Attached files

| file | filename |

|---|---|

| EX-31.1 - EX-31.1 - SATCON TECHNOLOGY CORP | a2202706zex-31_1.htm |

| EX-23.2 - EX-23.2 - SATCON TECHNOLOGY CORP | a2202706zex-23_2.htm |

| EX-32.1 - EX-32.1 - SATCON TECHNOLOGY CORP | a2202706zex-32_1.htm |

| EX-31.2 - EX-31.2 - SATCON TECHNOLOGY CORP | a2202706zex-31_2.htm |

| EX-23.1 - EX-23.1 - SATCON TECHNOLOGY CORP | a2202706zex-23_1.htm |

| EX-22.1 - EX-22.1 - SATCON TECHNOLOGY CORP | a2202706zex-22_1.htm |

| EX-10.55 - EX-10.55 - SATCON TECHNOLOGY CORP | a2202706zex-10_55.htm |

| EX-10.56 - EX-10.56 - SATCON TECHNOLOGY CORP | a2202706zex-10_56.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Year Ended December 31, 2010

Commission file number 1-11512

SATCON TECHNOLOGY CORPORATION

(Exact name of registrant as specified in its charter)

| DELAWARE (State or other jurisdiction of incorporation or organization) |

04-2857552 (I.R.S. Employer Identification Number) |

|

27 Drydock Avenue, Boston, Massachusetts (Address of principal executive offices) |

02210 (Zip Code) |

(617) 897-2400

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class | Name of Exchange on Which Registered | |

|---|---|---|

| Common Stock, $.01 Par Value | The NASDAQ Stock Market, LLC | |

| Preferred Stock Purchase Rights | The NASDAQ Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer, "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated Filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's Common Stock, $.01 par value per share, held by non-affiliates of the registrant was $205,765,352 based on the last reported sale price of the registrant's Common Stock on the Nasdaq Capital Market as of the close of business on the last business day of the registrant's most recently completed second quarter $2.86. There were 118,908,772 shares of Common Stock outstanding as of March 1, 2011.

DOCUMENTS INCORPORATED BY REFERENCE: Portions of the registrant's Proxy Statement for its 2011 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

2

Statement Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains or incorporates forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Act of 1934. You can identify these forward-looking statements by our use of the words "believes," "anticipates," "plans," "expects," "may," "will," "intends," "estimates," and similar expressions, whether in the negative or in the affirmative. Forward-looking statements include statements regarding our position as a leading provider of power conversion solutions; our ability to create innovative products in the markets we target; the expected demand for our products in the markets we target; our ability to address our customers' needs; our ability to execute on our growth strategy; and our ability to compete in the markets we target. Although we believe that these forward-looking statements reasonably reflect our plans, intentions and expectations disclosed in the forward-looking statements, our actual results could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have included important factors in the cautionary statements under the heading "Risk Factors" under Item 1A that we believe could cause our actual results to differ materially from the forward-looking statements that we make. Forward-looking statements contained in this Annual Report speak only as of the date of this report. Subsequent events or circumstances occurring after such date may render these statements incomplete or out of date. We undertake no obligation and expressly disclaim any duty to update such statements.

Overview

Satcon Technology Corporation ("Satcon" or "Company") is a leading clean energy technology provider of utility-grade power conversion solutions for the renewable energy market, primarily the large-scale commercial and utility-scale solar photovoltaic, or PV, markets. We design and deliver advanced power conversion solutions that enable large-scale producers of renewable energy to convert clean energy into grid-connected, efficient and reliable electrical power.

Our power conversion solutions boost total system power production through system intelligence, advanced command and control capabilities, industrial-grade engineering and total lifecycle performance optimization. Our power conversion solutions feature the widest range of power ratings in the solar industry. We also offer system design services and solutions for management, monitoring, and performance measurement to maximize capital investment and improve overall quality and performance over the entire lifespan of an installation.

Revenue Comparison with Prior Years

Consolidated revenues by geographic area for the years ended December 31, 2010, 2009 and 2008 were as follows:

| |

Year Ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | ||||||||

United States |

$ | 76,079,866 | $ | 39,734,485 | $ | 46,371,717 | |||||

International |

97,222,107 | 12,801,148 | 7,921,617 | ||||||||

Total |

$ | 173,301,973 | $ | 52,535,633 | $ | 54,293,334 | |||||

These numbers have been adjusted to reflect the January 2010 sale of our Satcon Applied Technology business unit and the September 2008 sales of our Electronics and Power Systems US

3

business units. See Note D (Discontinued Operations) to the Consolidated Financial Statements included in this Annual Report on Form 10-K.

Industry Background & Market Opportunity

Inverters, which are the engines of power conversion solutions, are essential components for renewable energy systems. Their primary function is to convert direct current (DC) power into alternating current (AC) power. Advanced solar Photovoltaic ("PV") inverters are emerging as the core enabling technology platform for the growth of large-scale distributed power systems. Through a combination of increased capacity, improved output quality and advanced control features, these more powerful, efficient and intelligent inverters are expected to enable a stepped improvement in both the controllability and the overall performance of solar PV production and distribution. We believe they will also be critical elements in improving the performance of future solar PV systems.

As our industry advances, we are committed to providing leadership and developing intellectual property in both the technology and the delivery model. In terms of the technology, our value-driving innovation expands beyond a component focus into building a better system architecture for energy harvest, connecting the panel to the grid. Solstice is our first example of this expanded architectural approach, and we are committed to further innovation in this category. This is what we see as our place in the smart grid—as a provider of solutions and systems that deliver smarter and faster performance on the supply side of the power grid. Our vision is to enable not only better integration of intermittent renewable resources onto the grid, but also to deliver value-added capabilities that will improve the overall performance of the grid itself. We see a future in which the inverter evolves from the electromechanical device that it is now into the digital device of the truly intelligent smart grid network. We are committed to a total systems approach for our customers, including a full range of design services and complete lifecycle management services. Both our design and lifecycle management services are unique in that they are fully localized in geography and specialized in function.

The growth in large-scale solar energy plants has created strong worldwide demand for large-scale solar PV power conversion solutions, and is driving significant innovation in the technologies that are being deployed in order to maximize system performance and grid interoperability. Industry research estimates that the global PV inverter market will grow globally at an average annual growth rate of about 10% from 2011 through 2014, with the majority of this growth expected to come from turn-key utility-scale PV inverters of 500 kW and above, which is a core competency for us.

The strong growth in our market is catalyzed by the interaction of several market trends:

- •

- Socio-political factors and energy supply-demand imbalances are creating an environment ripe for solar power

worldwide. Socio-political unrest in oil-producing countries as well as long-term macroeconomic factors such as

increasing electricity usage, power grid capacity constraints, fossil fuel price volatility, and harmful levels of pollution and greenhouse gases are driving increased demand for solar and other forms

of renewable energy.

- •

- Government incentives are accelerating growth in the power conversion market. Many countries, including Germany, France, Italy, Greece, the United States, Canada, China and India, have set policies, such as renewable portfolio standards, to achieve a certain percentage of their overall energy generation from alternative energy sources. Several countries have committed to generating at least 20 percent of their electrical energy from renewable energy sources by 2020. Governments have also enacted a variety of tax incentives and subsidies to fuel the construction of renewable energy power plants. As our power conversion systems are integral components of many renewable energy power plants, primarily solar PV plants, we expect demand for them to continue to experience growth as a direct result of these government programs.

