Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Digital Locations, Inc. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - Digital Locations, Inc. | ex321.htm |

| EX-31.1 - EXHIBIT 31.1 - Digital Locations, Inc. | ex311.htm |

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

|

T

|

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011

|

||

|

o

|

TRANSITION REPORT UNDER SECTION13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

FOR THE TRANSITION PERIOD FROM __________ TO __________

|

COMMISSION FILE NUMBER: 333-144931

CARBON SCIENCES, INC.

(Name of registrant in its charter)

|

NEVADA

(State or other jurisdiction of incorporation or organization)

|

20-5451302

(I.R.S. Employer Identification No.)

|

5511C Ekwill Street, Santa Barbara, CA 93111

(Address of principal executive offices) (Zip Code)

Issuer’s telephone Number: (805) 456-7000

Securities registered under Section 12(b) of the Exchange Act: None.

Securities registered under Section 12(g) of the Exchange Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files. Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated Filer []

Non-accelerated filer [ ] (Do not check if a smaller reporting company) Smaller reporting company[x]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based upon the price at which the Company’s common stock was sold as reported on the OTC-Bulletin Board on June 30, 2011 was $22,862,798.

The number of shares of registrant’s common stock outstanding, as of March 30, 2012 was 9,893,138.

DOCUMENTS INCORPORATED BY REFERENCE

None.

1

TABLE OF CONTENTS

|

Page

|

|

|

PART I

|

|

|

Item 1. Business

|

3

|

|

Item 1A. Risk Factors

|

8

|

|

Item 2. Properties

|

15

|

|

Item 3. Legal Proceedings

|

15

|

|

Item 4. Mine Safety Disclosures

|

15

|

|

PART II

|

|

|

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

16

|

|

Item 6. Selected Financial Data

|

17

|

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

17

|

|

Item 8. Financial Statements and Supplementary Data

|

20

|

|

Item 9. Changes In and Disagreements with Accountants on Accounting and Financial Disclosure

|

20

|

|

Item 9A. Controls and Procedures

|

20

|

|

Item 9B. Other Information

|

20

|

|

PART III

|

|

|

Item 10. Directors, Executive Officers and Corporate Governance

|

21

|

|

Item 11. Executive Compensation

|

24

|

|

Item 12. Security Ownership of Certain Beneficial Owners and Management

|

|

|

and Related Stockholder Matters

|

26

|

|

Item 13. Certain Relationship and Related Transactions, and Director Independence

|

27

|

|

Item 14. Principal Accounting Fees and Services

|

27

|

|

Item 15. Exhibits, Financial Statement Schedules

|

28

|

|

SIGNATURES

|

30

|

2

PART I

ITEM 1. BUSINESS.

Unless otherwise stated or the context requires otherwise, references in this annual report on Form 10-K to “Carbon Sciences”, the “Company”, “we”, “us”, or “our” refer to Carbon Sciences, Inc.

Introduction

We are currently developing a technology to make transportation fuels and other valuable products from natural gas methane (CH4) and carbon dioxide (CO2). Our highly scalable, clean-tech process will enable the world to reduce its dependence on petroleum by transforming abundant and affordable natural gas into gasoline, diesel and jet fuel, and other products, such as hydrogen, methanol, ammonia, solvents, plastics and detergent alcohols. The key to this process is a breakthrough catalyst that can reduce the cost of reforming natural gas into synthetic gas (syngas), the most costly step in making products from natural gas.

Our goal is to help reduce the world’s dependence on petroleum by developing technology to enable the cost effective use of natural gas as a feedstock to produce clean and green liquid fuels for use in the existing transportation infrastructure.

We believe that natural gas is the world’s next primary source of fuel. While found in abundant supply at affordable prices in the U.S. and throughout the world, natural gas cannot be used directly in cars, trucks, trains and planes without a massive overhaul of the existing liquid fuels infrastructure. We intend to address this problem by developing an industrial clean-tech process to enable the transformation of natural gas into liquid transportation fuels such as gasoline, diesel, jet fuel and other valuable products. The key to our technology is a patented catalyst that reacts carbon dioxide (CO2) with natural gas methane (CH4) to produce a synthesis gas mixture of hydrogen and carbon monoxide (CO + H2), often referred to as syngas. This syngas can be fed into existing industrial scale gas-to-liquids (GTL) processes to produce liquid fuels.

We believe our competitive advantage over other natural gas reforming technologies is that our processes can significantly lower the cost of reforming natural gas into synthetic gas (syngas), the most costly step in the gas-to-liquids (GTL) process for making liquid transportation fuels from natural gas. As part of our business plan, we intend to demonstrate and prove this point. Based on original laboratory testing results and validated in commercial testing facilities, we believe that we have a very robust reforming catalyst to enable cost effective syngas production.

Our business model is to develop and license technologies related to our catalyst such as but not limited to methods of manufacturing, integration into existing syngas processes and new process designs. We do not intend to manufacture or sell catalyst, syngas or any final products in the market place. We will seek to license our intellectual property portfolio to catalyst manufacturers, as well as to energy, chemical and engineering firms throughout the world for the purposes of syngas and fuel production.

While natural gas is currently the largest source of methane for gas-to-liquids production, other renewable sources of methane such as landfill gas, algae biomass, flare gas, and livestock gas can be captured and used as the methane feedstock for our technology.

We were incorporated in the State of Nevada on August 25, 2006, as Zingerang, Inc. Our name was changed to Carbon Sciences, Inc on April 9, 2007. Our principal executive offices are located at 5511-C Ekwill Street, Santa Barbara, CA 93111, and our telephone number is (805)456-7000. Our fiscal year end is December 31.

Market Opportunity

In the International Energy Outlook 2010 report, the EIA predicts that worldwide energy consumption will increase by 49% from 2007 to 2035. This increase translates to a requirement of over 114 million barrels of crude oil per day in 2035, up from 86 million barrels per day in 2007. The EIA reports that the biggest use of crude oil, making up nearly 80% of the increase, is in the production of liquid fuels for the transportation sector.

3

The 2010 World Energy Outlook report published by the IEA stated that 2006 was the year that the world’s conventional oil production reached its peak of 70 million barrels per day.

In the World Energy Outlook 2011 report, the IEA postulates that the world is entering a “Golden Age of Gas.” Management believes that while the supply of world crude oil is declining, the global natural gas resource base is vast and widely dispersed geographically. The IEA estimates that conventional recoverable gas resources are equivalent to more than 120 years of current global consumption, while total recoverable resources could sustain today’s production for over 250 years.

The current global market for hydrogen exceeds $150 billion/year with methanol at more than $20 billion/year. Steam reforming of natural gas into syngas (CO+H2) is the most common way to make hydrogen and methanol. In fact, 95% of the hydrogen in the U.S. is produced by steam reforming. The 2,000 existing steam reforming plans in the world usually replace their catalysts every 3-5 years. Many of these catalyst replacements cost as much as $5-$10MM.

