Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CHINA HGS REAL ESTATE INC. | v303113_8k.htm |

China HGS Real Estate Inc. (NASDAQ: HGSH)

2 2 Forward Looking Statement CAUTIONARY STATEMENT REGARDING FORWARD - LOOKING STATEMENTS This presentation includes or incorporates by reference statements that constitute forward - looking statements within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended . These statements relate to future events or to our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance, or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward - looking statements . In some cases, you can identify forward - looking statements by the use of words such as “may,” “could,” “expect,” “intend,” “plan,” “seek,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “continue,” or the negative of these terms or other comparable terminology . You should not place undue reliance on forward - looking statements since they involve known and unknown risks, uncertainties and other factors which are, in some cases, beyond our control and which could materially affect actual results, levels of activity, performance or achievements . The forward - looking statements contained in this presentation are made only as of August 22 , 2011 and HGSH is under no obligation to revise or update these forward - looking statements .

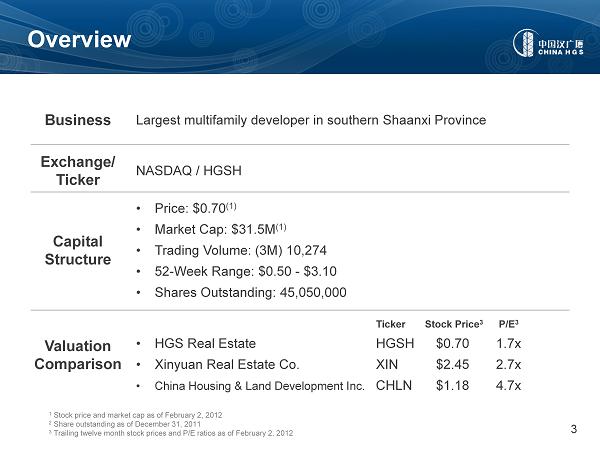

3 3 Business Largest multifamily developer in southern Shaanxi Province Exchange/ Ticker NASDAQ / HGSH Capital Structure • Price: $0.70 (1) • Market Cap: $31.5M (1) • Trading Volume: (3M) 10,274 • 52 - Week Range: $0.50 - $3.10 • Shares Outstanding: 45,050,000 Valuation Comparison Overview Ticker Stock Price 3 P/E 3 • HGS Real Estate HGSH $0.70 1.7x • Xinyuan Real Estate Co . XIN $2.45 2.7x • China Housing & Land Development Inc. CHLN $1.18 4.7x 1 Stock price and market cap as of February 2, 2012 2 Share outstanding as of December 31, 2011 3 Trailing twelve month stock prices and P/E ratios as of February 2, 2012

4 4 • Founded in 1995 with a solid track record of completed projects • Largest multifamily developer in southern Shaanxi Province • Ten - year aggregate sales of 6.7 million Sq. Ft. • Focused on Tier - III cities in central and western China • A Credit A ssociation of Shaanxi Province “ 2010 Trustworthy Enterprise ” • National Grade - I real estate certification Overview

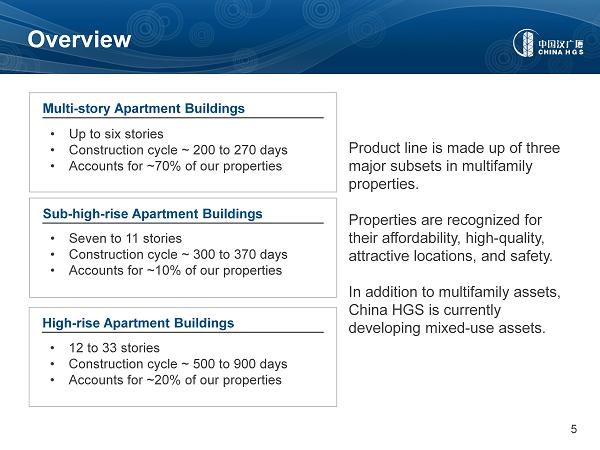

5 5 • Up to six stories • Construction cycle ~ 200 to 270 days • Accounts for ~70% of our properties Product line is made up of three major subsets in multifamily properties. Properties are recognized for their affordability, high - quality, attractive locations, and safety. In addition to multifamily assets, China HGS is currently developing mixed - use assets. Overview Multi - story Apartment Buildings Sub - high - rise Apartment Buildings • Seven to 11 stories • Construction cycle ~ 300 to 370 days • Accounts for ~10% of our properties High - rise Apartment Buildings • 12 to 33 stories • Construction cycle ~ 500 to 900 days • Accounts for ~20% of our properties

