Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CVR ENERGY INC | d296554d8k.htm |

Credit Suisse Global Energy Conference

February 8, 2012

Exhibit 99.1 |

1

1

1

1

1

This

presentation

should

be

reviewed

in

conjunction

with

CVR

Energy,

Inc.’s

Third

Quarter

earnings

conference

call

held

on

November

3,

2011.

The

following

information

contains

forward-looking

statements

based

on

management’s

current

expectations

and

beliefs,

as

well

as

a

number

of

assumptions

concerning

future

events.

These

statements

are

subject

to

risks,

uncertainties,

assumptions

and

other

important

factors.

You

are

cautioned

not

to

put

undue

reliance

on

such

forward-looking

statements

(including

forecasts

and

projections

regarding

our

future

performance)

because

actual

results

may

vary

materially

from

those

expressed

or

implied

as

a

result

of

various

factors,

including,

but

not

limited

to

(i)

those

set

forth

under

“Risk

Factors”

in

CVR

Energy,

Inc.’s

Annual

Report

on

Form

10-K,

Quarterly

Reports

on

Form

10-Q

and

any

other

filings

CVR

Energy,

Inc.

makes

with

the

Securities

and

Exchange

Commission,

and

(ii)

those

set

forth

under

“Risk

Factors”

and

“Cautionary

Note

Regarding

Forward-Looking

Statements”

in

the

CVR

Partners,

LP

Prospectus

and

any

other

filings

CVR

Partners,

LP

makes

with

the

Securities

and

Exchange

Commission.

CVR

Energy,

Inc.

assumes

no

obligation

to,

and

expressly

disclaims

any

obligation

to,

update

or

revise

any

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise. |

2

2

2

2

2

Management Attendees

Jack Lipinski

Chief Executive Officer

Ed Morgan

Executive Vice President of Investor Relations

Jay Finks

Director of Finance |

Company Overview |

4

4

4

4

4

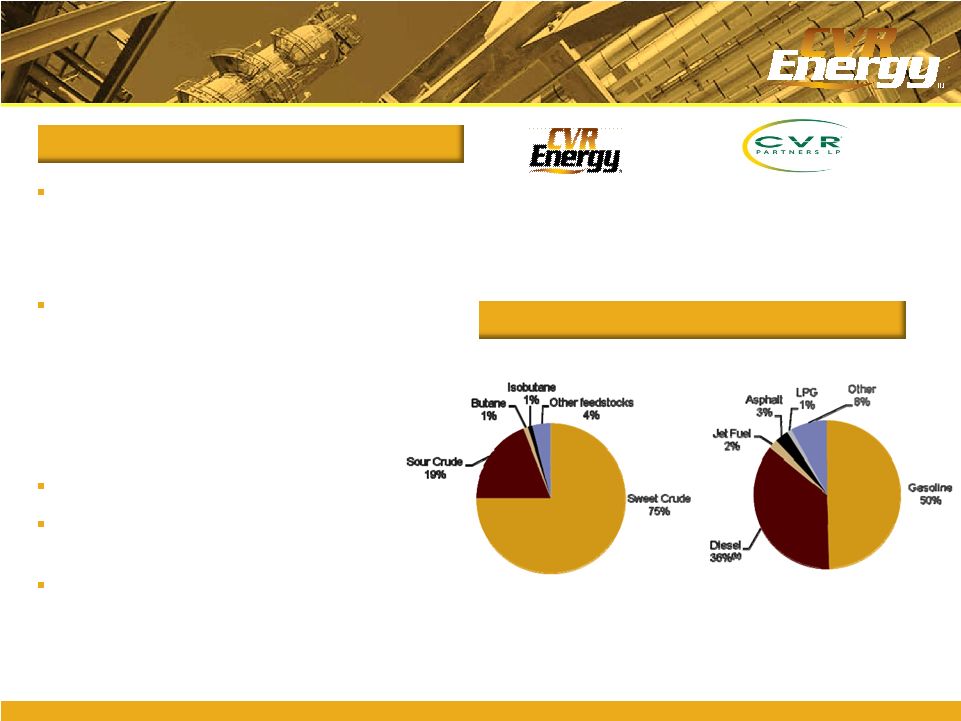

Pro Forma Company Overview

Two top-tier Mid-Continent refineries

–

115,000 bpd Coffeyville, Kansas refinery

–

70,000 bpd Wynnewood, Oklahoma

Refinery

A nitrogen fertilizer plant using pet coke

gasification (CVR Partners LP)

–

Rated capacity of 1,225 tpd ammonia;

2,025 tpd UAN Nitrogen

–

Current $100.0 million expansion

ongoing to increase UAN capacity by

400,000 tons

Operates in higher margin markets

Logistics assets supporting both

businesses

Financial flexibility

Pro Forma LTM Refinery Feedstock &

Product Slate

(a)

CVR Energy: About Us

Note: LTM as of September 30, 2011.

(a)

Pro forma based on weighted average of refinery capacity.

(b)

CVR distillate assumed to be diesel for pro forma.

NYSE–

CVI

Market Cap(1) -

$2.3 billion

NYSE–

UAN

Market Cap(1) -

$2.2 billion

CVI owns ~ 70%

(1)

As of 2/2/2012 |

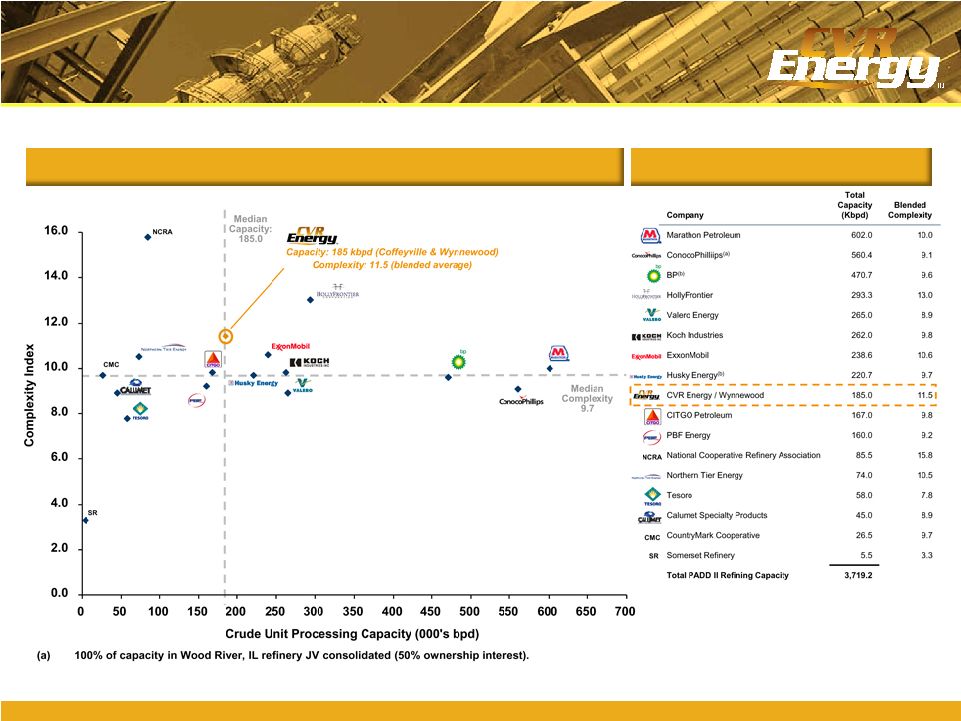

5

5

5

5

5

(b)

Includes 50% interest in JV in Toledo, OH refinery.

