparral.

Chaparral acreage over 260,000 net acres in the NOMP.

Over 132 MMBoe of potential.

1,600 unrisked drilling well inventory.

Chaparral Acreage

11

11

Overview

NOMP Asset Map

NOMP Well Economics

IP Rates:

100 - 700 Boe/d

EUR:

100 - 400 MBoe

Well Cost:

$2.5 - 4.0 million

% Oil:

60% - 90%

IRR:

35% - 75%

KS

OK |

12

12

NOMP: Recent Results

NOMP: Recent Results

Current

Net

Production

–

4,000

Boepd

2012

Capital

-

$73

mm

NOMP Core (93,000 Net Acres)

Significant industry activity in the play

Drilled or participated in 34 wells to date (18 operated); 2 WOCU

3-5 additional wells in 2012

Average IP ~600 Boepd; Average EUR ~350 MBoe

Current

Net

Production

–

3,375

Boepd

45% Oil

Emerging NOMP (167,000 Net Acres)

In

de-risking

phase

–

industry

activity

increasing

Drilled 6 wells to date

Average IP ~200+ Boepd; Average EUR ~120 MBo

Current

Net

Production

–

625

Boepd

92% Oil |

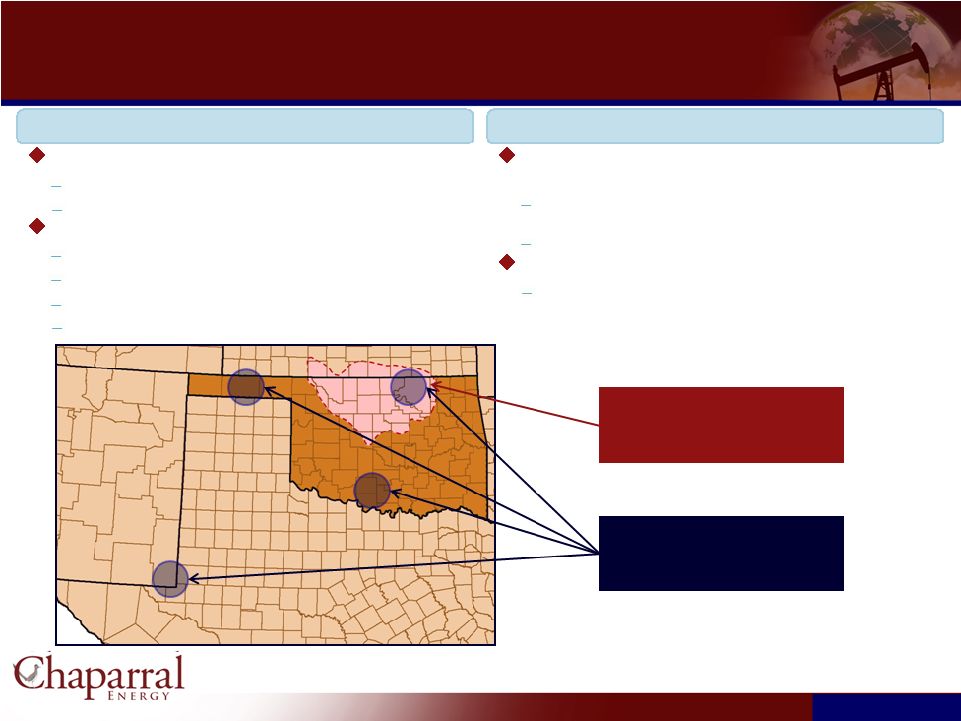

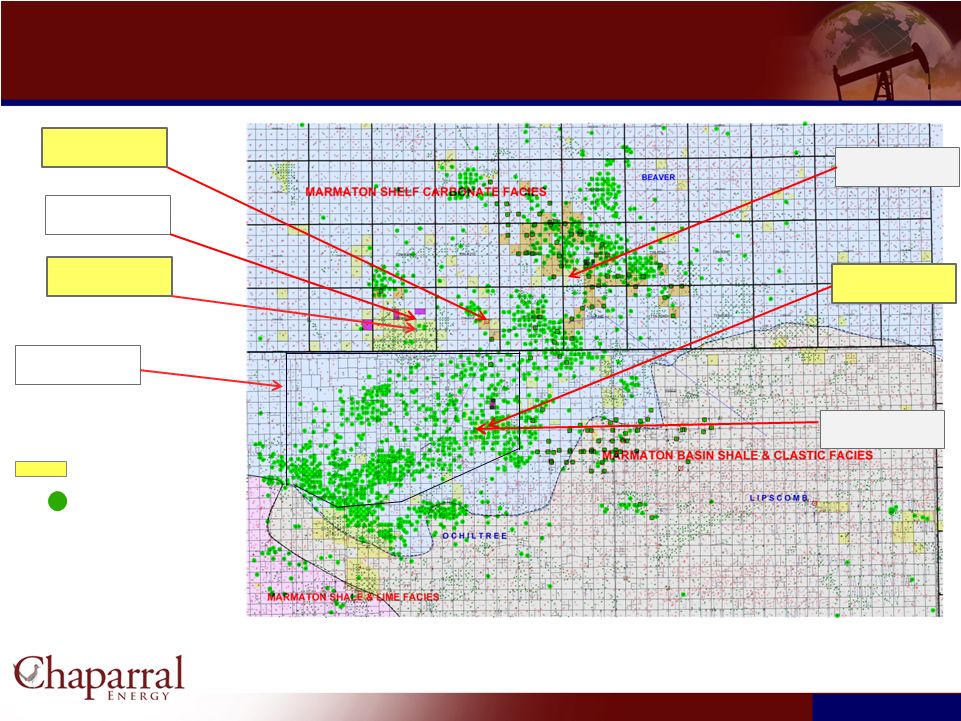

Marmaton Shelf

Play Marmaton Shelf Play

Marmaton Production

Chaparral Acreage

Net Acreage

48,000

EUR/well (Mboe)

150

Cost per Well (MM$)

$3.6

13

13

Johnston 1H-24

IP +300 Boepd

Leatherman 1H-14

2012 Location

Lamaster 1H-23

Flowing back

Buy Area

Ochiltree Co, Tx

Cornell 1H-30

2012 Location

Jay 1H-1098

Flowing back

Wright 1H-1099

2012 Location |

Chaparral:

Chaparral:

A Growing Mid-Continent

CO

2

EOR Company

A Growing Mid-Continent

CO

2

EOR Company

14

14 |

15

15

# of Active

Producer

CO2-EOR Projects

31

22

8

7

7

7

6

5

4

4

4

Total

105

Source: April 2012 Oil & Gas Journal

Note: Chaparral projects include the North Burbank Unit

Chaparral is the third most active CO2-EOR producer in the U.S.