4

- •

- Utilities are deploying large-scale PV plants which drive power conversion solution

sales. To satisfy mandates, utilities are building increasingly large renewable energy installations, often in the form of large-scale

solar PV plants. These megawatt ("MW") -size plants require the use of large-scale, high-grade power conversion systems. The technical expertise of leading power conversion

companies is becoming increasingly important as utilities become more rigorous in specifications for the systems that connect these plants to the grid.

- •

- PV module price declines are encouraging new solar installations. Solar PV power plants rely on PV arrays, a linked collection of PV modules, to convert solar energy into raw electricity. PV modules have seen significant and continual price declines in recent years due to advances in semiconductor processing technology and the increased availability of silicon, the substance used by a PV panel to generate electricity. The decreased cost of the basic building blocks of solar PV installations increases the attractiveness of solar power economics and helps catalyze the development of new solar plants, which in turn increases demand for power conversion systems.

Within this renewable energy market we believe that the fastest growth area for Satcon involves large-scale, utility-grade renewable energy and distributed power generation. These solutions require power quality control products to manage the performance of individual solar installations and monitor how it will interconnect with larger energy infrastructure (grid). In order to be commercially viable and operate effectively, these solutions must be highly reliable, efficient, and deliver the command and control performance required to profitably manage multi-megawatt solar power plants. Our intellectual property, in the form of technical expertise and innovative product offerings, uniquely positions the company to provide the next generation of large-scale, utility-grade renewable energy projects with the energy storage, power quality, and distributed power systems they will require.

Products

We deliver a full suite of power conversion solutions and services for large commercial and utility-scale renewable energy installations. We produce a broad range of products to provide the critical bridge between clean energy sources and large-scale power grids, helping companies meet the rising demand for clean energy with efficiency and profitability.

Our core solutions for renewable energy consist of utility-grade inverters for solar PV a applications. Inverters convert the DC power generated by these renewable energy sources into useable AC power. They provide the interface with the electric utility grid, an energy storage device, and end user applications. Our inverters' advanced utility-ready features enable simplified grid interconnection and can be easily integrated into supervisory control and data acquisition, or SCADA, systems through standardized communication interfaces. Our Renewable Energy Solutions product family includes the following:

- •

- PowerGate® Plus is, we believe, the world's most widely

deployed large-scale, utility-ready PV inverter with over 1.7 gigawatts sold since its introduction in 2005. PowerGate Plus increases efficiency and maximizes system uptime and power production. By

combining sophisticated system intelligence with in-depth performance monitoring, PowerGate Plus provides power plant operators with an advanced level of command and control.

- •

- Equinox™ is our next generation power conversion solution.

Equinox features superior efficiency combined with three extreme climate packages to provide power plant operators with enhanced levels of system performance and uptime and the PV industry's broadest

thermal operating range. Equinox is built on the foundation of Satcon PowerGate Plus.

- •

- Prism® is a fully integrated one MW medium voltage solution optimized for large-scale commercial and utility-scale PV installations. Incorporating advanced components and our

5

- •

- Solstice™ is the PV industry's first complete power harvesting

and array management solution for large-scale commercial and utility-scale solar PV plants. Solstice is a total system solution enabling intelligent management of the entire PV system while offering

the flexibility of localized control over every component in the array, from the panel, to a single string, to the inverter, to the grid. Solstice breaks large arrays up into smaller, controllable

increments of less than three kW and enables string-level energy harvest, which is then combined with a highly-optimized central power conversion system. A typical PV array only operates at an energy

output of the lowest performing PV panel in the array. With Solstice, power output from each string of panels is independently optimized, allowing each string to operate at its full potential all day.

The result is increased energy production from the entire array by 5-12% compared to the traditional inverter system, enabling a significant improved return on invested capital for our

customers.

- •

- Energy Equity Protection™ is our complete range of lifecycle

management services designed to help customers ensure that their system delivers optimum performance across its entire twenty-plus year life span. Energy Equity Protection includes Satcon

Design Services, APEX™ Project Management, Preventative Maintenance and Warranty Programs, and System Uptime Guarantees. Our Design Services offerings range from straightforward design

consulting to complete end-to-end system design. Our APEX Project Management services are designed to handle project planning and logistics details associated with complex

orders. Our Preventative Maintenance and Warranty Programs keep our customers' inverters running at their maximum efficiency. Our 99% System Uptime Guarantees compensate customers for lost energy

production in the case of a malfunctioning inverter. All of our services are fully localized in geography and specialized in function.

- •

- Other Legacy Power Products. We also provide static transfer switches, static voltage regulators, frequency converters and AC arc furnace line controllers from 5 kilowatts to 100 megawatts.

PowerGate Plus inverter, Prism comes ready to connect a solar PV array to the utility grid, enabling fast installation through a modular prepackaged design.

Revenues by product category for the years ended December 31, 2010, 2009 and 2008 were as follows:

| |

Year Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

(Amounts in Millions)

|

2010 | 2009 | 2008 | |||||||

Product Revenue |

||||||||||

Renewable Energy Solutions |

$ | 173.3 | $ | 47.7 | $ | 52.2 | ||||

Other Legacy |

— | 4.8 | 2.1 | |||||||

Total Product Revenue |

$ | 173.3 | $ | 52.5 | $ | 54.3 | ||||

Financial Results by Business Segment

In prior years we have included segment disclosures as it related to the operations of our business units. With the sale in 2008 of our Electronics and Power Systems US business units and the classification in 2009 of our Applied Technology business unit as part of discontinued operations, since 2009 we have viewed our operations as one segment and as one business unit. Accordingly, until such time as circumstances change and we determine that we have reportable segments, we will no longer report this information. See Note S to the Consolidated Financial Statements included in this Annual Report on Form 10-K.

6

Satcon Power Conversion Solution Attributes

We strive to meet our customers' needs by providing power conversion solutions and systems that encompass the following key attributes:

- •

- Innovation. We are committed to innovation in the core

inverter technology, the complete energy harvest architecture, and the comprehensive services delivery model for our customers.

- •

- Performance. Our products use proprietary designs and

technology to ensure that high-quality power is efficiently produced in all operating conditions. Our robust designs deliver high system up-time.

- •

- Reliability. We design and manufacture

high-reliability, long-life power electronics for solar PV and fuel cell applications. We design, manufacture and test our systems for optimal performance over the entire

lifespan of the photovoltaic system. We design our products to support the long-life, always-on requirements of the power quality markets through a comprehensive suite of

programs including support services, system design services, and warranty and preventative maintenance programs.

- •

- Efficiency. We design and manufacture our products to meet

the efficiency needs of our customers as defined by their specifications and the end use of the product. The overall efficiency of a renewable power system, or its ability to deliver power with

minimum energy loss, is vital to its effective commercialization and overall profitability dynamic, and depends on the efficiency of all of its component parts. Our products continually lead in system

yield, harvest, and power production, delivering stepped improvements in PV total system output, due to our advanced state-of-the-art technologies, namely inverters

and architectures such as Solstice.

