Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE RE EARNINGS 5-5-11 - AutoWeb, Inc. | ex99_1.htm |

| 8-K - 8-K RE EARNINGS RELEASE ON 5-5-11 - AutoWeb, Inc. | form8k_05062011.htm |

Exhibit 99.2

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 1

AUTOBYTEL INC.

Moderator: Roger Pondel

May 5, 2011

5:00 p.m. ET

|

Operator:

|

Good day, ladies and gentlemen, and welcome to Autobytel’s 2011 first quarter earnings conference call.

|

At this time, all participants are in a listen-only mode. Later, we’ll have a question-and-answer session, and instructions will follow at that time. If anyone should require assistance during the conference, please press star, then zero on your touch tone telephone. As a reminder, today’s conference is being recorded.

I would now like to turn the conference over to your host for today, Mr. Roger Pondel, investor relations for Autobytel. Sir, you may begin.

|

Roger Pondel:

|

Thank you, Mary. Hello everyone, and welcome to Autobytel’s 2011 first quarter conference call. With us on the line today are Jeffrey Coats, President and Chief Executive Officer, and Curt DeWalt, Senior Vice President and Chief Financial Officer. Before we begin, I’d like to remind you that during today’s call, including the Q&A session, any projections and forward-looking statements made regarding future events and Autobytel’s future financial performance are covered by the safe harbor statements contained in today’s press release and in the company’s public filings with the SEC. Actual events and results may differ materially from those forward-looking statements.

|

Specifically, please refer to the company’s Form 10-K for the year ended 2010, the company’s Form 10-Q for the quarter ended March 31, 2011, which is expected to be filed shortly, and other filings with the SEC. These filings identify the principal factors that could cause results to differ materially from those forward-looking statements.

Now, slides are included with today’s presentation to help illustrate some of the points being made and discussed during the call. You can access the slides by clicking on the link in today’s press release or by going to Autobytel’s Web site at www.autobytel.com. When you’re there, go to “Investor Relations” and then click “Events and Presentations.”

Also, please note that during this call we will be discussing adjusted operating expenses, EBITDA and cash flow, which are non-GAAP financial measures as defined by SEC Regulation G. Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP financial measure will be included in the slides that are posted on the Autobytel Web site.

With that, I would like to turn the call over to Jeff.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 2

|

Jeffrey Coats:

|

Thank you, Roger. Good afternoon, and thank you for joining us today.

|

We continue to make progress toward our business goals. Of particular note, as you can see on slides 3 and 4, we achieved positive cash flow for the first quarter boosted by the strategic acquisition of Cyber Ventures and Autotropolis. This is in addition to the actions we have taken over the past two years to rebuild our internal purchase request generation capabilities, while also significantly reducing costs and restructuring our operations.

The acquisition – for Autobytel and for our shareholders – could not have come at a better time, with industry analysts predicting steady momentum for most manufacturers in the years ahead.

Unfortunately, in the more immediate term, Japanese automakers are suffering from production problems related to the March 11th earthquake and tsunami. As you can see on slide 5, industry sentiment is rapidly evolving, making it difficult to fully assess what the industry impact will be this year and possibly next.

To provide a sense for how quickly things are moving, on April 19th at the NADA/IHS Automotive Forum held in conjunction with the New York International Auto Show, Toyota said they were at that time still holding to their original 2011 sales forecast, yet a few days later reported that they do not expect to return to normal production until at least November of this year.

Honda issued similar guidance, while other industry forecasters decreased their original 2011 U.S. SAAR estimates, including AutoNation, which just last week reduced its industry projections from 12.8 million to the mid-12 million range. At Autobytel, we believe there will be some month-to-month disruption in U.S. automotive sales during the remainder of 2011 and potentially a reduction in projected total vehicle sales for the year.

While the Japanese automakers are bearing the brunt of the industry’s current challenges, consensus seems to be building that the Detroit Three will likely gain market share as a result, with broad product lines that include many well-made, fuel-efficient models. Based on what we know directly from our customers and from our own research, it is plausible that consumers may switch to domestic brands rather than delaying vehicle purchases outright, as pent-up demand needs to be met. Although we have not yet seen a direct benefit related to this scenario, it is possible that we will see some upside from it during the course of this year. However, it is too soon to tell how significant the impact might be and in which quarters.

Despite some near-term uncertainty and some recent spending cutbacks by a few of our Japanese automotive customers in the past 10 days, we remain confident that Autobytel will remain cash flow positive for the second quarter. At the same time, since we are still evaluating the impacts of events in Japan, we now have less visibility with respect to achieving net income profitability in the second quarter. However, I want to stress that we do expect continued improvement in our second quarter results, both in our gross margin and bottom line, and I want to reiterate that we expect to remain cash flow positive in the second quarter.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 3

There is considerable positive change happening at Autobytel and a sense of renewed excitement and energy throughout the company. I will share an update with you momentarily, but first Curt will review our financial performance. Curt?

|

Curt DeWalt:

|

Thank you, Jeff.

|

First, a reminder that the slides we’ll be referring to on today’s call can be found on the Autobytel Web site under “Investor Relations” and then “Events and Presentations.”

