Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CITIZENS REPUBLIC BANCORP, INC. | d387041d8k.htm |

Investor Presentation

Second Quarter 2012

Exhibit 99.1 |

2

Safe Harbor Statement

Discussions and statements in this presentation that are not statements of

historical fact (including without limitation statements that include terms such as

“will,”

“may,”

“should,”

“believe,”

“expect,”

“anticipate,”

“estimate,”

“project”,

“intend,”

and

“plan”)

and

statements

regarding

Citizens’

future

financial

and

operating results, plans, objectives, expectations and intentions, are

forward- looking

statements

that

involve

risks

and

uncertainties,

many

of

which

are

beyond

Citizens’

control or are subject to change. No forward–looking statement is a

guarantee of future performance and actual results could differ

materially. Factors that could cause or contribute to such differences

include, without limitation,

risks

and

uncertainties

detailed

from

time

to

time

in

Citizens’

filings

with

the Securities and Exchange Commission.

Other factors not currently anticipated may also materially and adversely affect

Citizens’

results of operations, cash flows, financial position and prospects. There

can be no assurance that future results will meet expectations.

While Citizens

believes that the forward-looking statements in this presentation are

reasonable, you should not place undue reliance on any forward-looking

statement. In addition, these statements speak only as of the date

made. Citizens does not undertake, and expressly disclaims any

obligation to update or alter any statements, whether as a result of new

information, future events or otherwise, except as required by applicable

law. |

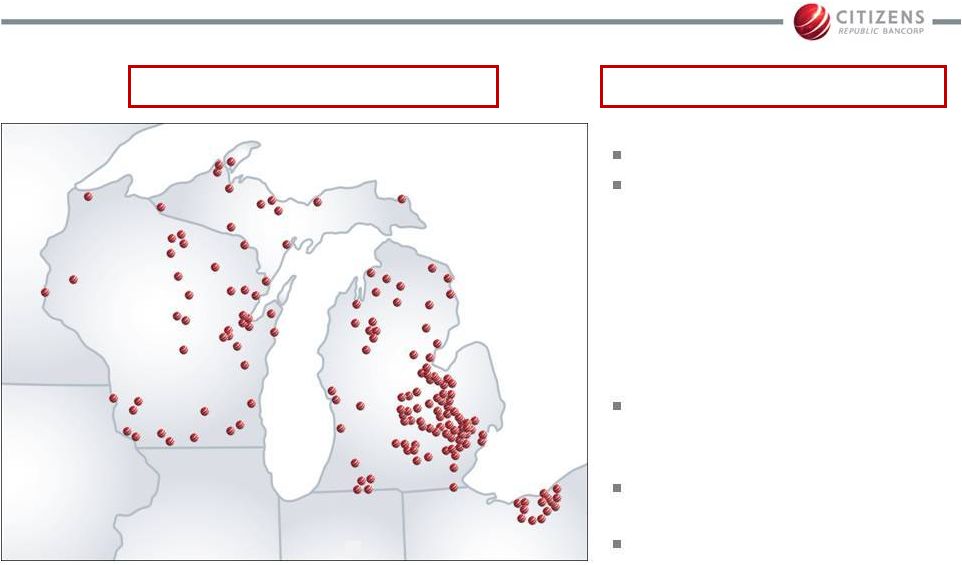

Who

We Are |

4

Who We Are

Established in 1871

57

th

largest bank holding

company in the U.S. ranked

by assets

–

$9.7 billion assets and

$7.3 billion deposits

–

Presence in 3 Upper

Midwest states with 219

branches and 248 ATMs

Increased market share in

49% of our counties since

2008

Growing number of new

clients 10% annually

80% of revenue is Michigan

based

Company Overview

219 Branches / 248 ATMs |

5

How We Deliver Our Service

Core Banking

86% of revenue

Retail consumer

Commercial clients up to $5 million loan size

Treasury Management: 31% of commercial clients use TM

services

Public Funds: focus on generating lasting relationships rather

than temporary deposits

Preferred SBA Lender: dedicated specialists to fast track

process. Expertise in other state and local loan programs.

Mortgage: accommodate and sell

Indirect marine and RV lending

Investment Center: introduce single service CD clients to

financial consultants

Corporate Banking

10% of revenue

Asset Based Lending

Corporate

Specialty healthcare focus in assisted living & skilled nursing

Wealth Management

4% of revenue

Personal Trust

Employee Benefits

Institutional Trust |

Local teams focus on delivery of :

Client service

Closing pipeline opportunities

Referring business

6

Wealth

Business

Development

Officer

Local

Advisory

Board

Commercial

Banker

Mortgage

Loan

Officer

Public

Funds

Officer

Branch

Manager

Treasury

Management

Officer

Investment

Consultant

Client

Local Delivery of Service |

Where We’ve Been |

8

Strategically Managed Through Cycle

Acquired Michigan-based bank with heavy real

estate concentrations in late 2006

Economic downturn and challenging Michigan

economy resulted in elevated credit costs

Employed strategies to reduce balance sheet risk

Enhanced capital

–

suspended dividend (1Q08)

–

$200 million common equity raise (3Q08)

–

$300 million TARP issuance (4Q08)

