Attached files

| file | filename |

|---|---|

| 8-K - A 2011 3Q MEMBER LETTER 8K - Federal Home Loan Bank of Chicago | a20113qmemberletter8k.htm |

EXHIBIT 99.1

October 27, 2011

To Our Members:

This letter will update you on the Federal Home Loan Bank of Chicago's financial results for the third quarter of 2011. While the results discussed here are preliminary and unaudited, we are pleased to report that we continue to build on our financial strength, earning net income of $141 million for the quarter. Based on these results, we announced our dividend payment of 0.10% per share (annualized) earlier this week. We expect to file our third quarter 2011 report (Form 10-Q) with the Securities and Exchange Commission next month. You will be able to access it through our website, www.fhlbc.com, or the SEC's reporting website, www.sec.gov.

As you know, our capital stock conversion plan has been approved by our regulator, the Federal Housing Finance Agency, and will become effective as of January 1, 2012. This milestone is critical to the strength of the cooperative by providing a foundation of stable capital. Subject to the Finance Agency's approval of the stock repurchase plan we intend to submit in December, and the satisfaction of certain conditions articulated in the plan, we will begin repurchasing excess stock of current and former members as expeditiously as possible following the effective date. This is an essential step in normalizing our relationships with our members and, over time, returning full liquidity to your investment in the Bank.

As we move from remediating the conditions of the past to building an advances-focused Bank, we have combined our member relationship group with our financial markets group to form the Members and Markets Group headed by Executive Vice President Sanjay Bhasin. We did this to leverage our substantial capital markets expertise to provide members with solutions that complement their risk management, liquidity management, and earnings strategies and support their community investment objectives. All of the Bank staff is focused on our plans to build the value of membership in the Bank, enhance our products and services, and contribute to the long-term financial strength of the cooperative by:

• | Providing you with short-term liquidity and long-term funding as integral components of your business strategies; |

• | Generating consistent, profitable results while extending the benefits of our funding advantage to you; |

• | Paying an appropriate dividend; |

• | Maintaining our financial strength; |

• | Simplifying the business model and operations of the Bank; and |

• | Restoring full liquidity to your capital stock over time through a stock repurchase plan to be submitted in December to our regulator for approval. |

1

Third Quarter 2011 Financial Highlights

• | We recorded net income of $141 million for the third quarter of 2011 compared to net income of $117 million for the third quarter of 2010. Both quarters were characterized by hedging gains and significant advance prepayment fees from large members. Net interest income of $131 million was 36% lower than net interest income of $204 million in the third quarter of 2010 due to lower levels of prepayment fees and lower net interest income for a reduced level of interest-earning assets. A settlement of $14.5 million related to a dispute over some our private-label mortgage-backed securities (MBS) increased other income. Credit-related other-than-temporary-impairment (OTTI) charges on our private-label MBS portfolio were $14 million; we may experience additional credit-related OTTI charges in the future. |

• | Advances outstanding at September 30, 2011, were $14.3 billion, 17% lower than the previous quarter-end level of $17.3 billion and 24% lower than the year-end 2010 level of $18.9 billion. During the third quarter, two large members paid down advances, one in conjunction with its merger. Our healthy members continue to report high levels of deposits on their balance sheets and slow growth, if any, in lending activity. Our challenged members continue to work to strengthen their capital positions by reducing borrowings. We have identified opportunities for increasing advances in certain scenarios and certain industry sectors shorter-term; we believe improved economic conditions will contribute to increases in advance levels over the long term. |

• | Mortgage Partnership Finance® (MPF®) loans held in portfolio at September 30, 2011, declined $3.1 billion (17%) to $15.2 billion from $18.3 billion at December 31, 2010. These reductions are a direct result of our 2008 decision not to add MPF loans to our balance sheet. |

• | Total investment securities were $40.5 billion at September 30, 2011, an increase of $1.5 billion (4%) over the $39.0 billion portfolio at December 31, 2010, principally due to increases in short-term investments which we believe have relatively low risk. However, the largest portion of the investment portfolio was acquired in prior years to create an income bridge to transition the primary business of the Bank to advances. This portfolio will decline over time as we are not currently purchasing longer-term asset classes and are positioning the balance sheet for reductions associated with anticipated repurchases and redemptions of capital stock after the conversion of our capital stock. |

• | As a result of our net income during the first three quarters of 2011, our retained earnings grew $206 million to $1.3 billion at September 30, 2011, another indication of our financial strength. |

