Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Longhai Steel Inc. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - Longhai Steel Inc. | exhibit32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Longhai Steel Inc. | exhibit32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - Longhai Steel Inc. | exhibit31-2.htm |

| EX-10.12 - EXHIBIT 10.12 - Longhai Steel Inc. | exhibit10-12.htm |

| EX-31.1 - EXHIBIT 31.1 - Longhai Steel Inc. | exhibit31-1.htm |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31,

2011

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to

_____________

Commission File No. 001-35017

| LONGHAI STEEL INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada | 11-3699388 |

| (State or other jurisdiction of | (I.R.S. Employer Identification No.) |

| incorporation or organization) |

| No. 1 Jingguang Road, Neiqiu County |

| Xingtai City, Hebei Province 054000 |

| People’s Republic of China |

| (Address of principal executive offices) |

| +86 (319) 686-1111 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer [ ] | Accelerated Filer [ ] |

| Non-Accelerated Filer [ ] (Do not check if a smaller reporting company) |

Smaller reporting company [X] |

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [ ] No [X]

As of June 30, 2011 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of the registrant’s common stock held by non-affiliates (based upon the closing bid price of such shares as reported on the OTC Bulletin Board) was approximately $0 million, as the registrant’s shares were not then publicly traded. Shares of the registrant’s common stock held by each executive officer and director and each by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were a total of 10,050,418 shares of the registrant’s common stock outstanding as of March 28, 2012.

DOCUMENTS INCORPORATED BY REFERENCE

None.

2

| Annual Report on Form 10-K |

| Year Ended December 31, 2011 |

TABLE OF CONTENTS

PART I

| Item 1. | Business. | 2 |

| Item 1A. | Risk Factors. | 11 |

| Item 1B. | Unresolved Staff Comments. | 20 |

| Item 2. | Properties. | 20 |

| Item 3. | Legal Proceedings | 21 |

| Item 4. | Mine Safety Disclosures | 21 |

PART II

PART III

PART IV

| Item 15. | Exhibits, Financial Statement Schedules. | 43 |

Special Note Regarding Forward Looking Statements

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, including those identified in Item 1A “Risk Factors” included herein, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

Use of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

- “we,” “us,” “our,” or the “Company” are to the combined business of

Longhai Steel Inc., a Nevada corporation, and its consolidated subsidiaries;

- “Longhai” are to Xingtai Longhai Wire Rod Co. Ltd., a PRC company;

- “Kalington” are to Kalington Limited, a Hong Kong company;

- “Kalington Consulting” are to Xingtai Kalington Consulting Service Co.,

Ltd., a PRC company;

- “Hong Kong” are to the Hong Kong Special Administrative Region of the

People’s Republic of China;

- “PRC” and “China” are to the People’s Republic of China;

- “SEC” are to the U.S. Securities and Exchange Commission;

- “Securities Act” are to the Securities Act of 1933, as amended;

- “Exchange Act” are to the Securities Exchange Act of 1934, as amended;

- “Renminbi” and “RMB” are to the legal currency of China;

- “U.S. dollars,” “dollars” and “$” are to the legal currency of the United

States; and

- “VIE” are to variable interest entity.

1

PART I

ITEM 1. BUSINESS.

Overview of Our Business

We are a manufacturer of steel wire products in eastern China. We produce steel wire ranging from 5.5 mm to 18 mm in diameter on two wire production lines, which have a combined annual capacity of approximately 1.5 million metric tons (MT) per year. Our products are sold to a number of distributors who transport the wire to nearby wire processing facilities. Our wire is then further processed by these third party wire refiners into a variety of products such as nails, screws, and wire mesh for use in reinforced concrete and fencing.

Demand for our steel wire is driven primarily by spending in the construction and infrastructure industries. We have benefited from strong fixed asset investment and construction growth as the PRC has rapidly grown increasingly urbanized and invested in modernizing its infrastructure.

We sell our products to a number of distribution companies that transport our wire to nearby wire processors. Our products are manufactured on an on-demand basis, and we usually collect payment in advance. Sales prices are set at the market price for wire on a daily basis. Our customers generally prepay for their orders, and the final price may be adjusted to the market price on the day of pick up. This allows us to maintain a low inventory of both wire and billet and protects us from exposure to commodity price volatility. In order to increase sales and be competitive in the market, we occasionally offer discounted wholesale prices to customers at our discretion. Our sales efforts are directed toward developing long-term relationships with customers who are able to purchase in large quantities. During the years ended December 31, 2011 and 2010, our top five distributors accounted for approximately 49% and 35% of our revenue, respectively.

Our production facilities are located at a 197,500 square meter property in Xingtai, Hebei Province. Our production facilities include a steel rolling mill, the unique feature of which is that two rolling lines are arranged in a “Y”-layout, i.e., two wire drawing lines share one furnace, one coarse and intermediate rolling mill, and other supporting equipment. This particular design facilitates cost savings and higher output at a higher quality. In the third quarter of 2011, we entered into a five year operating lease for a newly constructed wire plant adjacent to our current facilities. The new facility has an area of 90,500 square meters and an annual capacity of 600,000 MT and will increase our production capacity by approximately 60%. The new facility is leased at a yearly cost of $2.2 million from Longhai Steel Group, the Company’s related party. Our corporate headquarters is located at No. 1 Jingguang Road, Neiqiu County, Xingtai City, Hebei Province, 054000, People’s Republic of China, and our telephone number is (86) 319 686-1111.

Our Corporate History and Background

We were originally incorporated under the laws of the State of Georgia on December 4, 1995. On March 14, 2008, the Georgia corporation was merged with and into a newly formed Nevada corporation named Action Industries, Inc., and all of the outstanding shares of the Georgia corporation were exchanged for shares in the surviving Nevada corporation. Prior to our reverse acquisition of Kalington discussed below, we were primarily in the business of providing prepaid long distance calling cards and other telecommunication products and had not commenced planned principal operations. As a result of our reverse acquisition of Kalington, active business operations were revived. On July 16, 2010, we amended our Articles of Incorporation to change our name to “Longhai Steel Inc.” to reflect the current business of our Company.

On March 26, 2010, we completed a reverse acquisition transaction through a share exchange with Kalington and its shareholders, whereby we acquired 100% of the issued and outstanding capital stock of Kalington in exchange for 10,000 shares of our Series A Preferred Stock, which constituted 98.5% of our issued and outstanding capital stock on an as-converted basis as of and immediately after the consummation of the reverse acquisition. As a result of the reverse acquisition, Kalington became our wholly-owned subsidiary and the former shareholders of Kalington became our controlling stockholders. The share exchange transaction with Kalington was treated as a reverse acquisition, with Kalington as the acquirer and Longhai Steel Inc. as the acquired party.

