Attached files

| file | filename |

|---|---|

| EX-31 - CHINA HGS REAL ESTATE INC. | exhibit31.htm |

| EX-21 - CHINA HGS REAL ESTATE INC. | exhibit21.htm |

| EX-32 - CHINA HGS REAL ESTATE INC. | exhibit32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x |

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2009

|

o |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File No. 000-49687

CHINA HGS REAL ESTATE INC.

(Name of small business issuer in its charter)

|

Florida |

33-0961490 |

|

(State or Other Jurisdiction of Incorporation) |

(I.R.S. Employer Identification Number) |

6 Xinghan Road, 19th Floor, Hanzhong City

Shaanxi Province, PRC 723000

(Address of principal executive offices) (zip code)

(212) 232-0120

(Registrant's telephone number, including area code)

|

Securities registered under Section 12(b) of the Exchange Act: | |

|

Title of each class registered: |

Name of each exchange on which registered: |

|

None |

None |

|

Securities registered under Section 12(g) of the Exchange Act: | |

|

Common Stock, par value $0.001

(Title of class) | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference Part III of this Form 10-K or any amendment

to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

o |

Accelerated filer |

o | |

|

Non-accelerated filer

(Do not check if a smaller reporting company) |

o |

Smaller reporting company |

x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the registrant’s voting common stock held by non-affiliates as of December 24, 2009 based upon the closing price reported for such date on the OTC Bulletin Board was US $12,886,500.

As of December 24, 2009, the registrant had 45,050,000 shares of its common stock outstanding.

Documents Incorporated by Reference: None.

TABLE OF CONTENTS

|

PAGE | ||||

|

PART I |

||||

|

ITEM 1. |

Business |

3 | ||

|

ITEM 1A. |

Risk Factors |

19 | ||

|

ITEM 2. |

Properties |

29 | ||

|

ITEM 3. |

Legal Proceedings |

29 | ||

|

ITEM 4. |

Submission of Matters to a Vote of Security Holders |

29 | ||

|

PART II |

||||

|

ITEM 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

30 | ||

|

ITEM 6. |

Selected Financial Data |

31 | ||

|

ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operation |

32 | ||

|

ITEM 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

48 | ||

|

ITEM 8. |

Financial Statements and Supplementary Data |

F-1-F-27 | ||

|

ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

49 | ||

|

ITEM 9A(T). |

Controls and Procedures |

49 | ||

|

PART III |

||||

|

ITEM 10. |

Directors, Executive Officers and Corporate Governance |

52 | ||

|

ITEM 11. |

Executive Compensation |

53 | ||

|

ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

55 | ||

|

ITEM 13. |

Certain Relationships and Related Transactions |

55 | ||

|

ITEM 14. |

Principal Accounting Fees and Services |

56 | ||

|

PART IV |

||||

|

ITEM 15. |

Exhibits, Financial Statement Schedules |

57 | ||

|

SIGNATURES |

58 |

2

PART I

ITEM 1. BUSINESS

Our Organization

China HGS Real Estate Inc. (the “Company” or “China HGS”), formerly known as China Agro Sciences Corp., is a corporation organized under the laws of the State of Florida. We were incorporated under the name M-GAB Development Corporation in March 2001. From inception through early 2003, our business

was the development, marketing, and distribution of an interactive travel brochure. On May 16, 2003, we filed an election to be treated as a business development company (“BDC”) under the Investment Company Act of 1940 (the “1940 Act”), which became effective on the date of filing. As a BDC we never made any investments into eligible portfolio companies.

On March 17, 2006, China Agro Sciences Corp., a Florida corporation formerly known as M-GAB Development Corporation (hereinafter “China Agro”) entered into an Agreement and Plan of Merger (the “Agreement”) with Dalian Holding Corp., a Florida corporation (formerly known as China Agro Sciences Corp.) (“DHC”). This

transaction closed on May 1, 2006, at which time, in accordance with the Agreement, DHC merged with DaLian Acquisition Corp, a Florida corporation that was our wholly-owned subsidiary (“DaLian”) (the “Merger”). As a result of the Merger, DaLian merged into DHC, with DHC remaining as the surviving entity and our wholly-owned subsidiary, DaLian, ceased to exist, and we issued 13,449,488 shares of our common stock to the former shareholders of DHC.

Prior to DaLian’s merger with DHC, DHC had acquired all the outstanding common stock of Ye Shun International (“Ye Shun”), a company that owns all the outstanding common stock of DaLian Runze Chemurgy Co., Ltd. (“Runze”). In the transaction in which DHC acquired all the outstanding common stock of Ye

Shun, Ye Shun was determined to be the accounting acquirer. Ye Shun is a Hong Kong registered enterprise. Runze is classified by the Chinese government as an enterprise entity with 100% of its capital coming from Hong Kong. As a result of the Merger, on April 28, 2006, we filed a Form N-54C and terminated our status as a business development company and, through our wholly-owned subsidiary, commenced operations, specializing in the sale and distribution of low toxic pesticides

and herbicides, and consequently ceased being a development stage company. Our only operations are conducted through our wholly-owned subsidiary, which controls the assets of Runze.

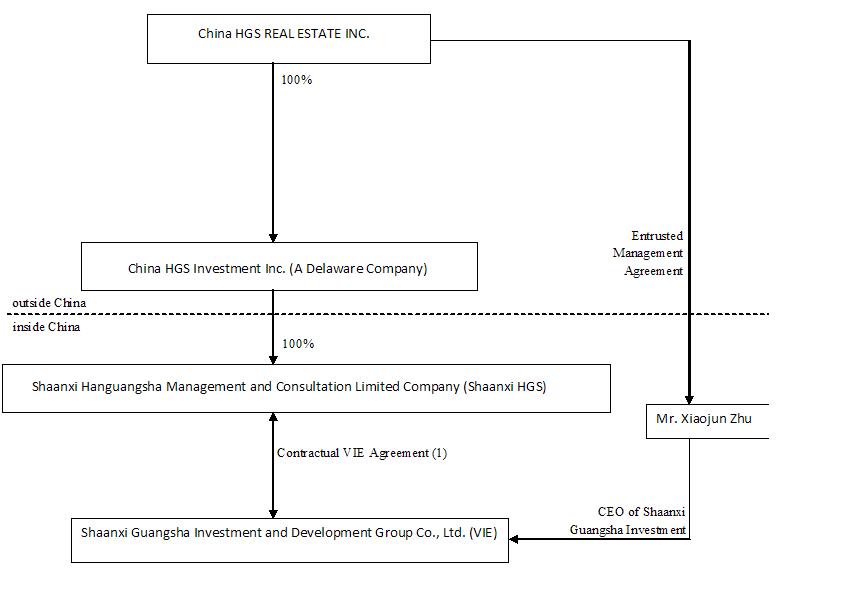

On August 21, 2009, the Company entered into a Share Exchange Agreement (“Share Exchange”) by and among the Company, China HGS Investment Inc. (“HGS Investment”), a corporation formed under the laws of the State of Delaware, and Rising Pilot, Inc., a British Virgin Island business company which owns 100% issued and

outstanding capital stock of HGS Investment (the “HGS Shareholder”). The closing of the Share Exchange transaction occurred on August 31, 2009.

Pursuant to the Share Exchange Agreement, the HGS Shareholder transferred and assigned to the Company all of the issued and outstanding capital stock of HGS to exchange for the issuance of a total of 14,000,000 shares of the Company’s common stock with $0.001 par value. As a result of this Share Exchange, HGS Investment

becomes a wholly-owned subsidiary of the Company.

