Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BRINKS CO | form_8k.htm |

The Brink’s Company

Investor Overview

Investor Overview

NYSE:BCO

December 2011

Exhibit 99.1

Forward-Looking Statements

This presentation, including questions and answers, contains forward-looking

information within the meaning of the Private Securities Litigation Reform Act

of 1995. Actual results could differ materially from projected results.

Additional information regarding factors that could affect financial

performance is in our press release dated October 27, 2011, and in our filings

with the Securities and Exchange Commission, including our most recent forms

10-K and 10-Q. Information included in this presentation is representative as

of today only and the company assumes no obligation to update any forward-

looking statements.

information within the meaning of the Private Securities Litigation Reform Act

of 1995. Actual results could differ materially from projected results.

Additional information regarding factors that could affect financial

performance is in our press release dated October 27, 2011, and in our filings

with the Securities and Exchange Commission, including our most recent forms

10-K and 10-Q. Information included in this presentation is representative as

of today only and the company assumes no obligation to update any forward-

looking statements.

2

Today’s Presentation

¢ Business Overview

¢ Growth Opportunities

¢ Creating Value for Investors

3

4

¢ Premier Brand

¢ Safety, security, service, trust

¢ Global Footprint

¢ Unique operational advantage

¢ Supports high-value Global Services business

¢ Market Fundamentals

¢ Cash growing worldwide

¢ Increased outsourcing

¢ Dangerous world

¢ Economic recovery, interest rates

¢ Growth Opportunities

¢ Maximize profits in developed markets

¢ Expand in emerging markets

¢ Invest in solutions and adjacent markets

Investment Highlights

4

5

¢ World’s Largest Secure Logistics Company

¢ Premier global brand

¢ Customers in more than 100 countries

¢ ~70,000 employees; 1,000 branches and 13,000

vehicles

vehicles

¢ 2010 Revenue - $3.1 billion

¢ Acquisitions add $450 million in 2011

¢ Global Cash-In-Transit (CIT) network supports

growth in High-Value Services

growth in High-Value Services

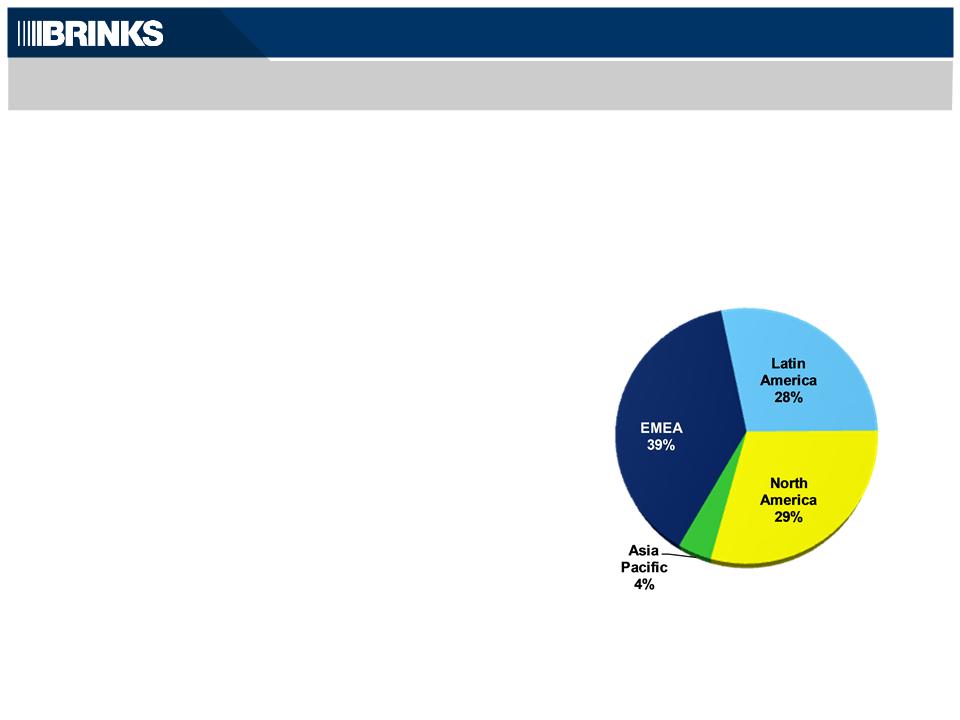

Company Snapshot

2010 Revenue

($3.1 billion)