• | Nearly 200 members have registered to access down payment and closing cost assistance for their homebuying customers through the Downpayment Plus® (DPP®) Program in 2011. We look forward to announcing the awards for our competitive Affordable Housing Program (AHP) next month. |

• | We remain in compliance with all of our regulatory capital requirements. |

2

Income Statement: Foundation for Consistent Net Interest Spread and Profitability

Net interest income for the third quarter of 2011 of $131 million includes $15 million in net prepayment fees and is in line with net interest income levels over recent quarters. Excluding the impact of advance prepayment fees, net interest income for the first three quarters of 2011 has ranged from $116 million to $122 million. Net income for the quarter was $141 million. We believe consistent net interest spread, close attention to non-interest expenses, and lower sensitivity to market movements will be the bases for a successful business model focused on advances.

Credit-related OTTI charges of $14 million in the third quarter of 2011 compared favorably with OTTI charges of $76 million in the third quarter of 2010. However, while we carefully analyze the impact of OTTI charges quarterly, we cannot predict the level of any future charges. We also recorded an increase in other income of $14.5 million related to the settlement of a dispute over some of our private-label MBS securities.

We recognized gains of $95 million on derivatives and hedging activities for the third quarter of 2011, compared to gains of $62 million in the third quarter of 2010, largely driven by the positive effect of the decrease in interest rates associated with our hedge positions. As long as the MPF portfolio remains a relatively large component of the overall balance sheet, we anticipate fluctuations in gains or losses from derivatives and hedging activities from quarter to quarter and year to year.

We are actively managing the components of non-interest expenses that we control. However, non-interest expenses increased to $36 million compared to $28 million for the third quarter of 2010, primarily due to severance pay and increased employee benefit expenses.

Balance Sheet: Reduction in Total Assets

Total assets at September 30, 2011, were $73.3 billion, down 13% from $84.1 billion at December 31, 2010. The smaller balance sheet reflects reductions in advances and the MPF loan portfolio. Advances at September 30, 2011, were $14.3 billion, down from $18.9 billion at year-end 2010. Several factors continue to contribute to lower levels of advances, including loan demand in members' markets, relatively high deposits on members' balance sheets, and members' efforts to strengthen capital ratios. In addition, we have experienced several significant advances paydowns over the past year resulting from member mergers and resolutions. However, we are working to identify opportunities involving asset liability management and ongoing daily and short-term funding that will raise the profile of the Bank as a core provider of members' funding.

Total MPF loans held in portfolio were $15.2 billion at the end of the third quarter of 2011, a reduction of $3.1 billion (17%) from December 31, 2010. We increased our MPF loan loss allowance from $33 million at December 31, 2010, to $41 million, reflecting an increase in our nonperforming and impaired MPF Loan amounts. Despite the increase in the MPF loan loss allowance, MPF loans continue to have lower delinquency rates than the national average for conventional conforming mortgage loans.

The MPF Xtra® product has proven to be popular with our members, as well as the members of the Federal Home Loan Banks of Boston, Des Moines, and Pittsburgh. Since the inception of the program in late 2008, 307 participating financial institutions System-wide have funded $8.3 billion in loans through September 30, 2011. MPF Xtra loan volume was $768 million program-wide and

3

$494 million for the Bank during the third quarter of 2011. We are in the process of piloting a servicing-released option under the MPF Xtra product.

Retained earnings totaled $1.3 billion at the end of the third quarter of 2011, including $28 million of restricted retained earnings. As we announced in March 2011, the 12 FHLBanks have worked together to develop a “System Capital Initiative” to set aside funds previously used to satisfy the Resolution Funding Corporation (REFCORP) obligation, which was satisfied in the second quarter. Each FHLBank is required to allocate approximately 20% of its net income quarterly to a separate, restricted retained earnings account. Unlike the REFCORP assessments, however, the amounts allocated to this restricted account will not reduce our net income. As a result, net income available for contribution to the Affordable Housing Program will increase. The purpose of the restricted earnings account is to provide additional capital protection to absorb potential or unanticipated losses.

Summary

We believe that the recent approval of the capital plan sets the stage for an important shift in the priorities of the Bank. For several years, we have presented our plans for remediating the Bank. Now that the Bank is financially strong, and our capital plan is about to be implemented, we can focus our energy on enhancing the value of your FHLBC membership. While we demonstrated during the credit crisis that we are a critical source of contingent liquidity, it is essential to the future health of the cooperative that we also support your short- and long-term funding by providing solutions that help you manage your liquidity and interest rate risk in conjunction with your strategic goals.