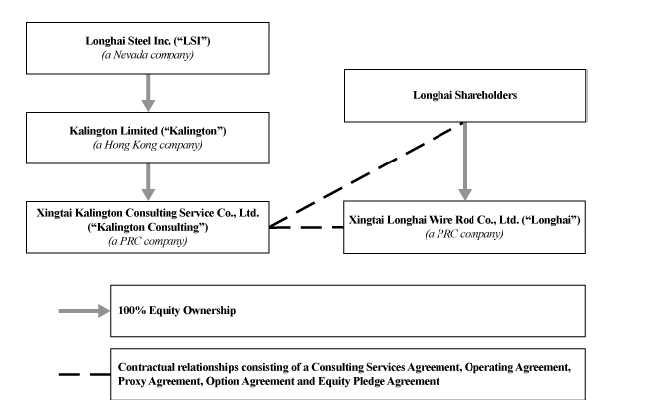

As a result of our acquisition of Kalington, we now own all of the issued and outstanding capital stock of Kalington, which in turn owns all of the issued and outstanding capital stock of Kalington Consulting. In addition, we effectively and substantially control Longhai through the VIE agreements discussed below.

Kalington was established on November 5, 2009 in Hong Kong to serve as an intermediate holding company. On March 18, 2010, Kalington established Kalington Consulting in the PRC. On March 5, 2010, the local government of the PRC issued a certificate of approval regarding the foreign ownership of Kalington Consulting. Longhai, our operating VIE, was established in the PRC on August 26, 2008, as a result of a carve-out from Xingtai Longhai Steel Group Co., Ltd., or Longhai Steel Group, for the purpose of engaging in the production of steel wire. Our Chairman and CEO, Chaojun Wang, serves as the Chairman of the Board of Directors and General Manager of Longhai and owns 80% of the capital stock in Longhai. Longhai’s additional shareholders are Wealth Index International (Beijing) Investment Co., Ltd. (15% owner), and Wenyi Chen (5% owner). Mr. Wang also owns 80% of the capital stock of and is the chief executive officer of Longhai Steel Group.

2

On March 19, 2010, prior to the reverse acquisition transaction, Kalington Consulting and Longhai entered into a series of agreements, or the VIE Agreements, pursuant to which Longhai became Kalington Consulting’s VIE. The use of VIE agreements is a common structure used to acquire PRC companies, particularly in certain industries in which foreign investment is restricted or forbidden by the PRC government. The VIE Agreements include:

- a Consulting Services Agreement through which Kalington Consulting has the

right to advise, consult, manage and operate Longhai and collect and own all

of the net profits of Longhai;

- an Operating Agreement through which Kalington Consulting has the right to

recommend director candidates and appoint the senior executives of Longhai,

approve any transactions that may materially affect the assets, liabilities,

rights or operations of Longhai, and guarantee the contractual performance by

Longhai of any agreements with third parties, in exchange for a pledge by

Longhai of its accounts receivable and assets;

- a Proxy Agreement under which the three owners of Longhai have vested

their collective voting control over Longhai to Kalington Consulting and will

only transfer their respective equity interests in Longhai to Kalington

Consulting or its designee(s);

- an Option Agreement under which the owners of Longhai have granted to

Kalington Consulting the irrevocable right and option to acquire all of their

equity interests in Longhai; and

- an Equity Pledge Agreement under which the owners of Longhai have pledged all of their rights, title and interests in Longhai to Kalington Consulting to guarantee Longhai’s performance of its obligations under the Consulting Services Agreement.

On March 18, 2010, prior to the reverse acquisition transaction, Mr. Wang entered into a call option agreement with Jinhai Guo, the sole shareholder of Merry Success Limited, which was the majority shareholder of Kalingon prior to the reverse acquisition, pursuant to which Mr. Wang was granted the right to acquire up to 100% of the shares of Merry Success Limited for fixed consideration within the next three years. The option agreement also provides that Mr. Guo shall not dispose of any of the shares of Merry Success Limited without Mr. Wang’s consent. As a result of the option agreement, Mr. Wang beneficially owns a majority of our capital stock and voting power, as well as of Longhai and Longhai Steel Group.

Because of the common control between Kalington, Kalington Consulting and Longhai, for accounting purposes, the acquisition of these entities has been treated as a recapitalization with no adjustment to the historical basis of their assets and liabilities. The restructuring has been accounted for using the “as if” pooling method of accounting and the operations were consolidated as if the restructuring had occurred as of the beginning of the earliest period presented in our consolidated financial statements and the current corporate structure had been in existence throughout the periods covered by our consolidated financial statements.

Our Corporate Structure

All of our business operations are conducted through our Hong Kong and Chinese subsidiaries and our VIE. The following chart reflects our corporate organizational structure:

3

Our Industry and Principal Market

China is the world’s largest producer of steel, with annual production in 2010 and 2011 of 627 million MT and 690 million MT, respectively. China accounts for roughly 70% of 2011 global steel production, which equals to twice the total output of the rest of the world combined. China’s steel industry, while enormous in total scale, is a fractured industry where a great number of producers each account for a small amount of total output. China’s steel industry includes a wide range of producers, including smaller, inefficient backyard operations, huge state owned enterprises beset with unnecessarily large, unionized labor forces and their accompanying pension burdens as well as newly constructed steel plants possessing facilities built according to the highest technology and efficiency standards in the world.

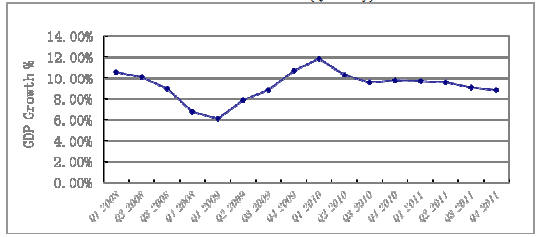

PRC Macroeconomic Drivers

The steel industry is a fundamental cornerstone of the economy and growth in the steel industry has coincided with consistent and strong growth in the PRC economy as a whole. The real gross domestic product, or GDP, year over year quarterly growth has averaged well over 9% since 2000, with a low of 6.1% in the first quarter of 2009, and has rebounded through 2011:

China - GDP Real Growth (Quarterly)

We believe that GDP growth will gradually slow down but remain positive as China continues its industrialization process.

4

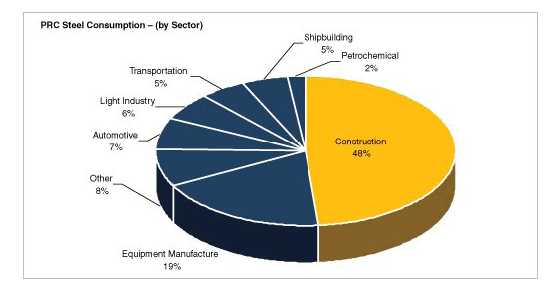

Steel Consumption, Construction and Fixed Asset Investment

Steel consumption in the PRC is highly correlated with nominal fixed asset investment, or FAI. Construction is the largest driver of steel usage in China. The following table details steel consumption by economic sector; construction consumes the most steel by a wide margin.

Construction growth has been strong and has rebounded from the financial downturn in late 2008. We expect to continue to benefit from the housing and commercial needs created by urbanization trends and infrastructure trends in the future.