- •

- Quality. We operate with quality management systems and

are ISO 9001:2000 certified. All of our high power level inverters are Underwriter Laboratory listed as meeting their requirements for safety.

- •

- Delivery Methodology. We deliver a comprehensive range of

services, from design services to complete lifecycle management services for our customers.

- •

- Flexibility. We develop and manufacture our products for use in various renewable energy and power quality systems such as photovoltaics, fuel cells, wind turbines, micro-turbines and UPS systems. Our products are modular and scalable to meet a wide range of power requirements. Our engineers work closely with our customers to address overall systems design issues and to ensure that our products meet their system specifications. A close working relationship between the customers' engineers and our engineers is particularly important in the rapidly evolving renewable energy industry.

Sales, Marketing and Service

We sell our products and services through direct sales personnel, distributor arrangements and sales agent arrangements which comprise a global market presence for Satcon. Our direct sales staff manages our key customer accounts, regional distributors and agents, provides customer support and identifies significant market opportunities in their respective markets.

In order to maximize our customer's return on assets and investment profitability, we offer a suite of services focused on delivering optimized design and total lifecycle management. Our services provide technical support throughout the entire lifespan of a product. We believe these factors are essential to building close, long-term value for our customers, and maintaining our competitive edge.

In each core worldwide market we serve, we have a full local organization encompassing sales, inside sales, pre-sales, project management, field service, and applications engineering. This localized

7

expertise allows us to work closely with our customers to fully understand their requirements and to rapidly respond to the tough challenges that inevitably come up with any large project, ensuring the highest levels of customer satisfaction.

Strategy

Our growth strategy is to leverage our proven execution with industry-leading products, our advanced innovation capabilities, and our global commercial and manufacturing footprint to increase our market share. Our focus continues to be on the following strategies:

- •

- Develop New Technology to Broaden Our High Value

Solutions. Global trends are fueling the development of ever larger solar plants and catalyzing the rapid growth for solar power

conversion solutions. We offer the widest power range of utility-grade power conversion products for the PV industry. We believe the combination of our advanced technology, intellectual property and

industry expertise position us to develop the industry's next generation of power conversion solutions. We believe that continuing to develop new products and technologies that meet the expanding and

demanding needs of our large-scale commercial and utility-scale customers will enhance our competitive position and maximize our growth opportunities.

- •

- Expand Our International Sales and Service Footprint. We

continue to expand and deepen our sales and service operations globally as we aim to increase our market share. We are committed to establishing a large, direct local presence in the European and

Asian countries where we compete, as well as maintaining and building upon the strong relationships we have in North America. We aim to strengthen and extend our existing strategic alliances and

relationships, which may take the form of marketing, sales or distribution agreements. We are actively working to develop alliances and relationships with new partners to extend our global reach and

take advantage of growth opportunities.

- •

- Expand Our International Manufacturing Footprint. Our primary manufacturing operations take place in Ontario, Canada and Shenzhen, China. We also perform certain manufacturing functions at our facilities located in Fremont, California and Boston, Massachusetts. We currently have the capacity to produce approximately 1.5 GW of power conversion systems per year. In addition, we recently established a manufacturing relationship with GCL Solar, one of China's largest PV plant developers, which will enhance our manufacturing capacity for the Asian markets. We expect to increase our manufacturing capacity by approximately 100% by the end of 2011.

Competition

We believe that competitive performance in the marketplace for power conversion and control products depends upon several factors, including product price, technical innovation, product quality and reliability, range of products, range of services, customer service and technical support. We believe the following represent our main competitors:

- •

- Advanced Energy Industries

- •

- Markets: Renewable Energy, Solar

Equipment

- •

- Products: Solar Inverters, Power Systems

- •

- PowerOne

- •

- Markets: Renewable Energy, Power

Conversion

- •

- Products: Solar Inverters, Wind Inverters, Monitoring and Control

8

- •

- PV Powered

- •

- Markets: Renewable Energy, Grid-Tied PV

Inverters

- •

- Products: Residential Solar Inverters, Commercial Solar

Inverters

- •

- Schneider Electric

- •

- Markets: Renewable Energy, Energy

Management

- •

- Products: Solar Inverters, Automation and Control, Electrical

Distribution, Energy Efficiency

- •

- Siemens

- •

- Markets: Industrial Plant Automation, Energy,

Healthcare

- •

- Products: Solar Inverters, Communication Software, Wind

Turbines, Gas Turbines, Steam Turbines, Generators, Compressors & Trains, Fans, Fuel Gasifier, Fuel Cells, Environmental Systems

- •

- SMA Solar Technology

- •

- Markets: Renewable Energy, Solar Inverters, Energy

Systems

- •

- Products: Residential Inverters, Commercial Inverters, Solar

Plants

- •

- Sungrow Power Supply

- •

- Markets: Renewable Energy, Solar and Wind

Equipment

- •

- Products: Solar Inverters, Wind Inverters

Satcon is focused on maintaining our industry-leading position as a provider of large-scale commercial and utility-scale power solutions. Our technical innovation emphasizing product performance and reliability, supported by our commitment to strong customer service and technical support, enables us to continue to compete successfully against our competitors.

Significant Customers

In 2010, no sales to any one customer exceeded 10% of our annual revenue but there were 3 customers (GCL Solar Limited, Enel Green Power S.p.A, and CE Solar, S.R.O) that were classified as significant customers in 2010 due to their gross receivables balance at December 31, 2010 exceeding 10% of our total gross accounts receivables at December 31, 2010 (approximately 34%), and two of these customers balances were backed by irrevocable letters of credit at December 31, 2010.

There was one customer (SunPower Corporation) that was classified as a significant customer in 2009 due to sales to this customer exceeding 10% of our annual revenue (approximately 14%). In addition, there was one customer (Enfinity, NV) that was classified as a significant customer in 2009 due to its gross receivable balance at December 31, 2009 exceeding 10% of our total gross receivables at December 31, 2009 (approximately 10%).

Backlog

Our backlog consists primarily of orders for power control systems. At December 31, 2010, our backlog was approximately $103 million all of which is scheduled to be shipped during 2011. Many of our contracts and sales orders may be canceled at any time with limited or no penalty.

9

Research and Development

We believe that the continued and timely development of new products and enhancements to our existing products is necessary to maintain our competitive position. We use technologies developed by our business units, together with information supplied by our distributors and customers, to design and develop new products and product enhancements and to reduce the time-to-market for our products.

We expended approximately $15.7 million, $8.4 million, and $5.1 million on internally funded research and development during the years ended December 31, 2010, 2009 and 2008, respectively.

Manufacturing

We manufacture our products at our facilities located in Burlington, Ontario, Canada, Boston, Massachusetts, Fremont, California and through our contract manufacturing partner in Asia. Our overall manufacturing process at these facilities and with our contract manufacturer has a current production capacity of approximately 1.5 gigawatts per year.

