Attached files

| file | filename |

|---|---|

| EX-21.1 - Merriman Holdings, Inc | v216411_ex21-1.htm |

| EX-31.1 - Merriman Holdings, Inc | v216411_ex31-1.htm |

| EX-32.1 - Merriman Holdings, Inc | v216411_ex32-1.htm |

| EX-31.2 - Merriman Holdings, Inc | v216411_ex31-2.htm |

| EX-23.1 - Merriman Holdings, Inc | v216411_ex23-1.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year ended December 31, 2010

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to ________

Commission File Number 001-15831

MERRIMAN HOLDINGS, INC.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware

|

|

11-2936371

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(IRS Employer

Identification No.)

|

600 California Street, 9th Floor

San Francisco, CA 94108

(Address of principal executive offices)(Zip Code)

(415) 248-5600

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes¨ No¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a “smaller reporting company.” See definition of “accelerated filer, large accelerated filer and smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer (Do not check if a smaller reporting company) ¨

|

Smaller Reporting Company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the 1,634,429 shares of common stock of the Registrant issued and outstanding as of June 30, 2010, the last business day of the registrant’s most recently completed second fiscal quarter, excluding 373,362 shares of common stock held by affiliates of the Registrant was $6,292,552. This amount is based on the closing price of the common stock on NASDAQ of $3.85 per share on June 30, 2010.

The number of shares of Registrant’s common stock outstanding as of March 25, 2011 was 2,482,408.

|

PART I

|

|||

|

Item 1.

|

Business

|

|

1

|

|

Item 1A.

|

Risk Factors

|

9

|

|

|

Item 1B.

|

Unresolved Staff Comments

|

22

|

|

|

Item 2.

|

Properties

|

22

|

|

|

Item 3.

|

Legal Proceedings

|

23

|

|

|

Item 4.

|

Reserved

|

||

|

PART II

|

|||

|

Item 5.

|

Market for Registrant’s Common Stock and Related Stockholder Matters

|

25

|

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

28

|

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures about Market Risk

|

47

|

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

48

|

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

98

|

|

|

Item 9A.

|

Controls and Procedures

|

98

|

|

|

Item 9B.

|

Other Information

|

98

|

|

|

PART III

|

|||

|

Item 10.

|

Directors and Executive Officers of the Registrant

|

99

|

|

|

Item 11.

|

Executive Compensation

|

99

|

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management

|

99

|

|

|

Item 13.

|

Certain Relationships and Related Transactions

|

99

|

|

|

Item 14.

|

Principal Accounting Fees and Services

|

99

|

|

|

PART IV

|

|||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

100

|

i

This Annual Report on Form 10-K and the information incorporated by reference in this Form 10-K include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Some of the forward-looking statements can be identified by the use of forward-looking words such as “believes,” “expects,” “may,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates” or “anticipates,” or the negative of those words or other comparable terminology. Forward-looking statements involve risks and uncertainties. You should be aware that a number of important factors could cause our actual results to differ materially from those in the forward-looking statements. We will not necessarily update the information presented or incorporated by reference in this Annual Report on Form 10-K if any of these forward-looking statements turn out to be inaccurate. Risks affecting our business are described throughout this Form 10-K and especially in the section “Risk Factors.” This entire Annual Report on Form 10-K, including the consolidated financial statements and the notes and any other documents incorporated by reference into this Form 10-K, should be read for a complete understanding of our business and the risks associated with that business.

PART I

Item 1. Business

Overview

We are a financial services holding company that primarily provides investment banking, sales and trade execution, and equity research through our primary operating subsidiary, Merriman Capital, Inc. (MC).

MC is an investment bank and securities broker-dealer focused on fast-growing companies and institutional investors. Our mission is to be the leader in researching, advising, financing, trading and investing in fast-growing companies under $1 billion in market capitalization. We originate differentiated equity research, brokerage and trading services primarily to institutional investors, as well as investment banking and advisory services to our fast-growing corporate clients.

We are headquartered in San Francisco, CA, with additional offices in New York, NY. As of December 31, 2010, we had 77 employees. Merriman Capital, Inc. is registered with the Securities and Exchange Commission (SEC) as a broker-dealer and is a member of Financial Industry Regulatory Authority (FINRA) and the Securities Investors Protection Corporation (SIPC).

Liquidity

Merriman Holdings, Inc. (the Company) incurred substantial losses in 2010 and 2009. The Company had net losses of $5,338,000 and $5,462,000 in 2010 and 2009, respectively, and negative operating cash flows of $1,525,000 in 2010 and $12,648,000 in 2009. As of December 31, 2010, the Company had a accumulated deficit of $130,154,000. While the Company believes its current funds will be sufficient to enable it to meet its planned expenditures through at least January 1, 2012, if anticipated operating results are not achieved, management has the intent and believes it has the ability to delay or reduce expenditures so as not to require additional financing sources. Failure to generate sufficient cash flows from operations, raise additional capital, or reduce certain discretionary spending could have a material adverse effect on the Company’s ability to achieve its intended business objectives.

During March 2011, the Company began offering debt which is scheduled to mature three years from the date of issuance and carries an interest rate of 10%, payable quarterly in arrears. In connection with this debt, the Company will also issue warrants to purchase common stock of the Company. These warrants will have a strike price equal to 15% less than the price per share of the Company's common stock on the closing date of the debt offering, which is anticipated to be in April 2011. Each $1 million of debt will be issued with 86,000 warrant shares. As of March 30, 2011, the Company has raised $2 million under this offering.

1

Principal Services

Our investment banking / broker-dealer line of business provides three service offerings: investment banking, institutional brokerage and equity research. We provide traditional research-based financial services to companies with market capitalizations up to $1 billion, which we believe is an underserved sector in the financial services industry.

Investment Banking

Our investment bankers provide a full range of corporate finance and strategic advisory services. Our corporate finance practice is comprised of industry coverage investment bankers that are focused on raising capital for fast-growing companies in selected industry sectors. Our strategic advisory practice tailors solutions to meet the specific needs of our clients at various points in their growth cycle.

Corporate Finance. Our corporate finance practice advises on and structures capital raising solutions for our corporate clients through public and private offerings of primarily equity and convertible debt securities. Our focus is to provide fast-growing companies with the capital necessary to deliver them to the next level of growth. We offer a wide range of financial services designed to meet the needs of fast-growing companies, including initial public offerings, secondary offerings, private investments in public equity (or PIPEs) and private placements. Our equity capital markets team executes underwritten securities offerings, assists clients with investor relations advice and introduces companies seeking to raise capital to investors who we believe will be supportive, long-term investors. Additionally, we draw upon our deep connections throughout the financial and corporate world, expanding the options available for our corporate clients.

