Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

| ¨ | TRANSITION REPORT PURSUANT TO SECTIONS 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-32188

ORAGENICS, INC.

(Exact name of registrant as specified in its charter)

| Florida | 59-3410522 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(IRS Employer Identification No.) |

| 3000 Bayport Drive, Suite 685 Tampa, FL |

33607 | |

| (Address of Principal Executive Offices) | (Zip Code) |

813-286-7900

(Issuer’s Telephone Number, Including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of each class |

Name of each exchange on which registered | |

| None |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

Common stock, par value $.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant, as of June 30, 2010 was approximately $17,209,815 based upon a last sales price of $7.00 as reported by the OTCBB.

As of March 23, 2011, there were 5,683,076 shares of the registrant’s Common Stock outstanding.

Table of Contents

| ii | ||||||||

| PART I | ||||||||

| ITEM 1. | 1 | |||||||

| ITEM 1A. | 22 | |||||||

| ITEM 2. | 38 | |||||||

| ITEM 3. | 38 | |||||||

| ITEM 4. | 38 | |||||||

| PART II | ||||||||

| ITEM 5. | 39 | |||||||

| ITEM 6. | 39 | |||||||

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

40 | ||||||

| ITEM 7A. | 52 | |||||||

| ITEM 8. | 53 | |||||||

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

53 | ||||||

| ITEM 9A | 53 | |||||||

| ITEM 9B. | 55 | |||||||

| PART III | ||||||||

| ITEM 10. | 56 | |||||||

| ITEM 11. | 59 | |||||||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED SHAREHOLDER MATTERS |

68 | ||||||

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

69 | ||||||

| ITEM 14. | 71 | |||||||

| PART IV | ||||||||

| ITEM 15. | 72 | |||||||

| 73 | ||||||||

| F-2–F-3 | ||||||||

| F-4 | ||||||||

| F-5 | ||||||||

| F-6 | ||||||||

| F-7 | ||||||||

| F-8–F-24 | ||||||||

NOTE REGARDING REVERSE STOCK SPLIT

On September 24, 2010, we filed Articles of Amendment to our Amended and Restated Articles of Incorporation with the Secretary of State of the State of Florida to effect a reverse split of our common stock at a ratio of one for twenty. All historical share and per share amounts have been adjusted to reflect the resulting reverse stock split.

i

Table of Contents

FORWARD LOOKING STATEMENTS AND CERTAIN CONSIDERATIONS

This report, along with other documents that are publicly disseminated by us, contains or might contain forward-looking statements within the meaning of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements included in this report and in any subsequent filings made by us with the SEC other than statements of historical fact, that address activities, events or developments that we or our management expect, believe or anticipate will or may occur in the future are forward-looking statements. These statements represent our reasonable judgment on the future based on various factors and using numerous assumptions and are subject to known and unknown risks, uncertainties and other factors that could cause our actual results and financial position to differ materially. We claim the protection of the safe harbor for forward-looking statements provided in the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act and Section 21E of the Exchange Act. Examples of forward-looking statements include: (i) projections of revenue, earnings, capital structure and other financial items, (ii) statements of our plans and objectives, (iii) statements of expected future economic performance, and (iv) assumptions underlying statements regarding us or our business. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as “believes,” “expects,” “estimates,” “may,” “will,” “should,” “could,” “seeks,” “plans,” “intends,” “anticipates” or “scheduled to” or the negatives of those terms, or other variations of those terms or comparable language, or by discussions of strategy or other intentions.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that could cause the actual results to differ materially from those contemplated by the statements. The forward-looking information is based on various factors and was derived using numerous assumptions. Important factors that could cause our actual results to be materially different from the forward-looking statements include the following risks and other factors discussed under the Item 1A “Risk Factors” in this Annual Report on Form 10-K. These factors include:

| • | Our inability to continue to raise capital, |

| • | We have incurred significant operating losses since our inception and cannot assure you that we will generate revenues or achieve profitability. |

| • | As a result of our lack of financial liquidity, our auditors have indicated there is substantial doubt about our ability to continue as a going concern. |

| • | If we fail to achieve positive cash flows from our operations and we fail to raise additional capital to meet our capital needs, we may need to significantly curtail operations. |

| • | If we raise additional capital it may be on terms that result in substantial dilution to our existing shareholders, |

| • | We are subject to extensive and costly regulation by the FDA, which must approve our product candidates in development and could restrict or delay the future commercialization of these product candidates. |

| • | We may be unable to achieve commercial viability and acceptance of our ProBiora3 products and proposed product candidates or increase sales of our ProBiora3 products. |

| • | Orders we receive for our consumer products may be subject to terms and conditions that could result in their cancellation or the return of products to us. |

| • | We may become dependent on a few large retail customers for sales of our consumer products. |

| • | We may be unable to successfully operate internationally. |

| • | We may be unable to improve upon, protect and/or enforce our intellectual property. |

| • | We may be unable to enter into strategic collaborations or partnerships for the development, commercialization, manufacturing and distribution of our proposed product candidates or maintain strategic collaborations or partnerships. |

ii

Table of Contents

| • | We may be adversely impacted by a continuing or worsening worldwide financial crises and its impact on consumers, retailers and equity and debt markets as well as our ability to obtain required additional funding to conduct our business. |

| • | We are subject to significant competition. |

| • | As a public company, we must implement additional and expensive finance and accounting systems, procedures and controls as we grow our business and organization to satisfy new reporting requirements, which will increase our costs and require additional management resources. |

| • | Success, timing and expenses of our expected clinical trials. |

| • | If we are unable to raise sufficient capital our license for our SMaRT™ Replacement Therapy and MU-1140 with the University of Florida Research Foundation could be terminated. |

We caution investors that actual results or business conditions may differ materially from those projected or suggested in forward-looking statements as a result of various factors including, but not limited to, those described above and in the Risk Factors section of this report. We cannot assure you that we have identified all the factors that create uncertainties. Moreover, new risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. Readers should not place undue reliance on forward-looking statements. Except as required by applicable law, we undertake no obligation to publicly release the result of any revision of these forward-looking statements to reflect events or circumstances after the date they are made or to reflect the occurrence of unanticipated events.

iii

Table of Contents

PART I

This description contains certain forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from the results discussed in the forward-looking statements as a result of certain of the risks set forth herein. We assume no obligation to update any forward-looking statements contained herein.

Overview

We are a biopharmaceutical company focused primarily on oral health products and novel antibiotics. Within oral health, we are developing our pharmaceutical product candidate, SMaRT Replacement Therapy, and we are also commercializing our oral probiotic blend, ProBiora3. Within antibiotics, we are developing our pharmaceutical product candidate, MU1140-S, and we intend to use our patented, novel organic chemistry platform to create additional antibiotics for therapeutic use.

Our SMaRT Replacement Therapy is designed to be a painless, one-time, five-minute topical treatment applied to the teeth that has the potential to offer lifelong protection against dental caries, or tooth decay. Dental diseases are the most prevalent chronic infectious diseases in the world, affecting up to 90% of schoolchildren and the vast majority of adults. In 2009, Popular Mechanics magazine named SMaRT Replacement Therapy as the “#1 New Biotech Breakthrough That Will Change Medicine.” In the United States alone, the annual cost to treat tooth decay is estimated to be $40 billion. SMaRT is based on the creation of a genetically modified strain of bacteria that colonizes in the oral cavity and replaces native decay-causing bacteria. We commenced a second Phase 1 clinical trial for our SMaRT Replacement Therapy, which we expect to conclude in the second half of 2011.