Carbon Sciences is developing one version of its proprietary catalyst to be a drop-in replacement for existing steam reforming catalyst. Our catalyst will benefit operators by delivering more output at a lower cost. This is accomplished by reducing the amount of steam required, which directly translates to lower energy costs, lower CO2 emissions, and higher profits from greater processing throughput.

We believe that we can apply our technology to natural gas resources to enable the production of non-petroleum liquid fuels to meet the world’s growing demand for use in cars, trucks, planes and ships. Additionally, because our technology consumes CO2, we believe we can help reduce the amount of CO2 emissions being released into the atmosphere, which we believe is harmful to the environment and may contributes to climate change.

Most of the world’s natural gas reserves contain some amount of CO2, which must be removed before the natural gas methane is marketable. If the CO2 content is high, then the removal process is prohibitively expensive, therefore leaving those natural gas reserves uneconomical to develop. Since our technology uses CO2 and methane as feedstocks, it can utilize high CO2 natural gas reserves directly. Natural gas containing as much as 50% CO2 by volume is suitable for our syngas technology. We believe this is a specific GTL market opportunity that existing technologies cannot address.

Gas to Liquids Overview

Many natural gas proponents are proposing the use of compressed natural gas (CNG) or liquefied natural gas (LNG) for use in new trucks and other vehicles. We believe this is a step in the right direction, but new engines mean new and expensive infrastructure. We believe a better solution is the direct transformation of natural gas into gasoline, diesel and jet fuel for use in existing engines and fuel delivery infrastructure.

We believe there are four main reasons why natural gas should be the new feedstock for liquid fuels:

|

·

|

Energy independence from petroleum;

|

|

·

|

Resulting liquid fuels can be used directly in the existing infrastructure;

|

|

·

|

Natural gas is abundant and affordable; and

|

|

·

|

Reduction of greenhouse gas emissions.

|

Current industrial scale gas-to-liquids (GTL) technology, invented by German chemists Franz Fischer and Hans Tropsch in the 1920’s, can convert a gas mixture of hydrogen (H2) and carbon monoxide (CO) into liquid fuels without using petroleum. However, H2 and CO do not exist naturally and must be manufactured synthetically. There are a number of ways to make this synthesis gas, or syngas, but the most promising and scalable approach is the reforming of natural gas, which is primarily methane (CH4).

4

There are four (4) known processes to reform natural gas (methane) into syngas:

|

·

|

Steam Reforming – Reacts steam with methane.

|

|

·

|

Partial Oxidation – Reacts pure oxygen with methane.

|

|

·

|

Autothermal Reforming – A combination of steam and partial oxidation reforming.

|

|

·

|

Dry Reforming – Reacts carbon dioxide with methane, without steam or oxygen.

|

To our knowledge, there are no commercial dry reforming syngas technologies available for GTL applications. In addition, none of the other natural gas reforming technologies can be utilized with natural gas fields that contain high CO2 contents.

Our Syngas Technology

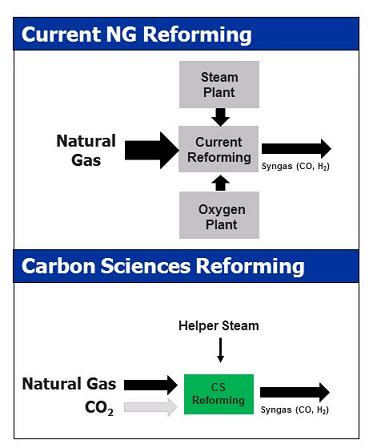

The following diagram illustrates how our processes compare to a conventional reforming system.

We are developing two versions of our breakthrough catalyst that can reduce the cost of reforming natural gas into synthetic gas (syngas), the most costly step in making products from natural gas.

|

I.

|

Dry Reforming. Another version of our catalyst can be used with captured CO2 or high CO2 content natural gas to make syngas.

|

We believe that with the help of a catalyst such as the one we are developing, a cost effective commercial grade dry reforming front end can be implemented, and will result in lower capital and operating costs when compared to other reforming processes for the following reasons: (i) does not use oxygen or steam, both of which require large co-production plants that consume large amounts of energy, (ii) is expected to require less capital because of reduced need for oxygen or steam plants, (iii) consumes CO2, an inexpensive product often already in natural gas reserves. We cannot predict whether the catalyst will be engineered as a drop-in catalyst for certain existing syngas plants or whether there may be a need to build new plants optimized to take advantage of our catalyst.

Current commercial dry reforming catalysts are made from rare noble metals, such as palladium and ruthenium, which are expensive and not suitable for mass-market applications, such as fuel production. To our knowledge, there are no commercial dry reforming technologies that are used in GTL applications. Based on our research, we believe that the reason for this is the lack of a low cost catalyst capable of running for a long period of time. We believe the catalyst we are developing will be an innovative catalyst which will address these issues.

Our currently patented catalyst has the following characteristics that we believe are not available from other known dry reforming catalysts:

|

·

|

Made from inexpensive, readily available metals, such as nickel and aluminum

|

|

·

|

High conversion efficiency of CO2 and CH4 into syngas

|

|

·

|

Minimum coking. Coking is the deposition of carbon on the catalyst surface that inhibits the catalyst activity and performance.

|

|

·

|

Over 1,000 hours of runtime. Long runtime eliminates the need for frequent and costly system shutdowns to reload the catalysts.

|

|

II.

|

Steam Reforming. One version of our catalyst can be used as a drop-in replacement for existing steam reforming catalyst to reduce the cost and increase the production of syngas, primarily for the production of hydrogen and methanol.

|

Steam reforming of natural gas to syngas is the primary method for making valuable, large volume products, such as hydrogen, methanol, ammonia, solvents, plastics and detergent alcohols. Our highest priority is developing a drop-in replacement catalyst to increase the output and lower the cost of steam reforming. Minimal equipment and plant changes will be needed by existing operators to use the steam reforming version of our catalyst.

5

Our patented catalyst is currently in a powdered form not yet suitable for industrial use. Our plan is to develop an industrial form of this catalyst, such as pellets, which may include adding new materials or designing new manufacturing methods. We are in the early research and development phase of this process. We intend to enter into discussions with catalyst manufacturers regarding possible co-development arrangements for developing the commercial catalyst. We expect to complete the commercial form of our catalyst by the end of 2012. By the end of 2013, we expect to complete the design of an industrial syngas production process optimized for our catalyst. After that we expect to build a demonstration system in 2014, either by ourselves or in conjunction with strategic partners. Once our commercial catalyst is proven in a demonstration system, we intend to aggressively expand our business development efforts and seek customers and strategic partners to license our technology.

Business Model

We are a technology development and licensing company. We do not intend to manufacture and market syngas or fuel as a final product. Instead, we will seek to license our intellectual property portfolio to catalyst manufacturers, as well as to major energy, chemical and engineering firms throughout the world for the purposes of syngas and fuel production.