Strategic Advisory. Our strategic advisory services include transaction-specific advice regarding mergers and acquisitions, divestitures, spin-offs and privatizations, as well as general strategic advice. Our commitment to long-term relationships and our ability to meet the needs of a diverse range of clients has made us a reliable source of advisory services for fast-growing public and private companies. Our strategic advisory services are also supported by our capital markets professionals, who provide assistance in acquisition financing in connection with mergers and acquisitions transactions.

Institutional Brokerage

We provide institutional sales, sales trading and execution services to institutional customers around the world. We execute securities transactions for money managers, mutual funds, hedge funds, insurance companies, and pension and profit-sharing plans. Institutional investors normally purchase and sell securities in large quantities, which require the distribution and trading expertise we provide.

We provide integrated research and trading solutions centered on assisting our institutional customers in investing profitably, to grow their portfolios and ultimately their businesses. We understand the importance of building long-term relationships with our customers who look to us for the professional resources and relevant expertise to provide answers for their specific situations. We believe it is important for us to assist public companies early in their corporate life cycles. We strive to provide unique investment opportunities in fast-growing, relatively undiscovered companies and to help our institutional customers to execute trades rapidly, efficiently and accurately.

2

Institutional Sales. Our sales professionals focus on communicating investment ideas to our customers and executing trades in securities of companies in our target growth sectors. By actively trading in these securities, we endeavor to couple the capital market information flow with the fundamental information flow provided by our analysts. We believe that this combined information flow is the underpinning of getting our customers favorable execution of investment strategies. Our sales professionals work with our research analysts to provide up-to-date information to our institutional customers. We interface actively with our customers and plan to be involved with our customers over the long term.

Sales Trading. Our sales traders are experienced in the industry and possess in-depth knowledge of both the markets for fast-growing company securities and the institutional traders who buy and sell them.

Trading. Our trading professionals facilitate liquidity discovery in equity securities. We make markets in securities traded on the NASDAQ stock market, other stock exchanges and electronic communication networks, and service the trading desks of institutions in the United States. Our trading professionals have direct access to the major stock exchanges, including the NASDAQ Stock Market, the New York Stock Exchange and the American Stock Exchange.

The customer base of our institutional brokerage business includes mutual funds, hedge funds, and private investment firms. We believe this group of potential customers to number over 4,000. We grow our business by adding new customers and increasing the penetration of existing institutional customers that use our equity research and trading services in their investment process.

Proprietary Trading. We frequently take significant positions in fast-growing companies that we feel are undervalued in the marketplace. We believe that our insights into these opportunities, due to the types of companies we research, offer us a significant competitive advantage.

Corporate & Executive Services. We offer brokerage services to corporations for purposes such as stock repurchase programs. We also serve the needs of company executives with restricted stock transactions, cashless exercise of options, and liquidity strategies.

Venture Services. The Venture Services team provides sales distribution for capital raises for private companies via the introduction to venture capital and private equity investors. Our venture services include distribution and liquidity programs, portfolio company advisory services, research dissemination and best-execution trading.

OTCQX Advisory. MC began offering services to sponsor companies on the International and Domestic OTCQX markets in 2007. In 2008, we solidified our position as the leading investment bank sponsor in this market. We enable non-U.S. and domestic companies to obtain greater exposure to U.S. institutional investors without the expense and regulatory burdens of listing on traditional U.S. exchanges. The International and Domestic OTCQX market tiers do not require full SEC registration and are not subject to the Sarbanes Oxley Act of 2002. Listing on the market requires the sponsorship of a qualified investment bank called a Principal American Liaison (PAL) for non-U.S. companies or a Designated Advisor for Disclosure (DAD) for domestic companies. MC was the first investment bank to achieve DAD and PAL designations. We believe that we are the leading investment bank in the number of listings of issuers on the OTCQX.

3

Equity Research

A key part of our strategy is to originate specialized and in-depth research. We leverage the ideas generated by our research teams, using them to attract and retain institutional brokerage customers. Supported by the firm’s institutional sales and trading capabilities, our research analysts deliver timely recommendations to customers on innovative investment opportunities. In an effort to make money for our investor customers, our analysts are driven to find undiscovered opportunities in fast-growing companies that we believe are undervalued. Given the contrarian and undiscovered nature of many of our research ideas, we, as a firm, specialize in serving sophisticated, aggressive institutional investors.

Our equity research focuses on bottom-up, fundamental analysis of fast-growing companies in selected growth sectors. Our analysts’ expertise in these categories of companies, along with their intensive industry knowledge and contacts, provides us with the ability to deliver timely, accurate and value-added information.

Our objective is to build long lasting relationships with our institutional customers by providing investment recommendations that directly equate to enhanced performance of their portfolios. Further, given our approach and focus on quality service, we believe our equity research analysts, and institutional sales people and sales traders, are in a unique position to maintain close, ongoing communication with our customers.

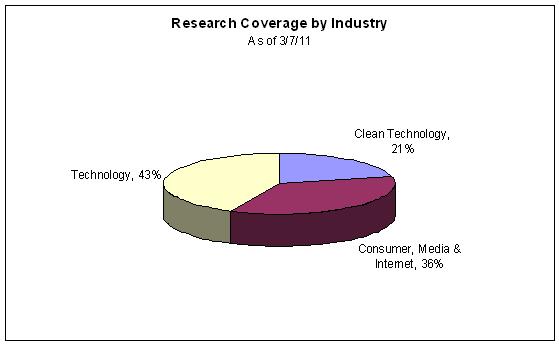

The industry sectors covered by our equity research analysts include:

|

|

·

|

Clean Technology

|

|

|

-

|

Clean Energy Semiconductors

|

|

|

-

|

Infrastructure Technologies and Efficiencies

|

|

|

·

|

Consumer, Media & Internet

|

|

|

-

|

Branded Consumer

|

|

|

-

|

Media/Entertainment

|

|

|

-

|

Internet Media and Infrastructure

|

|

|

·

|

Technology

|

|

|

-

|

Advanced Communications and Industrial Technologies

|

|

|

-

|

Communications - Wireless Technology

|

|

|

-

|

Emerging Data Center and Enterprise Technologies

|

|

|

-

|

Cloud Computing Service Providers

|

After initiating coverage on a company, our analysts seek to effectively communicate new developments to our institutional customers through our sales and trading professionals. We produce full-length research reports, notes and earnings estimates on the companies we cover. We also produce comprehensive industry sector reports. In addition, our analysts distribute written updates on these issuers both internally and to our customers through the use of daily morning meeting notes, real-time electronic mail and other forms of immediate communication. Our customers can also receive analyst comments through electronic media, and our sales force receives intra-day updates at meetings and through regular announcements of developments. All of the above is also available through a password protected searchable database of our daily and historical research archives found on our website at www.merrimanco.com.