6 6 • Strong market dynamics • Scalable cost - efficient b usiness model with efficient development schedule and no long term debt • Leveraging strong b rand awareness of safety and quality • Experienced management team • Growth strategy surrounding strict cost control, product innovation and large target market Investment Highlights

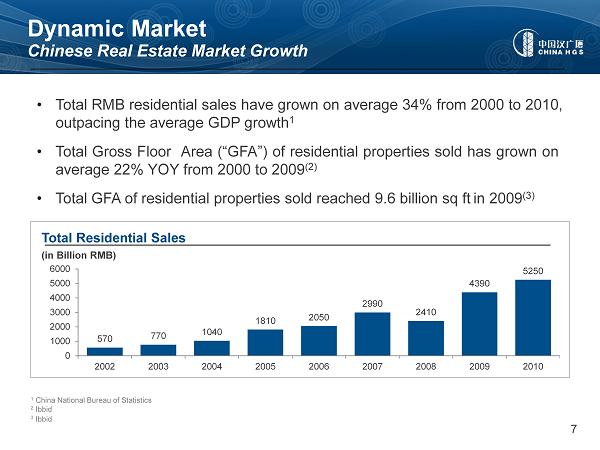

7 7 • Total RMB residential sales have grown on average 34 % from 2000 to 2010 , outpacing the average GDP growth 1 • Total Gross F loor Area (“GFA”) of residential properties sold has grown on average 22 % YOY from 2000 to 2009 ( 2 ) • Total GFA of residential properties sold reached 9 . 6 billion sq ft in 2009 ( 3 ) Total Residential Sales 570 770 1040 1810 2050 2990 2410 4390 5250 0 1000 2000 3000 4000 5000 6000 2002 2003 2004 2005 2006 2007 2008 2009 2010 Dynamic Market Chinese Real Estate Market Growth 1 China National Bureau of Statistics 2 Ibbid 3 Ibbid (in Billion RMB)

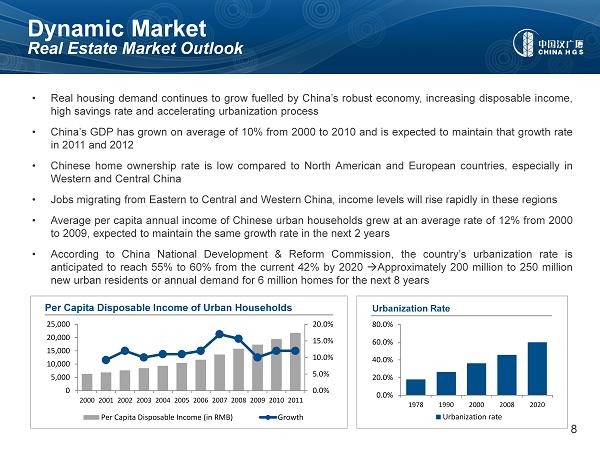

8 8 • Real housing demand continues to grow fuelled by China’s robust economy, increasing disposable income, high savings rate and accelerating urbanization process • China’s GDP has grown on average of 10 % from 2000 to 2010 and is expected to maintain that growth rate in 2011 and 2012 • Chinese home ownership rate is low compared to North American and European countries, especially in Western and Central China • Jobs migrating from Eastern to Central and Western China, income levels will rise rapidly in these regions • Average per capita annual income of Chinese urban households grew at an average rate of 12 % from 2000 to 2009 , expected to maintain the same growth rate in the next 2 years • According to China National Development & Reform Commission, the country’s urbanization rate is anticipated to reach 55 % to 60 % from the current 42 % by 2020 A pproximately 200 million to 250 million new urban residents or annual demand for 6 million homes for the next 8 years Per Capita Disposable Income of Urban Households Urbanization Rate 0.0% 20.0% 40.0% 60.0% 80.0% 1978 1990 2000 2008 2020 Urbanization rate 0.0% 5.0% 10.0% 15.0% 20.0% 0 5,000 10,000 15,000 20,000 25,000 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Per Capita Disposable Income (in RMB) Growth Dynamic Market Real Estate Market Outlook

