Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DYNEX CAPITAL INC | d8k.htm |

Dynex

Capital, Inc. Investor Presentation

June 15, 2011

Exhibit 99.1 |

2

Safe Harbor Statement

NOTE:

This presentation

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation Reform Act of 1995, including statements about projected future investment

strategies and leverage ratios, financial performance, the projected impact of NOL

carryforwards, future dividends paid to shareholders, and future investment

opportunities and capital raising activities. The words “will,”

“believe,”

“expect,”

“forecast,”

“anticipate,”

“intend,”

“estimate,”

“assume,”

“project,”

“plan,”

“continue,”

and similar expressions also identify forward-looking statements that are inherently

subject to risks and uncertainties, some of which cannot be predicted or quantified.

Although these forward-looking statements reflect our current beliefs, assumptions

and expectations based on information currently available to us, the Company’s

actual results and timing of certain events could differ materially from those

projected in or contemplated by these statements. Our forward-looking statements

are subject to the following principal risks and uncertainties: our ability to find suitable

reinvestment opportunities; changes in economic conditions; changes in interest rates and

interest rate spreads; our investment portfolio performance particularly as it relates

to cash flow, prepayment rates and credit performance; the cost and availability of

financing; the cost and availability of new equity capital; changes in our use of

leverage; the quality of performance of third-party servicer providers

of

our

loans

and

loans

underlying

our

securities;

the

level

of

defaults

by

borrowers

on

loans we have securitized; changes in our industry; increased competition; changes in

government regulations affecting our business; government initiatives to support the

U.S financial system and U.S. housing and real estate markets; GSE reform or other

government policies and actions; and an ownership shift under Section 382 of the

Internal Revenue Code that impacts the use of our tax NOL carryforward. For additional

information, see the Company’s Annual Report on Form 10-K for the year ended

December 31, 2010, and other reports filed with and furnished to the Securities and Exchange

Commission. |

3

Our Guiding Principles

Our Core Values

Generate dividends for our shareholders

Manage leverage conservatively

Remain owner-operators

Maintain a culture of integrity and employ the highest ethical standards

Provide a strong risk-management culture

Focus on long-term shareholder value while preserving capital

Our Mission

Manage a successful public mortgage REIT with a focus on capital

preservation and providing risk-adjusted returns reflective of a diversified,

leveraged fixed income portfolio. |

4

DX Snapshot

Company Highlights

Internally managed REIT commenced operations in 1988

Significant insider ownership and experienced management team

Diversified investment strategy in residential and commercial mortgage assets

Large NOL carryfoward for unique total return opportunity

Market Highlights

NYSE Stock Ticker

DX

Shares Outstanding (6/10/2011)

40,343,159

Quarterly Dividend (2Q 2011)

$0.27

Share Price (6/10/2011)

$9.71

Price to Book (6/10/2011)

1.02

Market Capitalization (6/10/2011)

