Attached files

| file | filename |

|---|---|

| 8-K - 8-K - MATERION Corp | d8k.htm |

| EX-99.2 - EX-99.2 - MATERION Corp | dex992.htm |

Investor Presentation

July 2011

Materion

Corporation

Exhibit 99.1 |

Forward-Looking Statements

These slides contain (and the accompanying oral discussion will contain)

“forward-looking statements”

within the meaning of the Private Securities Litigation

Reform Act of 1995. These statements involve known and unknown risks, uncertainties

and other factors that could cause the actual results of the Company to

differ materially from the results expressed or implied by these statements,

including health issues, litigation and regulation relating to our business,

our ability to achieve and/or maintain profitability, significant cyclical

fluctuations in our customers’ businesses, competitive

substitutes for our products, risks associated with our international operations,

including foreign currency rate fluctuations, energy costs and the

availability and prices of raw materials, the timing and ability to achieve

further efficiencies and synergies resulting from our name change and

product line alignment under the Materion name and brand, and other factors

disclosed in periodic reports filed with the Securities and Exchange

Commission. Consequently these forward-looking statements should be regarded as

the Company’s current plans, estimates and beliefs.

The Company does not undertake and specifically declines any obligation to publicly

release the results of any revisions to these forward-looking statements

that may be made to reflect any future events or circumstances after the

date of such statements or to reflect the occurrence of anticipated or

unanticipated events. 2 |

MATERION TODAY:

New Name, Same Impressive Performance

3

19%

CAGR

Sales

growth

(2005

–

2010)

30%

CAGR

Operating profit

growth

(2005

–

2010)

Successful

Repositioning

of company |

THESIS

Positioned to Deliver Long-Term, Sustainable Growth

4

A company

with a strong

platform… |

The

Repositioning of Materion Prior to 2002

2002 –

2010

2011 +

Metals and

mining focus

Repositioning

Sustained

growth

5 |

Successful

Repositioning

–

Snapshot

6

Revenues

Revenue % in

Advanced Materials

Sales per employee

(thousands)

Debt-to-Debt-Plus-Equity

Working capital

% of sales

Cyclicality

$373M

47%

$200

43%

41%

High

$1.3B

2010

2002

75%

$524

18%

25%

Low |

Operating Businesses are Well-Positioned and Growing

7

Business

End Markets

(Examples)

Products

(Examples)

Sales Growth

(2002-2010)

Advanced Materials

•

Wireless

•

LED

•

Optical

•

Medical

•

Alternative

energy

•

PVD targets

•

Optical / medical

coatings

•

Electronic packaging

•

Inorganic powders

453%

75% of revenues

Integrated Metals

•

Wireless

•

Oil & gas

•

Aerospace

•

Heavy equipment

•

Defense

•

Electronic connectors

•

Directional drilling

components

•

Optical structures

•

Bushings and bearings

68%

25% of revenues |

Positioned in Diverse Set of High-Growth Markets

8

Growth

Entered multiple leading-edge growth markets since 2002

Defense

Commercial Aerospace

Medical

Devices

Optics

Telecom

Infrastructure

LED’s

Alternative

Energy

LCD

Space /

Science

Notebooks

Cellular phones

(smartphones),

Tablet computers

Heavy

Equipment

Disk Drives |

High

Operating Margins Operating

Profit %

Operating Profit % of

Value-Added

(1)

Integrated Metals

11 –

13%

14 –

16%

Advanced Materials

5 –

7%

22 –

24%

Company

5 –

7%

13 –

15%

9

Removing High Value Metals Clarifies True Margins

2010

Note (1): Excludes high value metals from sales |

A

Global Platform Operations in US

and 11 Countries

Significant and Expanding

International Sales

2010

28%

“Direct”

International

Sales

10

Customers in >50 countries

Expect “direct”

international sales

to be 40 -

50% in 3-5 years |

THESIS

Positioned to Deliver Long-Term, Sustainable Growth

11

…

Leveraging a

high value-added

business

model… |

High Value-Added Business Model

12

1.

