Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Symetra Financial CORP | d300739d8k.htm |

Exhibit 99.1

February 15, 2012

Bank

of

America

Merrill

Lynch

2012 Insurance Conference |

Forward-Looking Statements

Statements made in the following presentation that relate to anticipated financial

performance or business operations, business services and product prospects

and plans, reinvestment opportunities, changes in the amount of cash flow testing

reserves, regulatory developments, accounting standard changes and similar matters

may be considered “forward-looking statements”

as defined in the Private Securities Litigation Reform Act of 1995. All

statements, other than statements of current or historical facts, are

forward-looking statements. Forward-looking statements are subject to a number of risks,

uncertainties and contingencies that may cause the operations, performance,

development and results of our business to differ materially from those

suggested by such statements. Consequently, all of the forward-looking statements made in this

presentation are qualified by these cautionary statements. The information

contained in this presentation speaks as of February 15, 2012. Symetra

undertakes no obligation to update any such forward-looking statements, whether as a result of

new information, future events or otherwise. Historical results are not necessarily

indicative of future results. Future results, including our financial

performance, business operations and trends in our business and industry, are subject to significant

risks and uncertainties, including without limitation the following:

›

the effects of fluctuations in interest rates and a prolonged low interest rate

environment; ›

general economic, market or business conditions, including further economic

downturns or other adverse conditions in the global and domestic capital

and credit markets; ›

investment losses;

›

recorded reserves for future policy benefits and claims subsequently proving to be

inadequate or inaccurate; ›

deviations

from

assumptions

used

in

setting

prices

for

insurance

and

annuity

products

or

establishing

cash

flow

testing

reserves;

›

continued viability of certain products under various economic and other

conditions; ›

market pricing and competitive trends related to insurance products and

services; ›

changes

in

amortization

of

deferred

policy

acquisition

costs

and

deferred

sales

inducements;

›

financial strength or credit ratings downgrades;

›

the availability and cost of capital and financing;

›

the continued availability and cost of reinsurance coverage;

›

changes in laws or regulations, or their interpretation, including those which

could increase Symetra's business costs and required capital levels;

›

the ability of subsidiaries to pay dividends to Symetra;

›

Symetra’s ability to successfully execute on its Grow & Diversify

strategy; ›

the effects of implementation of the Patient Protection and Affordable Care

Act; ›

the effects of implementation of the Dodd-Frank Wall Street Reform and

Consumer Protection Act; ›

the

effects

of

implementation

of

the

new

accounting

standard

for

deferred

acquisition

costs;