We have also developed and are commercializing a variety of products that contain the active ingredient ProBiora3, a patent-pending blend of oral probiotics that promotes fresher breath, whiter teeth and support overall oral health. The global probiotics market is expected to be $31.2 billion by 2014, representing a compound annual growth rate, or CAGR, of 12.6% from 2009. We have conducted extensive scientific studies on ProBiora3, in order to market our products under self-affirmed Generally Recognized As Safe status, or GRAS. We sell our ProBiora3 products through multiple distribution channels, and our customers include Walgreens, Kroger, and Garden of Life, among others.

While developing SMaRT Replacement Therapy, members of our scientific team discovered that the SMaRT bacterial strain produces MU1140, a molecule belonging to the novel class of antibiotics known as lantibiotics. MU1140 has proven active preclinically against Gram positive bacteria responsible for a number of healthcare-associated infections, HAIs. The direct cost to the U.S. healthcare system from HAIs is estimated to be up to $45 billion annually. We are in the process of scaling up production of our synthetic form of MU1140, or MU1140-S, and expect to commence preclinical testing during the first half of 2011 and to file an Investigational New Drug, or IND, application with the FDA in mid-2012. The key technology behind the production of MU1140-S is our Differentially Protected Orthogonal Lanthionine Technology platform, or DPOLT, which is a patented, novel organic chemistry platform that we believe will enable the first ever commercial scale, cost-effective production any of the 50 known lantibiotics. We intend to use DPOLT to create a pipeline of lantibiotics for therapeutic use.

Oragenics was founded in 1996 to commercialize the results of more than 30 years of research in oral biology by our principal founder and Chief Scientific Officer, Dr. Jeffrey Hillman. Dr. Hillman earned a DMD from Harvard School of Dental Medicine and a PhD in Molecular Genetics from Harvard University. He began his research career at the Harvard-affiliated Forsyth Institute in Boston, Massachusetts, where he introduced the concept of replacement therapy to prevent tooth decay by using a genetically modified strain of Streptococcus mutans, or S. mutans, to replace the decay-causing strains of S. mutans that are present on human teeth. He subsequently continued this research, now called SMaRT Replacement Therapy, at the University of Florida College of Dentistry. Under Dr. Hillman’s leadership, our scientific team has also developed other technologies such as ProBiora3, MU1140 and our DPOLT platform. Additionally, we are developing non-core technologies that originated from the discoveries of our scientific team, including LPT3-04, which is a potential weight loss product, and PCMAT, which is a biomarker discovery platform, both of which we believe could provide significant potential opportunities for us.

Our Product Portfolio

We are currently developing or commercializing three primary products or product candidates, including SMaRT Replacement Therapy, ProBiora3, and MU1140-S. Our product portfolio is protected by eight issued U.S. patents and eight filed U.S. patent applications, including patents exclusively licensed from the University of Florida Research Foundation, Inc., or UFRF. We are the exclusive worldwide licensee to the patents for SMaRT Replacement Therapy and MU1140, which are owned by the UFRF. We have retained worldwide commercialization rights to each of these products. Additionally, we believe that our SMaRT Replacement Therapy will qualify for a 12-year exclusivity period in the United States under the recently passed Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act.

1

Table of Contents

| Product/Candidate |

Description |

Application |

Status | |||

| SMaRT Replacement Therapy | Genetically modified strain of S. mutans that does not produce lactic acid | Tooth decay | Second Phase 1 clinical trial | |||

| ProBiora3 | Blend of three beneficial oral probiotic bacteria | Oral health, teeth whitening, breath freshening (humans, companion pets) | Commercial (GRAS) | |||

| MU1140-S | Member of lantibiotic class of antibiotics | Healthcare-associated infections | Preclinical testing | |||

SMaRT Replacement Therapy

SMaRT Replacement Therapy is designed to be a painless, one-time, five-minute topical treatment applied to the teeth that has the potential to offer lifelong protection against tooth decay caused by S. mutans, the principal cause of this disease. We have extensively and successfully tested the SMaRT strain for safety and efficacy in laboratory and animal models, and we are in the process of commencing a second Phase 1 clinical trial with an attenuated version of our SMaRT Replacement Therapy.

Market Opportunity

Dental diseases are the most prevalent chronic infectious diseases in the world, affecting up to 90% of schoolchildren and the vast majority of adults. Annual expenditures on the treatment of dental caries in the U.S. are estimated to be $40 billion a year according to the Dental, Oral and Craniofacial Data Resource Center. Tooth decay is characterized by the demineralization of enamel and dentin, eventually resulting in the destruction of the teeth. Dietary sugar is often misperceived as the cause of tooth decay; however, the immediate cause of tooth decay is lactic acid produced by microorganisms that metabolize sugar on the surface of the teeth. Studies suggest that of the approximately 700 oral microorganisms, S. mutans, a bacterium found in virtually all humans, is the principal causative agent in the development of tooth decay. Residing within dental plaque on the surface of teeth, S. mutans derives energy from carbohydrate metabolism as it converts dietary sugar to lactic acid which, in turn, promotes demineralization in enamel and dentin, eventually resulting in a cavity. The rate at which mineral is lost depends on several factors, most importantly the frequency and amount of sugar that is consumed.

Fluoride is used to reduce the effect of lactic acid-based demineralization of enamel and dentin. Despite the widespread use of fluoride in public water systems, toothpastes, dental treatments and sealants, and antiseptic mouth rinses, over 50% of 5-to-9-year-olds and almost 80% of 17-year-olds in the United States have at least one cavity or filling, according to the U.S. Surgeon General. In addition to non-compliance with the behavioral guidelines of the American Dental Association such as routine brushing and flossing, there are several factors that are likely to increase the incidence and frequency of tooth decay, including increasing consumption of both dietary sugar and bottled water. Bottled water generally does not contain fluoride, and thus does not impart any of the protective effects of fluoridated water from public systems. In 2008, U.S. consumers drank more bottled water than any other alcoholic or non-alcoholic beverage, with the exception of carbonated soft drinks, according to the Beverage Marketing Corporation.

Our Solution

Our replacement therapy technology is based on the creation of a genetically altered strain of S. mutans, called SMaRT, which does not produce lactic acid. Our SMaRT strain is engineered to have a selective colonization advantage over native S. mutans strains in that SMaRT produces minute amounts of a lantibiotic that kills off the native strains but leaves the SMaRT strain unharmed. Thus SMaRT Replacement Therapy can permanently replace native lactic acid-producing strains of S. mutans in the oral cavity, thereby potentially providing lifelong protection against the primary cause of tooth decay. The SMaRT strain has been extensively and successfully tested for safety and efficacy in laboratory and animal models.

2

Table of Contents

SMaRT Replacement Therapy is designed to be applied topically to the teeth by a dentist, pediatrician or primary care physician during a routine office visit. A suspension of the SMaRT strain is administered using a cotton-tipped swab during a single five-minute, pain-free treatment. Following treatment, the SMaRT strain should displace the native, decay-causing S. mutans strains over a six to twelve month period and permanently occupy the niche on the tooth surfaces normally occupied by native S. mutans.

Tooth decay is a largely preventable disease through implementation of an appropriate oral care hygiene program including brushing, flossing, irrigation, sealants and antiseptic mouth rinses. Nevertheless, tooth decay remains the most common chronic infectious disease in the world, which indicates that the lack of patient compliance with an overall oral care regimen remains a critical issue in tooth decay prevention. We believe that SMaRT Replacement Therapy addresses the issue of patient compliance by requiring only a one-time,five-minute treatment for the potential lifelong prevention of tooth decay.