–

exchanged sub debt & trust preferred for $200

million of common equity (3Q09) |

9

Successful Leaders in Key Roles

Name

Title

Held

Position

Since

Cathy Nash

Chief Executive Officer

Feb. 09

Lisa McNeely

Chief Financial Officer

Aug. 10

Mark Widawski

Chief Credit Officer

Feb. 09

Brian Boike

Treasurer

Oct. 09

Judi Klawinski

Director of Core Banking

Oct. 09

Ray Green

Director of Corporate Banking

May 10

Joe Czopek

Controller

Oct. 09

Ken Duetsch

Director of Wealth Management

Aug. 11 |

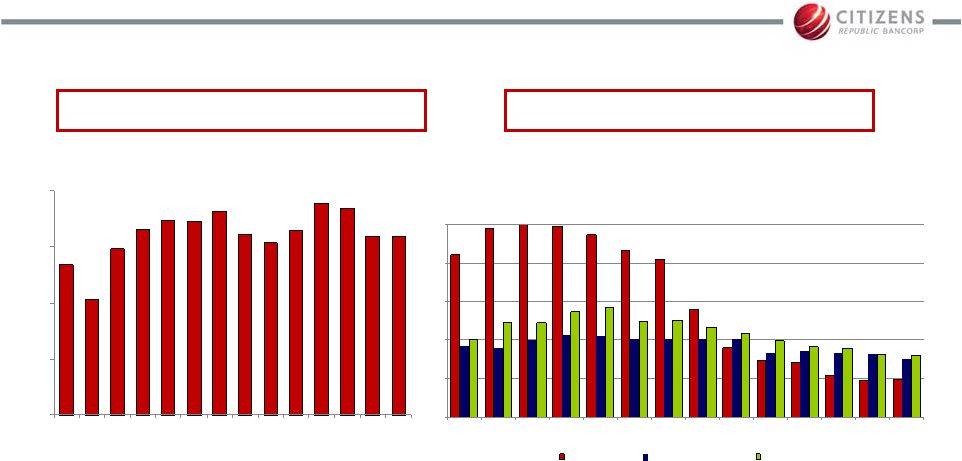

Since

2009, focused on clients/revenue while working through credit issues

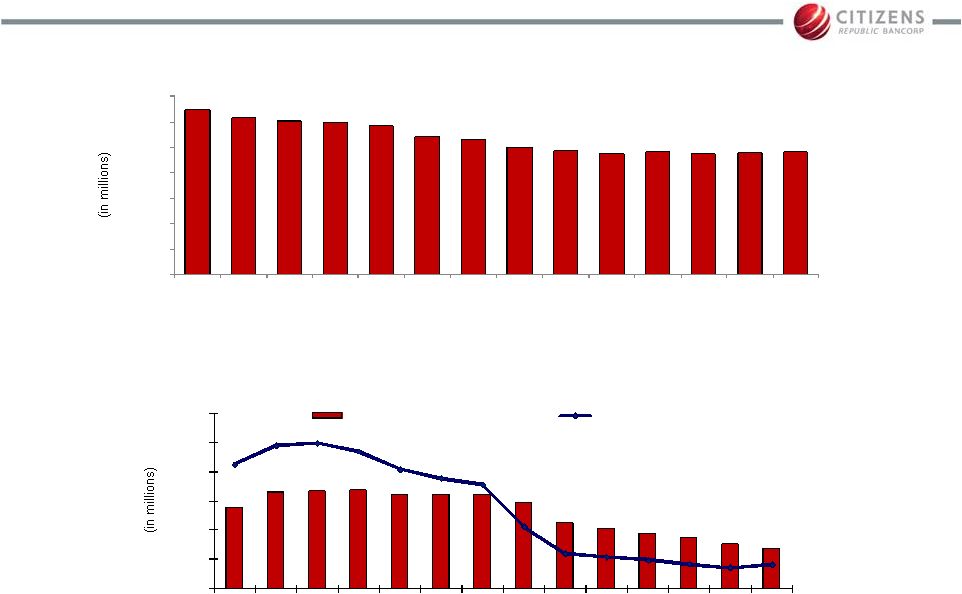

10

$26.6

$20.6

$29.6

$33.1

$34.7

$34.5

$36.2

$32.1

$30.7

$32.8

$37.8

$36.9

$31.7

$31.7

$0

$10

$20

$30

$40

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Pre-tax Pre-provision Profit*

Revenue Focus

Problem Asset Resolution Focus

Strengthened franchise

value

Eliminated uncertainty

around credit

0%

1%

2%

3%

4%

5%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q112

2Q12

NPAs / Assets %

CRBC

Peer Median**

Regional Peer Median**

(in millions)

* Non-GAAP measure, as defined by management, represents net income (loss) excluding income tax

provision (benefit) provision for loan losses, securities (gains)/losses, and any impairment

charges (including goodwill, credit write downs and fair-value adjustments) caused by this economic cycle.

** Source: SNL Financial MRQ data

|

Strategy from 2009 –

2010

1.

Preserved capital by managing assets

2.

Grew and maintained reserve levels in recognition of

portfolio risk

11

$0

$100

$200

$300

$400

$500

$600

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Allowance for Loan Losses

Non-Performing Loans

$12,982

$12,288

$12,072

$11,932

$11,652

$10,834

$10,639

$9,966

$9,724

$9,496

$9,600

$9,463

$9,577

$9,670

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Total Assets |

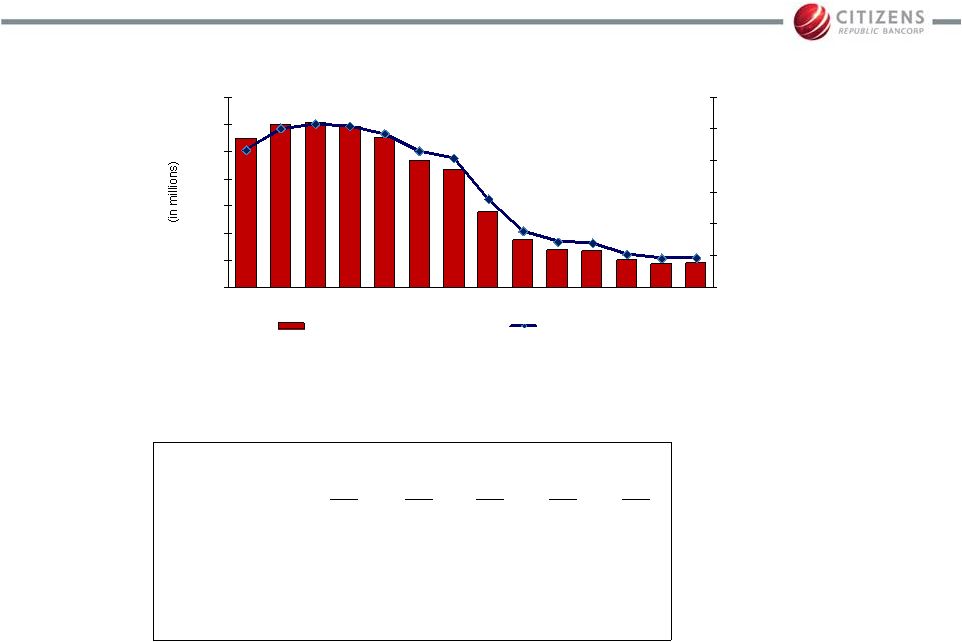

Strategy from 2009 –

2010

3.

Aggressively and actively worked out of problem assets

4.

Carefully managed capital levels to allow execution of

problem asset reduction

12

June 30,

2011

Sept. 30,

2011

Dec. 31,

2011

March 31,

2012

June 30,

2012

Leverage ratio

7.83%

8.21%

8.45%

8.71%

9.77%

Tier 1 capital ratio

12.43

12.81

13.51

13.70

14.70

Total capital ratio

13.77

14.14

14.84

14.97

15.96

Tier 1 common

equity (non-GAAP)

6.36

6.77

7.24

7.49

8.50

$549

$601

$606

$591

$551

$468

$436

$280

$175

$139

$137

$102

$91

$94

4.4%

5.0%

5.2%

5.1%

4.9%

4.3%

4.1%

2.8%

1.8%

1.5%

1.4%

1.1%

1.0%

1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

$0

$100

$200

$300

$400

$500

$600

$700

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Non-Performing Assets

NPAs as a % of Total Assets |

Where We’re Going |

Continue to Provide Top Tier Client Service

14

* Surveys conducted by Prime Performance ™

76

78

80

82

84

86

88

90

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

June 12

Likelihood to Recommend *

Citizens' Score

PPI Industry Average |

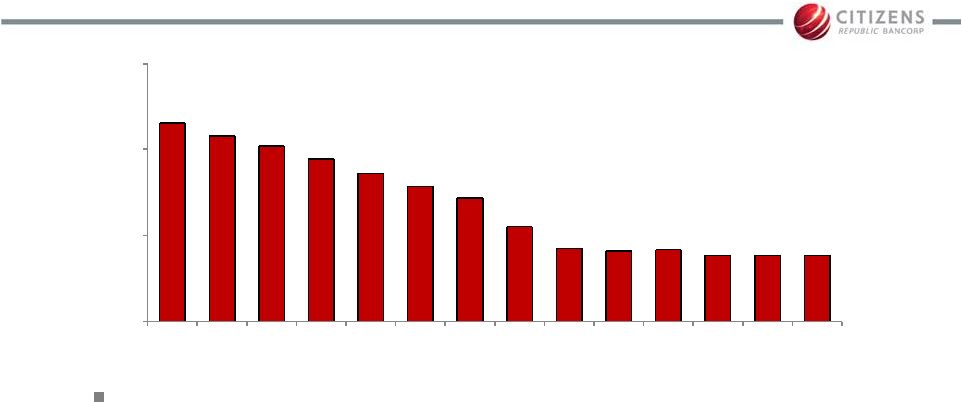

Rebuild Loan Portfolio

Focused on proven competencies

–

Business owner lending

–

Corporate lending –

structured finance, ABL, healthcare

expertise

–

Indirect marine and RV

15

$8,625

$8,302

$8,097

$7,788

$7,439

$7,138

$6,888

$6,217

$5,704

$5,628

$5,672

$5,530

$5,528

$5,522

$4,000

$6,000

$8,000

$10,000

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Loan Portfolio Balances

(in millions) |

Mitigate Expected Margin Pressure

16

2.74%

2.75%

2.99%

3.13%

3.14%

3.35%

3.32%

3.42%

3.53%

3.56%

3.63%

3.62%

3.56%

3.60%

2.00%

2.50%

3.00%

3.50%

4.00%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Net Interest Margin (FTE)