Urbanization

We believe that GDP growth will gradually slow down but remain positive as China continues its industrialization and urbanization process. China’s urbanization ratio is 48%, versus 85% in developed economies and the global average of 55%. China’s urbanization rate is expected to increase by 1 percentage point every year for the next 20 years. Along with the rapid urbanization, the government may need to spend a total of RMB 24 trillion, or approximately $3.8 trillion, on urban infrastructure by 2020 because the number of city residents will continue to increase. We believe China’s urbanization will provide sustainable investment and become a key factor in bolstering China’s growth.

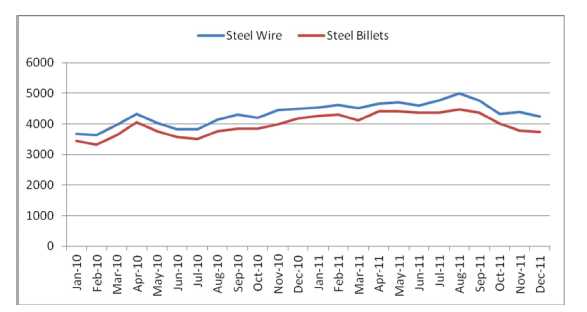

The Steel Wire Market

China has produced roughly 627 million MT of steel wire in 2010 and 690 million MT in 2011. Steel wire is used in a variety of products and serves the construction industry. The chart below details average steel wire prices in RMB we experienced since 2010 in our local market:

5

Our Growth Strategy

We believe that the market for high quality steel wire will continue to grow in the PRC. The PRC adopted a policy to reduce outdated steel production capacity and make it more difficult to approve new steel wire plant construction in July 2005 in an effort to encourage consolidation of facilities; therefore, our expansion plan is to build capacity through the acquisition of facilities at attractive prices from competitors who lack our management experience, efficient labor force, and financial resources. We plan to continue to improve margins through increased efficiencies in our production process and by adding higher grade steel wire to our product portfolio.

We intend to pursue the following strategies to achieve our goal:

- Expand production utilizing a newly leased facility: In the

third quarter of 2011, we entered into a five year operating lease for a newly

constructed wire plant adjacent to our current facilities. The new facility

has an area of 90,500 square meters and an annual capacity of 600,000 MT. The

new facility is leased at a yearly cost of $2.2 million from Longhai Steel

Group, a related party. The wire plant produces wire of a higher grade with

higher margins than our current products. The facility produces wire made of

Carbon Structure Steel, Cold Heading Steel and Welding Rod Steel, with a

diameter range of 5.5mm – 18mm, which has a wide range of applications such as

steel wire rope, steel strand, steel belted radial tires and steel welding

rod. We are in the process of upgrading the facility. Once fully upgraded, the

new facility will increase our production capacity by approximately 60% and

will have the capability to produce alloy steel, cold forging steel and

welding rods. These higher margin products will allow Longhai to also address

demand in additional markets beyond construction and infrastructure.

- Identify and acquire modern, high quality producers at low

valuations: In light of the restriction on building new wire making

facilities in China, we plan to expand our business and operations through the

acquisition of steel wire producers with production facilities in the vicinity

of our current facilities. We expect to limit our acquisition targets to

producers with facilities that have had a major overhaul or modernization of

production machinery in the last 2 – 3 years, as we expect such facilities to

achieve better production efficiency, lower maintenance costs and increased

output, as compared to less modern facilities, and will help us to more

rapidly achieve higher margins and increase our market share.

- Expansion to create economies of scale: We expect that our acquisition of modernized facilities will result in increased wire-making capacity, resulting in greater bargaining power with supplier pricing and otherwise enable us to capitalize on economies of scale and/or widen our product portfolio to produce at higher margins.

Our Products

Our products are steel wires ranging in diameter from 5.5mm to 18mm. All our wires are manufactured in accordance to ISO9001-2000 quality management system standards. Our 6.5mm diameter wires also meet PRC national GB/700-88 standards, the PRC national standard for carbon structural steel. We ensure a low quantity of oxide in our wire to provide our downstream customers with the highest quality products for further processing. Our end customers process the wire into a variety of end products vital to construction and infrastructure, including but not limited to nails, screws, wire mesh, and fencing. Our new facility will have the capability to produce alloy steel, cold forging steel and welding rods.

6

We sell 100% of our products in China, with approximately 80% being sold in Hebei province, our largest market. The industrial area in and around the nearby city of Hengshui contains one of the largest collective wire processing capacities in the world. Much of our wire is distributed in this area for further processing.

Domestic economic growth and the accompanying fixed asset investment in construction and infrastructure projects is the major macroeconomic driver of our growth.

Our Customers

We sell our products to a number of distribution companies that transport our wire to nearby wire processors. Our products are manufactured on an on-demand basis, and we usually collect payment in advance. Sales prices are set at the market price for wire on a daily basis. Our customers generally prepay for their orders, and the final price may be adjusted to the market price on the day of pick up. This allows us to maintain a low inventory of both wire and billet and largely protects us from exposure to commodity price volatility.

In order to increase sales and be competitive in the market, we occasionally offer discounted wholesale prices to newer or larger customers at our discretion. Our sales efforts are directed toward developing long term relationships with customers who we expect are or will be able to purchase in large quantities. During the year ended December 31, 2011, our top five distributors accounted for 49% of our revenues as follows:

| Rank | Customer | % of Total Revenue | ||||

| 1 | Beixin Building Materials (Group) Co., Ltd. | 15% | ||||

| 2 | Hebei Huanneng Development Co.,Ltd | 13% | ||||

| 3 | Jizhong Energy Trading Co., Ltd. | 12% | ||||

| 4 | Hebei Huatong Co., Ltd. | 6% | ||||

| 5 | Zhonggang Steel Co., Ltd. | 3% | ||||

| Total | 49% |

We pride ourselves on our ability to meet our customers’ demand for high quality products, fast turnaround and timely delivery, and customer support. We believe that our ability to consistently meet or exceed these standards is critical to our success and market share. Our sales department currently has 20 full time employees.

Our Major Supplier of Raw Materials

The principal raw material used in our products is steel billet. In 2011, steel billet accounted for more than 95% of our production costs. We generally purchase billet only after a customer has made a wire order and therefore avoid a large inventory of billet. This insulates us from commodity price fluctuation risk associated with holding large quantities of raw materials. We are generally able to pass higher costs due to fluctuations in raw material costs directly through to our customers.

Prior to 2009, we purchased our steel billet at a slight discount from Longhai Steel Group, a related entity owned and controlled by our CEO, Chaojun Wang. However, since 2009, we have purchased our steel billet at prevailing market prices from independent, third party trading companies. While they source their steel billet from local steel manufacturers, including Longhai Steel Group, they provide all of our billets only through Longhai Steel Group. They also function as financing intermediaries to facilitate delivery of steel billets to Longhai. The price of the billets is the published daily commodity index price, ensuring an arm’s length pricing transaction with Longhai Steel Group. Longhai Steel Group is able to supply steel to Longhai less expensively than competitors because, while the base price of steel billet is comparable across the region, (i) Longhai Steel Group’s cost of transporting steel to Longhai is lower given its proximity to Longhai and (ii) Longhai Steel Group can deliver hot steel billet given such proximity, which reduces Longhai’s energy costs and factors into Longhai’s calculation of its true steel billet costs. Our purchasing team monitors and tracks movements in steel billet prices daily and provides regular guidance to management to respond quickly to market conditions and aid in long term business planning.

