Attached files

| file | filename |

|---|---|

| EX-31.1 - KAIBO FOODS Co Ltd | v216607_ex31-1.htm |

| EX-21.1 - KAIBO FOODS Co Ltd | v216607_ex21-1.htm |

| EX-14.1 - KAIBO FOODS Co Ltd | v216607_ex14-1.htm |

| EX-31.2 - KAIBO FOODS Co Ltd | v216607_ex31-2.htm |

| EX-32.1 - KAIBO FOODS Co Ltd | v216607_ex32-1.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Fiscal Year Ended December 31, 2010

OR

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the Transition Period from _______________ to _________________

Commission file number: 001-34712

KAIBO FOODS COMPANY LIMITED

(Exact name of Registrant as Specified in Its Charter)

|

Nevada

|

42-1749358

|

|

(State or Other Jurisdiction

|

|

|

of Incorporation or Organization)

|

(I.R.S. Employer Identification No.)

|

|

Rm. 2102 F & G, Nan Fung Centre

264-298 Castle Peak Rd.

|

|

|

Tsuen Wan, N.T., Hong Kong

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code:

(852) 2412-2208

SECURITIES REGISTERED PURSUANT TO SECTION 12 (B) OF THE ACT:

COMMON STOCK, PAR VALUE $0.001 PER SHARE

SECURITIES REGISTERED PURSUANT TO SECTION 12 (G) OF THE ACT: NONE

Name of each exchange on which registered: The OTC Bulletin Board

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. £ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. £ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes £ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes £ No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated

filer ¨

|

Accelerated

filer ¨

|

Non-accelerated filer ¨

|

Smaller reporting

company x

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes £ No x

The aggregate market value of the shares of common stock, par value $0.001 per share, of the registrant held by non-affiliates on June 30, 2010 was $121,275, which was computed upon the basis of the closing price on that date.

There were 3,285,007 shares of common stock of the registrant outstanding as of March 30, 2011.

TABLE OF CONTENTS

|

PART I

|

3

|

||

|

Item 1

|

Business

|

3

|

|

|

Item 1A.

|

Risk Factors

|

23

|

|

|

Item 1B.

|

Unresolved Staff Comments

|

40

|

|

|

Item 2

|

Properties

|

40

|

|

|

Item 3

|

Legal Proceedings

|

41

|

|

|

Item 4

|

Removed and Reserved

|

42 | |

|

PART II

|

42

|

||

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

42

|

|

|

Item 6

|

Selected Financial Data

|

43

|

|

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

43

|

|

|

Item 7A

|

Quantitative and Qualitative Disclosures About Market Risk

|

53

|

|

|

Item 8

|

Financial Statements and Supplementary Financial Data

|

53

|

|

|

Item 9

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

|

53

|

|

|

Item 9A.

|

Controls and Procedures

|

54

|

|

|

Item 9B.

|

Other Information

|

55

|

|

|

PART III

|

|

55 | |

|

Item 10

|

Directors, Executive Officers and Corporate Governance

|

56

|

|

|

Item 11

|

Executive Compensation

|

59

|

|

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

60

|

|

|

Item 13

|

Certain Relationships and Related Transactions and Director Independence

|

61

|

|

|

Item 14

|

Principal Accounting Fees and Services

|

61

|

|

|

PART IV

|

|

||

|

Item 15

|

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES

|

62

|

1

Introductory Note

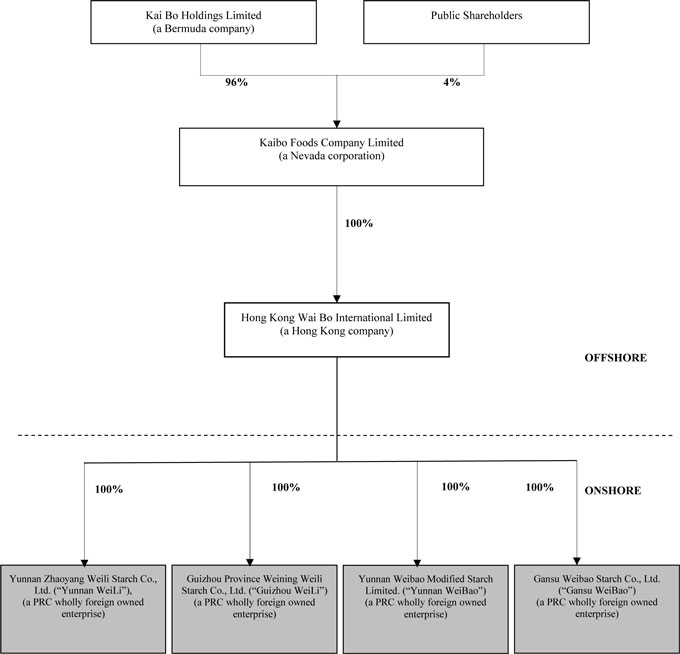

Except as otherwise indicated by the context, references in this Annual Report on Form 10-K (this “Form 10-K”) to the “Company,” “Kaibo Foods,” “we,” “us” or “our” are references to the combined business of Kaibo Foods Company Limited and its consolidated subsidiaries. References to “Waibo” are references to our wholly owned subsidiary, Hong Kong Wai Bo International Limited, a Hong Kong company; references to “Yunnan WeiLi” are to Waibo’s wholly owned subsidiary, Yunnan Zhaoyang Weili Starch Co., Ltd., a PRC wholly foreign owned enterprise; references to “Guizhou WeiLi” are to Waibo’s wholly owned subsidiary, Guizhou Province Weining Weili Starch Co., Ltd., a PRC wholly foreign owned enterprise; references to “Gansu WeiBao” are to Waibo’s wholly owned subsidiary, Gansu Weibao Starch Co., Ltd, a PRC wholly foreign owned enterprise; and references to “Yunnan WeiBao” are to Waibo’s wholly owned subsidiary, Yunnan WeiBao Modified Starch Limited, a PRC wholly foreign owned enterprise. References to “China” or “PRC” are references to the People’s Republic of China. References to “RMB” are to Renminbi, the legal currency of China, and all references to “$” and dollar are to the U.S. dollar, the legal currency of the United States.

On March 10, 2011 we effected a 1 for 16.09 reverse stock split (the “Reverse Stock Split”) of our outstanding common stock, par value $0.001 per share (“Common Stock”). All share and per share amounts in this Form 10-K give effect to the Reverse Stock Split, unless otherwise noted.

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements and information relating to Kaibo Foods that are based on the beliefs of our management as well as assumptions made by and information currently available to us. Such statements should not be unduly relied upon. When used in this Form 10-K, forward-looking statements include, but are not limited to, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions, as well as statements regarding new and existing products, technologies and opportunities, statements regarding market and industry segment growth and demand and acceptance of new and existing products, any projections of sales, earnings, revenue, margins or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements regarding future economic conditions or performance, uncertainties related to conducting business in China, any statements of belief or intention, and any statements or assumptions underlying any of the foregoing. These statements reflect our current view concerning future events and are subject to risks, uncertainties and assumptions. There are important factors that could cause actual results to vary materially from those described in this Form 10-K as anticipated, estimated or expected, including, but not limited to: competition in the industry in which we operate and the impact of such competition on pricing, revenues and margins, volatility in the securities market due to the general economic downturn; Securities and Exchange Commission (the “SEC”) regulations which affect trading in the securities of “penny stocks,” and other risks and uncertainties. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward- looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

2

PART I

|

Item 1.

|

Business.

|

Description of Business

We are a leading PRC producer of high quality potato starch, a value added and functional ingredient in many different types of packaged and processed foods. Our corporate headquarters are in Hong Kong and our operational headquarters are in Kunming city, Yunnan province. Our factories are in Yunnan, Guizhou and Gansu provinces in China. Our potato starch is sold under the “Wei Bao” and ”Jiabao” brands and we believe that our products are well known for their consistency, purity, quality and white color.