Reducing product cost is essential to our ability to further penetrate the market with our power conversion solutions and service offerings. We believe that most of the raw materials used in our products are readily available from a variety of vendors. Additionally, we design and develop our products to use commodity parts in order to simplify the manufacturing process. We have made and expect to continue to make technological improvements that reduce the costs to manufacture our products.

Our manufacturing facilities are subject to certain environmental laws and regulations, particularly with respect to industrial waste and emissions. Compliance with these laws and regulations has not had a material impact on our capital expenditures or competitive position.

Intellectual Property

Our success and competitiveness depend on our ability to develop and maintain the proprietary aspects of our technology and operate without infringing on the proprietary rights of others. We rely on a combination of patent, trademark, trade secret and copyright law and contract restrictions to protect the proprietary aspects of our technologies. We seek to limit disclosure of our intellectual property by requiring employees, consultants and any third parties with access to our proprietary information to execute confidentiality agreements and by restricting access to that information.

As of December 31, 2010, we held approximately 48 U.S. patents and had 2 patent applications pending with the U.S. Patent and Trademark Office. The expiration dates of our patents range from 2011 to 2027, with the majority expiring after 2015.

Many of the U.S. patents described above are the result of retaining ownership of inventions made under U.S. government-funded research and development programs. As a qualifying small business, we have retained commercial ownership rights to proprietary technology developed under various U.S. government contracts and grants, including small business innovation research contracts. With respect to any invention made with government assistance, the government has a nonexclusive, nontransferable, irrevocable, paid-up license to use the technology or have the technology employed for or on behalf of the U.S. government throughout the world. Under certain conditions, the U.S. government also has "march-in rights." These rights enable the U.S. government to require us to grant a nonexclusive, partially exclusive, or exclusive license in any field of use to responsible applicants, upon terms that are reasonable under the circumstances.

10

Foreign Operations

We have foreign operations through our manufacturing facility in Burlington, Ontario, Canada and our sales and service offices in Prague, Czech Republic, Shenzhen, China and Shanghai, China.

Government Regulation

We presently are subject to various federal, state and local laws and regulations relating to, among other things, export control energy generation, safe working conditions, handling and disposal of hazardous and potentially hazardous substances and emissions of pollutants into the atmosphere. To date, we believe that we have obtained all the necessary government permits and have been in substantial compliance with all of these applicable laws and regulations.

Government Contracts

On occasion we have acted as a prime contractor or major subcontractor for different U.S. government programs that involve energy-related products. Over its lifetime, a program may be implemented by the award of many individual contracts and subcontracts, or contracts with option years, or partially funded contracts.

U.S. government contracts include provisions permitting termination, in whole or in part, without prior notice, at the U.S. government's discretion. The U.S. government generally pays compensation for work actually done and commitments made at the time of termination, and some allowance for profit on the work performed. The U.S. government may also terminate for default in performance and pay only the value delivered to the U.S. government. It can also hold the contractor responsible for re-procurement costs.

Our government contracts are also subject to specific procurement statutes and regulations and a variety of socio-economic and other factors. Failure to comply with these regulations and requirements could lead to loss of contract or suspension or disbarment from U.S. government contracting or subcontracting for a period of time. Examples of these statutes and regulations are those related to procurement integrity, export control, employment practices, the accuracy of records and the recording of costs.

Sales to the U.S. government may be affected by changes in research interests in the areas in which we engage, changing government department budgets, and changing procurement policies. With the sale of our Applied Technology business unit in January 2010 we have no significant revenues from continuing operations being derived from government contracts.

Employees

At December 31, 2010, we had a total of 340 full-time employees, 4 part-time employees and 86 contract employees. Of the total, 125 persons were employed in engineering, 167 in manufacturing, 44 in administration, 30 in field service and 64 in sales and marketing. Our future success depends in large part on the continued service of our key technical and senior management personnel, and on our ability to attract, retain and motivate qualified employees, particularly those highly skilled design, process and test engineers involved in the manufacture of existing products and the development of new products and processes. The competition for such personnel is intense, and the loss of key employees could have a material adverse effect on us. None of our employees are represented by a union. We believe that relations with our employees are good.

Reports

Our web site is www.Satcon.com. Through our web site, we make available free of charge all of our Securities and Exchange Commission, or SEC, filings, including our annual reports on Form 10-K,

11

quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such reports are electronically filed with the SEC.

The risks described below may materially impact your investment in our company or may in the future, and, in some cases already do, materially affect us and our business, financial condition and results of operations. You should carefully consider these factors with respect to your investment in our securities. This section includes or refers to certain forward-looking statements; you should read the explanation of the qualifications and limitations on such forward-looking statements beginning on pages 4 of this report.

We have a history of operating losses, may not be able to achieve profitability and may require additional capital in order to sustain our businesses.

For each of the past ten fiscal years, we have experienced losses from operating our businesses. As of December 31, 2010, we had an accumulated deficit of approximately $243.5 million. During the year ended December 31, 2010 we had a loss from continuing operations of approximately $12.4 million. If we are unable to operate on a cash flow breakeven basis in the future, we may need to raise additional capital in order to sustain our operations. There can be no assurance that we will be able to achieve such results or to raise such funds if they are required.

We could issue additional common stock, which might dilute the book value of our common stock.

We have authorized 200,000,000 shares of our common stock, of which 117,911,278 shares were issued and outstanding as of December 31, 2010. Our board of directors has the authority, without action or vote of our stockholders in most cases, to issue all or a part of any authorized but unissued shares. Such stock issuances may be made at a price that reflects a discount from the then-current trading price of our common stock. In addition, in order to raise the capital that we may need at today's stock prices, we may need to issue securities that are convertible into or exercisable for a significant amount of our common stock. These issuances would dilute your percentage ownership interest, which would have the effect of reducing your influence on matters on which our stockholders vote, and might dilute the book value of our common stock. You may incur additional dilution of net tangible book value if holders of stock options, whether currently outstanding or subsequently granted, exercise their options or if warrant holders exercise their warrants to purchase shares of our common stock.

The sale or issuance of a large number of shares of our common stock could depress our stock price.

As of March 1, 2011, we have reserved 28,736,061shares of common stock for issuance upon exercise of stock options and warrants and 5,579,735 shares for future issuances under our stock plans. As of March 1, 2011, holders of warrants and options to purchase an aggregate of 21,576,253 shares of our common stock may exercise those securities and transfer the underlying common stock at any time subject, in some cases, to Rule 144.

The execution of our growth strategy is dependent upon the continued availability of third-party financing arrangements for our customers, and is affected by general economic conditions.

The recent recessionary condition of the general economy and limited availability of credit and liquidity could materially and adversely affect our business and results of operations. Many purchasers of our inverters and other products require financing from third-parties to finance their operations. Given the recent recession and the restricted credit markets, certain of our customers may be unable or

12

unwilling to finance the cost to purchase our products or may be forced to cancel previously submitted orders or delay taking shipment until suitable credit is again available. Collecting payment from customers facing liquidity challenges may also be difficult. These factors could materially and adversely affect our anticipated revenue and growth and, accordingly, our results of operations, cash flows and financial condition.

If we are unable to maintain our technological expertise in design and manufacturing processes, we will not be able to successfully compete.