Regulatory Status

We initiated our first Phase 1 clinical trial in April 2005, but we found it difficult to find subjects who fit the trial’s highly cautious inclusion and exclusion criteria, particularly with respect to the subjects’ lack of dentition. We concluded this trial early after enrolling only two of the 15 planned subjects. The FDA then recommended that we revise the protocol for the evaluation of ten healthy male subjects, ranging from 18 to 30 years old and with normal dentition, in an institutionalized setting. After we submitted additional information, the FDA issued a clinical hold letter in June 2007 for the proposed trial with the attenuated strain, citing the need for a plan with respect to serious adverse effects; a plan for the eradication of the attenuated strain in trial subjects’ offspring; and a required pregnancy test for female partners of subjects. We submitted additional protocols in response to the FDA’s concerns. In August 2007, the FDA issued a clinical hold letter with required revisions to the protocol for offspring of subjects. We submitted a response to the clinical hold letter in September 2007, and the FDA removed the clinical hold for our Phase 1 trial in the attenuated strain in October 2007.

We have commenced a second Phase 1 clinical trial of an attenuated version of our SMaRT Replacement Therapy, which will examine the safety and genetic stability of the SMaRT strain during administration to ten healthy adult male subjects over a two-week period. As a precautionary measure, this trial will use an attenuated version of the SMaRT strain that is dependent on D-alanine, which is a specific amino acid not normally found in the human diet. D-Alanine will be administered though a mouthwash provided to the patient group, and must be administered daily or the attenuated strain will perish in the oral cavity. We expect the second Phase 1 clinical trial of the attenuated strain, including a six-month follow-up examination of subjects, to be concluded in the second half of 2011. If the second Phase 1 trial of the attenuated strain is successful and if the FDA lifts the clinical hold on the IND for the non-attenuated version of the SMaRT strain, we anticipate that we would conduct a third Phase 1 trial using the non-attenuated SMaRT strain instead of the attenuated version.

The SMaRT strain has been extensively and successfully tested in the laboratory as well as in animal models, and has demonstrated the following:

| • | No lactic acid creation under any cultivation conditions tested; |

| • | Dramatically reduced ability to cause tooth decay; |

| • | Genetic stability as demonstrated in mixed culture and biofilm studies and in rodent model studies; |

| • | Production of a level of MU1140 that is comparable to its wild-type parent strain, which was previously shown to readily and persistently colonize the human oral cavity; and |

| • | Aggressive displacement of native, decay-causing strains of S. mutans and preemptive colonization of its niche on the teeth of laboratory rats. |

3

Table of Contents

In addition, during preclinical and early-stage clinical testing of our SMaRT Replacement Therapy, we observed the following:

| • | No adverse side effects in either acute or chronic testing in rodent models; |

| • | Colonization of the treated subjects following a five-minute application of SMaRT Replacement Therapy in our first Phase 1 study using the attenuated strain; and |

| • | No adverse side effects during our first Phase 1 study. |

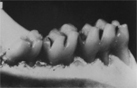

We conducted a preclinical study in which one group of rats was treated with the native S. mutans strain, and a second group of rats was treated with the SMaRT strain. Both groups of rats were subsequently fed a high-sugar diet for eight weeks. The group of rats treated with the SMaRT strain showed dramatically increased protection from tooth decay as compared to the group of rats treated with native S. mutans.

Rodent Teeth Treated with Native S. mutans (left) and SMaRT Strain (right)

|

|

Our Strategy

Our strategy is to develop our SMaRT Replacement Therapy through Phase 1 clinical trials. Upon the successful completion of Phase 1 trials, we intend to license our SMaRT Replacement Therapy to, or partner with, a major pharmaceutical company. We believe that the completion of Phase 1 trials would definitively establish clinical safety and therefore would represent a significant milestone in the development of SMaRT Replacement Therapy, which we anticipate would result in a substantial increase in the value of this technology. If we are unable to negotiate acceptable terms with a licensee or partner after Phase 1 trials have been completed, and assuming we are not required to undertake Phase 2 trials, we may consider pursuing Phase 3 clinical trials independently. However, we anticipate that we would need to partner with a major pharmaceutical company prior to marketing the product if our SMaRT Replacement Therapy ultimately achieves FDA approval. For our second Phase 1 clinical trial we have retained PRA International as the clinical research organization for clinical trials management services.

Manufacturing

The manufacturing methods for producing the SMaRT strain of S. mutans are standard Good Manufacturing Practice, or GMP, fermentation techniques. These techniques involve culturing bacteria in large vessels and harvesting them at saturation by centrifugation or filtration. The cells are then freeze dried or suspended in a pharmaceutical medium appropriate for application in the human oral cavity. These manufacturing methods are commonplace and readily available within the pharmaceutical industry. A single dose of our SMaRT Replacement Therapy contains approximately 10 billion S. mutans cells, which represents approximately 10 milliliters of fermentation product. The SMaRT strain grows readily in a variety of cultivation media and under a variety of common growth conditions including both aerobic and anaerobic incubations. The SMaRT strain can also utilize various carbon and nitrogen sources and is highly acid tolerant. There is no significant limitation to the manufacturing scale of our SMaRT strain other than the size of the containment vessel. For our first Phase 1 clinical trial, we engaged a contract manufacturer to produce an attenuated version our SMaRT strain, using a standard operating procedure provided by us that we believe is readily transferable to outside contract manufacturers with fermentation capabilities.

4

Table of Contents

ProBiora3

ProBiora3 is a proprietary blend of three naturally occurring strains of beneficial bacteria, including Streptococcus oralis, Streptococcus uberis, and Streptococcus rattus, which promote fresher breath, whiter teeth, and support overall oral health. We believe that ProBiora3 is the most comprehensive oral probiotic technology currently available in the oral care market. The scientific basis for the oral health and cosmetic benefits provided by these three strains of bacteria has been documented in numerous peer-reviewed publications over the last 30 years. We promote ProBiora3 as the active ingredient in our over-the-counter consumer branded products, including EvoraPlus, EvoraKids, Teddy’s Pride and the professional branded product, EvoraPro. EvoraPlus and EvoraKids are flavored probiotic tablets intended for twice-daily use by adults and children, respectively, after brushing their teeth. Teddy’s Pride is intended for companion pets such as cats and dogs, and comes in powder form, which is odorless and tasteless. The powder is intended to be sprinkled on a pet’s food once per day. EvoraPro is a professional strength product designed for the dental office channel. In addition to our house-branded products, we also market ProBiora3 as an active ingredient for private label products, as well as in bulk for licensing applications.

