Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CVR PARTNERS, LP | d282801d8k.htm |

Exhibit 99.1 |

2

The

following

information

contains

forward-looking

statements

based

on

management’s

current

expectations

and

beliefs,

as

well

as

a

number

of

assumptions

concerning

future

events.

These

statements

are

subject

to

risks,

uncertainties,

assumptions

and

other

important

factors.

You

are

cautioned

not

to

put

undue

reliance

on

such

forward-looking

statements

(including

forecasts

and

projections

regarding

our

future

performance)

because

actual

results

may

vary

materially

from

those

expressed

or

implied

as

a

result

of

various

factors,

including,

but

not

limited

to

those

set

forth

under

“Risk

Factors”

and

“Cautionary

Note

Regarding

Forward-Looking

Statements”

in

the

CVR

Partners,

LP

Prospectus

dated

April

7,

2011

and

any

other

filings

CVR

Partners,

LP

makes

with

the

Securities

and

Exchange

Commission.

CVR

Partners,

LP

assumes

no

obligation

to,

and

expressly

disclaims

any

obligation

to,

update

or

revise

any

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise.

Safe Harbor |

Company

Overview |

CVR Partners

Offering CVR Partners Offering

NYSE Ticker:

UAN

Total units with

over-allotment:

22.1m common units (30.2%)

Pricing:

$16 per LP unit ($3 higher than original mid-point)

March 31, 2012 LTM

estimated

distribution/yield:

$1.92 per unit / 12%

Use of proceeds:

Buy the GP and extinguish IDR’s, distribution to

Coffeyville Resources, general growth projects

including UAN expansion

As of January 12, 2012, CVR Partners market cap was $1.9 billion, of which $1.3 billion is

controlled by CVR Energy. CVR

Partners

is

a

growth

oriented

partnership

formed

by

CVR

Energy,

Inc.

in

June

2007.

CVR

Partners’

nitrogen

fertilizer

manufacturing

facility

produces

ammonia

and

Urea

Ammonium

Nitrate

(UAN).

The

facility

is

located

in

Coffeyville,

Kansas

and

produces

5%

of

the

total

UAN

demand

in

the

United

States.

4 |

5

Company Overview

Key Strategic Factors

Experienced management team

Fully utilized capacity

High run time rates

Strategically located plant

Favorable rail logistics

Stable & economic feedstock |

Company

Overview Experienced Management Team

Byron R. Kelley

CEO

Stan A. Riemann

COO

Frank A. Pici

CFO and Treasurer

Randal T. Maffett

EVP Business Development

Edmund S. Gross

SVP, General Counsel & Secretary

Years Experience: 41

Years Experience: 37

Years Experience: 28

Years Experience: 31

Years Experience: 33

6

Kevan A. Vick

EVP & GM Nitrogen Manufacturing

Years Experience: 36

Christopher G. Swanberg

VP Environmental, Health & Safety

Years Experience: 31 |

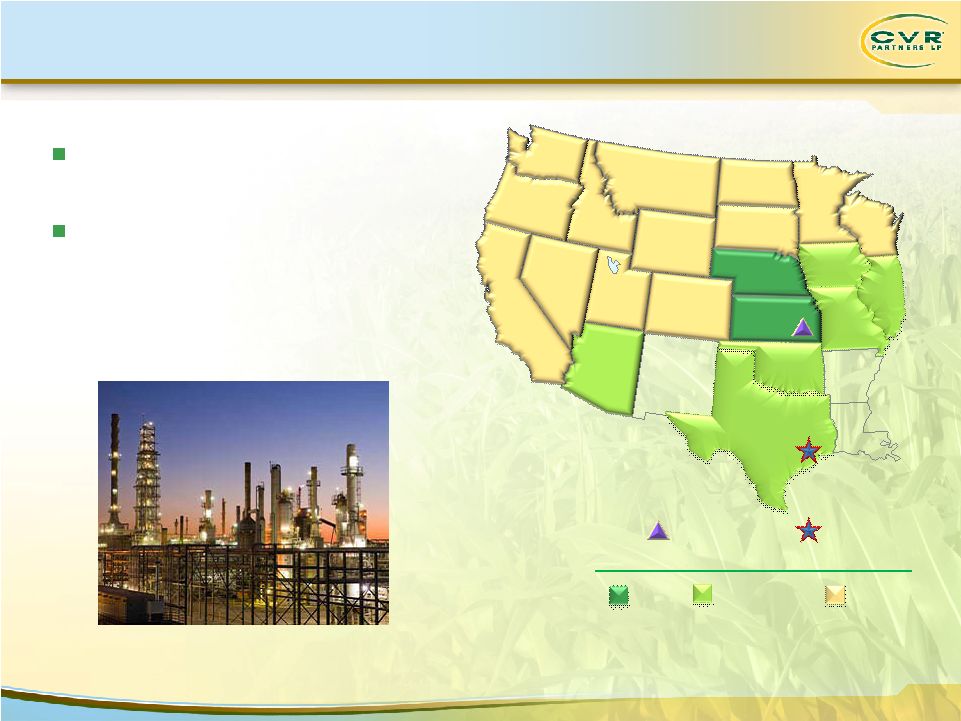

Company

Overview

Fully

Utilized

Capacity

/

High

Utilization

Rates

1)

Adjusted for major scheduled turnaround, third-party outage on air separation unit and UAN

vessel rupture. WA

OR

CA

NV

ID

MT

WY

UT

CO

NM

AZ

TX

OK

KS

NE

SD

ND

MN

IA

MO

AR

LA

WI

IL

Fertilizer Plant

Corporate

Headquarters

LTM Q3 2011 Tons Sold by State

100,000+

10,000 to 100,000

Up to 10,000

7

LTM Q3 2011 Total Tons Sold ~ 731,350

Capacity:

1,225

tons-per-day

ammonia

unit,

2,025

tons-per-day

UAN

unit

LTM

Q3

2011

on-stream

efficiency

(1)

—

Gasifier:

98.9%

—

Ammonia:

97.6%

—

UAN:

97.3% |

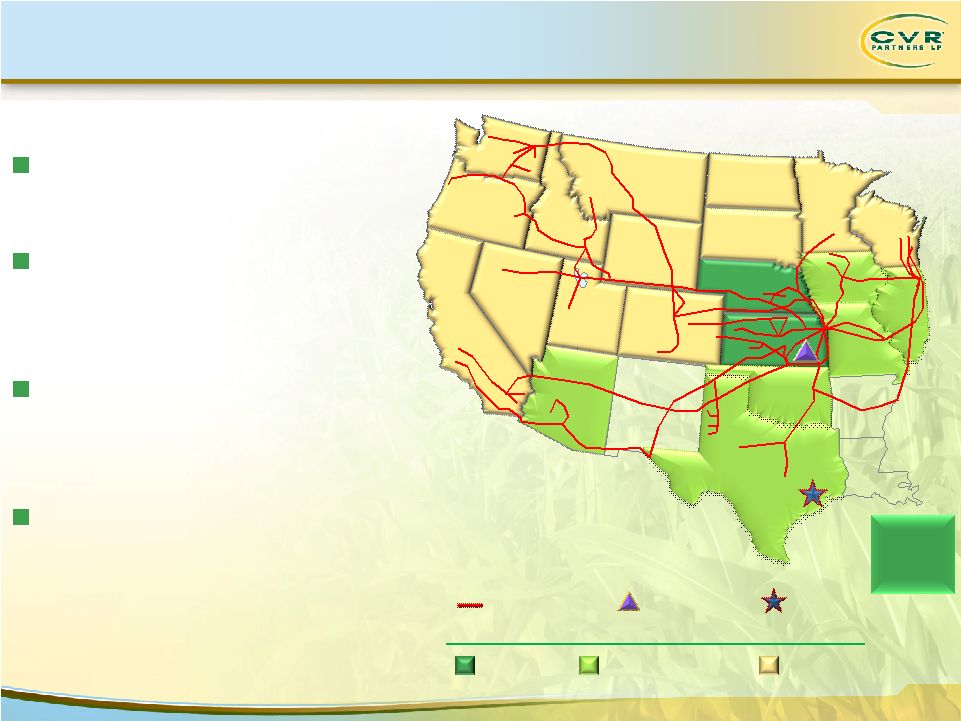

Company

Overview Strategically Located Assets & Logistics

8

WA

OR

CA

NV

ID

MT

WY

UT

CO

NM

AZ

TX

OK

KS

NE

SD

ND

MN

IA

MO

AR

LA

WI

IL

Additional

Shipments

East of the

Mississippi

Rail Distribution

LTM Q3 2011 Tons Sold by State

100,000+

10,000 to 100,000

Up to 10,000

Corporate

Headquarters

Fertilizer Plant

LTM Q3 2011 Total Tons Sold ~ 731,350

Located in the corn belt (on Union

Pacific

mainline)

45% of corn planted in 2010 was

within $35/UAN ton freight rate

of our plant

$25/ton transportation

advantage to corn belt vs. U.S.