Potato starch is a functional food additive, offering strong adhesion without chemicals. Potato starch is also a cost effective thickener, which does not interfere with taste. In addition, our premium potato starch is white in color and thus can be added to many foods without affecting product color. Our potato starch is used by makers of noodles, instant noodles, dumplings, fishballs, shrimp balls, meatballs, and many other mainstream Chinese foods.

We believe that we are among the top five makers of premium native potato starch in the PRC and that our manufacturing presence in Yunnan, Guizhou and Gansu makes us the single largest producer in these provinces. Our current overall production capacity is 111,500 metric tons per year. Our native potato starch has consistently received the government’s highest rating, which affords it a premium price in the PRC market place. We sell our products to distributors and food processing companies. In 2010 we sold to more than 50 customers, with only one customer comprising more than 5% of our annual total sales.

China’s modernization has brought about significant changes to its food industry. With increasing urbanization, the use of supermarkets and consumption of prepared and processed foods have grown rapidly. According to a July 2010 report of the United States Department of Agriculture, the PRC now has over 500,000 manufacturers of frozen and processed foods, with a total annual output of RMB 4.5 trillion in 2009. The potato starch market in the PRC is currently estimated at over 900,000 metric tons (China Potato Starch-Specialized Society 2009).

We benefit from favorable government policies in the PRC. Since January 1, 2008, we have enjoyed a full income tax exemption that has no expiration date for most of our business due to government policies aimed at providing extra incentive to rural food businesses involved in the PRC’s primary food supply. In addition, we have a successful track record at working with local governments to increase rural income levels through increased potato production. This is important to our business because obtaining high and steady quantities of premium potato resource is the key challenge facing large scale potato starch production.

We provide farmer education and assistance to enable better yields and higher starch potatoes, and we were selected in 2009 by the Ministry of Agriculture to establish the National R&D Center for Potato Processing. We are building new production lines that will expand our business into whole potato starch, which is used in the fast food industry, as well as modified potato starch, which is used in non food industries including paper, textiles, and building materials.

Company Background

Our History and Corporate Structure

Prior to October 21, 2010, we were a “shell company” (as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). The Company was originally incorporated in the State of Nevada on December 10, 2007 to assist companies in their need for CFO’s and CFO related services. As a result of our former sole officer and director, Norman LeBoeuf, only devoting limited time to our operations, our efforts to establish and develop business operations in our originally intended line of business were unsuccessful and by the middle of 2010, it became evident to the Board of Directors that it would not be possible to continue with the then-current business model.

3

As a result of an introduction by Millennium Group, Inc. in early October of 2010, the Board of Directors became aware of a company with operations in China manufacturing potato starch that was seeking to effect a “reverse merger” with a public company in the United States. After reviewing the potato starch company’s business plan and U.S. GAAP financial statements, the members of the board authorized Neville Pearson to negotiate the terms of an Agreement and Plan of Reorganization regarding the acquisition of Waibo (the “Exchange Agreement”), which Exchange Agreement was executed on October 21, 2010. As a result of the attractive terms offered by the founders of Waibo, our Board of Directors did not obtain a formal appraisal of the business operations of Waibo, but reviewed the audited financial statements provided by such founders and the other corporate documents relating to the business in reaching the decision to proceed with the Exchange Agreement.

On October 21, 2010, the (“Closing Date”), pursuant to the Exchange Agreement by and among the Company, Waibo, the holders of all outstanding shares of Waibo (the “Waibo Shareholders”) and Orion Investment Inc. (the “Company’s Principal Shareholder”), we acquired all of the outstanding shares of Waibo (the “Waibo Shares”) from the Waibo Shareholders and the Waibo Shareholders transferred all of the Waibo Shares to us. In exchange, we agreed to issue to the Waibo Shareholders or their designee, an aggregate of 22,493,475 shares of Common Stock (361,920,000 shares of our Common Stock without giving effect to the Reverse Stock Split) (the “Exchange Shares”), equal to 96% of all our outstanding shares, after giving effect to the conversion of an outstanding convertible note of the Company held by Millennium Group, Inc., in the principal amount of $25,000 (the “Convertible Note”), which such note is convertible into 586,804 shares of Common Stock (9,441,667 shares of Common Stock without giving effect to the Reverse Stock Split), and the planned amendment of our Articles of Incorporation. On the Closing Date, we did not have sufficient authorized shares to complete the issuance of the entire amount of Exchange Shares and shares issuable pursuant to the Convertible Note, so only 2,361,716 shares (38,000,000 shares without giving effect to the Reverse Stock Split) were issued to the designee of the Waibo Shareholders at the closing, and no shares were issued to the holder of the Convertible Note.

On March 10, 2011, we effectuated an amendment to our Articles of Incorporation to, among other things, increase our authorized shares, change our name to Kaibo Foods Company Limited from CFO Consultants, Inc., and effect the Reverse Stock Split. We are currently in the process of issuing the remaining 20,131,759 shares (323,920,000 shares prior to giving effect to the Reverse Stock Split) to the Waibo Shareholders, as well as 586,804 shares (9,441,667 shares prior to giving effect to the Reverse Stock Split) to Millennium Group, Inc., the holder of the Convertible Note.

As a result of the transactions contemplated by the Exchange Agreement, Waibo became our wholly owned subsidiary and we are in the business of producing potato starch.

4

Our current corporate structure is set forth below:

5

December 2010 Private Placement

On December 21, 2010, we entered into a securities purchase agreement (the “Purchase Agreement”), with certain accredited investors (the “Investors”) for the issuance and sale of an aggregate of (i) 571,797 shares of our Common Stock (the “Shares”) and (ii) warrants to purchase up to 114,356 shares of Common Stock underlying the warrants (the “Warrant Shares”), each such warrant having an initial exercise price of $5.23 per share and expiring on the three year anniversary of the effective date of the increase of our authorized shares of Common Stock (the “Authorized Increase Date”), for aggregate gross proceeds equal to approximately $2,300,000 (the “December 2010 Private Placement”).

In connection with the December 2010 Private Placement, we and our majority stockholder, Kai Bo Holdings Limited (“Kai Bo Holdings”), entered into an escrow agreement (the “Make Good Escrow Agreement”) with the Investors pursuant to which Kai Bo Holdings placed 285,892 shares of its Common Stock of the Company into escrow for distribution of up to 142,946 shares of Common Stock to the Investors in each of 2011 and 2012 in the event that it fails to reach certain net income targets for its 2010 and 2011 fiscal years. Pursuant to the Make Good Escrow Agreement, if our after tax net income for fiscal 2010 is less than 95% of $25,882,536 (95% of such amount being the “2010 Guaranteed ATNI”), the escrow agent will transfer to each Investor on a pro rata basis a number of shares that is equal to 7,148 shares of Common Stock for each full percentage point by which the 2010 Guaranteed ATNI was not achieved up to a maximum of 142,946 shares. If our after tax net income for fiscal 2011 is less than 95% of $33,382,670 (95% of such amount being the “2011 Guaranteed ATNI”), the escrow agent will transfer to each Investor a number of shares that is equal to 7,148 shares of Common Stock for each full percentage point by which the 2011 Guaranteed ATNI was not achieved up to a maximum of 142,946 shares. For the purposes of the Make Good Escrow Agreement, after tax net income excludes any expense item (other than tax expense and interest expense) deducted in determining net income not appearing under the heading “Operating expenses” on our Consolidated Statement of Operations, including but not limited to fair value change on derivatives, warrants and make good shares.

