Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HEADWATERS INC | d8k.htm |

| EX-99.3 - PRESS RELEASE - HEADWATERS INC | dex993.htm |

| EX-99.1 - PRESS RELEASE - HEADWATERS INC | dex991.htm |

Exhibit 99.2

HEADWATERS INCORPORATED

SUPPLEMENTAL REGULATION FD DISCLOSURE STATEMENT

DATED OCTOBER 13, 2009

SUMMARY

You should read the following summary together with the more detailed information and consolidated financial statements and their notes included in Headwaters Incorporated’s Annual Report filed on Form 10-K for the year ended September 30, 2010, referred to as the 2010 Form 10-K, and in Headwaters Incorporated’s Quarterly Report filed on Form 10-Q for the three months ended December 31, 2010, referred to as the December 2010 Form 10-Q. The press release dated March 2, 2011 describing the offering of Headwaters’ senior secured notes (the “Secured Notes”) included on Exhibit 99.1 to Headwaters’ Form 8-K filed with the Securities Exchange Commission on March 2, 2011 is referred to in this disclosure statement as the “Secured Notes Offering Press Release.” In this disclosure statement, unless otherwise indicated or the context otherwise requires, the terms “Headwaters,” “we,” “us,” and “our” refer to Headwaters Incorporated and its subsidiaries. Certain other capitalized terms used in this disclosure statement are defined in the 2010 Form 10-K, the December 2010 Form 10-Q or elsewhere in this disclosure statement.

Non-GAAP Financial Data

EBITDA and Adjusted EBITDA presented in this disclosure statement are supplemental measures that are not required by, or presented in accordance with, generally accepted accounting principles in the United States (“GAAP”).

EBITDA and Adjusted EBITDA are not measurements of our financial performance under GAAP and should not be considered as alternatives to net income, operating income or any other performance measures derived in accordance with GAAP or as a measure of our liquidity. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow available for management’s discretionary use, as they do not consider certain cash requirements such as interest payments, tax payments and debt service requirements. In addition, our method of calculating EBITDA and Adjusted EBITDA may vary from the method used by other companies. We have used the method for calculating EBITDA used historically. Although Adjusted EBITDA contains certain additional adjustments, our management considers Adjusted EBITDA to be a key indicator of financial performance. Adjusted EBITDA contains certain adjustments that do not comply with the SEC’s rules governing the use of non-GAAP financial measures.

We believe EBITDA and Adjusted EBITDA are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. In addition, we believe that investors, analysts and rating agencies consider EBITDA and Adjusted EBITDA useful means of measuring our ability to meet our debt service obligations and evaluating our financial performance, and management uses these measurements for one or more of these purposes. Our presentation of EBITDA and Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or nonrecurring items. EBITDA and Adjusted EBITDA have important limitations as analytical tools and you should not consider them in isolation or as a substitute for analysis of our results as reported under GAAP. Because of these limitations, EBITDA and Adjusted EBITDA should not be considered as measures of discretionary cash available to us to service our indebtedness or invest in our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only for supplemental purposes.

Our Company

Headwaters is a diversified company providing products, technologies and services to the building products, construction materials and energy industries. We have leadership positions in many of the product categories in which we compete. We generate revenue by selling building products such as manufactured architectural stone, siding accessory products and concrete blocks; managing and marketing coal combustion products (“CCPs”), which are used as a replacement for cement in concrete; and reclaiming waste coal. We intend to continue expanding our business through growth of existing operations and commercialization of new technologies and products.

We conduct our business primarily through the following three reporting segments: light building products; heavy construction materials; and energy technology.

Light Building Products

We compete in the light building products industry, which is currently our largest reporting segment based on revenue. Our light building products segment generated approximately $315.4 million in revenue for the twelve months ended December 31, 2010. Our light building products segment has leading positions in several light building products categories.

We are a leading designer, manufacturer and marketer of siding accessories as well as professional tools used in residential home improvement and construction. Our siding accessories include decorative window shutters, gable vents, and mounting blocks for exterior fixtures, roof ventilation, window and door trim products. We also market functional shutters and storm protection systems, specialty siding products, specialty roofing products, trim board and window wells. Our siding accessory sales are primarily driven by the residential repair and remodeling construction market and, to a lesser extent, by the new residential construction market.

We are a leading producer of manufactured architectural stone. Our Eldorado Stone product line is designed and manufactured to be one of the most realistic manufactured architectural stone products in the world. We utilize two additional brands to segment the manufactured architectural stone market and sell at lower price points than the Eldorado Stone product line, allowing us to compete across a broad spectrum of customer profiles. Eldorado Stone’s sales are driven by new residential construction and residential repair and remodeling, as well as commercial construction markets.

We are the largest manufacturer of concrete block in the Texas market, which we believe to be one of the largest concrete block markets in the United States. We offer a variety of concrete based masonry unit products and employ a regional branding and distribution strategy. A large portion of our sales are generated from the institutional construction markets in Texas, including school construction, allowing us to benefit from positive demographic trends.

We have a large customer base for our building products, represented by approximately 5,200 non-retail ship-to locations and approximately 6,100 retail ship-to locations across the country. Sales are broadly diversified by serving a large variety of customers in various distribution channels. We believe we attract a large base of customers because we continually upgrade our product offerings through product extensions and new products and brands.

Heavy Construction Materials

We compete in the heavy construction materials industry and generated approximately $265.6 million in revenue for the twelve months ended December 31, 2010. We are the national leader in the management and marketing of CCPs, procuring CCPs from coal-fueled electric generating utilities and supplying them to our customers for use in a variety of concrete infrastructure and building projects. CCPs, such as fly ash and bottom ash, are the non-carbon components of coal that remain after coal is burned. CCPs have traditionally been an environmental and economic burden for power generators but can be a source of value when properly managed.

Fly ash is most valuable when it is used as a replacement for a portion of the portland cement used in concrete. Concrete made with fly ash has better performance characteristics than concrete made only from portland cement, including improved durability, decreased permeability and enhanced corrosion-resistance. Further, concrete made with CCPs is easier to work with than concrete made only with portland cement, due in part to its better pumping and forming properties. Because fly ash is generally less expensive per ton than portland cement, the manufacturing cost of concrete made using fly ash as a partial replacement for portland cement can be lower than the manufacturing cost of concrete made exclusively with portland cement.