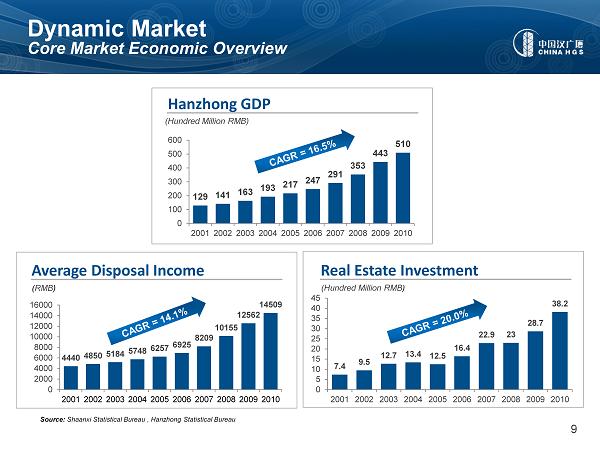

9 9 Source: Sha a nxi Statistical Bureau , Hanzhong Statistical Bureau Dynamic Market Core Market Economic Overview 4440 4850 5184 5748 6257 6925 8209 10155 12562 14509 0 2000 4000 6000 8000 10000 12000 14000 16000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Average Disposal Income ( RMB ) 129 141 163 193 217 247 291 353 443 510 0 100 200 300 400 500 600 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 (Hundred Million RMB) Hanzhong GDP 7.4 9.5 12.7 13.4 12.5 16.4 22.9 23 28.7 38.2 0 5 10 15 20 25 30 35 40 45 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 (Hundred Million RMB ) Real Estate Investment

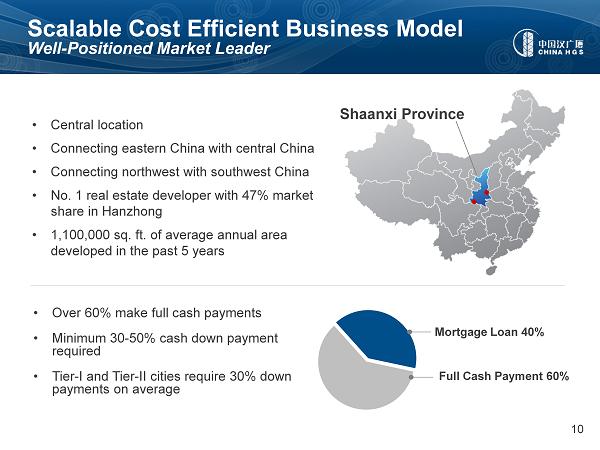

10 10 • Central location • Connecting eastern China with central China • Connecting northwest with southwest China • No . 1 real estate developer with 47% market share in Hanzhong • 1,100,000 sq. ft. of average annual area developed in the past 5 years Scalable Cost Efficient Business Model Well - Positioned Market Leader • Over 60 % make full cash payments • Minimum 30 - 50 % cash down payment required • Tier - I and Tier - II cities require 30% down payments on average Shaanxi Province Mortgage Loan 40% Full Cash Payment 60%

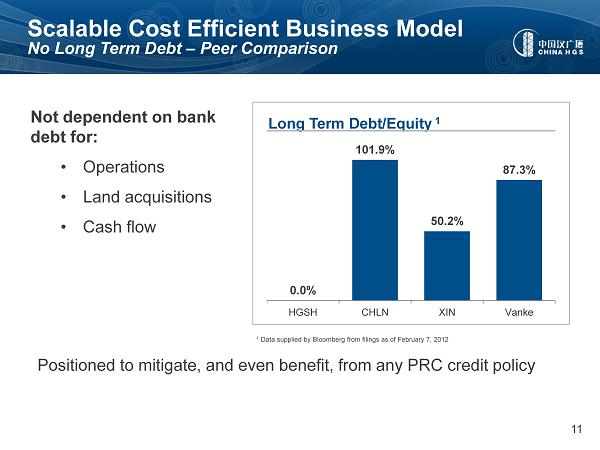

11 11 Not dependent on bank debt for: • Operations • L and acquisitions • Cash flow 1 Data supplied by Bloomberg from filings as of February 7, 2012 Positioned to mitigate, and even benefit, from any PRC credit policy Scalable Cost Efficient Business Model No Long Term Debt – Peer Comparison Long Term Debt/Equity 1 0.0% 101.9% 50.2% 87.3% HGSH CHLN XIN Vanke