As you can see on slide 3, total revenue for the 2011 first quarter rose 36% to $16.0 million from $11.8 million in last year’s first quarter, marking the fourth consecutive quarter of sequential revenue growth. Total revenue grew 9% over the preceding fourth quarter.

The year-over-year increases primarily related to contributions from the acquisition, as well as continued recovery in the automotive sectors that was still present through Q1 2011. While we are continuing to see increased demand from certain OEMs and especially large dealer groups, as well as from third party online automotive lead distributors, we can all appreciate that the situation in Japan has temporarily dampened original growth plans for some auto manufacturers, and as Jeff said earlier, the impact to the industry and to Autobytel is not yet completely known.

On slide 6 you can see our quarterly revenue broken out by source.

For 2011 first quarter, total automotive purchase request revenue grew 42% over last year’s first quarter, paced by a 130% increase in OEM and other wholesale purchase request channels, compared with last year’s first quarter, largely due to the Cyber Ventures acquisition. On a sequential basis, auto purchase request revenue rose 9%, with a 6% increase in OEM and other wholesale purchase request revenue compared with the 2010 fourth quarter.

As consumer credit is becoming more available, we are continuing to see an increase in finance request revenue, which grew 20% in the most recent quarter to $1.8 million from $1.5 million in last year’s first quarter and $1.6 million in the preceding fourth quarter. We delivered approximately 112,000 finance requests in Q1, compared with 98,000 in the 2010 first quarter, and 105,000 in the fourth quarter of last year.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 4

After several quarters of inconsistent ad revenue performance, we are pleased that advertising revenue grew on a sequential basis to more than $1 million from $856,000 in Q4, reflecting the benefit of additional page views to our Web sites. Advertising revenue amounted to $1.1 million a year ago. We are working toward fully monetizing our advertising opportunity, and while this will not happen overnight, we believe we can make steady forward progress as the industry continues to recover and as Autobytel improves page view quality and quantity.

We delivered approximately 995,000 purchase requests in the first quarter of 2011, up 59% from last year’s first quarter, and up 9% sequentially from last year’s fourth quarter, primarily reflecting the increased delivery of purchase requests into the OEM and other wholesale channels.

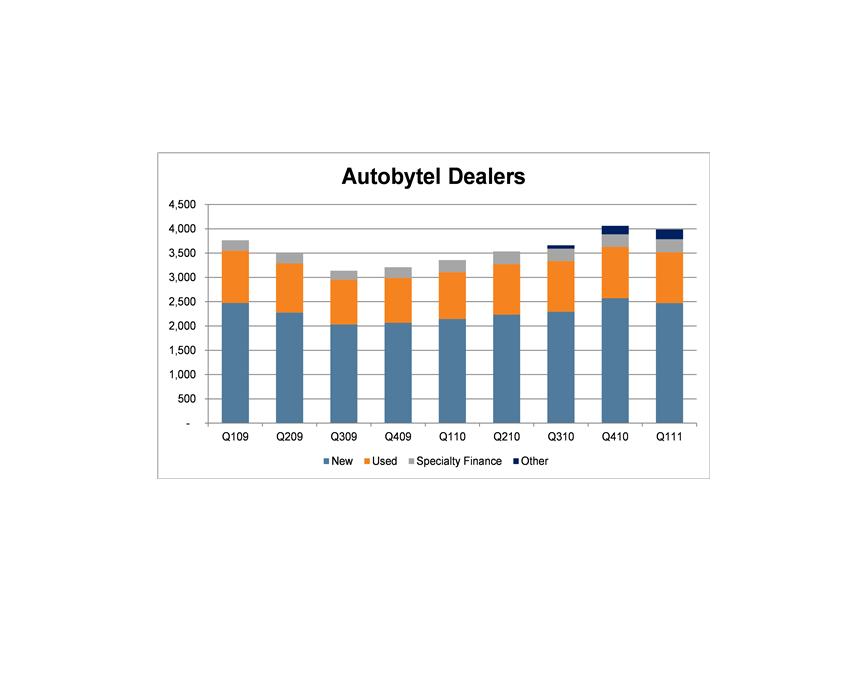

As seen on slide 7, our dealer network comprised approximately 3,700 new, used and other car dealers, up 20% from last year’s first quarter, but down 2% on a sequential basis. The reduction relates primarily to attrition during the acquisition integration process and a focus on dealers in areas where we have significant purchase request availability. There were 270 finance dealers in our network at the end of the 2011 first quarter, up approximately 8% from last year’s first quarter and up 5% on a sequential basis.

Gross profit was up 30% for the 2011 first quarter on a year-over-year basis, although as a percentage of revenue, gross margin was down slightly to 38.4% from 40.2% last year and 39.3% for the 2010 fourth quarter. The year-over-year and sequential decline in gross margin is principally due to a shift in revenue mix which provided increased gross profit dollars at a lower margin. Both gross profit and gross margin rose in the latter half of the 2011 first quarter as a result of optimization initiatives related to search engine marketing, which we expect to be reflected in future periods. With approximately 70% of all of our purchase requests now coming directly from Autobytel’s network of Web sites versus 31% a year ago, there remains significant opportunity for margin enhancement going forward.

