Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Bristow Group Inc | d8k.htm |

Fourth Quarter FY 2011

Earnings Presentation

Bristow Group Inc.

May 11, 2011

Exhibit 99.1 |

Fourth quarter earnings call agenda

Introduction

(Linda

McNeill,

Investor

Relations

Manager)

CEO

remarks

(Bill

Chiles,

President

and

CEO)

Financial

discussion

(Jonathan

Baliff,

SVP

and

CFO)

Operational

highlights

(Bill

Chiles,

President

and

CEO)

Questions and answers

2 |

Forward-looking statements

3

This presentation may contain “forward-looking statements” within the meaning of the

Private Securities Litigation Reform Act of 1995. Forward-looking statements include

statements about our future business, operations, capital expenditures, fleet composition,

capabilities and results; modeling information, earnings guidance, expected operating margins

and other financial projections; future dividends; plans, strategies and objectives of our

management, including our plans and strategies to grow earnings and our business, our general

strategy going forward and our business model; expected actions by us and by third parties, including

our customers, competitors and regulators; our use of excess cash; the valuation of our company and

its valuation relative to relevant financial indices; assumptions underlying or relating to any

of the foregoing, including assumptions regarding factors impacting our business, financial

results and industry; and other matter Our forward-looking statements reflect our views and

assumptions on the date of this presentation regarding future events and operating performance.

They involve known and unknown risks, uncertainties and other factors, many of which may be

beyond our control, that may cause actual results to differ materially from any future results,

performance or achievements expressed or implied by the forward-looking statements. These

risks, uncertainties and other factors include those discussed under the captions “Risk

Factors” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations” in our Annual Report on Form 10-K for the fiscal year ended

March 31, 2010 and our Quarterly Reports on Form 10-Q for the quarters ended June 30,

September 30 and December 31, 2010. We do not undertake any obligation, other than as

required by law, to update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise.

|

Chief Executive comments

Bill

Chiles,

President

and

CEO

4 |

Aviation Support Services KPI History

* Includes commercial operations only

5 |

Q4

and FY2011 highlights 6

•

Bristow delivered to shareholders in FY2011:

•

Second half performance was stronger than the first half with increased levels of

activity, aircraft sales, pricing in Europe and earnings from our

unconsolidated affiliate in Brazil

•

Our cost of capital was significantly lowered with refinancings and a corporate

reorganization •

A new capital allocation framework was introduced culminating in

the announcement of the initiation

of a quarterly dividend of $0.15

•

Earnings per share guidance will also commence with a FY 2012 range of $3.55 to

$3.90 •

Q4 Revenue of $310M (10% increase from Q4 FY2010,

2% decrease from Q3 FY2011)

•

Q4 EPS, excluding special items, of $1.00 (37% increase

from Q4 FY2010, 41% increase from Q3 FY2011)

•

Q4 GAAP EPS of $0.84 (8% increase from Q4 FY2010,

26% decrease from Q3 FY2011)

•

Q4 Operating income of $50M (16% increase from Q4

FY2010, 7% increase from Q3 FY2011)

•

Q4 EBITDA of $77M (30% increase from Q4 FY2010,

18% increase from Q3 FY2011)

•

FY 2011 Revenue of $1.233B (6% increase from FY2010)

•

FY 2011 EPS, excluding special items, of $3.30 (9% increase from

FY2010)

•

FY 2011 GAAP EPS of $3.60 (16% increase from FY2010)

•

FY 2011 Operating income of $190M (5% increase from FY2010)

•

FY 2011 EBITDA of $277M (7% increase from FY2010) |

•

Oil prices have fallen from highs but still relatively strong. Lower prices

create a more sustainable economic recovery

•

Overall international Exploration & Production (E&P) capital expenditures

and operating expenditures continue to grow

•

The modest growth in 2010, has led to solid recovery so far in calendar

year 2011 with signals of faster expansion in 2012 and 2013

•

Balanced across non-U.S. geographies, with Brazil and Australia looking

particularly promising

•

Although U.S. ops were challenging in early 2011, recovery is discernable

•

This E&P confidence is reflected in improved helicopter tender activity,

principally for FY 2012/2013 work

•

Aircraft sales for our helicopters improved significantly this quarter

Current market environment

7 |

Q4

2011 YOY Operational performance highlights Europe

Revenue

and

operating

margin

is

higher

year

over

year

due

to

new

customers,

increased

activity and cost management.

West Africa

Revenue rose because of new contracts and rate escalations on existing contracts

and reduced number of aircraft maintenance delays. However, operating

margin is lower due to a high level of maintenance and freight costs in the

quarter. Australia

Revenue

increased

significantly

from

new

contracts

and

favorable

exchange

rates; higher

compensation costs and non-recurring costs drove operating margin lower.

However, sequentially better versus the third quarter.

Other International

Revenue benefited from new contracts in the Baltic Sea and Suriname and higher

activity in Brazil, Trinidad and Russia. Operating income improved

significantly due to strong performance by Lider in Brazil.

North America

Lower revenue and profitability due to poor weather in February and end of support

work for BP. A few drilling permits were issued in Q4. Activity

has started to pick up very recently. 8 |

Financial discussion

Jonathan

Baliff,

SVP

and

CFO

9 |

Financial highlights –

Earnings per share summary

4Q FY10 to 4Q FY11 bridge

FY10 to FY11 bridge

10 |

Financial highlights –

EBITDA summary

4Q FY10 to 4Q FY11 bridge

11

FY10 to FY11 bridge |

Reconciliation of special items

Fourth Quarter FY 2011 & Full Year FY 2011

12

See the reconciliation of special items for the Fourth Quarter FY 2010 & Full

Year FY 2010, and the footnotes to this table included in the appendix to this

presentation. March 2011 Quarter

Operating

Income

EBITDA

Net

Income

Diluted

Earnings

Per

Share

(Unaudited)

(In thousands, except per share amounts)

Adjusted for special items...............

