Attached files

| file | filename |

|---|---|

| 8-K - 8-K_09/19/2011 - NORTHWESTERN CORP | ek_091911.htm |

September 19-21, 2011

Investor Update

2

forward-looking statement…

During the course of this presentation, there will be forward-looking

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

The information in this presentation is based upon our current

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason.

Although our expectations and beliefs are based on reasonable

assumptions, actual results may differ materially. The factors that may

affect our results are listed in certain of our press releases and

disclosed in the Company’s public filings with the SEC.

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason.

Although our expectations and beliefs are based on reasonable

assumptions, actual results may differ materially. The factors that may

affect our results are listed in certain of our press releases and

disclosed in the Company’s public filings with the SEC.

3

who we are…

Above data as of 12/31/10

(1) Book capitalization calculated as total debt, excluding capital leases, plus shareholders’ equity.

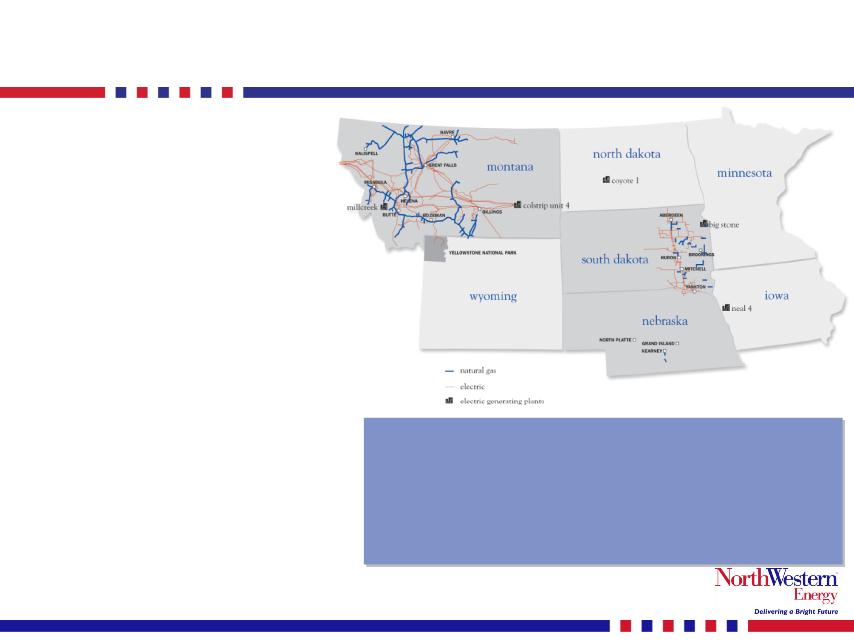

¾ 665,000 customers

» 399,000 electric

» 266,000 natural gas

¾ Approximately 123,000 square

miles of service territory in

Montana, South Dakota, and Nebraska

miles of service territory in

Montana, South Dakota, and Nebraska

» 27,500 miles of electric T&D lines

» 9,200 miles of natural gas T&D pipelines

» 20 Bcf natural gas storage

» 8.4 Bcf natural gas proven reserves

¾ Total owned generation

» MT - 372 MW - regulated

» SD - 312 MW - regulated

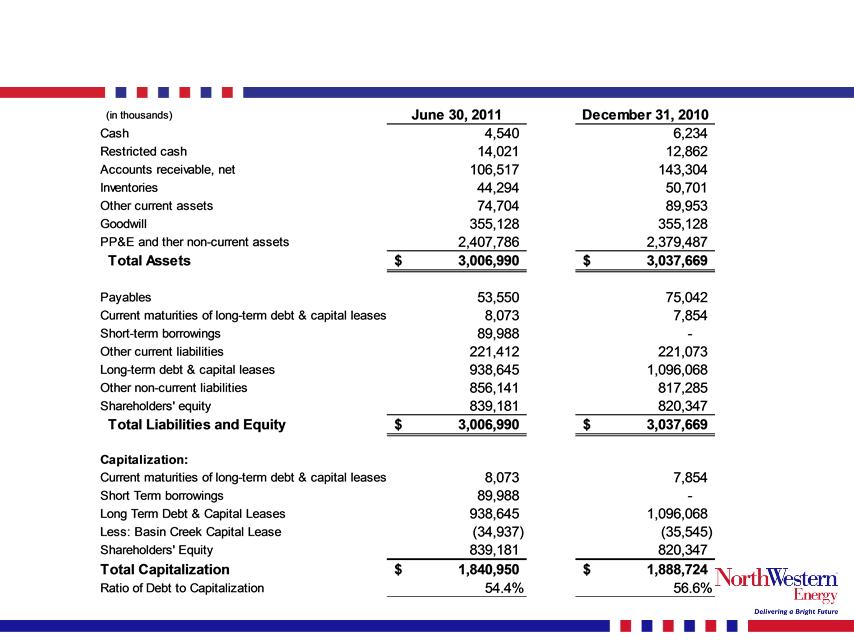

¾ Total Assets: $3,038 MM

¾ Total Capitalization: $1,889 MM(1)

¾ Total Rate Base: $1,750 MM (est.)

¾ Total Employees: 1,363