In addition, as a part of the Share Exchange transaction, the Company entered into an entrusted management agreement (the “Entrusted Management Agreement”) with the management of Shaanxi Guangsha Investment and Development Group Co., Ltd. (“Guangsha”) and issued to Mr. Zhu Xiaojun, CEO of Guangsha and his management

team an aggregate of 25,000,000 shares of common stock of the Company.

Prior to and in conjunction with the consummation of the Share Exchange, the Company also entered into certain purchase and sale agreement with Mr. Zhengquan Wang, the Company’s CEO prior to the close of the Share Exchange, to spin out the business and operations of Dalian Holding Corp. (“Dalian Holding”), a Florida corporation

and a wholly-owned subsidiary of the Company (the “Spin-Out”), including substantially all the assets and liabilities of Dalian Holding (the “Legacy Business”). Pursuant to such agreement, Mr. Wang shall return 14,000,000 shares of the Company’s common stock within ninety (90) days of the Closing of the Share Exchange for the exchange of current Dalian Holding assets and assume all the liabilities of Dalian Holding relating to the Legacy Business, and the Company shall be released

from any and all claims whatsoever with regard to such liabilities, whether such claim is known or unknown to Dalian Holding on the date hereof. Prior to the Share Exchange, on August 29, 2009, the Company also completed the spin-off of all its assets and liabilities to Dalian Holding Corp. so the only material asset of the Company following the Share Exchange is the ownership of HGS Investment.

As a result of the Share Exchange transaction, the shareholders of Guangsha now own the majority of the equity in the Company. In addition, the original officers and directors of the Company resigned from their positions and new directors and officers affiliated with Guangsha were appointed ten days after the notice pursuant to Rule 14f-1

had been mailed to the shareholders of record.

3

The transaction has been accounted for as a reverse merger under the purchase method of accounting since there has been a change of control. Accordingly, HGS Investment and its subsidiaries will be treated as the continuing entity for accounting purposes.

HGS Investment, Inc. is a holding company incorporated under the law of the State of Delaware on July 17, 2008. China HGS owns 100% of the equity interest of Shaanxi HGS Management and Consulting Co., Ltd. (“Shaanxi HGS”), a wholly foreign-owned entity incorporated under the laws of the People’s Republic of China (“PRC”

or “China”) on June 3, 2009.

China HGS does not conduct any substantive operations of its own. Instead, through its subsidiary, Shaanxi HGS, it had entered certain exclusive contractual agreements with Shaanxi Guangsha Investment and Development Group Co., Ltd. (“Guangsha”), a company incorporated in Hanzhong City, Shaanxi Province, China in November 2007.

Pursuant to these agreements, Shaanxi HGS is obligated to absorb a majority of the risk of loss from Guangsha’s activities and entitles it to receive a majority of its expected residual returns. In addition, Guangsha’s shareholders have pledged their equity interest in Guangsha to Shaanxi HGS, irrevocably granted Shaanxi HGS an exclusive option to purchase, to the extent permitted under PRC Law, all or part of the equity interests in Guangsha and agreed to entrust all the rights to exercise their

voting power to the person(s) appointed by Shaanxi HGS. Through these contractual arrangements, the Company and Shaanxi HGS hold all the variable interests of Guangsha, and the Company and Shaanxi HGS have been determined to be the most closely associated with Guangsha. Therefore, our Company is the primary beneficiary of Guangsha.

Based on these contractual arrangements, we believe that Guangsha should be considered as Variable Interest Entity (“VIE”) under ASC 810 “Consolidation of Variable Interest Entities, an Interpretation of ARB No. 51”, because the equity investors in Guangsha no longer have the characteristics of a controlling financial

interest, and the Company through Shaanxi HGS is the primary beneficiary of Guangsha. Accordingly, management believes that Guangsha should be consolidated under ASC 810.

Our Company, along with our subsidiaries and VIE, is now engaging in real estate development, primarily in the construction and sale of residential apartments, car parks as well as commercial properties.

Shaanxi Guangsha Investment and Development Group Co., Ltd.

Shaanxi Guangsha Investment was organized in August 1995 as a liability limited company under the laws of The People’s Republic of China. Shaanxi Guangsha Investment is headquartered in city of Hanzhong, Shaanxi Province. Due to rapid growth of the business, the shareholders of Shaanxi Guangsha Investment have boosted its

registered capital twice, once in 2000, from the original registered capital of RMB 2.1 million Yuan (approximately US$0.2 million) up to RMB 30 million Yuan (approximately US$3.6 million) and, again in 2008 to RMB 130 million Yuan (approximately US$17.6 million). As the business expands, Shaanxi Guangsha Investment has set up two additional branch offices separately in Weinan, a municipality county of Shaanxi Province, and Yang county of Hanzhong, in order to conduct and facilitate the project developments in

these sites with its headquarter office located at 6 Xinghan Road, 19th Floor, Hanzhong City, Shaanxi Province, in northwestern China. Shaanxi Guangsha Investment is engaged in developing large scale and high quality commercial and residential projects, which typically consist of multi-functional buildings that include multi-layer apartment buildings and office buildings, sub-high-rise apartment buildings or high-rise buildings.

Shaanxi Guangsha Investment also develops small scale commercial and residential properties. Shaanxi Guangsha Investment is aiming at providing middle-income consumers with a comfortable and convenient community life. In addition, it also provides property management as an auxiliary service to its residents. Shaanxi Guangsha Investment

acquires development sites primarily through public auctions of government land. This acquisition method allows Shaanxi Guangsha Investment to obtain unencumbered land use rights to unoccupied land without the need for additional work, re-settlement or protracted legal processes to obtain title. As a result, Shaanxi Guangsha Investment is able to commence construction relatively quick after a site for development is acquired.

4

Our corporate structure is set forth below:

(1) Agreements that provide us with effective control over Shaanxi Guangsha Investment and Development Group Co., Ltd. or the VIE, include a business operations agreement, an exclusive managerial consulting services agreement, an equity pledge agreement, a voting proxy agreement and an exclusive acquiring letter.

5

Business Overview

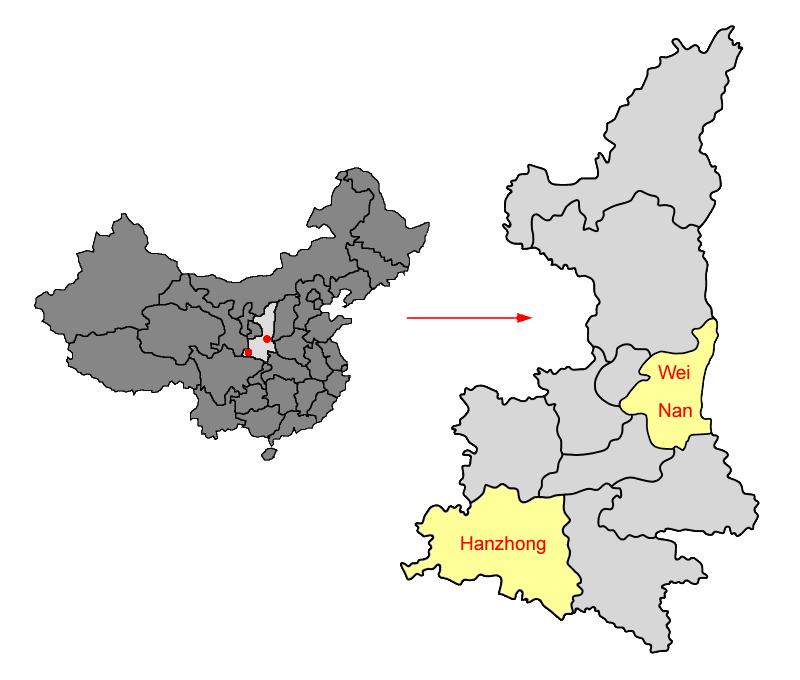

We conduct substantially all of our business through Shaanxi Guangsha Investment, located in Hanzhong City, Shaanxi Province. Shaanxi Guangsha Investment was founded by Mr. Xiaojun Zhu, our Chairman and Chief Executive Officer, and commenced operations in 1995 in Hanzhong, a prefecture-level city of Shaanxi Province. Since the initiation

of our business, we keep focusing on expanding our business in certain Tier II cities in China which we strategically selected based on a set of criteria. Our selection criteria includes population and urbanization growth rate, general economic condition and growth rate, income and purchasing power of resident consumers, anticipated demand for private residential properties, availability of future land supply and land prices and governmental urban planning and development policies. As of December 31, 2008,

we have established operations in two Tier II cities and one county in Hanzhong, Shaanxi Province, comprising of downtown area and west ring road in city of Hanzhong, city of Weinan, a municipality in Shaanxi Province, and Yang county.