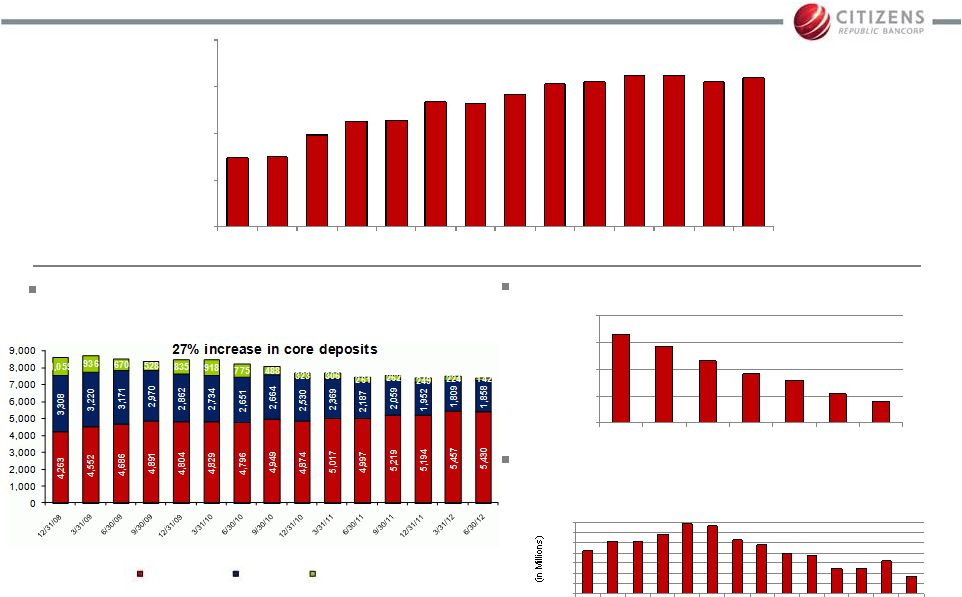

Reduce single service CD clients

Manage liquidity levels to reflect

improved credit trends

10,000

12,000

14,000

16,000

18,000

12/31/10

3/31/11

6/30/11

9/30/11

12/31/11

3/31/12

6/30/12

Single Service CD Clients

0

100

200

300

400

500

600

700

Fed Funds Sold (average)

(in millions)

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Continue focus on core deposits

Core Deposits

Retail CDs

Brokered CDs |

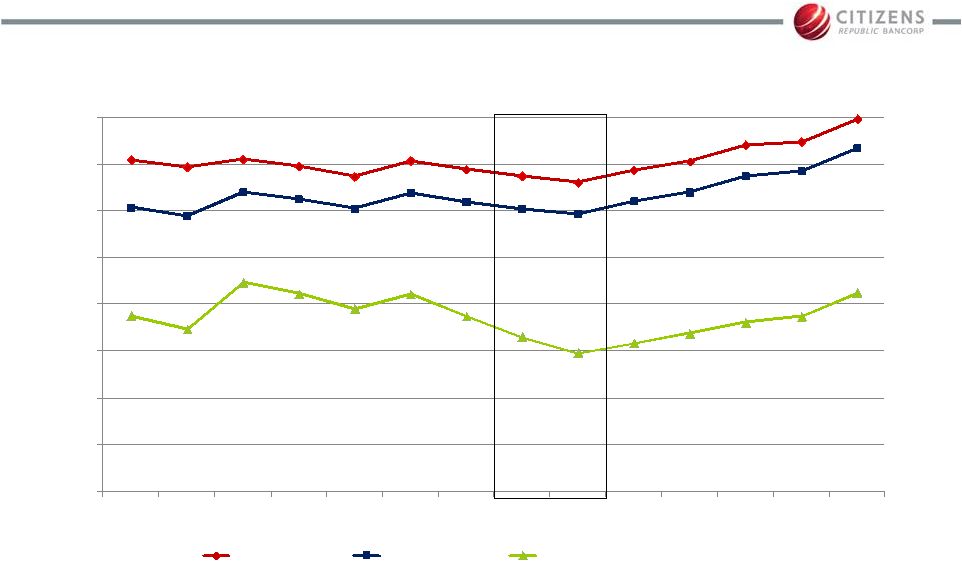

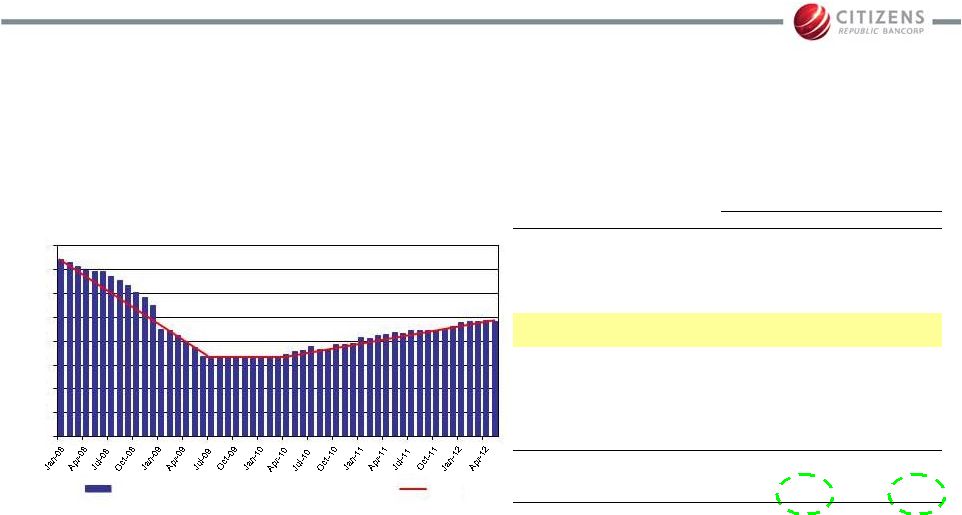

Reserve Reductions Follow Improved Metrics

17

Reserve model is historical looking; future

modeling will continue to reflect significantly

improved credit metrics

Ensure reserves reflect reduced portfolio risk and

support growth initiatives

0%

1%

2%

3%

4%

5%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Loan Loss Reserves / Loans %

CRBC

Peer Median*

Regional Peer Median*

* Source: SNL Financial MRQ data |

Report Consistent Profits

18

* Excludes discontinued operations

Reprice and add new fee income

streams to replace lost revenue from

regulatory changes

$0

$10

$20

$30

$40

$50

$60

$70

$80

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Operating Non-Interest Expense*

Salaries and Employee Benefits

Other Expenses

* Non-GAAP measure. See Appendix for reconciliation.