Our Equity Research Group annually hosts conferences targeting fast-growing companies and institutional investors, including our annual Investor Summit and other industry sector conferences. We use these events to primarily showcase our equity research to the institutional investment community.

4

Competition

Merriman Capital, Inc. is engaged in the highly competitive financial services and investment industries. We compete with other securities firms - from large U.S.-based firms, securities subsidiaries of major commercial bank holding companies and U.S. subsidiaries of large foreign institutions, to major regional firms, smaller niche players, and those offering competitive services via the Internet. Long term developments in the brokerage industry, including decimalization and the growth of electronic communications networks, or ECNs, have reduced commission rates and profitability in the brokerage industry. Many large investment banks have responded to lower margins within their equity brokerage divisions by reducing research coverage, particularly for smaller companies, consolidating sales and trading services, and reducing headcount of more experienced sales and trading professionals. The trend by competitors to reduce services to address these challenges has created an opportunity for us as many highly qualified individuals have been dislocated, expanding the pool of experienced employees which we might hire.

For a further discussion of the competitive factors affecting our business, see “We face strong competition from larger firms,” under “Item 1A - Risk Factors.”

Corporate Support

Accounting, Administration and Operations

Our accounting, administration and operations personnel are responsible for financial controls, internal and external financial reporting, human resources and personnel services, office operations, information technology and telecommunications systems, the processing of securities transactions, and corporate communications. With the exception of payroll processing, which is performed by an outside service bureau, and customer account processing, which is performed by our clearing broker, most data processing functions are performed internally.

Compliance, Legal, Risk Management and Internal Audit

Our compliance, legal and risk management personnel (together with other appropriate personnel) are responsible for our compliance with legal and regulatory requirements of our investment banking business and our exposure to market, credit, operations, liquidity, compliance, legal and reputation risk. In addition, our compliance personnel test and audit for compliance with our internal policies and procedures. Our general counsel also provides legal service throughout our company, including advice on managing legal risk. The supervisory personnel in these areas have direct access to senior management and to the Audit Committee of our Board of Directors to ensure their independence in performing these functions. In addition to our internal compliance, legal, and risk management personnel, we retain outside consultants and attorneys for their particular functional expertise.

Risk Management

In conducting our business, we are exposed to a range of risks including:

Market risk is the risk to our earnings or capital resulting from adverse changes in the values of assets resulting from movement in equity prices or market interest rates.

Credit risk is the risk of loss due to an individual customer’s or institutional counterparty’s unwillingness or inability to fulfill its obligations.

5

Operations risk is the risk of loss resulting from systems failure, inadequate controls, human error, fraud or unforeseen catastrophes.

Liquidity risk is the potential that we would be unable to meet our obligations as they come due because of an inability to liquidate assets or obtain funding. Liquidity risk also includes the risk of having to sell assets at a loss to generate liquid funds, which is a function of the relative liquidity (market depth) of the asset(s) and general market conditions.

Compliance risk is the risk of loss, including fines, penalties and suspension or revocation of licenses by self-regulatory organizations, or from failing to comply with federal, state or local laws pertaining to financial services activities.

Legal risk is the risk that arises from potential contract disputes, lawsuits, adverse judgments, or adverse governmental or regulatory proceedings that can disrupt or otherwise negatively affect our operations or condition.

Reputation risk is the potential that negative publicity regarding our practices, whether factually correct or not, will cause a decline in our customer base, costly litigation, or revenue reductions.

We have a risk management program which sets forth various risk management policies, provides for a risk management committee and assigns risk management responsibilities. The program is designed to focus on the following:

|

|

·

|

Identifying, assessing and reporting on corporate risk exposures and trends;

|

|

|

·

|

Establishing and revising policies, procedures and risk limits, as necessary;

|

|

|

·

|

Monitoring and reporting on adherence with risk policies and limits;

|

|

|

·

|

Developing and applying new measurement methods to the risk process as appropriate; and

|

|

|

·

|

Approving new product developments or business initiatives.

|

We cannot provide assurance that our risk management program or our internal controls will prevent or mitigate losses attributable to the risks to which we are exposed.

For a further discussion of the risks affecting our business, see “Item 1A Risk Factors.”

Regulation

As a result of federal and state registration and self-regulatory organization, or SRO, memberships, we are subject to overlapping layers of regulation that cover all aspects of our securities business. Such regulations cover matters including capital requirements; uses and safe-keeping of customers’ funds; conduct of directors; officers and employees; record-keeping and reporting requirements; supervisory and organizational procedures intended to ensure compliance with securities laws and to prevent improper trading on material nonpublic information; employee-related matters, including qualification and licensing of supervisory and sales personnel; limitations on extensions of credit in securities transactions; requirements for the registration, underwriting, sale and distribution of securities; and rules of the SROs designed to promote high standards of commercial honor and just and equitable principles of trade. A particular focus of the applicable regulations concerns the relationship between broker-dealers and their customers. As a result, many aspects of the broker-dealer customer relationship are subject to regulation including, in some instances, “suitability” determinations as to certain customer transactions, limitations on the amounts that may be charged to customers, timing of proprietary trading in relation to customers’ trades, and disclosures to customers.

6

As a broker-dealer registered with the SEC, and as a member firm of FINRA, we are subject to the net capital requirements of the SEC (Rule 15c3-1 of the Securities Exchange Act of 1934) as regulated and enforced by FINRA. These capital requirements specify minimum levels of capital, computed in accordance with regulatory requirements that most firms are required to maintain and also limit the amount of leverage that each firm is able to obtain in its respective business.

“Net capital” is essentially defined as net worth (assets minus liabilities, as determined under accounting principles generally accepted in the United States (“U.S. GAAP”), plus qualifying subordinated borrowings, less the value of all of a broker-dealer’s assets that are not readily convertible into cash (such as furniture, prepaid expenses, and unsecured receivables), and further reduced by certain percentages (commonly called “haircuts”) of the market value of a broker-dealer’s positions in securities and other financial instruments. The amount of net capital in excess of the regulatory minimum is referred to as “excess net capital.”

The SEC’s capital rules also (i) require that broker-dealers notify it, in writing, two business days prior to making withdrawals or other distributions of equity capital or lending money to certain related persons if those withdrawals would exceed, in any 30-day period, 30% of the broker-dealer’s excess net capital, and that they provide such notice within two business days after any such withdrawal or loan that would exceed, in any 30-day period, 20% of the broker-dealer’s excess net capital; (ii) prohibit a broker-dealer from withdrawing or otherwise distributing equity capital or making related party loans if, after such distribution or loan, the broker-dealer would have net capital of less than $300,000 or if the aggregate indebtedness of the broker-dealer’s consolidated entities would exceed 1,000% of the broker-dealer’s net capital in certain other circumstances; and (iii) provide that the SEC may, by order, prohibit withdrawals of capital from a broker-dealer for a period of up to 20 business days, if the withdrawals would exceed, in any 30-day period, 30% of the broker-dealer’s excess net capital and if the SEC believes such withdrawals would be detrimental to the financial integrity of the firm or would unduly jeopardize the broker-dealer’s ability to pay its customer claims or other liabilities.