Market Opportunity

Probiotics are live microorganisms that confer a health benefit to their host when administered in sufficient amounts. The beneficial bacteria in a probiotic formulation help to maintain a healthy balance of bacteria in the body. Examples of common probiotic applications are yogurt containing live cultures, a-cidophilus capsules to improve digestion, and products for improved immune system and vaginal and urinary tract health. According to MarketsandMarkets, the global probiotics market is expected to reach $31.2 billion by 2014, representing a CAGR of 12.6% from 2009 to 2014. Probiotics products are relatively more common in Asia and Europe, with Europe accounting for nearly 42% and Asia accounting for 30% of the global market. The probiotics market in the United States, however, is emerging, and products that address gastrointestinal problems and other uses are rapidly becoming available, especially as dietary supplements and cultured foods and beverages. The Probiotic Foods & Beverages category currently represents over 75% of the overall probiotics market in the United States.

| • | Oral Care: The oral care market in the United States was $9.1 billion in 2008 and is expected to reach $10.9 billion by 2014, according to Packaged Facts. Packaged Facts segments this market into three comprehensive product categories: (i) Dental Preparations, which include toothpastes, tooth cleaners/whiteners, and denture products; (ii) Implements/Appliances, including toothbrushes, dental floss and irrigators; and (iii) Gum/Mouthwash/Breath Fresheners, which represented $2.4 billion of the market in 2009. |

| • | Companion Pets: In 2009, approximately 62% of U.S. households owned a pet, with an estimated 38.2 million and 45.6 million households owning cats and dogs, respectively, according to the American Pet Products Association, or APPA. The APPA also estimates that total 2010 U.S. pet industry expenditures were $47 billion, representing an increase of 4.3% from 2009. Within this market, approximately $10.4 billion was spent on Supplies/OTC Medicine, representing a 4.0% increase over 2009. |

Our Solution

ProBiora3 is a blend of three naturally occurring strains of bacteria for use in the promotion of oral health, including Streptococcus oralis strain KJ3SM, or S. oralis; Streptococcus uberis strain KJ2SM, or S. uberis; and Streptococcus rattus strain JH145SM, or S. rattus. In a healthy human oral cavity, S. oralis and S. uberis are commonly found in significant amounts, and conversely, the levels of bacteria associated with periodontal disease are usually quite low. The opposite situation prevails in periodontal disease sites, at which the beneficial bacteria S. oralis and S. uberis are usually undetectable. Our scientists have demonstrated that S. oralis and S. uberis produce hydrogen peroxide, which interferes with the growth of certain potentially harmful periodontal bacteria, and also gently and naturally whitens teeth. The third bacterial strain in our ProBiora3 blend, S. rattus, is able to establish and maintain a healthy balance of bacteria on the tooth surfaces by competing with certain other potentially harmful bacteria associated with tooth decay.

ProBiora3 has been extensively tested for safety and efficacy in the laboratory and in animal and human trials. In our pilot human study, a twice-daily administration of ProBiora3 was well tolerated by subjects and no safety issues were observed. ProBiora3 produced substantial decreases in the numbers of key potentially pathogenic bacteria associated with tooth decay and periodontal disease in young healthy adults.

5

Table of Contents

We market products containing ProBiora3 under our own house brand names, and have branded ProBiora3 as an active ingredient for licensing and private labeling. Our house brand products contain different ratios, or blends, of the three natural strains contained in ProBiora3, which vary depending on the intended use of the product. Our ProBiora3 products are designed for repetitive use in order to achieve the intended benefits, which we believe provides us with the potential for recurring revenues as consumers who continue to seek the benefits of our products will continue to make purchases. Our ProBiora3 products include:

| • | EvoraPlus: a product with equal weight of all three strains that is optimally designed for the general consumer market. EvoraPlus was initially launched in December 2008, but distribution was limited to sales through our own website. In March 2010, we obtained national distribution for EvoraPlus in the domestic mass retail channel with the addition of Walgreens as a vendor. During 2010 we continued to expand our distribution in the domestic mass retail channel, and we believe that EvoraPlus is currently available for stocking at over 11,000 retail stores. EvoraPlus is a mint-flavored probiotic tablet packaged in a 60-unit box with four 15-dose blister packs, representing a one-month supply. The intended use for EvoraPlus is for consumers to take one tablet twice per day after brushing their teeth. |

| • | EvoraKids: a product that has higher levels of S. rattus, which addresses dental health, but reduced levels of S. oralis and S. uberis since periodontal disease is not typically a pediatric concern. EvoraKids is a fruit-flavored probiotic tablet packaged in a 60-unit box with four 15-dose blister packs, representing a one-month supply. The intended use for EvoraKids is for consumers to take one tablet twice per day after brushing their teeth. We launched distribution of EvoraKids in January 2010. |

| • | Teddy’s Pride: a product that has higher levels of S. oralis and S. uberis, which address tooth staining and breath problems common to dogs and cats, but reduced levels of S. rattus since tooth decay is not typically a concern in companion pets. Teddy’s Pride comes in powder form, which is odorless and tasteless. The powder is intended to be sprinkled on a pet’s food once per day. It is sold in a jar containing a measuring scoop that provides the recommended dosage per application, representing a two-month supply. We launched Teddy’s Pride in October 2009. We anticipate continuing to use our Teddy’s Pride brand internationally and rebrand Teddy’s Pride for the domestic market as EvoraPet. |

| • | EvoraPro: a professional strength version of EvoraPlus that is designed for the dental office channel. EvoraPro is packaged as a ten-dose blister pack and is shrink-wrapped with one box of EvoraPlus. The intended use for EvoraPro is to take one tablet per day for ten days after a routine dental cleaning. EvoraPro can only be purchased from a professional dental office. EvoraPro was launched in early August 2010. |

Package and Delivery Transition

We are continually attentive to the needs of the market and ultimate consumers regarding the use of our ProBiora3 products and as such continue to seek ways to revise and improve on our product delivery mechanisms. For example, we are undergoing a change from a blister pack of 60 tablets to a bottled container of 30 tablets to be taken once daily (as opposed to twice daily) for our consumer ProBiora3 products based on our understanding of customer preferences. Such a change in delivery mechanisms or packaging will result in increased expenses while the change is being implemented. In December 2010, we setup reserves for inventory in the amount of $255,814 and sales returns in the amount of $105,588 to replace our existing inventory and customer held inventory as a result of this change.

Our Regulatory Strategy

We market ProBiora3 as a food ingredient utilizing self-affirmed Generally Recognized as Safe, or GRAS, status. GRAS is available for food products that are generally recognized as being safe for human use and do not claim to treat, prevent, or cure a disease. Furthermore, food products that make only cosmetic or structure-function claims are typically able to enter the market through what is known as self-affirmed GRAS status, which designates that we have performed all necessary research, including the formation of an expert panel to review safety concerns, and are prepared to use these findings to defend ProBiora3’s self-affirmed GRAS status. In 2008, we convened a panel, the members of which we believed to be qualified as experts by their scientific training and professional experience, to analyze and evaluate the safety data for ProBiora3. After review, the panel concluded that the safety data of ProBiora3 was sufficient to support our claim to self-affirmed GRAS status for human consumption. The same data dossier could be applied to support the safety for companion pet consumption of ProBiora3.

6

Table of Contents

Our marketing for ProBiora3 includes the cosmetic claims of teeth whitening and breath freshening, along with the general structure-function claim that ProBiora3 supports oral health. Regulations vary in markets outside the United States and it may be possible to assert other benefits including health and disease prevention claims associated with probiotic use, especially after independent clinical studies have been completed and appropriate regulatory fillings are approved. At present, we are aware of several independent academic studies that have been initiated on a variety of potential health and cosmetic benefits associated with ProBiora3 probiotic use by humans.