Gulf

Coast

No intermediate transfer,

storage, barge freight or pipeline

freight charges |

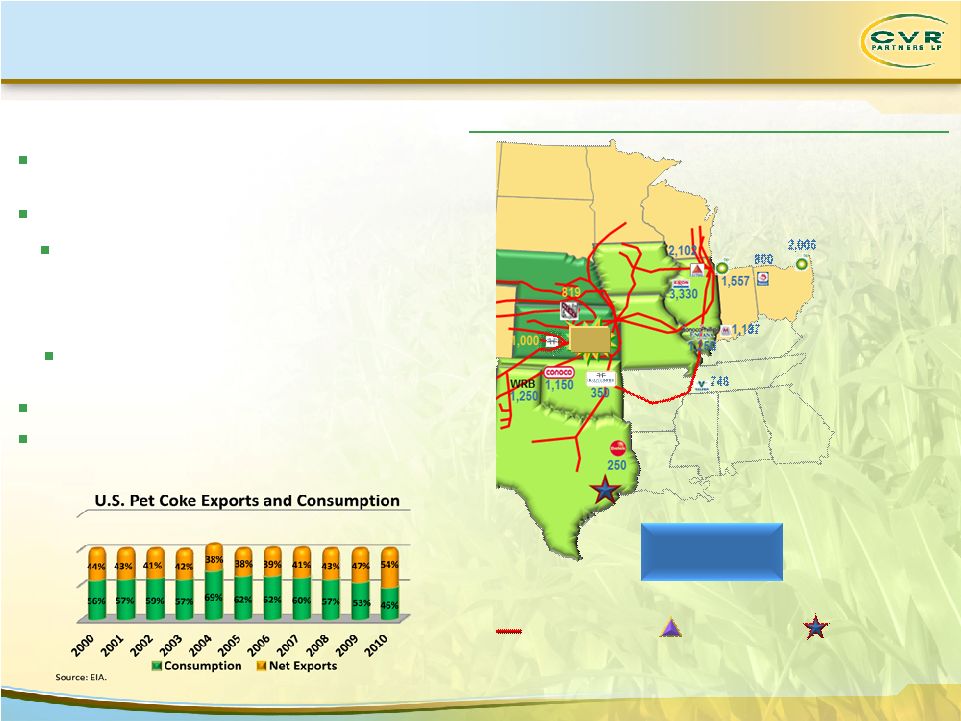

Company

Overview Stable & Economic Feedstock

Rail Distribution

Corporate

Headquarters

Fertilizer Plant

Abundant

Supply

of

Third-Party

Pet

Coke

in

the

Region

9

Texas Gulf Coast

Coke

Production = 40,000

tons/day

Source: Oil & Gas Journal

CVR Partners LP 2008 –

2010 average daily coke demand ~ 1,378

tons/day

Coke gasification technology uses petroleum coke as a feedstock

Dual train gasifier configuration ensures reliability

Ammonia synthesis loop and UAN synthesis use same processes

as natural gas based producers

Pet

coke

costs

lower

than

natural

gas

costs

per

ton

of

ammonia

produced,

and

pet

coke prices are significantly more stable

than natural gas prices

Over 70% of pet coke supplied by refinery

through long-term contract |

Market

Fundamentals Market Fundamentals |

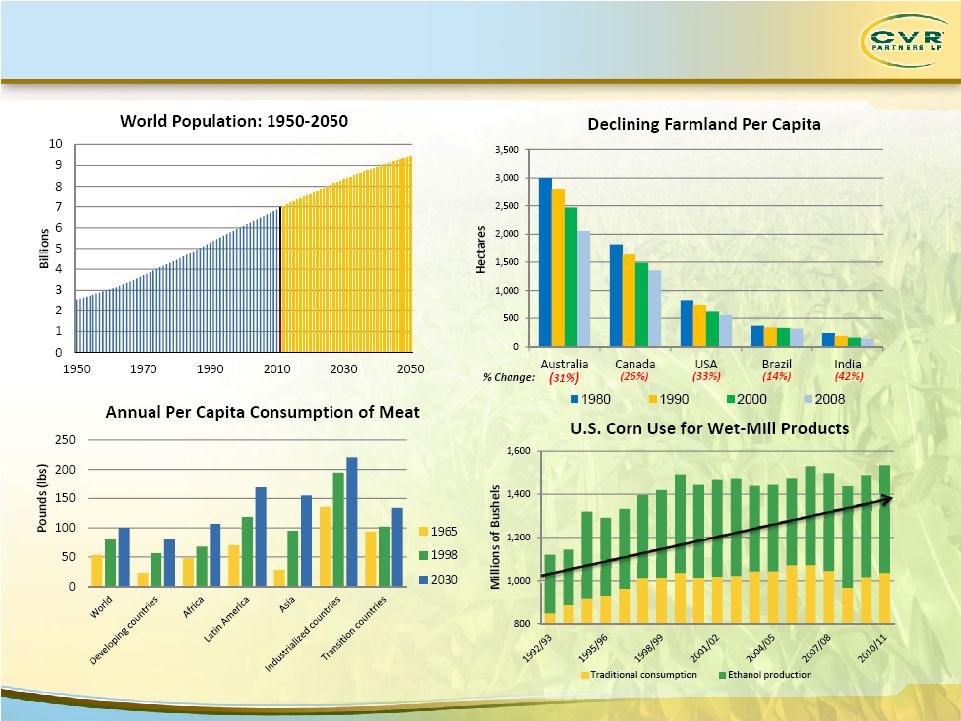

Market

Fundamentals Key Growth Factors

11

Fertilizer

consumption

is

driven

by:

—

Population growth

—

Decline in farmland per capita

—

Income growth in emerging markets, preference for proteins

—

Ethanol production |

Market

Fundamentals Key Growth Factors

12

Source:

USDA, Census Bureau, World Bank, http://data.worldbank.org/indicator/AG.LND.ARBL.HA.PC

|

Market

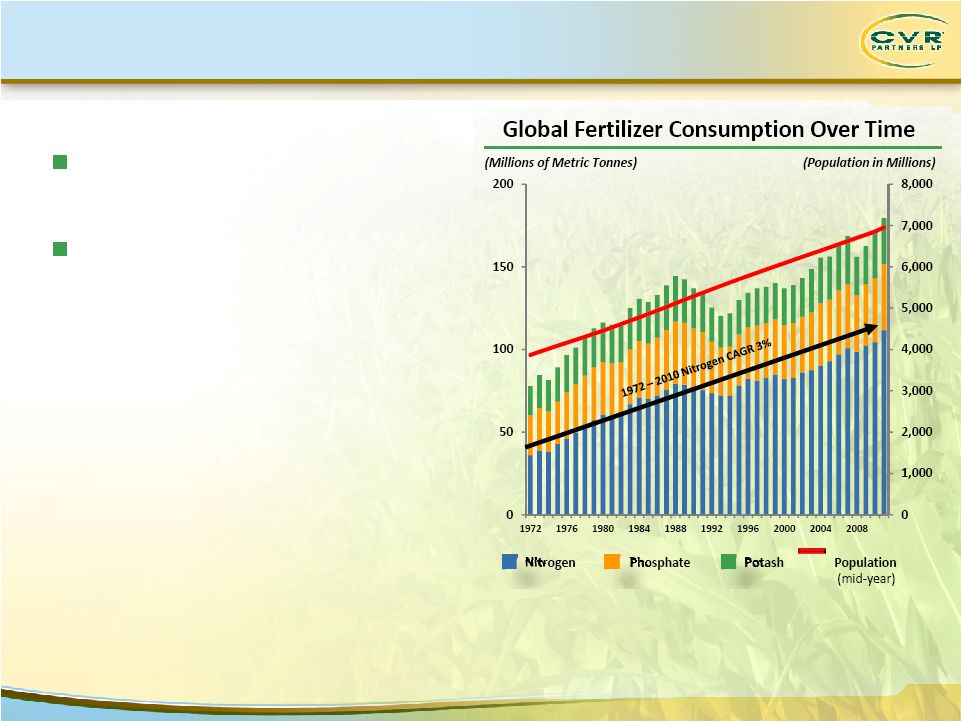

Fundamentals Consistent Fertilizer Demand Growth

13

1)

Per the International Fertilizer Industry Association

Nitrogen represents ~63% of fertilizer

consumption

(1)

Nitrogen based fertilizers have the

most stable demand because they all

must be applied annually

—

Primary determinant of crop yield

Note:

Nutrient Tonnes; Fertilizer Years.