For example, we will seek to license our catalyst technology to existing catalyst manufacturing companies who will be responsible for the manufacturing and sale of the physical catalysts. We may charge the manufacturer a royalty fee based on its catalyst sales. Likewise, we will seek to license or jointly develop various industrial syngas generation process designs based on our catalyst with engineering and construction firms. We may charge these firms a royalty fee based on their revenues received in the engineering and construction of syngas plants using our technology.

Marketing Strategy

We expect that our marketing strategy will include media and analyst communication, blogs, and selected trade show attendance. We intend to utilize appropriate opportunities to place our brand in general and industry specific publications, using press releases, white papers and authored articles and Internet publications.

Research and Development

We have hired technical personnel and have retained a number of scientific advisors and part-time technical contractors, to help us develop and commercialize our technology. We have purchased and developed research apparatus that enables us to refine our methodology and demonstrate our technology. Using computer-aided process engineering tools, we plan to develop a detailed computer simulation model that will allow us to demonstrate the commercial viability of our system.

In addition, we have entered into a consulting agreement with Emerging Fuels Technology or EFT based in Tulsa, OK to provide laboratory services to support the development of our process to convert CO2 and methane into syngas. EFT’s core competency is in the areas of Fischer-Tropsch and related synthesis and hydroprocessing chemistry. Pursuant to the agreement with EFT, we agreed to pay standard rates for time spent by EFT of $200 per hour for consulting services performed by their principals, and $50 per hour to $400 per day for laboratory services, and to reimburse EFT for the reasonable expenses incurred during the term of the agreement. The consulting agreement may be terminated at any time by either party by giving notice.

We have also entered into a consulting agreement with Dr. Howard Fong pursuant to which he is serving as our chief scientific advisor. The agreement with Dr. Fong provides for a monthly fee of $15,000. The consulting agreement runs through December 2012. However, we have an option to extend the term for an additional year through December 2013. See “Management –Key Consultants”

Government Regulation

We are a technology development and licensing company and do not intend to sell, manufacture or produce any products. We are currently not subject to any government regulations that have a material effect on our operations. Additionally, we are not aware of any pending legislation or regulations that would have a material effect on our operations.

6

Manufacturing and Distribution

As a technology licensing company, we do not intend on manufacturing and distributing any products as our primary business operation. However, we may build demonstration systems, either by ourselves or in conjunction with strategic partners.

Intellectual Property

We have filed numerous patent applications with the United States Patent and Trademark Office in the course of our business history.

On December 23, 2010, we entered in to a License Agreement with the University of Saskatchewan or UOS, pursuant to which we have an exclusive, worldwide, sub-licensable, royalty-bearing right and license to make, have made, use, offer for sale, sell, reproduce, distribute, incorporate into other technology, or otherwise exploit certain patent-pending technology and relevant improvements from UOS, for a high performance catalyst for the dry reforming of methane with carbon dioxide for the production of synthesis gas. This License Agreement commenced on December 23, 2010, and will continue until the expiration date of the last of the licensed patents. In consideration for the grant of the patents, we are required to pay license fee of $20,000 a year for the term of the license Agreement. In addition, we are obligated to pay UOS $50,000 upon the first application of a licensed product in a pilot-scale or commercial facility and $50,000 upon the first sale of a licensed product. We are also required to pay royalties ranging from 0.9% to 3.6% of the sales revenue from a customer that uses a tangible licensed product or system made by us. In the event that we sublicense the licensed patents, we shall pay UOS sublicense compensation ranging from 6.25% to 12.5% of the sublicense fees that we receive. Under the License Agreement, we are also required to maintain general liability insurance with policy limits of no less than $2,000,000 during the term of the License Agreement and products liability insurance coverage with policy limits of no less than $5,000,000 to protect against our activities in relation to the license agreement.

The License Agreement may be terminated upon the party’s mutual consent or upon the expiration of six months after notice of termination to the UOS. In addition, the License Agreement may be terminated upon the occurrence of an event of default under the agreement.

The patent subject to the license agreement was issued by the PTO on July 26, 2011 as patent No.7,985,710.

We intend to continue our research and development efforts in dry reforming. Based on the UOS catalyst and new developments in the course of our business, we intend to file additional applications and build a global patent portfolio related to methods of catalyst preparation, commercial form of the catalyst, application of the catalyst, process design and optimizations. Until patent protection is granted, we must rely on trade secret protection, which requires reasonable steps to preserve secrecy. Therefore, we require that our personnel, contractors and sublicensees not disclose the trade secrets and confidential information pertaining to the technology. In addition, trade secret protection does not provide any barrier to a third party “reverse engineering” fuel made with the technology, to the extent that the technology is readily ascertainable by proper means. Neither the patent, if it issues, nor trade secret protection will preclude third parties from asserting that the technology, or the products we or our sub-licensees commercialize using the technology, infringes upon their proprietary rights.

Competition

The market for liquid fuel is large, as is the number of competitors providing technology to the fuel industry. For example, companies that offer fuel production technologies include UOP LLC (A Honeywell Company), Chevron Corp, Royal Dutch Shell plc, BP plc, and ExxonMobil Corp.

We do not compete directly with other firms in the production of fuel from natural gas. Instead, we compete with technology firms that offer natural gas reforming technologies such as steam reforming, partial oxidation and autothermal. We are not aware of any commercially available dry reforming technology for GTL applications. There can be no assurance that companies are not currently developing or will develop technology similar to the one we are developing. There are, however, commercial dry reforming catalysts made from rare earth metals, but they are not used for GTL applications.

We believe our main competitive advantage over the current natural gas proponents is the cost of adapting equipment to use natural gas. Since the vast majority of trucks and vehicles are designed for consumption of petroleum-based fuels, many natural gas proponents often experience a second cost disadvantage – the expense of adopting new engines for these vehicles. We believe the ability of our technology to transform natural gas directly to gasoline, diesel and jet fuel for use in existing engines and fuel delivery infrastructure improves our ability to compete with the current natural gas proponents.

7

Technology Development Partners

We have entered into an agreement with Emerging Fuels Technology based in Tulsa, OK to provide laboratory and consulting services to support the development of our dry reforming technology. We may enter into technology development partnerships with other companies.

Employees

As of March 30, 2012 we had 3 full-time employees. We have not experienced any work stoppages and we consider relations with our employees to be good. We have used an outsourced work-for-hire development model to date. We intend to increase our internal research and development staffing with the proceeds of this offering.

We are in the early stages of development and have limited operating history which you can base an investment decision.

We were formed in August 2006 and are currently developing a new technology that is still being developed for commercial use. We have generated no revenues, have no real operating history upon which you can evaluate our business strategy or future prospects, and have negative working capital. As a result, our auditor issued an opinion in connection with our December 31, 2010 financial statements, which expressed substantial doubt about our ability to continue as a going concern unless we obtain additional financing. While this offering addresses such concern and is expected to see us through until we begin to generate revenues, our ability to generate such revenues will depend on whether we can successfully develop, commercialize and license our technology and make the transition from a development stage company to an operating company. We expect to continue to incur losses until approximately 2015 when we estimate we may begin to generate revenues. In making your evaluation of our prospects, you should consider that we are a start-up business focused on a new technology, are designing solutions that have no proven market acceptance, and operate in a rapidly evolving industry. As a result, we may encounter many expenses, delays, problems and difficulties that we have not anticipated and for which we have not planned. There can be no assurance that at this time we will successfully commercialize our technology, operate profitably or that we will have adequate working capital to fund our operations or meet our obligations as they become due.