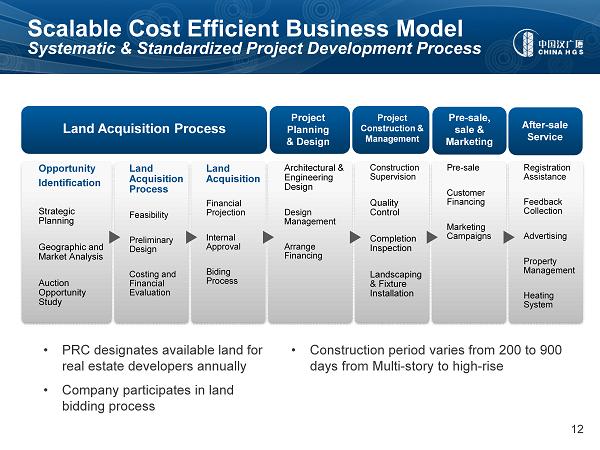

12 12 Opportunity Identification Strategic Planning Geographic and Market Analysis Auction Opportunity Study Land Acquisition Process Feasibility Preliminary Design Costing and Financial Evaluation Land Acquisition Financial Projection Internal Approval Biding Process Architectural & Engineering Design Design Management Arrange Financing Construction Supervision Quality Control Completion Inspection Landscaping & Fixture Installation Pre - sale Customer Financing Marketing Campaigns Registration Assistance Feedback Collection Advertising Property Management Heating System • PRC designates available land for real estate developers annually • Company participates in land bidding process • Construction period varies from 200 to 900 days from Multi - story to high - rise Scalable Cost Efficient Business Model Systematic & Standardized Project Development Process Project Planning & Design Land Acquisition Process Project Construction & Management After - sale Service Pre - sale, sale & Marketing

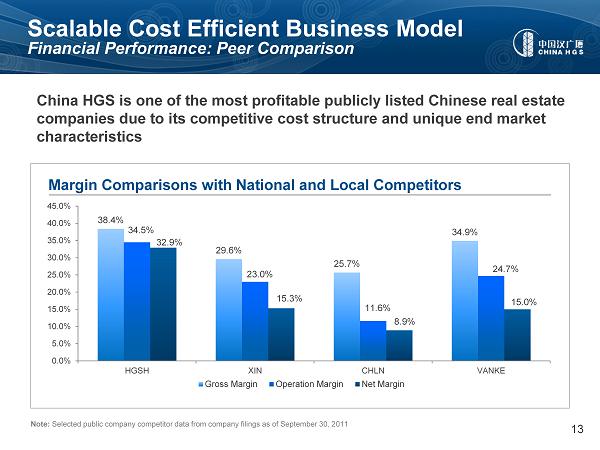

13 13 China HGS is one of the most profitable publicly listed Chinese real estate companies due to its competitive cost structure and unique end market characteristics Margin Comparisons with National and Local Competitors Note: Selected public company competitor data from company filings as of September 30, 2011 38.4% 29.6% 25.7% 34.9% 34.5% 23.0% 11.6% 24.7% 32.9% 15.3% 8.9% 15.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% HGSH XIN CHLN VANKE Gross Margin Operation Margin Net Margin Scalable Cost Efficient Business Model Financial Performance: Peer Comparison

14 14 Strict Quality Control Throughout the Entire Development Process • Disciplined bidding process for selecting partners • Developed systematic quality control process to monitor our property’s quality throughout all stages • Senior management closely supervises management and planning process Long Term Collaboration with Design, Material and Construction Vendors • Engages leading property design companies to provide modern and high - quality designs for our projects • Long - term cooperation with selective vendors to guarantee quality as well as competitive price • Construction contracts include standard quality warranties and penalty provisions Brand Name Recognition • Recognized as “2009 advanced taxpayer" by Hanzhong Municipal Government • “2010 Trustworthy Enterprise” Credit Association of Shaanxi Province • “2010 advanced taxpayer” by Hantai District Government Strong Brand Awareness Recent Awards