• Located in states with relatively stable economies with

opportunity for system investment and grid expansion.

opportunity for system investment and grid expansion.

• Footprint of service territory covers some of the best

wind regimes in the United States

wind regimes in the United States

•Unique opportunity to provide transmission services in

to two different power markets (West and Midwest)

to two different power markets (West and Midwest)

4

NorthWestern’s attributes…

¾ Solid operations

» Cost competitive

» Above-average reliability

» Award-winning customer service

¾ Single A secured credit ratings with a strong balance sheet and liquidity

» January 21, 2011 Moody’s upgraded secured and unsecured ratings to A2 and Baa1, respectively

» April 15, 2010 Fitch upgraded secured and unsecured ratings to A- and BBB+ respectively

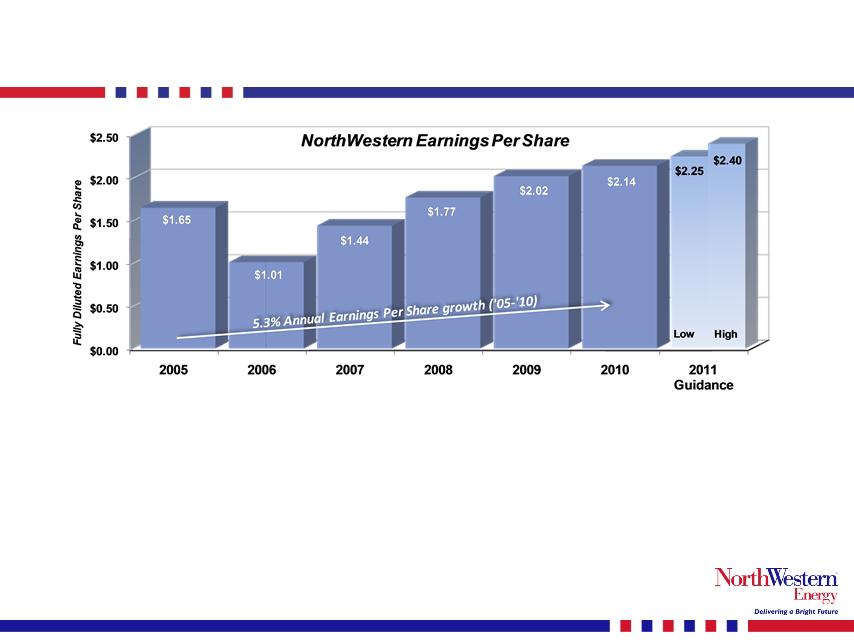

¾ Positive earnings and ROE trend

» Delivery services rate increase for Montana electric

» Mill Creek Generation Station achieved commercial operation on January 1, 2011

¾ Strong cash flows

» NOLs and repair tax deduction provide an effective tax shield likely beyond 2015

» 89% pension funded status at end of 2010

¾ Competitive shareholder return with a dividend that has increased every year since ‘05

» Added to S&P 600 SmallCap Index on April 9, 2010

¾ Constructive regulatory environment

¾ Forbes.com listed as one of “100 Most Trustworthy Companies”

¾ Realistic investment opportunities

strong credit ratings…

5

A security rating is not a recommendation to buy, sell or hold securities. Such rating may be subject to revision or withdrawal

at any time by the credit rating agency and each rating should be evaluated independently of any other rating.

at any time by the credit rating agency and each rating should be evaluated independently of any other rating.