Sales, Marketing and Distribution

All of our house-branded ProBiora3 products have been launched and are available through various distribution channels. We have selected our distribution channels by focusing on our potential channel impact, as well as potential return on marketing expenditures.

| • | Mass Retail: The mass retail channel encompasses several sub-channels including large national retail stores, mass drugstore chains, independent drugstores, and grocery stores. In order to develop and manage this channel, we retained a team of independent manufacturers’ representatives with industry expertise and strong relationships with the buyers for many of the large national mass retailers. We worked with this team to identify the mass drugstore channel as the lead sub-channel in the overall mass retail channel. Mass drugstores are typically the first to adopt a new wellness-related product or technology, and once mass drugstores adopt such a product, other sub-channels typically follow. In March 2010 we received an initial order from Walgreens for EvoraPlus, and in April 2010, we received an initial order from Rite Aid for EvoraPlus. In addition to these mass drugstore chains, we received initial orders for EvoraPlus from a number of larger national and regional mass retailers, including GNC, Kroger, A&P Supermarkets, Pathmark, Albertsons Supermarkets, Sweetbay Supermarkets, Fred Meyer, Winn Dixie, Meijers, Harris Teeter and Hannaford Supermarkets, among others. While we were pleased with the level of initial success we achieved in establishing the mass retail distribution channel, the maintenance, continued use and expansion of this channel requires us to commit to expend capital resources on advertising and marketing campaigns. Because our available capital resources currently limit our ability to engage in significant advertising and marketing campaigns, we are undertaking an evaluation of the continued pursuit of the mass retail channel relative to other options. In connection with our ongoing evaluation of this channel in first quarter of 2011 we determined to pull our EvoraPlus product from the store shelves of Rite Aid. Also during the first quarter of 2011, GNC has refocused their strategy on selling higher margin GNC branded products and as such the decision was made to end distribution of our EvoraPlus product. Through this action we reduced our mass retail store presence from approximately 17,000 stores to just over 11,000 stores. |

| • | Direct-to-Consumer: The direct-to-consumer channel encompasses four sub-channels, including (i) Internet sales through our own websites; (ii) direct mail; (iii) direct-response television, or DRTV, which is usually initiated through an infomercial; and (iv) electronic-response television, or ERTV, which entails marketing through television shopping networks such as Home Shopping Network and QVC. |

| i. | Internet sales: We currently operate one corporate website through which we market our branded products direct to the consumer. An “Oragenics Store” provides the consumer with access to purchase our products. We will be initiating in the first quarter of 2011 an affiliate marketing program whereby we will pay external website operators click-through revenues when a customer visits our websites via an affiliate site and subsequently makes a purchase. |

| ii. | Direct mail: We are currently in discussions with one of the largest direct mailers of nutraceutical products in the United States and developing our own direct mail piece for our branded products. |

7

Table of Contents

| iii. | DRTV: We are developing a two-minute spot infomercial for Teddy’s Pride, our pet oral care product, that we expect to test on select networks and in select markets. The infomercial has been designed to promote a direct response from viewers. If tests prove successful and we are able to forecast a positive return on our marketing spend, we would anticipate expanding the geographic area and broadcasting frequency of the infomercial. |

| iv. | ERTV: We have been in discussions with both of the major domestic ERTV operators as well as companies that have established brands on their respective channels. We anticipate consummating one or more ERTV marketing opportunities by the end of second quarter 2011. |

| • | Professional Offices: The professional offices channel encompasses several sub-channels, including (i) the dental professional channel, which includes dentists, orthodontists and dental hygienists; (ii) the veterinarian professional channel; and (iii) the alternative medicine professional channel, which includes chiropractors, massage therapists and occupational therapists, among others. In August 2010, we launched EvoraPro, which is a product exclusively for the dental professional sub-channel. EvoraPro is an extra-strength, probiotic designed to be taken after dental cleaning or treatment. It is coupled with a box of EvoraPlus to be used once the EvoraPro has been exhausted. In January 2011 we entered into a distribution agreement with a leading distributor of products to the dental professional market with approximately 1,500 sales representatives. We have also established an affiliate marketing program through which dental professionals can earn recurring revenues from their patients’ subsequent purchases of EvoraPlus. If successful, we intend on following a similar plan to penetrate the other sub-channels in the professional offices channel. We would look to initiate a campaign in the veterinarian channel by the end of the second quarter 2011. |

| • | Private Label: The private label channel encompasses arrangements whereby we or third-party manufacturers market our products for resale under a third-party’s brand name. We typically establish private labeling arrangements in order to leverage an existing company’s brand equity and distribution channels. The first major private labeling agreement we consummated was with Garden of Life, which is a leading U.S. nutritional supplement products brand. Garden of Life has contracted to sell our EvoraPlus product under the brand name Probiotic Smile. Garden of Life sells exclusively in the health food channel, which includes many stores geographically disbursed around the United States. Oragenics has entered into agreements with Nutrahealth (US) and Pharmaforce (Denmark) for the distribution of product incorporating ProBiora3. Another notable private labeling sub-channel is the multi-level marketing, or MLM, channel. We have been in discussions with a number of large MLM companies regarding private labeling opportunities for our products. |

| • | International: Since the launch of our first product, EvoraPlus, we have entered into exclusive distribution agreements for our products internationally in various geographic locations. For example, we have executed distributorship agreements, with Natural Pharma International (Italy, Slovakia), Australian Pharmaceuticals Industries (Australia, New Zealand), Zooglobe (Poland), Benelux Cosmetics (Belgium, Netherlands, Luxembourg), Vetcom (Korea), Best Supplies (Taiwan), and Celgen. The international distributorship agreements we have entered into to date typically provide for exclusivity and require that the distributors provide upfront payment to us either by irrevocable letters of credit or wire transfers prior to our initiating production and as a result, we believe that we do not bear any credit risk with such agreements. We also require distributors to take possession of product at our manufacturing facility, which substantially reduces our inventory risk. We continually evaluate the effectiveness of these arrangements and may seek to terminate distributorship agreements in which limited purchase activity occurs. |

| • | Licensing/Bulk: The licensing/bulk channel encompasses the incorporation of ProBiora3 as an active ingredient into existing branded products. We have been in discussions with a number of companies regarding the licensing or bulk sale of ProBiora3. |

8

Table of Contents

Manufacturing

When produced, ProBiora3 comes in powder form. ProBiora3 is manufactured by separate fermentation of each of the three strains. The cells are recovered by centrifugation or filtration and freeze dried. Experimentally determined amounts of the resulting powders are blended with natural bulking agents to deliver the proper number of viable cells of each strain per unit weight. ProBiora3 for human use may be incorporated into various delivery vehicles; for example, in the case of EvoraPlus and EvoraKids, flavoring agents are added and the powder is pressed into tablets, which are sealed in blister packs. We are undergoing a change from blister pack tablets to one a day bottled product based on our understanding of customer preferences. In the case of Teddy’s Pride, the powder is not flavored and is simply added in bulk to a plastic container. Freeze-dried cells in ProBiora3-containing products are stable for up to 18 months after manufacture when kept in cool, dry conditions. The cells are revitalized when they come in contact with moisture, for example the saliva present in the oral cavity.

We have contracted with multiple manufacturers to: (i) produce our active ingredient, ProBiora3, (ii) blend and tablet EvoraPlus, EvoraKids, Teddy’s Pride and EvoraPro, and (iii) package our products. Each of our contract manufacturers has the ability to scale production as needed. With each manufacturer, we place orders for components or finished product to be produced for a fixed fee which we are expected to pay upon completion of the manufacturing process. Packaged probiotics products are shipped to us or to a destination specified by us, which is a central distribution center in the case of a mass retail customer or a private label distributor. We currently maintain an inventory of our products for Internet sales and other sales to distributors. We believe our arrangements with our contract manufacturers are satisfactory to meet our current and expected future needs. We have qualified and used at least two contract manufacturers for each step in our manufacturing process, although we do not have a long-term supply agreement or commitment with any of our manufacturers.