$391.7 million |

5

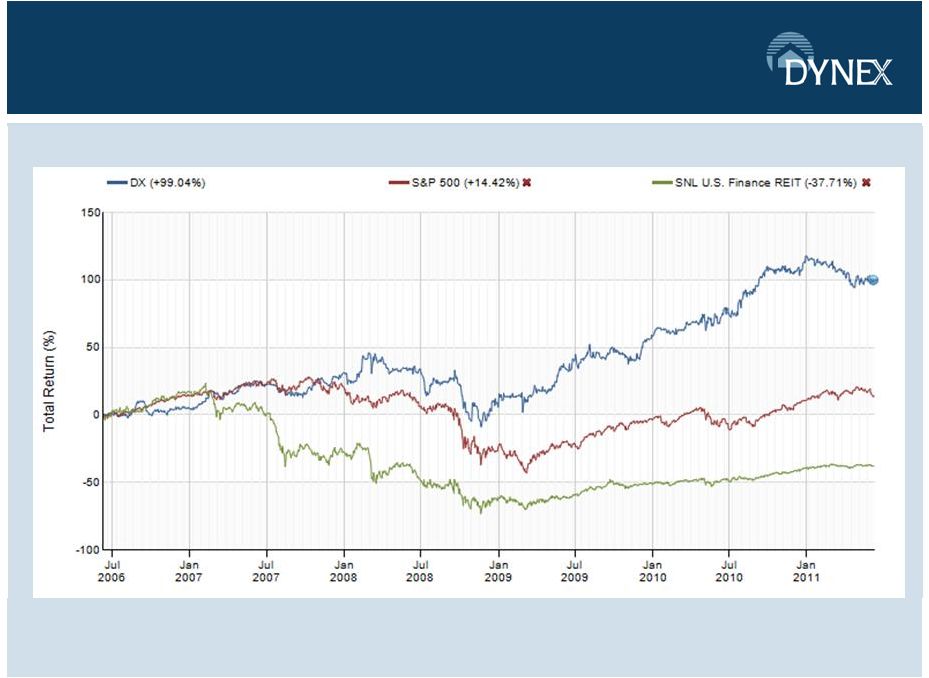

Long Term Performance

Five Year Total Return

Source: SNL Financial.

(1)

Based on beginning share price of $6.75 on 6/9/06 and ending share price of $9.72 on 6/9/11.

Assumes reinvestment of dividends. (2)

SNL U.S. Finance REIT: Includes all publicly traded (NYSE, NASDAQ, OTC BB, Pink Sheets)

Investment Companies with the following primary focuses: MBS REIT, Mortgage REIT, and

Specialty Finance REITs in SNL’s coverage universe. (1)

(2) |

6

Management Team

Experienced team of professionals with a combined 80 years of experience

managing mortgage REITs and mortgage portfolios

•

–

32 years of experience in the industry and 7 years at Dynex

–

Chairman since 2003 and CEO since 2008

–

Managing Member of Talkot Capital, LLC

–

16 years at Merrill Lynch and Salomon Brothers

•

Byron

L.

Boston

–

Chief

Investment

Officer

–

27 years of experience in the industry with 3 years as CIO at Dynex

–

13 years managing levered multi-product portfolios at Freddie Mac and Sunset Financial

Resources –

11 years trading MBS on Wall Street

–

3 years Senior Corporate Lending Officer at Chemical Bank

•

Stephen

J.

Benedetti

–

Chief

Financial

Officer

and

Chief

Operating

Officer

–

21 years of experience in the industry

–

Employed at Dynex for 16 years in various treasury, risk management and financial reporting

roles –

Managed Dynex from 2002 –

2007

–

Began career at Deloitte & Touche

•

Portfolio

Management

Team

–

4 member team with a collective 55 years of industry experience with broad and deep skill sets