We believe that our future success will depend upon our ability to develop and provide innovative products that meet the changing needs of our customers. This requires that we successfully anticipate and respond to technological changes in design and manufacturing processes in a cost-effective and timely manner. As a result, we continually evaluate the advantages and feasibility of new product design and manufacturing processes. We cannot, however, assure you that our process improvement efforts will be successful. The introduction of products embodying new technologies and the emergence of shifting customer demands or changing industry standards could render our existing products obsolete and unmarketable, which would have a significant impact on our ability to generate revenue. Our future success will depend upon our ability to continue to develop and introduce a variety of new products and product enhancements to address the increasingly sophisticated needs of our customers. We may experience delays in releasing new products and product enhancements in the future. Material delays in introducing new products or product enhancements may cause customers to forego purchases of our products and purchase those of our competitors.

The U.S. government has certain rights relating to our intellectual property.

Many of our patents are the result of inventions made under U.S. government-funded research and development programs. With respect to any invention made with government assistance, the government has a nonexclusive, nontransferable, irrevocable, paid-up license to use the technology or have the technology employed for or on behalf of the U.S. government throughout the world. Under certain conditions, the U.S. government also has "march-in rights," which enable the U.S. government to require us to grant a nonexclusive, partially exclusive, or exclusive license in any field of use to responsible applicants, upon terms that are reasonable under the circumstances.

Our business could be adversely affected if we are unable to protect our patents and proprietary technology.

As of March 1, 2011, we held approximately 48 U.S. patents and had 2 patent applications pending with the U.S. Patent and Trademark Office. The expiration dates of our patents range from 2011 to 2028, with the majority expiring after 2015. As a qualifying small business from our inception to date, we have retained commercial ownership rights to proprietary technology developed under various U.S. government contracts and grants.

Our patent and trade secret rights are of significant importance to us and to our future prospects. Our ability to compete effectively against other companies in our industry will depend, in part, on our ability to protect our proprietary technology and systems designs relating to our products. Although we have attempted to safeguard and maintain our proprietary rights, we do not know whether we have been or will be successful in doing so. Further, our competitors may independently develop or patent technologies that are substantially equivalent or superior to ours. No assurance can be given as to the issuance of additional patents or, if so issued, as to their scope. Patents granted may not provide meaningful protection from competitors. Even if a competitor's products were to infringe patents owned by us, it would be costly for us to pursue our rights in an enforcement action and there can be no assurance that we would be successful in enforcing our intellectual property rights. Because we intend to enforce our patents, trademarks and copyrights and protect our trade secrets, we may be

13

involved from time to time in litigation to determine the enforceability, scope and validity of these rights. This litigation could result in substantial costs to us and divert resources from operational goals. In addition, effective patent, trademark, service mark, copyright and trade secret protection may not be available in every country where we operate or sell our products. In addition, certain of our customers may request that we provide them with assurances that elements of our intellectual property be available for their use in the event that we are prevented from satisfying our service and warranty obligations to them or their customers.

We may not be able to maintain confidentiality of our proprietary knowledge.

In addition to our patent rights, we also rely on treatment of our technology as trade secrets through confidentiality agreements, which all of our employees are required to sign, assigning to us all patent rights and other intellectual property developed by our employees during their employment with us. Our employees have also agreed not to disclose any trade secrets or confidential information without our prior written consent. We also rely on non-disclosure agreement to protect our trade secrets and proprietary knowledge. These agreements may be breached, and we may not have adequate remedies for any breach. Our trade secrets may also be known without breach of these agreements or may be independently developed by competitors. Failure to maintain the proprietary nature of our technology and information could harm our results of operations and financial condition by reducing or eliminating our technological advantages in the marketplace.

Others may assert that our technology infringes their intellectual property rights.

We believe that we do not infringe the proprietary rights of others and, to date, no third parties have asserted an infringement claim against us, but we may be subject to infringement claims in the future. The defense of any claims of infringement made against us by third parties could involve significant legal costs and require our management to divert time from our business operations. If we are unsuccessful in defending any claims of infringement, we may be forced to obtain licenses or to pay royalties to continue to use our technology. We may not be able to obtain any necessary licenses on commercially reasonable terms or at all. If we fail to obtain necessary licenses or other rights, or if these licenses are costly, our operating results may suffer either from reductions in revenues through our inability to serve customers or from increases in costs to license third-party technologies.

Our success is dependent upon attracting and retaining highly qualified personnel and the loss of key personnel could significantly hurt our business.

To achieve success, we must attract and retain highly qualified technical, operational and executive employees. The loss of the services of key employees or an inability to attract, train and retain qualified and skilled employees, specifically engineering, operations and business development personnel, could result in the loss of business or could otherwise negatively impact our ability to operate and grow our business successfully.

We expect significant competition for our products and services.

Many of our competitors and potential competitors are well established and have substantially greater financial, research and development, technical, manufacturing and marketing resources than we do. Some of our competitors and potential competitors are much larger than we are. If these larger competitors decide to focus on the development of distributed power and power quality products, they have the manufacturing, marketing and sales capabilities to complete research, development and commercialization of these products more quickly and effectively than we can. There can also be no assurance that current and future competitors will not develop new or enhanced technologies perceived to be superior to those sold or developed by us. There can be no assurance that we will be successful in this competitive environment.

14

We are dependent on third-party suppliers for the supply of key components for our products.

We use third-party suppliers for components in many of our systems. From time to time, shipments can be delayed because of industry-wide or other shortages of necessary materials and components from third-party suppliers. A supplier's failure to supply components in a timely manner, or to supply components that meet our quality, quantity or cost requirements, or our inability to obtain substitute sources of these components on a timely basis or on terms acceptable to us, could impair our ability to deliver our products in accordance with contractual obligations.

We have established a contract manufacturing relationship with a Chinese supplier for certain of our inverter products.

We have entered a contract manufacturing relationship with a supplier in Asia for the manufacture of certain of our inverters as a means of reducing our costs and increasing the quality for those products, thereby enabling us to maintain a competitive advantage in the marketplace for these products. Our Asian partner, working closely with us, will in turn be developing a common Asian supply chain for the components that are incorporated into our inverters. While we believe that our Asian contract manufacturer is qualified to manufacture these inverters for us, we may need to address short-term quality and delivery scheduling issues as we develop this supply chain for these inverters. If we were to encounter significant quality or delivery schedule concerns it might materially and adversely affect our relationships with customers for these inverters and our results of operations.

If we experience a period of significant growth or expansion, it could place a substantial strain on our resources.

If our power control products continue to be successful in achieving rapid market penetration, we may be required to deliver even large volumes of technically complex products or components to our customers on a timely basis at reasonable costs to us. We have limited experience in ramping up our manufacturing capabilities to meet large-scale production requirements and delivering large volumes of our power control products. If we were to commit to deliver large volumes of our power control products, we cannot assure you that we will be able to satisfy large-scale commercial production on a timely and cost-effective basis or that such growth will not strain our operational, financial and technical resources.

Our business could be subject to product liability claims.