MU1140 and Other Lantibiotics

Our lantibiotic, MU1140, was discovered by Dr. Hillman in the course of developing SMaRT Replacement Therapy. MU1140 is a potent antibiotic that is naturally produced by the parent of the SMaRT strain, and we have produced a synthetic version of MU1140 known as MU1140-S. MU1140 is active against all Gram positive bacteria against which it has been tested, including those responsible for a variety of healthcare-associated infections, or HAIs. The key technology that enables our production of MU1140-S is our Differentially Protected Orthogonal Lanthionine Technology, or DPOLT, which is a patented, novel organic chemistry synthesis platform developed by our scientific team. We reported the successful, analytical scale synthesis of MU1140-S using DPOLT in October 2008, and thus achieved what we believe will lead to the first-ever synthetic route to commercial-scale production of lantibiotics.

Market Opportunity

The most common HAIs are caused by drug-resistant bacteria, including methicillin-resistant Staphylococcus aureus, or MRSA; vancomycin-resistant Enterococcus faecalis, or VRE; and Clostridium difficile, or C. diff. According to the Centers for Disease Control and Prevention, or CDC, HAIs are estimated to occur in approximately 5% of all acute-care hospitalizations, based on the 35 million patients admitted to 7,000 acute-care institutions in the United States, with an annual incidence of approximately 1.7 million cases, which result in 99,000 deaths. The CDC also estimates that the total direct medical cost to the U.S. healthcare system from HAIs is between $35.7 billion to $45 billion annually. HAIs are estimated to more than double the mortality and morbidity risks of any admitted patient in a U.S. hospital, which is the equivalent of 350,000 years of life lost annually. The critical care market for antibiotics is approximately $7 billion in the United States alone. Cubicin, a Gram positive lipopeptide antibiotic which was recently introduced by the biotechnology company Cubist, had 2010 sales of $600 million in the United States.

The need for novel antibiotics is increasing as a result of the growing resistance of target pathogens. In 2002, the CDC estimated that pathogenic bacteria resistant to known antibiotics cause between 6.3% and 89.1% of HAIs, and individual hospitals have resistance rates as high as 70% for many Gram positive infections. HAIs are not exclusively a problem in the United States as the rest of the world has also seen a dramatic rise in HAIs during the last decade. Vancomycin, which was introduced in 1956, has served as the last line of defense against certain life-threatening infections, and, more recently, Cubicin has also served in this capacity, but bacterial resistance to these drugs has been growing at an increasing rate. Novel antibiotics have become increasingly scarce as major pharmaceutical companies have focused more research and development resources on lifestyle drugs and fewer resources on specialty pharmaceuticals such as antibiotics. Between 1983 and 1987, 16 new antibiotics were approved by the FDA. Twenty years later, from 2003 to 2007, only five new antibiotics were approved, of which only two possessed a novel mechanism of action.

9

Table of Contents

Lantibiotics such as MU1140 are highly modified peptide antibiotics made by a small group of Gram positive bacterial species. Approximately 50 lantibiotics have been discovered since 1927 when the first lantibiotic, nisin, was discovered. Lantibiotics are known to be potent antibiotic agents, however, all attempts to investigate their usefulness have met with uniform failure due to the inability to produce sufficient pure amounts of any of these molecules to be able to test them as a therapeutic agent for the treatment of infectious diseases. Standard fermentation methods, such as those used to make a variety of other antibiotics, typically result in production of only minute amounts of the lantibiotic. In cases where large amounts of a lantibiotic are made, such as with nisin, the unique chemical structure of lantibiotics has prevented the necessary purification needed for clinical testing.

Our Solution

MU1140 has demonstrated activity against a wide variety of disease-causing Gram positive bacteria, including MRSA, VRE, C. diff., Mycobacterium tuberculosis, or M. tuberculosis, and anthrax. We have performed extensive preclinical testing on MU1140, which has demonstrated the molecule’s novel mechanism of action. In order to produce sufficient quantities for our clinical trials and commercialization efforts, we intend to use a synthetic version of MU1140, known as MU1140-S.

We created MU1140-S using our patented, novel organic chemistry synthesis platform known as DPOLT. We believe that DPOLT will enable large-scale, cost-effective production of clinical grade MU1140-S. We reported the successful, analytical scale synthesis of MU1140-S using DPOLT in October 2008, which we believe will lead to the first-ever synthetic route to commercial-scale production of a lantibiotic. In addition, we believe that DPOLT will allow us to synthetically produce any of the 50 known lantibiotics due to the shared chemical structure features of this class of molecule. We intend to use DPOLT to create a pipeline of lantibiotics for therapeutic use.

Regulatory Status

We have performed extensive preclinical testing using native MU1140, which demonstrated the following features:

| • | Bactericidal activity against Gram positive species and against both replicating and non-replicating M. tuberculosis; |

| • | Unusual chemical structure, which makes it extremely stable; |

| • | No immune response in a variety of animal models, even with the use of strong adjuvants and carriers; |

| • | Negligible toxicity when supra-therapeutic doses were tested in yeast, and fibroblast and kidney cell lines; |

In vivo efficacy in mouse and rat models, in which animals were infected intraperitoneally with MRSA (60xLD50) and MU1140 was administered intravenously at doses well below its maximum tolerated dose;

| • | Novel mechanism of action that involves binding to and abducting Lipid II, which is required for cell wall biosynthesis; |

| • | No spontaneous, genetically stable resistant mutants to MU1140; |

| • | Synergy with an aminoglycoside; and |

| • | Good pharmaceutical properties. |

We expect to conclude the preclinical testing of MU1140-S, including toxicity testing in rodent and non-rodent animal models, during the second half of 2011. Following successful completion of preclinical testing we would expect to file an Investigational New Drug, or IND, application with the FDA in early 2012. We estimate that, once commenced, the regulatory process will require at least four years of clinical testing and the application and FDA approval of a New Drug Application, or NDA, before MU1140-S would be commercially available. We have engaged Celerion (formerly known as MDS Pharma Services) on a fee-for-service basis to represent us in regulatory meetings with the FDA, and to perform the first-in-human trials with MU1140-S.

10

Table of Contents

Our Strategy

We intend to develop MU1140-S through Phase 1 clinical trials. If MU1140-S successfully completes Phase 1 trials, we believe that its value will substantially increase, and we would then seek to license MU1140-S to or partner with a major pharmaceutical company. If we are unable to consummate an acceptable licensing or partnership arrangement, we may pursue Phase 2 clinical trials independently.

Analysis of the 50 known lantibiotics suggests that there are possibly six to ten subclasses of lantibiotics as classified by known mechanisms of action, spectra of activity, or structural characteristics. In addition to MU1140-S, we intend to utilize DPOLT to synthesize additional lantibiotics of interest in the future.

Manufacturing

We have retained Almac Sciences, a leading contract manufacturer, to refine and scale-up GMP production of MU1140-S. Through this relationship, we expect to have access to sufficient amounts of MU1140-S during the first half of 2011 which will enable preliminary testing to demonstrate equivalence between the synthetic and native molecule.

Additional Areas of Development

As part of our past research efforts, we have identified and filed patent applications covering two technologies that we may seek to further develop internally or monetize through a sale, license, or partnership in the future. These areas include LPT3-04, our weight loss product, and PCMAT, our biomarker discovery platform.

Weight Loss Product (LPT3-04)

LPT3-04 is a naturally occurring compound, which is normally consumed in the human diet in small amounts. In the course of our SMaRT Replacement Therapy research, we discovered program that consumption of significantly larger amounts of LPT3-04 resulted in dose-dependent weight loss in experimental animal models. The mechanism of action appears to be induction of apoptosis, or programmed cell death, specifically in white fat cells. LPT3-04 consumption in the required amounts has been shown to be safe in humans. Anecdotally, weight loss has been observed in human volunteers. Due to the natural sweetness of LPT3-04 and the relatively large amounts of it that need to be consumed on a daily basis to achieve the desired weight loss effect, current product development efforts are focused on incorporating the compound into bars, milkshakes, and other food products. We expect to use these food products in a blinded placebo-controlled study to begin in 2011. We have submitted a patent application for the use of LPT3-04 for weight regulation with the United States Patent and Trademark Office, or U.S. PTO.