7

The table below lists our top suppliers as of December 31, 2011, showing the cumulative dollar amount of raw materials purchased from them during the fiscal year ended December 31, 2011 and the percentage of raw materials purchased from each supplier as compared to procurement of all raw materials. All of the listed suppliers are unrelated trading companies.

| Total Purchases | % of Total | ||||||||

| amount in 2011 | Purchases in 2011 | ||||||||

| Rank | Supplier | ‘000 | |||||||

| 1 | Beixin Buidling Material (Group) Co., Ltd. | $ | 198,468 | 36% | |||||

| 2 | Xingtai Roller Co., Ltd. | 76,210 | 14% | ||||||

| 3 | Hebei Huaneng Industrial Development Co., Ltd | 71,199 | 13% | ||||||

| 4 | Others | 211,013 | 37% | ||||||

| Total Purchasing Volume | $ | 556,890 | 100% |

Our Competition

Competition within the steel industry in the PRC is intense. There is an estimated 690 million MT of steel capacity in China. Our competitors range from small private enterprises to extremely large state-owned enterprises. Our operating subsidiary, Longhai, is located in Xingtai, Hebei Province. Hebei is the largest producer of steel by province in the PRC.

There are government restrictions in China related to opening new steel wire manufacturing facilities. Suppliers of steel wire compete largely on the basis of quality standards and order turn-around time. If, for example, a client orders different diameters of steel wire, the production line has to be stopped and adjusted at least once so that wire of a different diameter can be produced. The more often such changes are required, the more order turnaround will be impacted. By efficiently bundling different purchase orders and optimizing production management, we have achieved a significant reduction of order turn-around time (from an average of 21 days to seven days), which gives us a significant advantage over our competitors.

Market participants typically do not compete on price, given the level of margins typical in the steel wire industry.

Transportation cost provides an additional entry barrier for suppliers that are located at larger distances from a given client.

| Estimated Capacity | ||||

| Company | Production Lines | (in million MTs) | Line Speed (m/s) | Ownership |

| Xingtai Steel Company | 5 | 3 | 90 | State Owned |

| Hebei Xinjin Company | 2 | 0.8 | 70, 90 | Private |

| Wuan Mingfang Steel Company | 2 | 0.9 | 90 | Private |

| Yongnian Jianfa Company | 1 | 0.3 | 60 | Private |

We operate two production lines with a combined yearly steel wire capacity of 900,000 MT at a line speed of 90 meters per second, and operate one production facility with an annual capacity of 600,000 MT at 90 meters per second, which will become fully operational by May 2012.

Private steel product manufacturers in China generally focus on low-end products. Many of our competitors are significantly smaller than we are and use outdated equipment and production techniques. Due to our high quality equipment, economies of scale and management experience, we produce steel wire at higher efficiencies and lower prices than these competitors. The larger state owned enterprises with whom we compete often have oversized, unionized labor forces and associated pension and healthcare liabilities and cannot match our production efficiency. We believe that we distinguish ourselves in the market based on our extremely fast order turnaround, high quality and competitive prices.

Our Employees

As of December 31, 2011, we had 816 full-time and no part-time employees. The following table illustrates the allocation of these employees among the various job functions conducted at our company.

8

| Function |

Number of Employees |

||

| Management | 10 | ||

| Administrative | 12 | ||

| Accounting | 14 | ||

| Sales | 20 | ||

| Production | 760 | ||

| Total | 816 |

We believe that we maintain a satisfactory working relationship with our employees and we have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

Our employees in China participate in a state pension plan organized by Chinese municipal and provincial governments to which we are required to contribute 20% of monthly salaries of those employees who have elected to pay their plan contributions through us. Employees from the countryside can opt to pay their contributions in their home village instead, where contributions are lower thus getting higher net pay in return for a lower pension. The compensation expenses related to the state pension plan were $83,206 and $97,197 for fiscal years 2011 and 2010, respectively. In addition, we are required by Chinese law to cover employees in China with various types of social insurance. We have purchased social insurances for some employees.

Regulation

Our business is regulated by the national and local laws of the PRC. We believe our conduct of business complies with existing PRC laws, rules and regulations.

General Regulation of Businesses

We believe we are in material compliance with all applicable labor and safety laws and regulations in the PRC, including the PRC Labor Contract Law, the PRC Production Safety Law, the PRC Regulation for Insurance for Labor Injury, the PRC Unemployment Insurance Law, the PRC Provisional Insurance Measures for Maternity of Employees, PRC Interim Provisions on Registration of Social Insurance, PRC Interim Regulation on the Collection and Payment of Social Insurance Premiums and other related regulations, rules and provisions issued by the relevant governmental authorities from time to time, for our operations in the PRC.

According to the PRC Labor Contract Law, we are required to enter into labor contracts with our employees. We are required to pay no less than local minimum wages to our employees. We are also required to provide employees with labor safety and sanitation conditions meeting PRC government laws and regulations and carry out regular health examinations of our employees engaged in hazardous occupations.

Environmental Matters

We are subject to various governmental regulations related to environmental protection. Our manufacturing facilities are subject to various pollution control regulations with respect to noise, water and air pollution and the disposal of waste and hazardous materials, including, China’s Environmental Protection Law, China’s Law on the Prevention and Control of Water Pollution and its implementing rules, China’s Law on the Prevention and Control of Air Pollution and its implementing rules, China’s Law on the Prevention and Control of Solid Waste Pollution, and China’s Law on the Prevention and Control of Noise Pollution. We are subject to periodic inspections by local environmental protection authorities. We have received certifications from the relevant PRC government agencies in charge of environmental protection indicating that our business operations are in material compliance with the relevant PRC environmental laws and regulations. We are not currently subject to any pending actions alleging any violations of applicable PRC environmental laws.

Foreign Currency Exchange

All of our sales revenue and expenses are denominated in RMB. Under the PRC foreign currency exchange regulations applicable to us, RMB is convertible for current account items, including the distribution of dividends, interest payments, trade and service-related foreign exchange transactions. Currently, our PRC operating subsidiary and VIE may purchase foreign currencies for settlement of current account transactions, including payments of dividends to us, employee salaries (even if employees are based outside of China), and payment for equipment purchases outside of China, without the approval of the State Administration of Foreign Exchange of the People’s Republic of China, or SAFE, by complying with certain procedural requirements. Conversion of RMB for capital account items, such as direct investment, loan, security investment and repatriation of investment, however, is still subject to the approval of SAFE. In particular, if our PRC operating subsidiary and VIE borrow foreign currency through loans from us or other foreign lenders, these loans must be registered with SAFE, and if we finance subsidiaries by means of additional capital contributions, these capital contributions must be approved by certain government authorities, including the Ministry of Commerce, or MOFCOM, or their respective local branches. These limitations could affect our ability to obtain foreign exchange through debt or equity financing. In the event of a liquidation, SAFE approval is required before the remaining proceeds can be expatriated from China.