We believe operating expenses are now more appropriately aligned with revenue and business conditions. Slide 8 shows our cost structure on an adjusted basis. Total operating expenses for the 2011 first quarter were reduced by more than 27% to $6.6 million from $9.0 million in the preceding quarter, which included costs related to a workforce reduction and expenses associated with the Cyber Ventures acquisition. I would note that the $6.6 million in total operating expenses in the 2011 first quarter included approximately $600,000 of acquired operating expenses. A year ago, adjusted operating expenses were $6.9 million, excluding a $2.8 million credit related to patent litigation settlements.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 5

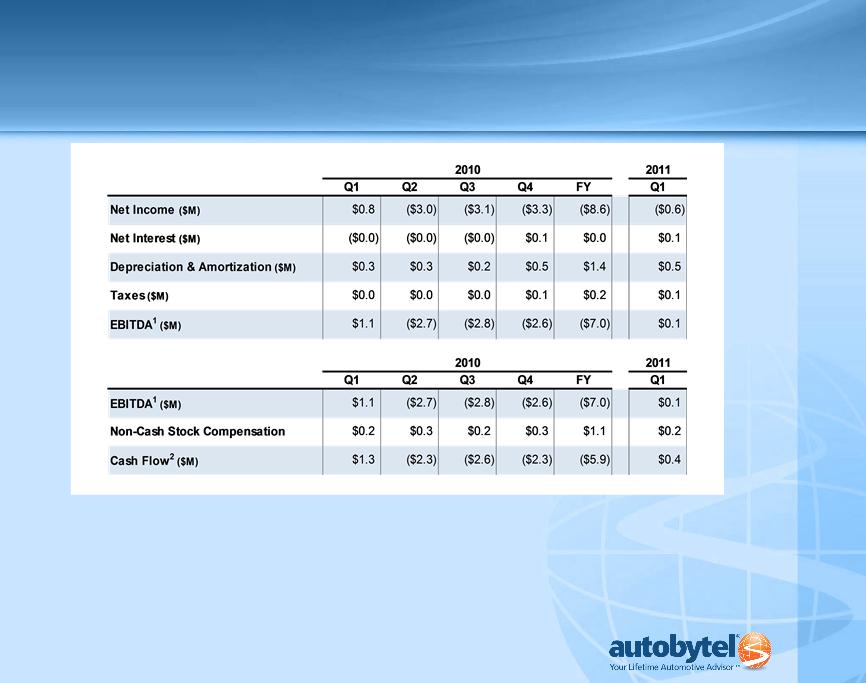

As you'll see on slide 4, non-cash share based compensation for the first quarter of 2011 was $227,000 compared with $242,000 for the first quarter of 2010. Depreciation and amortization was $510,000 for the most recent first quarter versus $322,000 in the first quarter a year ago. The increase in depreciation and amortization is the result of amortization of intangible assets associated with the acquisition.

This brings EBITDA to approximately $144,000 for the first quarter of 2011, compared with an EBITDA loss of $2.6 million in the fourth quarter of 2010 and positive EBITDA of $1.1 million in the first quarter of 2010.

As Jeff mentioned, we were non-GAAP cash flow positive by approximately $371,000 in 2011 first quarter for the first time in four years, excluding patent litigation settlements and escrow settlements.

Net loss for 2011 first quarter was reduced to $571,000, or $0.01 per share, over the preceding fourth quarter net loss of $3.3 million, or $0.07 per share. The company had net income of $797,000, or $0.02 per diluted share, for the first quarter of 2010. However, without the $2.8 million credit related to the patent litigation settlements, the net loss for last year’s first quarter would have been $2.0 million, or $0.04 per share.

At the end of the quarter, the company had cash and cash equivalents of $7.5 million, compared with $8.8 million at December 31, 2010, primarily due to changes in working capital. We also carry a $5 million convertible note from the acquisition, which pays simple interest at a rate of 6% per year.

With that, I’ll turn the call back to Jeff.

|

Jeffrey Coats:

|

Thanks, Curt.

|

It is gratifying that the hard work, tough decisions and strategic course we’ve embarked upon are converging in our favor as many players in the automotive sector, including Autobytel, continue to see positive recovery.

The most recent J.D. Power survey, as shown on slide 9, has auto sales growing approximately 12% this year to 13 million units, with additional growth of 15% for 2012. April light vehicle sales were up 18% year-over-year on the heels of strong retail volume, new models and fuel-efficient vehicles. J.D. Power’s head of global forecasting recently commented to Automotive News that, “retail sales continued to perform well in the second half of April despite growing inventory concerns and that increasing gas prices and shortages in vehicle inventory have yet to trump the overall recovery that has been progressing since the fall of 2010.” He went on to say, however, that, “looking at the remainder of the year, growing uncertainty about gas prices and inventories is increasing the risk that the industry may not reach the expected 13 million unit level for U.S. light vehicle sales.”