6

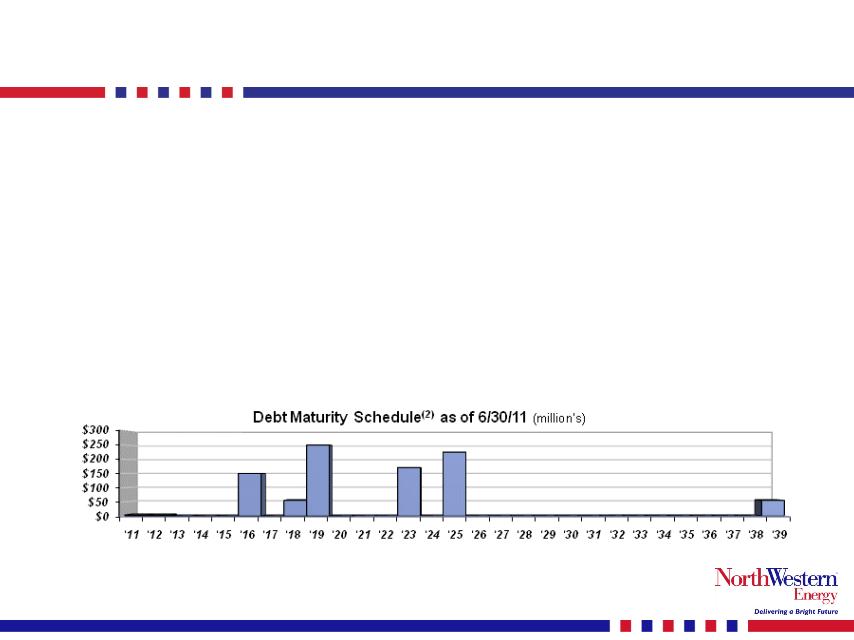

strong balance sheet and liquidity…

¾ Total liquidity of approximately $220 million as of August 26, 2011

¾ Total debt / total capitalization of 54.4%(1)

¾ In past two years refinanced nearly all outstanding debt

» Amended and restated revolving credit facility in July of 2011, extending term to

5 years (to June 2016), increased availability by $50 million (up to $300 million)

and reduced eurodollar spread by 1.5% (down to 1.25%)

5 years (to June 2016), increased availability by $50 million (up to $300 million)

and reduced eurodollar spread by 1.5% (down to 1.25%)

» Long-term debt refinancing has resulted in a reduction to average coupon of 1.2%

(from 6.8% down to 5.6%) and increased average maturity to over 10 years.

(from 6.8% down to 5.6%) and increased average maturity to over 10 years.

¾ No significant debt maturities until after 2015

(1) Total capitalization as of 6/30/11, excluding Basin Creek capital lease / PPA.

(2) Excludes outstanding 6/30/11 commercial paper balance of $90 million.

7

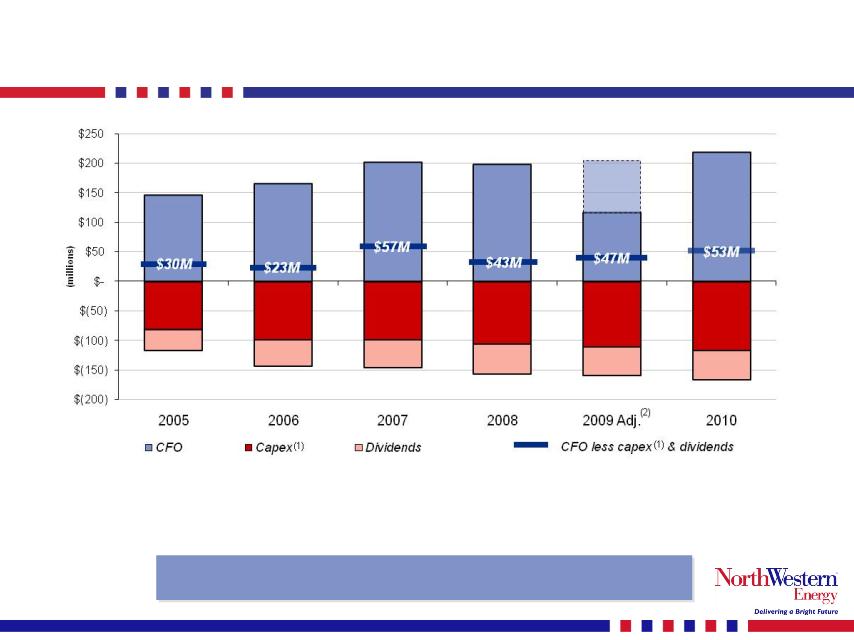

strong cash flows…

Earnings trend and NOLs provide strong cash flows to

fund future investment.

fund future investment.