Source: EIA and Wall Street research

PADD II Consolidated Refinery Statistics –

By Owner

“Top Quartile”

Consolidated Asset Profile

PADD II Refiners

Well Positioned to Compete in

Underserved PADD II Region |

6

6

6

6

6

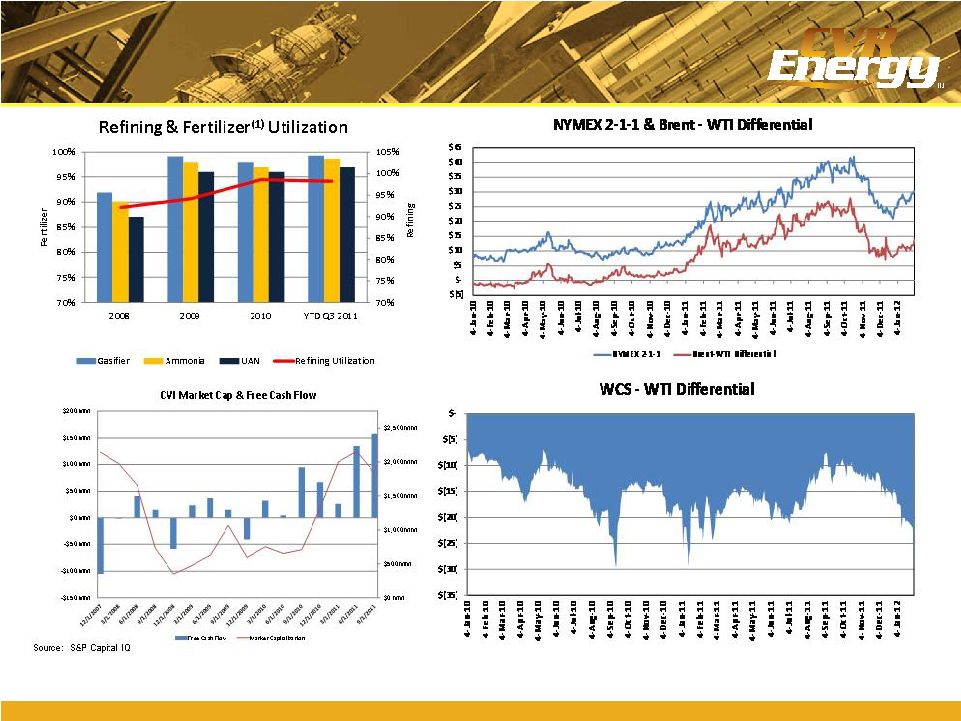

Key Business Drivers

(1) Adjusted for major scheduled turnaround, third-party outage on air

separation unit and UAN vessel rupture |

7

7

7

7

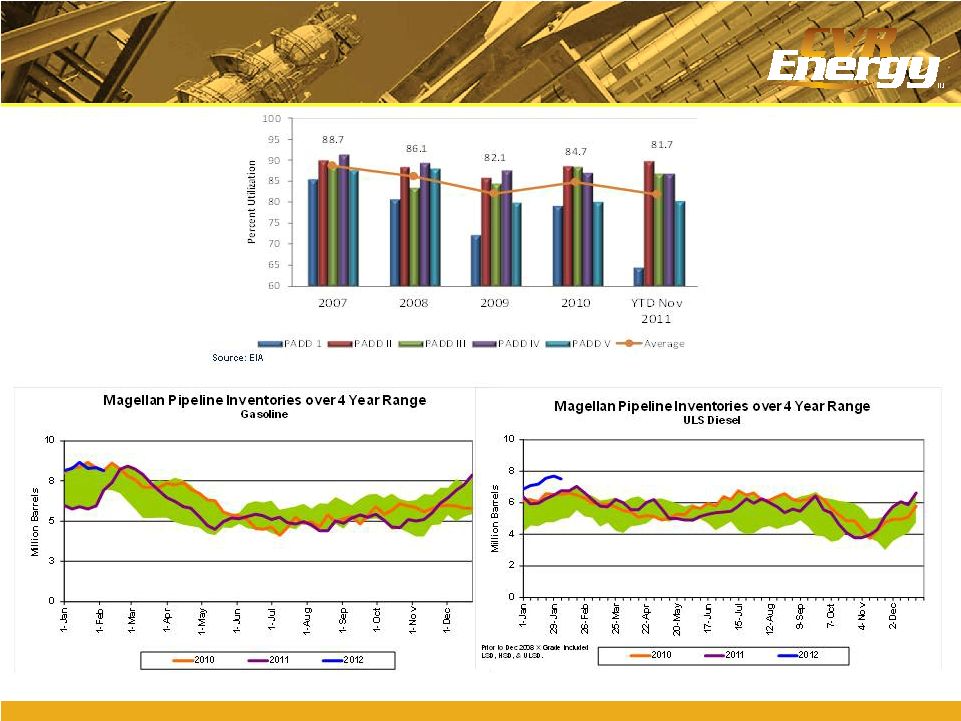

7

Utilization by PADD

Source: Magellan |

8

8

8

8

8

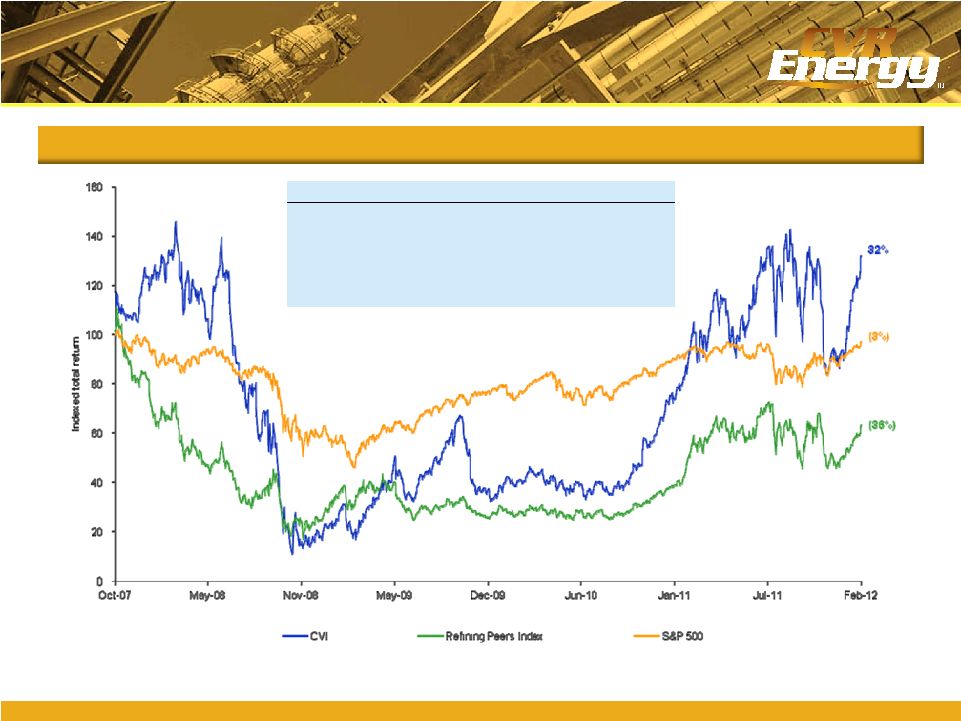

CVR Energy total shareholder return

Note:

Market data as of February 3, 2012. Peer index equal weighted and includes ALJ,

DK, HFC, TSO and WNR. CVI IPO price is based on closing price of the first day of

trading.