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 6

The automotive sector is highlighted in the news daily. Gasoline prices, of course, are a major part of those headlines. Although it appears that elevated gas prices have not yet hurt U.S. auto sales, the gas mileage of cars sold seems already to be shifting the mix of vehicles sold. Anecdotally, those in need of a new car who drive already a fuel-efficient car will undoubtedly purchase another fuel-efficient vehicle, and as you know, consumers now have many more fuel-efficient vehicles to consider, especially from the Detroit Three automakers. But those that drive lower gas mileage vehicles and are feeling the pinch at the pump might consider shifting segments, for example, trading down from a large SUV to a more fuel-efficient crossover.

While we expect continued market uncertainty over the near term, one thing remains clear to us – third party purchase requests continue to be a highly effective tool for OEMs and dealers. A study just published in April that looked at the closing rates for millions of purchase requests validated what we have known all along – that purchase requests from third party providers, such as Autobytel, deliver higher performance and a greater number of qualified buyers to help dealers sell more cars. The data revealed that closing ratios for third party leads in the five years from 2005 to 2010 improved 35% faster than overall dealership closing ratios over the same time period. Lastly, and quite interesting to note, the study also revealed that while social media can benefit offline branding for a dealership, it has little impact on a dealership’s online sales success, unlike third party leads, which if properly managed by dealers, drive both new and used vehicle sales. There have also been similar conclusions recently reported in the industry press.

Certainly we are pleased by the study’s reinforcement of the value we bring to the marketplace, which provides evidence of the advantageous competitive position our acquisition of Cyber Ventures has reinforced. And, while Curt and I have both spoken about the acquisition, I want to reiterate a few salient points to demonstrate how this transaction has been a real game changer for us and its effect on further consolidation within our market.

Perhaps most important, as noted on slide 10, is that we are self-generating approximately 70% of our new car purchase requests through Autobytel’s network of Web sites, and while we are proud of our direct-from-site volume position in the market, it is the increase in quality that comes with self-generated purchase requests that we now deliver to the industry that we believe uniquely positions Autobytel in the field. Specifically, our self-generated purchase requests drive significant enhancements of our product, namely the ability of purchase requests to convert into consumer sales. This, in turn, stimulates increased demand for our purchase requests from auto manufacturers, other wholesale channel partners, and of course, dealers.

Today, while more of our purchase requests are being delivered to OEMs and other third parties in the automotive leads distribution industry, we are actively embarking on programs to further enhance dealer sales. We are offering dealers highly innovative programs that are customized to their individual businesses and markets that we believe should also add new revenue streams and improved margins for Autobytel. We strongly believe that consumers are coming back to the automotive market in new ways in the face of a changing environment, so we are providing dealers with the tools they need to effectively reach those consumers.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 7

Among our newest dealer-oriented programs, which I mentioned on our last call, is Web Leads+™, which helps increase purchase request volume through dealers’ Web sites by presenting potential in-market buyers with special offers, coupons or incentives at the time they are actively searching for cars. Web Leads+™ is now being used by approximately 10% of our new and used dealer customers. This program was launched in the third quarter of last year, and many dealers are reporting to us that purchase request volume from their own Web sites has grown by more than 50%.

As we have previously discussed, we have also developed an offering that allows dealers to better match the marketing spend to their actual inventory. This product, iControl by Autobytel™, after being introduced in the second quarter of 2010, is now being used by approximately 40% of our new car dealers, up from approximately one-third reported on our last conference call. We believe it is the only offering of its kind that gives dealers the flexibility to custom configure their mix of online consumer purchase requests to reflect real-time inventory and other local market activity. This is particularly gratifying given our original vision for iControl, which was to address market fluctuations exactly like those we have all been witnessing in recent weeks.

During the first quarter of 2011, we launched the auto industry's newest jobs Web site, DealershipJobs.com, with the goal of becoming the premier job site for auto dealers. DealershipJobs is the first comprehensive, industry specific job portal, helping dealers attract high quality employees. Today, there are nearly 6,200 automotive jobs posted on the site, up from 5,000 just six weeks ago, covering a very diverse range of positions, from management and finance to sales and service. The site, which is free to dealers and job hunters, will over time add more functionality, such as job seeker advice, including resume tips and interviewing strategies. As it scales up, we anticipate generating advertising and other revenues from the site.

There is no question that the Internet today is a vibrant tool for consumers when purchasing cars. Taken from a recent J.D. Power study, slide 11 demonstrates the power of third party sites like Autobytel. As you will see, nearly 80% of automotive shoppers who use the Internet rely upon third party sites, like Autobytel, in the six months before they purchase a vehicle. That’s an impressive statistic given only 68% visit OEM sites and just 43% seek out dealer sites. With approximately 13 million monthly page views across Autobytel’s network of Web sites and click-through rates reaching new highs, we are working diligently on attracting and monetizing a broader base of users which, in turn, will produce greater numbers of purchase requests. Regardless of where consumers are in their automotive ownership life cycle, however, from purchase to maintenance to resale, we believe opportunities abound to serve consumers even more and at the same time add potential new revenue streams for the company.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 8

Toward that objective, we are at the finishing stages for a June launch of a major upgrade of our flagship site, autobytel.com. The site, a preview of which you can see on slide 12, reflects our new “Your Lifetime Automotive Adviser” focus and will offer many new features that we believe are key to attracting more users on a continuing basis during the full automotive lifecycle, rather than only every three to seven years when they are actively in the market to purchase or lease their next vehicle. Through this strategy we are creating attractive, new monetization opportunities, such as with parts and accessories, service and insurance.