9

Taxation

On March 16, 2007, the National People’s Congress of China passed a new Enterprise Income Tax Law, or EIT Law, and on November 28, 2007, the State Council of China passed its implementing rules, which took effect on January 1, 2008. Before the implementation of the EIT Law, foreign invested enterprises, or FIEs, established in the PRC, unless granted preferential tax treatments by the PRC government, were generally subject to an earned income tax, or EIT, rate of 33.0%, which included a 30.0% state income tax and a 3.0% local income tax. The EIT Law and its implementing rules impose a unified EIT of 25.0% on all domestic-invested enterprises and FIEs, unless they qualify under certain limited exceptions. Despite these changes, the EIT Law gives FIEs established before March 16, 2007, or Old FIEs, a five-year grandfather period during which they can continue to enjoy their existing preferential tax treatments. During this five-year grandfather period, the Old FIEs which enjoyed tax rates lower than 25% under the original EIT law will be subject to gradually increased EIT rates over a 5-year period until their tax rate reaches 25%. In addition, the Old FIEs that are eligible for other preferential tax treatments by the PRC government under the original EIT law are allowed to continue enjoying their preference until these preferential treatment periods expire.

In addition to the changes to the current tax structure, under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a resident enterprise and will normally be subject to an EIT of 25% on its global income. The implementing rules define the term “de facto management bodies” as “an establishment that exercises, in substance, overall management and control over the production, business, personnel, accounting, etc., of a Chinese enterprise.” If the PRC tax authorities subsequently determine that we should be classified as a resident enterprise, then our organization’s global income will be subject to PRC income tax of 25%. For detailed discussion of PRC tax issues related to resident enterprise status, see Item 1A “Risk Factors—Risks Related to Doing Business in China—Under the Enterprise Income Tax Law, we may be classified as a ‘resident enterprise’ of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC stockholders.”

In addition, the EIT Law and its implementing rules generally provide that an income tax rate of 10% will normally be applicable to dividends payable to investors that are “non-resident enterprises,” or non-resident investors, which (i) do not have an establishment or place of business in the PRC or (ii) have an establishment or place of business in the PRC, but the relevant income is not effectively connected with the establishment or place of business to the extent such dividends are derived from sources within the PRC. The State Council of the PRC or a tax treaty between China and the jurisdictions in which the non-PRC investors reside may reduce such income tax. Under the Arrangement between the Mainland and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income, effective as of January 1, 2007, such dividend withholding tax rate is reduced to 5% if a Hong Kong resident enterprise owns over 25% of the PRC company distributing the dividends. As Kalington is a Hong Kong company and owns 100% of Kalington Consulting, under the aforesaid arrangement, any dividends that Kalington Consulting pays Kalington may be subject to a withholding tax at the rate of 5%. However, if Kalington is not considered to be the “beneficial owner” of such dividends under the Notice Regarding Interpretation and Recognition of Beneficial Owners under Tax Treaties, or Notice 601, promulgated by the State Administration of Taxation on October 27, 2009, such dividends would be subject to the withholding tax rate of 10%. The withholding tax rate of 5% or 10% applicable to Kalington will have a significant impact on the amount of dividends to be received by the Company and ultimately by stockholders.

Pursuant to the Provisional Regulation of China on Value Added Tax and its implementing rules, all entities and individuals that are engaged in the sale of goods, the provision of repairs and replacement services and the importation of goods in China are generally required to pay value added tax, or VAT, at a rate of 17.0% of the gross sales proceeds received, less any deductible VAT already paid or borne by the taxpayer. Further, when exporting goods, the exporter is entitled to some or all of the refund of VAT that it has already paid or borne.

Dividend Distribution

Under applicable PRC regulations, FIEs in China may pay dividends only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, an FIE in China is required to set aside at least 10.0% of its annual after-tax profit based on PRC accounting standards each year to its general reserves until the cumulative amount of such reserves reaches 50.0% of its registered capital. These reserves are not distributable as cash dividends. The board of directors of an FIE has the discretion to allocate a portion of its after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

Circular 75

On November 1, 2005, SAFE issued the Notice on Relevant Issues Concerning Foreign Exchange Administration for Domestic Residents to Engage in Overseas Financing and Round Trip Investment via Overseas Special Purpose Vehicles, or Circular 75, which regulates the foreign exchange matters in relation to the use of a special purpose vehicle, or SPV, by PRC residents to seek offshore equity financing and conduct “round trip investment” in China. Under Circular 75, a SPV refers to an offshore entity established or controlled, directly or indirectly, by PRC residents or PRC entities for the purpose of seeking offshore equity financing using assets or interests owned by such PRC residents or PRC entities in onshore companies, while “round trip investment” refers to the direct investment in China by the PRC residents through the SPVs, including, without limitation, establishing FIEs and using such foreign-invested enterprises to purchase or control onshore assets through contractual arrangements. Circular 75 requires that, before establishing or controlling a SPV, PRC residents and PRC entities are required to complete foreign exchange registration with the local offices of SAFE for their overseas investments.

10

Circular 75 applies retroactively. PRC residents who have established or acquired control of the SPVs which have completed “round-trip investment” before the implementation of Circular 75 shall register their ownership interests or control in such SPVs with the local offices of SAFE before March 31, 2006. An amendment to the registration is required if there is a material change in the SPV, such as increase or reduction of share capital and transfer of shares. Failure to comply with the registration procedures set forth in Circular 75 may result in restrictions on the foreign exchange activities of the relevant FIEs, including the payment of dividends and other distributions, such as proceeds from any reduction in capital, share transfer or liquidation, to its offshore parent or affiliate and the capital inflow from the offshore parent, and may also subject relevant PRC residents to penalties under PRC foreign exchange administration regulations.

As we stated under Item 1A “Risk factors—Risks Related to Doing Business in China—Failure to comply with PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident stockholders to personal liability, limit our ability to acquire PRC companies or to inject capital into our PRC subsidiaries, limit our PRC subsidiaries’ ability to distribute profits to us or otherwise materially adversely affect us,” we have asked our stockholders, who are PRC residents as defined in Circular 75, to register with the relevant branch of SAFE, as currently required, in connection with their equity interests in us and our acquisitions of equity interests in our PRC subsidiaries. However, many of the terms and provisions in Circular 75 remain unclear and implementation by central SAFE and local SAFE branches of Circular 75 have been inconsistent since their adoption. Therefore, we cannot predict how Circular 75 will affect our business operations or future strategies. For example, our present and prospective PRC subsidiaries’ ability to conduct foreign exchange activities, such as the remittance of dividends and foreign currency-denominated borrowings, may be subject to compliance with Circular 75 by our PRC resident beneficial holders.