In order to ensure a steady and reliable supply of CCPs, we have entered into numerous long-term and exclusive management contracts with coal-fueled electric generating utilities, maintain 22 stand-alone CCP distribution terminals across North America and support approximately 100 plant-site supply facilities. We own or lease approximately 1,100 rail cars and more than 175 trucks, in addition to contracting with other carriers in order to meet transportation needs for the marketing and disposal of CCPs. Our extensive

distribution network allows us to transport CCPs across the nation, including into states that represent important construction markets but that have a low production of CCPs.

Our heavy construction materials business has grown with the expanded commercial use of CCPs and continues to support market recognition of the performance, economic and environmental benefits of CCPs. According to American Coal Ash Association (“ACAA”) 2009 estimates, coal ash replaced over 17% of the portland cement consumed in the United States.

In June 2010, the EPA proposed two alternative rules to regulate CCPs generated by electric utilities and independent power producers. One proposed option would classify CCPs disposed of in surface impoundments or landfills as “special wastes” subject to federal waste regulation under Subtitle C of the Resource Conservation and Recovery Act (“RCRA”). The second proposed option would instead regulate CCPs as solid waste under Subtitle D of RCRA, with states retaining the lead authority on regulating their handling, storage and disposal. The EPA has conducted multiple hearings on the proposed regulations and has received over 400,000 comments. No formal timeline has been established for the promulgation of a final regulatory proposal. See “Risk Factors—Risks Relating to Our Business—The EPA has proposed two alternative rules under RCRA to regulate CCPs to address environmental risks from the disposal of CCPs. Either option is likely to have an adverse effect on the cost of managing and disposing of CCPs. The option of regulating CCPs as hazardous waste would likely have an adverse effect on beneficial use and sales of CCPs and HRI’s relationship with utilities.”

Energy Technology

We are a leader in coal cleaning and coal upgrading, and have other technologies that enhance the value of coal and oil feedstocks. Our energy technology business generated approximately $88.8 million in revenue for the twelve months ended December 31, 2010. We own and operate coal cleaning facilities that separate ash from waste coal to provide a refined coal product that is higher in Btu value and lower in impurities than the feedstock coal. The cleaned coal is sold primarily to electric power plants and other industrial users, but approximately 25% of our production meets metallurgical coal standards and is sold to steel companies. This clean coal technology allows mining companies to reclaim waste coal sites and return them to a state of beneficial use. By December 2008, we had completed construction and operation of eleven coal cleaning facilities, eight of which are currently operating.

These facilities produce coal that results in reduced sulfur oxides, nitrogen oxides and mercury emissions from waste coal, greatly increasing its cleanliness and usability. The cleaned coal product is comparable in energy content and ash to run-of-mine coal products. We believe that our sales of cleaned coal products sold into the steam market will continue to generate refined coal tax credits under Section 45 of the Internal Revenue Code (“Section 45”). While our coal cleaning business incurred an operating loss in fiscal 2010, it generated Adjusted EBITDA of $1.2 million, including Section 45 tax credits.

Our energy technology segment has also developed and licensed a proprietary technology that improves catalytic heavy oil hydrocracking, or upgrading, in petroleum refineries with ebullated bed upgrading units. This HCAT® hydrocracking technology enables those refineries to operate at a higher level of residue conversion, or to utilize lower-cost opportunity crude feedstocks, for the production of distillate transportation fuels such as diesel and gasoline. The first full-time customer of Headwaters’ HCAT technology is Neste Oil, who conducted long-term trials in 2010 and now utilizes the process on an ongoing basis at their Porvoo Refinery in Finland. The combination of the HCAT molecular-scale liquid catalyst additive with conventional, solid, ebullated bed catalysts has been proven at Neste’s refinery and in other commercial plant trials as well as in pilot plant studies. HCAT improves the performance of existing ebullated bed upgrading units by not only making higher residue conversion possible, but also higher throughput, while simultaneously reducing sediment and improving byproduct fuel oil qualities. We have received inquiries and are developing proposals for several of the currently-operating ebullated bed units in North America, Europe, Middle East and Asia, and expect to have HCAT considered for inclusion in most if not all of the new ebullated bed projects currently in development.

In addition, we are also involved in production of ethanol and technology and licensing development for liquefaction of coal into liquid fuels.

Our Strengths

Market Leadership Positions in Diversified End Markets. We have leading market positions in multiple categories of both residential and non-residential building products that are used primarily in exterior siding applications. We are the number one national provider of siding accessories, which are principally used for residential repair and remodeling projects and to a lesser extent for new residential construction. We are a leading national producer of manufactured architectural stone siding, which is used in both residential and commercial construction. We are the number one producer of concrete block in the Texas market, which is used for institutional and commercial construction applications. We are the number one national supplier of CCPs. Our market share for high value CCPs in concrete products has increased from 38% to 46% from fiscal 2001 through fiscal 2010. We believe our market

leadership positions help us generate profit margins at the top of our light building products and heavy construction materials peer groups. We also believe our diversification within various construction end markets, along with our energy markets, provide more business stability than we would otherwise experience by participating in just one end market.

Strong Brand Recognition. Headwaters has strong brand recognition in the building products industry. We are widely recognized for our siding accessories that enhance the appearance of homes while delivering durability at a lower cost compared to similar aluminum, wood and plastic products. We leverage a multi-brand strategy to market similar products through various distribution channels. For example, we distribute our Builders Edge brand of shutters through The Home Depot and our Mid-America brand of shutters through the wholesale channel. We are able to capture a larger percentage of the market with this segmentation strategy. We believe our various product brands are among the most recognized brands in the siding accessory market and that these brands are recognized for quality, performance and aesthetics. Under our Eldorado Stone, StoneCraft and Dutch Quality Stone brands we market a wide variety of manufactured architectural stone products that offer high aesthetic quality, ease of installation, durability and reasonable cost to meet a variety of design needs and price points. We have a strong regional brand in the Texas concrete block market. We believe our strong brand recognition helps us increase demand for our building products and maintain our market leadership positions, and gives us the flexibility to further segment the market by customer type and by distribution channel.