The principal equity holders of Kai Bo Holdings are Kai Bo International Limited, a British Virgin Islands corporation, which holds approximately 68% of the outstanding ordinary shares of Kai Bo Holdings, and Elegant Century Investments, a British Virgin Islands corporation, which holds approximately 8% of the outstanding ordinary shares of Kai Bo Holdings. The equity holders of Kai Bo International Limited are Joanny Kwok (40%), Jacky Kwok (30%) and Lam Yukang (30%). The sole equity holder of Elegant Century Investments is Joanny Kwok. The remaining equity holders of Kai Bo Holdings are Sea Dragon Investments Limited, a British Virgin Islands corporation, Hong Kong Investments Group Limited, a British Virgin Islands corporation, Fiora Capital Holdings Ltd., a British Virgin Islands corporation, Pico International Holdings Limited, a British Virgin Islands corporation, Winning Gain Investments Limited, a British Virgin Islands corporation, and International Investment (Hong Kong) Trading Group Limited, a Hong Kong corporation. Other than certain loans made by our shareholders used to finance working capital as disclosed in our financial statements, Joanny Kwok’s positions as our chairman, chief executive officer and a director and Jacky Kwok’s position as a director, we do not have any material relationship with any of the equity holders of Kai Bo Holdings. There are no agreements among Kai Bo Holdings and Joanny Kwok, Jacky Kwok or Lam Yukang.

In connection with the December 2010 Private Placement, we entered into a registration rights agreement (the “Registration Rights Agreement”) with the Investors, in which we agreed to file a registration statement (the “Registration Statement”) with the U.S. Securities and Exchange Commission (the “SEC”) to register for resale the Shares, the Warrant Shares and the shares underlying the Agent Warrants (defined below) within 60 calendar days of the closing date of the December 2010 Private Placement, and to use our best efforts to have the registration statement declared effective within 180 calendar days of the closing date of the December 2010 Private Placement. We are obligated to pay liquidated damages of 1% of the dollar amount of the Shares sold in the December 2010 Private Placement per month, payable in cash, up to a maximum of 10%, if the registration statement is not filed within the foregoing time periods or if we do not respond in the time period prescribed in the Registration Rights Agreement to comments received from the SEC on the Registration Statement. ROTH Capital Partners, LLC (“Roth”) acted as the exclusive financial advisor and placement agent for us. Roth received warrants to purchase up to 57,179 shares of Common Stock at a price per share of $5.23 (the “Agent Warrants”), as well as $161,000 in cash. The Agent Warrants are for a term of three years from the Authorized Increase Date and have a cashless exercise feature.

6

Industry Overview

Starch is a carbohydrate consisting of a large number of glucose units joined together by glycosidic bonds. This polysaccharide is produced by all green plants as an energy store. It is the most important carbohydrate in the human diet and is contained in such staple foods as potatoes, wheat, maize (corn) and rice. Potato starch is starch extracted from potatoes and is a very refined starch, containing minimal amount of protein or fat. Native potato starch is a white powder with a neutral taste and high adhesive properties. This functional additive is widely used in many types of Chinese processed foods including instant noodles, dumplings, sauces, meatballs and sausages.

Market Overview

The potato starch industry in China is relatively young. According to an August 2010 report of the United States Department of Agriculture, approximately 90% of the potato starch factories categorized in China are characterized as small. We believe that Waibo, with 111,500 metric tons of annual capacity, already ranks among the top 5 producers in the PRC. We believe that premium potato starch usage will grow in step with the overall growth in processed and prepared foods. In addition, we expect that premium potato starch will increasingly be used as a value added substitute for corn starch as well as chemical thickeners and stabilizers. We believe that all natural additives like premium potato starch will be more sought after by food makers that are increasingly concerned about the use of chemical stabilizers and additives and by consumers who prefer more nutritious ingredients.

Increased Urbanization and Consumer Purchasing Power

Over the last thirty years, China has experienced rapid urbanization due to the increasingly limited capacity of rural areas to provide adequate economic support for a large agrarian population, the increasing disparity in disposable incomes between rural and urban dwellers and the easing of restrictions, which historically limited rural to urban migration from rural areas to towns and cities. According to the Annual Report on Urban Development of China in 2009, the population of Chinese cities by the end of 2009 exceeded 621 million people, representing an increase of 410 million since 1982. It is further estimated that China’s urban population will expand to 926 million by 2025 and hit the one billion mark by 2030.

Per capita incomes in urban centers have risen greatly in recently decades, from RMB 1,516 in 1990 to RMB 16,180 in 2008. As of 2008, there were over 34,000 (The National Bureau of Statistics of China Yearbook 2009) supermarkets in the PRC. By comparison, the US has over 35,000 supermarkets (U.S. Census Bureau, Food Marketing Institute 2009).

Increased demand for prepared and processed foods

Consumption of prepared and processed foods in the PRC has grown in step with the country’s urbanization trend. As people’s lives become busier, the traditional custom of making daily purchases of fresh raw produce from small farmers’ markets has increasingly given way to less frequent visits to supermarkets to buy prepared, packaged and processed foods. According to a July 2010 report of the United States Department of Agriculture, the prepared and processed food industry in China reached RMB 4.5 trillion (2009), representing a 20% increase from 2008. The industry remains highly fragmented with many thousands of different food makers and tens of thousands of products. The instant noodle market towers over most with demand reaching RMB 59 billion in 2009 (Noodles in China, Euromonitor, 2009).

Advantage Over Corn Starch

Corn starch is also used as a thickening agent, stabilizer, and emulsifier. Corn starch is approximately half the cost of potato starch and currently in greater supply in the PRC. According to a May 2009 report of the United States Department of Agriculture, there are over 160 corn-processing companies in China, with annual processing capacity estimated at 63.93 million metric tons. However, as food producers become more concerned about food-safety, potato starch is increasingly viewed as a superior alternative. Corn starch also has a lower melting point than potato starch and it can affect product color. It must therefore receive significant bleaching and modification to match the whiteness and temperature attributes of potato starch.

7

Raw Material Sourcing

Many potato starch manufacturers are beset with inconsistent potato supply channels. They typically find that potatoes cannot be bought in sufficient quantities from major farms or farmers’ markets to run a large potato starch production factory. Moreover, potato strains have been adapted to various soil and climate conditions over centuries of cultivation. These differences will produce varying degrees of starch content and whiteness.

The high fragmentation and disparities in product quality place a premium on locating potato starch factories in the high end regions around a concentration of small growers and soliciting active local government support.

Additional Potato Starch Varieties and Usages

Modified potato starch, which is similar to native potato starch in appearance, is composed mainly of native potato starch and other starch varieties. It is primarily used in many non-food industries, the largest which is the paper industry. A typical sheet of copy paper may have as much as 8% starch content (North Carolina State University report). Modified potato starch is also used for corrugated board adhesives as well as glue products used in a wide variety of applications including bookbinding, wall paper, paper sacks and other forms of paper bonding. Potato starch is also used in the construction products industry for gypsum board. Furthermore, modified potato starch is applied for biotechnical raw material, fabrics and textiles, pharmaceuticals and cosmetics and detergents.