Insurance

Insurance companies in China offer limited business insurance products. While business interruption insurance is available to a limited extent in China, we have determined that the risks of interruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. As a result, we could face liability from the interruption of our business as summarized under Item 1A “Risk Factors—Risks Related to Our Business—We do not carry business interruption insurance, so we have to bear losses ourselves.” We do not carry business interruption insurance so we could incur unrecoverable losses if our business is interrupted. We do, however, carry standard social insurances as required by PRC law for our employees and commercial insurance for our equipment.

ITEM 1A. RISK FACTORS.

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment. You should read the section entitled “Special Notes Regarding Forward-Looking Statements” above for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this report.

RISKS RELATED TO OUR BUSINESS

We face risks related to general domestic and global economic conditions.

Our current operating cash flows provide us with stable funding capacity. However, the uncertainty arising out of domestic and global economic conditions, including the recent disruption in credit markets, poses a risk to the PRC economy and may impact our ability to manage normal relationships with our customers, suppliers and creditors. If the current situation deteriorates significantly, our business could be materially negatively impacted, as demand for our products and services may decrease from a slow-down in the general economy, or supplier or customer disruptions may result from tighter credit markets.

11

Our business is dependent upon continued infrastructure and construction spending and our growth may be inhibited by the inability of potential customers to fund purchases of our products and services.

Our products are dependent on the continued growth of infrastructure and construction projects in the PRC. There is no guarantee that the PRC will continue to invest in infrastructure and construction.

If we are unable to attract and retain senior management and qualified technical and sales personnel, our operations, financial condition and prospects will be materially adversely affected.

Our future success depends in part on the contributions of our management team and key technical and sales personnel and our ability to attract and retain qualified new personnel. In particular, our success depends upon the continuing employment of our Chief Executive Officer, Mr. Chaojun Wang, our Chief Technology Officer, Ms. Dongmei Pan, and our Chief Financial Officer, Mr. Heyin Lv. There is significant competition in our industry for qualified managerial, technical and sales personnel, and we cannot assure you that we will be able to retain our key senior managerial, technical and sales personnel or that we will be able to attract, integrate and retain other such personnel that we may require in the future. If we are unable to attract and retain key personnel in the future, our business, operations, financial condition, results of operations and prospects could be materially adversely affected.

We do not carry business interruption insurance, so we have to bear losses ourselves.

We are subject to risk inherent to our business, including equipment failure, theft, natural disasters, industrial accidents, labor disturbances, business interruptions, property damage, product liability, personal injury and death. We carry insurance for our equipment but we do not carry any business interruption insurance or third-party liability insurance to cover risks associated with our business. As a result, if we suffer losses, damages or liabilities, including those caused by natural disasters or other events beyond our control and we are unable to make a claim against a third party, we will be required to bear all such losses from our own funds, which could have a material adverse effect on our business, financial condition and results of operations.

Our quarterly operating results are likely to fluctuate, which may affect our stock price.

Our quarterly revenues, expenses, operating results and gross profit margins vary from quarter to quarter. As a result, our operating results may fall below the expectations of securities analysts and investors in some quarters, which could result in a decrease in the market price of our common stock. The reasons our quarterly results may fluctuate include:

- variations in the price of steel and steel wire;

- changes in the general competitive and economic conditions; and

- delays in, or uneven timing in the delivery of, customer orders.

Period to period comparisons of our results should not be relied on as indications of future performance.

We will require additional capital to fund our future activities. If we fail to obtain additional capital, we may not be able to fully implement our planned expansion.

Historically, we have financed our business plan and operations primarily with internally generated cash flow and bank borrowings. The success of our planned expansion depends on substantial capital expenditures that may not be sufficiently fueled by internally generated cash flow and bank borrowings. Our future contractual commitments include a five-year operating lease obligation with an annual lease cost of $2.2 million. We entered into the lease agreement on August 1,2011, with Longhai Steel Group, which is related to Longhai, for a newly constructed wire plant adjacent to our current facilities. The new facility will enable us to increase our production capacity by approximately 60%. We also require capital to fund the purchase of raw materials and other working capital needs to increase production at the new facility.

If we fail to raise enough capital, we may not be able to fully implement our business plan. Even if additional capital is available, we may not be able to obtain debt or equity financing on terms favorable to us, or at all. If cash generated by operations or available under our credit facility is not sufficient to meet our capital requirements, the failure to obtain additional financing could result in a curtailment of our operations relating to exploration and development of our projects. In addition, we will require additional working capital to support other long-term growth strategies, which include identifying suitable points of market entry for expansion, growing the number of points of sale for our products, so as to enhance our product offerings and benefit from economies of scale.

Our working capital requirements and the cash flow provided by future operating activities, if any, may vary greatly from quarter to quarter, depending on the volume of business and the level of steel prices during the period. We may not be able to obtain adequate levels of additional financing, whether through equity financing, debt financing or other sources. Additional financings could result in significant dilution to our earnings per share or the issuance of securities with rights superior to our current outstanding securities. In addition, we may grant registration rights to investors purchasing our equity or debt securities in the future. If we are unable to raise additional financing, we may be unable to implement our long- term growth strategies, develop or enhance our products and services, take advantage of future opportunities or respond to competitive pressures on a timely basis.

12

Our management may have potential conflicts of interest with our related party, Longhai Steel Group, that could adversely affect our company.

Our chief executive officer and primary shareholder, Chaojun Wang, is also the controlling shareholder of Longhai Steel Group. Prior to the reorganization of Longhai in preparation for the reverse merger, Longhai operated largely as a member of Longhai Steel Group. As a result, Longhai had a number of related party transactions with Longhai Steel Group. For example, Longhai purchased substantially all of its steel billets requirement from Longhai Steel Group and leases space from Longhai Steel Group for its facilities.

Although Longhai has taken steps to reduce the number of related party transactions with Longhai Steel Group and has implemented safeguards to reduce the potential for related party transactions to benefit Longhai Steel Group to the detriment of Longhai, any related party transactions between Longhai and Longhai Steel Group may present conflicts of interest for our management. For example, although Longhai’s facility lease agreement with Longhai Steel Group restricts Longhai Steel Group’s ability to unilaterally terminate or change the terms of the lease, Longhai’s management—who also manage Longhai Steel Group — could have an incentive to amend these provisions of the lease to remove these protections or to increase lease payments to the benefit of Longhai Steel Group. Similarly, although Longhai purchases its steel billet needs from third parties (which, in turn, purchase from Longhai Steel Group) rather than from Longhai Steel Group directly, Longhai Steel Group could take steps to increase the costs of such billet to Longhai’s detriment. In particular, Longhai Steel Group is able to supply steel to Longhai less expensively than competitors because, while the base price of steel billet is comparable across the region, (i) Longhai Steel Group’s cost of transporting steel to Longhai is lower given its proximity to Longhai and (ii) Longhai Steel Group can deliver hot steel billet given such proximity, which reduces Longhai’s energy costs and factors into Longhai’s calculation of its true steel billet costs. Longhai Steel Group could use this advantage to increase its price to a level that is higher than it would otherwise charge, knowing that the ultimate price to Longhai would remain comparable after factoring in such additional benefits. At the same time, the management of Longhai could cause Longhai to purchase steel from third parties that purchase from Longhai Steel Group, even where such purchases would not be in Longhai’s best economic interest.