Compliance with regulatory net capital requirements could limit those operations that require the intensive use of capital, such as underwriting and trading activities, and also could restrict our ability to withdraw capital from our broker-dealer, which in turn could limit our ability to pay interest, repay debt, and redeem or repurchase shares of our outstanding capital stock.

We believe that at all times we have been in compliance with the applicable minimum net capital rules of the SEC and FINRA.

The failure of a U.S. broker-dealer to maintain its minimum required net capital would require it to cease executing customer transactions until it came back into compliance, and could cause it to lose its FINRA membership, its registration with the SEC or require its liquidation. Further, the decline in a broker-dealer’s net capital below certain “early warning levels,” even though above minimum net capital requirements, could cause material adverse consequences to the broker-dealer.

We are also subject to “Risk Assessment Rules” imposed by the SEC, which require, among other things, that certain broker-dealers maintain and preserve certain information, describe risk management policies and procedures, and report on the financial condition of certain affiliates whose financial and securities activities are reasonably likely to have a material impact on the financial and operational condition of the broker-dealer. Certain “Material Associated Persons” (as defined in the Risk Assessment Rules) of the broker-dealer and the activities conducted by such Material Associated Persons may also be subject to regulation by the SEC.

In the event of non-compliance by us or our subsidiary with an applicable regulation, governmental regulators and one or more of the SROs may institute administrative or judicial proceedings that may result in censure, fine, civil penalties (including treble damages in the case of insider trading violations), the issuance of cease-and-desist orders, the deregistration or suspension of the non-compliant broker-dealer, the suspension or disqualification of officers or employees, or other adverse consequences. The imposition of any such penalties or orders on us or our personnel could have a material adverse effect on our operating results and financial condition.

7

Additional legislation and regulations, including those relating to the activities of our broker-dealer, changes in rules promulgated by the SEC, FINRA, or other United States, state, or foreign governmental regulatory authorities and SROs or changes in the interpretation or enforcement of existing laws and rules, may adversely affect our manner of operation and our profitability. Our businesses may be materially affected not only by regulations applicable to us as a financial market intermediary, but also by regulations of general application.

Geographic Area

Merriman Holdings, Inc. is domiciled in the United States and most of our revenue is attributed to United States and Canadian customers. In 2007, through our broker-dealer subsidiary, we began advising both international and domestic companies on listing on OTCQX, a prime tier of Pink Sheets.

All of our long-lived assets are located in the United States.

Available Information

Our website address is www.merrimanco.com. You may obtain free electronic copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports on the “Investor Relations” portion of our website, under the heading “SEC Filings.” These reports are available on our website as soon as reasonably practicable after we electronically file them with the SEC. We are providing the address to our Internet site solely for the information of investors. We do not intend the address to be an active link or to otherwise incorporate the contents of the website into this report.

8

Item 1a. Risk Factors

We face a variety of risks in our business, many of which are substantial and inherent in our business and operations. The following are risk factors that could affect our business which we consider material to our industry and to holders of our common stock. Other sections of this Annual Report on Form 10-K, including reports which are incorporated by reference, may include additional factors which could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Risks Related to Our Business

We may not be able to achieve a positive cash flow and profitability.

Our ability to achieve a positive cash flow and profitability depends on our ability to generate and maintain greater revenue while incurring reasonable expenses. This, in turn, depends, among other things, on the development of our investment banking and securities brokerage business, and we may be unable to achieve profitability if we fail to do any of the following:

|

|

·

|

establish, maintain, and increase our customer base;

|

|

|

·

|

manage the quality of our services;

|

|

|

·

|

compete effectively with existing and potential competitors;

|

|

|

·

|

further develop our business activities;

|

|

|

·

|

attract and retain qualified personnel;

|

|

|

·

|

limit operating costs;

|

|

|

·

|

settle pending litigation, and

|

|

|

·

|

maintain adequate working capital

|

We cannot be certain that we will be able to achieve a positive cash flow and profitability on a quarterly or annual basis in the future. Our inability to achieve profitability or positive cash flow could result in disappointing financial results, impede implementation of our growth strategy, or cause the market price of our common stock to decrease. Accordingly, we cannot assure you that we will be able to generate the cash flow and profits necessary to sustain our business.

We have had a number of structural changes to our operations as we divested certain non-core business lines to focus our service and product offerings. Additionally, there have been a number of significant challenges faced by the securities and financial industries in the past three years. As a result of our structural changes and the uncertainty of the current economic environment, the factors upon which we are able to base our estimates as to the gross revenue and the number of participating customers that will be required for us to maintain a positive cash flow are unpredictable. For these and other reasons, we cannot assure you that we will not require higher gross revenue and an increased number of customers, securities brokerage, and investment banking transactions, and/or more time in order for us to complete the development of our business that we believe we need to be able to cover our operating expenses. It is more likely than not that our estimates will prove to be inaccurate because actual events more often than not differ from anticipated events. Furthermore, in the event that financing is needed in addition to the amount that is required for this development, we cannot assure you that such financing will be available on acceptable terms, if at all.

9

There are substantial legal proceedings against us involving claims for significant damages.

There are a number of legal actions against us as described in the Legal Proceedings section below. If we are found to be liable for the claims asserted in any or all of these legal actions, our cash position may suffer such that we are unable to continue our operations. Even if we ultimately prevail in all of these lawsuits, we may incur significant legal fees and diversion of management’s time and attention from our core businesses, and our business and financial condition may be adversely affected. We are attempting to negotiate a settlement with some of the litigants, but there is no assurance of any favorable outcome.

Our exposure to legal liability may be significant, and damages that we may be required to pay and the reputation harm that could result from legal action against us could materially adversely affect our businesses.

We face significant legal risks in our businesses and, in recent years, the volume of claims and amount of damages sought in litigation and regulatory proceedings against financial institutions have been increasing. These risks include potential liability under securities or other laws for materially false or misleading statements made in connection with securities offerings and other transactions, potential liability for “fairness opinions” and other advice we provide to participants in strategic transactions and disputes over the terms and conditions of trading arrangements. We are also subject to claims arising from disputes with employees for alleged discrimination or harassment, among other things. These risks often may be difficult to assess or quantify and their existence and magnitude often remain unknown for substantial periods of time.