5

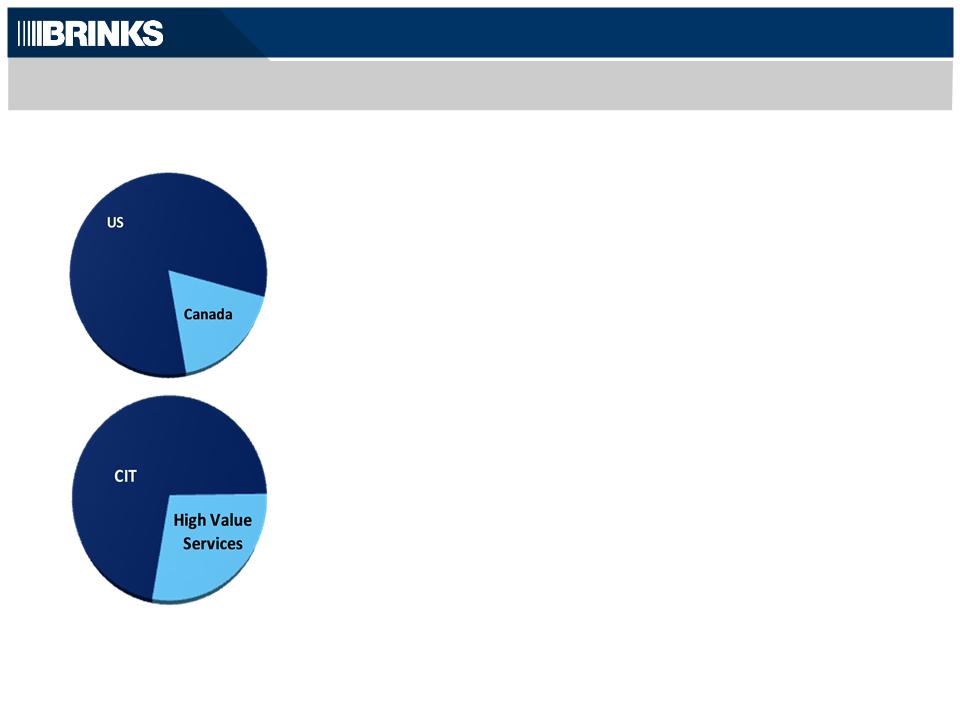

Diverse Business Lines: CIT Drives High-Value Services

¢ Global Infrastructure

High-Value Services

¢ Global Services

– Secure long-distance

transport of valuables

transport of valuables

¢ Cash Logistics

– Money processing

– Vaulting

– CompuSafe® Service

¢ Adjacencies

– Payment Services

– Commercial Security

6

¢ Guarding in select countries

– Airports, embassies

High-Value Services…High-Margin Solutions

CIT Footprint Supports High-Value Services

¢ Global Services

¢ Secure transport of valuables over long distances

¢ Diamonds, jewelry, banknotes, precious metals

¢ 7000 Customers, 5000 Cities, 1500 daily shipments

¢ Cash Logistics

¢ Money Processing

¢ Vaulting

¢ CompuSafe

¢ Adjacent Services

¢ Extending our brand into new markets

¢ Commercial Security, Payment Processing

7

8

¢ Maximize profits in developed markets

¢ EMEA, North America

¢ Invest in growth opportunities

¢ Emerging markets:

BRIC, LATAM, Asia-Pacific

BRIC, LATAM, Asia-Pacific

¢ High-Value Services:

Global Services, Cash Logistics

Global Services, Cash Logistics

¢ Adjacencies:

Commercial Security, Payment Processing

Commercial Security, Payment Processing

Global Secure Logistics

Market

Market

Source: Internal Company Estimates based on most recently available data

Global Leader…Global Growth Strategy

8

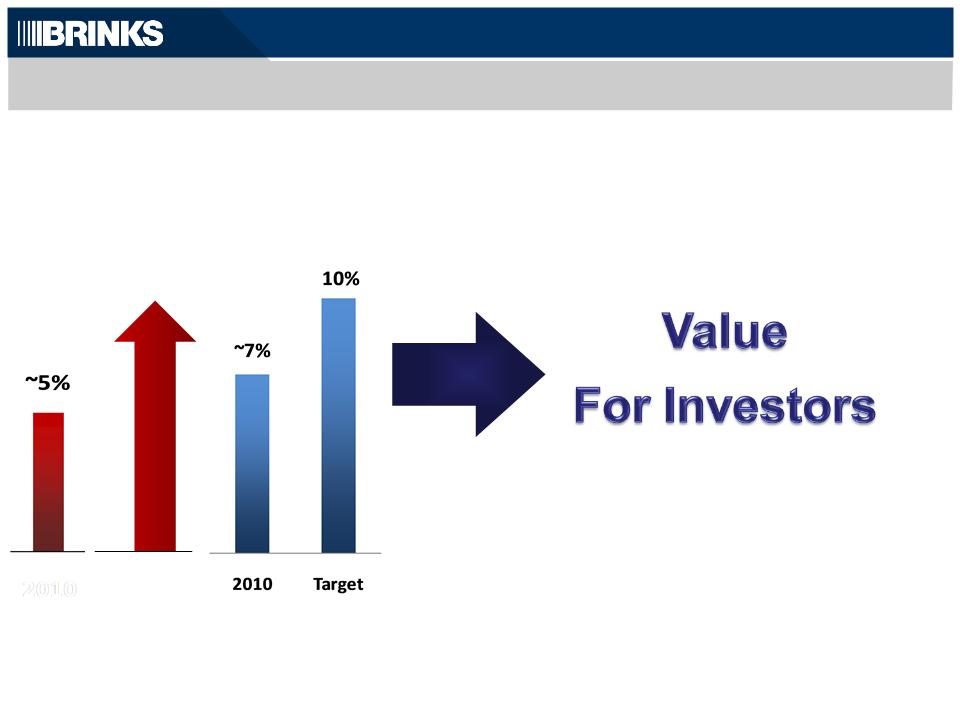

Leading Share in Fragmented Market

Long-Term Goal: Deliver Shareholder Value

Organic

Revenue

Revenue

8 - 10%

Growth

Segment

Margin

Target

9

Note: Organic revenue growth and segment margin are calculated on Non-GAAP revenue and segment profit.

See Appendix for reconciliation to GAAP.