Source: Capital IQ

Refiners relative total return performance

CVI

Refining peers

S&P 500

Since IPO

32%

(36%)

(3%)

3-year

405%

78%

71%

2-year

230%

140%

28%

1-year

57%

34%

5%

1-month

36%

18%

5% |

9

9

9

9

9

Building the business

Responsive to opportunities

Improving financial strength

Shareholder Value Focused

Increased total refining capacity to 185 kbpd

Integrating Wynnewood acquisition and

realizing synergies

Grown crude gathering to ~40,000 bpd

Expanding UAN capacity by 400,000 tpy

IPO of CVR Partners

Accretive acquisition of GWEC

Considering regular, fixed dividend initiation

Continuously evaluating alternatives to

realize CVR Partners’

value

Conservative leverage metrics

Tactical hedging for risk management

Ratings improvement to Ba3

Focus on maintaining discipline

Since IPO, CVR Energy is #1 in total

return among refining peers

(a)

and

remains focused on creating value for

shareholders

(a)

Total return based on period from October 23, 2007 to February 3, 2012. CVI

total return compared to total return of refining peers: ALJ, DK, HFC, TSO and WNR. |

Refining Business |

11

11

11

11

11

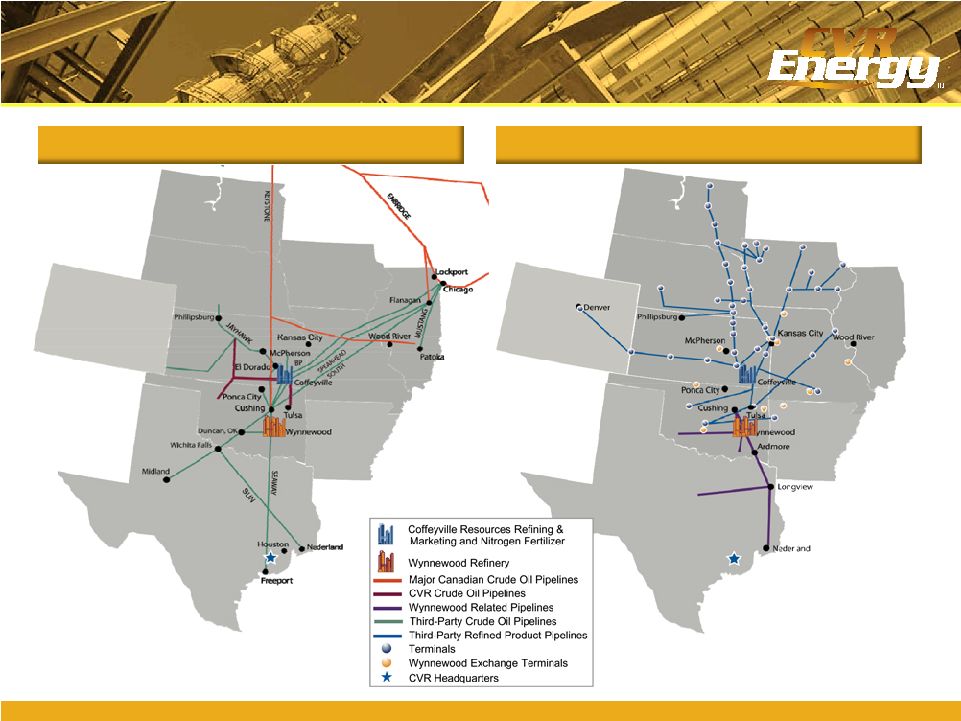

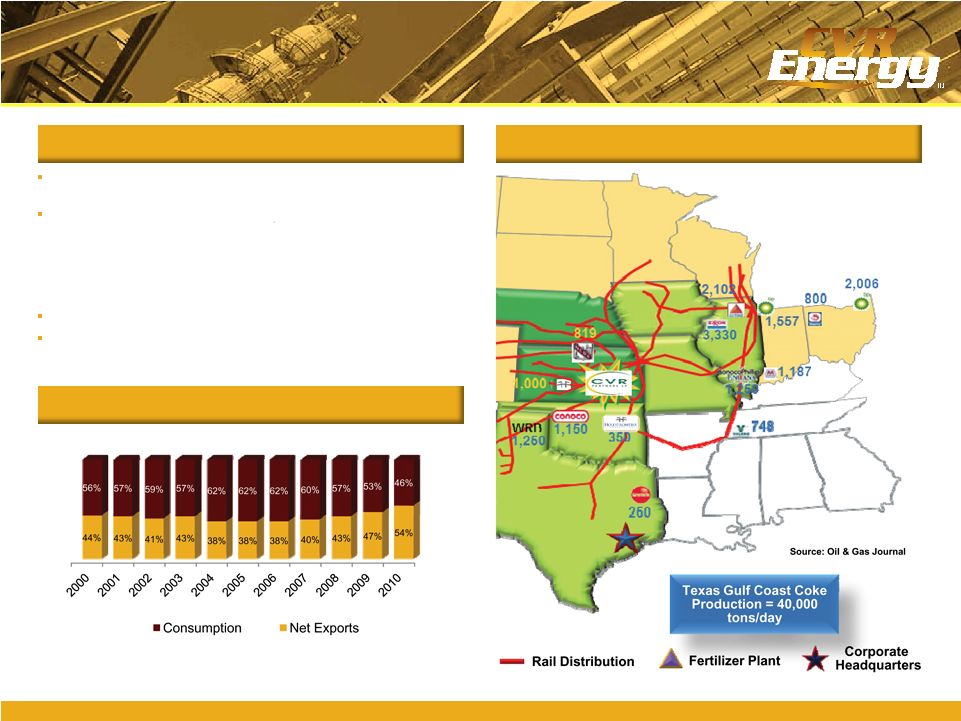

Consolidated Supply Network

Consolidated Marketing Network

Extensive Crude Oil Supply and

Product Distribution Network |

12

12

12

12

12

Logistics Overview

Operations Map

Logistics Drives Profitability

(a)

Under construction.