Chaparral is a Leader in the CO2-EOR Industry

Chaparral is a Leader in the CO2-EOR Industry |

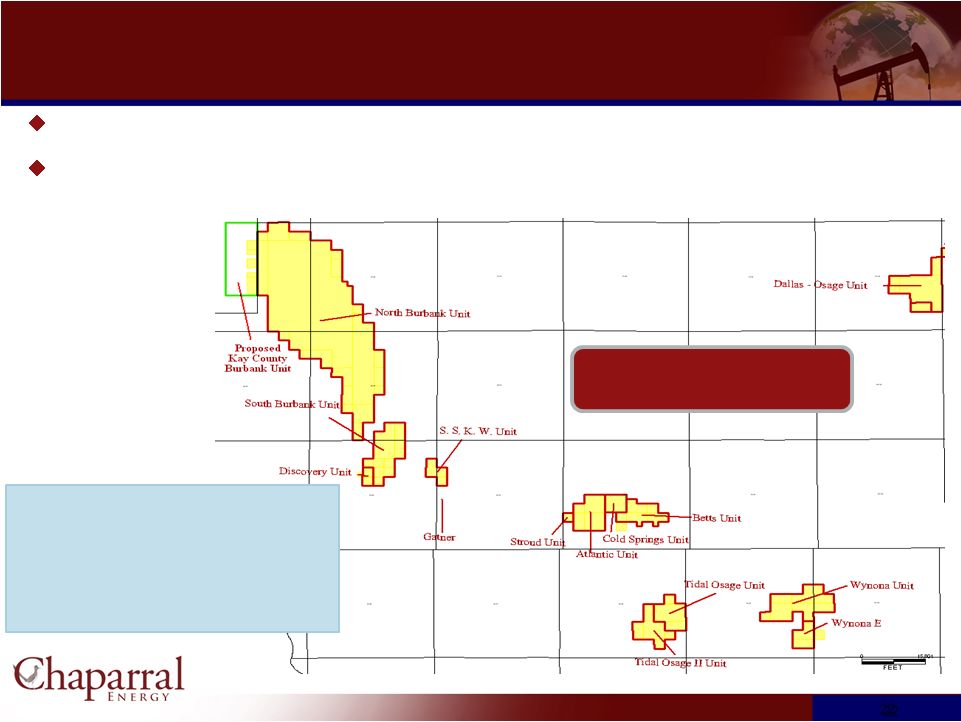

CO

2

EOR Focused Areas

CO

2

EOR Focused Areas

16

16

CO

2

Project Inventory

74 units with 1P, 2P & 3P EOR

reserves

8 units with proved reserves

8 units with CO

2

injection

CO

2

Infrastructure

–

473

Miles

318 miles of active line

68 miles under construction

87 miles of inactive line

CO

2

Supply

47 MMscf/D of existing CO

2

supply

43 MMscf/D new CO

2

supply

Panhandle Area

Permian Basin

Central

Oklahoma

Area

Burbank

Area

CO2 Tertiary Recovery Projects |

EOR 2012 Capital

Budget (1)

EOR 2012 Capital Budget

(1)

17

17

Budget by Category

($mm)

2011

Actual

2012

Budget

2012

Expanded

Budget

Infrastructure / Pipelines

14

90

106

Drilling

17

13

24

Enhancements / CO

2

Purchases

55

24

37

Total

$86

$127

$168

Panhandle

Area

Permian

Basin

Central

Oklahoma

Area

Burbank

Area

(1)

Does not include Capitalized G&A