and

›

the

risks

that

are

described

from

time

to

time

in

Symetra's

filings

with

the

Securities

and

Exchange

Commission,

including

those

in

Symetra's 2010 Annual Report on Form 10-K and 2011 quarterly reports on Form

10-Q. 2 |

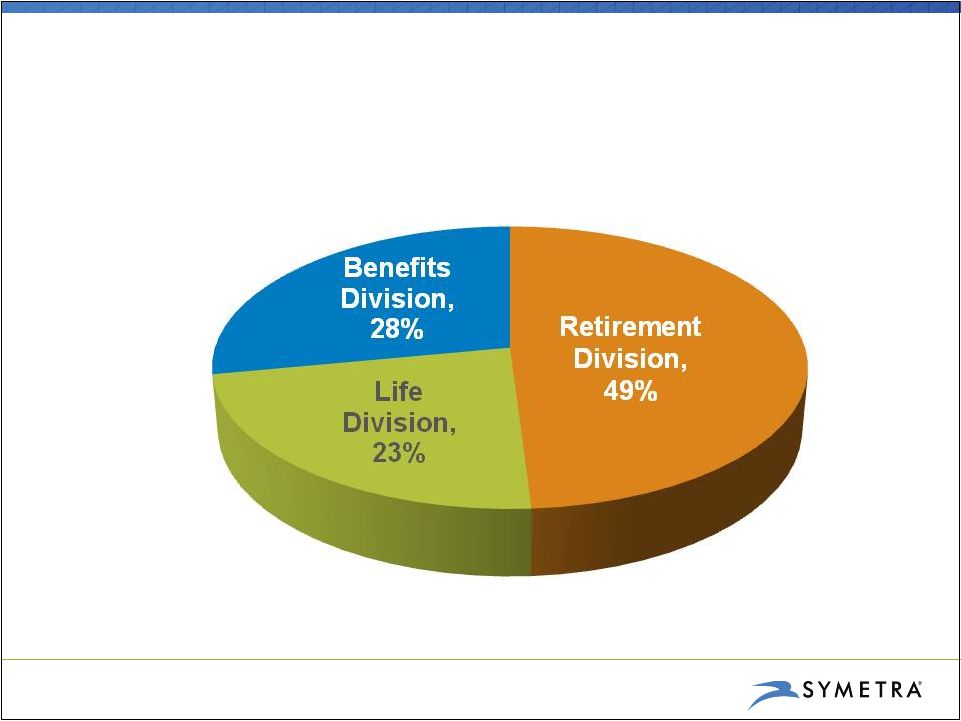

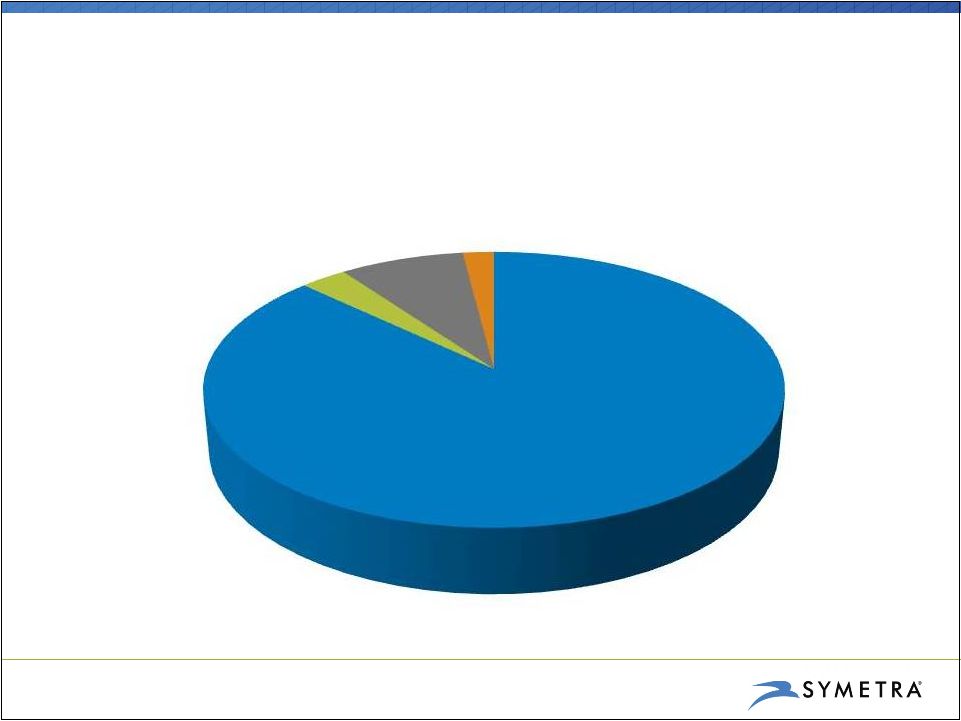

Our Businesses Are Aligned in Three Divisions

2011 Pretax Adjusted Operating Income

1

Excluding Other segment loss of $(10.7)M. A non-GAAP financial measure;