Continue prudent expense

management while adding key

revenue generating positions

-

5,000

10,000

15,000

20,000

25,000

30,000

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Operating Non-Interest Income*

Service charges on deposit accounts

Card-based and other nondeposit fees

Other non-interest income*

(49)

(359)

(69)

(68)

(85)

(35)

(57)

(103)

(69)

14

20

21

25

26

-400

-350

-300

-250

-200

-150

-100

-50

0

50

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Income (Loss) before Tax* |

19

2Q12 Highlights

Restored deferred tax asset

Reported consistent quarterly profit from banking

operations

–

Consistent net interest margin at 3.60%

–

Fee income from core banking services remained solid

–

Maintained control over operating expenses

Loan growth in focused areas of expertise

–

3% growth in C&I portfolio; 22% annualized YTD growth

–

6% growth in Indirect portfolio; 12% annualized YTD growth

–

Strong origination and pipeline activity in C&I and Indirect

Credit trends showed continued stability and

improvement |

Solid

Core Earnings 20

2.74%

2.75%

2.99%

3.13%

3.14%

3.35%

3.32%

3.42%

3.53%

3.56%

3.63%

3.62%

3.56%

3.60%

2.00%

2.20%

2.40%

2.60%

2.80%

3.00%

3.20%

3.40%

3.60%

3.80%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Net Interest Margin (FTE)

$109.9

$137.5

$138.2

$0

$20

$40

$60

$80

$100

$120

$140

$160

2009

2010

2011

Pre-tax Pre-provision Profit*

2.90%

3.31%

3.58%

2.00%

2.20%

2.40%

2.60%

2.80%

3.00%

3.20%

3.40%

3.60%

3.80%

2009

2010

2011

Net Interest Margin (FTE)

$26.6

$20.6

$29.6

$33.1

$34.7 $34.5

$36.2

$32.1

$30.7

$32.8

$37.8

$36.9

$31.7

$31.7

$0

$10

$20

$30

$40

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Pre-tax Pre-provision Profit* |

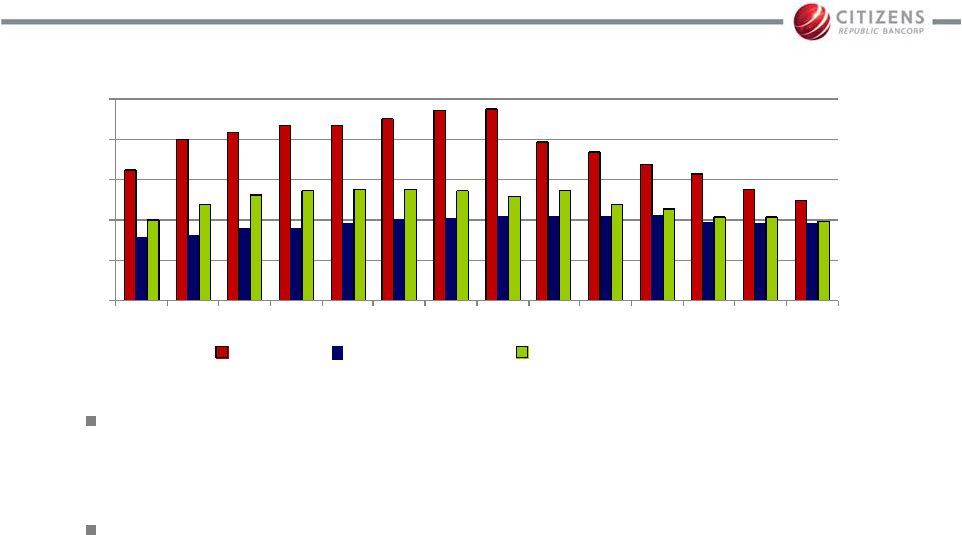

Efficiency Ratio Trends

21

70.16%

76.84%

79.23%

70.89%

68.39%

70.40%

64.19%

68.22%

67.09%

63.85%

59.89%

61.39%

65.20%

65.99%

50%

55%

60%

65%

70%

75%

80%

85%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Quarterly Efficiency Ratio

Peer Data Source: SNL Financial

74.21%

67.73%

63.05%

50%

55%

60%

65%

70%

75%

80%

2009

2010

2011

Annual Efficiency Ratio

Revenue per FTE of $207,000 is in line with peer median

of $210,000

Salary & benefits expense per FTE of $62,500 is better

than peer median of $72,200 |

Organically Growing Strong Capital Position

0%

2%

4%

6%

8%

10%

12%

14%

16%

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Total Capital

Tier 1 Capital

Tier 1 Common (non-GAAP)

22

Accelerated

resolution

of over

$920

million of

problem

assets |

23

Positioned for Growth

Successfully managed through credit cycle with a

strategic focus on revenue generation and problem

asset resolutions

Strategically focused into 2012 to

–

Continue providing top tier client service

–

Rebuild loan portfolio

–

Mitigate expected margin pressure

–

Evaluate reserve levels

–

Report consistent profitability |

24

Appendix |

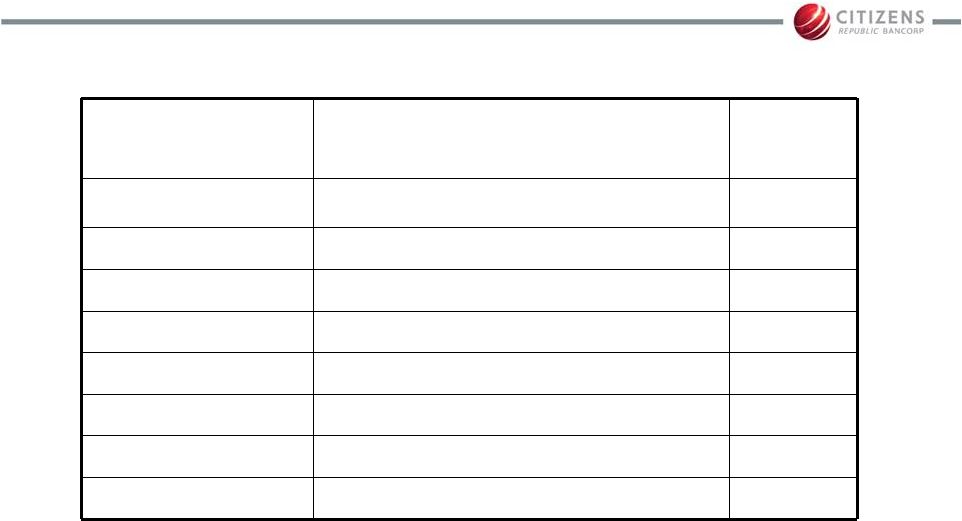

25

Upper Midwest Franchise

MSA

Rank

Number

of

Branches

Total

Deposits

($000)

% of

Franchise

% Market

Share

Michigan:

Flint, MI

1

20

1,529,744

20.4

40.48

Detroit-Warren-Livonia, MI

11

31

1,154,717

15.4

1.28

Saginaw-Saginaw Township North,

1

15

589,977

7.9

29.97

Lansing-East Lansing, MI

3

14

521,070

6.9

10.42

Jackson, MI

2

8

373,118

5.0

24.57

Bay City, MI

3

5

212,226

2.8

20.34

Ann Arbor, MI

11

6

208,963

2.8

3.37

Cadillac, MI

1

7

188,460

2.5

35.99

Owosso, MI

3

6

135,722

1.8

20.54

Sturgis, MI

3

4

107,782

1.4

15.76

Alpena, MI

1

2

94,514

1.3

27.74

Houghton, MI

3

3

87,682

1.2

13.87

Total Michigan

8

155

6,024,966

80.3

3.82

Non-Michigan:

Cleveland-Elyria-Mentor, OH

17

12

321,077

4.3

0.64

Green Bay, WI

9

9

218,449

2.9

3.29

Appleton, WI

11

6

159,161

2.1

4.10

Stevens Point, WI

5

2

92,474

1.2

7.83

Platteville, WI

8

4

74,056

1.0

6.32

Total Non-Michigan

60

1,480,553

19.7

Source: SNL Financial as of 6/30/11 |

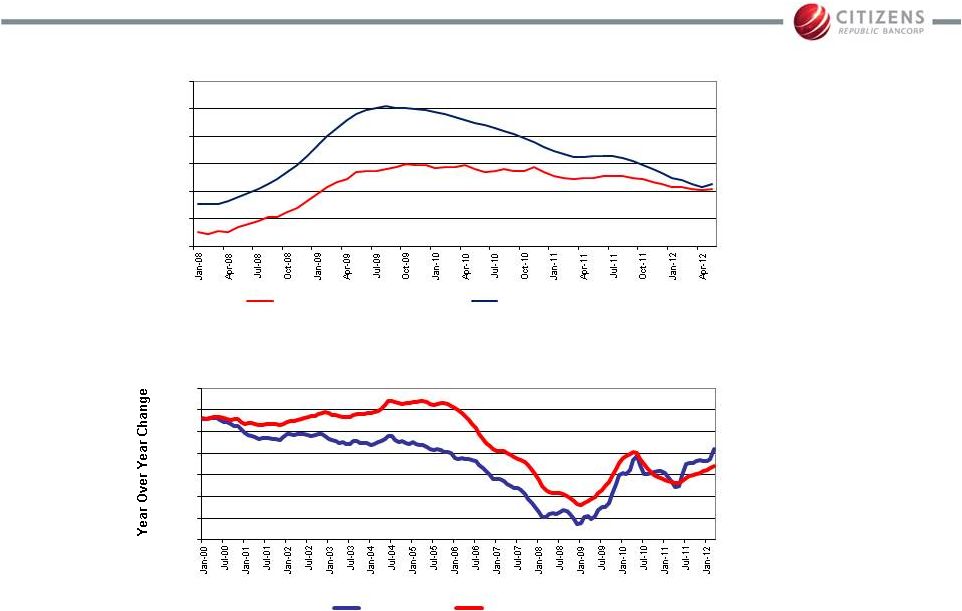

26

Continued Stabilization and Diversification

in Michigan’s Economy

Source: U.S. Bureau of Labor Statistics

Michigan Nonfarm Employment

Michigan Employment by Industry

May 2012

May 2002

$000s

%

$000s

%

Trade, Transportation, and Utilities

654.9

16.3%

754.7

16.7%

Government

617.2

15.4%

694.6

15.3%

Professional Services

579.2

14.4%

603.4

13.3%

Health Care

550.7

13.7%

472.9

10.4%

Leisure and Hospitality

389.6

9.7%

411.0

9.1%

Other Manufacturing

385.6

9.6%

486.6

10.7%

Motor Vehicle

208.7

5.2%

362.2

8.0%

Financial Activities

199.7

5.0%

214.1

4.7%

Other Services

169.2

4.2%

180.5

4.0%

Construction

123.9

3.1%

207.1

4.6%

Education Services

80.8

2.0%

65.2

1.4%

Information

53.6

1.3%

71.3

1.6%

Mining and Logging

7.7

0.2%

8.9

0.2%

Total Nonfarm

4,020.8

4,532.5

Total Manufacturing

594.3

14.8%

848.8

18.7%

in thousands

Michigan NonFarm Employment (Seasonally Adjusted)

Trend

3,500

3,600

3,700

3,800

3,900

4,000

4,100

4,200

4,300 |

27

Continued Stabilization and Diversification

in Michigan’s Economy

Unemployment Trends

Source: U.S. Bureau of Labor Statistics and Freddie Mac

4%

6%

8%

10%

12%

14%

16%

US Unemployment Rate

Michigan Unemployment Rate

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Freddie Mac House Price Index

Michigan

United States |

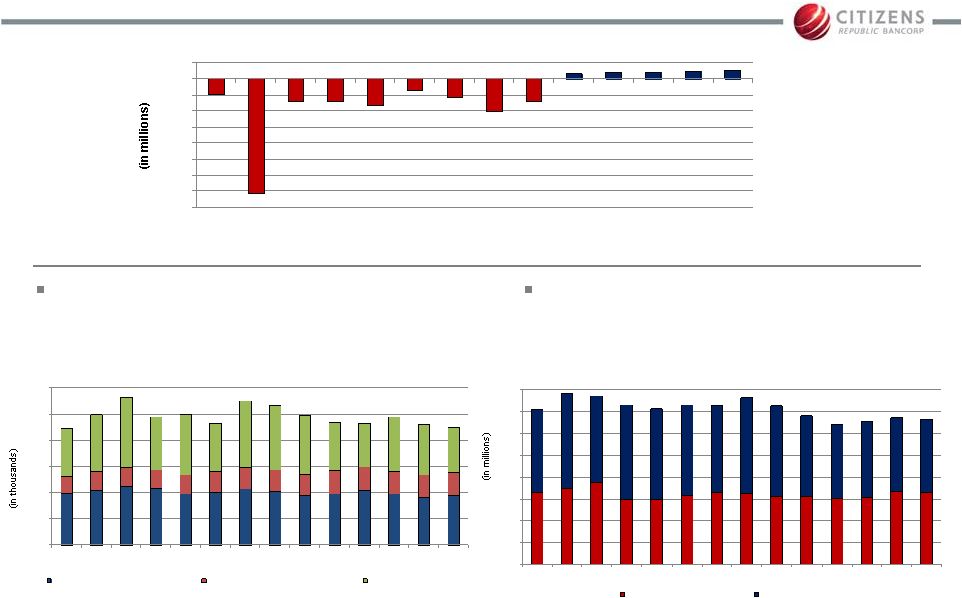

28

Core Earnings Strength

Pre-Tax Pre-Provision Profit (non-GAAP)

(in millions)

3Q11

4Q11

1Q12

2Q12

Income(loss) from continuing operations

$32.9

$18.2

$24.9

$303.2

Income tax (benefit) provision

(12.6)

2.5

-

(276.8)

Provision for loan losses

17.5

15.0

8.4

5.3

Investment securities (gains) losses

-

-

-

-

Net losses (gains) on LHFS

(2.0)

0.2

(0.9)

(0.0)

(Gains) losses on ORE

1.2

1.1

(0.4)

(0.2)

Fair-value adjustment on BOLI

0.4

(0.1)

(0.2)

0.1

Fair-value adjustment on swaps

0.3

(0.0)

(0.1)

0.1

Pre-Tax Pre-Provision Profit

(1)

$37.8

$36.9

$31.7

$31.7

Last 12 Months

$138.1

(1)

Non-GAAP measure, as defined by management, represents total revenue (total net interest income

and non-interest income) excluding any securities gains/losses, fair value adjustments on

loans held for sale, interest rate swaps, and bank owned life insurance, less non-interest

expense excluding any goodwill impairment charges, credit write downs, fair value adjustments and

special assessments. |

29

(in millions)

2009

2010

2011

Income (loss) from continuing operations

($505.7)

($289.1)

$6.7

Income tax (benefit) provision

(29.6)

12.9

(20.2)

Provision for loan losses

323.8

392.9

138.8

Goodwill impairment charge

256.3

-

-

Net loss on debt extinguishment

15.9

-

-

Investment securities (gains) losses

(0.0)

(13.9)

1.3

FDIC special assessment

5.4

-

-

Net losses (gains) on LHFS

20.1

20.6

(1.8)

Losses on ORE

23.3

13.4

12.8

Fair-value adjustment on BOLI

(0.1)

(0.1)

0.2

Fair-value adjustment on swaps

0.6

0.8

0.4

Pre-Tax Pre-Provision Profit

(1)

$109.9

$137.5

$138.2

Core Earnings Strength

Pre-Tax Pre-Provision Profit (non-GAAP)

(1)

Non-GAAP measure, as defined by management, represents total revenue (total net interest income

and non-interest income) excluding any securities gains/losses, fair value adjustments on

loans held for sale, interest rate swaps, and bank owned

life insurance, less non-interest expense excluding any goodwill impairment charges, credit write

downs, fair value adjustments and special

assessments. |

30

Quarterly Non-Interest Income Trends

(in thousands)

2Q 11

3Q 11

4Q 11

1Q12

2Q12

Service charges on deposit accounts

$9,753

$10,362

$9,724

$8,985

$9,355

Trust fees

3,811

3,622

3,747

3,602

3,582

Mortgage and other loan income

1,883

2,089

2,705

1,858

1,952

Brokerage and investment fees

1,533

1,188

1,243

1,324

1,331

Card-based and other nondeposit fees

4,394

4,475

4,305

4,265

4,444

Net (losses) gains on loans held for sale

1,179

1,952

(217)

916

6

Investment securities gains (losses)

(993)