Whole potato starch is the dehydrated part of fresh potatoes, except the potato skins. It is typically used in products such as French fries and processed mashed potatoes. It is used to add both texture and flavor to processed foods. Approximately 90% of our native potato starch is used by the food industry, while the rest is used in a variety of different food related industries.

Competitive Strengths

We believe we have the following competitive advantages:

Factories Built in Top Potato Producing Regions

We have located our factories in regions of China with moderate temperatures and long growing seasons, where potatoes can be grown to large sizes with smooth skins that are less contaminated with impregnated soil and gravel. In addition, we build our factories in rural regions where potato farming can bring important added benefit to low-income rural populations. Many of our competitors are state-owned and have positioned their production facilities primarily to serve local growers without much consideration to starch content or product quality.

Strong Brand Equity known for High Quality Product

Our “Wei Bao” and “Jiabao” brands are strongly associated with our commitment to quality, which has been supported over the years with numerous awards and certifications. The General Administration of Quality Supervision, Inspection and Quarantine of the PRC issues grades for the quality of potato starch: passed, first grade and excellent. Approximately 99% of our products received the “excellent” rating and approximately 1% the “first grade” rating.

Our production facilities have implemented stringent quality control procedures, from the procurement of raw materials to the delivery of our finished products. This includes active supervision and training assistance provided to our local farm suppliers.

Positioned in High Growth Industry Segment

In 2009, the food processing industry recorded a record high output of $662 billion (July 2010 report of the United States Department of Agriculture). We believe there are significant opportunities to increase sales of premium potato starch for processed foods, given its many benefits versus traditional food additives. Participants in many non-food industries are now actively using or exploring the use of potato starch. These include paper, bio-plastic, biotechnical raw materials, fabrics and textiles, pharmaceuticals and cosmetics and detergents.

8

Potato Starch Industry is the Beneficiary of Strong Government Support

Two main policy goals are to better assist rural low-income populations while developing and improving the country’s massive food needs. Our production facilities in Yunnan, Gansu and Guizhou provinces are beneficiaries of these initiatives. For example, in 2007 China implemented a 5-year anti-dumping tax on EU imports of potato starch of 17%, 18% or 35% depending on the original manufacturer (PRC Ministry of Commerce). The Ministry of Finance and State Administration of Taxation has also implemented beneficial tax policies to spur development of both agriculture and the downstream food-processing industry. We have successfully obtained a full exemption on Enterprise Income Tax (“EIT”) since 2008.

Business Strategies

We plan to increase our market presence and build on our core competitive strengths by implementing the following strategies:

Increase Production Capacity in Existing and New Locations

We plan to increase our production capacity by building facilities in strategic locations as well as pursuing mergers and acquisitions for growth. We are currently building a modified starch factory with an annual production capacity of 20,000 metric tons in Zhaotong City, Yunnan province and expect this to be completed by June 2011.

Our current expansion strategy is to build 4 new production facilities in the next 3 years, with an aggregate capacity of 123,000 metric tons of a variety of potato starch products. We plan to build native potato starch factories in Guizhou and Sichuan provinces. The Guizhou facility is expected to have a production capacity of 38,000 metric tons and we expect it to be operational by January 2012. The Sichuan facility will have a production capacity of 40,000 metric tons and should be operational by March 2013.

We plan to build a whole potato starch facility in Guizhou, with a production capacity of approximately 15,000 metric tons, which we expect to be operational by January 2012. We also plan to build a modified potato starch factory in Yunnan, with a production capacity of approximately 30,000 metric tons which we plan to be operational by August 2013. We evaluate facility locations based on land fertility, water availability and railway proximity. We also aim to identify those areas with adequate farm acreage that are amenable to our quality standards.

We expect that the total capital expenditures for the expansion plans referred to above in the next three years is approximately $108 million, which we expect to be financed by net proceeds received from future equity offerings and from cash generated from continuing operating activities.

We also believe there are opportunities to acquire existing state-owned potato-starch production facilities by leveraging our reputation for operating successful facilities and producing a premium product.

Penetrate New Markets with Expanded Product Offerings

We currently produce native potato starch and plan to begin production of modified potato starch by June 2011. Modified potato starch is used in various industries such as food processing, paper manufacturing, medical supplies, industrial chemicals and wood and furniture production. Modified starch tends to have higher profit margins and wider usages than native potato starch.

We also plan to produce whole potato starch, which is primarily used for food processing. Whole potato starch is the dehydrated part of fresh potatoes, except the potato skins. Popular products such as French fries are typically made using whole potato starch. It is used to add both texture and flavor to processed foods.

9

Maintain and Expand Our Customer Base

We plan to continue to build on our current customer relationships as well as enter new markets. We believe our diverse and wide customer base provides us beneficial word of mouth exposure, in addition to stabilizing product demand. Our customer base also gives us built in product demand as we increase our production capabilities. We intend to continue to increase our customer base to allow us to gain increased market presence in new and emerging markets in China.

R&D Efforts

In 2009, we were chosen by The Ministry of Agriculture to be the National R&D Center for Potato Processing. This cooperation with the government promotes open exchange of cultivation techniques and production technologies. Currently, the government provides minimal financial support for this award. However, we believe that our cooperation with the government gives us early access to the government’s most recent R&D achievements in our industry. We also anticipate the government will increase funding with the increasing significance of processed potato products in the PRC. We believe that it is important to have excellent R&D capabilities and have plans to build a new R&D center in Kunming in 2013. We believe this facility can serve as a center for innovation and new ideas that promotes us as a market leader.

Brands and Products

Product brand

We market our products using the “Wei Bao” and “Jiabao” brand names. Our Wei Bao brand is used primarily in the food processing industry while our Jiabao brand is used in the restaurant industry. The two separate brands allow us to better focus on two segments’ different purchasing criteria. We focus on building brand names known for high quality. In 2006, we registered our trademark for the Wei Bao brand name and in 2010 we registered our trademark for the Jiabao brand name. These trademarks are effective for 10 years and are typically renewable.

In 2010, approximately 98% of our revenue came from products sold under Wei Bao brand name and the “ “ logo.

“ logo.

“ logo.The Jiaobao brand is represented by the “ “ logo and accounted for approximately 2% of our revenue in 2010.

“ logo and accounted for approximately 2% of our revenue in 2010.

“ logo and accounted for approximately 2% of our revenue in 2010.Products

We produce native potato starch, which is primarily used in the food processing industry. Native potato starch is known for its thickening, adhesive and emulsifying properties, used in many processed foods including include ham, sausage, frozen foods, meatballs, prawn balls, starch strips, instant noodles, jelly, biscuits, cake, ice cream, yogurt, canned foods and candy. It is manufactured as white colored powder and has a shelf life of up to two years.

We plan to expand our product offerings to include modified starch and whole potato starch. We are currently building a production facility for modified starch factory in Zhaotong city, Yunnan province with a production capacity of approximately 20,000 tons. We anticipate this factory to be completed by June 2011. We anticipate our modified starch will be suitable for food processing, paper manufacturing, medical supplies and industrial chemicals. We also plan to produce whole potato starch. This type of starch typically used for food processing and adds flavor and the body for the processed food it is used for.

10

Research and Development

Our research and development center was established in 2003 in Yunnan province. In 2009, we were chosen by The Ministry of Agriculture to be the National R&D Center for Potato Processing. We collaborate with the government on developing new species of potatoes, increasing the crop yield of potatoes, raising starch content and developing potatoes resistant to diseases and pests. We receive minimum funding from the government as result of being selected for this position. However, we believe this cooperation gives us early access to recent governmental R&D developments, allowing us early implementation of the most current agricultural techniques and potato varieties.