Our role as advisor to our clients on important underwriting or mergers and acquisitions transactions involves complex analysis and the exercise of professional judgment, including rendering “fairness opinions” in connection with mergers and other transactions. Therefore, our activities may subject us to the risk of significant legal liabilities to our clients and third parties, including shareholders of our clients who could bring securities class actions against us. Our investment banking engagements typically include broad indemnities from our clients and provisions to limit our exposure to legal claims relating to our services, but these provisions may not protect us or may not be enforceable in all cases.

For example, an indemnity from a client that subsequently is placed into bankruptcy is likely to be of little value to us in limiting our exposure to claims relating to that client. As a result, we may incur significant legal and other expenses in defending against litigation and may be required to pay substantial damages for settlements and adverse judgments. Substantial legal liability or significant regulatory action against us could have a material adverse effect on our results of operations or cause significant reputation harm to us, which could seriously harm our business and prospects.

In the past, following periods of volatility in the market price of a company’s securities, securities class action litigation often has been instituted against many broker-dealers. Such litigation is expensive and diverts management’s attention and resources. We cannot assure you that we will not be subject to such litigation. If we are subject to such litigation, even if we ultimately prevail, our business and financial condition may be adversely affected.

We may not be able to continue operating our business

The Company incurred significant losses in 2010, 2009 and 2008. Even if we are successful in executing our plans, we will not be capable of sustaining losses such as those incurred in 2010. The Company’s ability to meet its financial obligations is highly dependent on market and economic conditions. We also recorded net losses in certain quarters within other past fiscal years. If operating conditions worsen in 2011 or if the Company receives material adverse judgments in its pending litigations, we may not have the resources to meet our financial obligations. If the Company is not able to continue in business, the entire investment of our common stockholders may be at risk, and there can be no assurance that any proceeds stockholders would receive in liquidation would be equal to their investment in the Company, or even that stockholders would receive any proceeds in consideration of their common stock.

Limitations on our access to capital and our ability to comply with net capital requirements could impair our ability to conduct our business

Liquidity, or ready access to funds, is essential to financial services firms. Failures of financial institutions have often been attributable in large part to insufficient liquidity. Liquidity is of importance to our trading business and perceived liquidity issues may affect our customers and counterparties’ willingness to engage in brokerage transactions with us. Our liquidity could be impaired due to circumstances that we may be unable to control, such as a general market disruption or an operational problem that affects our trading customers, third parties or us. Further, our ability to sell assets may be impaired if other market participants are seeking to sell similar assets at the same time.

10

The Company has historically accessed capital markets to raise money through the sale of equity. Holders of our Series D Preferred Stock have certain rights and restrictive provisions which may affect our ability to continue to raise capital through the issuance of additional common stock.

MC, our broker-dealer subsidiary, is subject to the net capital requirements of the SEC and various self-regulatory organizations of which it is a member. These requirements typically specify the minimum level of net capital a broker-dealer must maintain and also mandate that a significant part of its assets be kept in relatively liquid form. Any failure to comply with these net capital requirements could impair our ability to conduct our core business as a brokerage firm. Furthermore, MC is subject to laws that authorize regulatory bodies to prevent or reduce the flow of funds from it to Merriman Holdings, Inc. As a holding company, Merriman Holdings, Inc. depends on distributions and other payments from its subsidiary to fund all payments on its obligations. As a result, regulatory actions could impede access to funds that Merriman Holdings, Inc. needs to make payments on obligations, including debt obligations.

Our financial results may fluctuate substantially from period to period, which may impair our stock price.

We have experienced, and expect to experience in the future, significant periodic variations in our revenue and results of operations. These variations may be attributed in part to the fact that our investment banking revenue is typically earned upon the successful completion of a transaction, the timing of which is uncertain and beyond our control. In most cases we receive little or no payment for investment banking engagements that do not result in the successful completion of a transaction. As a result, our business is highly dependent on market conditions as well as the decisions and actions of our clients and interested third parties. For example, a client’s acquisition transaction may be delayed or terminated because of a failure to agree upon final terms with the counterparty, failure to obtain necessary regulatory consents or board or shareholder approvals, failure to secure necessary financing, adverse market conditions, or unexpected financial or other problems in the client’s or counterparty’s business. If the parties fail to complete a transaction on which we are advising or an offering in which we are participating, we will earn little or no revenue from the transaction.

Due to many factors, including the increased regulatory burden on corporate issuers, there have been fewer initial public offerings of securities of U.S. based companies. Consequently, many fast-growing companies have found a more cost effective method to attract capital through listing on the OTCQX. More companies initiating the process of an initial public offering are also simultaneously exploring merger and acquisition opportunities. If we are not engaged as a strategic advisor in any such dual-tracked process, our investment banking revenue would be adversely affected in the event that an initial public offering is not consummated.

As a result, we are unlikely to achieve steady and predictable earnings on a quarterly basis, which could in turn adversely affect our stock price.

Our ability to retain our professionals and recruit additional professionals is critical to the success of our business, and our failure to do so may materially adversely affect our reputation, business, and results of operations.

Our ability to obtain and successfully execute our business depends upon the personal reputation, judgment, business generation capabilities and project execution skills of our senior professionals, particularly D. Jonathan Merriman, our Co-Founder and Chief Executive Officer of Merriman Holdings, Inc., and the other members of our Executive Committee. Our senior professionals’ personal reputations and relationships with our clients are a critical element in obtaining and executing client engagements. We face intense competition for qualified employees from other companies in the investment banking industry as well as from businesses outside the investment banking industry, such as investment advisory firms, hedge funds, private equity funds, and venture capital funds. From time to time, we have experienced losses of investment banking, brokerage, research, and other professionals and losses of our key personnel may occur in the future. The departure or other loss of Mr. Merriman, other members of our Executive Committee or any other senior professional who manages substantial client relationships and possesses substantial experience and expertise, could impair our ability to secure or successfully complete engagements, or protect our market share, each of which, in turn, could materially adversely affect our business and results of operations. Please see Risk Factor below entitled “If our CEO leaves the Company, additional warrants will be issued, which may further dilute the ownership percentages of the holders of the Company’s Common Stock” for additional information regarding the consequences of the loss of the services of Mr. Merriman.

If any of our professionals were to join an existing competitor or form a competing company, some of our clients could choose to leave. The compensation plans and other incentive plans we have entered into with certain of our professionals may not prove effective in preventing them from resigning to join our competitors. If we are unable to retain our professionals or recruit additional professionals, our reputation, business, results of operations, and financial condition may be materially adversely affected.

11

Our compensation structure may negatively impact our financial condition if we are not able to effectively manage our expenses and cash flows.

Historically, the industry has been able to attract and retain investment banking, research, and sales and trading professionals in part because the business models have provided for lucrative compensation packages. Compensation and benefits are our largest expenditure and the variable compensation component, or bonus, has represented a significant proportion of this expense. The Company’s bonus compensation is discretionary. For 2010, the potential pool was determined by a number of components including revenue production, key operating milestones, and profitability. There is a potential, in order to ensure retention of key employees, that we could pay individuals for revenue production despite the business having negative cash flows and/or net losses.