Extensive and Established National Distribution Networks. We maintain sophisticated distribution systems in both our light building products and heavy construction materials segments. We have extensive distribution networks that provide national marketing and sales opportunities for our diversified portfolio of light building products. We maintain an extensive distribution network that consists of substantially all of the major vinyl siding, roofing and window distributors in the United States. We believe our penetration of these channels is due to contractor loyalty to our brands instilled by the quality and breadth of our products and our high level of services to distributors, including rapid order fulfillment. We distribute our manufactured architectural stone products on a wholesale basis through a network of distributors, including masonry and stone suppliers, roofing and siding materials distributors, fireplace suppliers and other specialty contractor stores.

In addition, we believe we have the most extensive CCP infrastructure in the United States with 22 stand-alone CCP distribution terminals across North America, as well as approximately 100 plant site facilities. We believe our extensive distribution network across all our businesses has been a key factor in our growth because it allows us to add other products which we have developed internally or acquired through strategic acquisitions, rapidly increasing sales opportunities.

Long-Term Customer Relationships and Exclusive Supply Contracts. We have developed attractive, long-term relationships with numerous important customers. Our light building products business enjoys a large customer base with over 5,200 non-retail ship-to-locations and more than 6,100 retail ship-to-locations. The non-retail channel consists of wholesale distributors, with some of these customer relationships in effect for more than 30 years. The wholesale distribution customers are very attractive to us due to the relationships they develop and maintain with the contractors who install the building products. Contractors have tended to continue using the products that they have grown accustomed to installing and the manufacturers upon whom they have come to rely for excellent product quality and customer service. Because we have consistently delivered high quality products on a timely basis for contractors, the wholesale channel has rewarded us with relationships that have grown and strengthened over the years. We have also developed relationships within the retail distribution channel. We have been supplying products to The Home Depot and Lowe’s for more than 15 years. We are the national vendor of choice to The Home Depot for shutters and the national vendor of choice to Lowe’s for mounting blocks and gable vents.

Our heavy construction materials segment has established long-term relationships and exclusive CCP management contracts with many of the nation’s major coal-fueled electric generating utilities. We contract with these utilities to manage and market CCPs, including high-value CCPs that are used as a replacement for portland cement and can also be used in many products manufactured in our light building products segment. We currently provide CCP management services at approximately 100 locations.

Well Positioned to Benefit from a Rebound in Housing Markets. Our light building products business relies on the home improvement and remodeling markets as well as new construction. As a result of the challenging housing market environment, we have taken significant actions to right size our manufacturing capacity and reduce our segment and corporate overhead. Given our market leadership positions and reduced cost structure, we believe that we are positioned to benefit from a rebound in the housing market when it occurs. We believe the long-term growth prospects in the industry are strong because the current seasonally-adjusted annualized housing starts are still well below the 10-year and 50-year averages. According to the National Association of Home Builders, new housing starts were 0.55 million and 0.59 million units in calendar 2009 and 2010, respectively, compared to 10- and 50-year averages of 1.4 million and 1.5 million units, respectively. The Leading Indicator of Remodeling Activity estimate issued by the Harvard University Joint Center for Housing Studies shows that the four-quarter moving average peaked at $146.2 billion in the second quarter of calendar 2007, fell to $112.0 billion in the fourth quarter of calendar 2009, and then rose to $115.9 billion in the third quarter of calendar 2010. That same center has estimated that the four-quarter moving average will be $123.5 billion in the third quarter of calendar 2011, which would be the highest level since the second quarter of calendar 2008. According to the Harvard Joint Center, the nation’s housing stock will have to accommodate approximately 12.5 million to 14.8 million additional households due to population growth over the next decade, or approximately 1.3 million to 1.5 million additional households per year.

Our Strategy

Introduce New Products and Brands to Leverage our Distribution System. We have a longstanding tradition of developing and commercializing innovative building products and technologies to better serve our customers. For example, we were the first company to introduce injection-molded shutters, vents and mounting blocks. In addition, we enhance existing products and introduce new brands in response to specific customer needs and market demand. We have one of the most extensive distribution networks in the building products industry, allowing us to reach most of the major vinyl siding, roofing, window and masonry distributors in the United States. This extensive distribution network provides us with an existing outlet for our newly developed or acquired products to quickly expand sales of such products. For example, in 2009 we added a Weathered Collection and a perfection shingle to our Foundry product offering. In 2010, our Foundry sales increased 14.9% over sales in 2009 and in 2010 these two new product offerings constituted more than 25% of sales from our Foundry offerings. We have expanded our new products and brands organically and through small acquisitions by introducing them into our national distribution system. We estimate that our sales of internally-developed and acquired new products and new brands within our light building products business grew from approximately 4% of annual sales in fiscal 2004 to 22% of annual sales in fiscal 2010. Included in this growth are sales from specialty siding, architectural brick, synthetic slate roofing, trim board, and sales of our Dutch Quality and Stonecraft branded manufactured architectural stone.

Grow Headwaters Resources Through Optimizing Our Distribution System, Increasing Supply and Expanding Services. We have the most extensive CCP infrastructure in the U.S., and are the only distributor of fly ash with a national reach. This infrastructure allows us to pursue CCP supply contracts throughout the nation and gives us an advantage when competing for supply contracts. We believe our industry-leading distribution network has been a significant factor in our historical growth and positions us well for future growth. We continue to grow our supply of high quality fly ash through extension of our distribution and storage system, blending fly ash to achieve a desired level of quality, and extending our existing exclusive supply agreements. Further, we have undertaken to increase our service work provided to utilities as our service revenue has been stable and provides additional interaction with utilities which could be suppliers of fly ash. This service work has been branded under Headwaters Plant Services (“HPS”) and we believe that HPS is the largest provider of plant services to the utility industry. As noted above and elsewhere in this offering memorandum, the EPA has proposed new rules potentially regulating the storage and/or usage of coal ash. Depending on the scope and nature of any rules actually adopted, there may be additional opportunities for us to increase the revenue we generate from assisting utilities with the management of their CCPs. Service revenue has grown from 18% to 30% of HRI’s revenues from fiscal 2007 to 2010.