Shaanxi Guangsha Investment has become a fast-growing residential real estate developer that focuses on Tier II cities in China. We utilize a standardized and scalable model that emphasizes rapid asset turnover, efficient capital management and strict cost control. We are currently ranked No.1 among all property developers in city of Hanzhong

in terms of market shares and contracted sales of residential units for the years of 2007 and 2008, according to statistics prepared by the Bureau of Real Estate Management in Hanzhong. Since 2001, we have planned to expand into strategically selected Tier II cities and even some smaller counties with real estate development potential in Shaanxi Province, and expect to benefit from rising residential housing demand as a result of increasing income levels of consumers and growing populations.

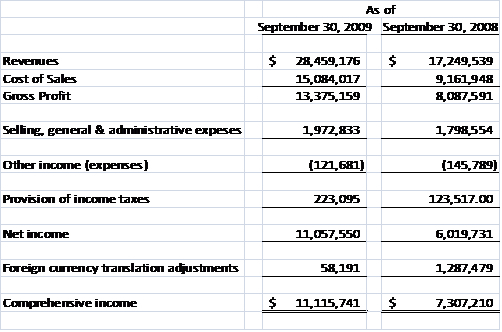

As of now, there are three projects under construction and planning with a total GFA (Gross Floor Area) of 412,285 square meters. Our Weinan project was completed in June 2008, with a total GFA of 103,727 square meters, and all units of Weinan Projects were sold as of December 31, 2008. For the past two years ended September 30, 2008 and

2009, our revenues were approximately $17.2 million and $28.4 million, respectively, representing an increase of 64.98% from 2008 to 2009. Our net income for each of those two years was $6.02 million and $11.06 million, respectively, representing an increase of 83.69% from 2008 to 2009.

We intend to continue our expansion into additional selected Tier II cities and counties as suitable opportunities arise. We will expand to more selected target Tier II cities including cities in Sichuan Province and other Tier II cities in Shaanxi Province which we are surveying for expansion in the near future. The following map illustrates

the geographic locations of our current operations,

6

Real Estate Industry Overview

General

Since early 2000s, the real estate industry in China has been transitioning from an arranged system controlled by the PRC government to a more market-oriented system. At the present, although the Chinese government still owns all urban land in China, the land use rights with terms up to 70 years can be granted to, and owned or leased by,

private individuals and companies. A large and active market in the private sector has developed for sales and transfers of land use rights which were initially granted by the Chinese government. All property units built on such land belong to private developers for the term of period indicated. The recent transition in terms of real estate industry structure in China has also fostered the development of real estate-related businesses, such as property development, property management and real estate agencies.

The real estate industry in China, like elsewhere, is highly influenced by the domestic macroeconomic environment. The significant growth of the Chinese economy during the past decade, has led to a significant expansion of its real estate industry. This expansion has been supported by other factors, including increasing urbanization, growing

personal affluence, as well as the emergence of the mortgage lending market. The following table sets forth selected statistics for the overall real estate industry in mainland China for the periods indicated.

Source: China Statistic Year Book (all government data is based on calendar year)

Under a recently-enacted PRC Property Rights Law, which became effective on October 1, 2007, the term of the land use rights for residential land may be automatically renewed upon expiration. We expect this new law to encourage further growth in the PRC residential property market.

7

Increasing Urbanization in China

The urban population in China has grown significantly in the past 10 years, creating higher demand for housing in many cities. The following table sets forth China’s urban population, total population and urbanization rates for periods indicated:

|

Source: |

China Statistical Yearbook (all government data is based on calendar year) |

The Real Estate Property Market in China

The following table sets forth selected statistics regarding the real estate property market in China for the periods indicated.

Source: China Statistical Yearbook (all government data is based on calendar year)

In the years of 2008 and 2009, the city of Hanzhong has won such titles as Sanitory City, Garden City and Civilized City. Hanzhong is going to strengthen the position of tourism in its economic and social development by making the most of its advantage as a historical and cultural city. The following sets forth an overview of Hanzhong and

its surrounding areas, the Tier II city and counties in which we operate our business:

8

Hanzhong and surrounding areas, Shaanxi Province

Hanzhong is located in the southwestern part of the Shaanxi province, in the center of the Hanzhong Basin, on the Han River, near the Sichuan border. According to the China City Statistical Yearbook, Hanzhong had a population of about 4.1 million as of September 30, 2009. The table below sets forth selected economic statistics

and real estate industry data during the periods indicated.

|

Source: |

China City Statistical Yearbook; China Real Estate Statistics Yearbook; Shaanxi Statistical Yearbook (all government data is based on calendar year) |

Recent Government Policies

The PRC government has announced on several occasions in recent years that its policy towards the development of the real estate industry is to promote healthy and sustainable growth, which includes encouraging the development of more low-to-medium priced housings. Since 2004, amidst growing concerns of overheating in the real estate industry,

particularly in Tier I cities where average property prices have risen by more than 20% through 2001 to 2005, the PRC government has introduced a series of measures intended to slow growth in both property demand and supply and discourage speculation in the residential property market.

Land Allocation and Real Estate Development

In May 2005, the Ministry of Construction and other relevant Chinese government authorities jointly issued the Notice Regarding Stabilizing Property Prices, which was followed by a set of implementation measures, including:

|

● |

the imposition of a charge on land that remains undeveloped for one year from the commencement date specified in the relevant government land grant contract; |

|

● |

the cancellation of land use rights for land that remains undeveloped for two years from the specified commencement date; |

|

● |

the revocation of approval for projects that fail to comply with relevant planning permits; |

|

● |

a ban on the grant of land use rights for the construction of villas; and |

|

● |

a restriction on the grant of land use rights for the construction of other types of luxury residential properties. A restriction on the grant of land use rights for the construction of other types of luxury residential |

9

Pre-Sales and Sales

In real estate development business, it is a convention that developers start to market and offer their properties before the construction are completed. Like other developers, we pre-sell properties prior to the completion of the construction. Under PRC pre-sales regulations, property developers must satisfy specific conditions before

they can pre-sell their properties that are under construction. These mandatory conditions include:

|

· |

the land premium must have been paid in full; |

|

· |

the land use rights certificate, the construction site planning permit, the construction work planning permit and the construction permit must have been obtained; |

|

· |

at least 25% of the total project development cost must have been incurred; |

|

· |

the progress and the expected completion and delivery date of the construction must be fixed; |

|

· |

the pre-sale permit must have been obtained; and |

|

· |

the completion of certain milestones in the construction processes must be specified by the local government authorities. |

These mandatory conditions are designed to require a certain level of capital expenditure and substantial progress in project construction before the commencement of pre-sales. Generally, the local governments also require developers and property purchasers to have standard pre-sale contracts prepared under the auspices of the government.