Pricing and other competitive pressures may impair the revenue and profitability of our brokerage business.

We derive a significant portion of our revenue from our brokerage business. Along with other brokerage firms, we have experienced intense price competition in this business in recent years. Recent developments in the brokerage industry, including decimalization and the growth of electronic communications networks, or ECNs, have reduced commission rates and profitability in the brokerage industry. We expect this trend toward alternative trading systems to continue. We believe we may experience competitive pressures in these and other areas as some of our competitors seek to obtain market share by competing on the basis of price.

In addition, we face pressure from larger competitors, which may be better able to offer a broader range of complementary products and services to brokerage customers in order to win their trading business. As we are committed to maintaining our comprehensive research coverage in our target sectors to support our brokerage business, we may be required to make substantial investments in our research capabilities. If we are unable to compete effectively with our competitors in these areas, brokerage revenue may decline and our business, financial condition, and results of operations may be adversely affected.

Finally, certain large U.S.-based broker-dealer firms operate under capital requirements which are less restrictive than the regulatory capital requirements we face, which puts smaller investment banks such as our Company at a competitive disadvantage in the market place.

We may experience significant losses if the value of our marketable security positions deteriorates.

We conduct active and aggressive securities trading, market making, and investment activities for our own account, which subjects our capital to significant risks. These risks include market, credit, counterparty, and liquidity risks, which could result in losses. These activities often involve the purchase, sale, or short sale of securities as principal in markets that may be characterized as relatively illiquid or that may be particularly susceptible to rapid fluctuations in liquidity and price. Trading losses resulting from such activities could have a material adverse effect on our business and results of operations.

Difficult market conditions could adversely affect our business in many ways.

Difficult market and economic conditions and geopolitical uncertainties have in the past adversely affected and may in the future adversely affect our business and profitability in many ways. Weakness in equity markets and diminished trading volume of securities could adversely impact our brokerage business, from which we have historically generated more than half of our revenue. Industry-wide declines in the size and number of underwritings and mergers and acquisitions also would likely have an adverse effect on our revenue. In addition, reductions in the trading prices for equity securities also tend to reduce the deal value of investment banking transactions, such as underwriting and mergers and acquisitions transactions, which in turn may reduce the fees we earn from these transactions. As we may be unable to reduce expenses correspondingly, our profits and profit margins may decline.

We may suffer losses through our investments in securities purchased in secondary market transactions or private placements.

Occasionally, our Company, its officers and/or employees may make principal investments in securities through secondary market transactions or through direct investment in companies through private placements. In many cases, employees and officers with investment discretion on behalf of our Company decide whether to invest in our account or their personal account. It is possible that gains from investing will accrue to these individuals because investments were made in their personal accounts, and our Company will not realize gains because it did not make an investment. It is possible that gains from investing will accrue to these individuals and /or to the Company, while the Company’s brokerage customers do not accrue gains in the same securities due to differences in timing of investment decisions. Conversely, it is possible that losses from investing will accrue to our Company, while these individuals do not experience losses in their personal accounts because the individuals did not make investments in their personal accounts.

12

We face strong competition from larger firms.

The brokerage and investment banking industries are intensely competitive. We compete on the basis of a number of factors, including client relationships, reputation, the abilities and past performance of our professionals, market focus and the relative quality and price of our services and products. We have experienced intense price competition with respect to our brokerage business, including large block trades, spreads, and trading commissions. Pricing and other competitive pressures in investment banking, including the trends toward multiple book runners, co-managers, and multiple financial advisors handling transactions, have continued and could adversely affect our revenue, even during periods where the volume and number of investment banking transactions are increasing. We believe we may experience competitive pressures in these and other areas in the future as some of our competitors seek to obtain market share by competing on the basis of price.

We are a relatively small investment bank with 77 employees as of December 31, 2010 and revenues of approximately $31million in 2010. Many of our competitors in the investment banking and brokerage industries have a broader range of products and services, greater financial and marketing resources, larger customer bases, greater name recognition, more senior professionals to serve their clients’ needs, greater global reach, have more established relationships with clients than we have, and some operate under less restrictive capital requirements. These larger and better capitalized competitors may be better able to respond to changes in the brokerage and investment banking industries, to compete for skilled professionals, to finance acquisitions, to fund internal growth, and to compete for market share generally.

The scale of our competitors has increased in recent years as a result of substantial consolidation among companies in the investment banking and brokerage industries. In addition, a number of large commercial banks, insurance companies, and other broad-based financial services firms have established or acquired underwriting or financial advisory practices and broker-dealers or have merged with other financial institutions. These firms operate under less restrictive capital requirements than we do and these firms have the ability to offer a wider range of products than we do, which enhances their competitive position. They also have the ability to support investment banking with commercial banking, insurance, and other financial services in an effort to gain market share, which has resulted, and could further result, in pricing pressure in our businesses. In particular, the ability to provide financing has become an important advantage for some of our larger competitors and, because we do not provide such financing, we may be unable to compete as effectively for clients in a significant part of the brokerage and investment banking market.

If we are unable to compete effectively with our competitors, our business, financial condition, and results of operations will be adversely affected.

We have incurred losses for the period covered by this report in the recent past and may incur losses in the future.

The Company recorded net losses of $5,338,000 for the year ended December 31, 2010 and $5,462,000 for the year ended December 31, 2009. We also recorded net losses in certain quarters within other past fiscal years. We may incur losses in future periods. If we are unable to finance future losses, those losses may have a significant effect on our liquidity as well as our ability to operate.

In addition, the Company may incur significant expenses in connection with initiating new business activities or in connection with any expansion of our underwriting, brokerage, or other businesses. We may also engage in strategic acquisitions and investments for which we may incur significant expenses. Accordingly, we may need to increase our revenue at a rate greater than our expenses to achieve and maintain profitability. If our revenue does not increase sufficiently, or even if our revenue does increase but we are unable to manage our expenses, we will not achieve and maintain profitability in future periods.

13

Capital markets and strategic advisory engagements are singular in nature and do not generally provide for subsequent engagements.

The ability to complete capital raising transactions for our clients is significantly affected by the state of the capital markets in general. Additionally, our investment banking clients generally retain us on a short-term, engagement-by-engagement basis in connection with specific capital markets or mergers and acquisitions transactions, rather than on a recurring basis under long-term contracts. As these transactions are typically singular in nature and our engagements with these clients may not recur, we must seek out new engagements when our current engagements are successfully completed or are terminated. As a result, high activity levels in any period are not necessarily indicative of continued high levels of activity in any subsequent period. If we are unable to generate a substantial number of new engagements and generate fees from those successful completion of transactions, our business and results of operations would likely be adversely affected.