We also have informal cooperation with the Agricultural Technology University and the Research Institute of Agriculture both of which are located in Kunming city. We plan to build a new research and development center in Kunming by 2013. The focus of this center will be on developing different types of modified starch. We incurred insignificant expenses on R&D during the 2010 and 2009 fiscal years.

11

Production Process

We manufacture potato starch at four different production facilities in China. In 2010, we produced 25,923, 25,690 and 46,620 metric tons of starch at our production faculties located in Yunnan (1 facility), Guizhou (1 facility) and Gansu (2 facilities) respectively. By June 2011, we anticipate completion of a fifth facility in Zhaotong City, Yunnan Province, capable of annually producing 20,000 metric tons of modified potato starch. Our total annual production capacity as of December 31, 2010 was 111,500 metric tons of native potato starch.

Native Potato Starch Processing

Our purchasing department buys potatoes from farmers located near our production facilities. We establish potato quality requirements at the outset and closely examine them for weight and texture. We have designated potato storage areas with man-made water channels in the center. High-pressure water guns push our potatoes into the water channels, which transports the naturally buoyant potatoes into our production facilities while beginning the cleansing process.

The potatoes enter our production facility and first undergo cleaning. They enter our tumbling machine which uses high-pressure water to remove dirt and any other unwanted particles. The clean potatoes are then transferred to a temporary storage container before the grinding process.

The grinding machines turn the potatoes into a pulp-like sludge, which results in dissolution of the potato cells and the release of the potato starch content. We separate the potato dreg, which is procured from the potato sludge using an extrication filter. The result is a thick, milky potato paste.

The potato paste is transferred into a high-speed centrifugal sieve to remove the potato fiber. The paste passes through a series of filters to remove tiny sand particles and water. The end result of this process is unfiltered starch. This starch is then run through an 18-layer filter device to further remove impurities and then placed into a refining container. The concentration of the potato starch is measured during this process.

The starch is then taken from the refining container and run through a vacuum hydro-extractor to reduce the water content to 40%. The starch then undergoes hot air drying and sterilization at temperatures of 140°C and gradually cooled to approximately 45-50°C. This process reduces the water content to 18-20%. We send this air-dried potato starch to cyclonic silos to separate the air from the starch. The potato starch powder is then sent to a vibrating sifter to produce a more refined and consistent product - high quality, pure white starch powder. We then package and store the finished potato starch product for delivery.

12

Production process chart

The following diagram illustrates the production process for potato starch.

Procurement

The primary raw material is potatoes, which we procure from more than 100,000 mostly small-sized local farms. We typically go to nearby villages and come to an oral agreement with the leading potato farmer in that region. This particular farmer acts as our main supplier and will coordinate with the other potato farmers in his village and collect their potatoes. We currently have a total of 270 such main suppliers.

Our production facility in Yunnan province has arrangements with 98 suppliers for a total of 154,000 tons of potatoes. Our production facility in Guizhou has arrangements with 83 suppliers, for approximately 155,000 tons of potatoes and our production facilities in Gansu have arrangements with 89 suppliers for approximately 266,000 tons of potatoes.

We have strict selection criteria for our raw material suppliers. First and foremost, they need to be located in ideal potato cultivating areas with high crop yields and long harvest seasons. Generally, the local government will help the farmers select the ideal potato types for regional production.

Typically, potatoes have one growing season that starts in March. The potatoes are harvested from July to December. We also set the quality requirements for our potatoes such as the starch content.

Potato farmers are highly fragmented with limited production capabilities. We typically rely on current market trends and historical prices during supplier negotiations. Prices are generally stable from year to year. We do not sign a formal contract with our suppliers. We negotiate prices yearly and pay cash on delivery.

13

Inventory Control and Management

We typically maintain raw material inventory equal to 3-5 days of production to maintain freshness. Towards the end of harvesting season, we can preserve the potatoes by storing them in cellars, extending their usability for several months.

The raw materials are weighed upon delivery to confirm the ordered amount before settling with cash. Because we are currently producing at near full capacity, we tend to make daily orders of constant quantities. Our finished goods warehouses hold approximately 200-300 metric tons of products, which are weighed before storage. We typically ship our finished goods within 1-3 days.

Quality Control

We have received all necessary governmental licenses and permits for potato processing, which include the Food Hygiene License, National Industrial Product Manufacture License and an “excellent” rating from the General Administration of Quality Supervision, Inspection and Quarantine. We have also obtained ISO 9001:2000 Quality Management System certification, ISO 22000:2005 Food Safety Management System certification, and Hazard Analysis and Critical Control Points certification (HACCP).

Raw materials quality control

We set potato quality standards with our suppliers before ordering, foremost of which is a minimum 15% starch content. Most potato species can only be cultivated for approximately 3 years before their starch content lowers to unacceptable levels. However, we know of more than 100 different suitable species that our nearby potato farmers could use, thus ensuring a constant supply. The local government agricultural bureau also works with the farmers to help pick the species of potatoes consistent with our product quality specifications.

During the cultivation process, we send quality assurance teams to selected farms in our potato producing regions to perform a visual inspection on site and test a random sample of potatoes for starch content. Only if the potatoes meet our requirements will we accept delivery. Additional visual examinations and tests for starch content are performed upon delivery.

Production process quality control

We pay particular attention to four key steps in the production process that will largely determine the quality of the finished product: grinding, centrifugal sieving, 18-layer filtering and hot air drying.

Finished products quality control

We perform a visual inspection, a smell test and laboratory testing on our finished goods. The General Administration of Quality Supervision, Inspection and Quarantine of the PRC performs a national standard test on our finished goods, which entails examinations of the chemical and physical properties every six months. Our quality assurance staff ensures that our potato starch meets the national standard every ten minutes during the production process. The finished goods also undergo semi-annual testing by the Measure for Quality Supervision and Administration of Food. This department is entrusted with upholding the national food safety standards and grants us the right to use a “Quality Safety Label” (QS label) on our products.

Sales and Customer Relations

Each of our sales offices in Kunming, Yunnan province has two sales staff. This is sufficient for present capacity levels to maintain customer relationships and process customer orders and will be expanded as required.

We have approximately 59 customers in industries such as food processing, food distribution and retail food sales. We select our customers based on creditworthiness, market share in respective industry, growth potential and product demand. We have grown a diversified customer base with evenly distributed sales patterns to reduce concentration risk and provide leverage during pricing negotiations.

14

Our customers are located in 12 provinces and four municipalities in China. We have a strong market share in Guangdong, Fujian and Shandong provinces.

The following map illustrates the geographical coverage of our sales and distribution network in the PRC:

Our customers use our potato starch in hundreds of different processed foods, including ham, sausage, frozen foods, meatballs, prawn balls, starch strips, instant noodles, jelly, biscuits, cake, ice cream, yogurt, canned foods, and candy.

Our customers sign bi-annual sales contracts for fixed product volumes. We deliver our products to our customers on a regular basis as defined by the sales contracts. We typically accumulate orders of shipment amounts up to shipment amounts of 60 tons, the capacity of a single rail car, for economical delivery. We typically only pay for transferring our goods to a railway station located near our facilities. We extend credit terms of up to 90 days from delivery for our top customers.