see Appendix for definition and reconciliation to the most directly

comparable GAAP measure. 3

1 |

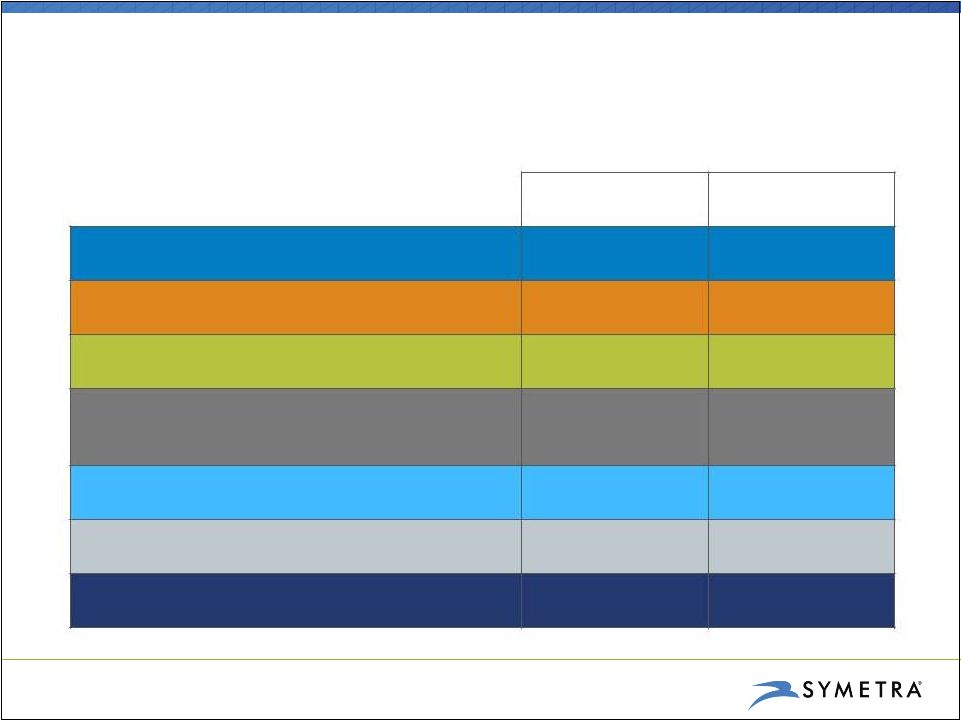

Diversifying Our Risks Over Time

4

Present

Future

Rising interest

rates

High

Medium

Falling interest rates

High

Medium

Morbidity

(loss

ratio)

Medium

Medium

Premium revenues

(underwriting cycles)

Medium

Medium

Mortality

Low

Medium

Equity

Low

Medium

Credit

High

Medium |

5

Executing on “Grow & Diversify”

Strategy

›

Driving profitable growth and diversifying revenue sources

(especially important in prolonged low interest rate environment)

›

Not taking easy route to growth

›

Targeting markets and products that offer higher ROE

›

Implementation

risk

–

not

balance

sheet

risk

›

Sustaining current positions of strength in:

›

Medical stop-loss

›

Banking channel distribution of fixed annuities

›

Excellent balance sheet and disciplined risk management

|

Grow

& Diversify Initiatives Growth and diversification goals within each

division: ›

Benefits

›

Group Life & Disability Income (DI)

›

Complete transition of AUL medical stop-loss business

›

Retirement

›

Non-living benefits variable annuity (VA)

›

Fixed indexed annuity (FIA)

›

Life

›

New universal life (UL) products for life professional distribution

›

Variable corporate-owned life insurance (COLI)

6

1

American United Life Insurance Co.

1 |

We’re Building in 2012

›

Higher expenses related to investments in infrastructure in 2012

›

Benefits: building out disability claims processing capabilities

›

Retirement: completing development of VA for mid-year launch

›

Life: steady, but more modest, cost to build product and distribution

›

Expanded distribution and product support capabilities add to the run rate

›

Pricing ROEs across all Grow & Diversify products are initially 12% or

higher ›

AUL is a net contributor to earnings in all years, with above-target ROE

›

Full investment in Grow & Diversify initiatives is recovered by

mid-2015 7

Grow & Diversify Initiatives

2012

2013

2014

2015

Net Contribution to Operating EPS

$(0.08)

$(0.02)

$0.07

$0.14

1

A non-GAAP financial measure also referred to as “adjusted operating income per common share

– diluted.”

See Appendix for definition.