Please refer to the attached Condensed Statements of Income and Statements of Condition and the discussion of the market value of the Bank's equity, level of retained earnings, and the spread of return on average regulatory capital to three-month Libor that follows.

As always, we welcome your comments and questions and look forward to working with you during the rest of 2011.

Best regards,

/s/ Matt Feldman

Matt Feldman

President and CEO

This letter contains forward-looking statements which are based upon our current expectations and speak only as of the date hereof. These statements may use forward-looking terms, such as “anticipates,” “believes,” “expects,” “could,” “plans,” “estimates,” “may,” “should,” “will,” or their negatives or other variations on these terms. We caution that, by their nature, forward-looking statements involve risk or uncertainty, that actual results could differ materially from those expressed or implied in these forward-looking statements, and that actual events could affect the extent to which a particular objective, projection, estimate, or prediction is realized. These forward-looking statements involve risks and uncertainties including, but not limited to, instability in the credit and debt markets; economic conditions (including effects on, among other things, mortgage-backed securities), changes in mortgage interest rates and prepayment speeds on mortgage assets; our ability to successfully transition to a new business model; our ability to pay future dividends; our ability to successfully convert our capital stock; whether we will receive regulatory approval to repurchase excess capital stock; the amounts and timing of such repurchases; and the risk factors set forth in our periodic filings with the Securities and Exchange Commission, which are available on our website at www.fhlbc.com. We assume no obligation to update any forward-looking statements made in this letter. The financial results discussed in this letter are preliminary and unaudited. “Mortgage Partnership Finance,” “MPF,” “MPF Xtra,” “Downpayment Plus,” and “DPP” are registered trademarks of the Federal Home Loan Bank of Chicago.

4

Condensed Statements of Income | ||||||||||||||||||||||

(Dollars in millions) | ||||||||||||||||||||||

(Preliminary and Unaudited) | ||||||||||||||||||||||

For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||||||||||

2011 | 2010 | Change | 2011 | 2010 | Change | |||||||||||||||||

Interest income | $ | 559 | $ | 700 | (20 | )% | $ | 1,714 | $ | 2,082 | (18 | )% | ||||||||||

Interest expense | 425 | 487 | (13 | )% | 1,325 | 1,534 | (14 | )% | ||||||||||||||

Provision for credit losses | 3 | 9 | (67 | )% | 12 | 20 | (40 | )% | ||||||||||||||

Net interest income | 131 | 204 | (36 | )% | 377 | 528 | (29 | )% | ||||||||||||||

Other-than-temporary impairment (credit loss) | (14 | ) | (76 | ) | 82 | % | (57 | ) | (147 | ) | 61 | % | ||||||||||

Other non-interest gain (loss) | 75 | 59 | 27 | % | 28 | 20 | 40 | % | ||||||||||||||

Non-interest expense | 36 | 28 | 29 | % | 101 | 82 | 23 | % | ||||||||||||||

Assessments | 15 | 42 | (64 | )% | 39 | 85 | (54 | )% | ||||||||||||||

Net income | $ | 141 | $ | 117 | 21 | % | $ | 208 | $ | 234 | (11 | )% | ||||||||||

Net yield on interest-earning assets | 0.73 | % | 0.97 | % | (0.24 | )% | 0.65 | % | 0.83 | % | (0.18 | )% | ||||||||||

Condensed Statements of Condition | |||||||||||

(Dollars in millions) | |||||||||||

(Preliminary and Unaudited) | |||||||||||

As of: | September 30, 2011 | December 31, 2010 | Change | ||||||||

Cash and due from banks | $ | 275 | $ | 282 | (2 | )% | |||||

Federal Funds sold and securities purchased under agreement to resell | 2,610 | 7,243 | (64 | )% | |||||||

Investment securities | 40,532 | 38,996 | 4 | % | |||||||

Advances | 14,294 | 18,901 | (24 | )% | |||||||

MPF Loans held in portfolio, net | 15,205 | 18,294 | (17 | )% | |||||||

Other | 335 | 400 | (16 | )% | |||||||

Total assets | $ | 73,251 | $ | 84,116 | (13 | )% | |||||

Consolidated obligation discount notes | $ | 19,830 | $ | 18,421 | 8 | % | |||||

Consolidated obligation bonds | 45,880 | 57,849 | (21 | )% | |||||||

Subordinated notes | 1,000 | 1,000 | — | % | |||||||

Other | 3,219 | 3,897 | (17 | )% | |||||||

Total liabilities | 69,929 | 81,167 | (14 | )% | |||||||

Capital stock | 2,390 | 2,333 | 2 | % | |||||||

Retained earnings | 1,305 | 1,099 | 19 | % | |||||||

Accumulated other comprehensive income (loss) | (373 | ) | (483 | ) | 23 | % | |||||