3

38

-

-

Other income

1,765

736

2,818

3,290

1,675

Total Non-Interest Income (GAAP)

$23,325

$24,427

$24,363

$24,240

$22,345

Investment securities gains (losses)

$993

(3)

$

(38)

$

-

$

-

$

Net (losses) gains on loans held for sale

(1,179)

(1,952)

217

(916)

(6)

Fair value adjustment on BOLI

48

385

(100)

(205)

118

Fair value adjustment on swaps

77

268

(46)

(61)

74

Operating Non-interest Income

(Non-GAAP)

$23,264

$23,125

$24,396

$23,058

$22,531 |

31

Annual Non-Interest Income Trends

(in thousands)

2009

2010

2011

Service charges on deposit accounts

$42,116

$40,336

$39,268

Trust fees

14,784

15,603

15,103

Mortgage and other loan income

12,393

10,486

9,620

Brokerage and investment fees

5,194

4,579

5,072

ATM network user fees

6,283

7,057

7,511

Bankcard fees

7,714

8,859

9,656

Net (losses) gains on loans held for sale

(20,086)

(20,617)

1,808

Net loss on debt extinguishment

(15,929)

-

-

Investment securities gains (losses)

5

13,896

(1,336)

Other income

10,659

14,460

8,555

Total Non-Interest Income (GAAP)

$63,133

$94,659

$95,257

Net loss on debt extinguishment

$15,929

-

$

-

$

Investment securities gains (losses)

(5)

(13,896)

1,336

Net (losses) gains on loans held for sale

20,086

20,617

(1,808)

Fair value adjustment on BOLI

(144)

(67)

233

Fair value adjustment on swaps

606

782

413

Operating Non-interest Income

(Non-GAAP)

$99,605

$102,095

$95,431 |

32

Quarterly Non-Interest Expense Trends

(in thousands)

2Q 11

3Q 11

4Q 11

1Q12

2Q12

Salaries and employee benefits

$31,265

$30,280

$30,952

$33,298

$32,801

Occupancy

6,047

6,125

6,326

6,696

6,140

Professional services

2,407

2,394

2,311

2,023

2,465

Equipment

2,841

2,918

3,326

3,303

2,904

Data processing services

4,247

3,823

3,709

4,048

3,721

Advertising and public relations

1,802

2,179

1,298

1,335

1,708

Postage and delivery

1,120

1,142

1,165

1,099

1,119

Other loan expenses

3,314

3,941

3,497

3,186

3,266

Losses on other real estate (ORE)

1,355

1,210

1,081

(385)

(173)

ORE expenses

1,029

529

995

450

266

Intangible asset amortization

778

732

688

578

545

Other expense

13,239

10,138

11,292

11,470

11,577

Total Non-Interest Expense (GAAP)

$69,444

$65,411

$66,640

$67,101

$66,339

Losses (gains) on ORE

1,355

1,210

1,081

(385)

(173)

Operating Non-Interest Expense

(Non-GAAP)

$68,089

$64,201

$65,559

$67,486

$66,512 |

33

Annual Non-Interest Expense Trends

(in thousands)

2009

2010

2011

Salaries and employee benefits

$135,389

$126,384

$123,514

Occupancy

26,723

26,963

26,059

Professional services

11,877

10,550

9,331

Equipment

11,714

12,482

12,136

Data processing services

17,692

18,734

16,131

Advertising and public relations

7,113

6,530

5,848

Postage and delivery

5,525

4,571

4,543

Other loan expenses

24,553

20,311

16,007

Losses on other real estate (ORE)

23,312

13,438

12,768

ORE expenses

4,389

4,970

4,322

Intangible asset amortization

7,036

3,923

3,027

Goodwill impairment

256,272

-

-

Other expense

53,544

58,231

49,464

Total Non-Interest Expense (GAAP)

$585,139

$307,087

$283,150

Goodwill impairment

256,272

$

-

$

-

$

FDIC Special Assessment

5,351

-

-

Fair-value adjustment on ORE

23,312

13,438

12,768

Operating Non-Interest Expense

(Non-GAAP)

$300,204

$293,649

$270,382 |

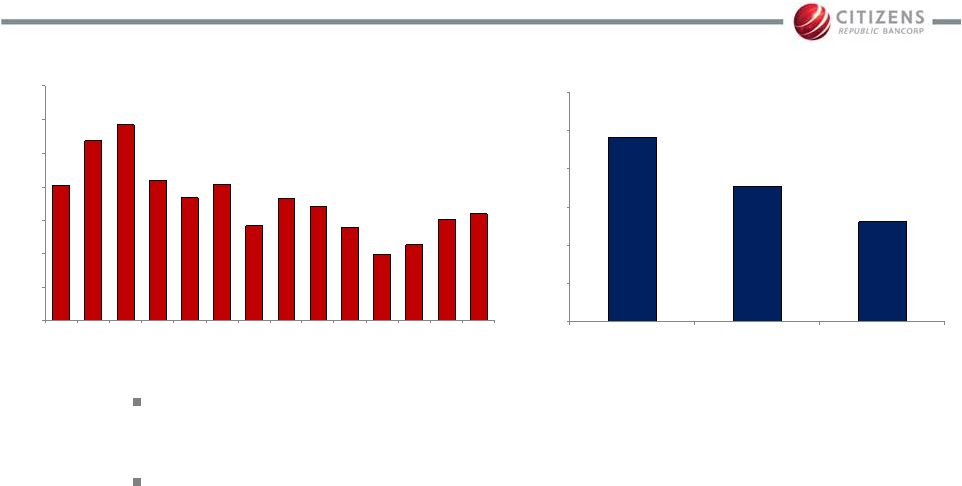

34

($ in millions)

Market

% of

Credit Rating

Value

Total

Gov't & Agency

2,538

$

89.7%

AAA

26

0.9%

AA

143

5.0%

A

43

1.5%

BAA1, BAA2 & BAA3

58

2.0%

BA1 & Lower

2

0.1%

Non-rated

19

0.7%

Total

2,829

$

100.0%

•

Over $2.1 billion in unpledged securities

•

No OTTI concerns

•

Over 70% of portfolio are GNMA securities

purchased over the last 2 –

3 years

($ in millions)

Book

Market

TEY*

Duration

Type

Value

Value

(%)

(years)

MBS Agency

989

$

1,028

$

2.87%

2.13

CMO - Agency

264

270

2.65%

1.50

CMO - Non-agency

69

68

3.53%

0.85

Municipals

108

114

6.31%

2.75

Total Available for Sale

1,430

$

1,480

$

3.12%

2.00

MBS Agency

873

$

911

$

3.04%

1.94

CMO - Agency

321

329

1.94%

2.00

Municipals

102

109

5.98%

3.06

Total Held to Maturity

1,296

$

1,349

$

3.00%

2.04

Total Investment Securities

2,726

$

2,829

$

3.06%

2.02

Investment Portfolio at June 30, 2012

* Taxable equivalent yield, except for Municipal yields which are before tax

effect Effective Management of Securities Portfolio Provides

Source of Liquidity |

35

Maintaining Strong Capital Levels

($ in millions)

6/30/10

9/30/10

12/31/10

3/31/11

6/30/11

9/30/11

12/31/11

3/31/12

6/30/12

Tier 1 capital

$ 952

$ 886

$ 777

$ 706

$ 727

$ 758

$ 773

$ 795

$ 860

Qualifying LLR

96

92

83

76

74

75

73

74

74

Qualifying capital securities

7

7

7

3

3

3

3

-

-

Total risk-based capital

$ 1,055

$ 985

$ 867

$ 785

$ 805

$ 836

$ 850

$ 869

$ 934

Tier 1 capital

$ 952

$ 886

$ 777

$ 706

$ 727

$ 758

$ 773

$ 795

$ 860

Qualifying capital securities

(74)

(74)

(74)

(74)

(74)

(74)

(74)

(74)