1 |

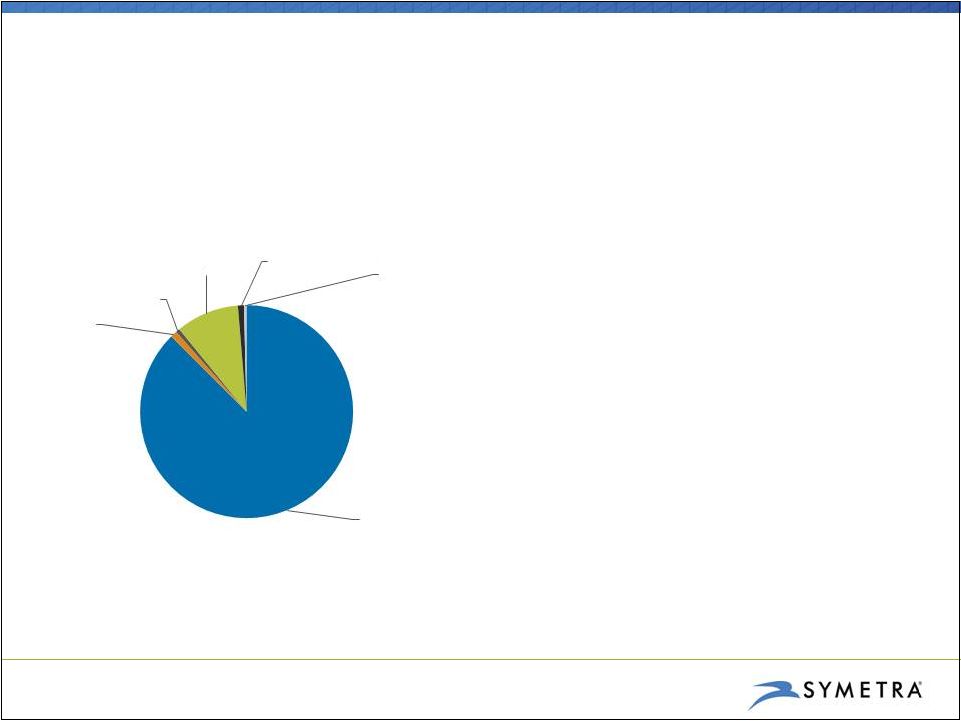

Benefits Division: Product Breakout

2011 Total Operating Revenues

8

Medical

Stop-Loss,

87%

MGU

Services, 3%

Limited

Benefit

Medical, 8%

Group Life

and Disability,

2% |

9

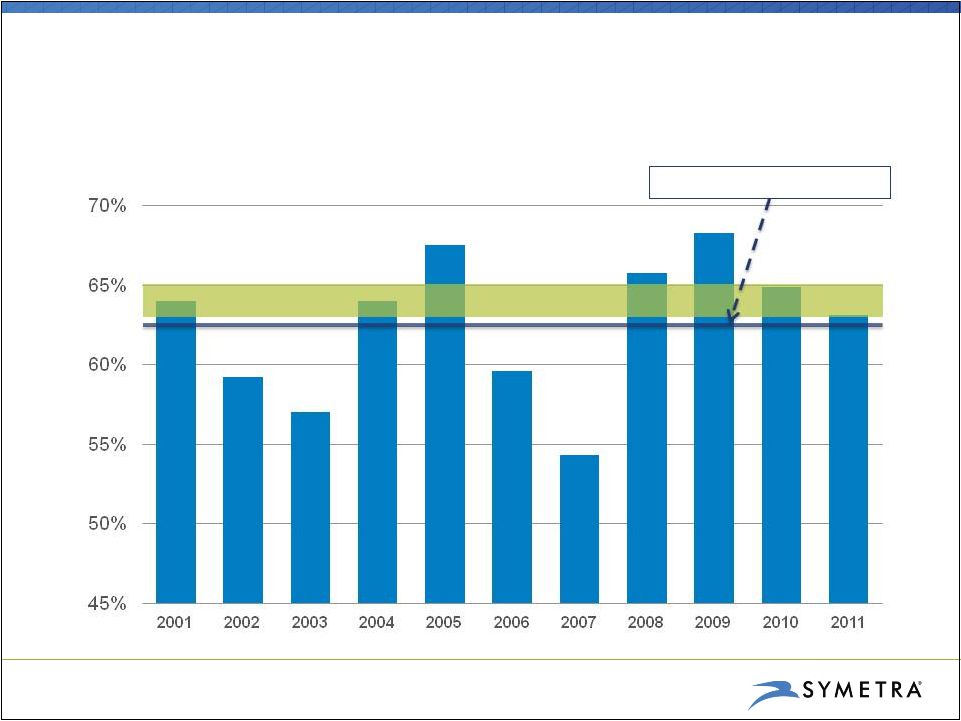

Excellent Track Record of Profitability

Benefits Loss Ratio

Long-term

target

range:

63%

-

65%

Average: 62.5% |

Medical Stop-Loss

•

Maintain leadership position

•

Through consistent, disciplined

underwriting, continue to achieve

long-term profitability targets

•

Complete transition of AUL policies

to Symetra

•

Capitalize on opportunities that

arise from healthcare reform

Group Life & DI

•

Drive growth in group life and

disability income premium, while

completing buildout of capabilities

•

Focus on the middle-market

opportunity

•

Leverage medical stop-loss

distribution network

Benefits Division’s Strategic Priorities

10 |

GAAP Account Values and Reserves

As of 12/31/11

Retirement Division: Product Breakout

11

Deferred

Fixed

Annuities,

59%

Deferred

Variable

Annuities, 4%

Structured

Settlements,

32%

Retail Payout

Annuities, 5% |

Account Values and Spreads¹

12

Fixed Annuity Block Is Growing Profitably

›

Pricing discipline will continue

›

Optimizing pricing and rates in

challenging rate environment

›

Optional guaranteed return

of purchase payment

›

Commission restructure

›

Increased surrender

charges

›

Rigorous reset of

guaranteed minimum rates

›

Spread will be a function of the

levers we pull

$ in millions

1

For 2009,

2010 and

2011, spread is base

interest spread, which excludes the impact

of asset prepayments and MBS prepayment speed

adjustments. Total interest spread for 2009, 2010 and 2011 was 1.81%, 1.87% and 1.94%, respectively.