Our business exposes us to potential product liability claims, which are inherent in the manufacturing, marketing and sale of our products, and we may face substantial liability for damages resulting from the faulty design or manufacture of products or improper use of products by end users. We currently maintain a moderate level of product liability insurance, and there can be no assurance that this insurance will provide sufficient coverage in the event of a claim. Also, we cannot predict whether we will be able to maintain such coverage on acceptable terms, if at all, or that a product liability claim would not harm our business or financial condition. In addition, negative publicity in connection with the faulty design or manufacture of our products would adversely affect our ability to market and sell our products.

We are subject to a variety of environmental laws that expose us to potential financial liability.

Our operations are regulated under a number of federal, state and foreign environmental and safety laws and regulations that govern, among other things, the discharge or release of hazardous materials into the air and water as well as the handling, storage and disposal of these materials. These laws and regulations include the Clean Air Act, the Clean Water Act, the Resource, Conservation and Recovery Act, and the Comprehensive Environmental Response, Compensation and Liability Act, as

15

well as analogous state and foreign laws. Because we use hazardous materials in certain of our manufacturing processes, we are required to comply with these environmental laws. In addition, because we generate hazardous wastes, we, along with any other person who arranges for the disposal of our wastes, may be subject to potential financial exposure for costs associated with an investigation and remediation of sites at which we have arranged for the disposal of hazardous wastes if those sites become contaminated and even if we fully comply with applicable environmental laws. If we were found to be a responsible party, we could be held jointly and severably liable for the costs of remedial actions. To date, we have not been cited for any improper discharge or release of hazardous materials.

Businesses and consumers might not adopt alternative energy solutions as a means for obtaining their electricity and power needs.

On-site distributed power generation solutions, such as fuel cell, photovoltaic and wind turbine systems, which utilize our products, provide an alternative means for obtaining electricity and are relatively new methods of obtaining electrical power that businesses may not adopt at levels sufficient to grow this part of our business. Traditional electricity distribution is based on the regulated industry model whereby businesses and consumers obtain their electricity from a government regulated utility. For alternative methods of distributed power to succeed, businesses and consumers must adopt new purchasing practices and must be willing to rely upon less traditional means of purchasing electricity. We cannot assure you that businesses and consumers will choose to utilize on-site distributed power at levels sufficient to sustain our business in this area. The development of a mass market for our products may be impacted by many factors which are out of our control, including:

- •

- market acceptance of fuel cell, photovoltaic and wind turbine systems that incorporate our products;

- •

- the cost competitiveness of these systems;

- •

- regulatory requirements; and

- •

- the emergence of newer, more competitive technologies and products.

If a mass market fails to develop or develops more slowly than we anticipate, we may be unable to recover the losses we will have incurred to develop these products.

Reductions in government subsidies could impact revenue growth in the renewable energy markets.

Various government subsidies, including feed-in tariffs, have been a significant driver in the growth of the renewable energy industry, with countries throughout the world providing incentives to spur adoption of renewable energy. While many countries are beginning to adopt feed-in tariffs and varying subsidies, others are re-evaluating the level of incentive they wish to provide or have proposed reductions to their feed-in tariffs. Any reduction in such subsidies could result in a decline in demand and price levels for renewable energy products, which could have a material adverse effect on our business, financial condition or results of operations.

Our quarterly operating results are subject to fluctuations, and if we fail to meet the expectations of securities analysts or investors, our share price may decrease significantly.

Our annual and quarterly results may vary significantly depending on various factors, many of which are beyond our control. Because our operating expenses are based on anticipated revenue levels, our sales cycle for development work is relatively long and a high percentage of our expenses are fixed for the short term, a small variation in the timing of recognition of revenue can cause significant variations in operating results from quarter to quarter. If our earnings do not meet the expectations of securities analysts or investors, the price of our stock could decline. Also, because our sales are

16

primarily made on a purchase order basis, customers may generally cancel, reduce or postpone orders without penalty, resulting in reductions to our net sales and profitability.

We may not be able to realize our deferred tax assets.

At December 31, 2010, we had approximately $60.7 million of deferred tax assets against which we have recognized valuation allowances equal to the entire amount of such deferred tax assets. Losses for federal income tax purposes can generally be carried back two years and carried forward for a period of 20 years. In order to realize our net deferred tax assets, we must generate sufficient taxable income in such future years.

In addition, our ability to utilize net operating losses and certain other tax attributes ("NOLs") for federal and state income tax purposes would be limited if we were to experience an "ownership change," as determined under Section 382 of the Internal Revenue Code of 1986, as amended ("Section 382"). Generally, an "ownership change" relates to the cumulative change in ownership among stockholders with at least a 5% ownership interest in our common stock increase their ownership by more than 50% over a rolling three-year period. If an "ownership change" occurs, our ability to use the NOLs for income tax purposes could be limited substantially or lost altogether. This would significantly impair the value of our NOL asset and, as a result, have a negative impact on our financial position and results of operations.

In January 2011, our board of directors adopted a stockholder rights agreement designed to protect our ability to use the NOLs for income tax purposes. However, the adoption of the stockholder rights agreement cannot guarantee complete protection against an "ownership change" and it remains possible that one may occur.

Provisions in our charter documents and Delaware law and our NOL-related stockholders rights agreement may delay, deter or prevent the acquisition of Satcon, which could decrease the value of your shares.

Some provisions of our certificate of incorporation and bylaws may delay, deter or prevent a change in control of Satcon or a change in our management that you, as a stockholder, may consider favorable. These provisions include:

- •

- authorizing the issuance of "blank check" preferred stock that could be issued by our board of directors to increase the

number of outstanding shares and deter a takeover attempt;

- •

- a board of directors with staggered, three-year terms, which may lengthen the time required to gain control of

our board of directors;

- •

- prohibiting cumulative voting in the election of directors, which would otherwise allow less than a majority of

stockholders to elect director candidates; and

- •

- limitations on who may call special meetings of stockholders.

In addition, Section 203 of the Delaware General Corporation Law and provisions in some of our stock incentive plans may delay, deter or prevent a change in control of Satcon. Those provisions serve to limit the circumstances in which a premium may be paid for our common stock in proposed transactions, or where a proxy contest for control of our board may be initiated. If a change of control or change in management is delayed, deterred or prevented, the market price of our common stock could suffer.

We also have a stockholder rights plan designed to protect our ability to use our NOLs for federal and state income tax purposes. In general terms, the rights plan is intended to act as a deterrent to any person or group that acquires 4.99% or more of our common stock without approval of our board of directors by allowing other stockholders to acquire our equity securities at half of their fair value. The

17

ownership limitations in the rights plan may have the effect of inhibiting or impeding a change in control.

We are subject to stringent export laws and risks inherent in international operations.

We market and sell our products and services both inside and outside the United States. We are currently selling our products and services throughout North America and in certain countries in South America, Asia and Europe. Certain of our products are subject to the International Traffic in Arms Regulations (ITAR) 22 U.S.C 2778, which restricts the export of information and material that may be used for military or intelligence applications by a foreign person. Additionally, certain products of ours are subject to export regulations administered by the Department of Commerce, Bureau of Industry Security, which require that we obtain an export license before we can export certain products or technology. Failure to comply with these laws could result in enforcement responses by the government, including substantial monetary penalties, denial of export privileges, debarment from government contracts and possible criminal sanctions.