Developers are required to file all pre-sale contracts with local land bureaus and real estate administrations after entering into such contracts.

After-sale Services and Delivery

We assist customers in arranging for and providing information related to financing. We also assist our customers in various title registration procedures related to their properties, and we have set up an ownership certificate team to assist purchasers to obtain their property ownership certificates. We offer various communication channels

to customers to facilitate customer feedback collection. We also cooperate with property management companies that manage our properties and ancillary facilities, to handle customer feedback.

We endeavor to deliver the units to our customers on a timely basis. We closely monitor the progress of construction of our property projects and conduct pre-delivery property inspections to ensure timely delivery. The time frame for delivery is set out in the sale and purchase agreements entered into with our customers, and we are subject

to penalty payments to the purchasers for any delay in delivery caused by us. Once a property development has been completed, has passed the requisite government inspections and is ready for delivery, we will notify our customers and hand over keys and possession of the properties.

10

Marketing and Distribution Channel

As of September 2009, we maintain a marketing and sales force for our development projects with 60 personnel specializing in marketing and sales. We also train and use outside real estate agents to market and increase the public awareness of our products, and spread the acceptance and influence of our brand. However, we still primarily

let our own sales force represents our brand and project rather than rely on third party brokers or agents, for the reason that we believe our own dedicated sales representatives are better motivated to serve our customers and to control our property pricing and selling expenses.

Our marketing and sales teams work closely with each other in order to determine the appropriate advertising and selling plans for a particular project. We develop public awareness through our marketing and advertising efforts and also referrals from our satisfied customers. We utilize our customer relationship management system to track

customer profiles to forecast future individual requirements and general demand for our products. This allows us to have real-time information on the status of individual customer transactions and the vacancy of product types for each project, and to anticipate the product preferences of current and future customers. We mainly develop customer awareness through advertising.

As for advertisement, we use various advertising media to market our property developments, including newspapers, magazines, television, radio, e-marketing and outdoor billboards. We also participate in real estate exhibitions to enhance our brand name and promote our property developments.

The majority of our customers purchase our properties using mortgage financing. Under current PRC law, the minimum down payment is 30% of the total purchase price for the purchase of the first self-use residential unit with total GFA of 90 square meters or more on all existing units and those yet to be completed, and a down payment of 20%

on the first residential units for self use with total GFA of under 90 square meters. The loan-to-value of the mortgage loan is also subject to change according to the economic policies of the central and local governments and banks in China of where the applicants apply for the mortgage loan.

A typical sales transaction usually consists of three steps. First, the customer pays a deposit to us. Within seven days after paying the deposit, the customer will sign a purchase contract with us and make down payment to us in cash. After making the down payment, the customer arranges for a mortgage loan for the balance of the purchase

price. Once the loan is approved, the mortgage loan proceeds are paid to us directly by the bank. Finally, we deliver the property to the customer. Legal title, as evidenced by a property ownership certificate issued by local land and construction bureaus, will be delivered to the customer in 12 months.

As is customary in the property industry in China, we provide guarantees to mortgagee banks in respect of the mortgage loans provided to the purchasers of our properties up until completion of the registration of the mortgage with the relevant mortgage registration authorities. Guarantees for mortgages on residential properties are typically

discharged when the individual property ownership certificates are issued. In our experience, the issuance of the individual property ownership certificates typically takes six to 12 months, so our mortgage guarantees typically remain outstanding for up to 12 months after we deliver the underlying property.

Our Markets

We currently operate in three local markets in Shaanxi Province — downtown area of Hanzhong, city of Weinan, and Yang county in city of Hanzhong.

11

The following table sets forth our projects and the total GFA in each location indicated as of September 2009

|

Yang County |

Nan Dajie |

Mingzhu Real Estate | ||

|

Properties under construction |

163,566 |

42,476 |

66,504 | |

|

Properties under planning |

113,034 |

N/A |

26,705 | |

|

Completed projects |

34,348 |

N/A |

28,666 | |

|

Total number of projects |

3 |

2 |

3 | |

|

Total GFA (m2) |

310,948 |

42,476 |

121,875 |

(1) The amounts for ‘‘total GFA’’ in this table and elsewhere in this statement are the amounts of total saleable residential GFA and are derived on the following basis:

|

· |

for properties that are sold, the stated GFA is based on the sales contracts relating to such property; |

|

· |

for unsold properties that are completed or under construction, the stated GFA is calculated based on the detailed construction blueprint and the calculation method approved by the PRC government for saleable GFA, after necessary adjustments; and |

|

· |

for properties that are under planning, the stated GFA is based on the land grant contract and our internal projection. |

We intend to seek attractive opportunities to expand into additional Tier II cities and counties. Our selections are based on certain criteria, including economic growth, per capita income, population, urbanization rate as well as availability of suitable land supply and local residential property market conditions.

Suppliers

In China, the supply of land is controlled by the government. Generally, there are two ways the Company usually applies to acquire the land use right.

|

· |

Purchase by auction held by the Land Consolidation and Rehabilitation Center; |

|

· |

Purchase by auction held by court under bankruptcy proceedings; |

In 2005, the company acquired the land of a bankrupted company, Weinan Chemical Company which covers an area of 80 acres. After the acquisition, the company started the construction of Lijing Garden Projects, and finished all 3 projects of Lijing Garden in June 2008. In May 2008, the company successfully acquired a land covering 236 acres

through bidding on an auction held by the local Land Consolidation and Rehabilitation Center of Yang County. After the acquisition, the company started the construction of Yangzhou Garden Projects on the acquired land, and as of September 30, 2009 and December 26, 2009, the first and second projects of Yangzhou Garden were already finished, while the third project of Yangzhou Garden was still under construction and expect to be completed next year.

12

In July 2008, the company acquired the land of another bankrupted company, Hanzhong Energy Company which covers an area of 30 acres in city of Hanzhong. After the acquisition, the company started the construction of Qinju Garden Projects on the acquired land, and as of September 30, 2009, all projects of Qinju Garden were still under

construction. In 2009, the company successfully acquired another partial of land covering 180 acres through bidding on an auction held by the local Land Consolidation and Rehabilitation Center of Hanzhong City. After the acquisition, the company started the construction of Mingzhu Garden Projects on the acquired land, and as of September 30, 2009, all projects of Mingzhu Garden were still under construction.

All such purchases of land are required to be reported to and authorized by the Xi’an Bureau of Land and Natural Resources. As to the real estate project design and construction services, the Company typically selects the lowest-cost provider based on quality ensured through an open bidding process. Such service providers are numerous

in China and the Company foresees no difficulties in securing alternative sources of services as needed.

Intellectual Property

The Company currently has no registered intellectual property.

We rely on a combination of trademarks, service marks, domain name registrations, copyright protection and contractual restrictions to establish and protect our brand name and logos, marketing designs and internet domain names.

We have registered the trademark of “汉中广厦”and the associated logo for the real estate related service in the PRC. We have also applied the same trademark for other goods and services directly or indirectly related to our business operations,

to strengthen the protection of our trademark and brand.