Seasonality

We typically stop our production process from May through July for our Yunnan and Guizhou production facilities. The potato-planting season typically begins in March and the potatoes are delivered to our facilities from August until the end of December. The harvested potatoes can typically be stored up to 4 months in cellars allowing us to expand our production period to April.

15

Our factories in Gansu are in a colder region in China and typically halt production from January to February. During these months, we store potatoes for production from March through May. Our Gansu factory will then close for production from June to July and resume production in August. During the off-season, we spend time performing routine production line maintenance.

Pricing

We price our products based on market trends, raw material costs and competitors’ prices. Our raw materials constitute approximately 80% of production costs. The prices of potatoes have increased by 87% over the past 5 years. Whereas, the market price for potato starch has increased by 66% over the past 5 years. The following table shows our price trends for potatoes and potato starch for the past five years.

|

Average price of potatoes

(per ton)

|

Average selling price of potato starch

(per ton) (with VAT)

|

||||||||||

|

Year

|

Price (RMB)

|

Calendar Year

|

Price (RMB)

|

||||||||

|

2006

|

370 | 2006 | 4,450 | ||||||||

|

2007

|

455 | 2007 | 5,650 | ||||||||

|

2008

|

450 | 2008 | 5,850 | ||||||||

|

2009

|

420 | 2009 | 5,540 | ||||||||

|

2010

|

691 | 2010 | 7,392 | ||||||||

Competition

The potato starch market is highly fragmented, with more than 50 medium-sized enterprises and more than 1,000 small-sized enterprises. According to the CPSSS, in 2007, there were 11 enterprises with an annual capacity of 10,000 - 28,200 metric tons, 20 enterprises with an annual capacity of 2,000-8,000 metric tons, and 10 enterprises with an annual capacity of 300 - 1,800 metric tons.

We believe we are one of the top 5 potato starch producers in the PRC. Our main competitors include the following:

|

China Essence Group Ltd (China Essence) headquartered in Beijing and listed on the Singapore Exchange in 2006. It is one of the largest producers of potato-related products in the PRC with five potato-processing facilities and a total of 17 production lines. China Essence has locations in Heilongjiang province and Inner Mongolia. It produces a wide range of products including vermicelli, starch strips and five-grain noodles, potato starch, modified starch and potato by-products. Its distribution network covers 48 cities in the PRC.

|

|

Yunnan Run Kai Industry Co Ltd (Run Kai) is based in Yunnan Province and has a potato starch annual production capacity of 30,000 metric tons. It has a well-known brand called, “Run Kai.” Run Kai also exports to foreign countries such as Japan, Korea, Hong Kong, Singapore and Indonesia.

|

|

Qinghai Weisidun Co., Ltd (Weisidun) is based in Qinghai and has an annual production capacity of 77,000 metric tons of potato starch. It has 5 production lines - 1 for modified starch, 2 for instant vermicelli, 1 for crystal vermicelli and 1 that produces a microbiologic agent.

|

|

Heilongjiang Beidahuang Potato Industry Group (Beidahuang) produces potato starch and has an annual production capacity of 100,000 metric tons. The group has expanded its businesses into modified starch, potato biological feed, ethanol and other by-products.

|

Employees

Our production staff operates the production lines 24 hours a day in three eight-hour shifts, 6 days a week. All of our staff are full-time employees. The chart below describes the number of employees per department as of December 31, 2010.

16

|

Department

|

Total

|

|||

|

Senior Executive Management

|

4 | |||

|

Senior Management

|

16 | |||

|

HR

|

10 | |||

|

Administration

|

78 | |||

|

Financial Staff

|

13 | |||

|

Sales people

|

5 | |||

|

Quality Control

|

21 | |||

|

R&D

|

3 | |||

|

Manufacturing Managers

|

61 | |||

|

Manufacturing Workers

|

279 | |||

|

Total

|

490 | |||

We have made employee retirement fund contributions. We believe we are in material compliance with all applicable labor and safety laws and regulations in the PRC, including the PRC Labor Contract Law, the PRC Production Safety Law, the PRC Regulation for Insurance for Labor Injury, the PRC Unemployment Insurance Law, the PRC Provisional Insurance Measures for Maternity of Employees, PRC Interim Provisions on Registration of Social Insurance, the PRC Interim Regulation on the Collection and Payment of Social Insurance Premiums and other related regulations, as well as rules and provisions issued by the relevant governmental authorities from time to time.

According to the PRC Labor Contract Law, we are required to enter into labor contracts with our employees. We are required to pay no less than local minimum wages to our employees. We are also required to provide employees with labor safety and sanitation conditions meeting PRC government laws and regulations and carry out regular health examinations of our employees engaged in hazardous occupations.

Intellectual Property Rights

We registered the “Wei Bao” and “Jiabao” brand trademarks on August 14, 2006 and January 21, 2010 respectively. These trademarks are effective and renewable after 10 years. We have a registered PRC design patent for package bags under the patent number ZL 200930129068.x with a valid term of ten years commencing from September 29, 2009.

Insurance

We believe that we maintain insurance in line with industry standards. Our insurance covers 100% of the net book value of our property, plant and equipment and inventories.

Legal Proceedings

We are not engaged in any material litigation, arbitration or claim, and no material litigation, arbitration or claim is known by our management to be pending or threatened by or against us that would have a material adverse effect on our results from operations or financial condition.

PRC Government Regulations

Our operations are subject to numerous laws, regulations, rules and specifications of the PRC relating to various aspects. We are in compliance in all material respects with such laws, regulations, rules, specifications and have obtained all material permits, approvals and registrations relating to human health and safety, the environment, taxation, foreign exchange administration, financial and auditing, and labor and employments. We make capital expenditures from time to time to stay in compliance with applicable laws and regulations. Below we set forth a summary of the most significant PRC regulations or requirements that may affect our business activities operated in the PRC or our shareholders’ right to receive dividends and other distributions of profits from our PRC subsidiaries.

17

Any company that conducts business in the PRC must have a business license that covers a particular type of work. The business license of each of our PRC subsidiaries covers its present business of production and deep processing of potato starch. Prior to expanding any of our PRC subsidiaries’ business beyond that of its business license, we are required to apply and receive approval from the PRC government.

Annual Inspection

In accordance with relevant PRC laws, all types of enterprises incorporated under the PRC laws are required to conduct annual inspections with the State Administration for Industry and Commerce of the PRC or its local branches. In addition, foreign-invested enterprises are also subject to annual inspections conducted by PRC government authorities. In order to reduce enterprises’ burden of submitting inspection documentation to different government authorities, the Measures on Implementing Joint Annual Inspection issued by the PRC Ministry of Commerce together with other six ministries in 1998 stipulated that foreign-invested enterprises shall participate in a joint annual inspection jointly conducted by all relevant PRC government authorities. Our PRC subsidiaries, as foreign-invested enterprises, have participated and passed all such annual inspections since their establishment.

Employment laws

We are subject to laws and regulations governing our relationship with our employees, including: wage and hour requirements, working and safety conditions, citizenship requirements, work permits and travel restrictions. These include local labor laws and regulations, which may require substantial resources for compliance.

China’s National Labor Law, which became effective on January 1, 1995, and China’s National Labor Contract Law, which became effective on January 1, 2008, permit workers in both state and private enterprises in China to bargain collectively. The National Labor Law and the National Labor Contract Law provide for collective contracts to be developed through collaboration between the labor union (or worker representatives in the absence of a union) and management that specify such matters as working conditions, wage scales, and hours of work. The laws also permit workers and employers in all types of enterprises to sign individual contracts, which are to be drawn up in accordance with the collective contract.