$

56,653

$

79,905

$

37,001

$

1.00

Impairment of IT system

(1)

...........

(5,306)

—

(3,449)

(0.09)

Held for sale aircraft

impairment

(2)

............................

(1,500)

—

(1,095)

(0.03)

Impairment of investment in

affiliate

(3)

....................................

—

(2,445)

(1,589)

(0.04)

As reported.....................................

$

49,847

$

77,460

$

30,868

0.84

Fiscal Year Ended

March 31, 2011

Operating

Income

EBITDA

Net

Income

Diluted

Earnings

Per

Share

(Unaudited)

(In thousands, except per share amounts)

Adjusted for special items...............

$

193,030

$

278,708

$

121,285

$

3.30

Impairment of IT system

(1)

...........

(5,306)

—

(3,449)

(0.09)

Held for sale aircraft

impairment

(2)

.............................

(1,500)

—

(1,095)

(0.03)

Impairment of investment in

affiliate

(3)

....................................

—

(2,445)

(1,589)

(0.04)

Power-by-the-hour credit

(4)

..........

3,500

3,500

2,520

0.07

Retirement of 6 1/8% Senior

Notes

(5)

.......................................

—

(2,300)

(3,055)

(0.08)

Income tax items

(6)

.....................

—

—

17,698

0.48

As reported....................................

$

189,724

$

277,463

$

132,315

3.60 |

Quarterly dividend initiation

13

•

On May 4, 2011, the Board of Directors of Bristow declared a first quarter cash

dividend of $0.15 per share of our common stock.

•

The dividend will be paid on June 10, 2011 to stockholders of record on May 20,

2011; approximately $5.4 million payment expected.

•

If held at this level and paid quarterly (subject to quarterly Board approval), we

expect the dividend to yield 1.4% annually based on a $43.81 stock

price. •

We are confident in the underlying ability of Bristow to generate cash flow while

growing the business across the globe.

•

We believe a dividend payment will make our stock more attractive to international

and income-oriented investors.

•

In FY 2012 and future periods, we will continually evaluate excess liquidity and

optimal capital structure in consideration of any increase in the level of

dividends or other possible return of cash to our investors.

|

FY

2012 earnings guidance •

Issuance of annual earnings guidance demonstrates Bristow’s confidence in our

business model anchored by the underlying contractual stability serving

mostly offshore production, which makes our operating performance more

stable and predictable. •

Our objectives in providing annual earnings guidance include:

•

Aligning shareholders and other market participants with management’s

expectation of our operational performance and how management directs and

operates our business. •

Increasing BRS trading liquidity and lowering our cost of equity.

•

Earnings per share guidance for fiscal year 2012 is $3.55 to $3.90.

•

Earnings per share guidance does not include unrealized gains and losses on

disposals of assets as well as special items because their timing and

amounts are more variable and less predictable. •

Perspectives on the FY 2012 adjusted earnings guidance range will be updated on

subsequent quarterly calls.

14 |

Operational highlights

Bill

Chiles,

President

and

CEO

15 |

Quarter-over-quarter changes in Operating Income

16

Operating income for Q4 2011 is $50.5M

Operating income for Q4 2010 is $42.8M

*

Excludes centralized operations, corporate, gain on sale of assets, and Bristow

Academy. In Q4 FY 2011, North America was loss of $1.6 million and is

not included. |

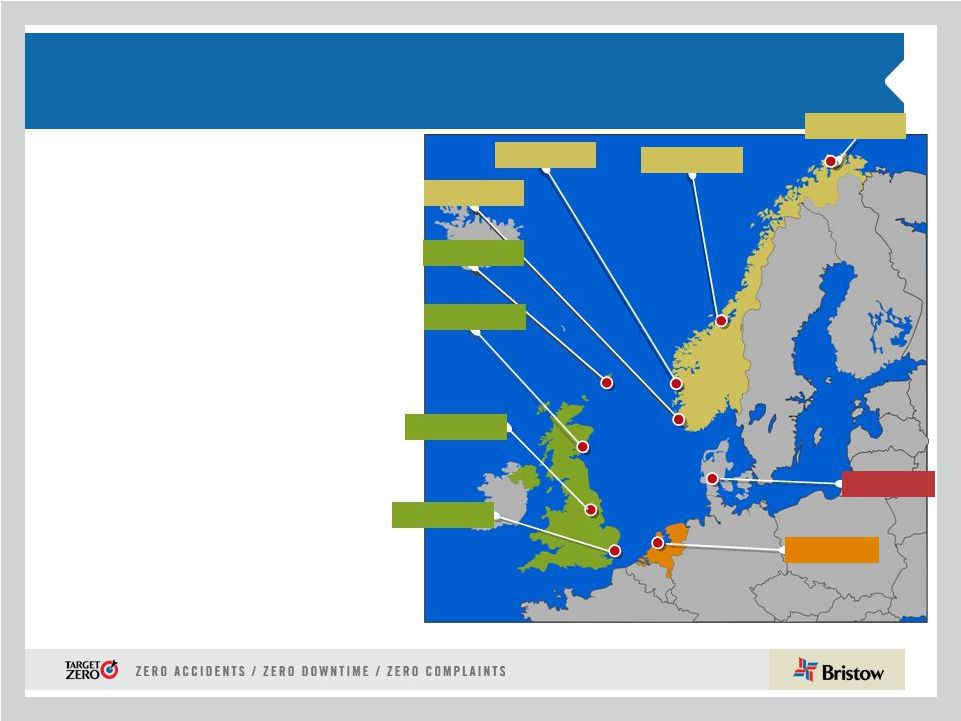

Europe (EBU)