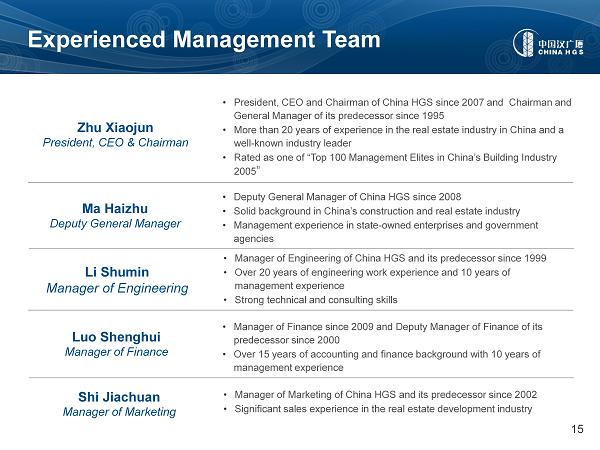

15 15 Zhu Xiaojun President, CEO & Chairman • President, CEO and Chairman of China HGS since 2007 and Chairman and General Manager of its predecessor since 1995 • More than 20 years of experience in the real estate industry in China and a well - known industry leader • Rated as one of “Top 100 Management Elites in China’s Building Industry 2005 ” Ma Haizhu Deputy General Manager • Deputy General Manager of China HGS since 2008 • Solid background in China’s construction and real estate industry • Management experience in state - owned enterprises and government agencies Li Shumin Manager of Engineering • Manager of Engineering of China HGS and its predecessor since 1999 • Over 20 years of engineering work experience and 10 years of management experience • Strong technical and consulting skills Luo Shenghui Manager of Finance • Manager of Finance since 2009 and Deputy Manager of Finance of its predecessor since 2000 • Over 15 years of accounting and finance background with 10 years of management experience Shi Jiachuan Manager of Marketing • Manager of Marketing of China HGS and its predecessor since 2002 • Significant sales experience in the real estate development industry Experienced Management Team

16 16 Effectively Control Land Acquisition Cost Stable Construction Material and Building Cost • With over 15 years of experience, we have established long - term relationships with key material suppliers and construction vendors • Our scale and creditworthiness also allow us to negotiate better rates • Favorable treatment offered by local government in terms of land acquisition fees, levies and taxes to compensate and encourage our infrastructure investments in the communities projects we develop High Pre - sale Rate • About 70% of houses are pre - sold by sales center near the site with several sales representatives • Group sales made to officers from government agencies, school teacher and doctors Fast Development Cycles • ~ 70% of our property products have construction period less than 300 days vs. 3 years for typical developers in Tier - I and Tier - II cities • Significantly lower capital cost and higher return to capital Growth Strategy Effective Cost Management