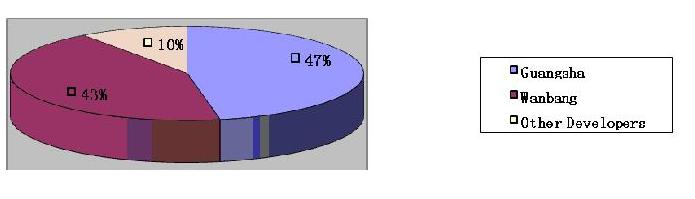

Competition

The real estate industry in China is highly competitive. In Tier II cities that we focus on, the markets are relatively more fragmented than Tier I cities. We compete primarily with local and regional property developers and an increasing number of large national property developers who have also started to enter these markets. Competitive

factors include the geographical location of the projects, the types of products offered, brand recognition, price, designing and quality. In the regional markets which we operate, our major competitors include Wanbang Real Estate Development Co. Ltd., and other national real estate developers who have also started their projects in the local markets.

Nationally, there are numerous companies that have real estate projects across China. There are 79 housing and land development companies listed on the Shanghai, Shenzhen and Hong Kong Stock Exchanges. However, such companies usually undertake large scale projects and are unlikely to compete with Guangsha for business as the Company targets

small to medium sized projects in Tier II cities and counties.

In the regional market, the Company’s only direct competitor with likely market shares in market is Wanbang Real Estate Development Co. Ltd. This company generally undertakes medium and small scale projects. By the end of September, 2009, Wanbang had developed realty about 600 acres across Hangzhong city and other counties surrounding.

As of September, 2009, Wanbang had about 200,000 square meters of construction area.

13

The demonstration graph set forth below describes the market shares ownership structure as of September 2009 in terms of real estate industry field in city of Hanzhong, Shaanxi Province:

Competitive Strengths:

We believe the following strengths allow us to compete effectively in regional real estate development industry:

Well Positioned to Capture Opportunities in Tier II Cities and Counties.

As the ascend intendancy in consumer disposable income and urbanization rates, a growing middle-income consumer market was emerged consequently, driving demand of affordable and high quality housing in many cities across northwest China. We focus on building large communities of modern, mid-sized residential properties for this

market segment and have accumulated substantial knowledge and experience about the residential preferences and demands of mid-income customers. We believe we can leverage our experience to capture the growth opportunities in the markets.

Standardized and Scalable Business Model.

Our business model focuses on a standardized property development process designed for rapid asset turnover. We break up the overall process into well-defined stages and closely monitor costs and development schedules through each stage. These stages include (i) identifying land, (ii) pre-planning and budgeting, (iii) land acquisition,

(iv) detail project design, (v) construction management, (vi) pre-sales, sales and (vii) after-sale service. We commence pre-planning and budgeting prior to the land acquisition, which enables us to acquire land at costs that meet our pre-set investment targeted returns and to quickly begin the development process upon acquisition. Our enterprise resource planning enables us to collect and analyze information on a real-time basis throughout the entire property development process. We utilize our customer relationship

management system to track customer profiles and sales to forecast future individual preferences and market demand.

14

Experienced Management Team Supported by Trained and Motivated Workforce.

Our CEO and founder Mr. Xiaojun Zhu has experience in real estate industry over 15 years. Mr. Zhu gained considerable strategic planning and business management expertise in the past decade. Our management and workforce are well-trained and motivated. Employees receive on-going training in their areas of specialization at our head office

in Hanzhong. In addition, we have adopted broad performance-based stock incentive plans, which we believe will further enable us to retain and motivate the workforce, and also attract new talent to facilitate our rapid expansion.

Guangsha is also an “AAA Enterprise in Shaanxi Construction Industry” as recognized by the Credit Association of Agricultural Bank of China, Shaanxi Branch.

Strategies

Our goal is to become the leading residential property developer focused on China’s Tier II cities by implementing the following strategies:

Continue Expanding in Selected Tier II Cities. We believe that Tier II cities present development opportunities that are well suited for our scalable business model of rapid asset turnover. Furthermore, Tier II cities currently tend to be in an early stage of market maturity and have fewer large national developers. We believe that

the fragmented market and relative abundance of land supply in Tier II cities, as compared to Tier I cities, offer more opportunities for us to generate attractive margins and we also believe that our given experience afford us the opportunity to emerge as a leading developer in these markets. In the near future, we plan to enter into other Tier II cities that have:

|

· |

Increasing urbanization rate and population growth; |

|

· |

High economic growth and increasing individual income; and |

|

· |

Sustainable land supply for future developments |

We plan to continue to closely monitor our capital and cash positions and carefully manage our cost for land use rights, construction costs and operating expenses. We believe that we will be able to use our working capital more efficiently by adhering to prudent cost management, which will help to maintain our profit margins. When selecting

a property project for development, we will continue to follow our established internal evaluation process, including utilizing the analysis and input of our institutional shareholders and choosing third-party contractors through a tender process open only to bids which meet our budgeted costs.

15

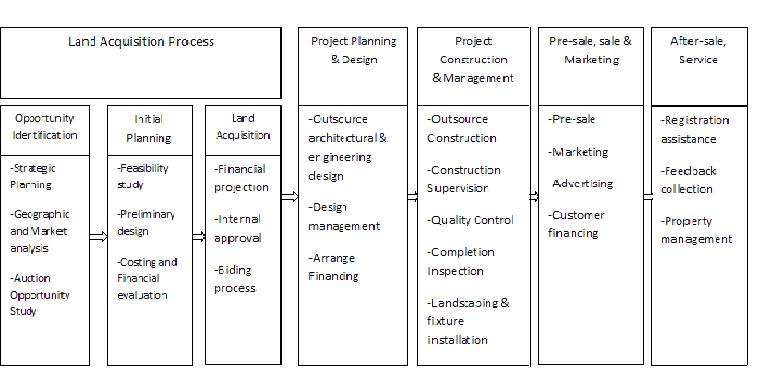

Our Property Development Operations

We have a systematic and standardized process to project development, which we implement through several well-defined phases. One critically significant portion of our process is land acquisition process, which is segmented into three stages: (i) opportunity identification, (ii) initial planning and budgeting and (iii) land acquisition.

The following diagram sets forth the key stages of our property development process.

Our Property Projects

Overview

We offer the following three main types of real estate property products:

|

· |

multi-layer apartment buildings, which are typically six stories or less and normally require 200 to 270 days to construct after we obtain the related construction permit; |

|

· |

sub-high-rise apartment buildings, which are typically seven to 11 stories and normally require 300 to 370 days to construct after we obtain the related construction permit; and |

|

· |

high-rise apartment buildings, which are typically 12 to 33 stories and normally require 500 to 900 days to construct after we obtain the related construction permit. |

16

Our projects are in one of the following three stages:

|

· |

completed projects, comprising projects that the construction of which has been completed; |

|

· |

properties under construction, comprising properties that the construction permits have been obtained; |

|

· |

properties under planning, comprising properties that we have entered into land grant contracts and are in the process of obtaining the required permits to begin construction. |

Completed Projects

The following table sets forth each of our completed projects as of September 30, 2009

|

Project Name |

Location |

Type of Projects |

Completion Date |

Total GFA(1) square meters |

Total Number of Unit |

Number of Sold Units |

|

Weinan Lijing Garden – Project I |

Weinan |

Multi-layer |

April 2005 |

44,373 |

31 |

31 |

|

Weinan Lijing Garden – Project II |

Weinan |

Multi-layer |

December 2006 |

55,390 |

39 |

39 |

|

Weinan Lijing Garden – Project III |

Weinan |

Multi-layer |

June 2008 |

3,964 |

3 |

3 |

|

Yangzhou Mingzhu- Project I |

Multi-layer |

September 2009 |

34,348 |

27 |

16 | |

|

Mingzhu Garden-Project I&II |

Multi-layer |

September 2009 |

28,666 |

6 |

6 | |

|

Total |

166,723 |

106 |

95 |

(1) The amounts for “total GFA” in this table are the amounts of total saleable residential GFA and are derived on the following basis:

|

· |

for properties that are sold, the stated GFA is based on that sales contracts relating to such property; |

|

· |

for unsold properties that are completed, the stated GFA is calculated based on the detailed construction blueprint and the calculation method approved by the PRC government for saleable GFA, after necessary adjustments; |

|

· |

for properties that are under planning, the stated GFA is based on the land grant contract and our internal projections. |

