Attached files

| file | filename |

|---|---|

| 8-K - BRYN MAWR BANK CORPORATION -- FORM 8-K - BRYN MAWR BANK CORP | d341980d8k.htm |

| EX-99.1 - SCRIPT FOR APRIL 27, 2012 EARNINGS CONFERENCE CALL - BRYN MAWR BANK CORP | d341980dex991.htm |

First Quarter

2012

Update

March 31, 2012

Bryn Mawr Bank

Corporation

NASDAQ: BMTC

Strong -

Stable -

Secure

Exhibit 99.2 |

1

Safe Harbor

This presentation contains statements which, to the extent that they are not

recitations of historical fact may constitute forward-looking statements for

purposes of the Securities Act of 1933, as amended, and the Securities

Exchange Act of 1934, as amended.

Please see the section titled Safe Harbor at the end of the presentation for more

information regarding these types of statements.

The

information

contained

in

this

presentation

is

correct

only

as

of

April

26,

2012.

Our business, financial condition, results of operations and

prospects may have changed since that date, and we do not undertake to

update such information. |

2

Bryn Mawr Bank Corporation

Profile

Founded in 1889 –

122 year history

A unique business model with a traditional commercial bank ($1.8

billion)

and a trust company ($5.2 billion) under one roof at March 31, 2012

Wholly owned subsidiary –

The Bryn Mawr Trust Company

Largest community bank in Philadelphia’s affluent western suburbs

26 years on the NASDAQ |

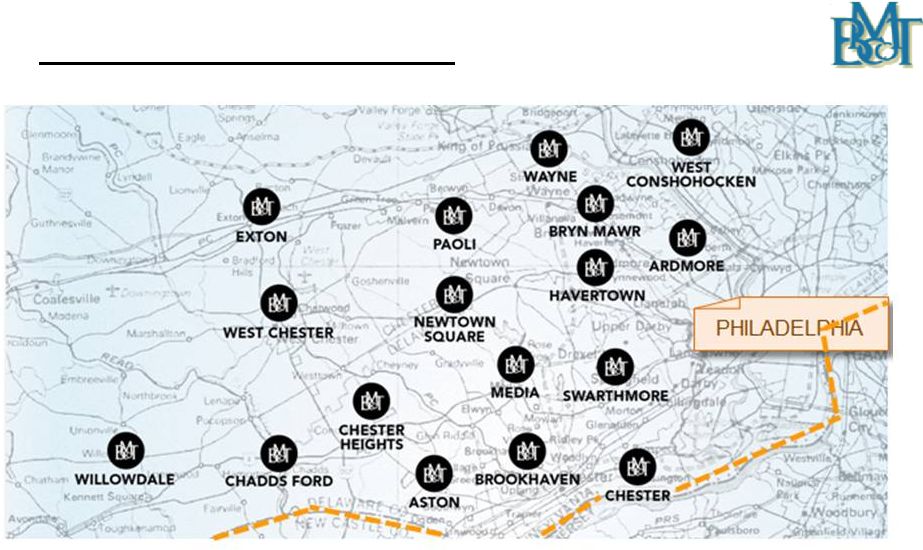

3

Southeast PA Footprint

•

17 BMTC Full Service Branch Locations |

4

Investment Considerations

Quarterly dividend of $0.16 per share

Year to Date at March 31, 2012:

Return on Average Assets (ROA):

1.18%

Return on Average Equity (ROE):

11.26%

Solid financial fundamentals and well capitalized

New business initiatives driving growth

$5.2 billion wealth management business that provides a significant

source of non-interest income |

5

Comments on BMTC from Bank Analysts

Well Positioned to Outperform in Sustained Low Rate Environment –

BMTC

(Sterne Agee, April 2012)

Advocate an overweight position in BMTC given its strong growth

prospects, benign credit costs, and positive operating leverage

potential

(Keefe, Bruyette & Woods, February 2012)

Bryn Mawr continues to be an attractive name, given its premium

profitability and substantial franchise value

(Stifel Nicolaus, April 2012)

The Company has better profitability compared to peers, manageable

credit issues and a healthy capital base

(Sandler O’Neill + Partners, February 2012) |

6

First Quarter 2012 BMTC Stock Performance

Closing price on December 30, 2011:

$19.49

Closing price on March 30, 2012:

$22.44

Dividends declared per share –

First Quarter 2012:

$0.16

Security or Index

Year to Date

2012 Return

Dividend Yield**

BMTC*

16.02%

3.02%

NASDAQ Bank Index*

14.14%

1.97%

KBW Bank Index*

26.95%

1.76%

*Source: Bloomberg

**Trailing 12-month period |

7

Consistent BMTC Annual Dividend

Year

Annual

Dividend

Dividend Yield

Year-End

Dividend Payout

Ratio

2008

$0.54

2.69%

50.0%

2009

$0.56

3.71%

47.5%

2010

$0.56

3.21%

65.9%*

2011

$0.60

3.08%

39.0%

*Excluding the $5.7 million of merger related and due diligence expense,

the dividend payout ratio was 46.0%. |

8

Growth Initiatives |

9

2012 Strategic Initiatives

3-5-3 Strategic Plan

$3

billion

in

banking

assets

-

$5

billion

in

wealth

assets

–

3

years

(Spring 2015)

Organic

growth

–

opportunistic

expansion

Management requires additional acquisitions to be accretive to

earnings per share in first 12 months (excluding merger costs)

|

10

2012 Strategic Initiatives -

continued

Focus on the net interest margin

Concentrate on growing fee based income

Continued emphasis on strong credit quality

Integrate, streamline and assimilate recent acquisitions into more

effective and efficient wealth operations

Lower the efficiency ratio |

11

Financial Review |

12

Financial Highlights

1

st

Qtr

2012

4

th

Qtr

2011

3

rd

Qtr

2011

2

nd

Qtr

2011

1

st

Qtr

2011

Total Assets

($ in billions)

$1.84

$1.78

$1.76

$1.74

$1.71

Portfolio Loans & Leases

($ in billions)

$1.30

$1.29

$1.28

$1.25

$1.22

Total Deposits

($ in billions)

$1.43

$1.38

$1.35

$1.34

$1.32

Total Wealth Assets

($ in billions)

$5.15

$4.83

$4.50

$4.83

$3.60

Market Capitalization

($ in millions)

$297.4

$253.2

$215.0

$262.1

$257.9

Net Income

($ in millions)

$5.24

$5.17

$5.02

$4.81

$4.72 |

13

Financial Highlights -

continued

1

st

Qtr

2012

4

th

Qtr

2011

3

rd

Qtr

2011

2

nd

Qtr

2011

1

st

Qtr

2011

Diluted Earnings Per

Common Share

$0.40

$0.40

$0.39

$0.38

$0.38

Dividends Declared

$0.16

$0.15

$0.15

$0.15

$0.15

Book Value Per Share

$14.43

$14.09

$14.30

$14.17

$13.61

Tangible Book Value Per

Share

$11.25

$10.82

$11.11

$10.91

$11.65

Tangible Common Equity

Ratio

8.30%

8.27%

8.48%

8.31%

8.65%

Efficiency Ratio

64.7%

64.8%

64.1%

62.0%

62.8% |

14

4.03%

4.01%

3.90%

3.91%

3.93%

3.2%

3.4%

3.6%

3.8%

4.0%

4.2%

4.4%

Quarterly Net Interest Margin

On a tax-equivalent basis |

15

32%

34%

37%

37%

38%

10%

20%

30%

40%

50%

Quarterly Non-Interest Income

(As a % of Total Revenue) |

16

Capital Considerations

Maintain a “well capitalized”

capital position including a target tangible

common equity to tangible asset ratio of 8.00%

Selectively

add

capital

as

needed

to

maintain

capital

levels

and

fund

asset

growth and acquisitions. Place more emphasis on retained earnings.

Active Dividend Reinvestment and Stock Purchase Plan with Request for

Waiver program

The Corporation’s shareholders’

equity grew $5.4 million or 2.9% from

December 31, 2011 to March 31, 2012

Shelf Registration (Form S-3) of $150 million renewed on April 11, 2012

|

17

Capital Position -

Bryn Mawr Bank Corporation

3/31/2012

12/31/2011

3/31/2011

Tier I

11.63%

11.26%*

12.07%

Total (Tier II)

14.23%

13.83%*

14.52%

Tier I Leverage

9.16%

8.97%*

9.80%

Tangible Common

Equity

8.30%

8.27%

8.65%

*On 12/19/2011 the Corporation prepaid $12 million of junior subordinated

debt acquired during the First Keystone Bank acquisition which had a

rate of 9.7%. The prepayment reduced Tier I capital by $12 million with no

effect on the tangible common equity ratio. |

18

Return on Average Equity and Average Tangible

Equity (a Non-GAAP Measure*)

-----

Return on Average Tangible

Equity

-----

Return on Average Equity

*Tangible

equity

equals

equity

minus

goodwill

and

other

intangible

assets

** Annualized |

19

Return

on

Average

Equity

and

Average

Tangible

Equity

Excluding

Tax-Effected

Due

Diligence

and

Merger-Related

Expenses (a Non-GAAP Measure*)