UK

Netherlands

Norway

Norwich

Aberdeen

Scasta

Stavanger

Den Helder

Bergen

Hammerfest

•

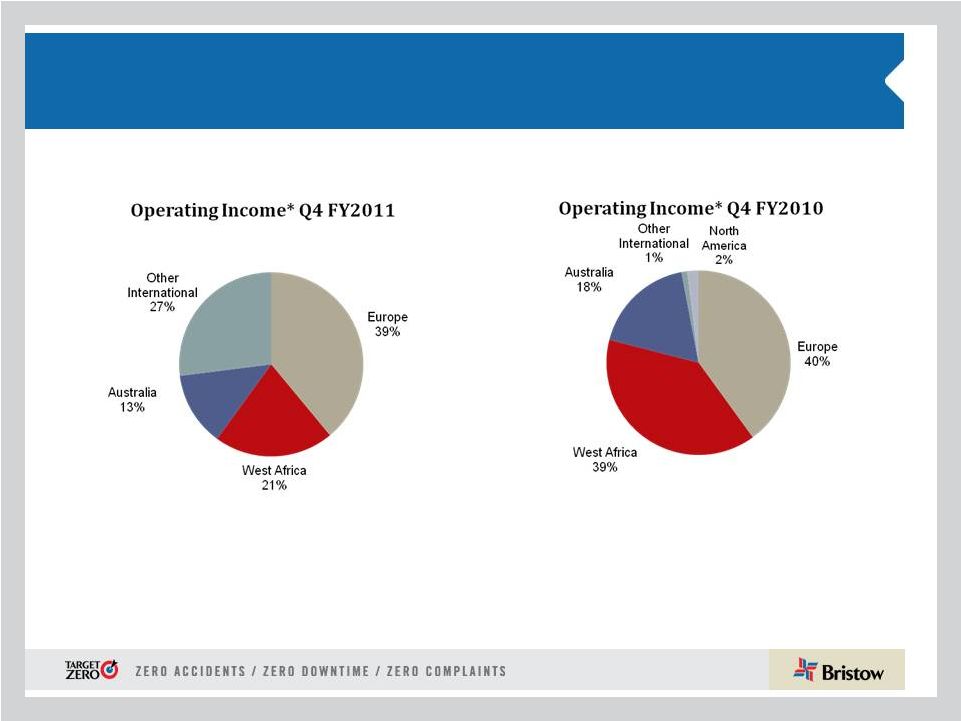

Europe represents 41% of total revenue in Q4

FY11 and 39% of operating income

•

Operating margin of 18.8% vs. 18.1% in prior

year quarter

•

Increase in activity with new client contracts

commencing generated more the $1mm in

revenues

•

Additional work in Humberside for additional

customers in Q4 2011 not in Q4 2010

•

Cost management also contributed to the higher

operating margin

Outlook:

•

Several major tenders outstanding in UK,

Norway and Denmark for FY12 & FY13;

tender awarded for Statoil Sola renewal

Operating margins expected for FY12 to

be ~ high teens

17

Esbjerg

Humberside

Kristiansund |

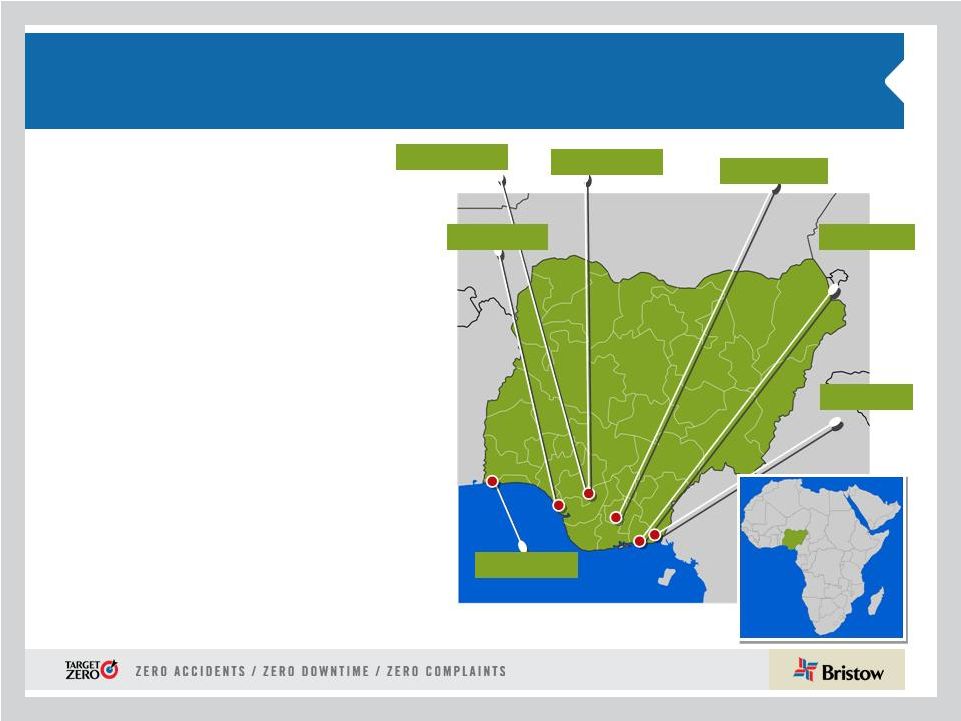

West Africa (WASBU)