(1) Utility maintenance capex only, excludes investment growth projects.

(2) 2009 Cash Flow from Operations adjusted to add back pension funding in excess of expense and Ammondson settlement

paid..

paid..

solid pension funding position…

8

Data source: SNL Financial

As a result of significant contributions to our pension

plan over the past several years and solid market returns in 2009 and

2010, we are better positioned than our peers at December 31, 2010.

plan over the past several years and solid market returns in 2009 and

2010, we are better positioned than our peers at December 31, 2010.

9

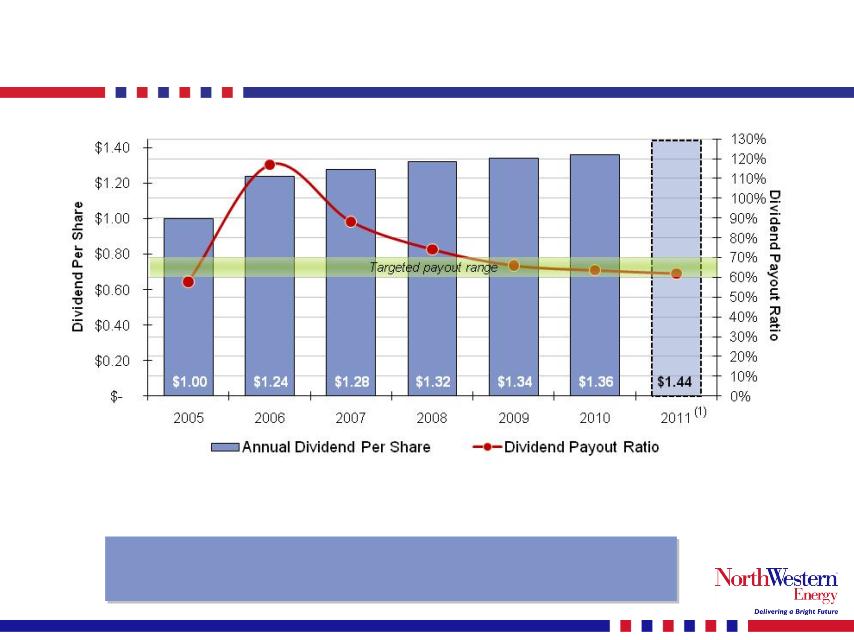

and sustainable dividend…

Goal for dividend payout ratio of 60% - 70%. Current dividend

yield about 5% with year-over-year dividend growth of approximately

6.3% (2005-2011 CAGR).

yield about 5% with year-over-year dividend growth of approximately

6.3% (2005-2011 CAGR).

(1) 2011 estimated payout range assumes midpoint of guidance range $2.25 - $2.40

10

reaffirming 2011 EPS guidance…

¾ The major assumptions include, but are not limited to, the following expectations:

» We expect strong hydro conditions west of our Colstrip Transmission System to persist, causing additional declines to

our wholesale transmission revenues for the third quarter of 2011;

our wholesale transmission revenues for the third quarter of 2011;

» We expect a reduction in general & administrative expenses for the rest of 2011 from the second quarter levels;

» Normal weather in the Company’s electric and natural gas service territories for the remainder of 2011; and

» Fully diluted average shares of 36.5 million.

11

constructive regulatory environment…

¾ Montana

» Electric and natural gas general rate case

♦ April 2011: MPSC and Company settled the overall rate increase in Montana:

● A net $6.1 million increase in annual revenue with authorized electric and natural gas

ROE’s set at 10.25%

ROE’s set at 10.25%

» Dave Gates Generating Station (DGGS) at Mill Creek

♦ Interim rates approved by the MPSC and included in our monthly electric supply rates

beginning January 1, 2011

beginning January 1, 2011

♦ Compliance filing reflecting final construction costs was filed in March of 2011

♦ Procedural schedule established setting a November 9, 2011 hearing date

» Distribution System Infrastructure Plan

♦ Received an accounting order from the MPSC in March 2011 to defer and amortize related