17 Current and Completed Projects

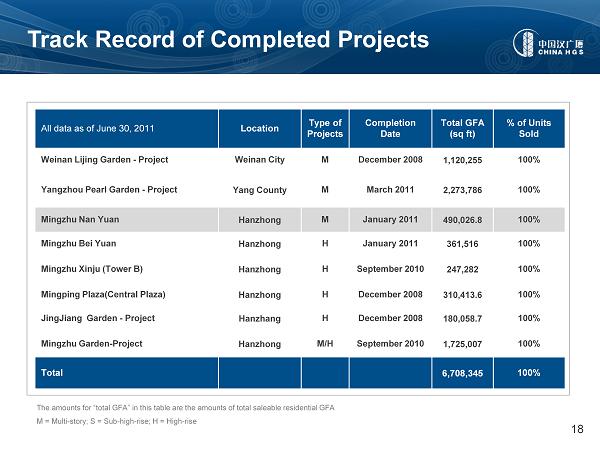

18 18 All data as of June 30, 2011 Location Type of Projects Completion Date Total GFA (sq ft) % of Units Sold Weinan Lijing Garden - Project Weinan City M December 2008 1,120,255 100% Yangzhou Pearl Garden - Project Yang County M March 2011 2,273,786 100% Mingzhu Nan Yuan Hanzhong M January 2011 490,026.8 100% Mingzhu Bei Yuan Hanzhong H January 2011 361,516 100% Mingzhu Xinju (Tower B) Hanzhong H September 2010 247,282 100% Mingping Plaza(Central Plaza) Hanzhong H December 2008 310,413.6 100% JingJiang Garden - Project Hanzhang H December 2008 180,058.7 100% Mingzhu Garden - Project Hanzhong M/H September 2010 1,725,007 100% Total 6,708,345 100% Track Record of Completed Projects The amounts for “total GFA” in this table are the amounts of total saleable residential GFA M = Multi - story; S = Sub - high - rise; H = High - rise

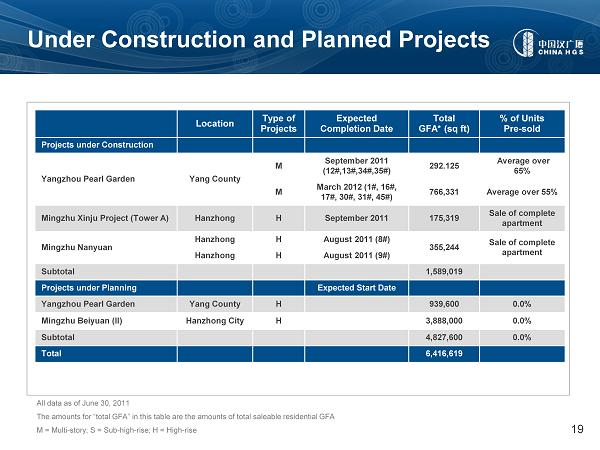

19 19 Location Type of Projects Expected Completion Date Total GFA* (sq ft) % of Units Pre - sold Projects under Construction Yangzhou Pearl Garden Yang County M September 2011 (12#,13#,34#,35#) 292.125 Average over 65% M March 2012 (1#, 16#, 17#, 30#, 31#, 45#) 766,331 Average over 55% Mingzhu Xinju Project (Tower A) Hanzhong H September 2011 175,319 Sale of complete apartment Mingzhu Nanyuan Hanzhong H August 2011 (8#) 355,244 Sale of complete apartment Hanzhong H August 2011 (9#) Subtotal 1,589,019 Projects under Planning Expected Start Date Yangzhou Pearl Garden Yang County H 939,600 0.0% Mingzhu Beiyuan (II) Hanzhong City H 3,888,000 0.0% Subtotal 4,827,600 0.0% Total 6,416,619 All data as of June 30, 2011 The amounts for “total GFA” in this table are the amounts of total saleable residential GFA M = Multi - story; S = Sub - high - rise; H = High - rise Under Construction and Planned Projects

20 Financial Summary Mingzhu Nanyuan (under construction)

21 21 $17.2 $28.5 $ 47. 3 $56.9 0 10 20 30 40 50 2008 2009 2010 2011 $US Million Strong Revenue Growth

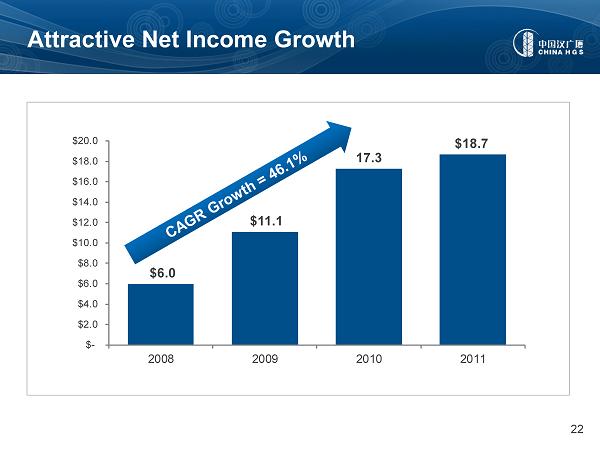

22 22 $6.0 $11.1 17.3 $18.7 $- $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0 $16.0 $18.0 $20.0 2008 2009 2010 2011 Attractive Net Income Growth