Located 100 miles from the global crude hub of

Cushing, CVR has access to global crudes with

storage to optimize purchasing and crude slates

Shipper status of 35,000 bpd on Spearhead and

Keystone Pipelines

40,000+ bpd crude oil gathering system serving

Kansas, Oklahoma, Missouri and Nebraska

145,000 bpd proprietary pipeline system to

transport crude to the Coffeyville refinery

Currently constructing an additional one million

barrel storage facility in Cushing |

13

13

13

13

13

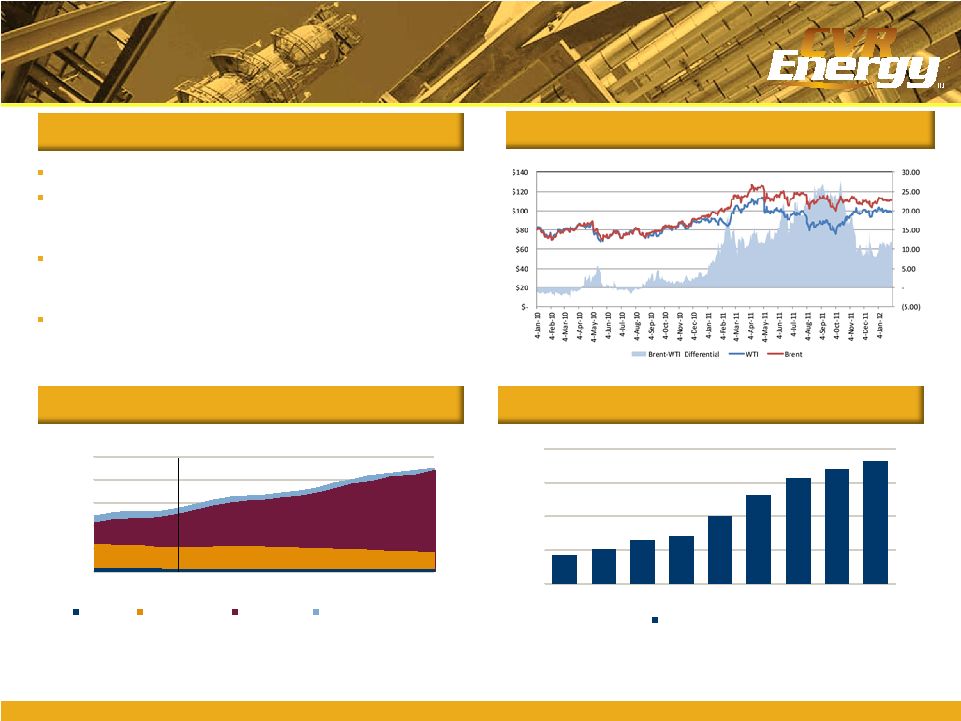

Overview

Historical & Projected Canadian Production

Historical & Projected Bakken Crude Production

Access to WTI Priced Crudes

(a)

Source: Canadian Association of Petroleum Producers June 2011 publication.

Source: Wood Mackenzie Upstream Service database

Both refineries benefit from the current WTI-Brent spread

WTI price-linked crudes are currently trading at

historically wide discounts to crudes, such as Brent

and

LLS

Growing production from the U.S. Bakken and Canada

flowing into Cushing, OK is contributing to this

differential

Expected pipeline capacity (Seaway reversal) necessary

to move production from Cushing to the Gulf Coast

projected to move 250k bpd heavy/sour by 2013

0

1,000

2,000

3,000

4,000

5,000

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

Other

Conventional

Oil Sands

Atlantic Canada Offshore

(thousand barrels per day)

Actual

Forecast

87.6

102.1

132.7

142.3

201.8

262.9

313.1

340.0

362.4

0

100

200

300

400

2006

2007

2008

2009

2010

2011

2012

2013

2014

Bakken Crude Production

(thousand barrels per day)

Historical WTI-Brent Spread ($/bbl) |

14

14

14

14

14

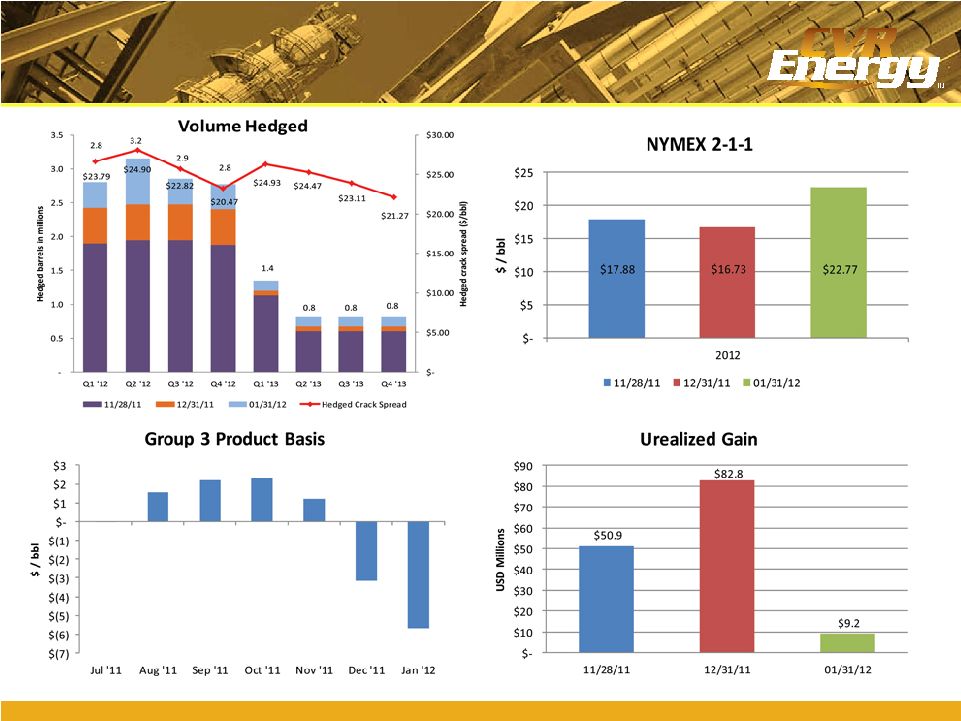

Hedging Activity |

15

15

15

15

15

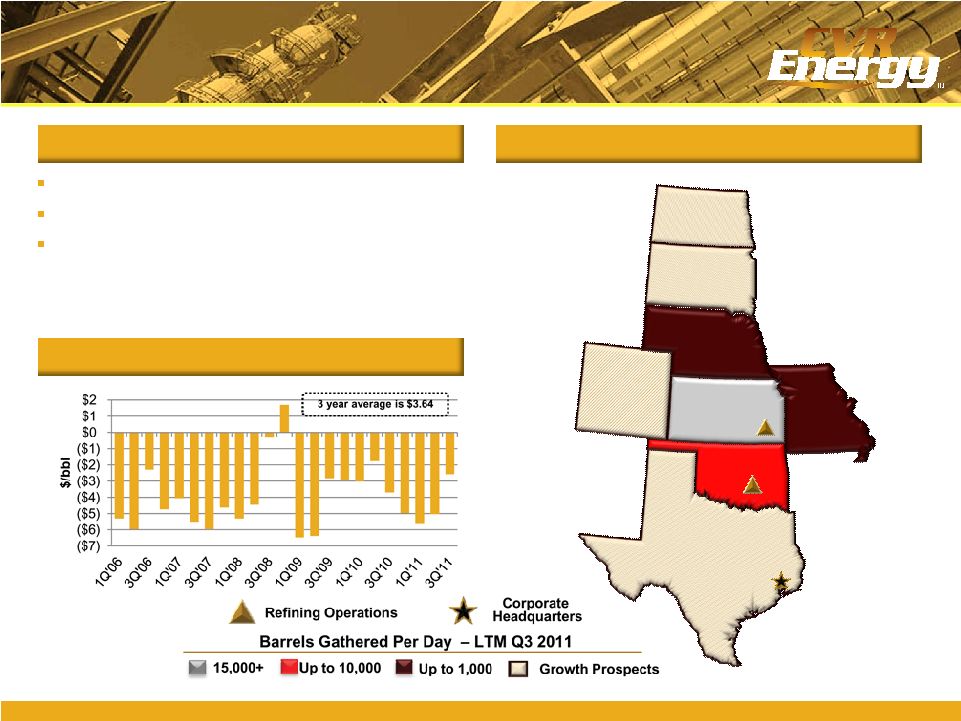

Overview

Asset Map

Total Consumed Crude Discount to WTI

Crude Gathering

Gathered 7,000 bpd in 2005

Today gathering over 40,000+ bpd

Growth target 10% –

20% per year for the

next 2 –

5 years

Texas

Oklahoma

Missouri

Nebraska

Kansas

Colorado

South Dakota

North Dakota |

16

16

16

16

16

Phillipsburg

Valley Center

Station

Winfield

(Gathering South)

Plainville

(Gathering North)

Hooser

Station

Broome

Station

Humboldt

(Gathering South)

Coffeyville

East Tank Farm

Cushing

Plains/TEPPCO

Bartlesville

(Gathering South)

Shidler

(Gathering South)