Total capital | 3,322 | 2,949 | 13 | % | |||||||

Total liabilities and capital | $ | 73,251 | $ | 84,116 | (13 | )% | |||||

Regulatory capital stock plus Designated Amount of subordinated notes (minimum required $3,600) | $ | 3,720 | $ | 3,863 | (4 | )% | |||||

Regulatory capital to assets ratio (minimum required 4.76%) | 6.86 | % | 5.90 | % | 0.96 | % | |||||

5

Remediation Dashboard

In order to provide our members with greater clarity as we work to transition the Bank, we regularly monitor our ratio of Market Value to Book Value of Equity, the level of our Retained Earnings, and our Spread of the Return of Average Regulatory Capital to Three-Month Libor. Together, these metrics provide a view of our progress in restructuring our business model and our balance sheet to fortify the financial strength of the Bank.

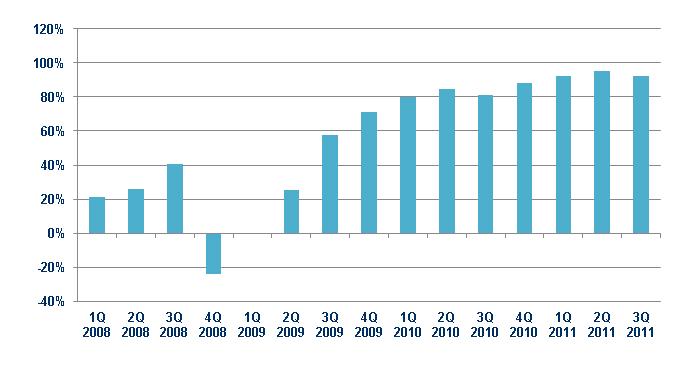

Ratio of Market Value to Book Value of Equity

The market value of the Bank continues to be positively impacted by our previous restructuring of the balance sheet and the increase in value of investment securities. The ratio of market value to book value improved from 81% at September 30, 2010, to 92% at September 30, 2011.

6

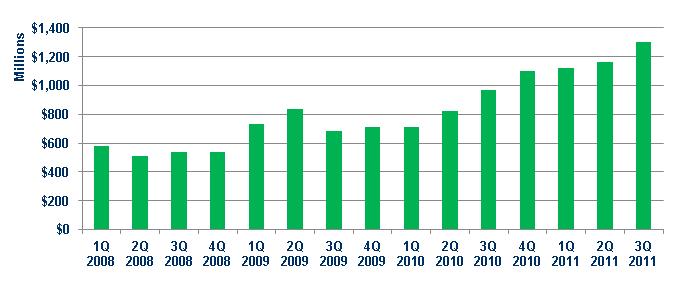

Retained Earnings

The growth of retained earnings is a key element in the Bank's plan to improve its financial strength and stability. Total retained earnings at September 30, 2011, were $1.3 billion compared to $967 million at September 30, 2010.

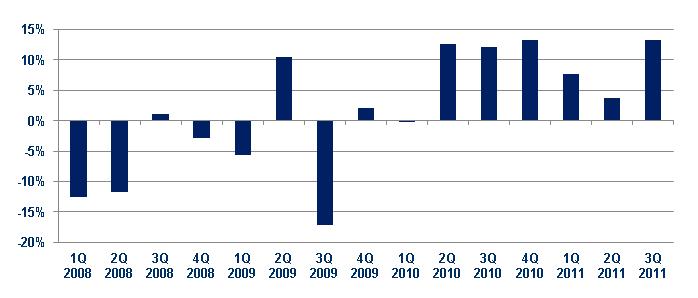

Spread of Return on Average Regulatory Capital to Three-Month Libor

Over time, we have seen substantial variability in the spread of our return on average regulatory capital (which excludes subordinated notes) relative to three-month Libor. This measure is driven in large part by fluctuating gains and losses on derivatives and hedging activities and continuing OTTI charges. Our goal is to reduce the variability in this measure over time.

7