2012 Field Projects ($mm)

Panhandle Area

Burbank Area

Central Oklahoma

Permian

Camrick Area

$18

Farnsworth Unit

28

NE Hardesty (Non-op)

7

Booker Area

4

Other

3

$60

North Burbank Unit

$104

NW Velma Hoxbar

$3

No planned expenditures for 2012 |

North Burbank Unit

– Overview

North Burbank Unit –

Overview

Chaparral’s

North

Burbank

Unit

is

its

largest

EOR

field

and

plans

to

introduce

CO

2

injection

into

the

North

Burbank Unit in 1Q 2013

Chaparral

anticipates

that

it

will

spend

$800

million

associated

with

this

EOR

project

throughout

the

life

of

the field

18

18

18

18

Total OOIP

1,163 MMBbls

Primary Production

239 MMBbls

Secondary Recovery

211 MMBbls

Tertiary Potential

119 MMBbls

Net Tertiary Potential

100 MMBbls

Burbank Area:

Net Potential: 100 MMBoe, 51% of total |

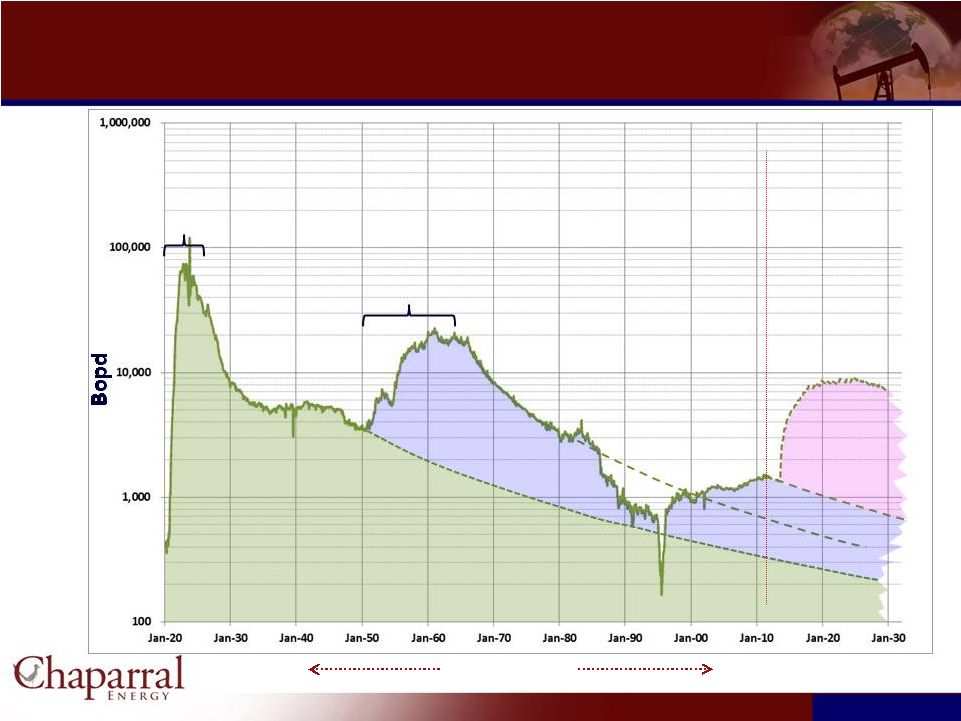

Burbank in

Perspective Burbank in Perspective

19

19

Secondary

Development

Primary

Development

Tertiary

Development

110 Years

“CO2 EOR”