2010

2010 Revenue: $1.2B

Region Overview:

¢ 2010: 3% organic growth…low single-digit margin

¢ Diverse competitive, regulatory and threat environments

¢ Customers want outsourced solutions

Strategy:

¢ Europe: Maximize CIT profits; increase efficiency; fix

underperformers

underperformers

¢ Invest in High-Value Services and Developing Markets

EMEA: Improve Operating Performance

10

2010 Revenue: $918M

Region Overview:

¢ Market leader

¢ 2010: Organic revenue flat…4.8% margin

¢ Price and volume pressure

Strategy:

¢ Maximize CIT profits ─ reduce costs, improve processes

¢ Remain disciplined on price, service and security

¢ Shift mix to High-Value Services

North America: Maximize CIT…Grow High-Value Services

11

Region Overview:

¢ Growing economies

¢ High-risk threat environment…customers value security

¢ Growing need to protect product supply chains

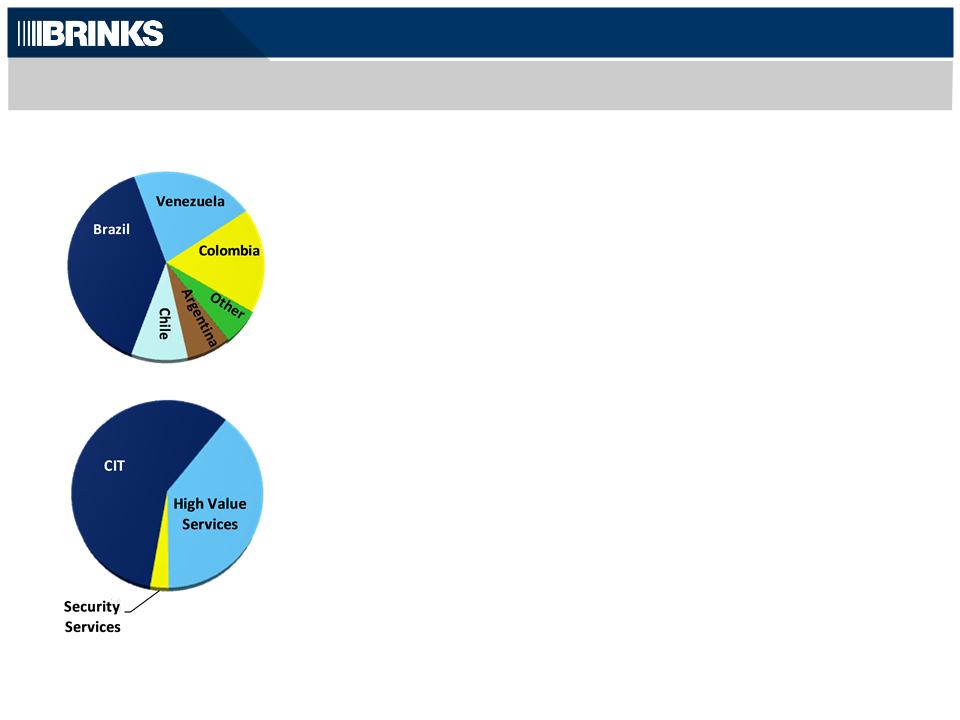

¢ 2010: 19% organic growth, double-digit profit margin

Strategy:

¢ Strengthen and expand footprint

¢ Leverage footprint to grow High-Value Services

¢ Mexico: Increase CIT margins, add High-Value Services, labor

agreement extended

agreement extended

2010 Revenue: $877M

Latin America: Continued Strong Growth

12

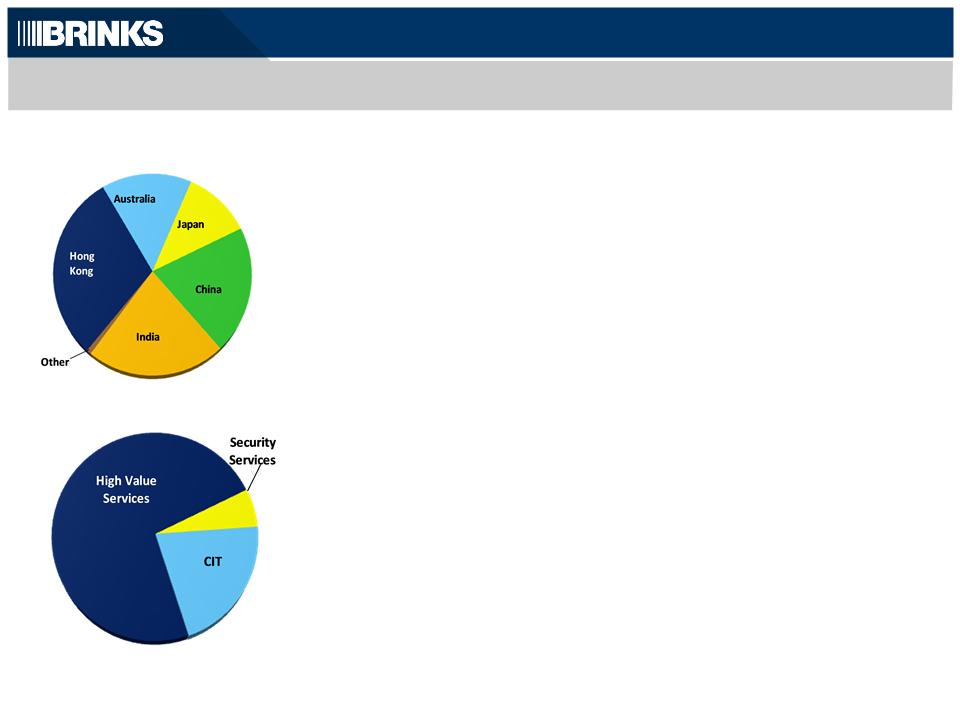

2010 Revenue: $127M

Region Overview:

¢ High-growth, service-driven economies

¢ Varying degrees of banking sophistication, gov’t restrictions

¢ Strong in Hong Kong; growing in China, India, Japan

¢ 2010: 23% organic growth, profits more than doubled

Strategy:

¢ Leverage Global Services network

¢ Accelerate China and India growth

¢ Expand commercial security capabilities

Asia Pacific: Invest and Grow

13

Financial Strength and Flexibility

n Solid Revenue Growth

n 8% CAGR 2006-2010, primarily organic

n Late 2010 acquisitions added $450 million

n Cash Flow Supports Continued Growth

n ~40% of Capex focused on Emerging

Markets and High-Value Services (’07 - ’10)

n Strong Balance Sheet

n Investment grade credit rating

n $230 million net debt; $342 million available

credit (9/30/11)

credit (9/30/11)

n Manageable cash outflow for legacy

liabilities (see appendix)

liabilities (see appendix)

14

Note: CAGR calculated on Non-GAAP revenues. Net debt is a Non-GAAP

measure. See appendix for reconciliation to GAAP.

measure. See appendix for reconciliation to GAAP.

Achieve Targets…Create Shareholder Value

2011 Outlook:

n Mid-to-high single-digit organic revenue growth

n 6.0% to 6.3% segment margin

n Includes $450 million of acquisition revenue at breakeven margin

2012 Outlook:

n Mid-to-high single-digit organic revenue growth

n 6.5% to 7.0% segment margin

Long-Term Targets:

n High single-digit organic revenue growth

n 10% segment margin

15

Note: Organic revenue growth and segment margin are calculated on Non-GAAP revenue and segment profit.

See Appendix for reconciliation to GAAP.

16

¢ Premier Brand

¢ Safety, security, service, trust

¢ Global Footprint

¢ Unique operational advantage

¢ Supports high-value Global Services business

¢ Market Fundamentals

¢ Cash growing worldwide

¢ Increased outsourcing

¢ Dangerous world

¢ Economic recovery, interest rates

¢ Growth Opportunities

¢ Maximize profits in developed markets

¢ Expand in emerging markets

¢ Invest in solutions and adjacent markets

Investment Highlights

16

Appendix

Appendix

Page

5-Year Non-GAAP Revenue Growth 2006 - 2010.......................................................19

5-Year Non-GAAP Operating Profit............................................................................20

Reconciliation to Amounts Reported under GAAP...................................................21

2010 Segment Results, GAAP and non-GAAP............................................................25

Legacy Liabilities.........................................................................................................27

18

Non-GAAP Revenue (1)

($MM)

(1) Non-GAAP financial information is reconciled to amounts reported under U.S. GAAP on pages 21, 22 & 23.

Non-GAAP Revenue Growth

19

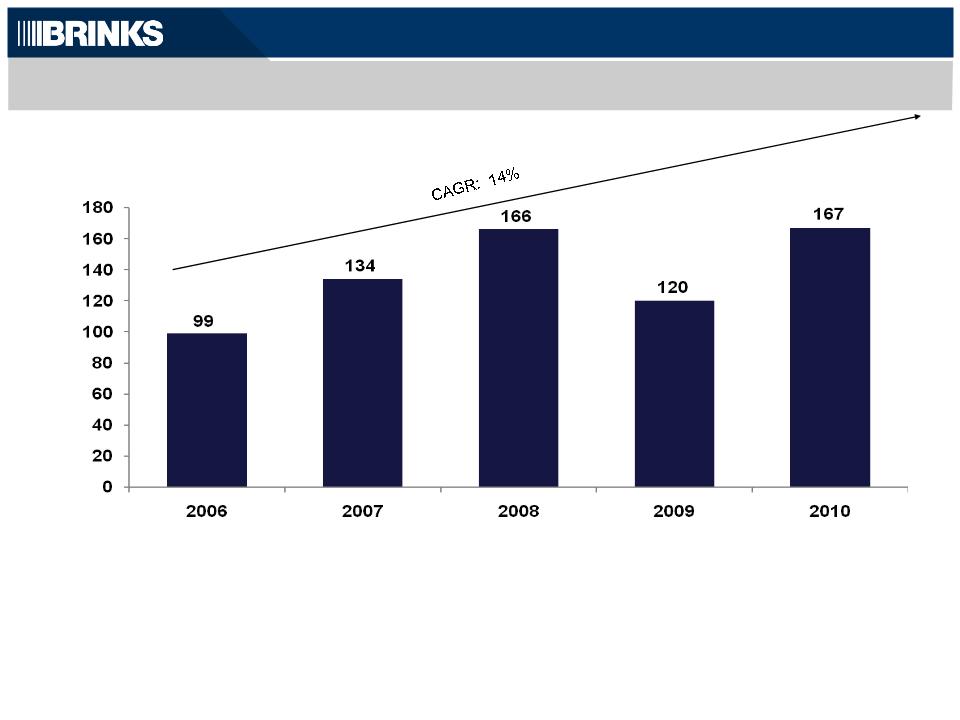

Total Non-GAAP Operating Profit (1)

($MM)

|

Segment

|

172

|

196

|

223

|

175

|

226

|

|

Non-Segment

|

(73)

|

(62)

|

(58)

|

(55)

|

(59)

|

|

Total

|

99

|

134

|

166

|

120

|

167

|

(1) Non-GAAP financial information is reconciled to amounts reported under U.S. GAAP on pages 21, 22 & 23.