Our risk management policies and procedures could expose us to unidentified or unanticipated risk.

Our risk management strategies and techniques may not be fully effective in mitigating our risk exposure in all market environments or against all types of risk.

We are exposed to the risk that third parties that owe us money, securities, or other assets will not perform their obligations. These parties may default on their obligations to us due to bankruptcy, lack of liquidity, operational failure, breach of contract, or other reasons. We are also subject to the risk that our rights against third parties may not be enforceable in all circumstances. Although we regularly review credit exposures to specific clients and counterparties and to specific industries and regions that we believe may present credit concerns, default risk may arise from events or circumstances that are difficult to detect or foresee. In addition, concerns about, or a default by, one institution could lead to significant liquidity problems, losses, or defaults by other institutions, which in turn could adversely affect us. Also, risk management policies and procedures that we utilize with respect to investing our own funds or committing our capital with respect to investment banking or trading activities may not protect us or mitigate our risks from those activities. If any of the variety of instruments, processes, and strategies we utilize to manage our exposure to various types of risk are not effective, we may incur losses.

Our operations and infrastructure may malfunction or fail.

Our business is highly dependent on our ability to process, on a daily basis, a large number of increasingly complex transactions across diverse markets. Our financial, accounting, or other data processing systems may fail to operate properly or become disabled as a result of events that are wholly or partially beyond our control, including a disruption of electrical or communications services or our inability to occupy one or more of our buildings. The inability of our systems to accommodate an increasing volume of transactions could also constrain our ability to expand our businesses. If any of these systems do not operate properly or are disabled or if there are other shortcomings or failures in our internal processes, people, or systems, we could suffer impairment to our liquidity, a financial loss, a disruption of our businesses, liabilities to clients, regulatory intervention, or reputation damage.

We also face the risk of operational failure of any of our clearing agents, the exchanges, clearing houses, or other financial intermediaries we use to facilitate our securities transactions. Any such failure or termination could adversely affect our ability to execute transactions and to manage our exposure to risk.

In addition, our ability to conduct business may be adversely impacted by a disruption in the infrastructure that supports our businesses and the communities in which located. This may include a disruption involving electrical, communications, transportation, or other services used by us or third parties with which we conduct business, whether due to fire, other natural disaster, power or communications failure, act of terrorism or war or otherwise. Nearly all of our employees in our primary locations, including San Francisco and New York, work in proximity to each other. If a disruption occurs in one location and our employees in that location are unable to communicate with or travel to other locations, our ability to service and interact with our clients may suffer and we may not be able to implement successfully contingency plans that depend on communication or travel. Insurance policies to mitigate these risks may not be available or may be more expensive than the perceived benefit. Further, any insurance that we may purchase to mitigate certain of these risks may not cover our loss.

14

Our operations also rely on the secure processing, storage, and transmission of confidential and other information in our computer systems and networks. Our computer systems, software, and networks may be vulnerable to unauthorized access, computer viruses, or other malicious code and other events that could have a security impact. If one or more of such events occur, this potentially could jeopardize our or our clients’ or counterparties’ confidential and other information processed by, stored in, and transmitted through our computer systems and networks, or otherwise cause interruptions or malfunctions in our, our clients’, our counterparties’, or third parties’ operations. We may be required to expend significant additional resources to modify our protective measures or to investigate and remediate vulnerabilities or other exposures, and we may be subject to litigation and financial losses that are either not insured against or not fully covered through any insurance maintained by us.

Strategic investments or acquisitions and joint ventures may result in additional risks and uncertainties in our business.

We may grow our business through both internal expansion and through strategic investments, acquisitions or joint ventures. To the extent we make strategic investments or acquisitions or enter into joint ventures, we face numerous risks and uncertainties combining or integrating businesses, including integrating relationships with customers, business partners, and internal data processing systems. In the case of joint ventures, we are subject to additional risks and uncertainties in that we may be dependent upon, and subject to liability, losses or reputation damage relating to systems, controls, and personnel that are not under our control. In addition, conflicts or disagreements between us and our joint venture partners may negatively impact our businesses.

Future acquisitions or joint ventures by us could entail a number of risks, including problems with the effective integration of operations, the inability to maintain key pre-acquisition business relationships and integrate new relationships, the inability to retain key employees, increased operating costs, exposure to unanticipated liabilities, risks of misconduct by employees not subject to our control, difficulties in realizing projected efficiencies, synergies and cost savings, and exposure to new or unknown liabilities.

Any future growth of our business may require significant resources and/or result in significant unanticipated losses, costs, or liabilities. In addition, expansions, acquisitions or joint ventures may require significant managerial attention, which may be diverted from our other operations.

Evaluation of our prospects may be more difficult in light of our limited operating history.

As a result of the volatile economic conditions faced by the securities and financial industries, and the restructuring of our business lines, there have been a number of changes to our operations. Given these changes, we can no longer rely upon prior operating history to evaluate our business and prospects. Additionally, we are subject to the risks and uncertainties that face a company in the process of restructuring its business in the midst of uncertain economic environment. Some of these risks and uncertainties relate to our ability to attract and retain employees and clients on a cost-effective basis, expand and enhance our service offerings, raise additional capital, and respond to competitive market conditions. We may not be able to address these risks adequately, and our failure to do so may adversely affect our business and the value of an investment in our Common Stock.

Risks Related to Our Industry

Risks associated with volatility and losses in the financial markets.

In the last 3 years, the U.S. financial markets have experienced tremendous volatility and uncertainty. Several mortgage-related financial institutions and large, reputable investment banks were not able to continue operating their businesses. In the event that the securities and financial industries face similar or greater volatility, there can be no assurance that we will be able to continue our operations.

15

Employee misconduct could harm us and is difficult to detect and deter.

There have been a number of highly publicized cases involving fraud or other misconduct by employees in the financial services industry in recent years. Our experience with a former employee disrupted our business significantly, and we run the risk that employee misconduct could occur at our Company. For example, misconduct by employees could involve the improper use or disclosure of confidential information, which could result in regulatory sanctions and serious reputation or financial harm to us. It is not always possible to deter employee misconduct. The precautions we take to detect and prevent this activity may not be effective in all cases and we may suffer significant reputation harm for any misconduct by our employees.

Risks associated with regulatory impact on capital markets.