+8000 BOPD

“Waterflood” |

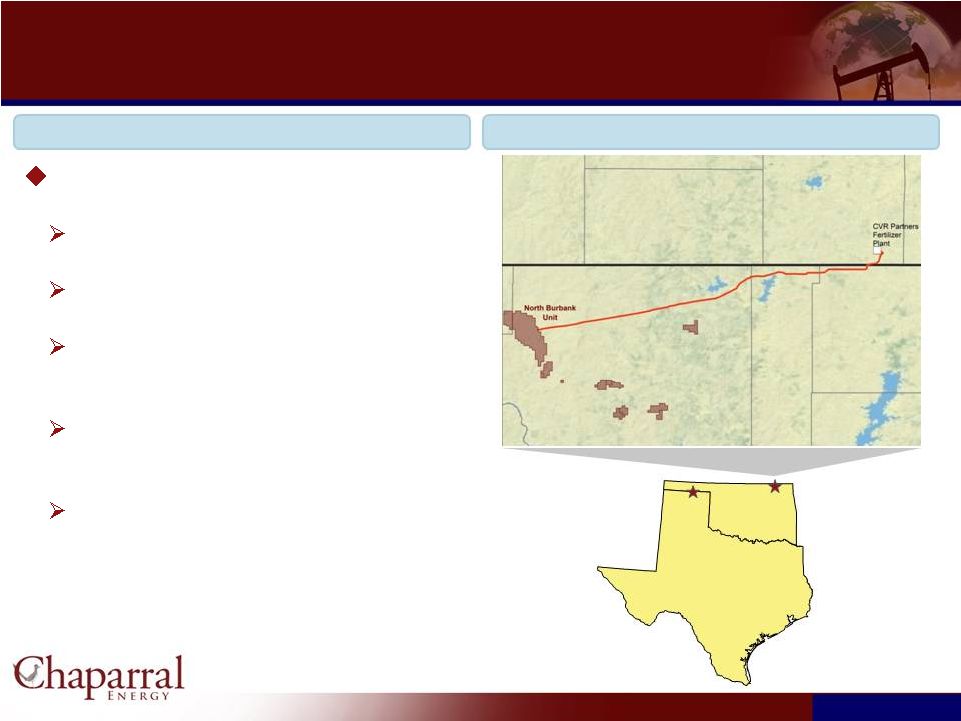

Coffeyville CO

2

System

Coffeyville CO

2

System

20

20

The Coffeyville CO

2

System

$84 million of total capital expenditures

23,500 HP compression facility

68.3-mile 8-inch pipeline with potential

capacity of approximately 60 MMcf/d.

CO

2

is sourced from the CVR Partners

fertilizer plant in Coffeyville, KS.