55k

2,700k

Capacity 17,900 bpd w/DRA

Capacity 4,800 bpd

Capacity 24,000 bpd w/DRA

Capacity 110,000 bpd

Capacity 5,100 bpd

Capacity 4,700 bpd

Capacity 38,000 bpd

660k

160k

75k

200k

10k

40k

20k

20k

Jayhawk/Kaw

Pipeline system

150 miles

67 miles

23 miles

100 miles

Plains Pipeline

20 miles

19 miles

42 miles

1.6 miles

62.5 miles

Capacity 107,000 bpd

18 miles

156,000 b/d

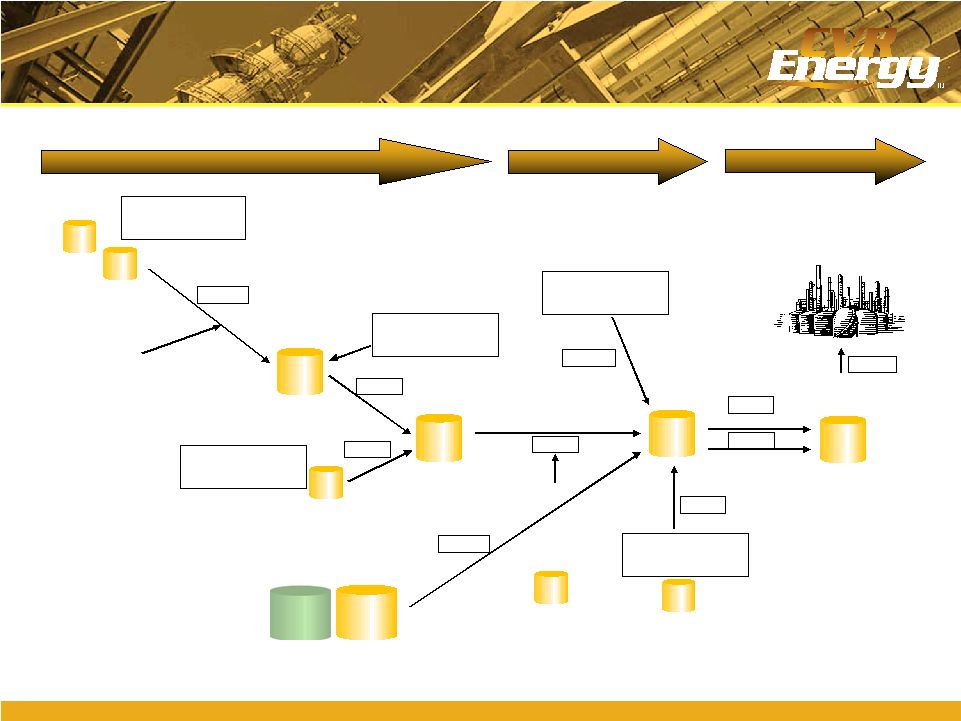

Crude Gathering System

“No Barrel Left Behind”

Gathered

Blended

Refined

Osage Station

1,000k |

Nitrogen Fertilizer MLP |

18

18

18

18

18

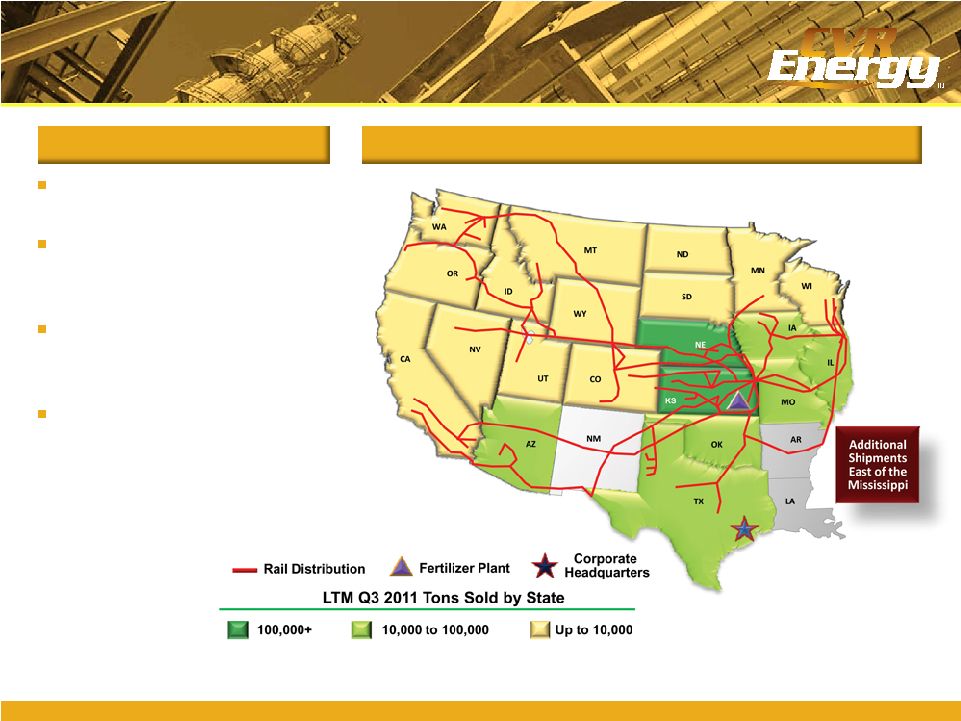

Overview

Fertilizer Operations

Strategically Located Assets and Logistics

Located in the corn belt

(on Union Pacific

mainline)

45% of corn planted in

2010 was within $35/UAN

ton freight rate of our plant

$25/ton transportation

advantage to corn belt vs.