Non-GAAP Profit Growth

Amounts may not add due to rounding

20

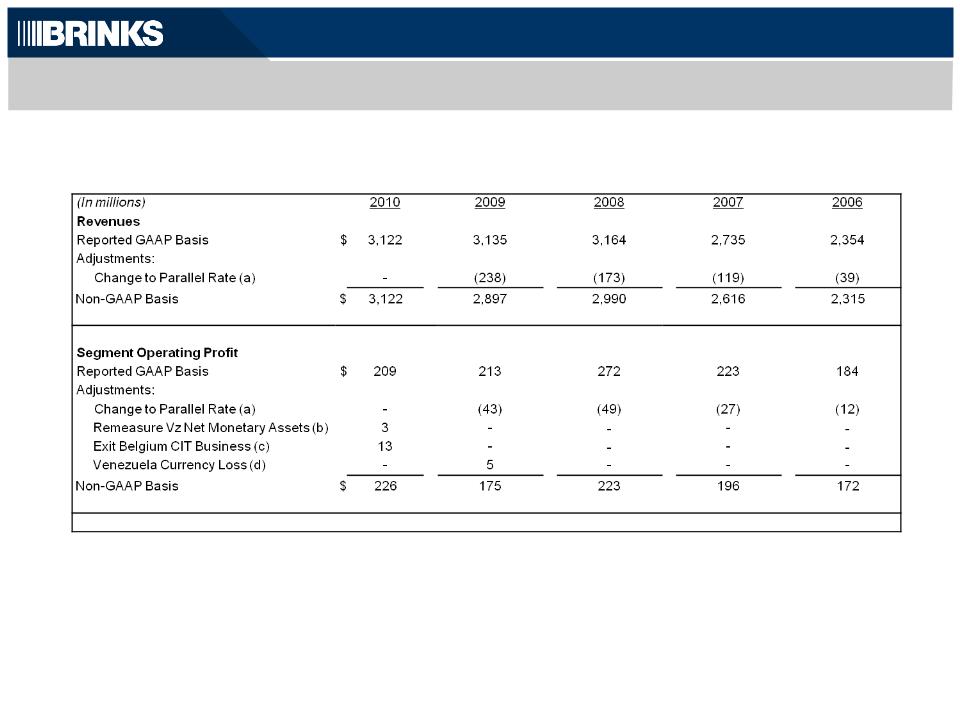

Non-GAAP Results - Reconciled to Amounts Reported under GAAP

Non-GAAP results described in this presentation are financial measures that are not required by, or presented in accordance with generally

accepted accounting principles (“GAAP”).

accepted accounting principles (“GAAP”).

Purpose of Non-GAAP Information

The purpose of the non-GAAP information is to report our financial information

• without income and expense items described below in 2008, 2009 and 2010,

• as if our results from Venezuela had been translated at the less-favorable parallel exchange rate in 2006, 2007, 2008 and 2009, and

• after adjusting tax expense for items described below.

The non-GAAP information provides information to assist comparability and estimates of future performance. Brink’s believes these

measures are helpful in assessing operations and estimating future results and enable period-to-period comparability of financial

performance. Non-GAAP results should not be considered as an alternative to revenue or income amounts determined in accordance with

GAAP and should be read in conjunction with their GAAP counterparts.

measures are helpful in assessing operations and estimating future results and enable period-to-period comparability of financial

performance. Non-GAAP results should not be considered as an alternative to revenue or income amounts determined in accordance with

GAAP and should be read in conjunction with their GAAP counterparts.

a) To reduce revenues and segment operating income to reflect the 2009, 2008, 2007 and 2006 results of Venezuelan

subsidiaries had they been translated using the parallel currency exchange rate in effect at the time. The average parallel

exchange rate used for the 2009 non-GAAP full-year earnings was 6.0 bolivar fuertes to the U.S. dollar, compared to an

average rate of 2.2 bolivar fuertes to the U.S. dollar that was used for the GAAP financial statements. The official rate of

2.15 bolivar fuertes to the U.S. dollar was used for translation of Venezuela for most of 2009 until the parallel rate was

adopted during December. The use of the weaker rate to translate 2009 non-GAAP revenues and earnings of the

Venezuelan subsidiaries decreased each measure by 63%.

subsidiaries had they been translated using the parallel currency exchange rate in effect at the time. The average parallel

exchange rate used for the 2009 non-GAAP full-year earnings was 6.0 bolivar fuertes to the U.S. dollar, compared to an

average rate of 2.2 bolivar fuertes to the U.S. dollar that was used for the GAAP financial statements. The official rate of

2.15 bolivar fuertes to the U.S. dollar was used for translation of Venezuela for most of 2009 until the parallel rate was

adopted during December. The use of the weaker rate to translate 2009 non-GAAP revenues and earnings of the

Venezuelan subsidiaries decreased each measure by 63%.