Nigeria

Lagos

Escravos

Port Harcourt

Warri Osubi

Eket

Calabar

18

•

Nigeria represents 18% of total revenue in Q4 FY11

and 21% of operating income

•

Revenue of $55.2M increased slightly from

$54.2M

•

Increased operating expense in Q4 FY2011

associated with maintenance and freight

charges

•

Operating income decreased to $13.3M from

$18.8M

•

Operating margin of 24.0% vs. 34.6% in prior

year quarter

•

Increased competition and new entrants

Outlook:

•

Awaiting results of recent tenders

Operating margins expected in FY12 to be

back in the ~ mid twenties

Warri Texaco |

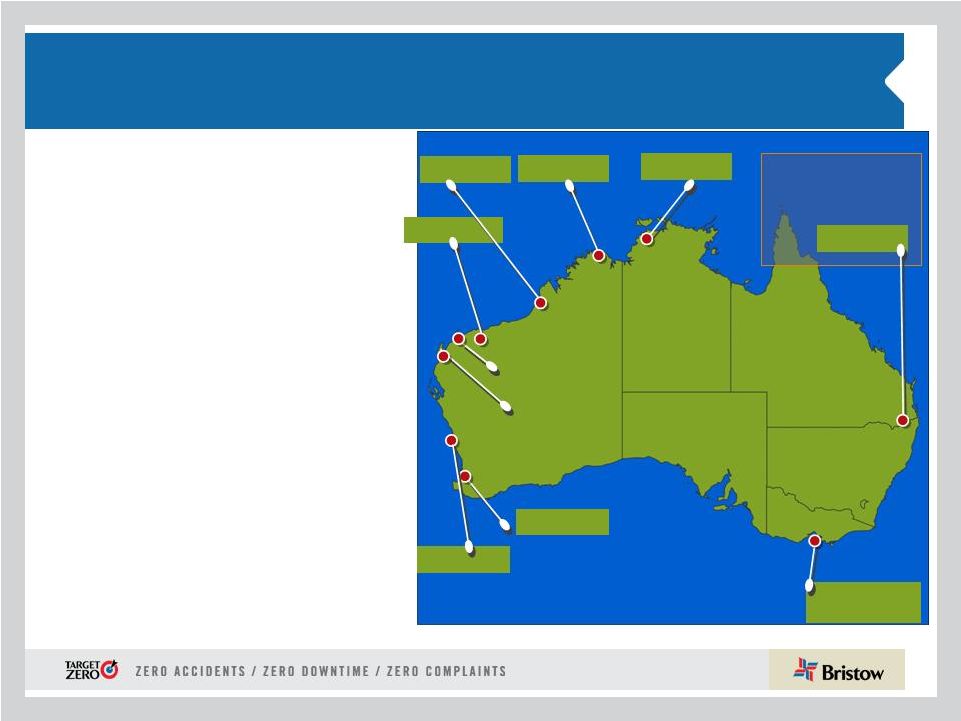

Karratha

Exmouth

Learmonth

Varanus Is

Barrow Is

Australia (AUSBU)

Australia

Perth

Dongara

Essendon

Tooradin

Broome

Truscott

Darwin

BDI provide support

to the Republic of

Singapore Air Force

Oakey

•

Australia represented 15% of total revenue in

Q4 FY11 and 13% of operating income

•

Revenue of $45M increased from $34M on

strong activity levels

•

Operating income declined to $7.8M from

$8.3M

•

Higher compensation costs and other

one time costs

•

Impairment loss shows up as increased

depreciation on three held for sale

aircraft, which were being used for

parts

•

Operating margin 17.4% vs. 24.5% for the

prior year quarter

Outlook:

•

Loss of Woodside as of May 31, 2011; we expect

to be replaced with other work

•

Higher activity levels to date due to increased gas

demand in Asia

Operating margins expected for FY12

to be ~ mid to upper teens

19 |

Other International (OIBU)

Consolidated in OIBU

Unconsolidated Affiliate

•

OIBU represented 12% of total revenue and 27% of

operating income for Q4 FY11

•

Revenue increased to $37.3 from $32.1M

•

Operating income to $17.1M from $0.6M

•

Operating margin was 45.8% vs 1.9% in the

prior year quarter

•

Increased revenue from the Baltic Sea, Suriname,

Ghana and Russia

•

Brazil –

Lider generated equity earnings of $6.2M

•

Reduced exposure in Mexico from transfer of

indemnity on performance bonds. Investment in

affiliate impaired for loss of $2.4M

•

PAS dividend in Egypt of $2.5 million in March 2011

Outlook:

•

Tender activity in Ghana and Equatorial Guinea

Expect operating margins in FY12 to be

~high teens to lower twenties

20 |

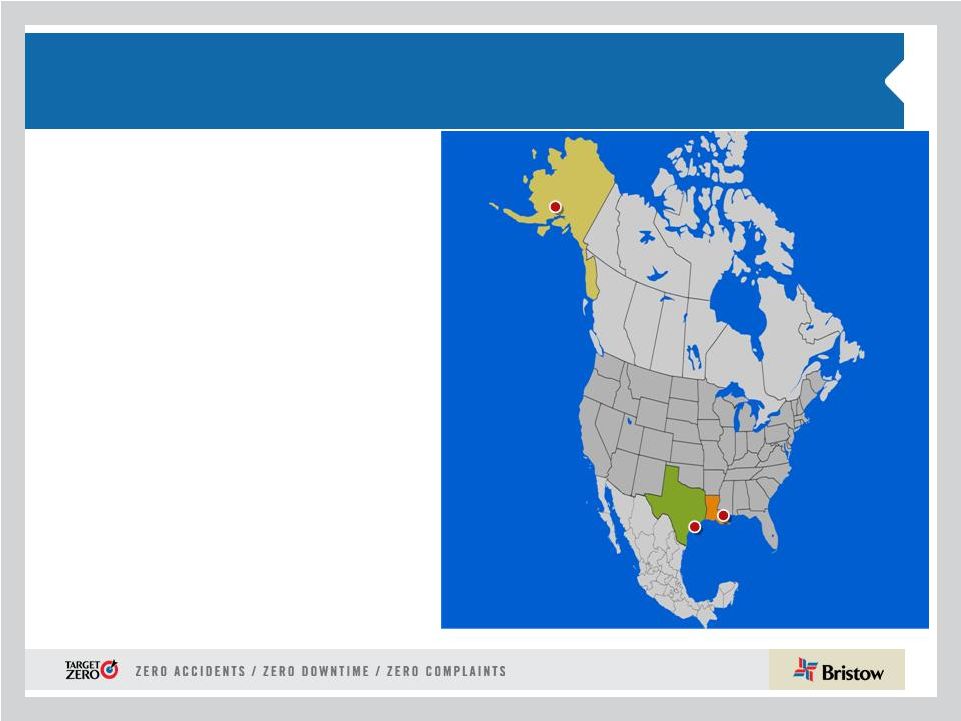

North America (NABU)

•

Revenue fell to $40.1M from $45.5M and

represented 13% of total revenue

•

Operating loss of $1.6M vs. operating income of

$1M

•

Operating margin of negative 4% declined from

2.2% in the prior year quarter

•

Gulf of Mexico outlook

•

BP work concluded in February 2011

•

Continues to be in a state of flux and

challenging market

•

We continue to redeploy aircraft to other

regions of the world

•

We are starting to see the signs of a

recovery

Expect operating margins for FY12 to

be single digits

21 |

Summary

22

Open for Q and A

•

Bristow had an excellent FY2011 with promises made and kept in safety,

operations and financial performance.

•

Strong cash flow generation has supported dividend initiation to

common

shareholders.

•

We see expansion for FY2012 and FY2013.

Our medium to long term

outlook remains strong given better market dynamics and our financial

strength.

•

Expect growth in earnings in fiscal 2012, with EPS expected in the range of

$3.55 to $3.90. |

Appendix

23 |

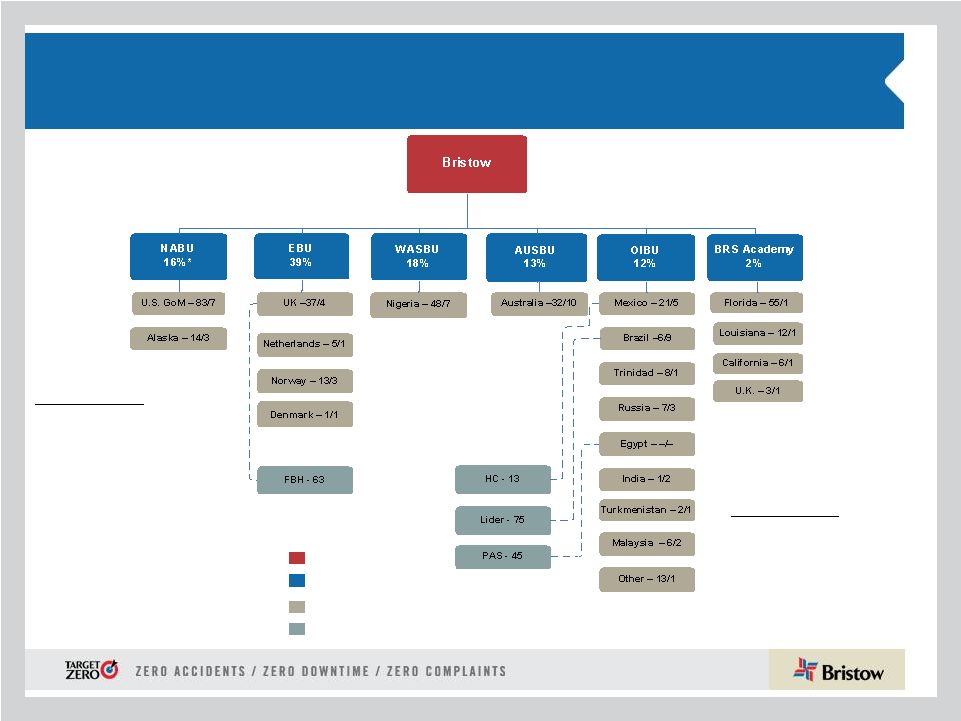

Organizational Chart -

as of March 31, 2011

Business

Unit

(*

%

of

FY11

Revenues)

Corporate

Region

(

#

of

Aircraft

/

#

of

Locations)

Joint

Venture

(No.

of

aircraft)

Key

Operated Aircraft

Bristow owns and/or operates

373 aircraft as of March 31, 2011

Affiliated Aircraft

Bristow affiliates and joint

ventures operate 196 aircraft

as of March 31,2011

24 |

Aircraft Fleet –

Medium and Large

As of March 31, 2011

Next Generation Aircraft

Medium capacity 12-16 passengers

Large capacity 18-25 passengers

25

Mature Aircraft Models

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Medium Helicopters

AW139

12

Twin Turbine

7

4

11

-

Bell 212

12

Twin Turbine

3

22

25

-

Bell 412

13

Twin Turbine

39

46

85

-

EC155

13

Twin Turbine

4

-

4

-

Sikorsky S-76 A/A++

12

Twin Turbine

20

8

28

-

Sikorsky S-76 C/C++

12

Twin Turbine

54

26

80

-

127

106

233

0

Large Helicopters

AS332L Super Puma

18

Twin Turbine

30

-

30

-

Bell 214ST

18

Twin Turbine

1

-

1

-

EC225

25

Twin Turbine

15

-

15

3

Mil MI 8

20

Twin Turbine

7

-

7

-

Sikorsky S-61

18

Twin Turbine

2

-

2

-

Sikorsky S-92

19

Twin Turbine

23

1

24

3

78

1

79

6 |

Aircraft Fleet –

Small, Training and Fixed

As of March 31, 2011 (continued)