While we have adopted a majority independent board of directors and have implemented a code of ethics to reduce the likelihood of such conflicts of interest, such potential conflicts of interest might occur from time to time, and the effect of any such conflict could be materially adverse to our Company.

RISKS RELATED TO THE VIE AGREEMENTS

The PRC government may determine that the VIE Agreements are not in compliance with applicable PRC laws, rules and regulations.

Kalington Consulting manages and operates our steel wire production business through Longhai pursuant to the rights it holds under the VIE Agreements. Almost all economic benefits and risks arising from Longhai’s operations are transferred to Kalington Consulting under these agreements. Details of the VIE Agreements are set out in Item 1 “Business—Our Corporate History and Background” above.

There are risks involved with the operation of our business in reliance on the VIE Agreements, including the risk that the VIE Agreements may be determined by PRC regulators or courts to be unenforceable. Our PRC counsel has provided a legal opinion that the VIE Agreements are binding and enforceable under PRC law, but has further advised that if the VIE Agreements were for any reason determined to be in breach of any existing or future PRC laws or regulations, the relevant regulatory authorities would have broad discretion in dealing with such breach, including:

- imposing economic penalties;

- discontinuing or restricting the operations of Longhai or Kalington Consulting;

- imposing conditions or requirements in respect of the VIE Agreements with which Longhai or Kalington Consulting may not be able to comply;

- requiring our company to restructure the relevant ownership structure or operations;

- taking other regulatory or enforcement actions that could adversely affect our company’s business; and

- revoking the business licenses and/or the licenses or certificates of Kalington Consulting, and/or voiding the VIE Agreements.

Any of these actions could adversely affect our ability to manage, operate and gain the financial benefits of Longhai, which would have a material adverse impact on our business, financial condition and results of operations.

13

Our ability to manage and operate Longhai under the VIE Agreements may not be as effective as direct ownership.

We conduct our steel wire production business in the PRC and generate virtually all of our revenues through the VIE Agreements. Our plans for future growth are based substantially on growing the operations of Longhai. However, the VIE Agreements may not be as effective in providing us with control over Longhai as direct ownership. Under the current VIE arrangements, as a legal matter, if Longhai fails to perform its obligations under these contractual arrangements, we may have to (i) incur substantial costs and resources to enforce such arrangements, and (ii) reply on legal remedies under PRC law, which we cannot be sure would be effective. Therefore, if we are unable to effectively control Longhai, it may have an adverse effect on our ability to achieve our business objectives and grow our revenues.

As the VIE Agreements are governed by PRC law, we would be required to rely on PRC law to enforce our rights and remedies under them, and PRC law may not provide us with the same rights and remedies as are available in contractual disputes governed by the law of other jurisdictions.

The VIE Agreements are governed by the PRC law and provide for the resolution of disputes through arbitral proceedings pursuant to PRC law. If Longhai or its shareholders fail to perform the obligations under the VIE Agreements, we would be required to resort to legal remedies available under PRC law, including seeking specific performance or injunctive relief, or claiming damages. We cannot be sure that such remedies would provide us with effective means of causing Longhai to meet its obligations, or recovering any losses or damages as a result of non-performance. Further, the legal environment in China is not as developed as in other jurisdictions. Uncertainties in the application of various laws, rules, regulations or policies in the PRC legal system could limit our liability to enforce the VIE Agreements and protect our interests.

The payment arrangement under the VIE Agreements may be challenged by the PRC tax authorities.

We generate our revenues through the payments we receive pursuant to the VIE Agreements. We could face adverse tax consequences if the PRC tax authorities determine that the VIE Agreements were not entered into based on arm’s length negotiations. For example, PRC tax authorities may adjust our income and expenses for PRC tax purposes, which could result in our being subject to higher tax liability or cause other adverse financial consequences.

The controlling shareholder of Longhai may have potential conflicts of interest with our company that may adversely affect our business.

Chaojun Wang is our chief executive officer, and is also the largest shareholder of Longhai. Conflicts could arise from time to time between our interests and the interests of Mr. Wang. Conflicts could also arise between us and Longhai that would require our shareholders and Longhai’s shareholders to vote on corporate actions necessary to resolve the conflict. There can be no assurance in any such circumstances that Mr. Wang will vote his shares in our best interest or otherwise act in the best interests of our company. If Mr. Wang fails to act in our best interests, our operating performance and future growth could be adversely affected.

We rely on the approval certificates and business license held by Kalington Consulting and any deterioration of the relationship between Kalington Consulting and Longhai could materially and adversely affect our business operations.

We operate our steel wire production business in China on the basis of the approval certificates, business license and other requisite licenses held by Kalington Consulting and Longhai. There is no assurance that Kalington Consulting and Longhai will be able to renew their licenses or certificates when their terms expire with substantially similar terms as the ones they currently hold.

Further, our relationship with Longhai is governed by the VIE Agreements, which are intended to provide us with effective control over the business operations of Longhai. However, the VIE Agreements may not be effective in providing control over the application for and maintenance of the licenses required for our business operations. Longhai could violate the VIE Agreements, become insolvent, suffer from difficulties in its business or otherwise become unable to perform its obligations under the VIE Agreements and, as a result, our operations, reputations and business could be materially harmed.

If Kalington Consulting exercises the purchase option it holds over Longhai’s share capital pursuant to the VIE Agreements, the payment of the purchase price could materially and adversely affect our financial position.

Under the VIE Agreements, Longhai’s shareholders have granted Kalington Consulting an option for the maximum period of time allowed by law to purchase all of the equity interest in Longhai at a price equal to the capital paid in by the transferors, adjusted pro rata for purchase of less than all of the equity interest, unless applicable PRC laws and regulations require an appraisal of the equity interest or stipulate other restrictions regarding the purchase price of the equity interest. Since Longhai is already our contractually controlled affiliate, our exercise of the option would not bring immediate benefits to our Company, and we would only do so if Longhai or its shareholders fail to perform the obligations under the VIE Agreements and we are unable to obtain specific performance, injunctive relief, or other damages in PRC courts, or otherwise protect our interests. The parties have agreed that if the applicable PRC laws and regulations require an appraisal of the equity interest or stipulate other restrictions regarding the purchase price of the equity interest at the time that the option is exercised, then the purchase price will be set at the lowest price permissible under the applicable laws and regulations. However, due to uncertainties in the application of various laws, rules, regulations or policies in PRC legal system, we cannot be sure that if we choose to exercise such option, any appraisal of equity interest or other stipulated restrictions required by PRC law will not materially increase the payment price for the option and adversely affect our results of operations.

14

RISKS RELATED TO DOING BUSINESS IN CHINA

If we become directly subject to the recent scrutiny, criticism and negative publicity involving U.S.-listed Chinese companies, we may have to expend significant resources to investigate and resolve the matter which could harm our business operations, stock price and reputation and could result in a loss of your investment in our stock, especially if such matter cannot be addressed and resolved favorably.