Expand the Use of CCPs. We undertake a variety of marketing efforts to expand the use of CCPs and emphasize the performance value of CCPs, as well as the attendant benefits such as conserving landfill space and reducing greenhouse gases. These activities include professional outreach, technical publications, relationships with industry organizations, and involvement in legislative initiatives leading to greater use of CCPs. In addition, we have developed several specialty products that increase market penetration of CCPs and name recognition for our products for road bases, structural fills and industrial fillers. We have also developed new products that utilize high volumes of CCPs. For example, through research and development activities, we developed two products to utilize the fly ash generated at fluidized bed combustion (“FBC”) power plants, which is generally unsuitable for use in traditional concrete applications. We have also developed technologies that maintain or improve the quality of CCPs, further expanding and enhancing their marketability. To date, the value of utilizing CCPs in concrete has been recognized by federal and many state agencies. The EPA has historically encouraged CCP utilization in federal and state transportation projects because of improved concrete characteristics, reduced landfill usage and an indirect reduction in carbon dioxide. However, the EPA has proposed new rules potentially regulating the storage and/or use of fly ash. See “Risk Factors—Risks Relating to Our Business—If the EPA adopts more stringent regulations under the Clean Air Act or Clean Water Act governing coal combustion, water discharges at coal mines and power plants, or power plant cooling water, this would likely have an adverse effect on the cost, beneficial use and sales of CCPs.”

Focus on Continuous Improvement to Position our Business for Macroeconomic Recovery.

We are actively engaged in continuous improvement in all three of our operating segments. In 2010, our Adjusted EBITDA improved by 25% over 2009, even though revenue declined, primarily as a result of our cost reduction and improvement activities. For example, our accessory products business, through a combination of alternative material sourcing, scrap reduction, energy cost reduction and process improvements, has reduced its manufacturing costs in 2010 by approximately $3 million over 2009. We are implementing purchasing best practices in our three segments, and anticipate additional cost savings in 2011 and 2012.

Recent Developments

Tender Offer and Consent Solicitation for 11 3/8% Senior Secured Notes due 2014

On February 15, 2011, we commenced a cash tender offer to purchase any and all of the outstanding $328.3 million aggregate principal amount of our outstanding 11 3/8% Senior Secured Notes due 2014 (“the “11 3/8% Notes”) (the “Tender Offer”) and a consent solicitation to amend the related indenture to eliminate substantially all of the restrictive covenants and certain events of default. We intend to use the proceeds of the offering of the secured notes to purchase the 11 3/8% Notes tendered and to pay related transaction fees and expenses. Completion of the Tender Offer is conditioned upon, among other things, our having received the proceeds of this offering, which is our proposed financing for the Tender Offer and related consent solicitation.

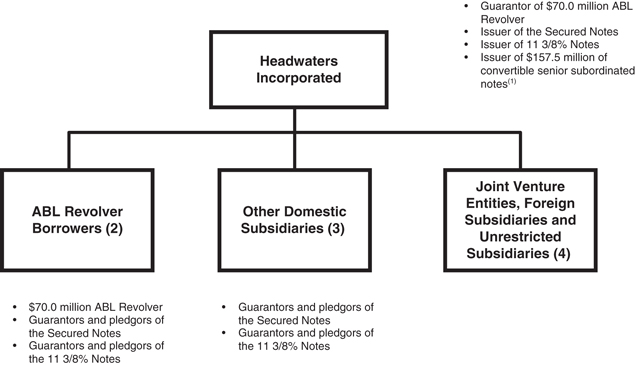

Corporate Structure

The chart below is a summary of our organizational structure and illustrates the long-term debt that will be outstanding following the offering of notes and the Tender Offer.

| (1) | Consists of 16% Convertible Senior Subordinated Notes due 2016, 2.50% Convertible Senior Subordinated Notes due 2014 and 14.75% Convertible Senior Subordinated Notes due 2014. The aggregate amount of such notes net of discount is $136.2 million. |

| (2) | Headwaters Construction Materials, Inc. and Tapco International Corporation and their operating subsidiaries and Headwaters Resources Inc. and its operating subsidiaries are borrowers under the ABL Revolver. |

| (3) | Headwaters Energy Services and its subsidiaries and Headwaters Plant Services, Inc. |

| (4) | HES Ethanol Holdings LLC (owner of 51% interest in ethanol plant), Flexcrete Building Systems, LC (90% owned), American Lignite Energy, LLC (40% owned) and Coal Creek Drying and Storage, LLC (20% owned). |

Summary Financial and Operating Data

The following table sets forth a summary of our consolidated financial data. We derived the summary consolidated financial data as of September 30, 2009 and 2010 and for the years ended September 30, 2008, 2009 and 2010 from the audited consolidated financial statements and related notes included in the 2010 Form 10-K. We derived the summary consolidated financial data as of December 31, 2010 and for the three month periods ended December 31, 2009 and 2010 from the unaudited condensed consolidated financial statements contained in the December 2010 Form 10-Q, which, in the opinion of our management, have been prepared on the same basis as the audited financial statements and reflect all adjustments, consisting only of normal recurring adjustments necessary for a fair presentation of our results of operations and financial position for such periods. We derived the financial information as of September 30, 2008 from our audited consolidated financial statements that are not included in this disclosure statement. We derived the financial information as of December 31, 2009 from our unaudited condensed consolidated financial statements that are not included in this disclosure statement. Results for the three month periods ended December 31, 2009 and 2010 are not indicative of results that may be expected for the entire fiscal year or any future period. We have derived the summary consolidated financial data for the twelve months ended December 31, 2010 by adding the financial data from our audited consolidated financial statements for the year ended September 30, 2010 to the financial data from our unaudited condensed consolidated financial statements for the three months ended December 31, 2010 and subtracting the financial data from our unaudited condensed consolidated financial statements for the three months ended December 31, 2009. Results for the twelve months ended December 31, 2010 are not indicative of results that may be expected in the future. The summary consolidated financial data set forth below should be read in conjunction with, and is qualified by reference to, the discussion under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the audited consolidated financial statements and unaudited condensed interim financial statements and accompanying notes included in the 2010 Form 10-K and the December 2010 Form 10-Q.