in both agency and non-agency investment strategies

Thomas B. Akin –

Chairman and Chief Executive Officer |

7

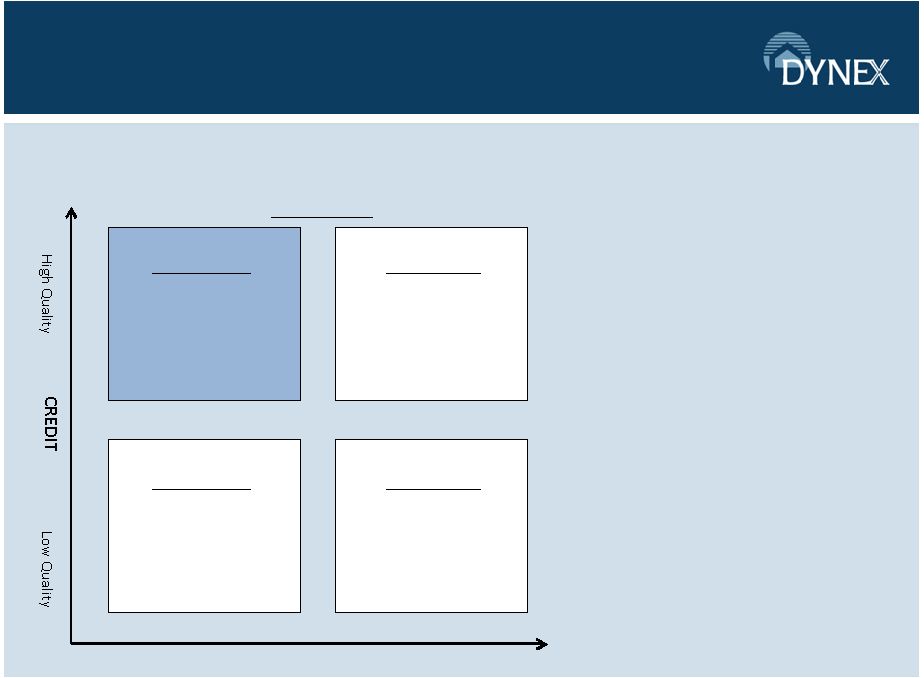

Diversified Investment Strategy

Diversified Investment Strategy

that invests in a combination of Agency and non-Agency

residential and commercial assets to maximize risk adjusted total return.

DURATION

Examples include:

-

Short Duration Agency

ARMs

-

Seasoned non-Agency

RMBS & CMBS

Target Strategy

Examples include:

-

Floating Rate Mezzanine

Examples include:

-

30 year Agency MBS

Current Coupon

-

Super Senior CMBS

Examples include:

-

Credit Sensitive

-

Securities Rated below BBB

Long

Short

FUNDING:

•Prudent leverage

•Diversified counterparty profile to

avoid concentration risk

•Active maturity management to

ensure stable financing profile

Lower Credit Quality /

Short Duration

Lower Credit Quality /

Long Duration

Higher Credit Quality /

Short Duration

Higher Credit Quality /

Long Duration |

8

Myriad of MREIT Risks

•

Interest Rate Risk –

net duration gap

•

Extension Risk –

limited duration extension is key

•

Credit Risk –

higher probability of repayment vs. higher yield

•

Leverage Risk –

liquidity of assets financed is key

•

Prepayment Risk –

most attractive theme over the past 3 years

•

Management Risk –

management and shareholder alignment

•

Regulatory Risk –

uncertainty around complex business model

•

Financing Risk –

most important risk |

9

Investment Portfolio as of 3/31/11

A

2%

AA

1%

Below A

3%

AAA

94%

Seasoned

DX

RMBS/loans

3%

Agency MBS

82%

Other

CMBS/

RMBS

3%

Seasoned

DX

CMBS/loans

12%

•

High quality portfolio of primarily Agency securities, as well as seasoned loans originated by

Dynex in 1990’s

•

94% AAA securities, 97% rated A or higher

•

Relative to other diversified REITs Dynex maintains a higher credit quality portfolio

(1) Percentages based on asset carrying basis.

Composition

(1)