Source:

International Fertilizer Industry Association; U.S. Bureau of the Census, International Data

Base |

Market

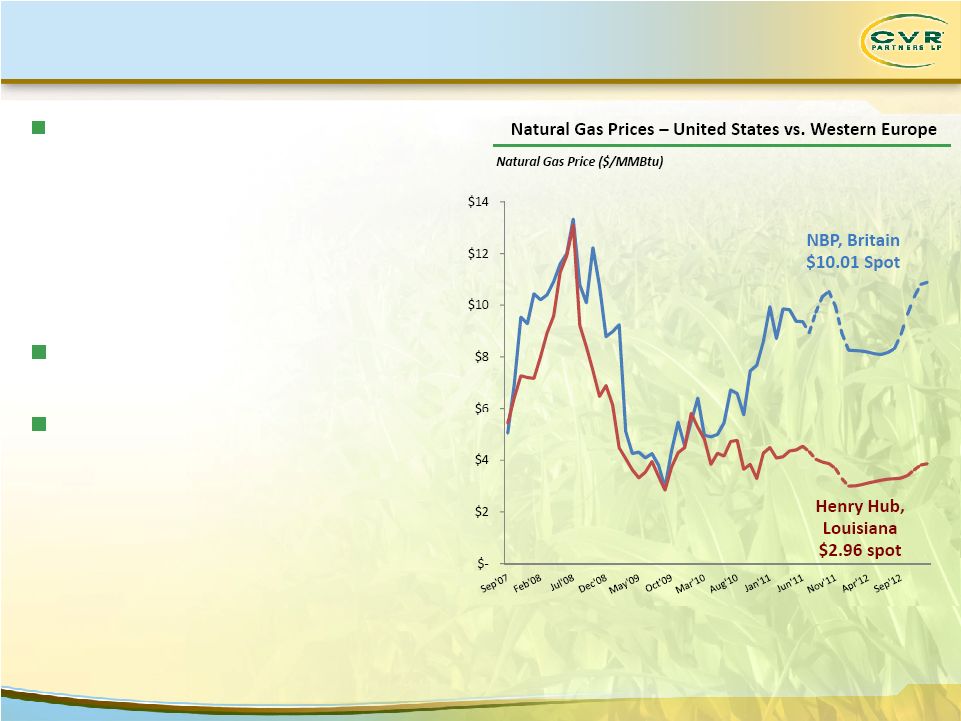

Fundamentals Global Shift in Cost of Production

14

Source:

European prices converted from GBP/Therm to $/MMBtu, based on daily exchange rate

Historical Sources: Capital IQ NBP Monthly Spot Rate, Henry Hub Monthly Spot Rate

Forecast Sources: Capital IQ NBP Forward Rate 01/06/12, Henry Hub Futures Nymex Exchange