| Year ended September 30, | Three Months Ended December 31, |

Twelve months ended December 31, 2010 |

||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||

| Revenue: |

||||||||||||||||||||||||

| Light building products |

$ | 457,008 | $ | 340,688 | $ | 316,884 | $ | 71,231 | $ | 69,709 | $ | 315,362 | ||||||||||||

| Heavy construction materials |

313,373 | 260,934 | 258,264 | 55,875 | 63,215 | 265,604 | ||||||||||||||||||

| Energy technology |

116,023 | 65,054 | 79,551 | 12,540 | 21,777 | 88,788 | ||||||||||||||||||

| Total revenue |

886,404 | 666,676 | 654,699 | 139,646 | 154,701 | 669,754 | ||||||||||||||||||

| Cost of revenue: |

||||||||||||||||||||||||

| Light building products |

337,315 | 258,809 | 227,637 | 52,638 | 53,849 | 228,848 | ||||||||||||||||||

| Heavy construction materials |

226,077 | 186,067 | 192,785 | 43,393 | 48,352 | 197,744 | ||||||||||||||||||

| Energy technology |

90,201 | 75,252 | 70,962 | 14,230 | 19,685 | 76,417 | ||||||||||||||||||

| Total cost of revenue |

653,593 | 520,128 | 491,384 | 110,261 | 121,886 | 503,009 | ||||||||||||||||||

| Gross profit |

232,811 | 146,548 | 163,315 | 29,385 | 32,815 | 166,745 | ||||||||||||||||||

| Year ended September 30, | Three Months Ended December 31, |

Twelve months ended December 31, 2010 |

||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||

| Amortization |

22,396 | 23,358 | 22,218 | 5,611 | 5,547 | 22,154 | ||||||||||||||||||

| Research and development |

14,996 | 9,774 | 8,212 | 1,915 | 1,945 | 8,242 | ||||||||||||||||||

| Selling, general and administrative |

143,300 | 115,902 | 113,481 | 28,187 | 27,776 | 113,070 | ||||||||||||||||||

| Asset impairments |

0 | 0 | 37,962 | 0 | 0 | 37,962 | ||||||||||||||||||

| Goodwill impairment |

205,000 | 465,656 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Total operating expenses |

385,692 | 614,690 | 181,873 | 35,713 | 35,268 | 181,428 | ||||||||||||||||||

| (14, | ||||||||||||||||||||||||

| Operating loss |

(152,881 | ) | (468,142 | ) | (18,558 | ) | (6,328 | ) | (2,453 | ) | (14,683 | ) | ||||||||||||

| Other Income (expense): |

||||||||||||||||||||||||

| Net interest expense |

$ | (29,775 | ) | $ | (46,101 | ) | $ | (71,618 | ) | $ | (17,420 | ) | $ | (16,994 | ) | $ | (71,192 | ) | ||||||

| Other, net |

6,499 | (1,841 | ) | 4,479 | 1,280 | 320 | 3,519 | |||||||||||||||||

| Total other income (expense), net |

(23,276 | ) | (47,942 | ) | (67,139 | ) | (16,140 | ) | (16,674 | ) | (67,673 | ) | ||||||||||||

| Loss before income taxes |

(176,157 | ) | (516,084 | ) | (85,697 | ) | (22,468 | ) | (19,127 | ) | (82,356 | ) | ||||||||||||

| Income tax benefit (provision) |

2,691 | 90,399 | 36,215 | 8,570 | (1,560 | ) | 26,085 | |||||||||||||||||

| Net loss |

$ | (173,466 | ) | $ | (425,685 | ) | $ | (49,482 | ) | $ | (13,898 | ) | $ | (20,687 | ) | $ | (56,271 | ) | ||||||

| Other Financial Data: |

||||||||||||||||||||||||

| Operating income (loss) without goodwill impairment and other impairments |

$ | 52,119 | $ | (2,486 | ) | $ | 19,404 | $ | (6,328 | ) | $ | (2,453 | ) | $ | 23,279 | |||||||||

| Adjusted EBITDA(1) |

110,065 | 78,973 | 95,381 | 14,560 | 17,870 | 98,691 | ||||||||||||||||||

| Adjusted EBITDA margin(2) |

13.4 | % | 11.8 | % | 14.6 | % | 10.4 | % | 11.6 | % | 14.7 | % | ||||||||||||

| Capital expenditures |

$ | 116,201 | $ | 64,208 | $ | 25,316 | $ | 7,329 | $ | 5,203 | $ | 23,190 | ||||||||||||

| Cash paid for interest |

26,113 | 31,808 | 56,345 | 12,300 | 13,853 | 57,898 | ||||||||||||||||||

| Total secured debt(3) |

200,000 | 188,000 | 328,250 | 328,250 | 328,250 | 328,250 | ||||||||||||||||||

| Total secured debt / Adjusted EBITDA(4) |

3.3x | |||||||||||||||||||||||

| Adjusted EBITDA / cash paid for interest(5) |

1.7x | |||||||||||||||||||||||

| Balance Sheet Data (at period end): |

||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 21,637 | $ | 15,934 | $ | 90,984 | $ | 90,288 | $ | 67,998 | ||||||||||||||

| Net property, plant and equipment |

304,835 | 321,316 | 268,650 | 317,223 | 263,628 | |||||||||||||||||||

| Total assets |

1,400,853 | 891,182 | 888,974 | 932,704 | 838,384 | |||||||||||||||||||

| Total liabilities |

744,809 | 566,462 | 607,033 | 619,609 | 575,727 | |||||||||||||||||||

| Total stockholders’ equity |

656,044 | 324,720 | 281,941 | 313,095 | 262,657 | |||||||||||||||||||

| (1) | EBITDA is defined as net income (loss) plus net interest expense, income taxes (as defined), depreciation and amortization, stock-based compensation, foreign currency translation gain or loss and goodwill and other impairments. Adjusted EBITDA is defined to exclude the impact of our former Section 45K business which was not conducted after December 31, 2007, a one-time gain on the sale of our mortars and stuccos business, one-time gains on convertible debt exchanges, severance costs, asset impairments and other items as described below. |

EBITDA and Adjusted EBITDA are not measurements of our financial performance under GAAP and should not be considered as alternatives to net income, operating income or any other performance measure derived in accordance with GAAP or as a measure of our liquidity. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow available for management’s discretionary use, as they do not consider certain cash requirements such as interest payments, tax payments and debt service requirements. Our presentations of EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider them in isolation, or as a substitute for analysis of our results as reported under GAAP. Because the definitions of EBITDA and Adjusted EBITDA (or similar measures) may vary among companies and industries, they are not comparable to other similarly-titled measures used by other companies. See “Non-GAAP Financial Data.” Our presentations of EBITDA and Adjusted EBITDA may not be in accordance with current SEC practice or with regulations adopted by the SEC that apply to registration statements filed under the Securities Act and periodic reports presented under the Exchange Act.