Online and Operational in early 2013

Oklahoma

Kansas

Panhandle

CO2

System

Coffeyville

CO2

System

Coffeyville CO2 System

Asset Map |

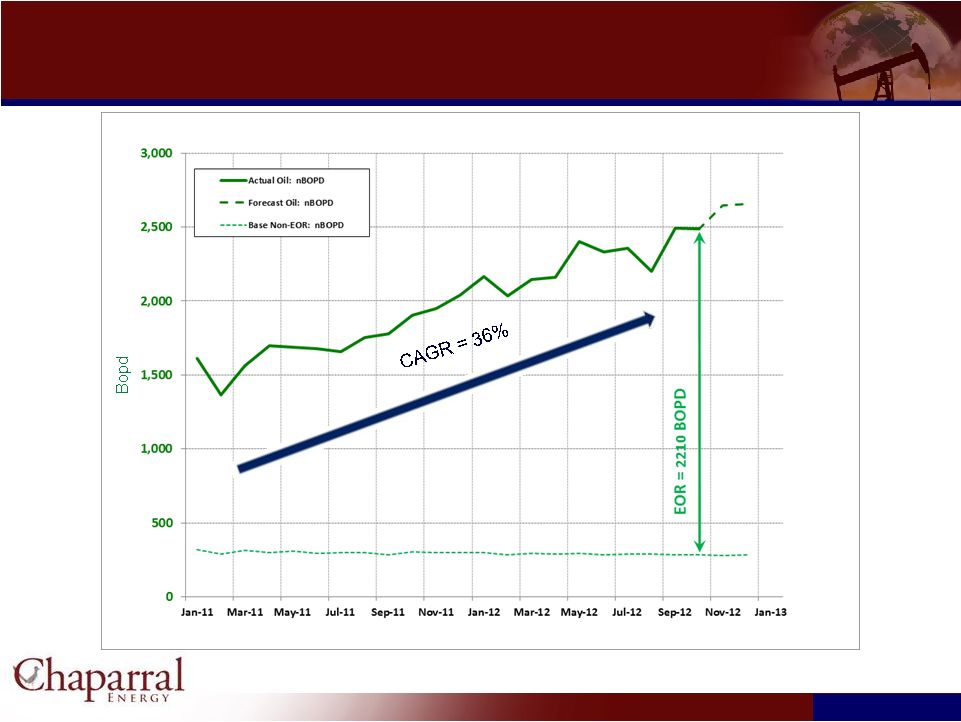

Monthly Incremental EOR

from Active CO 2

Projects

21

21 |

22

22

Potential in Excess of 740 MMBoe

Potential in Excess of 740 MMBoe

Near-term + Long-term

strategy yields significant

value increase

~ 70% Oil

De-risk play, unlock value

Production growth

Low-risk production upside

Long-life, stable production

* Woodford, Bone Spring, Avalon, Cleveland Sand, Granite

Wash, and Marmaton

Near-term focus on NOMP

Long-term focus on EOR |

Financial Performance,

Projections, and Credit Statistics

Financial Performance, Projections,

and Credit Statistics

23

23 |

24

24

Financial Summary

Financial Summary

2009

2010

2011

1H 2012

Price

Oil & NGL –

Wellhead ($/Bbl)

$55.04

$74.53

$87.52

$84.12

Gas –

Wellhead ($/Mcf)

$3.51

$4.36

$4.08

$2.21

Production (MMBoe)

7.6

8.1

8.7

4.2

Oil & NGL (MMBbls)

3.9

4.1

5.0

2.6

Gas (Bcf)

22.6

23.7

21.6

9.4

Financial Data ($mm)

Operating Expenses:

Lease Operating Expenses

$94.1

$106.1

$121.4

$63.7

Production and Ad Valorem Taxes

20.3

26.5

34.3

15.5

General and Administrative Expenses

(excludes noncash deferred comp)

22.7

27.3

38.3

23.9

Interest Expense

$90.1

$81.4

$96.7

$48.6

Adjusted EBITDA

$224

$288

$313

$153

Total Capital Expenditures

$154

$344

$336

$275

1

Includes oil & gas capex and capitalized G&A

1 |

Strong Financial

Performance Strong Financial Performance

Production (MMBoe)

Adjusted EBITDA ($mm)

Total Leverage

Capital Expenditures ($mm)

1

Includes oil & gas capex and capitalized G&A

25

25

2

Total Debt to EBITDA

7.6

8.1

8.7

7.0

7.5

8.0

8.5

9.0

2009

2010

2011

$154

$344

$336

$0

$100

$200

$300

$400

2009

2010

2011

5.3x

3.3x

3.3x

-

1.0

2.0

3.0

4.0

5.0

6.0

2009

2010

2011

$224

$288

$313

$0

$50

$100

$150

$200

$250

$300

$350

2009

2010

2011

1

2 |

Operating

Statistics 2011 Results

2012

Updated Guidance

Capital

Expenditures

$336 million

$460 million

Production

8.7 MMBoe

8.8 -

9.0 MMBoe

General and Administrative

$4.86/Boe

$5.75 -

$6.25/Boe

Lease Operating Expense

$14.03/Boe

$14.25 -

$14.75/Boe

2011 Results and 2012 Updated Guidance

2011 Results and 2012 Updated Guidance

26

26

1

Includes oil & gas capex and capitalized G&A

1 |

27

27

Hedge Portfolio

Note:

Dollars

represent

average

strike

price

of

hedges

(includes

all

derivative

instruments)

Gas Basis Hedges

YR

Price

% TP

’12

$

0.23

78%

’13

$

0.20

75%

’14

$

0.23

66%

%

of

Total

Proved

Reserves

Hedged

(as

of

October

31,

2012)

$4.44

$4.31

$3.95

$94.45

$102.45

$ 108.79

$96.28

$73.85

$ 114.26

$99.94

$77.88

$ 107.84

$95.24

$77.50

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nov -

Dec 2012

2013

2014

3 -

Way Oil Collars

Oil Swaps

Gas Swaps |

Question &

Answer Question & Answer

28

28 |