01/06/12 Spot price as of 01/06/12

North America has shifted from being

a

high

cost region globally to a lower

cost

region

—

Shale gas has increased natural gas supply

—

Natural gas costs in North America have

declined

—

Russian gas to Ukraine increasingly priced on

market basis

U.S. imports nitrogen from Eastern Europe,

represents price floor for domestic product

Change in dynamics has served to

strengthen economic position of all North

American producers |

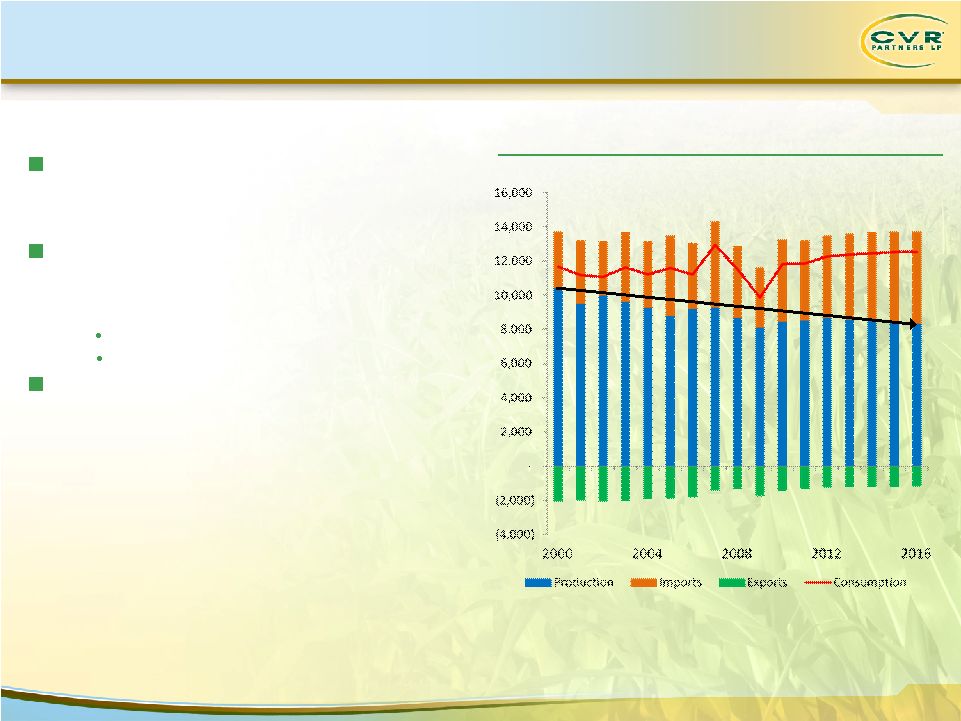

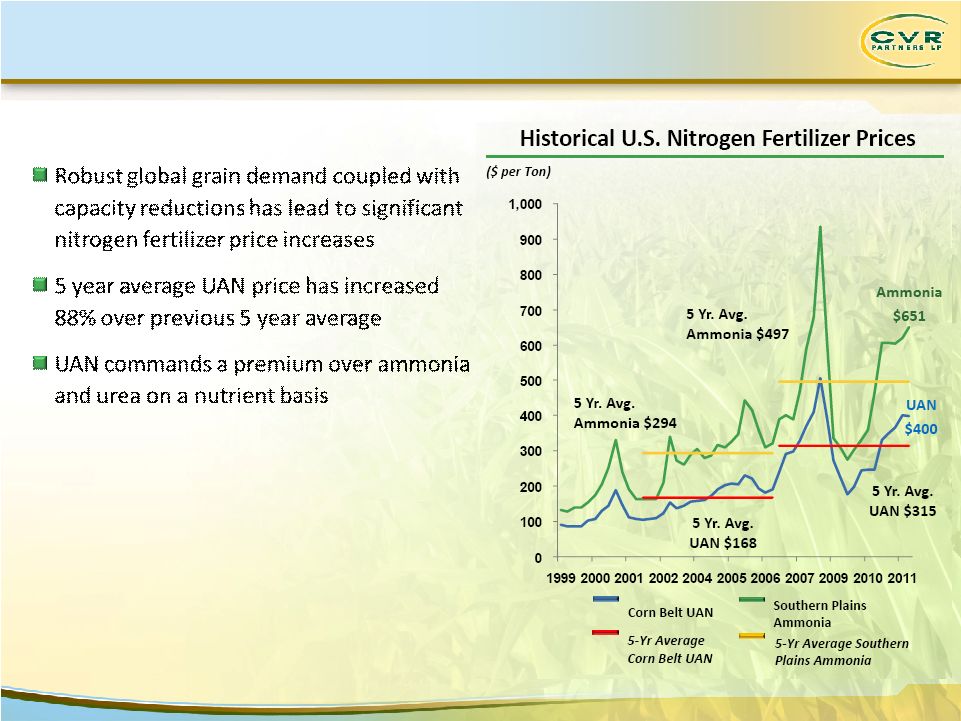

Market

Fundamentals Supply Rationalization and Consolidation

(000 Tonnes N)

Historical U.S. Nitrogen Production and Consumption

Source:

Fertecon

15

Between 1999 to 2010, U.S. nitrogen

fertilizer capacity was reduced by 34% as

producers shut down less attractive plants

Industry has also consolidated significantly

through mergers and acquisitions

—

Top 5 producers market share:

Today: 78%

2000: 56%

U.S. will continue to increase its net imports

of Nitrogen fertilizer |

16

Market Fundamentals

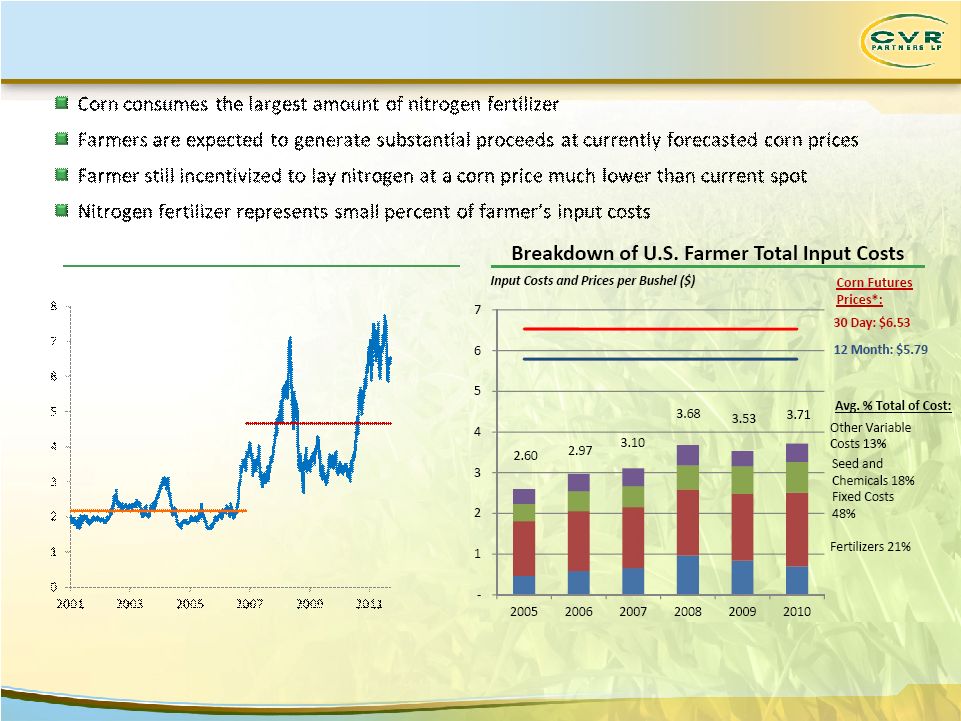

Farmer Profitability Supports Fertilizer Pricing

Corn Spot Prices

Note: Fixed Costs include labor, machinery, land, taxes, insurance, and

other. 5-Yr Prior Avg.

$2.17

5-Yr Avg.

$4.67

Current

$6.43*

*As of Jan. 06, 2012

Source:

CIQ

*As of Jan. 06, 2012

Source:

CIQ,

USDA |

Source:

Green Markets Data, Fertecon

17

Market Fundamental

Strong Pricing Environment |

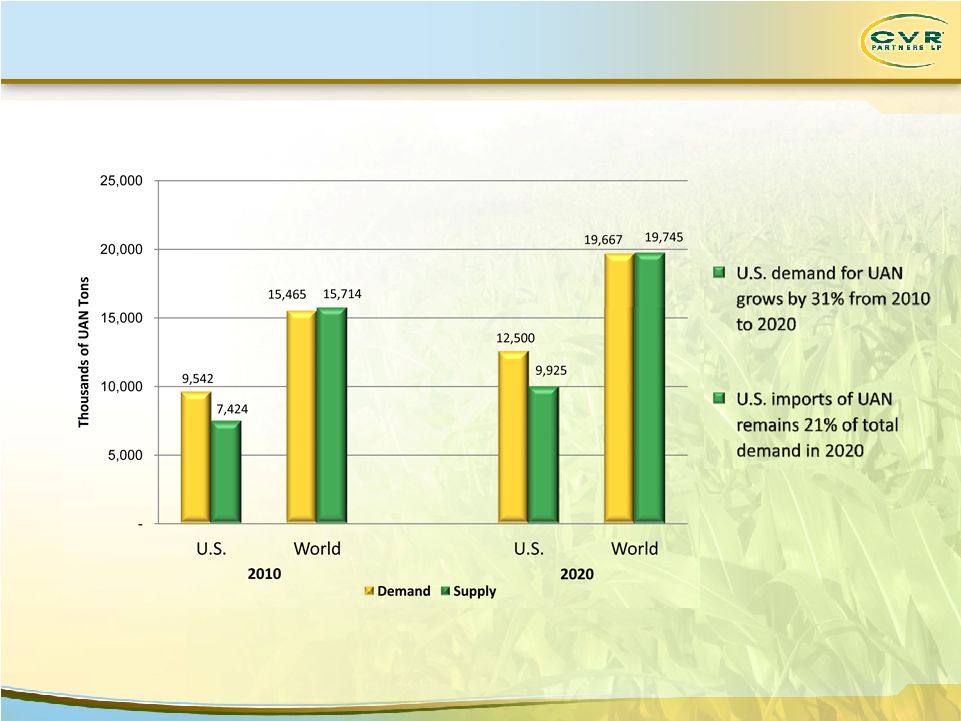

Market

Fundamentals UAN Demand Growth

Source:

Integer Focus Report 2011: Global Outlook for UAN

18

Demand Growth |

Growth

Opportunities Growth Opportunities |

Growth

Opportunities 20

Current

12-24

Months

3-5

Years |

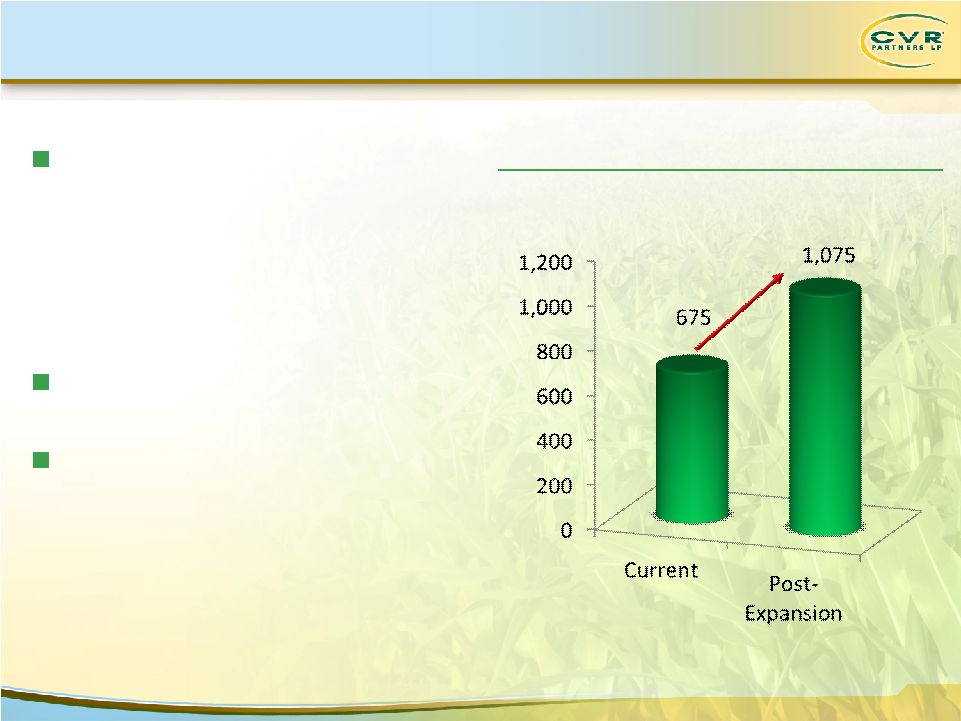

Growth

Opportunities UAN Expansion

(000’s Tons of UAN)

UAN Upgrading Capacity

1)

Excludes $5MM of capitalized interest

21

UAN expansion project

—

Increase exposure to strong UAN

market

dynamics

—

Expand UAN capacity by 400,000 tons per

year

or by ~50%

—

Provides flexibility to upgrade 100% of

ammonia

to

UAN

—

On-line in Q1 2013

Approximately $100MM cost to

complete

(1)

At current pricing, ROI exceeds 24% |

Growth

Opportunities Diesel Emission Fluid (DEF)

22

* FERTECON

Ammonia

Outlook

–

Issue

2011

(3)

P.

81

DEF is the most widely accepted technology for reducing NOX and particulate

matter from diesel vehicle exhaust emissions

Solution

of

32.5%

urea

and

67.5%

water

injected

at

approximately

2%

of

fuel

consumption

North America forecasted DEF consumption in vehicle emission reduction*:

2011: 240,000 tones

2013: 530,000 tones

2015: 1,525,000 tones

2020: 3,462,000 tones |

Growth

Opportunities Enhanced Distribution

23

Logistic assets are key to enhancing annual

margin during the shift between

application and fill season Target 60,000 –

70,000 tons per year of sales through

off premise storage facilities

Net margin increased by $15 per ton |

Financial

Statistics Financial Statistics |

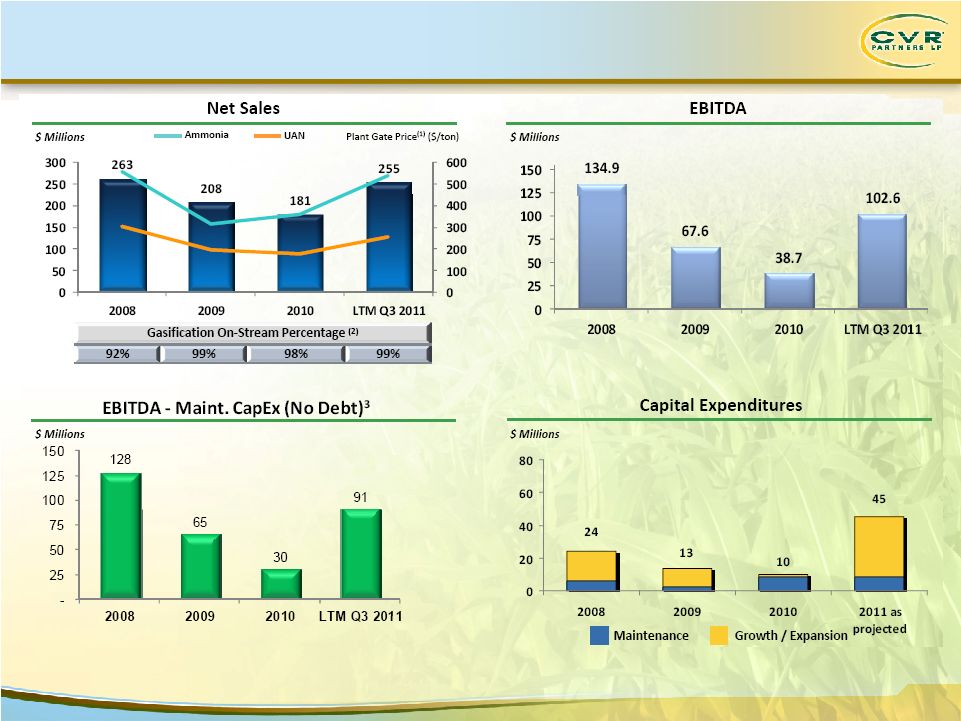

1)

Plant gate price per ton represents net sales less freight costs

and hydrogen revenue (from hydrogen sales to CVR Energy’s refinery) divided by product

sales volume in tons in the reporting period. Plant gate price per ton is shown in order

to provide a pricing measure that is comparable across the fertilizer industry. 2)

Adjusted for major scheduled turnaround, third-party outage on air separation unit and UAN

vessel rupture. 3)

Not Pro Forma for $125MM Term Loan

25

Financial Statistics |

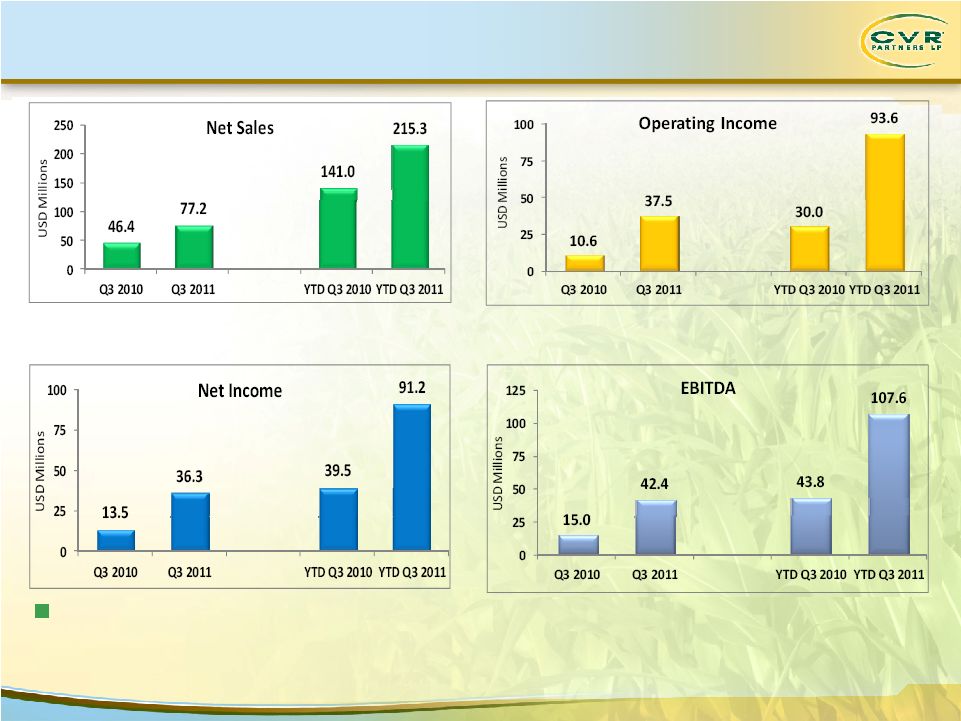

26

We expect our distribution for the 12 months ending March 31, 2012 to be at

least $1.92 per common unit yielding 7.3% as of January 12, 2012.

Financial Statistics

Strong YTD Financial Performance |

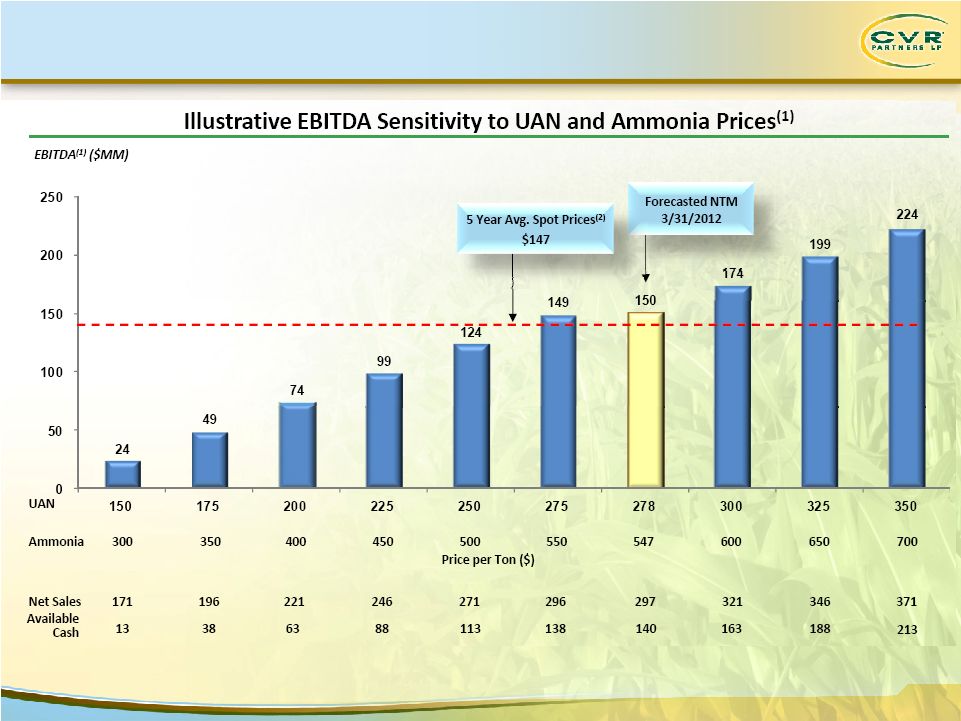

Financial

Statistics Forecasted Distributable Cash

1)

Based on projected cost structure as provided in our prospectus dated April 7, 2011.