EBITDA and Adjusted EBITDA are calculated as follows:

| Year ended September 30, | Three months ended December 31, |

Twelve months ended December 31, 2010 |

||||||||||||||||||||||

| 2008 | 2009 | 2010 | 2009 | 2010 | ||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Net loss |

$ | (173,466 | ) | $ | (425,685 | ) | $ | (49,482 | ) | $ | (13,898 | ) | $ | (20,687 | ) | $ | (56,271 | ) | ||||||

| Goodwill impairment |

205,000 | 465,656 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| Income taxes(a) |

8 | (82,108 | ) | (29,808 | ) | (10,260 | ) | 4,436 | (15,112 | ) | ||||||||||||||

| Net interest expense |

29,775 | 46,101 | 71,618 | 17,420 | 16,994 | 71,192 | ||||||||||||||||||

| Depreciation and amortization |

68,884 | 66,073 | 60,398 | 14,164 | 15,086 | 61,320 | ||||||||||||||||||

| Stock-based compensation and foreign currency translation gain / loss |

11,920 | 4,005 | 2,119 | 534 | 1,061 | 2,646 | ||||||||||||||||||

| Inducement loss on debt to equity exchange and additional book gain on convertible debt exchange |

0 | 31,362 | 0 | 0 | 0 | 0 | ||||||||||||||||||

| EBITDA |

$ | 142,121 | $ | 105,404 | $ | 54,845 | $ | 7,960 | $ | 16,890 | $ | 63,775 | ||||||||||||

| Section 45K(b) |

(25,276 | ) | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||

| Gain on sale of mortars and stuccos business(c) |

(7,612 | ) | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||

| Gain on convertible debt exchanges(d) |

0 | (29,304 | ) | 0 | 0 | 0 | 0 | |||||||||||||||||

| Severance costs |

832 | 2,873 | 0 | 0 | 980 | 980 | ||||||||||||||||||

| Non-recurring banking fees |

0 | 0 | 3,300 | 3,300 | 0 | 0 | ||||||||||||||||||

| Litigation settlement |

0 | 0 | 1,550 | 0 | 0 | 1,550 | ||||||||||||||||||

| Section 45 tax credit adjustments |

0 | 0 | 1,600 | 3,300 | 0 | (1,700 | ) | |||||||||||||||||

| Asset impairments(e) |

0 | 0 | 37,962 | 0 | 0 | 37,962 | ||||||||||||||||||

| Gain on sale of South Korean joint venture |

0 | 0 | (3,876 | ) | 0 | 0 | (3,876 | ) | ||||||||||||||||

| Adjusted EBITDA |

$ | 110,065 | $ | 78,973 | $ | 95,381 | $ | 14,560 | $ | 17,870 | $ | 98,691 | ||||||||||||

| (a) | Income taxes differ from income tax benefit (provision) primarily due to income tax credits that are already included in Net income (loss). |

| (b) | Represents our Section 45K business. By law, Section 45K tax credits for synthetic fuel produced from coal expired for synthetic fuel sold after December 31, 2007. With the expiration of Section 45K at the end of calendar 2007, our licensees’ synthetic fuel facilities and the facilities we owned were closed because production of synthetic fuel was not profitable absent the tax credits. |

| (c) | Represents the gain recognized in fiscal 2008 on the sale of our non-strategic mortar/stucco assets in our light building products segment. |

| (d) | Represents the gains recognized on the extinguishments of convertible debt in fiscal 2009. |

| (e) | Represents a $34,500 impairment on our coal cleaning assets and a $3,462 impairment on certain assets in our heavy construction materials segment. |

| (2) | Adjusted EBITDA margin is calculated by dividing Adjusted revenue by Adjusted EBITDA. Adjusted revenue is calculated by subtracting Section 45K revenue from total revenue. |

| (3) | Total secured debt is the aggregate principal amount of debt outstanding that is secured by some or all of our assets. |

| (4) | On an as adjusted basis after giving effect to the offering of the secured notes and the redemption of all of our 11 3/8% Notes under the Tender Offer our ratio of Total secured debt / Adjusted EBITDA on December 31, 2010, would have been 4.1 x. |

| (5) | On an as adjusted basis after giving effect to the offering of the secured notes and the redemption of all of our 11 3/8% Notes under the Tender Offer as if they had occurred on January 1, 2010, our ratio of Adjusted EBITDA / Cash paid for interest would have been x. |

| (6) | Working Capital is total current assets less total current liabilities. |

RISK FACTORS

Risks relating to our business and our common stock are described in Item 1A of the 2010 Form 10-K. The following information supplements the information contained therein.

Risks Relating to Our Business

The building products industry continues to experience a severe downturn that may continue for an indefinite period into the future. Because the markets for our building products are heavily dependent on the residential construction and remodeling market, our revenues could remain flat or decrease as a result of events outside our control that impact home construction and home improvement activity, including economic factors specific to the building products industry.

Since 2006, there has been a severe slowing of new housing starts and in home sales generally. Bank foreclosures have put a large number of homes into the market for sale, effectively limiting some of the incentives to build new homes. The homebuilding industry continues to experience a significant and sustained decrease in demand for new homes and an oversupply of new and existing homes available for sale. While our residential building products business relies upon the home improvement and remodeling markets as well as new construction, we have experienced a slowdown in sales activity beginning in fiscal 2007, and continuing through 2010. Interest rate increases, limits on credit availability, further foreclosures, depressed home prices, and an oversupply of homes for sale in the market may adversely affect homeowners’ and/or homebuilders’ ability or desire to engage in construction or remodeling, resulting in a continued or further slowdown in new construction or remodeling and repair activities.

We, like many others in the building products industry, experienced a large drop in orders and a reduction in our margins in 2008 through 2010, relative to prior years. In 2007-2009, we recorded significant goodwill impairments associated with our building products business. We can provide no assurances that the building products market will improve in the near future. To the extent weakness continues into 2011, it will have an adverse effect on our business and our results of operations.

The construction markets are seasonal. The majority of our building products sales are in the residential construction market, which tends to slow down in the winter months. If there is more severe weather than normal, or other events outside of our control, there may be a negative effect on our revenues. For the winter months of late 2010 and early 2011, our decreased seasonal revenues from HBP and HRI may result in negative cash flow.