Revenue from sales to our international customers for the years ended December 31, 2010, 2009 and 2008 were approximately $97.2 million, $13.0 million and $7.9 million, respectively. Our success depends, in part, on our ability to expand our market for our products and services to foreign customers and our ability to manufacture products that meet foreign regulatory and commercial requirements. We have limited experience developing and manufacturing our products to comply with the commercial and legal requirements of international markets. We face numerous challenges in penetrating international markets, including unforeseen changes in regulatory requirements, export restrictions, fluctuations in currency exchange rates, longer accounts receivable cycles, difficulties in managing international operations, and the challenges of complying with a wide variety of foreign laws.

We are exposed to credit risks with respect to some of our customers.

To the extent our customers do not advance us sufficient funds to finance our costs during the execution phase of our contracts, we are exposed to the risk that they will be unable to accept delivery or that they will be unable to make payment at the time of delivery. Occasionally, we accept the risk of dealing with thinly financed entities. We attempt to mitigate this risk by seeking to negotiate more timely progress payments and utilizing other risk management procedures.

Our loan agreement with Silicon Valley Bank subjects us to various restrictions, which may limit our ability to pursue business opportunities.

Our loan agreement with Silicon Valley Bank subjects us to various restrictions on our ability to engage in certain activities without the prior written consent of the bank, including, among other things, our ability to:

- •

- dispose of or encumber assets, other than in the ordinary course of business,

- •

- incur additional indebtedness,

- •

- merge or consolidate with other entities, or acquire other businesses, and

- •

- make investments

The agreement also subjects us to various financial and other covenants with which we must comply on an ongoing or periodic basis. The financial covenant requires us to maintain certain operating results net of capital expenditures, which varies from quarter to quarter. If we violate this or any other covenant, any outstanding debt under this agreement could become immediately due and payable, the bank could proceed against any collateral securing indebtedness and our ability to borrow funds in the future may be restricted or eliminated. These restrictions may also limit our ability to

18

pursue business opportunities or strategies that we would otherwise consider to be in the best interests of the Company.

Our subordinated debt agreement subjects us to various restrictions, which may limit our ability to pursue business opportunities.

In June 2010, we entered into a subordinated loan agreement with Compass Horizon Funding Company LLC under which we incurred $12.0 million of indebtedness. The loan agreement subjects us to various restrictions on our ability to engage in certain activities without the prior written consent of the lender, including, among other things, our ability to dispose of or encumber certain assets, incur additional indebtedness, merge or consolidate with other entities, or make investments. As of December 31, 2010, $12 million remained outstanding. Beginning in March 2011 we are obligated to begin repaying the principal amount of the loan. Our ability to meet our debt obligations will depend upon future performance, which will be subject to financial, business and other factors affecting our operations, many of which are beyond our control.

The holders of our certain of our outstanding warrants have the right to put those warrants to us for cash if we issue common stock or common stock equivalents at a price per share less than $1.65.

As of March 1, 2011, we had outstanding Warrant As to purchase up to an aggregate of 556,061 shares of common stock and Warrant Cs to purchase up to an aggregate of 348,485shares of common stock. The holder of those warrants may put those warrants to us for a cash amount equal to their Black-Scholes value if we issue common stock or common stock equivalents at a price per share less than $1.65, subject to certain exceptions. These rights are exercisable for the 45-day period following any such issuance. The existence of these rights could limit our ability to raise necessary capital in the future. Furthermore, the exercise of these rights could materially impact our capital resources and materially affect our ability to fund operations.

We are responsible for maintaining the registration of the resale of shares of common stock issued upon conversion of our Series C Preferred Stock and related warrants with the SEC and will incur liquidated damages if we do not meet fulfill this obligation.

Pursuant to our agreement with the investors in the Series C Preferred Stock financing transaction, we were obligated to file a registration statement covering the resale of the common stock underlying the Series C Preferred Stock and related warrants with the SEC and cause the registration statement to be declared effective, which we completed. We are further obligated to use our best efforts to keep the registration statement effective until the earlier of (i) the date all of the securities covered by the registration statement have been publicly sold and (ii) the date all of the securities covered by the registration statement may be sold without restriction under SEC Rule 144. If we fail to comply with these or certain other provisions, then we will be required to pay liquidated damages of one twentieth of a percent (.05%) of the aggregate purchase price paid by the investors for the securities that can be registered on the registration statement for each day the failure continues. The total liquidated damages under this provision are capped at 9.9% of the aggregate purchase price paid by the investors in the private placement. Any such payments could materially affect our ability to fund operations.

As a result of the conversion of the Series C Preferred Stock, the former holders continue to have substantial voting power on matters submitted to our stockholders and to be able to exert considerable influence over the board level decision-making at our company.

As a result of the conversion of the Series C Preferred Stock on October 27, 2010, the former holders of the Series C Preferred Stock hold approximately 23% of our outstanding common stock. In addition, such holders own warrants to acquire approximately 13,414,272 shares of our common stock. Because these holders continue to own a significant percentage of our voting power, they have

19

considerable influence in determining the outcome of any corporate transaction or other matter submitted to our stockholders for approval, including the election of directors and approval of merger, consolidations and the sale of all or substantially all of our assets. In addition, these holders continue to be entitled to designate members of our board of directors and designees to serve on our board committees, enabling them to exert considerable influence over the board level decision-making at our company.

Item 1B. UNRESOLVED STAFF COMMENTS

None.

We lease office, manufacturing and research and development space in the following locations:

Location

|

Primary Use | Approximate Number of Square Feet |

Expiration of Lease |

||||||

|---|---|---|---|---|---|---|---|---|---|

Boston, MA |

Corporate headquarters and research and development | 28,000 | 2011 | ||||||

Boston, MA |

Research and development and manufacturing | 20,000 | 2016 | ||||||

Fremont, CA |

Sales and marketing | 20,000 | 2016 | ||||||

Burlington, Ontario, Canada |

Manufacturing | 60,000 | 2011 | ||||||

Prague, Czech Republic |

Sales and marketing | 5,000 | 2014 | ||||||

Shenzhen, China |

Sales and marketing | 8,000 | 2013 | ||||||

Shanghai, China |

Sales and marketing | 5,000 | 2014 | ||||||

We believe our facilities are adequate for our current needs and that adequate facilities for expansion, if required, are available. The lease on our corporate headquarters and our Canadian manufacturing facility expire in 2011; we have entered into a new lease for our corporates that expires in 2016 and we are in the process of extending the Canadian facility lease.

In the normal course of our business, we are party to various claims and suits pending for alleged damages to persons and property, alleged violations of certain laws and alleged liabilities arising out of matters occurring during the normal operation of our business.

We accrue for legal proceedings when losses become probable and reasonably estimable. As of the end of each applicable reporting period, we review each of our legal proceedings to determine whether it is probable, reasonably possible or remote that a liability has been incurred and, if it is at least reasonably possible, whether a range of loss can be reasonably estimated. In instances where we determine that a loss is probable and we can reasonably estimate a range of losses we may incur with respect to such a matter, we record an accrual for the amount within the range that constitutes our best estimate of the possible loss. If we are able to reasonably estimate a range but no amount within the range appears to be a better estimate than any other, we record an accrual in the amount that is the low end of such range. When a loss is reasonably possible but not probable we will not record an accrual but we will disclose our estimate of the possible range of loss where such estimate can be made. As of December 31, 2010, there were no accruals established related to our outstanding legal proceedings.