I have mentioned the My Garage® feature as one example which gives consumers access to personalized advice and discounts on a wide variety of car ownership subjects, from insurance and financing to parts and accessories, service and maintenance, recalls and more. My Garage®, which aggregates a consumer’s ownership information in one place, will be fully integrated on our new site. I encourage each of you to visit the site, once re-launched, and make use of its benefits.

Our recent hire of Michelle Naranjo as managing editor of autobytel.com is also strengthening our voice with consumers through exclusive articles, videos and automotive reviews to make the site more robust and beneficial. Michelle has established herself as a clear voice in the automotive industry under the pen name Miss Motormouth, where she covered numerous aspects of the automotive industry, including consumer interests, OEM activity, dealer issues and automotive service providers. She is a weekly panelist on The RoundAbout Show, a popular podcast; is host of MingleMediaTV.com’s weekly automotive web show; and founder and host of the Open Line Show for AutolineDetroit.TV. Michelle, who spent time at eBay Motors, will continue to host these shows as managing editor of autobytel.com, thus further raising our brand visibility across both industry and consumer audiences.

Moving from content to data, we believe there is a high margin opportunity for us to capitalize on the data that we already own to help advertising agencies, OEMs and dealers analyze, select and measure their digital marketing efforts. Many entities in the automotive sector utilize statistics and various market data from a wide range of sources for both insights and the direct targeting of media. We have entered that market through recent agreements with Datran Media and eXelate. These arrangements combine our real-time auto intender data to produce analytics and identify targeted media that we anticipate will provide value for advertisers, media trading desks, OEMs and other entities seeking these services.

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 9

We believe Autobytel is well-positioned to participate in the recovery in the automotive market in a meaningful way, notwithstanding the current situation in Japan. The market remains ripe for ongoing consolidation, and as we’ve demonstrated, Autobytel can be a major beneficiary of this consolidation.

Our business has been reinvigorated. We are positioned to meaningfully enhance our margins, and we are focused on developing new revenue streams in an expanding market arena.

Many of you on today’s call have been stalwart supporters for a long time. I thank you for your patience and confidence during a period of rebuilding. While there is more work to do, I believe we are beginning to hit our stride as we look forward to seeing and sharing the benefits of our hard work in the coming quarters and years.

Mary, we will now take questions.

|

Operator:

|

Certainly. Ladies and gentlemen, if you have a question at this time, please press star, then one on your touch-tone telephone. If your question has been answered or you wish to remove yourself from the queue, please press the pound key. Once again, if you have a question, please press star, then one.

|

Our first question comes from the line of Steve Dyer from Craig-Hallum. Your line is open.

|

Steve Dyer:

|

Good afternoon guys, and congratulations on the long slog to profitability here.

|

|

Jeffrey Coats:

|

Thank you.

|

|

Steve Dyer:

|

A couple quick questions. So you kind of mentioned the potential lull in sales just due to some disruptions relating to Japan over the next quarter or two. You kind of mentioned – which I agree with – that the Big Three domestically will benefit. The other guys will lose share. Net-net, how do you feel like that plays out to you? Anecdotally, is it better? Is it worse? Too early to say?

|

|

Jeffrey Coats:

|

The truth is, it’s probably too early to say. You know, there’s some rumblings. We may see some benefits from the Detroit Three in the near term, but a lot of these things have only really come up in the last 10 days in terms of a couple of our Japanese customers pulling back a little bit on advertising or lead volumes because they have inventory problems.

|

|

Steve Dyer:

|

Great. OK. So I guess, with that said, how do you feel directionally about your revenue for the next couple quarters? Q1 was obviously a pleasant surprise at $16 million. Is that a number you can stay above, or should we think a little bit lower than that for the next couple quarters?

|

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 10

|

Jeffrey Coats:

|

Well, I think we have a shot at probably being flat – right in the $16 million level for revenue.

|

|

Steve Dyer:

|

OK.

|

|

Jeffrey Coats:

|

I don’t mean to hesitate, but it’s just a little unclear as to what we’re going to see ultimately with the Japanese somewhat offset by some pickups with the domestics.

|

|

Steve Dyer:

|

Yes, understood. How do you envision the product mix going forward, and ultimately, obviously, what I’m trying to get at is, from a gross margin standpoint, do you view Q1 as more of an anomaly as to that level or is that just sort of the way the business is trending?

|

|

Jeffrey Coats:

|

Well, we’ve said before that we expect to see margin improvement through the course of this year. We said before we would expect to see a few hundred basis point increase in our gross margin during the course of this year, and we still feel that way. So it’s really been a mix issue, as we’ve been digesting and integrating the acquisition and getting our arms around some of our new supply relationships with other players in the lead distribution game. But, you know, based on, as we’ve said in the remarks, some optimization that we’ve been doing in our search engine marketing, we’ve already seen a pickup in our gross margin during the latter part of the quarter which we would expect to continue into the second quarter.