(74)

Preferred stock

(275)

(277)

(278)

(280)

(282)

(283)

(285)

(287)

(289)

Tier 1 common equity

$ 603

$ 535

$ 425

$ 352

$ 371

$ 401

$ 415

$ 435

$ 497

Total Capital Ratio

14.17%

13.80%

13.51%

13.24%

13.77%

14.14%

14.84%

14.97%

15.96%

Tier 1 Capital Ratio

12.79%

12.41%

12.11%

11.90%

12.43%

12.81%

13.51%

13.70%

14.70%

Tier 1 Leverage Ratio

8.72%

8.50%

7.71%

7.39%

7.83%

8.21%

8.45%

8.71%

9.77%

Tier 1 Common Ratio *

8.10%

7.50%

6.62%

5.93%

6.36%

6.77%

7.24%

7.49%

8.50%

TCE to TA *

5.83%

5.34%

4.20%

3.59%

4.05%

4.31%

4.47%

4.68%

7.73%

TA -

tangible assets

* Non-GAAP

TCE -

tangible common equity |

36

Non-GAAP Common Equity Ratios

(1)

Other assets deducted from Tier 1 capital and risk-weighted assets consist of

intangible assets (excluding goodwill) ($ in thousands)

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Total assets

$9,724

$9,496

$9,600

$9,463

$9,577

$9,670

Goodwill

(318)

(318)

(318)

(318)

(318)

(318)

Other intangible assets

(10)

(9)

(8)

(7)

(7)

(6)

Tangible assets

$9,396

$9,169

$9,274

$9,137

$9,252

$9,346

Total shareholders' equity

$945

$980

$1,009

$1,020

$1,045

$1,336

Goodwill

(318)

(318)

(318)

(318)

(318)

(318)

Other intangible assets

(10)

(9)

(8)

(7)

(7)

(6)

Tangible equity

$618

$653

$683

$694

$720

$1,011

Preferred stock

(280)

(282)

(283)

(285)

(287)

(289)

Tangible common equity

$338

$371

$400

$409

$433

$723

Total shareholders' equity

$945

$980

$1,009

$1,020

$1,045

$1,336

Qualifying capital securities

74

74

74

74

74

74

Goodwill

(318)

(318)

(318)

(318)

(318)

(318)

Disallowed tax assets

-

-

-

-

-

(236)

Accumulated other comprehensive income

14

1

1

6

2

10

Other assets

(1)

(10)

(9)

(8)

(7)

(7)

(6)

Total Tier 1 capital (regulatory)

$706

$728

$758

$773

$795

$860

Qualifying capital securities

(74)

(74)

(74)

(74)

(74)

(74)

Preferred stock

(280)

(282)

(283)

(285)

(287)

(289)

Total Tier 1 common equity (non-GAAP)

$352

$372

$401

$415

$435

$497

Net risk-weighted assets (regulatory)

(1)

$5,930

$5,850

$5,913

$5,723

$5,804

$5,852

Tangible common equity to tangilbe assets ratio

3.59%

4.05%

4.31%

4.47%

4.68%

7.73%

Tier 1 common equity ratio (non-GAAP)

5.93%

6.36%

6.77%

7.24%

7.49%

8.50% |

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

37

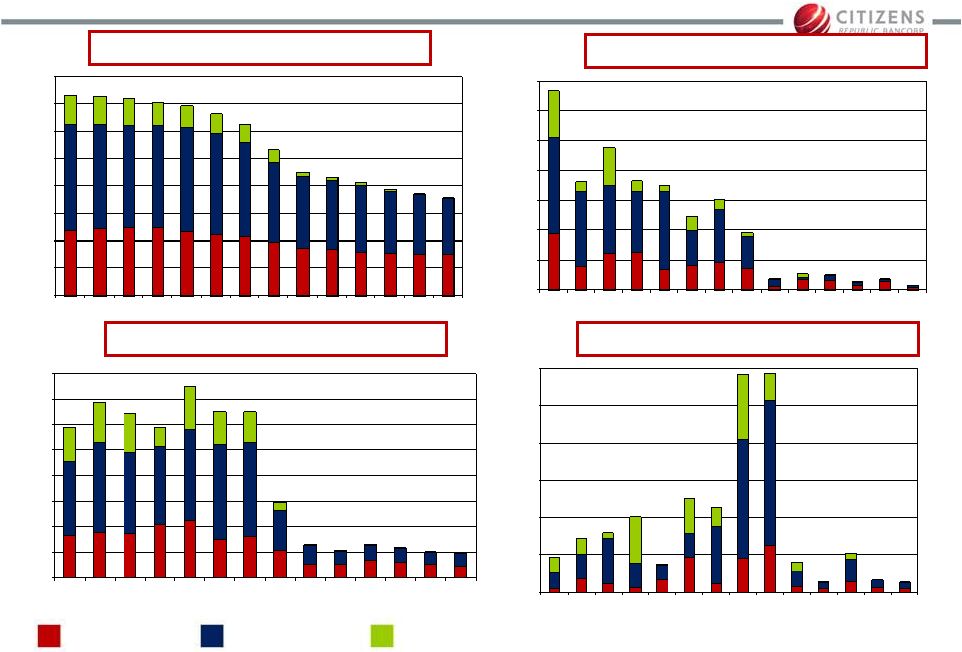

Proactive Credit Management

$0

$50

$100

$150

$200

$250

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

30-89 Day Past Due

Portfolio Balances

Non-Performing Loans

($ in millions)

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Net Charge-Offs

$0

$2,000

$4,000

$6,000

$8,000

$10,000

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Residential Mtg

Consumer

Income Producing

Land Hold, Land Dev. & Const.

Owner Occupied

C&I |

$0

$5

$10

$15

$20

$25

$30

$35

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

$0

$20

$40

$60

$80

$100

$120

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

$0

$10

$20

$30

$40

$50

$60

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

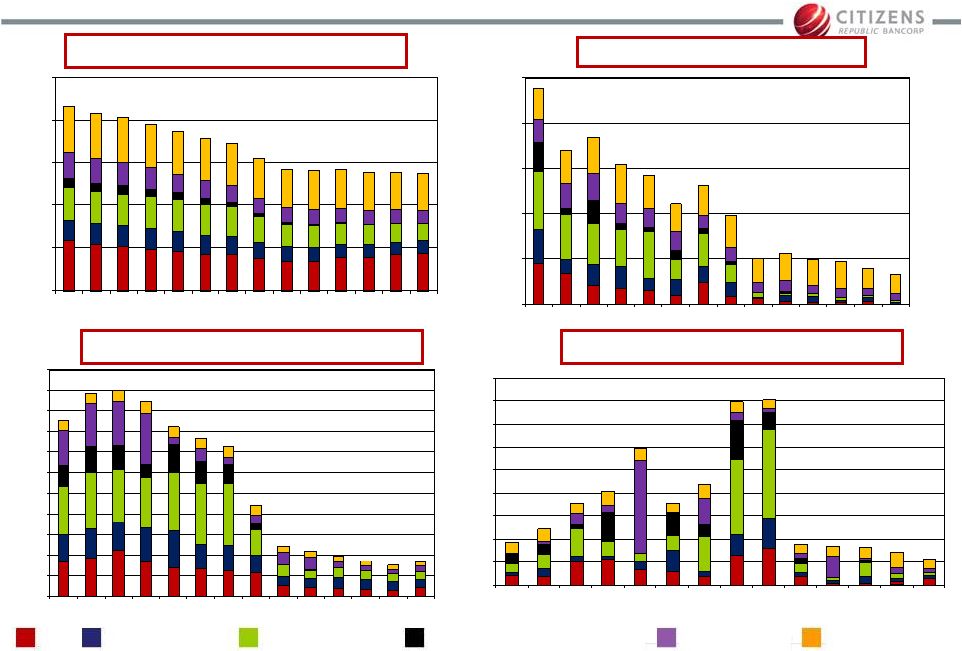

38

Commercial & Industrial Portfolio

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

30-89 Day Past Due

Portfolio Balances

($ in millions)