Our proposed operations are subject to all of the risks inherent in the initial expenses, challenges, complications and delays frequently encountered in connection with the formation of any new business. Investors should evaluate an investment in our company in light of the problems and uncertainties frequently encountered by companies attempting to develop markets for new products, services and technologies. Despite best efforts, we may never overcome these obstacles to achieve financial success. Our business is speculative and dependent upon the implementation of our business plan, as well as our ability to successfully complete the development of our technology or enter into licensing agreements with third parties on terms that will be commercially viable for us. There can be no assurance that our efforts will be successful or result in revenue or profit. There is no assurance that we will earn significant revenues or that our investors will not lose their entire investment.

If we are unable to effectively manage the transition from a development stage company to an operating company, our financial results will be negatively affected.

For the period from our inception, August 25, 2006, through December 31, 2011, we incurred an aggregate net loss, and had an accumulated deficit, of $7,678,672. For the years ended December 31, 2011 and 2010, we incurred net losses of $1,861,490 and $2,302,583. Our losses are expected to continue to increase for at least the next 48 months as we commence full scale development of our technology. We believe we will require at least the net proceeds of this offering to make this transition and do not expect to transition from a development stage company to an operating company until 2015. As we do make such transition, we expect our business to grow significantly in size and complexity. This growth is expected to place significant additional demands on our management, systems, internal controls and financial and operational resources. As a result, we will need to expend additional funds to hire additional qualified personnel, retain professionals to assist in developing appropriate control systems and expand our operating infrastructures. Our inability to secure additional resources, as and when needed, or manage our growth effectively, if and when it occurs, would significantly hinder our transition to an operating company, as well as diminish our prospects of generating revenues and, ultimately, achieving profitability.

8

Sufficient customer acceptance for our technology may never develop or may take longer to develop than we anticipate, and as a result, our revenues and profits, if any, may be insufficient to fund our operations.

Sufficient markets may never develop for our technology, may develop more slowly than we anticipate or may develop with economics that are not favorable for us. The development of sufficient markets for our technology at favorable pricing may be affected by cost competitiveness of our technology, customer reluctance to try new technology and emergence of more competitive technologies. Because out technology has not yet been used to manufacture syngas or liquid fuels, potential customers may be skeptical about product stability, supply availability, quality control and our financial viability, which may prevent them from purchasing our technology or entering into long-term licensing agreements with us. We cannot estimate or predict whether a market for our technology will develop, whether sufficient demand for our technology will materialize at favorable prices, or whether satisfactory profit margins will be achieved. If such pricing levels are not achieved or sustained, or if our technologies and business approach to our markets do not achieve or sustain broad acceptance, our business, operating results and financial condition will be materially and adversely impacted.

The ability of our catalyst technology to be utilized on a commercially sustainable basis is unproven, and until we can develop and prove our technology, we likely will not be able to generate or sustain sufficient revenues to continue operating our business.

While producing syngas is not a new technology, our dry reforming catalyst is not currently suitable for commercial use and has never been utilized on a commercially sustainable basis. The tests that we have conducted to date with respect to our technology have been performed in a limited scale environment, and the same or similar results may not be obtainable at competitive costs on a large-scale commercial basis. While industrial processes exist to convert syngas into liquid fuels, we have not conducted end-to-end tests on the ability of our technology to produce liquid gas.

We have never utilized our technology under the conditions or in the volumes that will be required for us to be profitable and cannot predict all of the difficulties that may arise. Our technology requires further research, development, regulatory approvals, environmental permits, design and testing prior to commercialization. Accordingly, our technology may not perform successfully on a commercial basis and may never generate any meaningful revenues or profits.

We likely will not be able to generate significant revenues until we can successfully validate the performance of our technology with customers.

To date, we have generated no revenues. Revenue generation could be impacted by any of the following:

|

•

|

delays in demonstrating the technological advantages or commercial viability of our proposed technology;

|

|

|

•

|

delays in developing our technology; and

|

|

|

•

|

inability to interest early adopter customers in our technology.

|

We may not be able to enter into agreements to license our technology at prices that will cover our costs. Potential customers may require lengthy or complex trials or long sampling periods before committing to license our technology.

The current credit and financial market conditions may exacerbate certain risks affecting our business.

Due to the continued disruption in the financial markets arising from the global recession and the slow pace of economic recovery, many of our potential customers are unable to access capital necessary to accommodate the use of our technology. Many are operating under austerity budgets that limit their ability to invest in infrastructure necessary to use alternative fuels and that make it significantly more difficult to take risks with new fuel sources. As a result, we may experience increased difficulties in convincing customers to adopt our technology as a viable alternative at this time.

We may not be able to generate revenues from licensing our technology.

Our business plan includes, as our main revenue stream, the collection of royalties through licensing our technology intellectual property portfolio that we currently have and will build in the course of our business. Companies to which we grant licenses may not be able to produce, market and sell enough products to pay us royalty fees or they may default on the payment of royalties. We may not be able to achieve profitable operations from collecting royalties from the licensing of our proprietary technology.

9

We do not maintain theft or casualty insurance, and only maintain modest liability and property insurance coverage and therefore we could incur losses as a result of an uninsured loss.

We cannot assure that we will not incur uninsured liabilities and losses as a result of the conduct of our business. Any such uninsured or insured loss or liability could have a material adverse effect on our results of operations.

If we lose key employees and consultants or are unable to attract or retain qualified personnel, our business could suffer.

Our success is highly dependent on our ability to attract and retain qualified scientific, engineering and management personnel. Competition for these qualified personnel is intense. We are highly dependent on our management, including Mr. Byron Elton, who has been critical to the development of our business. The loss of the services of Mr. Elton could have a material adverse effect on our operations. We do not have an employment agreement with Mr. Elton. Accordingly, there can be no assurance that he will remain associated with us. His efforts will be critical to us as we continue to develop our technology and as we attempt to transition from a development stage company to a company with commercialized products and services. If we were to lose Mr. Elton or any other key employees or consultants, we may experience difficulties in competing effectively, developing our technology and implementing our business strategies.

The strategic relationships upon which we may rely are subject to change.

Our ability to successfully test our technology and identify and enter into commercial arrangements with licensees will depend on developing and maintaining close working relationships with industry participants. These relationships will need to change and evolve over time, as we enter different phases of development. Our strategic relationships most often are not yet reflected in definitive agreements, or the agreements we have do not cover all aspects of the relationship. Our success in this area also will depend on our ability to select and evaluate new strategic relationships and to consummate transactions. To test our technology, we will be dependent on strategic partners for the use or construction of demonstration systems. Our inability to identify suitable companies or enter into and maintain strategic relationships may affect our ability to commercialize our technology and impair our ability to grow. The terms of relationships with strategic partners may require us to incur expenses or undertake activities we would not otherwise be inclined to incur or undertake in order to maintain these relationships.