US Gulf

Coast

No intermediate transfer,

storage, barge freight or

pipeline freight charges

LTM Q3 2011 Total Tons Sold ~ 731,500 |

19

19

19

19

19

Overview

Abundant Supply of Third-party Pet Coke

US Pet Coke Exports and Consumption

Stable & Economic Feedstock

Source: EIA

CVR Partners LP 2008 –

2010 average daily coke demand ~ 1,378

tons/day

Coke gasification technology uses petroleum coke as a feedstock

–

Pet coke costs lower than natural gas costs per ton of ammonia

produced, and pet coke prices are significantly more stable than

natural gas prices

–

Over 70% of pet coke supplied by refinery through long-term

contract

Dual train gasifier configuration ensures reliability

Ammonia synthesis loop and UAN synthesis use same processes as

natural gas based producers |

20

20

20

20

20

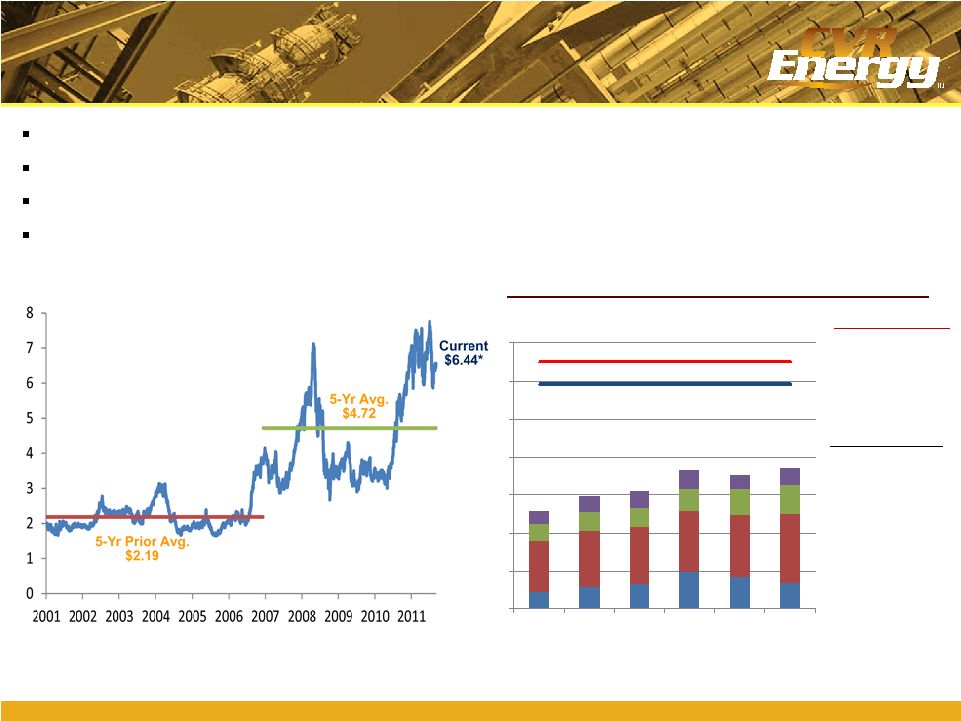

Market Fundamentals

Farmer Profitability Supports Fertilizer Pricing

Corn consumes the largest amount of nitrogen fertilizer

Farmers are expected to generate substantial proceeds at currently forecasted corn

prices Farmers are still incentivized to apply nitrogen fertilizer at corn

prices lower than current spot Nitrogen fertilizer represents a small

percentage of a farmer’s input costs Corn Spot Prices

Breakdown of U.S. Farmer Total Input Costs

Input Costs and Prices per Bushel ($)

Other Variable Costs 13%

Seed and Chemicals 18%

Fixed Costs 48%

Avg. % Total of Cost:

Corn Futures Prices*:

30 Day: $6.52

12 Month: $5.93

Note: Fixed Costs include labor, machinery, land, taxes, insurance, and other.

Fertilizers 21%

*As of Feb. 4, 2012

Source: CIQ

*As of Feb .4, 2012

Source: CIQ, USDA

2.60

2.97

3.10

3.68

3.53

3.71

-

1

2

3

4

5

6

7

2005

2006

2007

2008

2009

2010 |

21

21

21

21

21

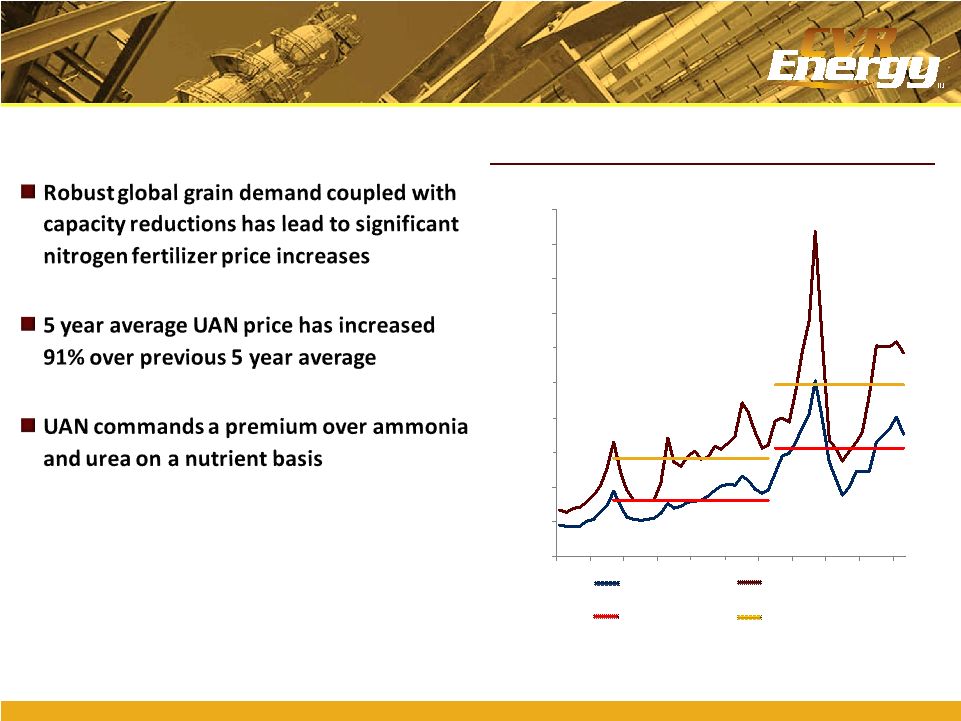

Market Fundamentals

Strong Pricing Environment

($ per Ton)

Historical U.S. Nitrogen Fertilizer Prices

0

100

200

300

400

500

600

700

800

900

1,000

1999

2000

2001

2002

2004

2005

2006

2007

2009

2010

2011

Ammonia

$686

UAN

$352

Southern Plains

Ammonia

Corn Belt UAN

5-Yr Average Southern

Plains Ammonia

Source:

Green Markets Data, Fertecon

5 Yr. Avg.

UAN $163

5-Yr Average

Corn Belt UAN

5 Yr. Avg.

Ammonia $283

5 Yr. Avg.

Ammonia $493

5 Yr. Avg.

UAN $312 |

Financial Highlights |

23

23

23

23

23

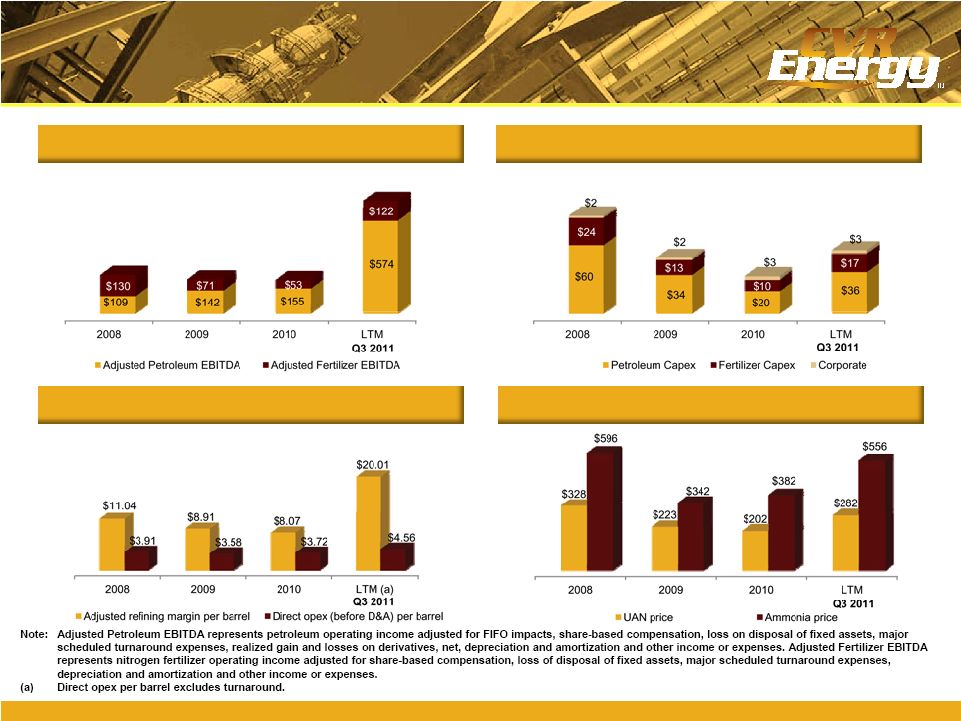

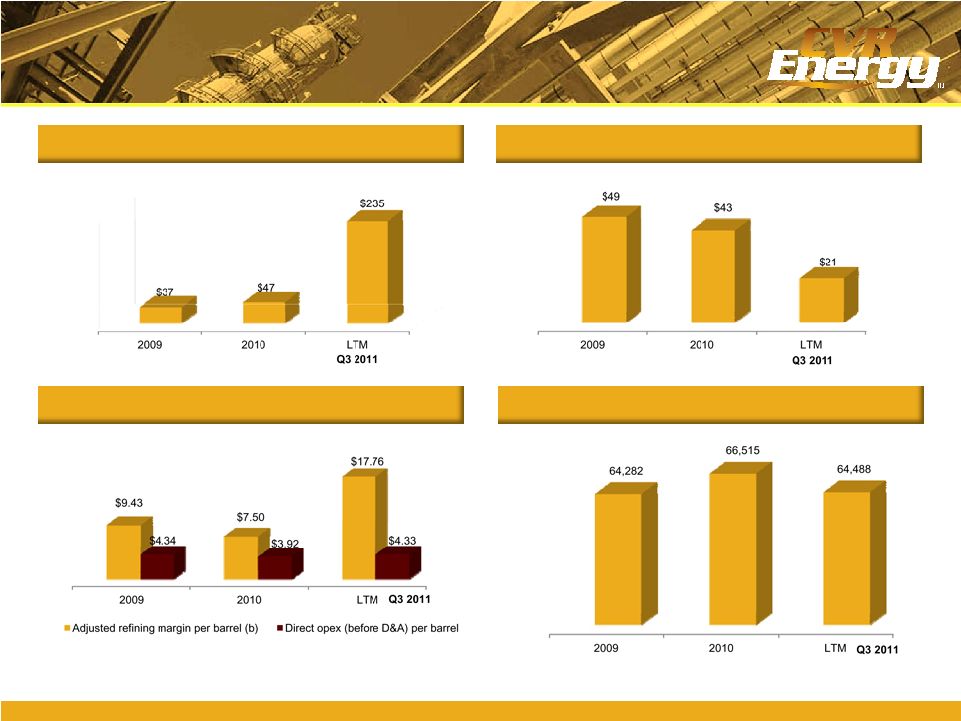

EBITDA by Operating Segment ($mm)

Capital Expenditures ($mm)

Refining Margins and Expenses ($/bbl)

Fertilizer Prices ($/Ton)

Key Historical Financial Statistics

CVR Energy Standalone |

24

24

24

24

24

Adjusted EBITDA ($mm)

(a)

Capital Expenditures ($mm)

Refining Margins and Expenses ($/bbl)

Total Throughput (bpd)

Key Historical Financial Statistics

Gary Williams Standalone

(a)

Adjusted EBITDA represents GWEC operating income adjusted for FIFO impacts, major

scheduled turnaround expenses, realized gain and losses on derivatives, net,

depreciation and amortization and other income or expenses.

(b)

Adjusted refining margin per barrel is equal to gross operating margin adjusted for

FIFO inventory gains or losses divided by crude throughput. |

25

25

25

25

25

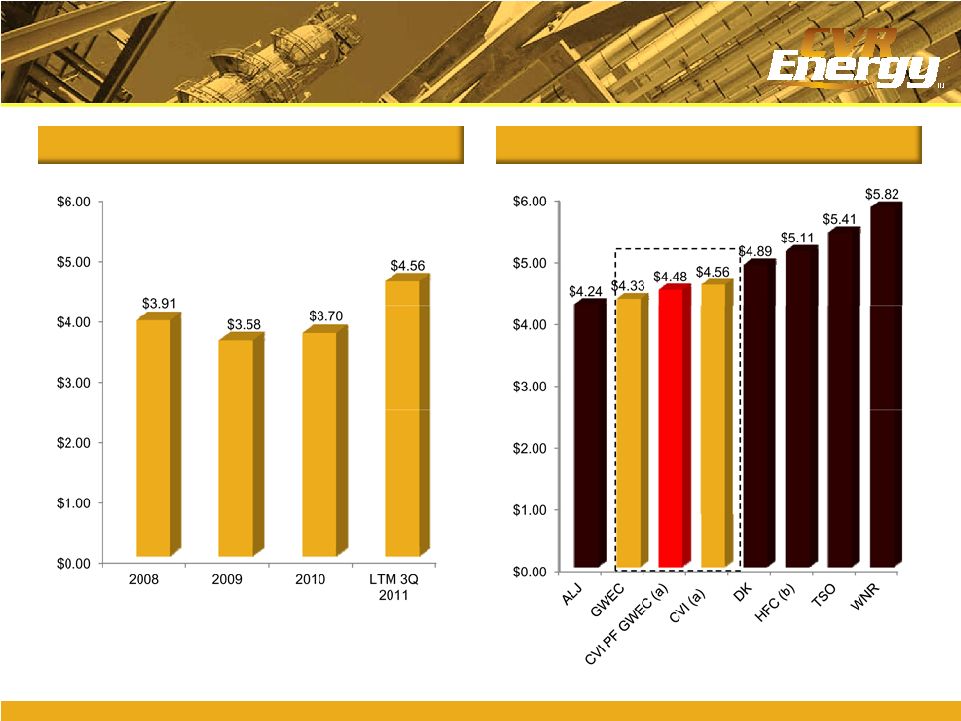

CVI Operating Expenses

(a)

($/bbl)

LTM Q3 ‘11 Operating Expense ($/bbl)

Combined Company –

Controlled Operating Expenses

(a)

Excludes

turnaround.

CVI

PF

GWEC

based

on

weighted

average

crude

throughput.

(b)

HFC

combined

results

from

legacy

companies

3Q

2011

report. |

Appendix |

27

27

27

27

27

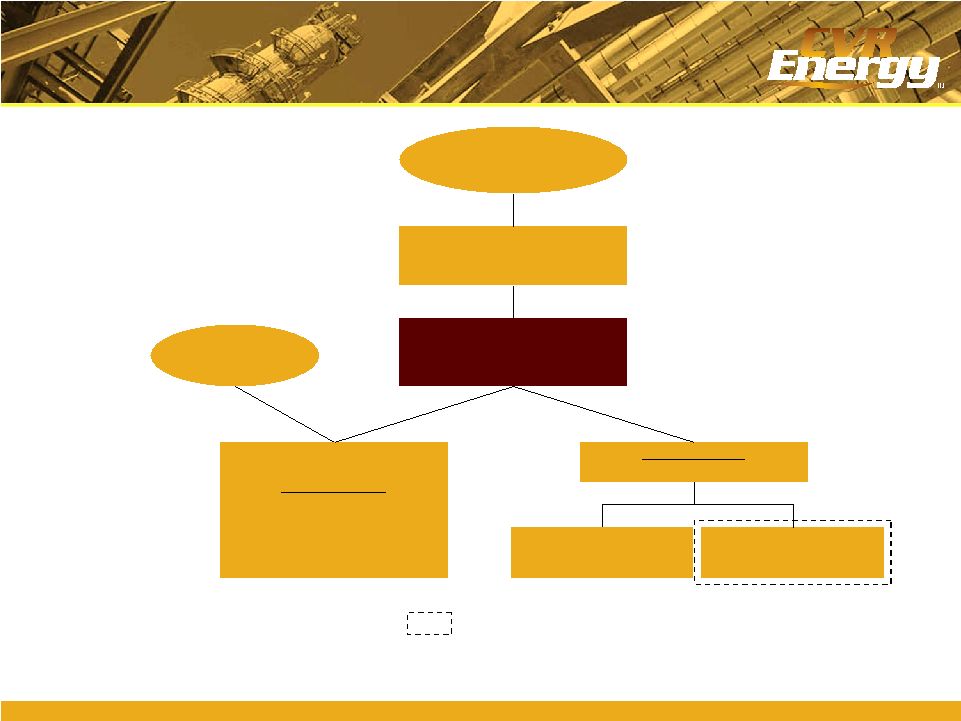

Pro Forma Organizational Structure

CVR Energy, Inc.