Recently, U.S. public companies that have substantially all of their operations in China, particularly companies like us which have completed so-called reverse merger transactions, have been the subject of intense scrutiny, criticism and negative publicity by investors, financial commentators and regulatory agencies, such as the SEC. Much of the scrutiny, criticism and negative publicity has centered around financial and accounting irregularities and mistakes, a lack of effective internal controls over financial accounting, inadequate corporate governance policies or a lack of adherence thereto and, in many cases, allegations of fraud. As a result of the scrutiny, criticism and negative publicity, the publicly traded stock of many U.S. listed Chinese companies has sharply decreased in value and, in some cases, has become virtually worthless. Many of these companies are now subject to shareholder lawsuits, SEC enforcement actions and are conducting internal and external investigations into the allegations. It is not clear what effect this sector-wide scrutiny, criticism and negative publicity will have on our Company, our business and our stock price. If we become the subject of any unfavorable allegations, whether such allegations are proven to be true or untrue, we will have to expend significant resources to investigate such allegations and/or defend our company. This situation will be costly and time consuming and distract our management from growing our company. If such allegations are not proven to be groundless, our company and business operations will be severely affected and your investment in our stock could be rendered worthless.

Adverse changes in political, economic and other policies of the Chinese government could have a material adverse effect on the overall economic growth of China, which could materially and adversely affect the growth of our business and our competitive position.

Most of our business operations are conducted in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. The Chinese economy differs from the economies of most developed countries in many respects, including:

- the degree of government involvement;

- the level of development;

- the growth rate;

- the control of foreign exchange;

- the allocation of resources;

- an evolving regulatory system; and

- a lack of sufficient transparency in the regulatory process.

While the Chinese economy has experienced significant growth in the past 30 years, growth has been uneven, both geographically and among various sectors of the economy. The Chinese economy has also experienced certain adverse effects due to the recent global financial crisis. The Chinese government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures benefit the overall Chinese economy, but may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us.

The Chinese economy has been transitioning from a planned economy to a more market-oriented economy. Although in recent years the Chinese government has implemented measures emphasizing the utilization of market forces for economic reform, the reduction of state ownership of productive assets and the establishment of sound corporate governance in business enterprises, a substantial portion of the productive assets in China is still owned by the Chinese government. The continued control of these assets and other aspects of the national economy by the Chinese government could materially and adversely affect our business. The Chinese government also exercises significant control over Chinese economic growth through the allocation of resources, controlling payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies.

15

Any adverse change in the economic conditions or government policies in China could have a material adverse effect on overall economic growth, which in turn could lead to a reduction in demand for our products and consequently have a material adverse effect on our businesses.

Uncertainties with respect to the PRC legal system could limit the legal protections available to you and us.

We conduct substantially all of our business through our operating subsidiary and affiliate in the PRC. Our principal operating subsidiary and controlled affiliate, Kalington Consulting and Longhai, respectively, are subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to foreign-invested enterprises. The PRC legal system is based on written statutes, and prior court decisions may be cited for reference but have limited precedential value. Since 1979, a series of new PRC laws and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to you and us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention.

You may have difficulty enforcing judgments against us.

Our principal operating subsidiary and affiliate, Kalington Consulting and Longhai, respectively, are located in the PRC. We conduct most of our current operations in the PRC, and most of our assets are located outside the United States. In addition, most of our officers and directors are nationals and residents of countries other than the United States. A substantial portion of the assets of these persons are also located outside the United States. As a result, it could be difficult for investors to effect service of process in the United States or to enforce a judgment obtained in the United States against our Chinese operations and subsidiary and/or controlled affiliate. It may also be difficult for you to enforce in U.S. courts judgments predicated on the civil liability provisions of the U.S. federal securities laws against us and our officers and directors, most of whom are not residents in the United States and the substantial majority of whose assets are located outside the United States. In addition, there is uncertainty as to whether the courts of the PRC would recognize or enforce judgments of U.S. courts. The recognition and enforcement of foreign judgments are provided for under the PRC Civil Procedures Law. Courts in China may recognize and enforce foreign judgments in accordance with the requirements of the PRC Civil Procedures Law based on treaties between China and the country where the judgment is made or on reciprocity between jurisdictions. China does not have any treaties or other arrangements that provide for the reciprocal recognition and enforcement of foreign judgments with the United States. In addition, according to the PRC Civil Procedures Law, courts in the PRC will not enforce a foreign judgment against us or our directors and officers if they decide that the judgment violates basic principles of PRC law or national sovereignty, security or the public interest. So it is uncertain whether a PRC court would enforce a judgment rendered by a court in the United States.

The PRC government exerts substantial influence over the manner in which we must conduct our business activities.

The PRC government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, import and export tariffs, environmental regulations, land use rights, property, and other matters. We believe that our operations in China are in material compliance with all applicable legal and regulatory requirements. However, the central or local governments of the jurisdictions in which we operate may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations.

Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof and could require us to divest ourselves of any interest we then hold in Chinese properties or joint ventures.

Future inflation in China may inhibit our ability to conduct business in China.

In recent years, the Chinese economy has experienced periods of rapid expansion and highly fluctuating rates of inflation. During the past ten years, the rate of inflation in China has been as high as 5.9% and as low as -0.8% . These factors have led to the adoption by the Chinese government, from time to time, of various corrective measures designed to restrict the availability of credit or regulate growth and contain inflation. High inflation may in the future cause the Chinese government to impose controls on credit and/or prices, or to take other action, which could inhibit economic activity in China, and thereby harm the market for our products and our company.

16

Restrictions on currency exchange may limit our ability to receive and use our revenues effectively.

All of our revenues are generated in RMB and any future restrictions on currency exchanges may limit our ability to use revenue generated in RMB to fund any future business activities outside China or to make dividend or other payments in U.S. dollars. Although the Chinese government introduced regulations in 1996 to allow greater convertibility of the RMB for current account transactions, significant restrictions still remain, including primarily the restriction that foreign-invested enterprises may only buy, sell or remit foreign currencies after providing valid commercial documents, at those banks in China authorized to conduct foreign exchange business. In addition, conversion of RMB for capital account items, including direct investment and loans, is subject to governmental approval in China, and companies are required to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the Chinese regulatory authorities will not impose more stringent restrictions on the convertibility of the RMB.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

The value of our common stock will be indirectly affected by the foreign exchange rate between U.S. dollars and RMB and between those currencies and other currencies in which our sales may be denominated. Appreciation or depreciation in the value of the RMB relative to the U.S. dollar would affect our financial results reported in U.S. dollar terms without giving effect to any underlying change in our business or results of operations. Fluctuations in the exchange rate will also affect the relative value of any dividend we issue that will be exchanged into U.S. dollars as well as earnings from, and the value of, any U.S. dollar- denominated investments we make in the future. Please refer to a further discussion of exchange rates in the Section titled “Foreign Currency Exchange Rates” of this report.

Since July 2005, the RMB is no longer pegged to the U.S. dollar. Although the People’s Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the RMB may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

Very limited hedging transactions are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited, and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.