Failure to obtain the patents for our applications could prevent us from securing royalty payments in the future, if appropriate.

In addition to our license to the patented UOS catalyst, we intend to file new patent applications and build a global patent portfolio related to the methods of catalyst preparation, commercial form of the catalyst, application of the catalyst, process design and optimizations, in the normal course of our business. We cannot be certain that patents will be granted nor can we be certain that other companies will not file for patent protection for the similar technology before us. Even if we are granted patent protection for our technology, there is no assurance that we will be in a position to enforce our patent rights. Failure to be granted patent protection for our technology could result in greater competition or in limited royalty payments. This could result in inadequate revenue and cause us to cease operations.

We may never fully realize the value of our technology license agreement, which presently is the principal asset reflected on our balance sheet.

We may not be successful in realizing the expected benefits from our Exclusive License Agreement with the UOS. We intend to incorporate the licensed technology in our development of a high performance catalyst for the dry reforming of methane with carbon dioxide for the production of synthesis gas. To date, we have incurred approximately $915,867 in research and development costs separate from our license payments, and we are continuing to incur additional research and development costs to commercialize the catalyst and optimize the process.

If we do not obtain protection for our intellectual property rights, our competitors may be able to take advantage of our research and development efforts to develop competing technology.

Our success, competitive position and future revenues will depend in part on our ability to obtain and maintain patent protection for our methods, processes and other technologies, to preserve our trade secrets, to prevent third parties from infringing on our proprietary rights and to operate without infringing the proprietary rights of third parties.

10

We have yet to complete an infringement analysis and, even if such an analysis were available at the current time, we could not be certain that no infringement exists, particularly as our products have not yet been fully developed. We may need to acquire additional licenses from third parties in order to avoid infringement claims, and any required licenses may not be available to us on acceptable terms, or at all. To the extent infringement claims are made, we could incur substantial costs in the resulting litigation, and the existence of this type of litigation could impede the development of our business.

We anticipate filing patent applications both in the U.S. and in other countries, as appropriate. However, the patent process is subject to numerous risks and uncertainties, and there can be no assurance that we will be successful in protecting our technology by obtaining and defending patents. These risks and uncertainties include but are not limited to the following:

|

·

|

Patents that may be issued or licensed may be challenged, invalidated, or circumvented, or otherwise may not provide any competitive advantage.

|

|

·

|

Our competitors, many of which have substantially greater resources than us and many of which have made significant investments in competing technologies, may seek, or may already have obtained, patents that will limit, interfere with, or eliminate our ability to make, use, and sell our potential products either in the United States or in international markets.

|

|

·

|

Countries other than the United States may have less restrictive patent laws than those upheld by United States courts, allowing foreign competitors the ability to exploit these laws to create, develop, and market competing products.

|

In addition to patents, we also intend to rely on trade secrets and proprietary know-how. Although we take measures to protect this information by entering into confidentiality and inventions agreements with our employees, scientific advisors, consultants, and collaborators, we cannot provide any assurances that these agreements will not be breached, that we will be able to protect ourselves from the harmful effects of disclosure if they are breached, or that our trade secrets will not otherwise become known or be independently discovered by competitors. If any of these events occurs, or we otherwise lose protection for our trade secrets or proprietary know-how, the value of this information may be greatly reduced.

Patent protection and other intellectual property protection are important to the success of our business and prospects, and there is a substantial risk that such protections will prove inadequate.

Intellectual property disputes could require us to spend time and money to address such disputes and could limit our intellectual property rights.

We may become subject to infringement claims or litigation arising out of patents and pending applications of competitors, or additional proceedings initiated by third parties or the United States Patent and Trademark Office, or PTO, to reexamine the patentability of our licensed patents. The defense and prosecution of intellectual property suits, PTO proceedings, and related legal and administrative proceedings are costly and time-consuming to pursue, and their outcome is uncertain. Litigation may be necessary to enforce our intellectual property rights, to protect our trade secrets and know-how, or to determine the enforceability, scope, and validity of the proprietary rights of others. An adverse determination in litigation or PTO proceedings to which we may become a party could subject us to significant liabilities, require us to obtain licenses from third parties, restrict or prevent us from selling our technology in certain markets, or invalidate or render unenforceable our licensed or owned patents. Although patent and intellectual property disputes might be settled through licensing or similar arrangements, the costs associated with such arrangements may be substantial and could include our paying large fixed payments and ongoing royalties. Furthermore, the necessary licenses may not be available on satisfactory terms or at all.

If we infringe the rights of third parties we could be prevented from licensing our technologies and forced to pay damages, and defend against litigation.

If our methods, processes and other technologies infringe the proprietary rights of other parties, we could incur substantial costs and we may have to do one or more of the following:

|

·

|

obtain licenses, which may not be available on commercially reasonable terms, if at all;

|

|

·

|

redesign our processes to avoid infringement;

|

|

·

|

stop using the subject matter claimed in the patents held by others;

|

|

·

|

pay damages; or

|

|

·

|

defend litigation or administrative proceedings, which may be costly whether we win or lose, and which could result in a substantial diversion of our financial and management resources.

|

11

Any of these events could substantially harm our financial condition and operations.

Our technology may become ineffective or obsolete.

To be competitive in the industry, we may be required to continually enhance and update our technology. The costs of doing so may be substantial, and if we are unable to maintain the efficacy of our technology, our ability to compete may be impaired. In addition, interest in our technology may wane as alternative fuels and other energy sources gain market acceptance. If competitors develop, obtain or license technology that is superior to ours, we may lose our competitive edge which may have a material adverse effect on our business, financial condition, results of operations and prospects.

Competition resulting from advances in alternative fuels may reduce the demand for our technology.

Alternative fuels and other energy sources are continually under development. A wide array of entities, including automotive, industrial and power generation manufacturers, the federal government, academic institutions and small private concerns are seeking to develop alternative clean-power systems. These technologies include using fuel cells or clean-burning gaseous fuels that, like biodiesel, may address increasing worldwide energy costs, the long-term availability of petroleum reserves and environmental concerns. Additionally, there is significant research and development being undertaken regarding the production of ethanol from cellulosic biomass, the production of methane from anaerobic digestors, and the production of electricity from wind and tidal energy systems, among other potential sources of renewable energy. If these alternative fuels continue to expand and gain broad acceptance, there may not be sufficient interest in our technology.

If we breach or default under our license agreement with the UOS, the licensor will have the right to terminate the license agreement, which termination may materially harm our business.