C&I

Non-Performing Loans

Net Charge-Offs

Small Business |

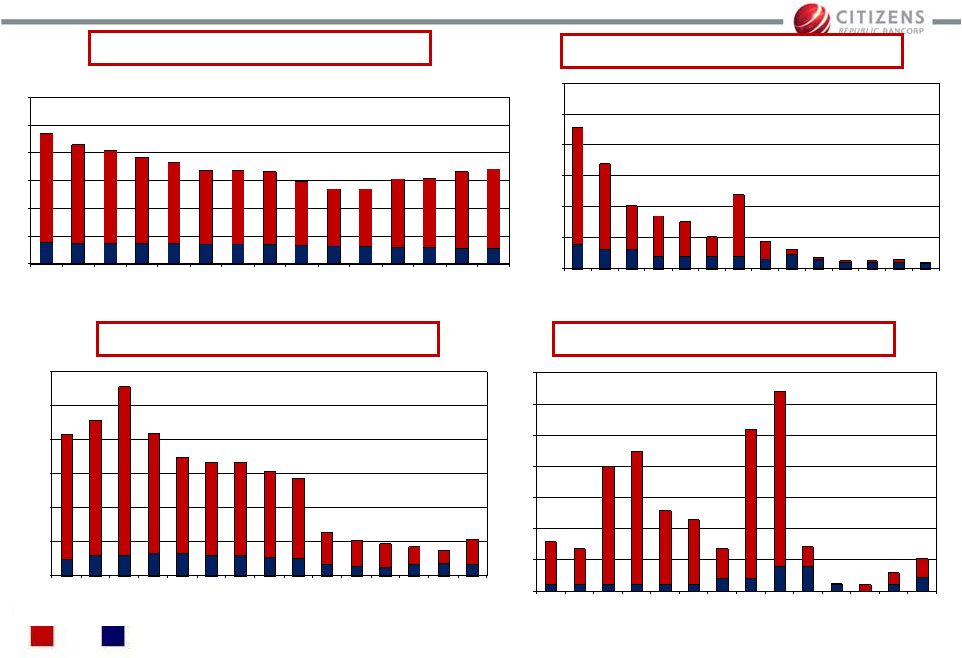

39

Commercial Portfolio Size Characteristics

< $5 million

$5 - $10 million

> $10 million

Total

Total Commercial Portfolio

Total (millions)

1,982

$

578

$

569

$

3,129

$

# of loans

7,005

83

37

7,125

Average loan size

$283,000

$6,961,000

$15,368,000

$439,000

Delinquencies

Total (millions)

4

$

-

$

-

$

4

$

# of loans

28

-

-

28

Average loan size

$144,000

-

$

-

$

$144,000

Nonperforming Loans

Total (millions)

53

$

6

$

-

$

60

$

# of loans

198

1

-

199

Average loan size

$269,000

$6,375,000

-

$

$299,000

Loan size category: |

$0

$40

$80

$120

$160

$200

$240

$280

$320

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

$0

$20

$40

$60

$80

$100

$120

$140

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

40

Commercial Real Estate Portfolio

$0

$400

$800

$1,200

$1,600

$2,000

$2,400

$2,800

$3,200

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

30-89 Day Past Due

Portfolio Balances

($ in millions)

Owner Occupied

Income Producing Land

Hold, Land Development & Construction Non-Performing Loans

$0

$20

$40

$60

$80

$100

$120

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Net Charge-Offs |

41

Commercial Real Estate Portfolio

By Collateral

By Region |

$0

$20

$40

$60

$80

$100

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

42

Consumer Portfolio

$0

$20

$40

$60

$80

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

30-89 Day Past Due *

Portfolio Balances

Non-Performing Loans *

Net Charge-Offs *

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q12

($ in millions)

$0

$20

$40

$60

$80

$100

$120

$140

$160

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

Indirect

Other Direct

Home Equity

Residential Mortgage

* Other direct included with Home Equity

|

43

Consumer Portfolio Profiles

Home Equity

$36,200 avg

loan size

Indirect

(1)

$23,700 avg

loan size

(1) Indirect loans are RV and marine only (no auto)

Consumer Portfolio

Strong refreshed FICO scores

740 Home Equity

740 Indirect

726 Other Direct

45% of home equity is first lien position

Indirect NPLs have been less than

$2.6 million, or 0.33% of total,

throughout the cycle

Other

Direct

$19,500 avg

loan size

Residential Mortgage Portfolio

$165,000 average loan size

721 refreshed FICO score

66% average original LTV

Seasoned portfolio –

53% originated

2004 or earlier

Foreclosures are handled by PHH;

Michigan does not follow a judicial

foreclosure process

Michigan

84%

Ohio

6%

Wisconsin

4%

Other

6% |

44

Non-Performing Loans

Commercial

Real Estate

$37.9

45.0%

Commercial

$21.7

25.7%

Residential

Mortgage

$13.5

16.0%

($ in millions)

Direct

Consumer

$9.3

11.0%

$84.3 million or 1.53% of portfolio

Indirect

Consumer

$1.9

2.2%

Loans 90+

Accruing

$0.01

Loan loss reserve = $136.1

million

Allowance for loan losses to

NPLs = 161.5% |

45

(in millions)

3Q11

4Q11

1Q12

2Q12

Beginning NPAs

$139.4

$136.9

$102.2

$90.6

Commercial:

Additions

23.9

13.3

14.0

23.8

Payments

(11.0)

(8.0)

(11.7)

(12.0)

Returned to accruing status

(0.3)

-

-

(0.5)

Charge-Offs/ OREO writedown

(6.3)

(12.7)

(10.3)

(0.9)

Consumer - net change

(8.8)

(27.3)

(3.6)

(7.1)

Ending NPAs

$136.9

$102.2

$90.6

$94.0

Aggressive Non-Performing Asset Management

Quarterly Non-Performing Asset Activity

*

* 2Q12 inflows include a single $14 million relationship

|

46

Peer Groups

Company Name

Ticker

Company Name

Ticker

Associated Banc-Corp

ASBC

Huntington Bancshares Incorporated

HBAN

Comerica Incorporated

CMA

KeyCorp

KEY

Commerce Bancshares, Inc.

CBSH

MB Financial, Inc.

MBFI

Fifth Third Bancorp

FITB

Old National Bancorp

ONB

First Midwest Bancorp, Inc.

FMBI

PNC Financial Services Group, Inc.

PNC

FirstMerit Corporation

FMER

TCF Financial Corporation

TCB

Flagstar Bancorp, Inc.

FBC

Wintrust Financial Corporation

WTFC

Company Name

Ticker

Company Name

Ticker

Associated Banc-Corp

ASBC

MB Financial, Inc.

MBFI

BancorpSouth, Inc.

BXS

National Penn Bancshares, Inc.

NPBC

Chemical Financial Corporation

CHFC

Old National Bancorp

ONB

Commerce Bancshares, Inc.

CBSH

Park National Corporation

PRK

Cullen/Frost Bankers, Inc.

CFR

Sterling Financial Corporation

STSA

F.N.B. Corporation

FNB

Susquehanna Bancshares, Inc.

SUSQ

First Citizens BancShares, Inc.

FCNCA

TFS Financial Corporation (MHC)

TFSL

First Midwest Bancorp, Inc.

FMBI

Trustmark Corporation

TRMK

FirstMerit Corporation

FMER

UMB Financial Corporation

UMBF

Flagstar Bancorp, Inc.

FBC

Valley National Bancorp

VLY

Fulton Financial Corporation

FULT

Wintrust Financial Corporation

WTFC

Regional Peers

Selected Peers |

www.citizensbanking.com |