$4,445

$5,725

$7,656

$9,244

$10,613

1.68%

1.67%

1.80%

1.80%

1.82%

1.00%

1.10%

1.20%

1.30%

1.40%

1.50%

1.60%

1.70%

1.80%

1.90%

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

YE '07

YE '08

YE '09

YE '10

YE '11

Account Value

Spread

Account Values and Spreads

1 |

Deferred Fixed

Annuities

•

Maintain leadership

position in the bank

distribution channel

•

Maintain strong interest

spread on fixed

annuities

•

Accelerate the uptake of

FIA product on bank and

broker-dealer platforms

Variable

Annuities

•

Complete development

of VA for the lower cost,

non-living benefits

market

•

Build the infrastructure

to support administration

of registered products

•

Launch in mid-2012

Income

Annuities

•

Continue to stabilize the

profitability of existing

block in low interest rate

environment with

commercial mortgage

loan origination strategy

•

Focus sales effort on

shorter duration

opportunities

Retirement Division’s Strategic Priorities

13 |

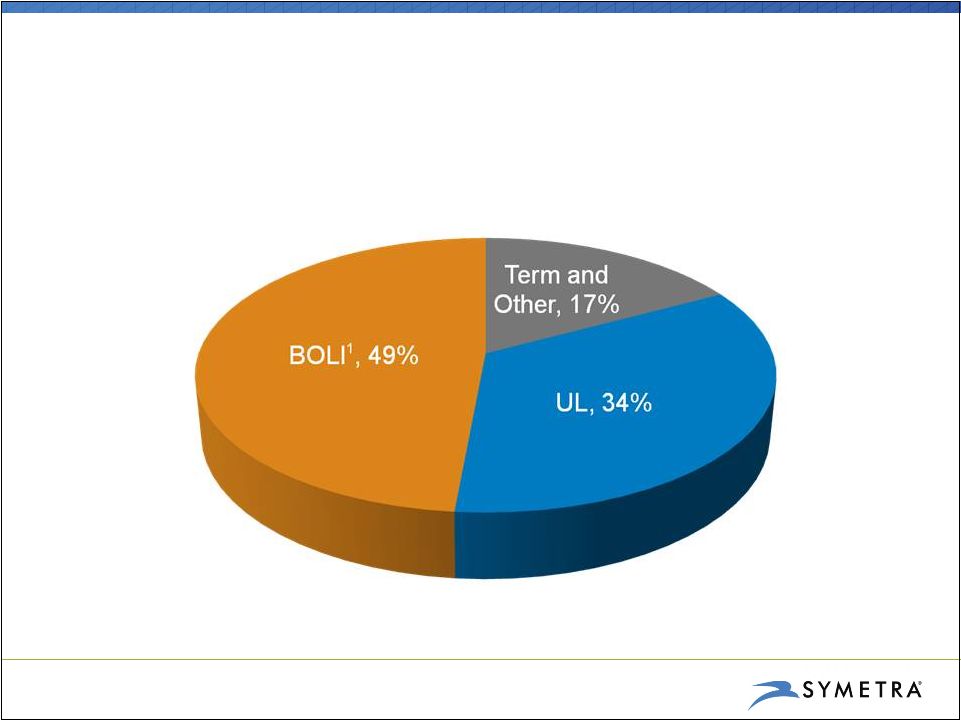

Life Division: Product Breakout

2011 Pretax Adjusted Operating Income

1

Bank-Owned Life Insurance

14 |

Develop New Product

•

Develop competitive features

(riders) for new core UL product

launched on September 30, 2011

•

Launch COLI product for

institutional market

Broaden Distribution

•

Roll out UL on national life-focused

brokerage general agent (BGA)

distribution partners’

sales

platforms

•

Expand opportunities for BOLI,

while leveraging BOLI expertise to

expand into the COLI market

Life Division’s Strategic Priorities

15 |

Maintaining Excellent Balance Sheet Strength

›

Conservative investment strategy:

›

ALM -

matching asset and liability cash flows

›

Driving improved yield through commercial mortgage loan origination

›

Approx. 84% of liabilities are mostly illiquid

›

Debt-to-capital ratio = 13%

›

Tangible book value

= 89% of total stockholders’

equity

›

Risk-based capital ratio = 457%

16

(As of 12/31/11)

1

A non-GAAP financial measure; see Appendix for definition and reconciliation

to most directly comparable GAAP measure.

1 |

Grow & Diversify: 2012 Targets

17

$250M in sales of fixed indexed

annuities and variable annuities

$25M in sales of group life and

disability income insurance

$25M in sales of universal life

and BOLI/COLI

Retirement Division:

Benefits Division:

Life Division: |

We’re Focused on Building Long-Term Value

›

Strong balance sheet provides a firm foundation

›

Symetra has market leadership positions in fixed deferred

annuities sold in banks and medical stop-loss

›

Grow & Diversify initiatives aim to generate incremental growth

from new, primarily non-interest rate sensitive earnings sources

›

Working to expand ROE over time

18 |

Appendix

19 |

Financial Results

20

2011

2010

Return on Equity (ROE)

7.3%

9.3%

Operating

Return

on

Average

Equity

(ROAE)

1

9.5%

9.8%

2011

2010

Net Income

$ 199.6

$ 200.9

Adjusted Operating Income

$ 194.1

$ 175.2

$ in millions

1

A non-GAAP financial measure. See Appendix for a definition of these measures and

reconciliations to the most directly comparable GAAP measures.

1 |

21

Benefits Segment

Priorities:

›

Maintain leadership position in medical stop-loss market, while achieving

loss ratio in line with long-term target range of 63% -

65%

›

Complete transition of AUL medical stop-loss policies to Symetra

›

Drive growth in group life and disability income premium, while completing

buildout of capabilities

2011

2010

Operating Revenues

$ 533.3

$ 463.6

Pretax Adjusted Operating Income

$ 79.2

$ 71.6

Loss Ratio

63.1%

64.9%

Total Sales

$ 118.7

$ 95.5

$ in millions

1

Total revenue excluding net realized investment gains (losses).