The success of our business will depend in part on the maintenance of our license agreement with UOS. Pursuant to the terms of the license agreement, we are required to pay UOS an additional $20,000 in cash per year until the expiration date of the last of the licensed patents. In addition, we are required to pay an aggregate of $100,000 if we hit certain commercialization milestones. The license agreement also provides that UOS may terminate the agreement if we file an assignment in bankruptcy or apply for reorganization or other similar proceedings. To the extent we default on any of the required payments or breach any other material provisions of the license agreement, UOS could terminate the agreement and pursue any remedy available to it in law or in equity, in which event we would lose our rights to commercialize our technology covered by the license, which loss may materially harm our business.

Our current and potential competitors, some of whom have greater resources than we do, may develop products and technologies that may cause demand for, and the prices of, our products to decline.

While we are not aware of any direct competitors offering commercial dry reforming technology to produce liquid fuels from natural gas, our potential customers may choose to buy or build their own systems instead of licensing our technology. Furthermore, our competitors may combine with each other, and other companies may enter our markets by acquiring or entering into strategic relationships with our competitors. Current and potential competitors have established, or may establish, cooperative relationships among themselves or with third parties to increase the abilities of their products to address the needs of our prospective customers.

Many of our current and potential competitors have longer operating histories, significantly greater financial, technical, product development and marketing resources, greater name recognition and larger customer bases than we do. Our present or future competitors may be able to develop technology comparable or superior to those we offer, adapt more quickly than we do to new technologies, evolving industry trends and standards or customer requirements, or devote greater resources to the development, promotion and sale of their technology than we do. Accordingly, we may not be able to compete effectively in our markets, competition may intensify and future competition may harm our business.

12

RISKS RELATING TO OUR COMMON STOCK

Our common stock is subject to volatility.

There can be no assurance that the market price for our common stock will remain at its current level and a decrease in the market price could result in substantial losses for investors. The market price of our common stock may be significantly affected by one or more of the following factors:

|

·

|

announcements or press releases relating to the industry or to our own business or prospects;

|

|

|

·

|

regulatory, legislative, or other developments affecting us or the industry generally;

|

|

|

·

|

sales by holders of restricted securities pursuant to effective registration statements or exemptions from registration; and

|

|

|

·

|

market conditions specific to biopharmaceutical companies, the healthcare industry and the stock market generally.

|

If our common stock remains subject to the SEC’s penny stock rules, broker-dealers may experience difficulty in completing customer transactions and trading activity in our securities may be adversely affected.

Unless our common stock is listed on a national securities exchange, including the Nasdaq Capital Market or we have stockholders’ equity of $5,000,000 or less and our common stock has a market price per share of less than $4.00, transactions in our common stock will be subject to the SEC’s “penny stock” rules. If our common stock remains subject to the “penny stock” rules promulgated under the Securities Exchange Act of 1934, broker-dealers may find it difficult to effectuate customer transactions and trading activity in our securities may be adversely affected.

In accordance with these rules, broker-dealers participating in transactions in low-priced securities must first deliver a risk disclosure document that describes the risks associated with such stocks, the broker-dealer's duties in selling the stock, the customer's rights and remedies and certain market and other information. Furthermore, the broker-dealer must make a suitability determination approving the customer for low-priced stock transactions based on the customer's financial situation, investment experience and objectives. Broker-dealers must also disclose these restrictions in writing to the customer, obtain specific written consent from the customer, and provide monthly account statements to the customer. The effect of these restrictions will probably decrease the willingness of broker-dealers to make a market in our common stock, decrease liquidity of our common stock and increase transaction costs for sales and purchases of our common stock as compared to other securities. Our management is aware of the abuses that have occurred historically in the penny stock market.

As a result, if our common stock becomes subject to the penny stock rules, the market price of our securities may be depressed, and you may find it more difficult to sell our securities.

If we fail to maintain effective internal controls over financial reporting, the price of our common stock may be adversely affected.

Our internal control over financial reporting may have weaknesses and conditions that could require correction or remediation, the disclosure of which may have an adverse impact on the price of our common stock. We are required to establish and maintain appropriate internal controls over financial reporting. Failure to establish those controls, or any failure of those controls once established, could adversely affect our public disclosures regarding our business, prospects, financial condition or results of operations.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require an annual assessment of internal controls over financial reporting, and for certain issuers an attestation of this assessment by the issuer’s independent registered public accounting firm. The standards that must be met for management to assess the internal controls over financial reporting as effective are evolving and complex, and require significant documentation, testing, and possible remediation to meet the detailed standards. We expect to incur significant expenses and to devote resources to Section 404 compliance on an ongoing basis. It is difficult for us to predict how long it will take or costly it will be to complete the assessment of the effectiveness of our internal control over financial reporting for each year and to remediate any deficiencies in our internal control over financial reporting. As a result, we may not be able to complete the assessment and remediation process on a timely basis. In addition, management’s assessment of internal controls over financial reporting may identify weaknesses and conditions that need to be addressed in our internal controls over financial reporting or other matters that may raise concerns for investors. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting or disclosure of management’s assessment of our internal controls over financial reporting may have an adverse impact on the price of our common stock.

13

We are authorized to issue "blank check" preferred stock without stockholder approval, which could adversely impact the rights of holders of our common stock.

Our Articles of Incorporation authorize our Company to issue up to 20,000,000 shares of blank check preferred stock. Currently no preferred shares are issued; however, we can issue shares of our preferred stock in one or more series and can set the terms of the preferred stock without seeking any further approval from our common stockholders. Any preferred stock that we issue may rank ahead of our common stock in terms of dividend priority or liquidation premiums and may have greater voting rights than our common stock. In addition, such preferred stock may contain provisions allowing those shares to be converted into shares of common stock, which could dilute the value of common stock to current stockholders and could adversely affect the market price, if any, of our common stock. In addition, the preferred stock could be utilized, under certain circumstances, as a method of discouraging, delaying or preventing a change in control of the Company. Although we have no present intention to issue any shares of authorized preferred stock, there can be no assurance that we will not do so in the future.

Shares eligible for future sale may adversely affect the market.

From time to time, certain of our stockholders may be eligible to sell all or some of their shares of common stock by means of ordinary brokerage transactions in the open market pursuant to Rule 144 promulgated under the Securities Act, subject to certain limitations. In general, pursuant to amended Rule 144, non-affiliate stockholders may sell freely after six months subject only to the current public information requirement. Affiliates may sell after six months subject to the Rule 144 volume, manner of sale (for equity securities), current public information and notice requirements. Of the approximately 9,594,567 shares of our common stock outstanding as of December 31, 2011, approximately 2,221,568 shares are freely tradable without restriction, as of December 31, 2011. Any substantial sales of our common stock pursuant to Rule 144 may have a material adverse effect on the market price of our common stock.

We do not expect to pay dividends in the future and any return on investment may be limited to the value of our common stock.