b) To reverse remeasurement gains and losses in Venezuela. For accounting purposes, Venezuela is considered a highly

inflationary economy. Under GAAP, subsidiaries that operate in Venezuela record gains and losses in earnings for the

remeasurement of bolivar fuerte-denominated net monetary assets.

inflationary economy. Under GAAP, subsidiaries that operate in Venezuela record gains and losses in earnings for the

remeasurement of bolivar fuerte-denominated net monetary assets.

c) To eliminate loss on exit of Belgium cash-in-transit (CIT) business.

d) To eliminate currency losses incurred in Venezuela related to increases in cash held in U.S. dollars by Venezuelan

subsidiaries. These losses would not have been incurred had the operations been translated at the parallel rate.

subsidiaries. These losses would not have been incurred had the operations been translated at the parallel rate.

e) To eliminate gains/losses recognized related to acquisitions of controlling interests in subsidiaries that were previously

accounted for as equity method or cost method investments.

accounted for as equity method or cost method investments.

f) To eliminate royalty income from Brink’s Home Security.

g) To eliminate certain non-segment gains on sales of assets.

21

See page 21 for explanation of footnotes

Reconciliation

Amounts may not add due to rounding

Non-GAAP Results - Reconciled to Amounts Reported under GAAP (Cont.)

22

|

(In millions)

|

|

2010

|

|

2009

|

|

2008

|

|

2007

|

|

2006

|

|

Non-Segment

|

|

|

|

|

|

|

|

|

|

|

|

Reported GAAP Basis

|

$

|

(63)

|

|

(46)

|

|

(43)

|

|

(62)

|

|

(73)

|

|

Adjustments:

|

|

|

|

|

|

|

|

|

|

|

|

Venezuela Currency Loss (d)

|

|

-

|

|

23

|

|

-

|

|

-

|

|

-

|

|

Acquisition (Gain) Loss (e)

|

|

9

|

|

(15)

|

|

-

|

|

-

|

|

-

|

|

Royalty from BHS (f)

|

|

(5)

|

|

(7)

|

|

(1)

|

|

-

|

|

-

|

|

Non-segment asset sales (g)

|

|

-

|

|

(10)

|

|

(13)

|

|

-

|

|

-

|

|

Non-GAAP Basis

|

$

|

(59)

|

|

(55)

|

|

(58)

|

|

(62)

|

|

(73)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Operating Profit

|

|

|

|

|

|

|

|

|

|

|

|

Reported GAAP Basis

|

$

|

146

|

|

167

|

|

229

|

|

161

|

|

111

|

|

Adjustments:

|

|

|

|

|

|

|

|

|

|

|

|

Change to Parallel Rate (a)

|

|

-

|

|

(43)

|

|

(49)

|

|

(27)

|

|

(12)

|

|

Remeasure Vz Net Monetary Assets (b)

|

|

3

|

|

-

|

|

-

|

|

-

|

|

-

|

|

Exit Belgium CIT Business (c)

|

|

13

|

|

-

|

|

-

|

|

-

|

|

-

|

|

Venezuela Currency Loss (d)

|

|

-

|

|

27

|

|

-

|

|

-

|

|

-

|

|

Acquisition (Gain) Loss (e)

|

|

9

|

|

(15)

|

|

-

|

|

-

|

|

-

|

|

Royalty from BHS (f)

|

|

(5)

|

|

(7)

|

|

(1)

|

|

-

|

|

-

|

|

Non-segment asset sales (g)

|

|

-

|

|

(10)

|

|

(13)

|

|

-

|

|

-

|

|

Non-GAAP Basis

|

$

|

167

|

|

120

|

|

166

|

|

134

|

|

99

|

See page 21 for explanation of footnotes

Reconciliation

Amounts may not add due to rounding

Non-GAAP Results - Reconciled to Amounts Reported under GAAP (Cont.)

23

Net Debt

|

|

|

September 30,

|

|

December 31,

|

|

|

|

2011

|

|

2010

|

|

Debt:

|

|

|

|

|

|

Short-term debt

|

$

|

18.6

|

|

36.5

|

|

Long-term debt

|

|

382.8

|

|

352.7

|

|

Total Debt

|

|

401.4

|

|

389.2

|

|

|

|

|

|

|

|

Cash and cash equivalents

|

|

200.5

|

|

183.0

|

|

Less amounts held by certain cash logistics operations (a)

|

|

(28.7)

|

|

(38.5)

|

|

Amount available for general corporate purposes

|

|

171.8

|

|

144.5

|

|

|

|

|

|

|

|

Net Debt

|

$

|

229.6

|

|

244.7

|

(a) Title to cash received and processed in certain of our secure cash logistics operations transfers to us for a short period of time.

The cash is generally credited to customers’ accounts the following day and we do not consider it as available for general

corporate purposes in the management of our liquidity and capital resources and in our computation of Net Debt.

The cash is generally credited to customers’ accounts the following day and we do not consider it as available for general

corporate purposes in the management of our liquidity and capital resources and in our computation of Net Debt.

Net Debt is a supplemental financial measure that is not required by, or presented in accordance with GAAP. We use Net Debt as a

measure of our financial leverage. We believe that investors also may find Net Debt to be helpful in evaluating our financial leverage.

measure of our financial leverage. We believe that investors also may find Net Debt to be helpful in evaluating our financial leverage.