Highly publicized financial scandals in recent years have led to investor concerns over the integrity of the U.S. financial markets and have prompted Congress, the SEC, the NYSE, and FINRA to significantly expand corporate governance and public disclosure requirements. To the extent that private companies, in order to avoid becoming subject to these new requirements, decide to forgo initial public offerings, our equity underwriting business may be adversely affected. In addition, provisions of the Sarbanes-Oxley Act of 2002 and the corporate governance rules imposed by self-regulatory organizations have diverted many companies’ attention away from capital market transactions, including securities offerings and acquisition and disposition transactions. In particular, companies that are or are planning to register their securities with the SEC or to become subject to the reporting requirements of the Securities Exchange Act of 1934 are incurring significant expenses in complying with the SEC and accounting standards relating to internal control over financial reporting, and companies that disclose material weaknesses in such controls under the new standards may have greater difficulty accessing the capital markets. These factors, in addition to adopted or proposed accounting and disclosure changes, may have an adverse effect on the business.

Financial services firms have been subject to increased scrutiny over the last several years, increasing the risk of financial liability and reputation harm resulting from adverse regulatory actions.

Firms in the financial services industry have been operating in a differentiated and difficult regulatory environment. The industry has experienced increased scrutiny from a variety of regulators, including the SEC, the NYSE, FINRA and state attorneys general. Penalties and fines sought by regulatory authorities have increased substantially over the last several years. This regulatory and enforcement environment has created uncertainty with respect to a number of transactions that had historically been entered into by financial services firms and that were generally believed to be permissible and appropriate. We may be adversely affected by changes in the interpretation or enforcement of existing laws and rules by these governmental authorities and self-regulatory organizations. We also may be adversely affected as a result of new or revised legislation or regulations imposed by the SEC and other United States or foreign governmental regulatory authorities or self-regulatory organizations that supervise the financial markets. Among other things, we could be fined, prohibited from engaging in some of our business activities or subjected to limitations or conditions on our business activities. Substantial legal liability or significant regulatory action against us could have material adverse financial effects or cause significant reputation harm to us, which could seriously harm our business prospects.

In addition, financial services firms are subject to numerous conflicts of interests or perceived conflicts. The SEC and other federal and state regulators have increased their scrutiny of potential conflicts of interest. We have adopted various policies, controls and procedures to address or limit actual or perceived conflicts and regularly seek to review and update our policies, controls and procedures. However, appropriately dealing with conflicts of interest is complex and difficult and our reputation could be damaged if we fail, or appear to fail, to deal appropriately with conflicts of interest. Our policies and procedures to address or limit actual or perceived conflicts may also result in increased costs, additional operational personnel and increased regulatory risk. Failure to adhere to these policies and procedures may result in regulatory sanctions or client litigation. For example, the research areas of investment banks have been and remain the subject of heightened regulatory scrutiny which has led to increased restrictions on the interaction between equity research analysts and investment banking personnel at securities firms. Several securities firms in the United States reached a global settlement in 2003 and 2004 with certain federal and state securities regulators and self-regulatory organizations to resolve investigations into equity research analysts’ alleged conflicts of interest. Under this settlement, the firms have been subject to certain restrictions and undertakings, which have imposed additional costs and limitations on the conduct of our businesses.

Financial service companies have experienced a number of highly publicized regulatory inquiries concerning market timing, late trading and other activities that focus on the mutual fund industry. These inquiries have resulted in increased scrutiny within the industry and new rules and regulations for mutual funds, investment advisers, and broker-dealers.

16

Our exposure to legal liability is significant, and damages that we may be required to pay and the reputational harm that could result from legal action against us could materially adversely affect our businesses.

We face significant legal risks in our businesses and, in recent years, the volume of claims and amount of damages sought in litigation and regulatory proceedings against financial institutions have been increasing. These risks include potential liability under securities or other laws for materially false or misleading statements made in connection with securities offerings and other transactions, potential liability for “fairness opinions,” and other advice we provide to participants in strategic transactions, and disputes over the terms and conditions of complex trading arrangements. We are also subject to claims arising from disputes with employees for alleged discrimination or harassment, among other things. These risks often may be difficult to assess or quantify and their existence and magnitude often remain unknown for substantial periods of time.

Our role as advisor to our clients on important underwriting or mergers and acquisitions transactions involves complex analysis and the exercise of professional judgment, including rendering “fairness opinions” in connection with mergers, and other transactions. Therefore, our activities may subject us to the risk of significant legal liabilities to our clients and aggrieved third parties, including stockholders of our clients who could bring securities class actions against us. Our investment banking engagements typically include broad indemnities from our clients and provisions to limit our exposure to legal claims relating to our services, but these provisions may not protect us or may not be enforceable in all cases.

For example, an indemnity from a client that subsequently is placed into bankruptcy is likely to be of little value to us in limiting our exposure to claims relating to that client. As a result, we may incur significant legal and other expenses in defending against litigation and may be required to pay substantial damages for settlements and adverse judgments. Substantial legal liability or significant regulatory action against us could have a material adverse effect on our results of operations or cause significant reputational harm to us, which could seriously harm our business and prospects.

In the past, following periods of volatility in the market price of a company’s securities, securities class action litigation often has been instituted against broker-dealer companies. Such litigation is expensive and diverts management’s attention and resources. We cannot assure you that we will not be subject to such litigation. If we are subject to such litigation, even if we ultimately prevail, our business and financial condition may be adversely affected.

Risks Related to Ownership of Our Common Stock

We have issued Series D Convertible Preferred Stock with rights preferences and privileges that are senior to those of our Common Stock. The exercise of some or all of these Series D Convertible Preferred Stock rights may have a detrimental effect on the rights of the holders of the Common Stock.

On September 8, 2009, we closed a private placement Preferred Stock financing transaction. We sold 23,720,916 shares of our Series D Convertible Preferred Stock at $0.43 per share (equivalent to 3,388,677 shares of common at a conversion price of $3.01 per share after adjusting for our reverse stock split in August 2010) and warrants to purchase 3,388,677 share of Common Stock at $4.55 per share on a post-reverse split basis to an investor group that includes certain of our officers and directors, in addition to outside investors. In connection with this transaction, the Company converted the principal and accrued interest of certain notes issued by the Company between May 2009 and July 2009 into Series D Convertible Stock. The aggregate principal amount from these cancelled notes was $1,425,000.

As the warrants originally contained a full ratchet anti-dilution provision, we recorded a non-cash warrant liability of approximately $26 million as of September 30, 2009 in accordance with generally accepted accounting principles (“GAAP”), which resulted in a stockholders’ deficit (negative stockholders’ equity). This, in turn, caused us to fall outside of the NASDAQ Listing Rules which require a minimum of $2,000,000 of stockholders’ equity.

We have since remedied the noncompliance with the NASDAQ listing rules by amending the warrants to remove the full ratchet anti-dilution provision and thus removed the resulting stockholders’ deficit. At December 31, 2009, we no longer carried warrant liabilities on our Statement of Financial Condition. In consideration for such amendment, the Company has agreed to pay the holders of the warrants $0.035 per warrant share in cash on a post-reverse split basis, which was paid in February 2011.

17