We do not currently anticipate paying cash dividends in the foreseeable future. The payment of dividends on our common stock will depend on earnings, financial condition and other business and economic factors affecting it at such time as the board of directors may consider relevant. Our current intention is to apply net earnings, if any, in the foreseeable future to increasing our capital base and development and marketing efforts. There can be no assurance that we will ever have sufficient earnings to declare and pay dividends to the holders of our common stock, and in any event, a decision to declare and pay dividends is at the sole discretion of the our Board of Directors. If we do not pay dividends, our common stock may be less valuable because a return on your investment will only occur if its stock price appreciates.

Our management will have broad discretion over the use of the net proceeds from this offering and we may use the net proceeds in ways with which you disagree.

We currently intend to use the net proceeds from this offering for general corporate purposes and working capital. We have not allocated specific amounts of the net proceeds from this offering for any of the foregoing purposes. Accordingly, our management will have significant discretion and flexibility in applying the net proceeds of this offering. You will be relying on the judgment of our management with regard to the use of these net proceeds, and you will not have the opportunity, as part of your investment decision, to assess whether the proceeds are being used appropriately. It is possible that the net proceeds will be invested in a way that does not yield a favorable, or any, return for us or our stockholders. The failure of our management to use such funds effectively could have a material adverse effect on our business, prospects, financial condition, and results of operation.

We are controlled by our current officers, directors and principal stockholders.

Our directors, executive officers and principal stockholders and their affiliates beneficially own approximately 8.24% of outstanding shares of common stock. Accordingly, our executive officers, directors, principal stockholders and certain of their affiliates will have the ability to control matters requiring shareholder approval, including the election of our Board of Directors and approval of significant corporate transactions, such as merger or other sale of our company or assets. Thus, actions might be taken even if other stockholders, including those who purchase shares in this offering, oppose them. This concentration of ownership might also have the effect of delaying or preventing a change of control of our company, which could cause our stock price to decline.

14

Our principal office is located at 5511C Ekwill Street, Santa Barbara, California 93111. We lease approximately 2,800 square feet. Our lease provides for a monthly base rent of $2,800 per month through September 30, 2011. Commencing October 1, 2011, our monthly base rent increased to $2,884 and shall increase annually thereafter by 3%. The current term of the lease expires September 30, 2012.

ITEM 3. LEGAL PROCEEDINGS.

We are not currently a party to, nor is any of our property currently the subject of, any pending legal proceeding that will have a material adverse effect on our business.

ITEM 4. MINE SAFETY DISCLOSURES

N/A

15

PART II

ITEM 5. MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Our common stock has been quoted on the OTC Bulletin Board under the symbol “CABN” since September 28, 2007. The following table provides, for the periods indicated, the range of high and low bid prices for our common stock. These over-the-counter market quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission, and may not represent actual transactions. Where applicable, the prices set forth below give retroactive effect to our one-for-forty reverse stock split which was effected on May 9, 2011.

|

Fiscal Year 2009

|

High

|

Low

|

||||||

|

First Quarter

|

$

|

13.60

|

$

|

5.60

|

||||

|

Second Quarter

|

12.80

|

8.00

|

||||||

|

Third Quarter

|

9.20

|

2.36

|

||||||

|

Fourth Quarter

|

7.80

|

3.60

|

||||||

|

Fiscal Year 2010

|

High

|

Low

|

||||||

|

First Quarter

|

$

|

6.16

|

$

|

3.28

|

||||

|

Second Quarter

|

4.60

|

2.00

|

||||||

|

Third Quarter

|

4.40

|

2.84

|

||||||

|

Fourth Quarter

|

3.80

|

1.84

|

||||||

|

Fiscal Year 2011

|

High

|

Low

|

||||||

|

First Quarter

|

$

|

3.60

|

$

|

2.40

|

||||

|

Second Quarter

|

6.50

|

2.40

|

||||||

|

Third Quarter

|

6.30

|

2.12

|

||||||

|

Fourth Quarter

|

3.35

|

1.40

|

||||||

On March 30, 2012 there were 106 holders of record of our common stock. This number does not include stockholders for whom shares were held in “nominee” or “street” name.

Dividend Policy

We have not declared or paid any cash dividends on our common stock and do not anticipate declaring or paying any cash dividends in the foreseeable future. We currently expect to retain future earnings, if any, for the development of our business.

Common Stock

Our Articles of Incorporation, as amended, authorize the issuance of 100,000,000 shares of common stock, $.001 par value per share. Holders of shares of common stock are entitled to one vote for each share on all matters to be voted on by the stockholders. Holders of common stock have cumulative voting rights. Holders of shares of common stock are entitled to share ratably in dividends, if any, as may be declared, from time to time by the Board of Directors in its discretion, from funds legally available therefor. In the event of a liquidation, dissolution, or winding up of our company, the holders of shares of common stock are entitled to share pro rata all assets remaining after payment in full of all liabilities. Holders of common stock have no preemptive or other subscription rights, and there are no conversion rights or redemption or sinking fund provisions with respect to such shares.

As of March 30, 2012, our common stock was held by 106 stockholders of record and we had 9,893,138 shares of common stock issued and outstanding. We believe that the number of beneficial owners is substantially greater than the number of record holders because a significant portion of our outstanding common stock is held of record in broker street names for the benefit of individual investors. The transfer agent of our common stock is Computershare Investor Services, 250 Royall Street Canton, MA 02021.

16

Equity Compensation Plan Information

The following table shows information with respect to each equity compensation plan under which our common stock is authorized for issuance as from inception (April 24, 2006) through December 31, 2011.

EQUITY COMPENSATION PLAN INFORMATION

|

Plan category

|

Number of securities

to be issued upon

exercise of

outstanding options,

warrants and rights

|

Weighted average

exercise price of

outstanding options,

warrants and rights

|

Number of securities

remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)

|

||||||

|

(a)

|

(b)

|

(c)

|

|||||||

|

Equity compensation plans approved by security holders

|

-0-

|

-0-

|

2,000,000

|

||||||

|

Equity compensation plans not approved by security holders

|

-0-

|

-0-

|

-0-

|

||||||

|

Total

|

-0-

|

-0-

|

2,000,000

|

||||||

Recent Sales of Unregistered Securities

None.

Issuer Purchases of Equity Securities

None.

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OR FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

The following discussion and analysis should be read together with our financial statements and the related notes appearing elsewhere in this filing. This discussion contains forward-looking statements reflecting our current expectations that involve risks and uncertainties. See “Forward-Looking Statements” for a discussion of the uncertainties, risks and assumptions associated with these statements. Actual results and the timing of events could differ materially from those discussed in our forward-looking statements as a result of many factors, including those set forth under “Risk Factors” and elsewhere in this prospectus.

17

Our Company

Innovating at the forefront of chemical engineering, Carbon Sciences is developing a breakthrough technology to make cleaner and greener transportation fuels and other valuable, large volume products from natural gas. Our highly scalable, clean-tech process will enable the world to reduce its dependence on petroleum by transforming abundant and affordable natural gas into gasoline, diesel and jet fuel, and other products, such as hydrogen, methanol, ammonia, solvents, plastics and detergent alcohols. The key to this process is a breakthrough catalyst that can reduce the cost of reforming natural gas into synthetic gas (syngas), the most costly step in making products from natural gas.