Net Debt should not be considered as an alternative to Debt determined in accordance with GAAP and should be reviewed in

conjunction with our consolidated balance sheets. Set forth above is a reconciliation of Net Debt, a non-GAAP financial measure, to

Debt, which is the most directly comparable financial measure calculated and reported in accordance with GAAP, as of September 30,

2011 and December 31, 2010. At September 30, 2011, Net Debt is $245 million excluding cash and debt in Venezuelan operations.

NET DEBT RECONCILED TO AMOUNTS REPORTED UNDER GAAP

(in millions)

24

2010 Segment Results, GAAP

|

|

|

|

|

|

||||||||||

|

|

|

|

|

Organic

|

|

Acquisitions/

|

|

Currency

|

|

|

|

|

|

|

|

|

|

2009

|

|

Change

|

|

Dispositions (b)

|

|

(c)

|

|

2010

|

|

Total

|

|

Organic

|

|

Revenues:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMEA

|

$

|

1,258

|

|

33

|

|

(45)

|

|

(46)

|

|

1,200

|

|

(5%)

|

|

3%

|

|

Latin America

|

|

905

|

|

171

|

|

52

|

|

(250)

|

|

877

|

|

(3%)

|

|

19%

|

|

Asia Pacific

|

|

79

|

|

18

|

|

25

|

|

5

|

|

127

|

|

61%

|

|

23%

|

|

International

|

|

2,241

|

|

222

|

|

32

|

|

(290)

|

|

2,204

|

|

(2%)

|

|

10%

|

|

North America

|

|

894

|

|

7

|

|

-

|

|

17

|

|

918

|

|

3%

|

|

1%

|

|

Total

|

$

|

3,135

|

|

228

|

|

32

|

|

(273)

|

|

3,122

|

|

-

|

|

7%

|

|

Operating profit:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

International

|

$

|

157

|

|

80

|

|

(4)

|

|

(68)

|

|

165

|

|

5%

|

|

51%

|

|

North America

|

|

57

|

|

(13)

|

|

-

|

|

1

|

|

44

|

|

(22%)

|

|

(24%)

|

|

Segment operating profit

|

|

213

|

|

67

|

|

(4)

|

|

(67)

|

|

209

|

|

(2%)

|

|

31%

|

|

Non-segment (a)

|

|

(47)

|

|

(15)

|

|

(24)

|

|

23

|

|

(63)

|

|

34%

|

|

32%

|

|

Total

|

$

|

167

|

|

52

|

|

(28)

|

|

(44)

|

|

146

|

|

(12%)

|

|

31%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Segment operating margin:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

International

|

|

7.0%

|

|

|

|

|

|

|

|

7.5%

|

|

|

|

|

|

North America

|

|

6.3%

|

|

|

|

|

|

|

|

4.8%

|

|

|

|

|

|

Segment operating margin

|

|

6.8%

|

|

|

|

|

|

|

|

6.7%

|

|

|

|

|

Full Year 2010 vs. 2009

(In millions)

Segment Results - GAAP

See footnotes on page 26.

25

Amounts may not add due to rounding

2010 Segment Results, non-GAAP

|

|

|

|

|

|

||||||||||

|

(In millions)

|

|

|

|

Organic

|

|

Acquisitions/

|

|

Currency

|

|

|

|

|

|

|

|

|

|

2009

|

|

Change

|

|

Dispositions (b)

|

|

(c)

|

|

2010

|

|

Total

|

|

Organic

|

|

Revenues:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMEA

|

$

|

1,258

|

|

33

|

|

(45)

|

|

(46)

|

|

1,200

|

|

(5%)

|

|

3%

|

|

Latin America

|

|

667

|

|

100

|

|

52

|

|

59

|

|

877

|

|

32%

|

|

15%

|

|

Asia Pacific

|

|

79

|

|

18

|

|

25

|

|

5

|

|

127

|

|

61%

|

|

23%

|

|

International

|

|

2,003

|

|

150

|

|

32

|

|

19

|

|

2,204

|

|

10%

|

|

8%

|

|

North America

|

|

894

|

|

7

|

|

-

|

|

17

|

|

918

|

|

3%

|

|

1%

|

|

Total

|

$

|

2,897

|

|

157

|

|

32

|

|

36

|

|

3,122

|

|

8%

|

|

5%

|

|

Operating profit:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

International

|

$

|

118

|

|

49

|

|

9

|

|

6

|

|

181

|

|

53%

|

|

41%

|

|

North America

|

|

57

|

|

(13)

|

|

-

|

|

1

|

|

44

|

|

(22%)

|

|

(24%)

|

|

Segment operating profit

|

|

175

|

|

35

|

|

9

|

|

7

|

|

226

|

|

29%

|

|

20%

|

|

Non-segment (a)

|

|

(55)

|

|

(4)

|

|

-

|

|

-

|

|

(59)

|

|

6%

|

|

6%

|

|

Total

|

$

|

120

|

|

32

|

|

9

|

|

7

|

|

167

|

|

39%

|

|

26%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Segment operating margin:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

International

|

|

5.9%

|

|

|

|

|

|

|

|

8.2%

|

|

|

|

|

|

North America

|

|

6.3%

|

|

|

|

|

|

|

|

4.8%

|

|

|

|

|

|

Segment operating margin

|

|

6.0%

|

|

|

|

|

|

|

|

7.2%

|

|

|

|

|

(a) Includes income and expense not allocated to segments.

(b) Includes operating results and gains/losses on acquisitions, sales and exit of businesses.