17

Properties under Construction and Properties under Planning

The following table sets forth each of our properties currently under construction or planning as of September 30, 2009:

|

Projects under Construction |

Location |

Type of Projects |

Actual or

Estimated

Construction

time |

Actual or

Estimated Pre-sale

Commencement

Date |

Total

GFA(1) (square meters) |

Total

Number

of Units |

Number of Pre-sold Units |

|

Yang County |

Yang County |

Multi-layer |

July 2008 |

October 2007 |

72,476 |

34 |

3 |

|

Nan Da Street |

Hanzhong City |

M/S |

May 2008 |

February 2007 |

42,476 |

4 |

2.5 |

|

Mingzhu Real Estate |

Hanzhong City |

M/S/H |

January 2007 |

December 2006 |

37,015 |

6 |

6 |

|

Subtotal |

151,967 |

44 |

11.5 | ||||

|

Projects under Planning |

|||||||

|

Yang County Project IV |

Yang County |

M/S/H |

2009 or 2010 |

N/A |

246,471 |

114 |

N/A |

|

Nan Da Street Project II |

Hanzhong City |

M/S/H |

2009 |

N/A |

61,176 |

18 |

N/A |

|

Subtotal |

307,647 |

132 |

|||||

|

Total |

398,438 |

135 |

11.5 |

(1) The amounts for “total GFA” in this table are the amounts of total saleable residential GFA and are derived on the following basis:

|

· |

for properties that are sold, the stated GFA is based on that sales contracts relating to such property; |

|

· |

for unsold properties that are completed, the stated GFA is calculated based on the detailed construction blueprint and the calculation method approved by the PRC government for saleable GFA, after necessary adjustments; |

|

· |

for properties that are under planning, the stated GFA is based on the land grant contract and our internal projections. |

Quality Control

We emphasize quality control to ensure that our buildings and residential unit meet our standards and provide high quality service. We select only experienced design and construction companies. We, through our contracts with contraction contractors, provide customers with warranties covering the building structure and certain fittings and

facilities of our property developments in accordance with the relevant regulations. To ensure construction quality, our construction contracts contain quality warranties and penalty provisions for poor work quality. In the event of delay or poor work quality, the contractor may be required to pay pre-agreed damages under our construction contracts. Our construction contracts do not allow our contractors to subcontract or transfer their contractual arrangements with us to third parties. We typically withhold 2%

of the agreed construction fees for two to five years after completion of the construction as a deposit to guarantee quality, which provides us assurance for our contractors’ work quality.

Our contractors are also subject to our quality control procedures, including examination of materials and supplies, on-site inspection and production of progress reports. We require our contractors to comply with relevant PRC laws and regulations, as well as our own standards and specifications. We set up a profile for each and every unit

constructed and monitor the quality of such unit throughout its construction period until its delivery. We also employ independent surveyors to supervise the construction progress. In addition, the construction of real estate projects is regularly inspected and supervised by PRC governmental authorities.

Environmental Matters

As a developer of property in the PRC, we are subject to various environmental laws and regulations set by the PRC national, provincial and municipal governments. These include regulations on air pollution, noise emissions, as well as water and waste discharge. We in the past have never paid any penalties associated with the breach of any

such laws and regulations. Compliance with existing environmental laws and regulations has not had a material adverse effect on our financial condition and results of operations, and we do not believe it will have such an impact in the future.

Our projects are normally required to undergo an environmental impact assessment by government-appointed third parties, and a report of such assessment needs to be submitted to the relevant environmental authorities in order to obtain their approval before commencing construction. Upon completion of each project, the relevant environmental

authorities inspect the site to ensure the applicable environmental standards have been complied with, and the resulting report is presented together with other specified documents to the relevant construction administration authorities for their approval and record. Approval from the environmental authorities on such report is required before we can deliver our completed work to our customers. In the past, we have not experienced any difficulties in obtaining those approvals for commencement of construction

and delivery of completed projects.

18

Employees

We currently have 87 full-time staff and employees.

|

Department |

Headcount |

|

Management |

15 |

|

Accounting staff |

5 |

|

Sales and marketing staff |

60 |

|

Administrative |

7 |

|

Total |

87 |

ITEM 1A. RISK FACTORS

Risks Relating to Our Business

If we are unable to successfully manage our expansion into other Tier II cities, we will not be able to execute our business plan.

Historically, our business and operations have been concentrated in Hanzhong City and other surrounding counties. If we are unable to successfully develop and sell projects outside Hanzhong City, our future growth may be limited and we may not generate adequate returns to cover our investments in these Tier II cities. In addition, as we

expand our operations to Tier II cities with higher land prices, our costs may increase, which may lead to a decrease in our profit margin.

We require substantial capital resources to fund our land use rights acquisition and property developments, which may not be available.

Property development is capital intensive. Our ability to secure sufficient financing for land use rights acquisition and property development depends on a number of factors that are beyond our control, including market conditions in the capital markets, the PRC economy and the PRC government regulations that affect the availability and

cost of financing for real estate companies.

In addition, the People’s Bank of China, or the PBOC, has increased the reserve requirement ratio for commercial banks several times since July 5, 2006, raising it from 7.5% as of that date to the current 13.5%. The reserve requirement ratio refers to the amount of funds that banks must hold in reserve against deposits made by their

customers. These increases in the reserve requirement ratio have reduced the amount of commercial bank credit available to businesses in China, including us.

We may be unable to acquire desired development sites at commercially reasonable costs.

Our revenue depends on the completion and sale of our projects, which in turn depends on our ability to acquire development sites. Our land use rights costs are a major component of our cost of real estate sales and increases in such costs could diminish our gross margin. In China, the PRC government controls the supply of land and regulates

land sales and transfers in the secondary market. As a result, the policies of the PRC government, including those related to land supply and urban planning, affect our ability to acquire, and our costs of acquiring, land use rights for our projects. In recent years, the government has introduced various measures attempting to moderate investment in the property market in China.

19

Although we believe that these measures are generally targeted at the luxury property market and speculative purchases of land and properties, we cannot assure you that the PRC government will not introduce other measures in the future that adversely affect our ability to obtain land for development. We currently acquire our development

sites primarily by bidding for government land. Under current regulations, land use rights acquired from government authorities for commercial and residential development purposes must be purchased through a public tender, auction or listing-for-sale. Competition in these bidding processes has resulted in higher land use rights costs for us. We may also need to acquire land use rights through acquisition, which could increase our costs. Moreover, the supply of potential development sites in any given city will

diminish over time and we may find it increasingly difficult to identify and acquire attractive development sites at commercially reasonable costs in the future.

We provide guarantees for the mortgage loans of our customers which expose us to risks of default by our customers.

We pre-sell properties before actual completion and, in accordance with industry practice, and our customers’ mortgage banks require us to guarantee our customers’ mortgage loans. Typically, we provide guarantees to PRC banks with respect to loans procured by the purchasers of our properties for the total mortgage loan amount

until the completion of the registration of the mortgage with the relevant mortgage registration authorities, which generally occurs within six to 12 months after the purchasers take possession of the relevant properties. In line with what we believe to be industry practice, we rely on the credit evaluation conducted by mortgagee banks and do not conduct our own independent credit checks on our customers. The mortgagee banks typically require us to maintain, as restricted cash, 5% to 10% of the mortgage proceeds

paid to us as security for our obligations under such guarantees.