The recent financial crisis could continue to negatively affect our business, results of operations, and financial condition. Market conditions in the mortgage lending and mortgage finance industries deteriorated significantly in 2008 and 2009, which continues to adversely affect the availability of credit for home purchasers and remodelers in 2010 and 2011.

The financial crisis affecting the banking system and financial markets and the going concern threats to banks and other financial institutions have resulted in a tightening in the credit markets, a low level of liquidity in many financial markets, including mortgages and home equity loans, and extreme volatility in credit and equity markets. A continuation of poor borrowing markets or a further tightening of mortgage lending or mortgage financing requirements could adversely affect the availability of credit for purchasers of our products and thereby reduce our sales.

There could be a number of follow-on effects from the credit crisis on our business, including the inability of prospective homebuyers or remodelers to obtain credit to finance the purchase of our building products. These and other similar factors could:

| • | cause delay or decisions to not undertake new home construction or improvement projects, |

| • | cause our customers to delay or decide not to purchase our building products, |

| • | lead to a decline in customer transactions and our financial performance. |

Our building products business has been strengthened by the sales growth of new products. If we are unable to continue to successfully expand our new product sales, our revenue growth may be adversely affected.

Our growth strategy includes the introduction of new building products by our light building products business. Part of our revenues has come from sales in new product categories. New products require capital for development, manufacturing, and acquisition activities. If we are unable to sustain new product sales growth, whether for lack of access to adequate capital or for other reasons, sales will follow the general industry slowdown in new residential construction and remodeling activity, which will negatively affect our revenue and growth.

Demand for our building products may decrease because of changes in customer preferences or because competing products gain price advantages. If demand for our products declines, our revenues will decrease.

Our building products are subject to reductions in customer demand for reasons such as changes in preferred home styles and appearances. Many of our resin-based siding accessory products are complementary to an owner’s choice of vinyl as a siding material. If sales of vinyl siding decrease, sale of our accessories will also decrease. Similarly, sales of our manufactured architectural stone products are dependent on the continuing popularity of stone finishes.

Demand for our building products can also decline if competing products become relatively less expensive. For example, if costs of petroleum-based resins that are used to make vinyl siding and accessories increase faster than the costs of stucco, then stucco products, which we do not sell, will become more attractive from a price standpoint, and our vinyl siding and accessory sales may decrease. Similarly, manufactured architectural stone could lose price competitiveness compared to other finishes. If demand for our building products declines because of changes in the popularity or price advantages of our products, our revenues will be adversely affected.

A significant increase in the price of materials used in the production of our building products that cannot be passed on to customers could have a significant adverse effect on our operating income. Furthermore, we depend upon limited sources for certain key production materials, the interruption of which would materially disrupt our ability to manufacture and supply products, resulting in lost revenues and the potential loss of customers.

Our manufactured architectural stone and concrete block manufacturing processes require key production materials including cement, man-made and natural aggregates, oxides, packaging materials, and certain types of rubber-based products. The suppliers of these materials may experience capacity or supply constraints in meeting market demand that limit our ability to obtain needed production materials on a timely basis or at expected prices. We have no long-term contracts with such suppliers. We do not currently maintain large inventories of production materials and alternative sources meeting our requirements could be difficult to arrange in the short term. A significant increase in the price of these materials that cannot be passed on to customers could have a significant adverse effect on our cost of sales and operating income. Additionally, our manufacturing and ability to provide products to our customers could be materially disrupted if this supply of materials was interrupted for any reason. Such an interruption and the resulting inability to supply our manufactured architectural stone customers with products could adversely impact our revenues and our relationships with our customers.

Certain of our home siding accessory products are manufactured from polypropylene, a large portion of which material is sold to us by a single supplier. The price of polypropylene is primarily a function of manufacturing capacity, demand and the prices of petrochemical feedstocks, crude oil and natural gas liquids. Historically, the market price of polypropylene has fluctuated, and significantly increased as recently as 2011. A significant increase in the price of polypropylene that cannot be passed on to customers could have a significant adverse effect on our cost of sales and operating income. We do not have a long-term contract with our polypropylene supplier. We do not maintain large inventories of polypropylene and alternative sources of polypropylene could be difficult to arrange in the short term. Therefore, our manufacturing and ability to provide products to our customers could be materially disrupted if this supply of polypropylene was interrupted for any reason. Such an interruption and the resulting inability to supply our resin-based siding accessory customers with products could adversely impact our revenues and potentially our relationships with our customers.

Interruption of our ability to immediately ship individual or custom product orders could harm our reputation and result in lost revenues if customers turn to other sources for products.

Our building products business is highly dependent upon rapid shipments to contractors and distributors throughout the United States of individual orders, a large portion of which orders are manufactured upon demand to meet customer specifications. If there is significant interruption of business at any of our manufacturing plants or with our computer systems that track customer orders and production, we are at risk of harming our reputation for speed and reliability with important customers and losing short-term and long-term revenues if these customers turn to other sources.

Our siding accessory revenues would be materially adversely affected if we lost one or more of our three major customers.

Three customers of our resin-based siding accessory products together accounted for approximately 24% of our revenues for such products in the fiscal year ended September 30, 2010, and approximately 6% of our total revenues as of such date. There are no long-term contracts in place with these customers. Accordingly, a loss of or significant decrease in demand from these customers would have a material adverse effect on our business.

Our construction materials business has been severely affected by downturns in governmental infrastructure spending.

Our fly ash and concrete block products, and to a much lesser extent, our other building products, are used in public infrastructure projects, which include the construction, maintenance, and improvement of highways, bridges, schools, prisons and similar projects. Our business is dependent on the level of federal, state, and local spending on these projects. We cannot be assured of the existence, amount, and timing of appropriations for government spending on these projects.

Federal and state budget limitations may continue to decrease severely the funding available for infrastructure spending. The lack of available credit has limited the ability of states to issue bonds to finance construction projects. In addition, infrastructure spending continues to be adversely affected by the overall weakness in the economy, which leads to lower tax revenues and state government budget deficits. Shortages in state tax revenues can reduce the amounts spent on state infrastructure projects, even below amounts awarded by the legislatures. Delays in state infrastructure spending can hurt our business. Further, rising construction and material prices constrain infrastructure construction budgets.