*The returns on average tangible equity and average equity were calculated by

adding back to reported net income (a GAAP measure), the tax-effected

due diligence and merger-related expenses for the years referenced above. These non-GAAP ratios provide useful

supplemental information that is essential to understanding the Corporation’s

financial results. ** Annualized

----

Return on Average Tangible

Equity ----

Return on Average Equity |

20

Wealth Division Review |

21

Wealth Assets Under Management, Administration,

Supervision and Brokerage

($ in billions)

Excludes Community Bank’s assets in 2007

$2.28

$2.15

$2.87

$3.41

$4.83

$5.15

$1.5

$2.5

$3.5

$4.5

$5.5

2007

2008

2009

2010

2011

1st Qtr

2012 |

22

Wealth Management Fees

($ in millions)

*

2007

2008

2009

2010

2011

1st Quarter

2012

$13.5

$13.8

$14.2

$15.5

$21.7

$6.2

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0 |

23

Acquisition of Davidson Trust Company

Stock Purchase Agreement executed February 3, 2012

Closing

to

occur

after

all

regulatory

approvals,

expected

to

close

in

the

2

nd

Quarter

2012

Purchase price $10.5 Million in cash. Holdback 30% paid over 18 months

Expected to be accretive to earnings per share in the first 12 months, excluding

one time merger costs

Profile:

Approximately $1 Billion in assets under management and supervision

30 year history in market

80% Investment Management; 20% Fiduciary Trust

Long standing relationships

Significant cross selling opportunities |

24

Wealth Division Highlights

Traditional Trust Activities (Bryn Mawr, PA)

$2.4 billion in assets

Integrated solutions to protect and preserve wealth through estate planning,

retirement planning, investment management and custody services

Long standing client relationships

Private Wealth Management Group (Hershey, PA)

$1.1 billion in assets

Integrated solutions to protect and preserve wealth through estate planning,

retirement planning and investment management

Long standing client relationships –

70% more than 5 years |

25

Wealth Division Highlights -

continued

Bryn Mawr Asset Management (Bryn Mawr, PA)

$296 million in assets

Brokerage services, asset allocation, objective advice

“Lift Out”

strategy with other opportunities being continuously evaluated

BMTC of Delaware (Greenville, DE)

$726 million in assets

Provides

corporate

fiduciary

and

administrative

trustee

services

under

Delaware law and the full spectrum of tax advantaged strategies

Lau Associates (Greenville, DE)

$613 million in assets

Fee-only, independent multi-family office providing highly personalized

service and sophisticated financial planning |

26

Credit Review |

27

Portfolio Loan & Lease Growth

($ in millions)

* From

2010

forward,

includes

the

addition

of

the

First

Keystone

loan

portfolio.

$803

$900

$886

$1,197

$1,295

$1,304

$500

$700

$900

$1,100

$1,300

$1,500

2007

2008

2009

2010*

2011

1st Qtr 2012 |

28

Loan Composition at March 31, 2012

($ in millions)

Total loans and leases of $1.304 billion

Commercial Mortgages

(33%)

Commercial & Industrial

(21%)

Home Equity & Consumer

Loans (16%)

Residential Mortgages

(24%)

Construction

(4%)

Leases

(2%)

$431

$271

$216

$307

$51

$28 |

29

Quarterly Asset Quality Data

1

st

Qtr

2012

4

th

Qtr

2011

3

rd

Qtr

2011

2

nd

Qtr

2011

1

st

Qtr

2011

Non-Performing Loans as a % of

Portfolio Loans and Leases

1.73%

1.11%

1.11%

1.29%

0.88%

Allowance as a % of Portfolio

Loans and Leases

1.00%

0.98%

0.91%

0.90%

0.87%

Non-Performing Assets as a % of

Assets

1.25%

0.84%

0.88%

0.97%

0.77%

Annualized Net Charge-Offs as a

% of average quarterly loans and

leases

0.23%

-0.01%

0.49%

0.40%

0.30% |

30

Small Ticket National Leasing Business

Leases outstanding: $28 million at March 31, 2012

Average yield of 10.18%

Profitable in 2010 and 2011 as asset quality improved significantly

Projections are for 6.5% growth in 2012

Delinquency rate continues to improve:

0.68% at March 31, 2012

1.24% at December 31, 2011

2.05% at December 31, 2010 |

31

Summary

Outstanding franchise in a stable market

Focus on Wealth Services, Business Banking and Private Banking

Investing in growth opportunities today for anticipated earnings

growth tomorrow

Sound business strategy, strong asset quality, well capitalized

and solid risk management procedures serve as a foundation for

potential strategic expansion |

32

Thank You

Joseph Keefer, EVP

610-581-4869

jkeefer@bmtc.com

Duncan Smith, CFO

610-526 –2466

jdsmith@bmtc.com

Ted Peters, Chairman

610-581-4800

tpeters@bmtc.com

Frank Leto, EVP

610-581-4730

fleto@bmtc.com

Aaron Strenkoski, VP –

Investments & Shareholder Relations –

610-581-4822 –

astrenkoski@bmtc.com |

33

Safe Harbor

This presentation contains statements which, to the extent that they are not recitations of

historical fact may constitute forward-looking statements for purposes of the Securities Act

of 1933, as amended, and the Securities Exchange Act of 1934, as amended. Such

forward- looking statements may include financial and other projections as well as

statements regarding Bryn Mawr Bank Corporation’s (the “Corporation”) that may

include future plans, objectives, performance, revenues, growth, profits, operating expenses or

the Corporation’s underlying assumptions. The words “may”, “would”,

“should”, “could”, “will”, “likely”,

“possibly”, “expect,” “anticipate,” “intend”,

“estimate”, “target”, “potentially”, “probably”,

“outlook”, “predict”, “contemplate”, “continue”,

“plan”, “forecast”, “project” and “believe” or other

similar words, phrases or concepts may identify forward-looking statements. Persons reading

or present at this presentation are cautioned that such statements are only predictions, and

that the Corporation’s actual future results or performance may be materially different.

Such forward-looking statements involve known and unknown risks and uncertainties. A

number of factors, many of which are beyond the Corporation’s control, could cause our

actual results, events or developments, or industry results, to be materially different from any

future results, events or developments expressed, implied or anticipated by such forward-

looking statements, and so our business and financial condition and results of operations

could be materially and adversely affected. |

34

Safe Harbor (continued)

Such factors include, among others, our need for capital, our ability to control

operating costs and expenses, and to manage loan and lease delinquency

rates; the credit risks of lending activities and overall quality of the

composition of our loan, lease and securities portfolio; the impact of

economic conditions, consumer and business spending habits, and real estate market

conditions on

our

business

and

in

our

market

area;

changes

in

the

levels

of

general

interest

rates,

deposit

interest rates, or net interest margin and funding sources; changes in banking

regulations and policies and the possibility that any banking agency

approvals we might require for certain activities will not be obtained in a

timely manner or at all or will be conditioned in a manner that would impair

our ability to implement our business plans; changes in accounting policies and

practices; the inability of key third-party providers to perform their

obligations to us; our ability to attract and retain key personnel;

competition in our marketplace; war or terrorist activities; material

differences in the actual financial results, cost savings and revenue enhancements

associated with our acquisitions including our contemplated acquisition of

the Davidson Trust Company; and other factors as described in our securities

filings. All forward-looking statements and information made

herein

are

based

on

Management’s

current

beliefs

and

assumptions

as

of

April

26,

2012

and speak only as of that date. The Corporation does not undertake to update

forward-looking statements. |

35

Safe Harbor (continued)

For a complete discussion of the assumptions, risks and uncertainties related to our business, you

are encouraged to review our filings with the Securities and Exchange Commission, including our

most recent annual report on Form 10-K, as well as any changes in risk factors that we may

identify in our quarterly or other reports filed with the SEC. This presentation is for discussion purposes only, and shall not constitute any offer to sell

or the solicitation of an offer to buy any security, nor is it intended to give rise to any

legal relationship between the Corporation and you or any other person, nor is it a

recommendation to buy any securities or enter into any transaction with the Corporation. The information contained herein is preliminary and material changes to such information may be

made at any time. If any offer of securities is made, it shall be made pursuant to a definitive

offering memorandum or prospectus (“Offering Memorandum”) prepared by or on behalf of

the Corporation, which would contain material information not contained herein and which shall

supersede, amend and supplement this information in its entirety. Any decision to invest

in the Corporation’s securities should be made after reviewing an Offering Memorandum,

conducting such investigations as the investor deems necessary or appropriate, and consulting

the investor’s own legal, accounting, tax, and other advisors in order to make an

independent determination of the suitability and consequences of an investment in such

securities. |

36

Safe Harbor (continued)

No offer to purchase securities of the Corporation will be made or accepted prior to receipt by an

investor of an Offering Memorandum and relevant subscription documentation, all of which must

be reviewed together with the Corporation’s then-current financial statements and,

with respect to the subscription documentation, completed and returned to the Corporation in

its entirety. Unless purchasing in an offering of securities registered pursuant to the

Securities Act of 1933, as amended, all investors must be “accredited investors” as

defined in the securities laws of the United States before they can invest in the Corporation. |