If a purchaser defaults on its payment obligations during the term of our guarantee, the mortgagee bank may deduct the delinquent mortgage payment from the security deposit. If the delinquent mortgage payments exceed the security deposit, the banks may require us to pay the excess amount. If multiple purchasers default on their payment

obligations at around the same time, we will be required to make significant payments to the banks to satisfy our guarantee obligations. If we are unable to resell the properties underlying defaulted mortgages on a timely basis or at prices higher than the amounts of our guarantees and related expenses, we will suffer financial losses.

We rely on third-party contractors.

Substantially all of our project construction and related work are outsourced to third-party contractors. We are exposed to risks that the performance of our contractors may not meet our standards or specifications. Negligence or poor work quality by any contractors may result in defects in our buildings or residential units, which could

in turn cause us to suffer financial losses, harm our reputation or expose us to third-party claims. We work with multiple contractors on different projects and we cannot guarantee that we can effectively monitor their work at all times.

Although our construction and other contracts contain provisions designed to protect us, we may be unable to successfully enforce these rights and, even if we are able to successfully enforce these rights, the third-party contractor may not have sufficient financial resources to compensate us. Moreover, the contractors may undertake projects

from other property developers, engage in risky undertakings or encounter financial or other difficulties, such as supply shortages, labor disputes or work accidents, which may cause delays in the completion of our property projects or increases in our costs.

20

We may be unable to complete our property developments on time or at all.

The progress and costs for a development project can be adversely affected by many factors, including, without limitation:

|

● |

delays in obtaining necessary licenses, permits or approvals from government agencies or authorities; |

|

● |

shortages of materials, equipment, contractors and skilled labor; |

|

● |

disputes with our third-party contractors; |

|

● |

failure by our third-party contractors to comply with our designs, specifications or standards; |

|

● |

difficult geological situations or other geotechnical issues; |

|

● |

onsite labor disputes or work accidents; and |

|

● |

natural catastrophes or adverse weather conditions. |

Any construction delays, or failure to complete a project according to our planned specifications or budget, may delay our property sales, which could harm our revenues, cash flows and our reputation.

Changes of laws and regulations with respect to pre-sales may adversely affect our cash flow position and performance.

We depend on cash flows from pre-sale of properties as an important source of funding for our property projects and servicing our indebtedness. Under current PRC laws and regulations, property developers must fulfill certain conditions before they can commence pre-sale of the relevant properties and may only use pre-sale proceeds to finance

the construction of the specific developments.

Our results of operations may fluctuate from period to period.

Our results of operations tend to fluctuate from period to period. The number of properties that we can develop or complete during any particular period is limited due to the substantial capital required for land acquisition and construction, as well as the lengthy development periods required before positive cash flows may be generated.

In addition, several properties that we have developed or that are under development are large scale and are developed in multiple phases over the course of one to several years. The selling prices of the residential units in larger scale property developments tend to change over time, which may impact our sales proceeds and, accordingly, our revenues for any given period.

21

We rely on our key management members.

We depend on the services provided by key management members. Competition for management talent is intense in the property development sector. In particular, we are highly dependent on Mr. Xiaojun Zhu, our founder, Chairman and Chief Executive Officer. We do not maintain key employee insurance. In the event that we lose the services

of any key management member, we may be unable to identify and recruit suitable successors in a timely manner or at all, which will adversely affect our business and operations. Moreover, we need to employ and retain more management personnel to support our expansion into other Tier II cities on a much larger geographical scale. If we cannot attract and retain suitable human resources, especially at the management level, our business and future growth will be adversely affected.

Increases in the price of raw materials may increase our cost of sales and reduce our earnings.

Our third-party contractors are responsible for procuring almost all of the raw materials used in our project developments. Our construction contracts typically provide for fixed or capped payments, but the payments are subject to changes in government-suggested steel prices. The increase in steel prices could result in an increase in our

construction cost. In addition, the increases in the price of raw materials, such as cement, concrete blocks and bricks, in the long run could be passed on to us by our contractors, which will increase our construction cost. Any such cost increase could reduce our earnings to the extent we are unable to pass these increased costs to our customers.

Any unauthorized use of our brand or trademark may adversely affect our business.

We own trademarks for “汉中广厦”, in the form of Chinese characters and our company logo. We rely on the PRC intellectual property and anti-unfair competition laws and contractual restrictions to protect brand name and trademarks. We believe

our brand, trademarks and other intellectual property rights are important to our success. Any unauthorized use of our brand, trademarks and other intellectual property rights could harm our competitive advantages and business. Historically, China has not protected intellectual property rights to the same extent as the United States, and infringement of intellectual property rights continues to pose a serious risk of doing business in China. Monitoring and preventing unauthorized use is difficult. The measures

we take to protect our intellectual property rights may not be adequate. Furthermore, the application of laws governing intellectual property rights in China and abroad is uncertain and evolving, and could involve substantial risks to us. If we are unable to adequately protect our brand, trademarks and other intellectual property rights, our reputation may be harmed and our business may be adversely affected.

We may fail to obtain, or may experience material delays in obtaining necessary government approvals for any major property development, which will adversely affect our business.

The real estate industry is strictly regulated by the PRC government. Property developers in China must abide by various laws and regulations, including implementation rules promulgated by local governments to enforce these laws and regulations. Before commencing, and during the course of, development of a property project, we need to apply

for various licenses, permits, certificates and approvals, including land use rights certificates, construction site planning permits, construction work planning permits, construction permits, pre-sale permits and completion acceptance certificates. We need to satisfy various requirements to obtain these certificates and permits. To date, we have not encountered serious delays or difficulties in the process of applying for these certificates and permits, but we cannot guarantee that we will not encounter serious

delays or difficulties in the future. In the event that we fail to obtain the necessary governmental approvals for any of our major property projects, or a serious delay occurs in the government’s examination and approval progress, we may not be able to maintain our development schedule and our business and cash flows may be adversely affected.

22

We may forfeit land to the PRC government if we fail to comply with procedural requirements applicable to land grants from the government or the terms of the land use rights grant contracts.

According to the relevant PRC regulations, if we fail to develop a property project according to the terms of the land use rights grant contract, including those relating to the payment of land premiums, specified use of the land and the time for commencement and completion of the property development, the PRC government may issue a warning,

may impose a penalty or may order us to forfeit the land. Specifically, under current PRC law, if we fail to commence development within one year after the commencement date stipulated in the land use rights grant contract, the relevant PRC land bureau may issue a warning notice to us and impose an idle land fee on the land of up to 20% of the land premium. If we fail to commence development within two years, the land will be subject to forfeiture to the PRC government, unless the delay in development is caused

by government actions or force majeure. Even if the commencement of the land development is compliant with the land use rights grant contract, if the developed GFA on the land is less than one-third of the total GFA of the project or the total capital invested is less than one-fourth of the total investment of the project and the suspension of the development of the land continues for more than one year without government approval, the land will also be treated as idle land and be subject to penalty or forfeiture.

We cannot assure you that circumstances leading to significant delays in our development schedule or forfeiture of land will not arise in the future. If we forfeit land, we will not only lose the opportunity to develop the property projects on such land, but may also lose all past investments in such land, including land premiums paid and development costs incurred.

Any non-compliant GFA of our uncompleted and future property developments will be subject to governmental approval and additional payments.