(c) Revenue and Segment Operating Profit: The “Currency” amount in the table is the summation of the monthly currency changes, plus (minus) the U.S. dollar amount of

remeasurement currency gains (losses) of bolivar fuerte-denominated net monetary assets recorded under highly inflationary accounting rules in 2010 related to the Venezuelan

operations. The monthly currency change is equal to the Revenue or Operating Profit for the month in local currency, on a country-by-country basis, multiplied by the difference

in rates used to translate the current period amounts to U.S. dollars versus the translation rates used in the year-ago month. The functional currency in Venezuela was the

bolivar fuerte in 2009, and became the U.S. dollar in 2010 under highly inflationary accounting rules. Remeasurement gains and losses under these rules in 2010 are recorded

in U.S. dollars but these gains and losses are not recorded in local currency. Local currency Revenue and Operating Profit in 2010 used in the calculation of monthly currency

change for Venezuela have been derived from the U.S. dollar results of the Venezuelan operations under U.S. GAAP (excluding remeasurement gains and losses) using current

period currency exchange rates. Non-Segment Operating Profit: The “Currency” amount in the table is the 2009 losses incurred in Venezuela related to increases in cash

held in U.S. dollars by Venezuela subsidiaries.

remeasurement currency gains (losses) of bolivar fuerte-denominated net monetary assets recorded under highly inflationary accounting rules in 2010 related to the Venezuelan

operations. The monthly currency change is equal to the Revenue or Operating Profit for the month in local currency, on a country-by-country basis, multiplied by the difference

in rates used to translate the current period amounts to U.S. dollars versus the translation rates used in the year-ago month. The functional currency in Venezuela was the

bolivar fuerte in 2009, and became the U.S. dollar in 2010 under highly inflationary accounting rules. Remeasurement gains and losses under these rules in 2010 are recorded

in U.S. dollars but these gains and losses are not recorded in local currency. Local currency Revenue and Operating Profit in 2010 used in the calculation of monthly currency

change for Venezuela have been derived from the U.S. dollar results of the Venezuelan operations under U.S. GAAP (excluding remeasurement gains and losses) using current

period currency exchange rates. Non-Segment Operating Profit: The “Currency” amount in the table is the 2009 losses incurred in Venezuela related to increases in cash

held in U.S. dollars by Venezuela subsidiaries.

Amounts may not add due to rounding

26

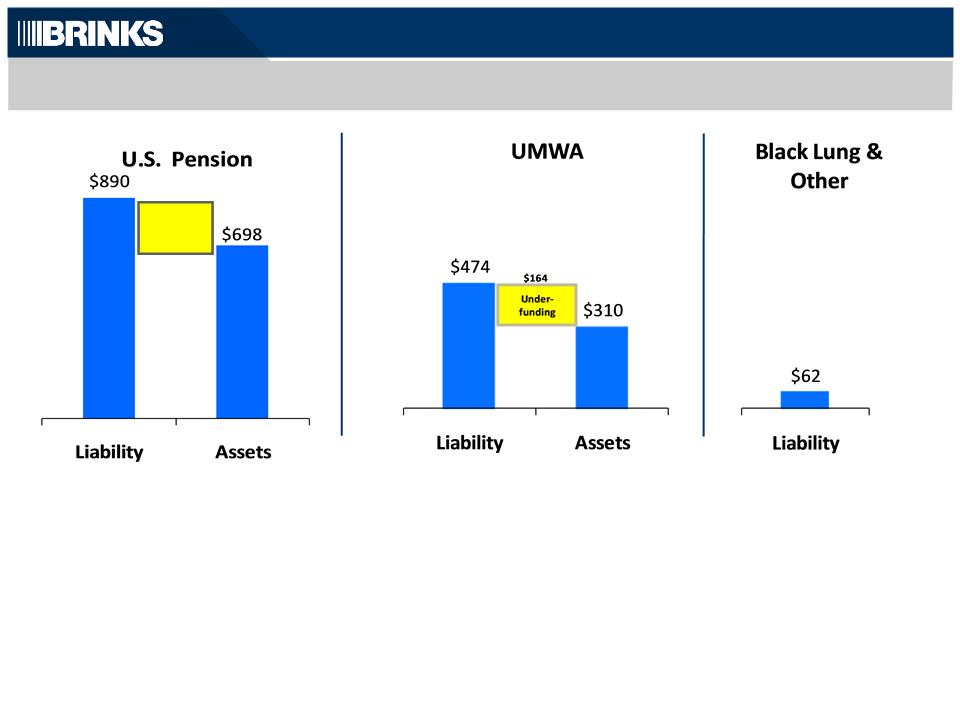

Legacy Liabilities

|

Estimated Contributions to U.S. Plans

|

|

|||||||||

|

|

2011

|

2012

|

2013

|

2014

|

2015

|

|||||

|

US Pension

|

$ 0

|

|

36 |

|

34 |

|

30 |

|

27 |

|

|

UMWA

|

0

|

|

0 |

|

0 |

|

0 |

|

0 |

|

|

Black Lung/Other

|

8

|

|

7 |

|

7 |

|

7 |

|

6 |

|

|

Total

|

$ 8

|

|

43 |

|

41 |

|

37 |

|

33

|

|

($ millions)

Under-

funding

funding

$192

Note: Amounts based on actuarial assumptions at December 31, 2010.

27