2)

Based

on

5

year

average

Ammonia

and

UAN

spot

prices

of

$467/ton

and

$292/ton

respectively

and

forecasted

next

twelve

months

cost

structure.

27 |

28

Strong industry fundamentals

High quality, strategically located assets

Premium product focus

Attractive growth opportunities

Pay out 100% of available cash each

quarter to Common Unitholders

No IDR’s

Experienced management team |

29

Q & A |

Appendix

Appendix |

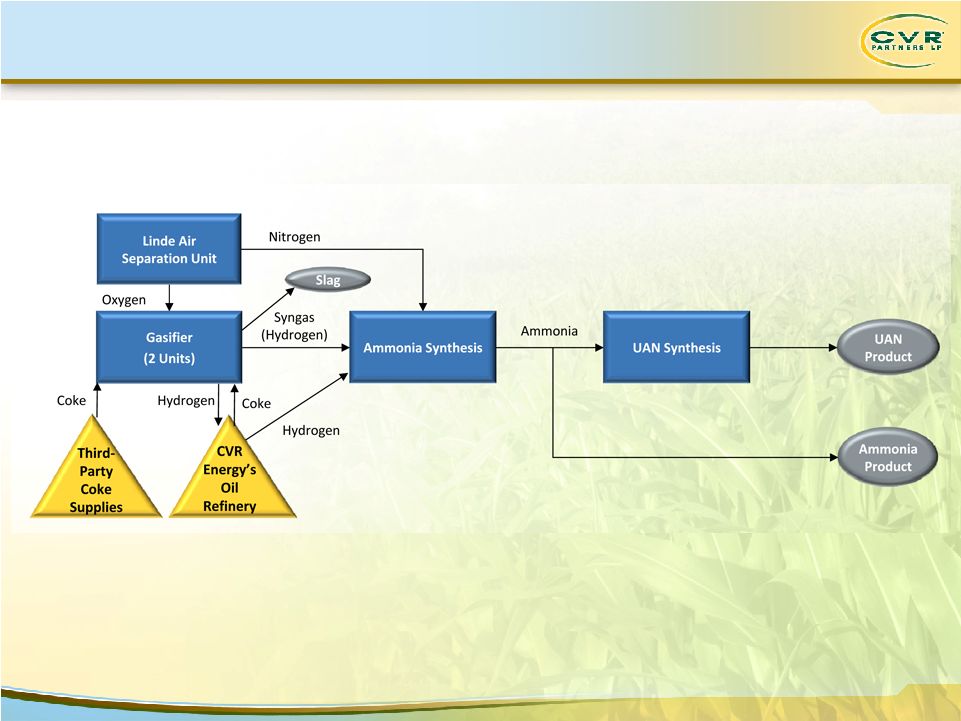

31

Manufacturing Process |

32

To

supplement

the

actual

results

in

accordance

with

U.S.

generally

accepted

accounting

principles

(GAAP),

for

the

applicable

periods,

the

Company

also

uses

certain

non-GAAP

financial

measures

as

discussed

below,

which

are

adjusted

for

GAAP-based

results.

The

use

of

non-GAAP

adjustments

are

not

in

accordance

with

or

an

alternative

for

GAAP.

The

adjustments

are

provided

to

enhance

the

overall

understanding

of

the

Company’s

financial

performance

for

the

applicable

periods

and

are

also

indicators

that

management

utilizes

for

planning

and

forecasting

future

periods.

The

non-GAAP

measures

utilized

by

the

Company

are

not

necessarily

comparable

to

similarly

titled

measures

of

other

companies.

The

Company

believes

that

the

presentation

of

non-GAAP

financial

measures

provides

useful

information

to

investors

regarding

the

Company’s

financial

condition

and

results

of

operations

because

these

measures,

when

used

in

conjunction

with

related

GAAP

financial

measures

(i)

together

provide

a

more

comprehensive

view

of

the

Company’s

core

operations

and

ability

to

generate

cash

flow,

(ii)

provide

investors

with

the

financial

analytical

framework

upon

which

management

bases

financial

and

operational

planning

decisions,

and

(iii)

presents

measurements

that

investors

and

rating

agencies

have

indicated

to

management

are

useful

to

them

in

assessing

the

Company

and

its

results

of

operations.

Non-GAAP Financial Measures |

33

EBITDA:

EBITDA

represents

net

income

before

the

effect

of

interest

expense,

interest

income,

income

tax

expense

(benefit)

and

depreciation

and

amortization.

EBITDA

is

not

a

calculation

based

upon

GAAP;

however,

the

amounts

included

in

EBITDA

are

derived

from

amounts

included

in

the

consolidated

statement

of

operations

of

the

Company.

Non-GAAP Financial Measures |

34

Below is a reconciliation of Net Income to EBITDA

(In USD Millions)

2008

2009

2010

LTM Q3 2011

Net Income

$118.9

$57.9

$33.3

$85.0

Interest expense

-

-

-

2.7

Interest (income)

(2.0)

(9.0)

(13.1)

(3.6)

Depreciation and amortization

18.0

18.7

18.5

18.5

Income tax expense

-

-

-

-

EBITDA

$ 134.9

$ 67.6

$38.7

$102.6

Non-GAAP Financial Measures |

35

Below is a reconciliation of Net Income to EBITDA

Three Months Ended

Nine Months Ended

September 30,

September 30,

2011

2010

2011

2010

(in millions)

(unaudited)

Net Income

$ 36.3

$ 13.5

$ 91.2

$ 39.5

Adjustments:

Depreciation and amortization

4.7

4.5

13.9

13.9

Interest (income) expense

1.4

(3.0)

2.5

(9.6)

Tax provision

-

-

-

EBITDA

$ 42.4

$ 15.0

$ 107.6

$ 43.8

Non-GAAP Financial Measures |