The local government authorities inspect property developments after their completion and issue the completion acceptance certificates if the developments are in compliance with the relevant laws and regulations. If the total constructed GFA of a property development exceeds the GFA originally authorized in the relevant land grant contracts

or construction permit, or if the completed property contains built-up areas that do not conform with the plan authorized by the construction permit, the property developer may be required to pay additional amounts or take corrective actions with respect to such non-compliant GFA before a completion acceptance certificate can be issued to the property development.

Our failure to assist our customers in applying for property ownership certificates in a timely manner may lead to compensatory liabilities to our customers.

We are required to meet various requirements within 90 days after delivery of property, or such other period contracted with our customers, in order for our customers to apply for their property ownership certificates, including passing various governmental clearances, formalities and procedures. Under our sales contract, we are liable

for any delay in the submission of the required documents as a result of our failure to meet such requirements, and are required to compensate our customers for delays. In the case of serious delays on one or more property projects, we may be required to pay significant compensation to our customers and our reputation may be adversely affected.

We are subject to potential environmental liability.

We are subject to a variety of laws and regulations concerning the protection of health and the environment. The particular environmental laws and regulations that apply to any given development site vary significantly according to the site’s location and environmental condition, the present and former uses of the site and the nature

of the adjoining properties. Environmental laws and conditions may result in delays, may cause us to incur substantial compliance and other costs and can prohibit or severely restrict project development activity in environmentally-sensitive regions or areas. Although the environmental investigations conducted by local environmental authorities have not revealed any environmental liability that we believe would have a material adverse effect on our business, financial condition or results of operations to date,

it is possible that these investigations did not reveal all environmental liabilities and that there are material environmental liabilities of which we are unaware. We cannot assure you that future environmental investigations will not reveal material environmental liability. Also, we cannot assure you that the PRC government will not change the existing laws and regulations or impose additional or stricter laws or regulations, the compliance of which may cause us to incur significant capital expenditure.

23

We have never paid cash dividends and are not likely to do so in the foreseeable future.

We have never declared or paid any cash dividends on our common stock. We currently intend to retain any future earnings for use in the operation and expansion of our business. We do not expect to pay any cash dividends in the foreseeable future but will review this policy as circumstances dictate.

If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence

in our reported financial information and have a negative effect on the market price for shares of our common stock.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud. We maintain a system of internal control over financial reporting, which is defined as a process designed by, or under the supervision of, our principal executive officer and principal financial officer, or persons performing

similar functions, and effected by our board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

As a public company, we will have significant additional requirements for enhanced financial reporting and internal controls. We will be required to document and test our internal control procedures in order to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act of 2002, which requires annual management assessments of the

effectiveness of our internal controls over financial reporting and a report by our independent registered public accounting firm addressing these assessments. The process of designing and implementing effective internal controls is a continuous effort that requires us to anticipate and react to changes in our business and the economic and regulatory environments and to expend significant resources to maintain a system of internal controls that is adequate to satisfy our reporting obligations as a public company.

We cannot assure you that we will not, in the future, identify areas requiring improvement in our internal control over financial reporting. We cannot assure you that the measures we will take to remediate any areas in need of improvement will be successful or that we will implement and maintain adequate controls over our financial processes

and reporting in the future as we continue our growth. If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our common stock.

Lack of experience as officers of publicly-traded companies of our management team may hinder our ability to comply with Sarbanes-Oxley Act.

It may be time consuming, difficult and costly for us to develop and implement the internal controls and reporting procedures required by the Sarbanes-Oxley Act. We may need to hire additional financial reporting, internal controls and other finance staff in order to develop and implement appropriate internal controls and reporting procedures.

If we are unable to comply with the Sarbanes-Oxley Act’s internal controls requirements, we may not be able to obtain the independent auditor certifications that Sarbanes-Oxley Act requires publicly-traded companies to obtain.

We will incur increased costs as a result of being a public company.

As a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act of 2002, as well as new rules subsequently implemented by the SEC, has required changes in corporate governance practices of public companies. We expect these new rules and regulations

to increase our legal, accounting and financial compliance costs and to make certain corporate activities more time-consuming and costly. In addition, we will incur additional costs associated with our public company reporting requirements. We are currently evaluating and monitoring developments with respect to these new rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs.

24

Risk Relating to the Residential Property Industry in China

The PRC government may adopt further measures to curtail the overheating of the property sector.

Along with the economic growth in China, investments in the property sectors have increased significantly in the past few years. In response to concerns over the scale of the increase in property investments, the PRC government has introduced policies to curtail property development. We believe the following regulations, among others, significantly

affect the property industry in China.

The PRC government’s restrictive regulations and measures to curtail the overheating of the property sector could increase our operating costs in adapting to these regulations and measures, limit our access to capital resources or even restrict our business operations. We cannot be certain that the PRC government will not issue additional

and more stringent regulations or measures, which could further slow down property development in China and adversely affect our business and prospects.

We are heavily dependent on the performance of the residential property market in China, which is at a relatively early development stage.

The residential property industry in the PRC is still in a relatively early stage of development. Although demand for residential property in the PRC has been growing rapidly in recent years, such growth is often coupled with volatility in market conditions and fluctuation in property prices. It is extremely difficult to predict how much

and when demand will develop, as many social, political, economic, legal and other factors, most of which are beyond our control, may affect the development of the market. The level of uncertainty is increased by the limited availability of accurate financial and market information as well as the overall low level of transparency in the PRC, especially in Tier II cities which have lagged in progress in these aspects when compared to Tier I cities.

The lack of a liquid secondary market for residential property may discourage investors from acquiring new properties. The limited amount of property mortgage financing available to PRC individuals may further inhibit demand for residential developments.

We face intense competition from other real estate developers.

The property industry in the PRC is highly competitive. In the Tier II cities we focus on, local and regional property developers are our major competitors, and an increasing number of large state-owned and private national property developers have started entering these markets. Many of our competitors, especially the state-owned and private

national property developers, are well capitalized and have greater financial, marketing and other resources than we have. Some also have larger land banks, greater economies of scale, broader name recognition, a longer track record and more established relationships in certain markets. In addition, the PRC government’s recent measures designed to reduce land supply further increased competition for land among property developers.

Competition among property developers may result in increased costs for the acquisition of land for development, increased costs for raw materials, shortages of skilled contractors, oversupply of properties, decrease in property prices in certain parts of the PRC, a slowdown in the rate at which new property developments will be approved

and/or reviewed by the relevant government authorities and an increase in administrative costs for hiring or retaining qualified personnel, any of which may adversely affect our business and financial condition. Furthermore, property developers that are better capitalized than we are may be more competitive in acquiring land through the auction process. If we cannot respond to changes in market conditions as promptly and effectively as our competitors, or effectively compete for land acquisition through the auction

systems and acquire other factors of production, our business and financial condition will be adversely affected.

25

In addition, risk of property over-supply is increasing in parts of China, where property investment, trading and speculation have become overly active. We are exposed to the risk that in the event of actual or perceived over-supply, property prices may fall drastically, and our revenue and profitability will be adversely affected.

PRC economic, political and social conditions as well as government policies can affect our business.

The PRC economy differs from the economies of most developed countries in many aspects, including:

|

● |

political structure; |

|

● |

degree of government involvement; |

|

● |

degree of development; |

|

● |

level and control of capital reinvestment; |

|

● |

control of foreign exchange; and |

|

● |

allocation of resources. |

The PRC economy has been transitioning from a centrally planned economy to a more market-oriented economy. For more than two decades, the PRC government has implemented economic reform measures emphasizing utilization of market forces in the development of the PRC economy. Although we believe these reforms will have a positive effect on