NYSE: CVI

Market cap: ~$2.2 bn

Coffeyville Resources, LLC

Fertilizer business

CVR Partners, LP

NYSE: UAN

Market cap: ~$1.8 bn

Refining business

~$809 mm LTM EBITDA

Public shareholders

Public unitholders

100%

100%

100% GP

69.7% LP

30.3% LP

Wynnewood Refinery (GWEC)

(Wynnewood, OK)

Coffeyville Refinery

(Coffeyville, KS)

100%

100%

Represents Acquisition

$400m ABL due ’15

$447m 9% 1

st

Lien notes due ‘15

$223m 10

7/8

% 2

nd

Lien notes due ‘17

$25m cash flow revolver due ’16

$125m term loan due ‘16 |

28

28

28

28

28

Non-GAAP Financial Measures

To

supplement

the

actual

results

in

accordance

with

U.S.

generally

accepted

accounting

principles

(GAAP),

for

the

applicable

periods,

the

Company

also

uses

certain

non-GAAP

financial

measures

as

discussed

below,

which

are

adjusted

for

GAAP-based

results.

The

use

of

non-GAAP

adjustments

are

not

in

accordance

with

or

an

alternative

for

GAAP.

The

adjustments

are

provided

to

enhance

the

overall

understanding

of

the

Company’s

financial

performance

for

the

applicable

periods

and

are

also

indicators

that

management

utilizes

for

planning

and

forecasting

future

periods.

The

non-GAAP

measures

utilized

by

the

Company

are

not

necessarily

comparable

to

similarly

titled

measures

of

other

companies.

The

Company

believes

that

the

presentation

of

non-GAAP

financial

measures

provides

useful

information

to

investors

regarding

the

Company’s

financial

condition

and

results

of

operations

because

these

measures,

when

used

in

conjunction

with

related

GAAP

financial

measures

(i)

together

provide

a

more

comprehensive

view

of

the

Company’s

core

operations

and

ability

to

generate

cash

flow,

(ii)

provide

investors

with

the

financial

analytical

framework

upon

which

management

bases

financial

and

operational

planning

decisions,

and

(iii)

presents

measurements

that

investors

and

rating

agencies

have

indicated

to

management

are

useful

to

them

in

assessing

the

Company

and

its

results

of

operations. |

29

29

29

29

29

Non-GAAP Financial Measures (cont’d)

EBITDA:

EBITDA

represents

net

income

before

the

effect

of

interest

expense,

interest

income,

income

tax

expense

(benefit)

and

depreciation

and

amortization.

EBITDA

is

not

a

calculation

based

upon

GAAP;

however,

the

amounts

included

in

EBITDA

are

derived

from

amounts

included

in

the

consolidated

statement

of

operations

of

the

Company.

Adjusted

EBITDA

by

operating

segment

results

from

operating

income

by

segment

adjusted

for

items

that

the

company

believes

are

needed

in

order

to

evaluate

results

in

a

more

comparative

analysis

from

period

to

period.

Additional

adjustments

to

EBITDA

include

major

scheduled

turnaround

expense,

the

impact

of

the

Company’s

use

of

accounting

for

its

inventory

under

first-in,

first-out

(FIFO),

net

unrealized

gains/losses

on

derivative

activities,

share-based

compensation

expense,

loss

on

extinguishment

of

debt,

and

other

income

(expense).

Adjusted

EBITDA

is

not

a

recognized

term

under

GAAP

and

should

not

be

substituted

for

operating

income

or

net

income

as

a

measure

of

performance

but

should

be

utilized

as

a

supplemental

measure

of

financial

performance

in

evaluating

our

business.

First-in,

first-out

(FIFO):

The

Company’s

basis

for

determining

inventory

value

on

a

GAAP

basis.

Changes

in

crude

oil

prices

can

cause

fluctuations

in

the

inventory

valuation

of

our

crude

oil,

work

in

process

and

finished

goods,

thereby

resulting

in

favorable

FIFO

impacts

when

crude

oil

prices

increase

and

unfavorable

FIFO

impacts

when

crude

oil

prices

decrease.

The

FIFO

impact

is

calculated

based

upon

inventory

values

at

the

beginning

of

the

accounting

period

and

at

the

end

of

the

accounting

period. |

30

30

30

30

30

Non-GAAP Financial Measures (cont’d)

CVR 9/30/11 LTM Adjusted EBITDA ($mm)

LTM 9/30/2011

Consolidated Net Income

$282.2

Interest expense, net of interest income

53.8

Depreciation and amortization

88.1

Income tax expense

181.5

EBITDA adjustments included in NCI

(3.4)

Unrealized (gain)/loss on derivatives

9.8

Loss on disposal of fixed assets

2.9

FIFO impact (favorable), unfavorable

(30.4)

Share based compensation

52.4

Loss on extinguishment of debt

3.6

Major turnaround expense

16.5

Other non-cash expenses

-

Consolidated Adjusted EBITDA

$657.0

Fertilizer Adjusted EBITDA

121.7

Adjusted EBITDA excl. Fertilizer

$535.3 |

31

31

31

31

31

Non-GAAP Financial Measures (cont’d)

CVR Adjusted EBITDA ($mm)

Petroleum:

2008

2009

2010

LTM 9/30/2011

Petroleum operating income

$31.9

$170.2

$104.6

$529.5

FIFO impact (favorable) unfavorable

102.5

(67.9)

(31.7)

(30.4)

Share-based compensation

(10.8)

(3.7)

11.5

17.1

Loss on disposal of fixed assets

-

-

1.3

1.5

Major scheduled turnaround

-

-

1.2

12.8

Realized gain (loss) on derivatives, net

(121.0)

(21.0)

0.7

(24.7)

Goodwill impairment

42.8

-

-

-

Depreciation and amortization

62.7

64.4

66.4

67.8

Other income (expense)

1.0

0.3

0.7

0.5

Adjusted EBITDA

$109.1

$142.3

$154.7

$574.1

Fertilizer:

2008

2009

2010

LTM 9/30/2011

Fertilizer operating income

$116.8

$48.9

$20.4

$84.0

Share-based compensation

(10.6)

3.2

9.0

14.1

Loss on disposal of fixed assets

2.3

-

1.4

1.4

Major scheduled turnaround

3.3

-

3.5

3.5

Depreciation and amortization

18.0

18.7

18.5

18.5

Other income (expense)

0.1

-

-

0.2

Adjusted EBITDA

$129.9

$70.8

$52.8

$121.7 |

32

32

32

32

32

Non-GAAP Financial Measures (cont’d)

(a)

Includes disposal of assets, asset impairments, discontinued operations and fire

related adjustments. GWEC Adjusted EBITDA ($mm)

GWEC:

2009

2010

LTM 9/30/2011

Net income (loss)

$52.5

$16.1

$161.6

Income taxes

-

-

-

Interest expense (net)

12.9

22.4

28.6

Depreciation and amortization

13.8

14.7

17.2

Hedge mark to market loss (gain)

-

-

37.9

Turnaround amortization

15.4

13.8

13.1

Non-cash inventory loss (gain)

(57.9)

(19.6)

(23.1)

Other unusual or non-recurring items

(a)

0.1

-

(0.2)

Adjusted EBITDA

$36.8

$47.4

$235.1 |