1 |

22

Deferred Annuities Segment

Priorities:

›

Maintain solid interest spread on fixed annuities

›

Increase sales of fixed annuities at many major bank distribution partners

and accelerate the uptake rate of fixed indexed annuities

›

Complete development for mid-year launch of variable annuity for the lower

cost non-living benefits market

2011

2010

Operating Revenues

$ 546.5

$ 482.5

Pretax Adjusted Operating Income

$ 102.1

$ 81.3

Base Interest Spread

1.82%

1.80%

Total Sales

$ 1,815.3

$ 1,810.7

Total Account Values

$11,326.9

$10,034.8

$ in millions

1

Total revenue excluding net realized investment gains (losses) and including net

investment gains (losses) on FIA options. 2

Excludes impact of asset prepayments and mortgage-backed securities prepayment speed

adjustments. 1

2 |

23

Income Annuities Segment

Priorities:

›

Continue

to

stabilize

the

profitability

of

existing

block

in

low

interest

rate

environment with commercial mortgage loan origination strategy

›

Focus sales effort on shorter duration opportunities

2011

2010

Operating Revenues

$ 414.9

$ 423.5

Pretax Adjusted Operating Income

$ 35.1

$ 33.2

Base Interest Spread

0.50%

0.49%

Total Sales

$ 221.9

$ 260.0

$ in millions

1

Total revenue excluding net realized investment gains (losses).

2

Excludes impact of asset prepayments and mortgage-backed securities prepayment speed

adjustments. 1

2 |

24

Life Segment

Priorities:

›

Roll out Symetra Classic UL insurance on new BGA partners’

sales platforms

›

Enhance Symetra Classic UL with additional benefits riders

›

Launch variable COLI product

2011

2010

Operating Revenues

$ 452.0

$ 429.4

Pretax Adjusted Operating Income

$ 64.9

$ 74.9

BOLI Base ROA

0.98%

0.97%

Individual Sales

$ 11.7

$ 10.2

BOLI Sales

$ --

$ 46.1

$ in millions

1

Total revenue excluding net realized investment gains (losses).

2

Excludes the impact of asset prepayments and reserve adjustments.

1

2 |

$26.2 billion

Portfolio Composition

As of 12/31/11

25

High-Quality Investment Portfolio

1

Included in trading marketable equity securities.

2

From inception of Symetra equity portfolio in January 2005 and

Symetra REIT portfolio in April 2011.

3

FTSE NAREIT All Equity REITS Index.

›

Pretax impairments of $5.5M in 4Q11 vs $6.2M in 4Q10

›

AOCI of $1,013.5M at 12/31/11 vs $432.5M at 12/31/10

›

RMBS $3.6B

›

Gross premium of ($66.2M)

›

Gross discount of $73.7M

›

Average mortgage loan rate = 5.4%

›

Outstanding long-term equity portfolio performance:

Life-to-date

annualized

total

return

of

9.7%

(vs

2.6% for

S&P 500 Total Return Index)

›

Life-to-date

annualized

total

return

for

REITs

of

2.7%

vs benchmark total return of 2.6%

›

European exposure of $1.4B

›

$0.6M of sovereign

›

$157.1M of financials

›

Largest holding = $116M of Shell

›

Commercial mortgage loans offer attractive yields:

4Q11 originations funded at over 300 bp spread to

Treasurys

Fixed

maturities,

87.5%

Equities,

1.0%

REITs¹

, 0.6%

Commercial

mortgage

Limited

partnerships,

0.9%

and other,

0.4%

Policy loans

loans, 9.6%

2

2

3 |

Impact of Federal Healthcare Reform

›

On March 23, 2010, the Patient Protection and Affordable Care Act (PPACA) was

signed into law:

›

Brings substantial change to insurance coverage for medical costs

›

Many changes apply primarily to fully insured group health plans, but some

provisions apply to self-funding

›

Many provisions of PPACA need to be clarified and will require follow-up

legislation ›

Specifically, PPACA:

›

Affects the market for major medical and mini-med plans

›

Mandates elimination of certain limits and exclusions

›

Establishes new payout standards with Medical Loss Ratio minimums

›

Studies find that the majority of employers (74% ) intend to continue to

offer employee healthcare plans, despite concerns that costs will rise as a

result of healthcare reform 26

1

Towers Watson survey, May 2010

Elimination of

coverage limitations

Ongoing medical

cost inflation

Increasing costs

of major medical

insurance

More employers to

self-fund their plans

and manage their

risks with stop-loss

insurance

1 |

Non-GAAP Measures

Adjusted Operating Income

Adjusted

Operating

Income

per

Common

Share

–

Diluted,

or

Operating

EPS

Adjusted Book Value

Operating Return on Average Equity, or Operating ROAE

Tangible Book Value

27

Adjusted operating income consists of net income, less after-tax net realized investment gains

(losses), plus after-tax net investment gains (losses) on our fixed indexed annuity

(FIA) options. Net income is the most directly comparable GAAP measure to adjusted operating

income. Adjusted operating income per common share – diluted, consists of adjusted operating income,

divided by the GAAP-basis weighted average diluted shares outstanding. Net

income per common share – diluted is the most directly comparable GAAP measure to adjusted

operating income per common share – diluted. Adjusted book value consists of stockholders’ equity, less accumulated other comprehensive income

(AOCI). Stockholders’ equity is the most directly comparable GAAP measure to

adjusted book value. Operating return on average equity, or operating ROAE, consists of adjusted operating income for the

most recent four quarters, divided by average adjusted book value, both of which are

non-GAAP measures. We measure average adjusted book value by averaging adjusted book value

for the most recent five quarters. Return on stockholders’ equity, or ROE, is the most directly

comparable GAAP measure. Return on stockholders’ equity for the most recent four quarters is

calculated as net income for such period divided by the average stockholders’ equity for

the most recent five quarters. Tangible book

value is a non-GAAP financial measure calculated as stockholders’ equity excluding deferred policy acquisition costs,

goodwill and other non-tangible assets. Stockholders’ equity is the most directly comparable

GAAP measure to tangible book value. |

Reconciliation of Non-GAAP Measures

28

Twelve Months Ended

December 31

2011

2010

Net income

$199.6

$200.9

Less: Net realized investment gains (net of

taxes)

4.6

25.9

Add: Net investment gains (losses) on FIA

options (net of taxes)

(0.9)

0.2

Adjusted operating income

$194.1

$175.2

Adjusted operating income per diluted share

of common stock

1,2

$ 1.41

$ 1.29

Twelve Months Ended

December 31

2011

2010

Return on equity (ROE)

7.3%

9.3%

Average book value

$ 2,730.6

$ 2,167.9

Operating return on average equity (ROAE)

9.5%

9.8%

Average adjusted book value

$ 2,033.7

$ 1,795.4

1

A non-GAAP measure; see slide 27 for a definition of this measure.

2

Diluted weighted average shares outstanding for the 12 months ended Dec. 31, 2011 and 2010 were

137.503 million and 135.618 million, respectively.

$ in millions

$ in millions

1

1 |

Reconciliation of Non-GAAP Measures (cont.)

29

Twelve Months Ended

December 31

2011

2010

Segment pretax adjusted operating income (loss):

Benefits

$ 79.2

$ 71.6

Deferred Annuities

102.1

81.3

Income Annuities

35.1

33.2

Life

64.9

74.9

Other

(10.7)

(11.4)

Pretax adjusted operating income

270.6

249.6

Add: Net realized investment gains, excluding net

investment gains (losses) on FIA options

8.4

39.5

Income from operations before income taxes

$279.0

$289.1

$ in millions

$ in millions |

Reconciliation of Non-GAAP Measures (cont.)

$ in millions

As of Dec. 31,

2011

Total stockholders‘

equity

3,134.0

Less:

Deferred policy acquisition costs

215.4

Goodwill

30.4

Intangible assets

26.7

Other non-tangible assets

63.6

Tangible book value

$ 2,797.9

30

1

A non-GAAP measure; see slide 27 for a definition of this measure.

1 |

Symetra®

and the Symetra logo are registered service marks of Symetra Life Insurance

Company, 777 108 Ave NE, Suite 1200, Bellevue, WA 98004.

th |