Target high growth

markets

2.

Own fast growing

niches

3.

Expand with

innovative

products

4.

Add synergistic

acquisitions

5.

Ensure

financial

discipline |

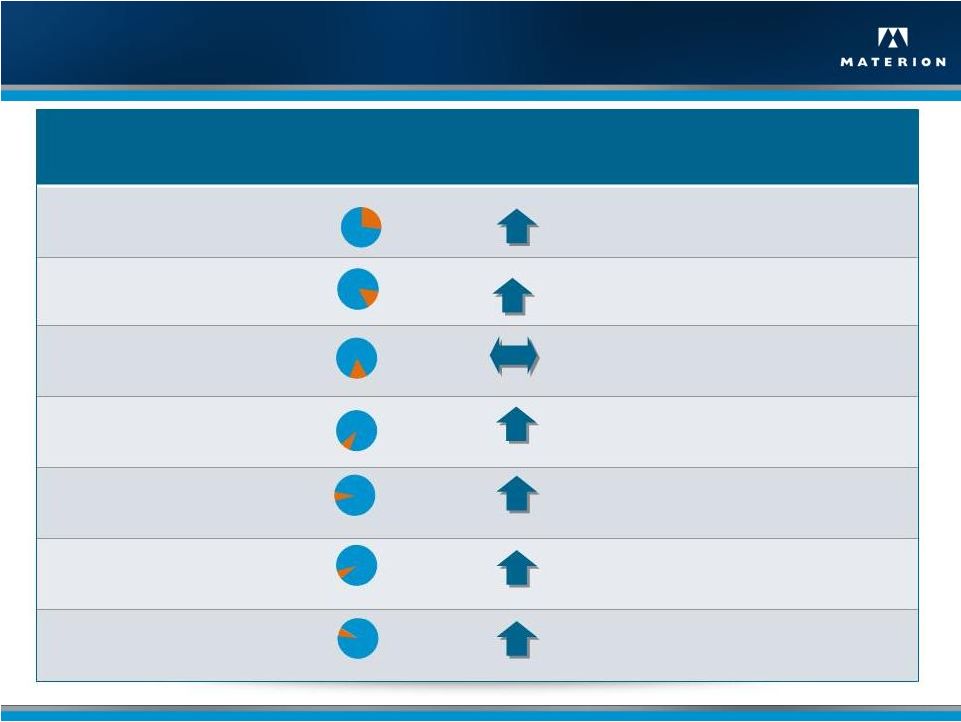

Market

Q1 2011

% of Value-

Added Sales

2011

Trends

Key Drivers

Consumer Electronics

26%

•

Smartphone growth

•

Tablet computers & LEDs

•

Miniaturization

Industrial Components &

Commercial Aerospace

14%

•

New airplane builds & retrofits

•

Increasing air travel

•

Heavy equipment builds

Defense & Science

13%

•

DoD & foreign military budgets

•

Demand for communications satellites

•

High performance optical devices

Automotive Electronics

8%

•

Increasing global car production

•

HEV/EV lithium ion battery components

•

Engine control & electronic systems

Energy

8%

•

Directional drilling

•

Rig counts

•

Solar, batteries & smart grid devices

Telecommunications

Infrastructure

7%

•

Global 3G/4G builds

•

Base stations

•

Undersea fiber-optics expansion

Medical

7%

•

Glucose testing

•

Diagnostics equipment

1. Target High Growth, Leading-Edge Markets

13 |

1.