Biomarker Discovery Platform (PCMAT)

Our biomarker discovery platform is based on our Proteomics-based Change Mediated Antigen Technology, or PCMAT, and was discovered by members of our scientific team while searching for protein targets associated with the diagnosis of periodontal disease. This technology rapidly identifies proteins that are expressed when a cell undergoes any sort of change. Such proteins are excellent targets for medical diagnostics and therapeutic strategies. PCMAT is able to identify proteins shed from diseased tissues into bodily fluids such as blood, saliva and urine. We believe that PCMAT is faster, more cost-efficient and significantly more sensitive than competing technologies such as differential proteomics and microarrays. In addition, our technology uses the actual diseased host rather than an animal model, so that biomarkers that we discover are more likely to be of high clinical value. We have identified several widespread disease states that we intend to pursue. If we are able to discover protein targets with sufficient degrees of sensitivity and specificity, we intend to license these targets to major pharmaceutical or medical diagnostics companies.

Our In-Licensed Technology Agreements

SMaRT Replacement Therapy

We have exclusively licensed the intellectual property for our replacement therapy technology from the University of Florida Research Foundation, Inc., or the UFRF. The original license agreement was dated August 4, 1998 and was subsequently amended on September 15, 2000, July 10, 2002, September 25, 2002 and March 17, 2003. The amended license agreement provides us with an exclusive worldwide license to make, use and sell products and processes covered by Patent No. 5,607,672, entitled “Replacement Therapy for Dental Caries”, which was filed in the U.S. PTO on June 7, 1995 and made effective on March 4, 1997. The patent will expire on June 7, 2015. Our license is for the period of the patent, subject to the performance of terms and conditions contained therein. The patent covers the genetically altered strain of S. mutans which does not produce lactic acid, a pharmaceutical composition for administering the genetically altered strain and the method of preventing tooth decay by administering the strain. See “Our Intellectual Property.”

11

Table of Contents

We issued 29,997 shares of our common stock to the UFRF as partial consideration for the initial license.

MU1140

We have exclusively licensed the intellectual property for our MU1140 lantibiotic technology from the UFRF. The original license agreement was dated June 22, 2000 and was subsequently amended on September 15, 2000, July 10, 2002, September 25, 2002 and March 17, 2003. The amended license agreement provides us with an exclusive worldwide license to make, use and sell products and processes covered by Patent No. 5,932,469 entitled “Antimicrobial Polypeptide, Nucleic Acid and Methods of Use.” Our license is for the period of the patent, subject to the performance of terms and conditions contained therein. See “Our Intellectual Property.”

Additional Terms of License Agreements

In the amended license agreements for SMaRT Replacement Therapy and MU1140 the UFRF has reserved the right to use and sell products and services for research purposes only. The amended license agreements also provide the UFRF with a license, for research purposes only, to any improvements that we make to the products and processes covered by the patents.

We are obligated to pay 5% of the selling price of any products developed from the licensed technologies that we may sell as royalty to the UFRF. In addition, if we sublicense any rights granted by the amended license agreements, we are obligated to pay the UFRF 20% of all revenues received from the sublicenses, excluding monies received solely for development costs.

We are also obligated to make minimum annual royalty payments to the UFRF for the term of the amended license agreement in the amount of $50,000 by the end of each year for each license agreement. The minimum royalty payments are required to be paid in advance on a quarterly basis. For the SMaRT Replacement Therapy and MU1140 minimum royalty payments, we must pay the UFRF an aggregate of $100,000 which is required to be paid in equal quarterly installments of $25,000.

Under the terms of the amended license agreements, in each calendar year and in addition to the royalty payment obligations, we are obligated to spend, or cause to be spent, an aggregate of $1,000,000 on the research, development, and regulatory prosecution of our SMaRT Replacement Therapy and MU1140 technologies combined, until a product which is covered wholly or partially by the claims of the patent, or is manufactured using a process which is covered wholly or partially by the claims of the patent, is sold commercially. If we fail to make these minimum research and development expenditures, the UFRF may terminate our license agreement.

We must also pay all patent costs and expenses incurred by the UFRF for the preparation, filing, prosecution, issuance and maintenance of the patent.

We have agreed to indemnify and hold the UFRF harmless from any damages caused as a result of the production, manufacture, sale, use, lease, consumption or advertisement of the product.

We are required to maintain liability insurance coverage appropriate to the risk involved in marketing our products. Our liability insurance has been renewed through March 2012, however, there is no assurance that we can obtain continued coverage on reasonable terms.

The amended license agreements further provide that the U.S. government funded research grant No. RO1 DE04529 during the course of or under which the licensed inventions covered by the patent were conceived. As such the U.S. government is entitled, as a right, to a nonexclusive, nontransferable, irrevocable, paid-up license to practice or have practiced the inventions of such patents for governmental purposes.

In order to protect our license rights and their patents, we or the UFRF may have to file lawsuits and obtain injunctions. If we do that, we will have to spend large sums of money for attorney fees in order to obtain the injunctions. Even if we do obtain the injunctions, there is no assurance that those infringing on our licenses or the UFRF’s patents will comply with the injunctions. Further, we may not have adequate funds available to prosecute actions to protect or to defend the licenses and patents, in which case those infringing on the licenses and patents could continue to do so in the future.

12

Table of Contents

Government Regulations

The formulation, manufacturing, processing, packaging, labeling, advertising, distribution and sale of our products are subject to regulation by federal agencies, including, but not limited to the Food and Drug Administration, or FDA, and the Federal

Trade Commission, or FTC. These activities also are regulated by various agencies of the states, localities and foreign countries in which our products are sold. In particular, the FDA, under the Federal Food, Drug, and Cosmetic Act, or FDCA, regulates the safety, manufacturing, labeling and distribution of drugs, medical devices, food, and dietary supplements. In addition, the FTC has primary jurisdiction to regulate the advertising of drugs, medical devices, food and dietary supplements.

In foreign countries these same activities may be regulated by Ministries of Health, or other local regulatory agencies. The manner in which products sold in foreign countries are registered, how they are formulated, or what claims may be permitted may differ from similar products and practices in the United States.

FDA Regulation—Food

Under the FDCA, the FDA is responsible for ensuring that foods are safe, wholesome, and correctly labeled. The FDA enforces statutory prohibitions against misbranded and adulterated foods, and establishes safety standards for food processing and ingredients, manufacturing procedures for processed foods, and labeling standards for food products.

All facilities engaged in manufacturing, processing, packing or holding food for consumption in the United States must be registered with FDA before such activities begin. Those who manufacture, package, or hold food must comply with the Good Manufacturing Practices, or GMPs, for foods. The GMPs describe the methods, equipment, facilities, and controls for producing processed food, including requirements for personnel such as education, training and cleanliness requirements; proper maintenance and sanitization of buildings, facilities, and equipment; and processes and controls.