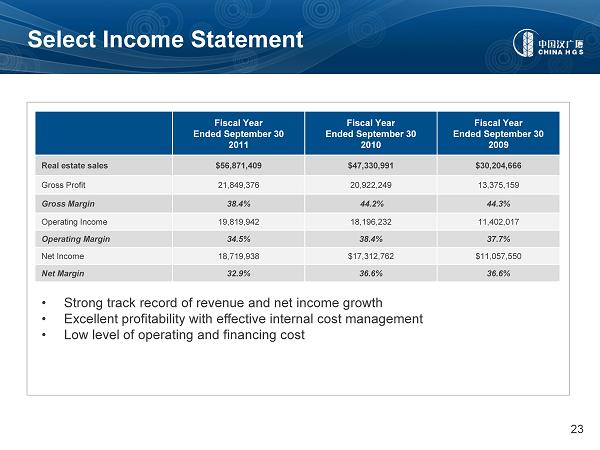

23 23 Fiscal Year Ended September 30 2011 Fiscal Year Ended September 30 2010 Fiscal Year Ended September 30 2009 Real estate sales $56,871,409 $47,330,991 $30,204,666 Gross Profit 21,849,376 20,922,249 13,375,159 Gross Margin 38.4% 44.2% 44.3% Operating Income 19,819,942 18,196,232 11,402,017 Operating Margin 34.5% 38.4% 37.7% Net Income 18,719,938 $17,312,762 $11,057,550 Net Margin 32.9% 36.6% 36.6% Select Income Statement • Strong track record of revenue and net income growth • Excellent profitability with effective internal cost management • Low level of operating and financing cost

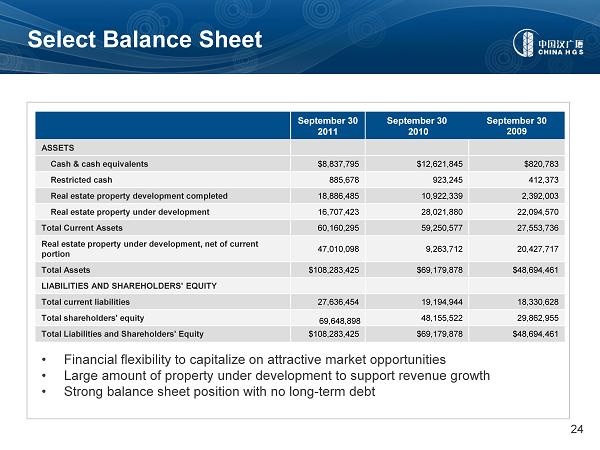

24 24 September 30 2011 September 30 2010 September 30 2009 ASSETS Cash & cash equivalents $8,837,795 $12,621,845 $820,783 Restricted cash 885,678 923,245 412,373 Real estate property development completed 18,886,485 10,922,339 2,392,003 Real estate property under development 16,707,423 28,021,880 22,094,570 Total Current Assets 60,160,295 59,250,577 27,553,736 Real estate property under development, net of current portion 47,010,098 9,263,712 20,427,717 Total Assets $108,283,425 $69,179,878 $48,694,461 LIABILITIES AND SHAREHOLDERS' EQUITY Total current liabilities 27,636,454 19,194,944 18,330,628 Total shareholders' equity 69,648,898 48,155,522 29,862,955 Total Liabilities and Shareholders' Equity $108,283,425 $69,179,878 $48,694,461 Select Balance Sheet • Financial flexibility to capitalize on attractive market opportunities • Large amount of property under development to support revenue growth • Strong balance sheet position with no long - term debt

25 25 • Strong market dynamics • Scalable cost - efficient business model with efficient development schedule and no long term debt • Leveraging strong brand awareness of safety and quality • Experienced management team • Growth strategy surrounding strict cost control, product innovation and large target market Conclusion

26 26 Company Contact China HGS Real Estate Inc. Mr. Ran Xiong, President Finance China HGS Real Estate Inc. Tel: +86 - 916 - 2622612 E - mail: xr968@163.net Independent Auditor Friedman LLP 1700 Broadway New York, NY 10019 Legal Counsel Loeb & Loeb LLP 345 Park Ave, Suite 18 New York, NY 10154 IR Contact RedChip Companies, Inc. Jon Cunningham Tel: 800 - 733 - 2447, ext. 107 Tel: 407 - 644 - 4256, ext. 107 E - mail: jon@redchip.com Contact Information