O&M expense for 2011 and 2012 over a 5 year period beginning 2013

O&M expense for 2011 and 2012 over a 5 year period beginning 2013

» Spion Kop wind project for 40 MW’s in rate base

♦ Executed an asset purchase agreement in April 2011 (contingent upon MPSC approval)

♦ Pre-approval application filed with the MPSC on May 31, 2011

♦ Procedural schedule established setting a December 14, 2011 hearing date

12

regulatory environment cont’d…

¾ South Dakota

» Filed natural gas rate case on May 20, 2011

♦ Requesting $4.1 million annual increase (7.2% average increase in rates)

♦ $2.7M related to rates (would impact earnings) - $1.4M related to recovery of manufactured

gas plant remediation costs (no earnings impact)

gas plant remediation costs (no earnings impact)

♦ 10.9% ROE, 8.68% ROR, 56.1% equity portion of capital structure

» State statute grants ability to file for automatic annual adjustment of charges for

environmental improvements (rider) for recovery of investment in Big Stone & Neal

emission compliance projects. Timing of the rider request will be in conjunction with

a general electric rate filing yet to be determined.

environmental improvements (rider) for recovery of investment in Big Stone & Neal

emission compliance projects. Timing of the rider request will be in conjunction with

a general electric rate filing yet to be determined.

¾ Nebraska

» Do not plan to file natural gas rate case during 2011 based on 2010 results

¾ FERC - Dave Gates Generating Station (DGGS)

» Docket filed on April 29, 2010 to establish rates as of January 1, 2011

» October 15, 2010, Order issued authorizing us to put our filed tariffs in place effective

January 1, 2011, subject to refund.

January 1, 2011, subject to refund.

» FERC subsequently set the docket for settlement discussions, which were

unsuccessful

unsuccessful

» Order issued June 2011 establishing a procedural schedule and set a January 23,

2012 hearing date with initial decision due by May 4, 2012

2012 hearing date with initial decision due by May 4, 2012

13

regulatory milestones in 2011…

Montana

Distribution Infrastructure

P Decision in favor of accounting order (MPSC)

Q1

Prudency Review for DGGS

P Interim rate filing (MPSC) 2010

Q4

ü Compliance Filing (MPSC)

Q1

ü Pre-hearing conference (FERC)

Q2

¾ Hearing (FERC)

Q4

Approval for Montana Wind Projects

P Pre-approval filing (MPSC)

Q2

¾ Hearing (MPSC)

Q4

Natural Gas - Rate Base Battle Creek

¾Filing to include in general rate base

(MPSC)

(MPSC)

Q3/Q4

|

South Dakota

|

|

|

Natural Gas Rate Case

|

|

|

ü Rate filing requesting $4.1M increase (SDPUC)

|

Q2

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

longer term investment opportunities…

¾ Distribution System Infrastructure Plan (DSIP)

» Incremental rate based investment to enhance safety, reliability

and capacity, improve rural service, and prepare the system for

adaptation of new technologies.

and capacity, improve rural service, and prepare the system for

adaptation of new technologies.

¾ Energy supply

» Big Stone and Neal plants’ pollution control equipment

» South Dakota peaking generation

» Wind projects and other renewable projects

» Natural gas reserves

¾ Transmission projects

» Network upgrades

» Colstrip 500 kV upgrade

» Mountain States Transmission Intertie (MSTI)

» 230 kV Renewable Collector System

» South Dakota transmission opportunities

14

15

potential project summary…

Note: Color / label indicate NorthWestern Energy's current probability of execution and timing of expenditures.

Opportunity to increase and diversify earnings as compared with our

existing $1.8 billion rate base.

existing $1.8 billion rate base.

in summary…

¾ Solid operations

¾ Single A secured credit ratings with a strong

balance sheet and liquidity

balance sheet and liquidity

¾ Positive earnings and ROE trend

¾ Strong cash flows

¾ Competitive total shareholder return with a

dividend that has increased every year since 2005

dividend that has increased every year since 2005

¾ Constructive regulatory environment

¾ Forbes.com “100 Most Trustworthy Companies”

¾ Realistic investment opportunities

16

appendix…

17

income statement…

18

balance sheet…

19

cash flow…

20

year over year earnings impacts…

21