Acceptable claims for foods fall into three categories: health claims, structure/function claims and nutrient content claims. Health claims describe a relationship between a food, food component, or dietary ingredient and reducing the risk of a disease or health-related condition. The FDA authorizes these types of health claims based on an extensive review of the scientific literature, generally as a result of the submission of a health claim petition. Manufacturers also may make certain health claims based on “authoritative statements” from a scientific body of the U.S. Government or the National Academy of Sciences. Structure/function claims describe the role of a nutrient or dietary ingredient intended to affect or maintain normal structure or function of the body, and may characterize the means by which a nutrient or dietary ingredient acts to maintain such structure or function. Nutrient content claims expressly or by implication characterize the level of a nutrient in a food, by using terms such as “free,” “high” or “low.” The FDA’s regulations define the nutrient content claims that may be used and the requirements for making such claims.

Labels for food must not be false or misleading. Required information for labels includes the name of the food, the net quantity, the name and address of the manufacturer, packer or distributor, the ingredient list, and a Nutrition Facts label. In addition to the information required to be in a Nutrition Facts label, other nutrients must be included in the Nutrition Facts label if the nutrients are added as a nutrient supplement to the food, if the label makes a nutrition claim about them, or if advertising or product literature connects the nutrients to the food. The FDA considers information that is required or permitted in the Nutrition Facts label, on the front label or elsewhere on the package to be a nutrition content claim. In such cases, the package label must comply with the regulations for nutrient content claims.

Under the FDCA, any substance that is intentionally added to food is a food ingredient, which is subject to premarket review and approval by the FDA, unless the substance is Generally Recognized As Safe, or GRAS, which means that the substance is generally recognized, among qualified experts, as having been adequately shown to be safe under the conditions of its intended use, or unless the use of the substance is otherwise excluded from the definition of a food ingredient. Under FDA’s regulations, the use of a food substance may be GRAS either through scientific procedures that may be voluntarily submitted to the FDA, or, for a substance used in food before 1958, through experience based on common use in food. General recognition of safety through scientific procedures requires the same quantity and quality of scientific evidence as required to obtain approval of the substance as a food ingredient and ordinarily is based upon published studies, which may be corroborated by unpublished studies and other data and information. General recognition of safety through experience based on common use in foods requires a substantial history of consumption for food use by a significant number of consumers. To be considered “safe” for its intended use, there must be a reasonable certainty in the minds of competent scientists that the substance is not harmful under its intended conditions of use. The specific data and information that demonstrate safety depend on the characteristics of the substance, the estimated dietary intake, and the population that will consume the substance.

13

Table of Contents

Registered food facilities that manufacture, process, pack, or hold food for human or animal consumption in the United States are required to submit a report to the FDA’s Reportable Food Registry, or RFR, when there is a reasonable probability that the use of, or exposure to, an article of food will cause serious adverse health consequences or death. The RFR covers all foods regulated by FDA except infant formula and dietary supplements. Registered facilities must report as soon as practicable, but in no case later than 24 hours after it is determined that an article of food is a reportable food.

FDA Regulation—Dietary Supplements

The Dietary Supplement Health and Education Act of 1994, or DSHEA, amended the FDCA by establishing regulatory standards with respect to dietary supplements, and defining dietary supplements as a new category of food. Dietary supplements include vitamins, minerals, amino acids, nutritional supplements, herbs and botanicals intended for ingestion that are labeled as dietary supplements and are not represented for use as a conventional food or as a sole item of a meal or the diet. Under DSHEA, a firm that manufactures or distributes dietary supplements must determine that such products are safe and that any representations or claims made about the products are substantiated by adequate evidence to show that the claims are not false or misleading.

DSHEA does not require manufacturers or distributors to seek approval from the FDA before producing or selling a dietary supplement unless the supplement contains one or more ingredients that are considered to be a “new dietary ingredient.” A “new dietary ingredient” is one that was not marketed in the United States before October 15, 1994. The manufacturer or distributor of a dietary supplement that contains a “new dietary ingredient” must provide the FDA with information, including any citations to published articles, demonstrating why the ingredient is reasonably expected to be safe for use in a dietary supplement at least 75 days before the dietary supplement is introduced or delivered for introduction into interstate commerce. This requirement does not apply if the ingredient has been recognized as a food substance and is present in the food supply.

Because dietary supplements are foods, manufacturers of dietary supplements must register the facilities where the supplements are manufactured, processed, packed or held with the FDA before such activities begin. Those who manufacture, package or hold dietary supplements also must comply with GMPs for dietary supplements. According to the GMPs, dietary supplements must be prepared, packaged, labeled and held in compliance with specific requirements, including detailed quality control requirements, such as those for maintaining and cleaning facilities and instruments, hiring and training personnel and ensuring the appropriate manufacturing environment, testing requirements, recordkeeping requirements and handling of customer complaints. Anyone who manufactures, packages, labels or holds dietary supplements must evaluate and ensure the identity, purity, strength and composition of the products. FDA regulations also require that certain information appear on dietary supplement labels, including the name of the dietary supplement, the amount of the dietary supplement, nutrition labeling, a complete list of ingredients and the name and place of business of the manufacturer, packer or distributor. Manufacturers must ensure, and have substantiation showing, that claims made about dietary supplements are truthful and not misleading. Acceptable claims for dietary supplements are the same as those for conventional foods: health claims, structure/function claims and nutrient content claims. However, additional requirements apply to manufacturers of dietary supplements who make structure/function claims. Manufacturers of dietary supplements must notify the FDA of any structure/function claims made for a dietary supplement within 30 days of first marketing the product with the identified claims. A dietary supplement that includes a structure/function claim on its labeling is also required to bear a prescribed disclaimer: “This statement has not been evaluated by the Food and Drug Administration. This product is not intended to diagnose, treat, cure or prevent any disease.” The manufacturer, packer, or distributor of a dietary supplement must submit to the FDA any report it receives of a serious adverse event associated with the dietary supplement when used in the United States, accompanied by a copy of the label of the dietary supplement, no later than 15 business days after the report is received. A “serious adverse event” is an adverse event that results in death, a life-threatening experience, inpatient hospitalization, a persistent or significant disability or incapacity, a congenital anomaly or birth defect, or requires, based on a reasonable medical judgment, medical or surgical intervention to prevent such outcomes.

The FDA may take action to restrict use of a dietary supplement or to remove it from the marketplace if the agency believes the supplement presents a significant or unreasonable risk of illness or injury under conditions of use suggested in the labeling or under ordinary conditions of use. Under DSHEA, the FDA bears the burden of proof to show that a dietary supplement presents a significant or unreasonable risk of illness or injury. The FDA also may take enforcement action against a dietary supplement manufacturer or distributor for unlawful promotion of a dietary supplement, such as making claims that a supplement treats, prevents or cures a specific disease or condition. These claims would subject the dietary supplement to regulation as a drug product. If dietary supplements do not meet applicable requirements, the manufacturer may need to undertake a voluntary recall.

14

Table of Contents

FDA Regulation—Biological Products and New Drug Products

Under the FDCA all new drugs and biological products are subject to pre-market approval by the FDA. In contrast to chemically synthesized small molecular weight drugs, which have a well-defined structure and can be thoroughly characterized, biological products are generally derived from living material—human, animal, or microorganism—are complex in structure, and thus are usually not fully characterized. Biological products include blood-derived products, vaccines, in vivo diagnostic allergenic products, immunoglobulin products, products containing cells or microorganisms, and most protein products. Biological products subject to the Public Health Service, or PHS, Act also meet the definition of drugs under the FDCA, therefore both biological products and drugs are regulated under provisions of the FDCA. However, only biological products are licensed under the PHS Act. The overall development process for biological products is similar to that for drugs. The steps ordinarily required before a biological product or new drug may be marketed in the United States include:

| • | completion of preclinical studies according to Good Laboratory Practice, or GLP, regulations; |

| • | the submission of an IND application to the FDA, which must become effective before human clinical trials may commence; |