|

|

Steve Dyer:

|

OK, and then with respect to operating expenses, you’ve done a nice job really taking a lot of the cost out of the business. Is this a pretty decent level to think about going forward? Does it pick up? How should we think about that?

|

|

Jeffrey Coats:

|

I think it’s generally a pretty good level. I mean, it’s probably something in the 6.3 to 6.5 range. We have a couple of open positions because there’s always turnover in your employee ranks, and that’s what accounts for a little bit of it being as low as it is at the 6.3 level. But, like I’ve said before, we think we’ve got good leverage on our expenses, and we think we can generate the revenue that we need to without any meaningful pickup in expenses from where we are.

|

|

Steve Dyer:

|

OK, and then a last question, and I’ll hop back in the queue. Aperture – you touched on it a little bit – when would you expect some meaningful contribution from that as we look forward?

|

|

Jeffrey Coats:

|

I think the best answer I can give you right now, Steve, is that we do expect to see something from that this year. I think some of what’s been going on related to Japan has caused some people to hesitate on moving forward, because some of the Japanese guys are pulling back on their advertising pretty significantly across a lot of different offline and online media, and as a result of doing that, they don’t need to buy the data to decide where to place their media. So the best answer I can give you is, we are still working with Datran. We still have interested OEM customers, so we do expect to generate something during the course of the year.

|

AUTOBYTEL INC.

Moderator: Roger Pondel

05-05-11/5:00 p.m. ET

Confirmation # 59988615

Page 11

|

Steve Dyer:

|

OK. Thanks guys.

|

|

Jeffrey Coats:

|

Thank you, Steve.

|

|

Operator:

|

Thank you. Once again, if you have a question, please press star, then one at this time.

|

I show no further questions in the queue and would like to turn the conference back to Mr. Jeff Coats for closing remarks.

|

Jeffrey Coats:

|

Thank you, Mary.

|

Again, thank you, everyone. We feel like we’ve made a significant amount of progress generating positive cash flow in the first quarter. We are bullish about our prospects for the year and expect to see our business to continue to improve throughout the course of this year, so stay tuned for further improvements. Thank you.

|

Operator:

|

Ladies and gentlemen, thank you for your participation in today’s conference. This does conclude the program, and you may all disconnect at this time.

|

|

|

END

|

1Q 2011 Results

May 5, 2011

Welcome to Autobytel.com The

auto-centric, auto-savvy site with

comprehensive information

comprehensive information

and expert advice about

buying, selling and

maintaining

Virtually any

vehicle.

The statements made in the accompanying conference call or contained in this presentation that are not historical facts are

forward-looking statements under the federal securities laws. These forward-looking statements, including, but not limited

to the company’s belief regarding achievement of positive cash flow or profitability for the second quarter of 2011, are not

guarantees of future performance and involve assumptions and risks and uncertainties that are difficult to predict. Actual

outcomes and results may differ materially from what is expressed in, or implied by, these forward-looking statements.

Autobytel undertakes no obligation to update publicly any forward-looking statements, whether as a result of new

information, future events or otherwise. Among the important factors that could cause actual results to differ materially from

those expressed in, or implied by, the forward-looking statements are changes in general economic conditions; the financial

condition of automobile manufacturers and dealers; changes in fuel prices; the economic impact of terrorist attacks, political

revolutions or military actions; dealer attrition; pressure on dealer fees; increased or unexpected competition; the failure of

new products and services to meet expectations; failure to retain key employees or attract and integrate new employees;

actual costs and expenses exceeding charges taken by Autobytel; changes in laws and regulations; costs of legal matters,

including, defending lawsuits and undertaking investigations and related matters; and other matters disclosed in Autobytel’s

filings with the Securities and Exchange Commission. Investors are strongly encouraged to review the company’s Annual

Report on Form 10-K for the year ended December 31, 2010, and other filings with the Securities and Exchange

Commission for a discussion of risks and uncertainties that could affect business, operating results, or financial condition of

Autobytel and the market price of the company’s stock. In addition, current year financial information could be subject to

change as a result of subsequent events or the finalization of the company’s financial statement close which culminates

with the filing of the company’s Annual Report on Form 10-K for the current year.

forward-looking statements under the federal securities laws. These forward-looking statements, including, but not limited

to the company’s belief regarding achievement of positive cash flow or profitability for the second quarter of 2011, are not

guarantees of future performance and involve assumptions and risks and uncertainties that are difficult to predict. Actual

outcomes and results may differ materially from what is expressed in, or implied by, these forward-looking statements.