Our goal is to help reduce the world’s dependence on petroleum by developing technology to enable the cost effective use of natural gas as a feedstock to produce clean and green liquid fuels for use in the existing transportation infrastructure.

We believe that natural gas is the world’s next primary source of fuel. While found in abundant supply at affordable prices in the U.S. and throughout the world, natural gas cannot be used directly in cars, trucks, trains and planes without a massive overhaul of the existing liquid fuels infrastructure. We intend to address this problem by developing an industrial clean-tech process to enable the transformation of natural gas into liquid transportation fuels such as gasoline, diesel, jet fuel and other valuable products. Our competitive advantage over other natural gas reforming technologies is that our processes can significantly lower the cost of reforming natural gas into synthetic gas (syngas), the most costly step in the gas-to-liquids (GTL) process for making liquid transportation fuels from natural gas. As part of our business plan, we intend to demonstrate and prove this point. Based on original laboratory testing results and validated in commercial testing facilities, we believe that we have a very robust reforming catalyst to enable cost effective syngas production.

We have not yet generated revenues. We currently have negative working capital and, in connection with our December 31, 2010 financial statements, we received an opinion from our auditors that expressed substantial doubt about our ability to continue as a going concern without additional financing. Subsequent to December 31, 2010, we obtained $1,482,000 in private placements. We believe that the financings received by us after December 31, 2010 and the net proceeds of this offering will fully address such concern and enable us to complete development of our catalyst and commercially deploy our technology, and implement our business plan through such time as revenues support our operations. If additional funds are required because our plans, expectations or assumptions change, we may also seek funding through additional equity or debt financing. There can be no assurance that such financing will be available or upon such terms that are acceptable to us, if at all.

Critical Accounting Policies

Our discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America or GAAP. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosures of contingent assets and liabilities. On an ongoing basis, we evaluate our estimates, including those related to impairment of property, plant and equipment, intangible assets, deferred tax assets and fair value computation using the Black Scholes option pricing model. We base our estimates on historical experience and on various other assumptions, such as the trading value of our common stock and estimated future undiscounted cash flows, that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions; however, we believe that our estimates, including those for the above-described items, are reasonable.

Use of Estimates

In accordance with GAAP, management utilizes estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements as well as the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. These estimates and assumptions relate to recording net revenue, collectability of accounts receivable, useful lives and impairment of tangible and intangible assets, accruals, income taxes, inventory realization, stock-based compensation expense and other factors. Management believes it has exercised reasonable judgment in deriving these estimates. Consequently, a change in conditions could affect these estimates.

Fair Value of Financial Instruments

The Company's cash, cash equivalents, investments, accounts receivable and accounts payable are stated at cost which approximates fair value due to the short-term nature of these instruments.

18

Recently Issued Accounting Pronouncements

Management reviewed accounting pronouncements issued during the three months ended September 30, 2011, and no pronouncements were adopted during the period.

Results of Operations

Year ended December 31, 2011 compared to the year ended December 31, 2010

General and Administrative Expenses

G&A expenses decreased by $(661,722) to $1,436,727 for the year ended December 31, 2011, compared to $2,098,449 for the year ended December 31, 2010. This decrease in G&A expenses was primarily due to the decrease of $(1,012,239) in non-cash stock compensation expense compared to the prior year. This was partially offset by the increase in other G&A expenses of $350,517.

Research and Development

R&D costs increased by $209,649 to $402,160 for the year ended December 31, 2011 compared to $192,511 for the year ended December 31, 2010. This increase in R&D costs was the result of an increase in outside consulting fees and supplies for testing and research of product development.

Net Loss

Net loss decreased by $(441,093) to $1,861,490 for the year ended December 31, 2011, compared to $2,302,583 for the year ended December 31, 2010. This decrease in net loss was the result of a decrease in non-cash stock compensation expense of $1,012,239, and the overall increase in operating expenses of $571,146. We had no revenues.

Liquidity and Capital Resources

As of December 31, 2011, we had a working deficit of $(230,854) compared to a working deficit of $(10,365) for the year ended December 31, 2010. The decrease of $(220,489) in working capital was due primarily to more current liabilities.

During the year ended December 31, 2011, we used $(1,509,968) of cash for operating activities, as compared to $(1,052,481) for the prior period December 31, 2010. The increase of $457,487 in the use of cash for operating activities was primarily due to an increase in operating net loss, in prepaid expenses, and in accounts payable.

Cash used by investing activities was $(78,189) for the year ended December 31, 2011, as compared to cash used of $(30,659) for the prior period ended December 31, 2010. The net increase of $(47,530) in cash used by investing activities in the current period was due to more funds used to purchase tangible and intangible assets as compared to the prior period ended December 31, 2010, which used fewer funds to purchase tangible and intangible assets, and received proceeds from the sale of a vehicle.

Cash provided from financing activities during the year ended December 31, 2011 was $1,557,000 as compared to $851,000 for the prior period ended December 31, 2010. Our capital needs have primarily been met from the proceeds of equity financings, and investor loans, as we are currently in the development stage and had no revenues.

Our financial statements as of December 31, 2011 have been prepared under the assumption that we would continue as a going concern. Our independent registered public accounting firm issued their report dated March 30, 2011 that included an explanatory paragraph expressing substantial doubt in our ability to continue as a going concern as the Company does not generate significant revenue and has negative cash flows from operations. Our ability to continue as a going concern ultimately is dependent on our ability to generate a profit which is dependent upon our ability to obtain additional equity or debt financing, attain further operating efficiencies and, ultimately, to achieve profitable operations. Our financial statements do not include any adjustments that might result from the outcome of this uncertainty.

19

During the first quarter of 2011, we issued Units comprising of an aggregate of 400,000 shares of common stock and warrants to purchase 1,600,000 shares of our common stock at a price of $1.00 per Unit for aggregate gross cash proceeds of $400,000. Each Unit consisted of 1 share and a warrant to purchase 4 shares of the Company’s common stock. The warrants were exercisable at a price of $1.00 for a term of five years. The net proceeds of the sales were used for working capital purposes. The warrants were subsequently exercised on a cashless basis for 1,333,335 shares of common stock.

During the second quarter of 2011, we issued Units comprising an aggregate of 800,000 shares of common stock and warrants to purchase 3,200,000 shares of our common stock at a price of $1.00 per Unit for aggregate gross cash proceeds of $800,000. Each Unit consisted of 1 share and a warrant to purchase 4 shares of the Company’s common stock. The warrants were exercisable at a price of $1.00 for a term of five years. The net proceeds of the sales were used for working capital purposes. The warrants were subsequently exercised on a cashless basis for 1,333,335 shares of common stock.

During the third quarter of 2011, we issued 341,000 shares of our common stock at a price of $2.00 per share for aggregate gross cash proceeds of $682,000. The net proceeds of the sales were used for working capital purposes.