Ratings

(1) |

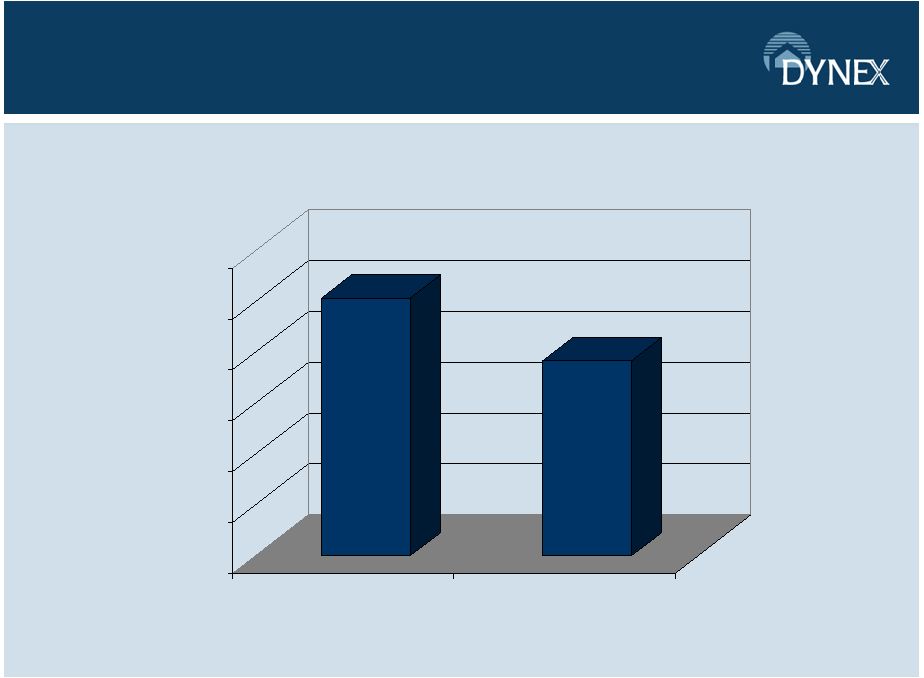

10

Credit Portfolio Comparisons

$101.43

$76.73

$-

$20

$40

$60

$80

$100

$120

DX

Wgt Average of Other Hybrid

REITs

Average 2010 Year-End Portfolio Non-Agency Price

(1) Consists of the weighted average of dollar prices for non-Agency investments as of

12/31/10 for MFA, IVR, and TWO. (1) |

11

Interest Rate Risk

Change in Value from Change in Rates

Portfolio Value

(2)

Equity Value

(3)

Ticker

+50

+75

+100

+75

+100

AGENCY MBS

NLY

6.3

-1.80%

-2.50%

-15.8%

ANH

7.1

-2.60%

-18.5%

HTS

6.1

-0.53%

-1.75%

-10.7%

AGNC

7.6

-0.40%

-1.10%

-8.4%

CYS

8.1

-2.14%

-3.25%

-26.3%

ARR

9.5

-0.79%

-1.74%

-16.5%

DIVERSIFIED MBS

DX

5.2

-0.50%

-1.10%

-5.7%

IVR

5.3

-0.56%

-1.24%

-6.6%

MFA

2.9

-0.54%

-1.19%

-3.5%

TWO

3.8

-0.20%

-0.40%

-2.0%

CIM

1.8

-2.50%

-3.79%

-6.8%

(1) As

disclosed

in

each

company’s

10-Q

for

quarter

ended

March

31,

2011.

Ratios

are

dependent

on

each

company’s

method

of

calculation.

(2) As of March 31, 2011, as disclosed in each company’s 10-Q for

quarter ended March 31, 2011. Percentages are dependent on each company’s assumptions, as

disclosed in their 10-Qs.

(3) Unless the figure is otherwise disclosed in a company’s 10-Q for

quarter ended March 31, 2011, equals estimated % decrease for the +75/+100 scenarios

multiplied

by

estimated

company

leverage,

and

is

meant

to

show

the

potential

change

in

equity

value

for

the

corresponding

change

in

rates.

Estimated

Company

Leverage

(1) |

Interest

Rate Risk as of March 31, 2011

Basis Point Change in Mortgage Spreads

Basis Point Change in

Interest Rates

-

50

-

25

0

+25

+50

+100

0.9%

(0.2)%

(1.1)%

(2.1)%

(3.1)%

+50

1.5%

0.5%

(0.5)%

(1.5)%

(2.4)%

0

2.0%

1.0%

–

(1.0)%

(1.9)%

-50

2.4%

1.4%

0.4%

(0.6)%

(1.6)%

-100

2.6%

1.6%

0.6%

(0.4)%

(1.3)% |

13

Important Macro Themes

Multiple factors combining to depress economic activity

Fed funds rate at historic lows with a steep yield curve

Global risk remains high

Government policy/regulations to influence investment returns

Both GSE’s and U.S. government are reducing MBS holdings

Improved financing environment

Low volatility environment rewarding leveraged investment

strategies

Tighter credit standards have created more predictable

mortgage cash flows and better investment opportunities

Securitization markets are healing slowly but unevenly |

14

Potential Return Profile for Prospective

Investments as of June 13, 2011

The above portfolio is for illustrative purposes only, does not represent actual or expected

performance and should not be relied upon for any investment decision. The range of

returns on equity is based on certain assumptions, including assumptions relating to asset allocation

percentages and spreads where new mortgage assets can be acquired versus a current cost of

funds to finance acquisitions of those assets. Rates

used

represent

a

range

of

asset

yields

and

financing

costs

based

on

data

available

as

of

the

date

referenced

above.