Next Generation Aircraft

Mature Aircraft Models

Small capacity 4-7 passengers

Training capacity 2-6 passengers

26

Training Helicopters

AS355

4

Twin Turbine

3

-

3

-

Bell 206B

6

Single Engine

9

-

9

-

Robinson R22

2

Piston

11

-

11

-

Robinson R44

2

Piston

2

-

2

-

Sikorsky 300CB/Cbi

2

Piston

50

-

50

-

Fixed Wing

1

-

1

-

76

-

76

-

-

Fixed Wing

3

37

40

-

Total

373

196

569

6

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Small Helicopters

Bell 206B

4

Turbine

2

2

4

-

Bell 206 L-3

6

Turbine

4

6

10

-

Bell 206 L-4

6

Turbine

31

2

33

-

Bell 407

6

Turbine

42

1

43

-

BK 117

7

Twin Turbine

2

-

2

-

BO-105

4

Twin Turbine

2

-

2

-

EC135

7

Twin Turbine

6

3

9

-

AS350

4

Turbine

-

36

36

-

Agusta 109

8

Twin Turbine

-

2

2

-

89

52

141

- |

Consolidated Fleet Changes and Aircraft Sales for

FY 2011

27

(2) 1 additional aircraft sold on April 1, 2011. Cash deposit received

in FY 2011. Estimated gain of $1.3M to be recorded in Q1 2012.

Q 1 FY11

Q2 FY 11

Q 3 FY11

Q4 FY 11

Total

Fleet Count Beginning Period

390

384

379

378

390

Delivered

Agusta AW 139

1

1

2

4

Sikorsky S-76 C++

3

3

Sikorsky S-92

1

1

Total Delivered

1

1

3

3

8

Removed

Sales

(5)

(4)

-

(7)

(16)

Other*

(2)

(2)

(4)

(1)

(9)

Total Removed

(7)

(6)

(4)

(8)

(25)

384

379

378

373

373

* Includes net lease returns/commencements and operated returns

# of A/C

Sold

Cash

Received

(1)

Gain/

Loss

(1)

Q1 FY 11

5

3,770

1,585

Q2 FY 11

4

4,350

1,842

Q3 FY 11

-

-

-

Q4 FY 11

7

(2)

12,071

6,751

Totals

16

20,191

10,178

(1) Amounts stated in thousands |

Reconciliation of Special Items

Fourth Quarter FY2010 & Full Year FY2010

28

See notes to this table on page 29.

Fiscal Year Ended

March 31, 2010

Operating

Income

EBITDA

Net

Income

Diluted

Earnings

Per

Share

(Unaudited)

(In thousands, except per share amounts)

Adjusted for special items...............

$

181,540

$

259,586

$

109,114

$

3.02

Allowance for receivables

(10)

........

(1,100)

(1,100)

(715)

(0.02)

Depreciation correction

(8)

..............

3,250

—

2,898

0.08

Australia local tax

(9

)

......................

2,041

2,041

1,327

0.04

Departure of officers

(11)

.................

(4,874)

(4,874)

(3,168)

(0.09)

Hedging gains

(12)

..........................

—

3,936

2,558

0.07

As reported

.....................................

$

180,857

$

259,589

$

112,014

3.10

March 2010 Quarter

Operating

Income

EBITDA

Net

Income

Diluted

Earnings

Per

Share

(Unaudited)

(In thousands, except per share amounts)

Adjusted for special items...............

$

39,920

$

60,385

$

26,630

$

0.73

Allowance for receivables

(7)

.........

(2,200)

(2,200)

(1,430)

(0.04)

Depreciation correction

(8)

..............

3,872

—

2,463

0.07

Australia local tax

(9

)

......................

1,200

1,200

780

0.02

As reported.....................................

$

42,792

$

59,385

$

28,443

0.78 |

Reconciliation of Special Items

Notes

29

(1)

Represents additional depreciation expense recorded as a result of the impairment of previously

capitalized internal software costs as the related project was abandoned in the March 2011

quarter. (2)

Represents additional depreciation expense recorded as a result of the impairment of three held for

sale aircraft in the March 2011 quarter. (3)

Represents a charge recorded as a reduction in other income (expense), net related to the impairment

of our 24% investment in Heliservicio, an unconsolidated affiliate in Mexico, resulting from a

pending sale of the investment. (4)

Represents a reduction in maintenance expense (included in direct cost) associated with a credit

resulting from the renegotiation of a “power-by-the- hour” contract for

aircraft maintenance with a third party provider. (5)

Represents to impact from the early retirement of the 6 % Senior Notes,

which resulted in a $2.3 million early redemption premium (included in other income (expense),

net) and the non-cash write-off of $2.4 million of unamortized debt issuance costs (included in interest expense).

(6)

Represents the impact of a reduction in the provision for income taxes related to adjustments to

deferred tax liabilities that were no longer required as a result of a restructuring during

the fiscal year ended March 31, 2011. (7)

Represents a $3.6 million bad debt allowance recorded for accounts receivable due from our

unconsolidated affiliate in Mexico, which we determined were not probable of collection, which

was partially offset by a $1.4 million reduction in a bad debt allowance for accounts receivable due from a client

in Nigeria; these items are included in direct cost.

(8)

Represents a reduction in depreciation expense recorded in the March 2010 quarter for errors in the

calculation of depreciation on certain aircraft in prior periods.