Foreign Investment in PRC Operating Companies

The Catalogue for the Guidance of Foreign Investment Industries jointly issued by the Ministry of Commerce, or the MOFCOM, and the National Development and Reform Commission, or the NDRC, in 2007 classified various industries/businesses into three different categories: (i) encouraged for foreign investment; (ii) restricted to foreign investment; and (iii) prohibited from foreign investment. For any industry/business not covered by any of these three categories, they will be deemed industries/businesses permitted to have foreign investment. Except for those expressly provided restrictions, encouraged and permitted industries/businesses are usually 100% open to foreign investment and ownership. With regard to those industries/businesses restricted to or prohibited from foreign investment, there is always a limitation on foreign investment and ownership. Our PRC subsidiaries’ business does not fall under the industry categories that are restricted to, or prohibited from foreign investment and is not subject to limitation on foreign investment and ownership.

Regulation of Foreign Currency Exchange

Foreign currency exchange in the PRC is governed by a series of regulations, including the Foreign Currency Administrative Rules (1996), as amended, and the Administrative Regulations Regarding Settlement, Sale and Payment of Foreign Exchange (1996), as amended. Under these regulations, the Renminbi is freely convertible for trade and service-related foreign exchange transactions, but not for direct investment, loans or investments in securities outside the PRC without the prior approval of the State Administration of Foreign Exchange, or SAFE. Pursuant to the Administrative Regulations Regarding Settlement, Sale and Payment of Foreign Exchange (1996), Foreign Invested Enterprises, or FIEs, may purchase foreign exchange without the approval of the SAFE for trade and service-related foreign exchange transactions by providing commercial documents evidencing these transactions. They may also retain foreign exchange, subject to a cap approved by SAFE, to satisfy foreign exchange liabilities or to pay dividends. However, the relevant Chinese government authorities may limit or eliminate the ability of FIEs to purchase and retain foreign currencies in the future. In addition, foreign exchange transactions for direct investment, loan and investment in securities outside the PRC are still subject to limitations and require approvals from the SAFE.

18

Regulation of FIEs’ Dividend Distribution

The principal laws and regulations in the PRC governing distribution of dividends by FIEs include:

|

|

(i)

|

The Sino-foreign Equity Joint Venture Law (1979), as amended, and the Regulations for the Implementation of the Sino-foreign Equity Joint Venture Law (1983), as amended;

|

|

|

(ii)

|

The Sino-foreign Cooperative Enterprise Law (1988), as amended, and the Detailed Rules for the Implementation of the Sino-foreign Cooperative Enterprise Law (1995), as amended;

|

|

|

(iii)

|

The Foreign Investment Enterprise Law (1986), as amended, and the Regulations of Implementation of the Foreign Investment Enterprise Law (1990), as amended.

|

Under these regulations, FIEs in the PRC may pay dividends only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, foreign-invested enterprises in the PRC are required to set aside at least 10% of their respective accumulated profits each year, if any, to fund certain reserve funds unless such reserve funds have reached 50% of their respective registered capital. These reserves are not distributable as cash dividends. The board of directors of a FIE has the discretion to allocate a portion of its after-tax profits to staff welfare and bonus funds, which may not be distributed to equity owners except in the event of liquidation.

Regulation of a Foreign Currency’s Conversion into RMB and Investment by FIEs

On August 29, 2008, the SAFE issued a Notice of the General Affairs Department of the State Administration of Foreign Exchange on the Relevant Operating Issues concerning the Improvement of the Administration of Payment and Settlement of Foreign Currency Capital of Foreign-Invested Enterprises or Notice 142, to further regulate the foreign exchange of FIEs. According to the Notice 142, FIEs shall obtain a verification report from a local accounting firm before converting its registered capital of foreign currency into Renminbi, and the converted Renminbi shall be used for the business within its permitted business scope. The Notice 142 explicitly prohibits FIEs from using RMB converted from foreign capital to make equity investments in the PRC, unless the domestic equity investment is within the approved business scope of the FIE and has been approved by SAFE in advance.

Regulation of Foreign Exchange in Certain Onshore and Offshore Transactions

In October 2005, the SAFE issued the Notice on Issues Relating to the Administration of Foreign Exchange in Fund-raising and Return Investment Activities of Domestic Residents Conducted via Offshore Special Purpose Companies, or SAFE Notice 75, which became effective as of November 1, 2005, and was further supplemented by two implementation notices issued by the SAFE on November 24, 2005 and May 29, 2007, respectively. SAFE Notice 75 states that PRC residents, whether natural or legal persons, must register with the relevant local SAFE branch prior to establishing or taking control of an offshore entity established for the purpose of overseas equity financing involving onshore assets or equity interests held by them. The term “PRC legal person residents” as used in SAFE Notice 75 refers to those entities with legal person status or other economic organizations established within the territory of the PRC. The term “PRC natural person residents” as used in SAFE Notice 75 includes all PRC citizens and all other natural persons, including foreigners, who habitually reside in the PRC for economic benefit. The SAFE implementation notice of November 24, 2005 further clarifies that the term “PRC natural person residents” as used under SAFE Notice 75 refers to those “PRC natural person residents” defined under the relevant PRC tax laws and those natural persons who hold any interests in domestic entities that are classified as “domestic-funding” interests.

19

PRC residents are required to complete amended registrations with the local SAFE branch upon: (i) injection of equity interests or assets of an onshore enterprise to the offshore entity, or (ii) subsequent overseas equity financing by such offshore entity. PRC residents are also required to complete amended registrations or filing with the local SAFE branch within 30 days of any material change in the shareholding or capital of the offshore entity, such as changes in share capital, share transfers and long-term equity or debt investments or, providing security, and these changes do not relate to return investment activities. PRC residents who have already organized or gained control of offshore entities that have made onshore investments in the PRC before SAFE Notice 75 was promulgated must register their shareholdings in the offshore entities with the local SAFE branch on or before March 31, 2006.

Under SAFE Notice 75, PRC residents are further required to repatriate into the PRC all of their dividends, profits or capital gains obtained from their shareholdings in the offshore entity within 180 days of their receipt of such dividends, profits or capital gains. The registration and filing procedures under SAFE Notice 75 are prerequisites for other approval and registration procedures necessary for capital inflow from the offshore entity, such as inbound investments or shareholders loans, or capital outflow to the offshore entity, such as the payment of profits or dividends, liquidating distributions, equity sale proceeds, or the return of funds upon a capital reduction.

Government Regulations Relating to Taxation

On March 16, 2007, the National People’s Congress or the NPC, approved and promulgated the PRC Enterprise Income Tax Law, which we refer to as the New EIT Law. The New EIT Law took effect on January 1, 2008. Under the New EIT Law, FIEs and domestic companies are subject to a uniform tax rate of 25%. The New EIT Law provides a five-year transition period starting from its effective date for those enterprises which were established before the promulgation date of the New EIT Law and which were entitled to a preferential lower tax rate under the then-effective tax laws or regulations.

On December 26, 2007, the State Council issued a Notice on Implementing Transitional Measures for Enterprise Income Tax, or the Notice, providing that the enterprises that have been approved to enjoy a low tax rate prior to the promulgation of the New EIT Law will be eligible for a five-year transition period since January 1, 2008, during which time the tax rate will be increased step by step to the 25% unified tax rate set out in the New EIT Law. From January 1, 2008, for the enterprises whose applicable tax rate was 15% before the promulgation of the New EIT Law , the tax rate will be increased to 18% for year 2008, 20% for year 2009, 22% for year 2010, 24% for year 2011, 25% for year 2012. For the enterprises whose applicable tax rate was 24%, the tax rate will be changed to 25% from January 1, 2008.