Any

change

in

the

assumed yields, financing costs or assumed leverage could materially alter the company’s

returns. The performance results above do not include assumption for the deduction of

investment advisory fees, expenses, or commissions. The performance results assume that no cash

was

added

to

or

assets

withdrawn

from

the

portfolio

and

that

all

dividends,

gains

and

other

earnings

in

the

portfolio

were

reinvested.

There

can be no assurance that asset yields or financing costs will remain at current levels. For a

discussion of risks that may affect our ability to implement

strategy

and

other

factors

which

may

affect

our

potential

returns,

please

see

the

section

entitled

“Risk

Factors”

in

our

Annual

Report on Form 10-K for the year ended December 31, 2010.

Investment

Range of

Prices

Range of

yields

Range of net

spread to

funding

Range of

ROEs

Agency

RMBS

103-108

2.3%-

3.8%

1.3%-3.0%

13%-27%

CMBS

105-109

3.5%-4.0%

1.3%-2.3%

12%-20%

Non–Agency

‘AAA’

RMBS

90-102

3.6%-6.0%

2.6%-4.0%

14%-21%

‘AAA’

CMBS

100-105

4.8%-6.1%

2.0%-3.0%

15%-16% |

15

Balance Sheet Overview

as of March 31, 2011

(1) Associated financing for investments includes repurchase agreements, securitization

financing issued to third parties and TALF financing (the latter two of which are

presented on the Company’s balance sheet as “non-recourse collateralized financing”).

(2) Includes hedging instruments, cash and cash equivalents, and other assets/other

liabilities. •

5.2x actual leverage

•

Unsecuritized single family and commercial mortgage

loans

•

Loans pledged to support repayment of securitization

bonds issued by the Company

•

Originated in the mid 1990’s

•

Principal balance of $15.7 mm

•

1Q 2011 weighted average annualized yield of 5.54%

•

71.9% “AAA”

and “AA”

rated

•

Principal balance of $244.7 mm

•

1Q 2011 weighted average annualized yield of 5.96%

•

~78.3% “AAA”

and “AA”

rated

•

Fixed rate agency CMBS

•

$1,340.4 mm in Hybrid Agency ARMs

-

Weighted average months-to-reset of 37 months

•

$280.2 mm in Agency ARMs

-

Weighted average months-to-reset of 6 months

Notes

5.5 –

6.5x

–

2 –

3x

4 –

5x

4 –

5x

7 –

8x

7 –

9x

Leverage

Target

$383.5

($1,976.3)

$2,359.8

Total

59.0

(21.2)

80.2

Other

(2)

1.2

–

1.2

Other

investments

40.2

(103.2)

143.4

Securitized

mortgage loans

3.4

(11.5)

14.8

Non-Agency

RMBS

42.1

(208.3)

250.4

Non-Agency

CMBS

74.0

(175.1)

249.1

Agency CMBS

$163.6

($1,457.0)

$1,620.7

Agency RMBS

Allocated

Shareholders

’

Equity

Associated

Financing

(1)