We offer no prediction of the outcome of any of the proceedings or negotiations described below. We are vigorously defending each of these lawsuits and claims. However, there can be no guarantee we

20

will prevail or that any judgments against us, if sustained on appeal, will not have a material adverse effect on our business, financial condition, results of operations or cash flows.

On February 17, 2011, FuelCell Energy, Inc. ("FuelCell Energy") filed a Demand for Arbitration with the American Arbitration Association seeking recovery of damages related to allegedly defective transformers that we procured for them. In its Demand for Arbitration, FuelCell Energy asserts that it is entitled to recovery of approximately $2.8 million from us. We vigorously deny the allegation that the transformers were defective, and have filed a counterclaim seeking recovery of amounts due to us from FuelCell Energy for materials and engineering services that we supplied to them totaling approximately $1.4 million. This matter is at the early stages of discovery, and we have not yet determined whether it is probable, reasonably possible or remote that we have incurred a liability.

21

Item 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is publicly traded on the Nasdaq Capital Market under the symbol "SATC."

The following table sets forth the range of high and low sales prices of our common stock as reported on the Nasdaq Capital Market for our years ended December 31, 2009 and 2010:

| |

High | Low | |||||

|---|---|---|---|---|---|---|---|

Year ended December 31, 2009 |

|||||||

First Quarter |

$ | 1.88 | $ | 1.10 | |||

Second Quarter |

$ | 2.43 | $ | 1.64 | |||

Third Quarter |

$ | 2.27 | $ | 1.69 | |||

Fourth Quarter |

$ | 2.82 | $ | 1.86 | |||

Year ended December 31, 2010 |

|||||||

First Quarter |

$ | 2.86 | $ | 2.20 | |||

Second Quarter |

$ | 3.08 | $ | 2.25 | |||

Third Quarter |

$ | 3.84 | $ | 2.72 | |||

Fourth Quarter |

$ | 4.74 | $ | 3.40 | |||

On March 1, 2011, the last reported sale price of our common stock as reported on the Nasdaq Capital Market was $3.26 per share. As of March 1, 2011, there were 118,908,772 shares of our common stock outstanding held by approximately 225 holders of record. The number of record holders does not include beneficial owners of common stock whose shares are held in the names of banks, brokers, nominees or other fiduciaries.

Dividend Policy

We have never paid cash dividends on our common stock. We currently intend to retain earnings, if any, to fund the development and growth of our business and do not anticipate paying cash dividends for the foreseeable future. Payment of future cash dividends, if any, will be at the discretion of our board of directors after taking into account various factors, including our financial condition, operating results, current and anticipated cash needs and plans for expansion.. Finally, under our credit facility with Silicon Valley Bank, we may not pay dividends on our common stock without the consent of the Bank.

Recent Sales of Unregistered Securities

None

22

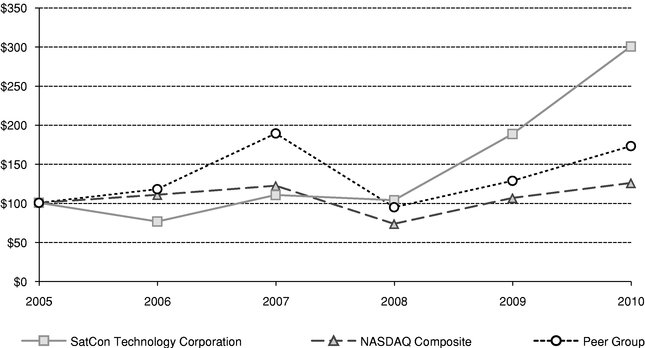

Comparative Stock Performance Graph

The comparative stock performance graph below compares the cumulative total stockholder return (assuming reinvestment of cash dividends, if any) from investing $100 on December 31, 2005, and plotted at the end of the last trading day of each fiscal year, in each of (i) the Corporation's Common Stock; (ii) the Nasdaq National Market Index of U.S. Companies (the "Nasdaq Market Index"); and (iii) a peer group index of five companies that provide similar services to those of the Corporation (Advanced Energy Industries, Inc, Power-One, Inc., Schneider Electric, SA, Siemens AG, and SMA Solar Technologies AG,) (the "Peer Group Index")).

COMPARISON OF CUMULATIVE TOTAL RETURN*

Among SatCon Technology Corporation, the NASDAQ Composite Index

and a Peer Group

- *

- Assumes

$100 invested on 1/1/2006 in stock or index, including reinvestment of dividends.

Fiscal year ending December 31.

| |

Period Ending | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Company/Market/Peer Group

|

12/31/2005 | 12/31/2006 | 12/31/2007 | 12/31/2008 | 12/31/2009 | 12/31/2010 | |||||||||||||

SatCon Technology Corporation |

$ | 100.00 | $ | 76.00 | $ | 110.00 | $ | 103.33 | $ | 188.00 | $ | 300.00 | |||||||

NASDAQ Composite |

$ | 100.00 | $ | 110.25 | $ | 121.88 | $ | 73.10 | $ | 106.22 | $ | 125.36 | |||||||

Peer Group |

$ | 100.00 | $ | 117.43 | $ | 188.73 | $ | 94.32 | $ | 128.13 | $ | 172.54 | |||||||

23

Item 6. SELECTED CONSOLIDATED FINANCIAL DATA

You should read the data set forth below in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes appearing elsewhere in this Annual Report on Form 10-K. The selected consolidated financial data set forth below for the years ended December 31, 2010, 2009 and 2008, and the consolidated balance sheet data as of December 31, 2010 and 2009 are derived from our audited consolidated financial statements appearing elsewhere in this Annual Report on Form 10-K. The selected consolidated statement of operations data for the year ended December 31, 2006 and 2007 and the consolidated balance sheet data as of December 31, 2007 and 2006 are derived from our audited consolidated financial statements that are not included in this Annual Report on Form 10-K. All data set forth below has been adjusted to reflect the classification of our Applied Technology business unit's assets as a discontinued operation, as the sale was finalized in the first quarter of 2010, along with the sale of our Electronics and Power Systems US business units, which were finalized in the third quarter of 2008. The results of operations for the Applied Technology, the Electronics and the Power Systems US business units are captured in the line item "Loss from discontinued operations" below. See Note D (Discontinued Operations) to the Consolidated Financial Statements included in this annual report.

| |

Year Ended December 31, | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||

Statement of Operations Data |

|||||||||||||||||

Product revenue |

$ | 173,302 | $ | 52,536 | $ | 54,293 | $ | 33,033 | $ | 14,164 | |||||||

Cost of product revenue |

129,360 | 49,334 | 45,818 | 33,456 | 13,545 | ||||||||||||

Gross margin |

43,942 | 3,202 | 8,475 | (423 | ) | 619 | |||||||||||

Operating expenses: |