The New EIT Law provides that an income tax rate of 20% may be applicable to dividends payable to non-PRC investors that are “non-resident enterprises”. Non-resident enterprises refer to enterprises which do not have an establishment or place of business in the PRC, or which have such establishment or place of business in the PRC but the relevant income is not effectively connected with the establishment or place of business, to the extent such dividends are derived from sources within the PRC. The income tax for non-resident enterprises shall be subject to withholding at the income source, with the payor acting as the obligatory withholder under the New EIT Law, and therefore such income taxes generally called withholding tax in practice. The State Council of the PRC has reduced the withholding tax rate from 20% to 10% through the Implementation Rules of the New EIT Law. It is currently unclear in what circumstances a source will be considered as located within the PRC. We are a U.S. holding company and substantially all of our income is derived from dividends we receive from our subsidiaries located in the PRC. Thus, if we are considered as a “non-resident enterprise” under the New EIT Law and the dividends paid to us by our subsidiary in the PRC are considered income sourced within the PRC, such dividends may be subject to a 10% withholding tax.

Such income tax may be exempted or reduced by the State Council of the PRC or pursuant to a tax treaty between the PRC and the jurisdictions in which our non-PRC shareholders reside. For example, the 10% withholding tax is reduced to 5% pursuant to the Double Tax Avoidance Agreement Between Hong Kong and Mainland China if the beneficial owner in Hong Kong owns more than 25% of the registered capital in a company in the PRC.

The new tax law provides only a framework of the enterprise tax provisions, leaving many details on the definitions of numerous terms as well as the interpretation and specific applications of various provisions unclear and unspecified. Any increase in the combined company’s tax rate in the future could have a material adverse effect on its financial conditions and results of operations.

20

In addition, according to the circular entitled Scope of Preliminary Processing of Agricultural Products Entitled to Preferential Enterprise Income Tax Policies (Trial Implementation) published by Ministry of Finance (“MOF”) and State Administrative of Taxation (“SAT”), our PRC subsidiaries are entitled to full exemption from the PRC corporate income tax beginning January 1, 2008. The exemption currently is not subject to any limitations.

Regulations of Overseas Investments and Listings

On August 8, 2006, six PRC regulatory agencies, including the MOFCOM, the China Securities Regulatory Commission or the CSRC, the State Asset Supervision and Administration Commission or the SASAC, the State Administration of Taxation, or the SAT, the State Administration for Industry and Commerce or the SAIC and SAFE, amended and released the New M&A Rule, which took effect as of September 8, 2006. This regulation, among other things, includes provisions that purport to require that an offshore special purpose vehicle (SPV) formed for purposes of overseas listing of equity interest in PRC companies and controlled directly or indirectly by PRC companies or individuals obtain the approval of the CSRC prior to the listing and trading of such SPV’s securities on an overseas stock exchange.

On September 21, 2006, the CSRC published on its official website procedures regarding its approval of overseas listings by SPVs. The CSRC approval procedures require the filing of a number of documents with the CSRC. The application of the New M&A Rule with respect to overseas listings of SPVs remains unclear with no consensus currently existing among the leading PRC law firms regarding the scope of the applicability of the CSRC approval requirement.

Environmental Protection

Our manufacturing operations are subject to PRC environmental laws and regulations on air emission, solid waste emission, sewage and waste water, discharge of waste and pollutants, and noise pollution. These laws and regulations include Law of the PRC on Environmental Protection, Law of the PRC on the Prevention and Control of Water Pollution, Law of the PRC on the Prevention and Control of Atmospheric Pollution, Law of the PRC on the Prevention and Control of Pollution from Environmental Noise and Law of the PRC on the Prevention and Control of Environmental Pollution of Solid Waste. We are also subject to periodic monitoring by relevant local government environmental protection authorities.

According to these environmental laws and regulations, all business operations that may cause environmental pollution and other public hazards are required to incorporate environmental protection measures into their operations and establish a reliable system for environmental protection. Such a system must adopt effective measures to prevent and control pollution levels and harm caused to the environment in the form of waste gas, waste water and solid waste, dust, malodorous gas, radioactive substance, noise, vibration and electromagnetic radiation generated in the course of production, construction or other activities. Companies in the PRC are also required to carry out an environment impact assessment before commencing construction of production facilities and the installation of pollution treatment facilities that meet the relevant environmental standards and treat pollutants before discharge. We carried out the required environment impact assessment before commencing construction of our production facilities and have obtained all the required permits and environmental approvals for our production facilities.

The main environmental impact from our operations is the generation of wastewater and noise pollution from the operation of production machinery. In order to comply with the relevant environmental protection laws and regulations, we have implemented an environmental protection system to ensure the emissions from production operations meet the pollution indicators. In addition, our production plant is located in an open area, away from residential areas and equipped with an appropriate convection and ventilation system. In order to reduce the impact on the environment, we have enhanced the convection and ventilation system at our production facilities to improve air quality and adopted various measures to prevent and minimize the noise pollution from our production operations.

21

Health and Safety Matters

The PRC Production Safety Law (the “Production Safety Law”) requires that we maintain safe working conditions under the Production Safety Law and other relevant laws, administrative regulations, national standards and industrial standards. We are required to offer education and training programs to our employees regarding production safety. The design, manufacture, installation, use and maintenance of our safety equipment are required to conform to applicable national and industrial standards. In addition, we are required to provide employees with safety and protective equipment that meet national and industrial standards and to supervise and educate them to wear or use such equipment according to the prescribed rules.

We consider the safety of our employees to be a priority. We have implemented internal health and safety policies in the work place, available through our handbook on production safety and security procedures, which incorporate safety laws and regulations in the PRC. We have implemented safety guidelines on production procedures for the safe operation of production equipment and machinery during each stage of the production process. We require our employees to attend occupational safety education training courses on our safety policies and procedures to enhance their awareness of safety issues. We provide and require our employees to wear suitable protective devices to ensure their safety. We also provide employees with free annual medical check-ups.

As required under the Regulation of Insurance for Labor Injury, Provisional Insurance Measures for Maternity of Employees, Interim Regulation on the Collection and Payment of Social Insurance Premiums and Interim Provisions on Registration of Social Insurance, we provide our employees in the PRC with welfare schemes covering pension insurance, unemployment insurance, maternity insurance, injury insurance and medical insurance.

We believe that we were in compliance with all applicable labor and safety laws and regulations in all-material respects, and implemented internal safety guidelines and operating procedures.

We believe that we are in compliance with the new PRC Labor Contract Law, which came into effect on January 1, 2008, in all respects, and do not believe this new law will have any impact on our business and operations. Since the commencement of our business, none of our employees has been involved in any major accident in the course of their employment and we have never been subject to disciplinary actions with respect to the labor protection issues.

Food Safety Regulations and Production Permit

Under previous legal regime, food producers and food processing companies are required to obtain both the food hygiene permit and food production permit for their operations. The New Food Safety Law (“Food Safety Law”) issued by the Standing Committee of the National Peoples’ Congress (“NPC”) on February 28, 2009 repealed the Food Hygiene Law (issued by the Standing Committee of NPC in 1995) and as a result the producers engaged in the production or processing of food-related products are only required to obtain the production permits issued by the local office of the PRC General Administration of Quality Supervision, Inspection and Quarantine for their operations.