/

Liability

Carrying

Basis

Asset

Carrying

Basis

•

5.2x actual leverage

•

Unsecuritized single family and commercial mortgage

loans

•

Loans pledged to support repayment of securitization

bonds issued by the Company

•

Originated in the mid 1990’s

•

Principal balance of $15.7 mm

•

1Q 2011 weighted average annualized yield of 5.54%

•

71.9% “AAA”

and “AA”

rated

•

Principal balance of $244.7 mm

•

1Q 2011 weighted average annualized yield of 5.96%

•

~78.3% “AAA”

and “AA”

rated

•

Fixed rate agency CMBS

•

$1,340.4 mm in Hybrid Agency ARMs

-

Weighted average months-to-reset of 37 months

•

$280.2 mm in Agency ARMs

-

Weighted average months-to-reset of 6 months

Notes

5.5 –

6.5x

–

2 –

3x

4 –

5x

4 –

5x

7 –

8x

7 –

9x

Leverage

Target

$383.5

($1,976.3)

$2,359.8

Total

59.0

(21.2)

80.2

Other

(2)

1.2

–

1.2

Other

investments

40.2

(103.2)

143.4

Securitized

mortgage loans

3.4

(11.5)

14.8

Non-Agency

RMBS

42.1

(208.3)

250.4

Non-Agency

CMBS

74.0

(175.1)

249.1

Agency CMBS

$163.6

($1,457.0)

$1,620.7

Agency RMBS

Allocated

Shareholders

’

Equity

Associated

Financing

(1)

/

Liability

Carrying

Basis

Asset

Carrying

Basis

(Dollars in Millions)

_ |

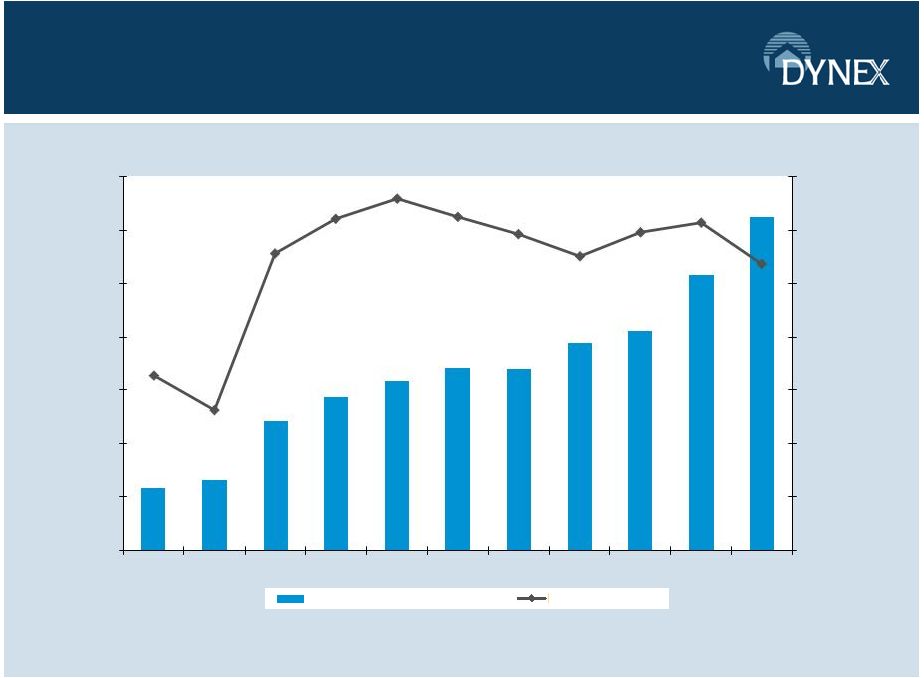

16

Earnings –

Paid and Retained

We Pay a Dividend AND Generate and Retain Earnings

(Utilizing our NOL) to Grow Book Value

($0.10)

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

Dividends Declared

Excess Earnings Retained |

17

Investment Portfolio Income and Spread

$ in thousands

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Net interest income after provision

Net interest spread |

18

Why Dynex

Excellent long term performance record

Strong and defensive balance sheet positioned to weather market

volatility

Experienced management with a track record of disciplined capital

deployment through multiple economic cycles

Alignment of interests with shareholders due to owner-operator

structure

Complementary investment opportunities exist with attractive

return profiles consistent with our investment philosophy

Opportunistic capital raises have increased shareholder value

without significant book value dilution |