(9)

Represents a net expense reduction in Australia upon resolution of local tax matters in the March

2010 quarter that reduced direct costs and in fiscal year ended March 31, 2010 that reduced

direct cost by $1.1 million and general and administrative expense by $0.9 million. (10)

Represents a $3.6 million bad debt allowance recorded for accounts receivable due from our

unconsolidated affiliate in Mexico, which we determined were not probable of collection, which

was partially offset by a $2.5 million reduction in a bad debt allowance for accounts receivable due from a client

in Kazakhstan; these items are included in direct cost.

(11)

Represents compensation costs associated with the departure of three of the Company’s officers

during the fiscal year ended March 31, 2010; these costs are included in general and

administrative costs. (12)

Represents the impact of pre-tax hedging gains of $3.9 million realized during the fiscal year

ended March 31, 2010 due to termination of forward contracts on euro-denominated aircraft

purchase commitments; these gains are included in other income (expense), net.

1/8 |

EBITDA and EBITDAR Reconciliations

30

($ in millions)

2000

2001

2002

2003

2004

Income from continuing operations

$8.8

$27.9

$42.5

$40.3

$49.6

Income tax expense

3.8

13.3

19.1

17.5

18.5

Interest expense

18.5

18.4

15.8

14.9

16.8

Depreciation and amortization

32.0

33.1

33.9

37.5

39.4

EBITDA Subtotal

63.1

92.7

111.4

110.2

124.3

Aircraft rental expense

–

–

–

–

–

EBITDAR

$63.1

$92.7

$111.4

$110.2

$124.3

($ in millions)

2005

2006

2007

2008

2009

Income from continuing operations

$49.2

$54.5

$72.5

$107.7

$125.5

Income tax expense

$20.4

$14.7

$38.8

$44.5

$50.5

Interest expense

$15.7

$14.7

$10.9

$23.8

$35.1

Depreciation and amortization

40.5

42.1

42.5

54.1

65.5

EBITDA Subtotal

125.8

125.9

164.7

230.1

276.7

Aircraft rental expense

–

2.1

6.3

6.3

8.2

EBITDAR

$125.8

$128.0

$171.0

$236.4

$284.9

($ in millions)

2010

2011

Income from continuing operations

$113.5

$133.3

Income tax expense

$29.0

$7.1

Interest expense

$42.4

$46.2

Depreciation and amortization

74.7

90.9

EBITDA Subtotal

259.6

277.5

Aircraft rental expense

9.1

5.9

EBITDAR

$268.7

$283.4

March 31,

March 31,

March 31, |

ROCE Reconciliation

31

31-Mar-06

30-Jun-06

30-Sep-06

31-Dec-06

31-Mar-07

Numerator:

Total assets

1,176.4

$

1,239.8

$

1,469.1

$

1,517.8

$

1,505.8

$

EBITDA

163.5

(-) Assets discountinued operations

(27.4)

(28.4)

(23.8)

(26.0)

(26.2)

Minority Interest

1.2

(-) Cash

(122.5)

(109.6)

(268.3)

(219.7)

(184.2)

164.7

(-) Progress payments for aircraft and other

(83.5)

(89.5)

(131.1)

(145.9)

(167.8)

(-) Current liabilities

(163.9)

(180.8)

(194.5)

(173.1)

(168.0)

(+) Current liabilities discontinued operations

5.5

4.7

3.3

3.0

5.9

(+) Short term deferred tax

5.0

6.6

10.0

10.9

17.6

(+) Estimated fair value of aircraft

665.3

750.1

772.3

846.6

946.5

(+) Net book value of property & equipment (non-aircraft)

126.0

134.5

178.8

201.4

223.3

Denominator:

(-) Net book value property & equipment (aircraft and

non-aircraft) (615.5)

(664.4)

(730.4)

(824.9)

(891.5)

Average Capital Employed

1,113.1

$

Capital employed

965.3

$

1,062.8

$

1,085.7

$

1,190.1

$

1,261.5

$

Return on capital employed:

15%

31-Mar-07

30-Jun-07

30-Sep-07

31-Dec-07

31-Mar-08

Numerator:

Total assets

1,505.8

$

1,844.4

$

1,899.2

$

1,960.4

$

1,977.4

$

EBITDA

230.3

(-) Assets discountinued operations

(26.2)

(23.9)

(25.3)

-

-

Minority Interest

(0.1)

(-) Cash

(184.2)

(339.5)

(276.4)

(315.3)

(290.1)

230.2

(-) Progress payments for aircraft and other

(167.8)

(189.4)

(206.8)

(247.9)

(182.9)

(-) Current liabilities

(168.0)

(173.0)

(183.7)

(170.8)

(165.0)

(+) Current liabilities discontinued operations

5.9

2.8

3.7

-

-

(+) Short term deferred tax

17.6

18.0

18.5

11.4

9.2

(+) Estimated fair value of aircraft

946.5

1,022.9

1,054.0

1,146.6

1,177.3

(+) Net book value of property & equipment (non-aircraft)

223.3

244.9

264.6

314.8

249.1

Denominator:

(-) Net book value property & equipment (aircraft and

non-aircraft) (891.5)

(1,017.1)

(1,099.5)

(1,150.2)

(1,172.5)

Average Capital Employed

1,450.3

$

Capital employed

1,261.5

$

1,390.1

$

1,448.3

$

1,549.0

$

1,602.6

$

Return on capital employed:

16%

Fiscal Year 2007

Fiscal Year 2008

Minority interest is added to EBITDA since the capital employed includes the full fair value of

aircraft operated by consolidated subsidiaries. Average capital employed represents the average

of the prior fiscal year end balance and quarter-end balances. Fair market value of aircraft is adjusted at the beginning of each fiscal year using our experience

buying and selling aircraft and a third-party valuation service. Also adjustments are made quarterly to reflect aircraft entering and exiting the fleet.