Autobytel undertakes no obligation to update publicly any forward-looking statements, whether as a result of new

information, future events or otherwise. Among the important factors that could cause actual results to differ materially from

those expressed in, or implied by, the forward-looking statements are changes in general economic conditions; the financial

condition of automobile manufacturers and dealers; changes in fuel prices; the economic impact of terrorist attacks, political

revolutions or military actions; dealer attrition; pressure on dealer fees; increased or unexpected competition; the failure of

new products and services to meet expectations; failure to retain key employees or attract and integrate new employees;

actual costs and expenses exceeding charges taken by Autobytel; changes in laws and regulations; costs of legal matters,

including, defending lawsuits and undertaking investigations and related matters; and other matters disclosed in Autobytel’s

filings with the Securities and Exchange Commission. Investors are strongly encouraged to review the company’s Annual

Report on Form 10-K for the year ended December 31, 2010, and other filings with the Securities and Exchange

Commission for a discussion of risks and uncertainties that could affect business, operating results, or financial condition of

Autobytel and the market price of the company’s stock. In addition, current year financial information could be subject to

change as a result of subsequent events or the finalization of the company’s financial statement close which culminates

with the filing of the company’s Annual Report on Form 10-K for the current year.

This presentation includes a discussion of "EBITDA," “Adjusted Operating Expenses,” and “Cash Flow,” which are non-GAAP financial measures. The

Company defines EBITDA as net income before (i) interest income (expense); (ii) income tax provision (benefit); and (iii) depreciation and amortization.

Company defines EBITDA as net income before (i) interest income (expense); (ii) income tax provision (benefit); and (iii) depreciation and amortization.

The Company defines Adjusted Operating Expenses as GAAP operating expenses adjusted for unusual, infrequent or non-recurring items. The Company

defines non-GAAP Cash Flow as EBITDA plus non-cash stock compensation related to the Company's grant of stock options and other equity instruments.

The Company believes these non-GAAP financial measures provide important supplemental information to management and investors. These non-GAAP

financial

measures reflect an additional way of viewing aspects of the Company's operations that, when viewed with the GAAP results and the accompanying

reconciliations to corresponding GAAP financial measures, provide a more complete understanding of factors and trends affecting the Company's business

and results of operations. These non-GAAP financial measures are used in addition to and in conjunction with results presented in accordance with GAAP

and should not be relied upon to the exclusion of GAAP financial measures. Management strongly encourages investors to review the Company's

consolidated financial statements in their entirety and to not rely on any single financial measure. Because non-GAAP financial measures are not

standardized, it may not be possible to compare these financial measures with other companies' non-GAAP financial measures having the same or similar

names. In addition, the Company expects to continue to incur expenses similar to the non-GAAP adjustments described above, and exclusion of these items

from the Company's non-GAAP measures should not be construed as an inference that these costs are unusual, infrequent or non-recurring.

defines non-GAAP Cash Flow as EBITDA plus non-cash stock compensation related to the Company's grant of stock options and other equity instruments.

The Company believes these non-GAAP financial measures provide important supplemental information to management and investors. These non-GAAP

financial

measures reflect an additional way of viewing aspects of the Company's operations that, when viewed with the GAAP results and the accompanying

reconciliations to corresponding GAAP financial measures, provide a more complete understanding of factors and trends affecting the Company's business

and results of operations. These non-GAAP financial measures are used in addition to and in conjunction with results presented in accordance with GAAP

and should not be relied upon to the exclusion of GAAP financial measures. Management strongly encourages investors to review the Company's

consolidated financial statements in their entirety and to not rely on any single financial measure. Because non-GAAP financial measures are not

standardized, it may not be possible to compare these financial measures with other companies' non-GAAP financial measures having the same or similar

names. In addition, the Company expects to continue to incur expenses similar to the non-GAAP adjustments described above, and exclusion of these items

from the Company's non-GAAP measures should not be construed as an inference that these costs are unusual, infrequent or non-recurring.

Copyright (c) 2011 Autobytel Inc.

Safe Harbor Statement and Non-GAAP

Disclosures

Disclosures

3

.

Comments

.

§ Fourth consecutive quarter of sequential revenue increases

.

§ Gross profit increased 7% from the prior quarter and 32% Y-O-Y

.

§ EBITDA and Cash Flow positive in Q1 2011

Financial Overview

1 See slide 8 for Adjusted Operating Expense reconciliation

2 EBITDA is equal to Net Income plus Interest, Taxes, and Depreciation and Amortization; See slide 4 for reconciliation

3 Cash Flow is equal to EBITDA plus Non-Cash Stock Compensation; See slide 4 for reconciliation

4 Cash decreased in Q3 2010 primarily as a result of the acquisition of Cyber Ventures / Autotropolis ($9M) and a strategic investment in Driverside ($1M)

Copyright (c) 2011 Autobytel Inc.

4

Copyright (c) 2011 Autobytel Inc.

EBITDA and Cash Flow

1 EBITDA is equal to Net Income plus Interest, Taxes, and Depreciation and Amortization

2 Cash Flow is equal to EBITDA plus Non-Cash Stock Compensation

3 Above financials are impacted by rounding to the nearest $0.1M

Comment

§ EBITDA and Cash Flow are positive for the first time since the downturn in the auto-

motive industry, excluding the $2.7M patent settlement payment in the first quarters

of ‘09 and ‘10, and the $1.3M escrow payment in the second quarter of '09

motive industry, excluding the $2.7M patent settlement payment in the first quarters

of ‘09 and ‘10, and the $1.3M escrow payment in the second quarter of '09

5

Auto Industry Impact - Japan

• March 11, 2011 - Magnitude 9.0 earthquake hits Japan

• April 19, 2011 - J.D. Power holds its forecast for 2011 stating “lost volume in the near-term is expected to be

made up by the end of the year. However, there remains a relatively low level of risk of a downward revision.”

made up by the end of the year. However, there remains a relatively low level of risk of a downward revision.”