Target High Growth, Leading-Edge Markets 14

Reportable Segments

ADVANCED MATERIAL

TECHNOLOGIES

PERFORMANCE

ALLOYS

BERYLLIUM &

COMPOSITES

TECHNICAL

MATERIALS

Key Markets

Precious, Non-precious,

Specialty Metal and Inorganic

Materials; Electronic Packages

and Components

Bulk and Strip Form Products

and Beryllium Hydroxide

Beryllium and Beryllia Ceramic

Products

Specialty Strip Metal

Products

CONSUMER

ELECTRONICS

DEFENSE & SCIENCE

INDUSTRIAL

COMPONENTS &

COMM. AEROSPACE

AUTOMOTIVE

ELECTRONICS

TELECOM

INFRASTRUCTURE

APPLIANCE

MEDICAL

ENERGY |

2.

Own The Niche – Examples

•

Only fully integrated producer of beryllium

–

one-of-a-kind business

15

Leading position

in niche

•

Unique

copper-nickel

material

ToughMet

–

multiple advanced applications growing at

over 30% annually

•

Optical coatings

–

highly sophisticated uses for defense

and medical applications

•

Smartphone applications

–

currently in 95% of all smartphones,

expected to grow 50% in 2011

TM |

3.

Continually Develop Innovative Products •

Customer-centric product development

•

Active research programs

•

New product areas include

–

LEDs

–

Medical

–

Commercial Optics

–

Disk drive arms

–

Solar

–

Batteries

–

Science

–

Commercial Aerospace

16 |

4.

Synergistic Acquisitions

–

Strong

Record

Add complementary

products / technology

Expand market

position

Accretive in

year 1

OMC –

shield kit cleaning

TFT –

thin film coatings

CERAC –

inorganic chemicals

Techni-Met –

thin film coatings

Barr –

thin film coatings

Academy –

precious metals

17

By 2010, added over $300M to sales and approximately 25% of company profit

Acquisitions 2005-2010 –

Impact |

4.

Synergistic Acquisitions Case Study of Growing a Niche Business

–

Optical Filters and Medical Coatings

(Revenues)

18

Today (2010)

•

Revenues of $91M

•

78% CAGR

•

Positioned in $1.2B+

market growing at

11% annually

$9M

$82M

Barr

(2009)

Barr

(2009)

Techni-

Met

(2008)

Techni-

Met

(2008)

TFT -

2006

Acquisitions & Growth |

5.

Ensure Financial Discipline Maintain strong

balance sheet

Debt-to-Debt-Plus-Equity

Strong

cash flow

•

Cash flow from operations

$30M -

$75M annually

•

Capex below depreciation

•

Reduction in working

capital

goal

to

<20%

sales

Resources to

finance

acquisitions of

$50M to $100M

annually

After $175M in acquisitions (net)

0%

10%

20%

30%

2005

2010

18%

21%

Maximum 30%

19 |

THESIS

Positioned to Deliver Long-Term, Sustainable Growth

20

…

Executing

a focused

growth plan

1

2

3 |

Financial Goals Next 3-5 Years

2010

Next 3-5 years

Revenue growth –

organic

35%

>10%

Acquisitions

$21M

$50 -

$100M

per year

Margins (OP % VA)

14%

14% -

18%

Working capital % sales

25%

<20%

Debt to Debt-Plus-Equity

18%

<30%

ROIC (pre-tax)

17%

>20%

21 |

Continuing to Execute Three Point Strategy

22

1

Grow and diversify revenue base

2

Expand margins

3

Improve fixed and

working capital utilization

Increasing Shareholder Value |

STRATEGY #1: GROWTH

Expand and Diversify Revenue Base

•

Targeting expansion in growth markets including:

–

smart mobile devices, 3G / 4G, commercial aerospace, oil & gas, alternative

energy, optics, LED / LCD

•

Ongoing global expansion

–

Asia

•

Strategic acquisition

fast accretion

–

Technology

–

Global reach

23 |

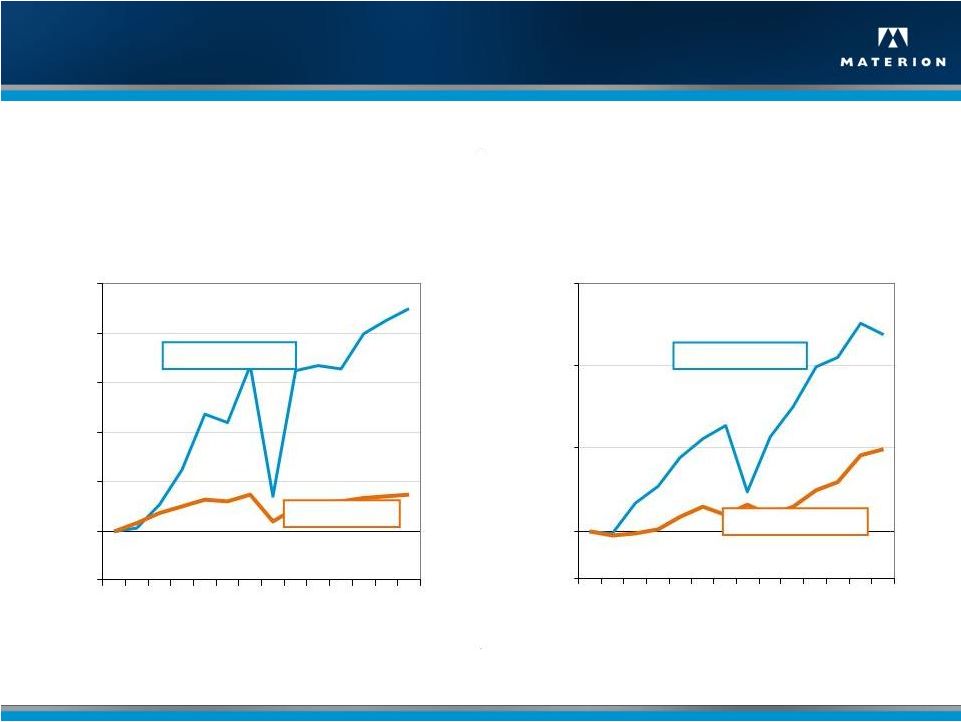

STRATEGY #1: GROWTH

Strategy in Action: Outgrowing Growth Markets

Growth of Materion

Oil and Gas Sales vs. Market

Growth of Materion

Aerospace Sales vs. Market

24

1.00

2.00

3.00

4.00

5.00

6.00

02

Index numbers

2002 = 1.00

Materion sales

Rig count

04

06

08

10

12-F

14-F

+450%

+80%

1.00

2.00

3.00

4.00

Index numbers

2002 = 1.00

Materion sales

Aircraft delivered

02

04

06

08

10

12-F

14-F

+240%

+100% |

STRATEGY #2: MARGINS

Expand Margins –

Key Drivers

25

1

Lean Sigma

operating

efficiency

2

Higher value

added products

3

Cost

reductions

Margin

Today

12 -

14%

Target

Margin

14 -

18%

(OP % VA) |

STRATEGY #3: CAPITAL EFFICIENCY

Improve Fixed and Working Capital Efficiency

26

Lean Sigma

•

Cycle time reduction

•

Yield improvement

•

On-time shipments

Based on 2011 projected sales, each 5% of working capital efficiency = $43M of

cash Improve Working Capital

Efficiency

Working capital % of sales

2002

2010

Target

41%

25%

< 20% |

2011 Outlook and Guidance

Revenues

($B)

EPS

($)

27

$1.55B

$2.35 -

$2.60

$1.3B

2010

2011(F)

$2.25

2010

2011(F) |

IN

SUMMARY Why Invest in Materion Corporation

28

Positioning

Niche leader in high-growth markets

Performance

Strong performance record

Growth

Executing three point strategy

•

Global player, strong secular market drivers

•

Sustainable long-term growth

•

Proven business model

•

Target, expand, then own niche

•

Clear financial goals, performance

continuing to improve |

Investor Presentation

July 2011

Materion

Corporation |