Excludes leased aircraft and aircraft operated for others. |

ROCE Reconciliation

32

31-Mar-08

30-Jun-08

30-Sep-08

31-Dec-08

31-Mar-09

Numerator:

Total assets

1,977.4

$

2,354.5

$

2,306.3

$

2,342.9

$

2,334.6

$

EBITDA

276.7

(-) Cash

(290.1)

(527.4)

(399.1)

(364.7)

(301.0)

(-) Progress payments for aircraft and other

(182.9)

(229.6)

(296.2)

(322.0)

(230.1)

(-) Current liabilities

(165.0)

(162.9)

(159.5)

(184.7)

(154.8)

(+) Short term deferred tax

9.2

12.3

11.6

7.2

6.2

(

+

) Estimated fair value of aircraft

1,177.3

1,361.9

1,420.2

1,601.2

1,612.5

(

+

) Net book value of property & equipment (non-aircraft)

249.1

297.5

360.1

392.3

309.9

Denominator:

(-) Net book value property & equipment (aircraft and

non-aircraft) (1,172.5)

(1,319.1)

(1,404.5)

(1,505.1)

(1,541.5)

Average Capital Employed

1,846.3

$

Capital employed

1,602.6

$

1,787.2

$

1,838.9

$

1,967.2

$

2,035.7

$

Return on capital employed:

15%

31-Mar-09

30-Jun-09

30-Sep-09

31-Dec-09

31-Mar-10

Numerator:

Total assets

2,334.6

$

2,458.1

$

2,476.4

$

2,533.6

$

2,494.6

$

EBITDA

259.6

(-) Cash

(301.0)

(138.3)

(143.2)

(107.1)

(77.8)

(-) Progress payments for aircraft and other

(230.1)

(191.6)

(107.5)

(127.0)

(152.8)

(-) Current liabilities

(154.8)

(197.4)

(165.9)

(187.5)

(166.1)

(+) Short term deferred tax

6.2

11.0

10.5

9.3

10.2

(+) Estimated fair value of aircraft

1,612.5

1,677.3

1,741.0

1,832.1

1,865.1

(+) Net book value of property & equipment (non-aircraft)

309.9

283.8

207.0

220.3

248.9

Denominator:

(-) Net book value property & equipment (aircraft and

non-aircraft) (1,541.5)

(1,573.7)

(1,600.4)

(1,706.9)

(1,719.3)

Average Capital Employed

2,350.5

$

Capital employed

2,035.7

$

2,329.2

$

2,417.9

$

2,466.8

$

2,502.7

$

Return on capital employed:

11%

Fiscal Year 2009

Fiscal Year 2010

Minority interest is added to EBITDA since the capital employed includes the full fair value of

aircraft operated by consolidated subsidiaries. Average capital employed represents the average

of the prior fiscal year end balance and quarter-end balances. Fair market value of

aircraft is adjusted at the beginning of each fiscal year using our experience buying and selling aircraft and a third-party valuation

service. Also adjustments are made quarterly to reflect aircraft entering and exiting the fleet.

Excludes leased aircraft and aircraft operated for others. |

ROCE Reconciliation

33

31-Mar-10

30-Jun-10

30-Sep-10

31-Dec-10

31-Mar-11

Numerator:

Total assets

2,494.6

$

2,504.7

$

2,606.9

$

2,638.7

$

2,662.6

$

EBITDA

277.5

(-) Cash

(77.8)

(73.9)

(108.5)

(100.9)

(116.4)

(-) Progress payments for aircraft and other

(152.8)

(161.2)

(168.6)

(121.4)

(112.4)

(-) Current liabilities

(166.1)

(161.1)

(168.6)

(163.6)

(167.3)

Short term deferred tax

10.2

10.1

10.7

13.3

12.2

Estimated fair value of aircraft

1,865.1

1,779.7

1,809.6

1,829.9

1,845.1

Net book value of property & equipment (non-aircraft)

248.9

258.5

268.6

221.6

216.6

Denominator:

(-) Net book value property & equipment (aircraft and

non-aircraft) (1,719.3)

(1,711.6)

(1,753.6)

(1,787.5)

(1,767.9)

Average Capital Employed

2,509.4

$

Capital employed

2,502.7

$

2,445.2

$

2,496.5

$

2,530.2

$

2,572.5

$

Return on capital employed:

11.1%

Fiscal Year 2011

Minority interest is added to EBITDA since the capital employed includes the full fair value of

aircraft operated by consolidated subsidiaries. Average capital employed represents the average of the prior fiscal year end balance and

quarter-end balances. Fair market value of aircraft is adjusted at the beginning of each fiscal year using our experience

buying and selling aircraft and a third-party valuation service. Also adjustments are made

quarterly to reflect aircraft entering and exiting the fleet. Excludes leased aircraft and aircraft operated for others.

(+)

(+)

(+) |

Leverage Reconciliation

34

Debt

Investment

Capital

Leverage

(a)

(b)

(c) = (a) + (b)

(a) / (c)

As of March 31, 2011

707.5

$

1,518.8

$

2,226.3

$

31.8%

Adjust for:

Unfunded Pension Liability

99.6

99.6

NPV of GE and Norsk Lease Obligations

40.5

40.5

Adjusted

847.6

$

(d)

1,518.8

$

2,366.4

$

35.8%

Calculation of debt to EBITDAR multiple

EBITDAR:

FY 2011

283.4

$

(e)

Annualized

377.9

$

= (d) / (e)

2.99:1 |

Bristow Group Inc. (NYSE: BRS)

2000 West Sam Houston Parkway South

Suite 1700, Houston, Texas 77042

t

713.267.7600

f

713.267.7620

bristowgroup.com

Contact Us

35 |