• April 25, 2011 - IHS trims US LV Sales to 12.9M from 13.3M, and suggests that 15% of Japanese production

will be completely lost

will be completely lost

• April 26, 2011 - AutoNation reduces its outlook for US LV Sales from 12.8M to mid 12M

• May 4, 2011 - J.D. Power is quoted “uncertainty about gas prices and stockpiles is increasing the risk that the

industry may not reach the expected 13M for US LV Sales”

industry may not reach the expected 13M for US LV Sales”

• GM, Ford, and Chrysler are positioned to take share, particularly in small, fuel efficient vehicles

• Hyundai Kia plants are already producing near capacity, allowing limited ability to take share

• Toyota and Honda will not see production return to normal levels until the end of 2011

• 15% of the lost volume in Japan will not be replaced, 55% will be replaced in 2011 and 30% in 2012

Japan impact appears to be a temporary setback in the ongoing

automotive recovery, with the Detroit 3 positioned to gain share

automotive recovery, with the Detroit 3 positioned to gain share

Events

Impact

Sources: Automotive News, HIS, J.D. Power and Associates

Copyright (c) 2011 Autobytel Inc.

Comments

§ OEM and other wholesale purchase request revenue continues to grow, up 130% Y-O-Y

and 6% sequentially

and 6% sequentially

§ Dealer revenue up 10% over the prior quarter and down slightly Y-O-Y

§ Specialty finance purchase request revenue up 20% Y-O-Y and 13% sequentially

(seasonality)

(seasonality)

Revenue Results

Source: Automotive News

(1) Cash for Clunkers Program occurred in Q3 2009

Copyright (c) 2011 Autobytel Inc.

Comments

§ Retail New and Used franchises were up 13% Y-O-Y as a result of organic growth and the

acquisition, however were down vs. the prior quarter due to attrition during the

acquisition integration process, and a focus on building and retaining dealers in areas

where we have significant purchase request availability

acquisition, however were down vs. the prior quarter due to attrition during the

acquisition integration process, and a focus on building and retaining dealers in areas

where we have significant purchase request availability

§ Dealers participating in other revenue products grew >15% sequentially

Dealer Base

Copyright (c) 2011 Autobytel Inc.

8

Copyright (c) 2011 Autobytel Inc.

Operating Expenses

1 Includes all patent settlements

2 Severance includes associated accelerated stock compensation of $(0.1) and $(0.1) for Q210 and Q410, respectively

3 Acquisition costs consist of professional fees associated with the acquisition of Cyber Ventures and Autotropolis during 2010

4 Acquisition amortization relates to acquired intangible assets from Cyber Ventures and Autotropolis during 2010

9

Comments

§ The automotive market is beginning to show signs of steady growth

§ SAAR averaging about 13M in the first 4 months of 2011

§ 2011 US light vehicle sales were projected to be up 12% to 13M as of February 2011

§ Impact from Japan earthquake and tsunami are still unknown, however there is

speculation that US LV sales will be impacted

speculation that US LV sales will be impacted

Auto Industry Sales

Source: Automotive News

Source: J.D. Power and Associates

Copyright (c) 2011 Autobytel Inc.

10

2.7 Million Total

Purchase Requests

Purchase Requests

4.0 Million Total

Purchase Requests

Purchase Requests

2.9 Million Total

Purchase Requests

Purchase Requests

§ Major competitors in consumer purchase request distribution acquire substantially all

of their purchase requests from third parties

of their purchase requests from third parties

§ Combination of internal purchase request generation and strong distribution creates

significant competitive advantage for Autobytel and drives higher gross margins

significant competitive advantage for Autobytel and drives higher gross margins

Comments

Autobytel Internally-Generated

Purchase Requests

Purchase Requests

2011

2011

Estimate

Estimate

Further Gross Margin Expansion

Further Gross Margin Expansion

Gross Margin 37.8%

Gross Margin 37.8%

Gross Margin 35.8%

Gross Margin 35.8%

Copyright (c) 2011 Autobytel Inc.

11

§ Third party sites, like Autobytel.com, provide objective and credible information to the

automotive consumer

automotive consumer

§ During the six months prior to purchase, consumers visit third party sites most often

(percent of Internet users viewing automotive sites)

Source: J.D. Power and Associates, October 2010.

Third Party Internet Sites Outperform

Copyright (c) 2011 Autobytel Inc.

12

Website Redesign

• Dynamic new redesign

(June 2011)

(June 2011)

• Unique consumer

proposition “Your

Lifetime Automotive

Advisor”

proposition “Your

Lifetime Automotive

Advisor”

• Distinctive consumer

content, engagement

and social dialogue

content, engagement

and social dialogue

Copyright (c) 2011 Autobytel Inc.

13