The American Recovery and Reinvestment Act (“ARRA”) enacted in early 2009 provided billions of dollars in new stimulus funding for transportation infrastructure. However, there has been a delay in Congressional appropriation of such funds and each state’s actions to take advantage of such funding. In addition, each state must approve various infrastructure projects to be funded through the new federal stimulus plan. The Obama administration is promoting new infrastructure legislation, but there can be no assurance that any such legislation will pass Congress or receive funding appropriations. We cannot be assured of the amount of funds to be expended and the timing of expenditures under the stimulus or any infrastructure plan.

If HRI’s coal-fueled electric utility industry suppliers fail to provide it with high-value coal combustion products (“CCPs”) due to environmental regulations or otherwise, HRI’s costs could increase and supply could fail to meet production needs, potentially negatively impacting our profitability or hindering growth.

HRI relies on the production of CCPs by coal-fueled electric utilities. HRI has occasionally experienced delays and other problems in obtaining high-value CCPs from its suppliers and may in the future be unable to obtain high-value CCPs on the scale and within the time frames required by HRI to meet customers’ needs. The coal-burning electric utility and coal mining industries are facing a number of new and pending initiatives by regulatory authorities seeking to address air and water pollution, greenhouse gas emissions and management and disposal of CCPs, as described below. Although our business managing CCPs for utility customers may benefit from opportunities to manage compliance with some new regulatory requirements, increasingly strict requirements generally will increase the cost of doing business and may make coal burning less attractive for utilities. Further, as the price of natural gas has decreased to current levels, coal-fueled electric utilities have in some instances switched from coal to natural gas. A reduction in the use of coal as fuel causes a decline in the production and availability of fly ash. To the extent the price of natural gas continues to remain low, more coal-fueled electric utilities may explore the feasibility of switching from coal to natural gas.

Faced with the prospect of more stringent regulations, litigation by environmental groups, and a decrease in the cost of natural gas, some electric utilities are reducing their portfolio of coal powered energy facilities. If HRI is unable to obtain CCPs or experiences a delay in the delivery of high-value or quality CCPs, HRI will have a reduced supply of CCPs to sell or may be forced to incur significant unanticipated expenses to secure alternative sources or to otherwise maintain supply to customers. Moreover, revenues could be adversely affected if CCP sales volumes cannot be maintained or if customers choose to find alternatives to HRI’s products.

The EPA has proposed two alternative rules under RCRA to regulate CCPs to address environmental risks from the disposal of CCPs. Either option is likely to have an adverse effect on the cost of managing and disposing of CCPs. The option of regulating CCPs as hazardous waste would likely have an adverse effect on beneficial use and sales of CCPs and HRI’s relationship with utilities.

In June 2010 the EPA proposed two alternative rules to regulate CCPs generated by electric utilities and independent power producers. One proposed option would classify CCPs disposed of in surface impoundments or landfills as “special wastes” subject to federal hazardous waste regulation under Subtitle C of the Resource Conservation and Recovery Act (“RCRA”). The second proposed option would instead regulate CCPs as non-hazardous waste under Subtitle D of RCRA, with states retaining the lead authority on regulating handling, storage and disposal of CCPs. Under both options, the current exemption from hazardous waste regulation for CCPs that are recycled for beneficial uses would remain in effect. The EPA requested comment on revising the definition of beneficial uses subject to the exemption, which could result in a narrowing of the scope of exempt uses in the final rule. Both rule options are controversial. During the comment period, the EPA conducted eight hearings in different locations and over 400,000 comments were submitted. Given the substantial number of comments, EPA may take additional time to release its final rule, which is currently scheduled for August 2011. At this time, it is not possible to predict what form the final regulations will take. Either option is likely to increase the complexity and cost of managing and disposing of CCPs. If the EPA decides to regulate CCPs as hazardous waste under RCRA Subtitle C, CCPs would become subject to a variety of regulations governing the handling, transporting, storing

and disposing of hazardous waste, increasing regulatory burden and costs of fly ash management for the utility industry and for HRI. The regulations could require modifications to or closure of disposal facilities, modifications to equipment used to handle, store and transport fly ash, additional training for personnel, new permitting requirements, increased recordkeeping and reporting, as well as increased disposal costs at landfills. There can be no guarantee that such regulations would not reduce or eliminate our supply or our ability to market fly ash and other CCPs which would have a material adverse impact on our operations and financial condition.

Regulation of CCPs as hazardous waste would likely have an adverse effect on beneficial use and sales of CCPs and HRI’s relationship with utilities. Even though the EPA proposal continues to exempt beneficial uses of CCPs from hazardous waste rules, users of fly ash and other CCPs are likely to attach a stigma to material that is identified as “hazardous waste” and may seek alternative products. Moreover, some environmental groups are urging the EPA to restrict some beneficial uses of CCPs, such as in cement, concrete and road base, alleging contaminants may leach into the environment. Some groups are asking the U.S. Green Building Council to stop allowing building products containing coal combustion residue to receive recycled materials credit in projects seeking approval in its Leadership in Energy and Environmental Design (LEED) certification program. This could reduce the demand for fly ash and other CCPs which would have an adverse affect on HRI’s CCP revenues. In addition, regulation of CCPs as hazardous waste would likely cause utilities and power producers to impose greater restrictions on the use of CCPs by HRI and its customers. Restrictions imposed by utilities may narrow the types of potential customers to which HRI can market CCPs and limit their uses of CCPs, reducing HRI’s sales opportunities. Utilities are also likely to negotiate to shift actual or perceived liabilities associated with CCPs and their use to HRI through more onerous contract and indemnity obligations. This could harm HRI’s business by reducing the number of or increasing our costs to perform CCP management contracts or by increasing HRI’s exposure to the contingent risks associated with any new regulation of CCPs.

HRI has managed numerous large scale CCP disposal projects, primarily for coal fueled utilities and power producers. In addition, CCPs have been used for road base, soil stabilization, and as large scale fill in contact with the ground. If the EPA decides to regulate CCPs as hazardous waste, HRI, together with CCP generators, could be subject to environmental cleanup and other possible claims and liabilities, which could result in material costs.

If the EPA adopts more stringent regulations under the Clean Air Act or Clean Water Act governing coal combustion, water discharges at coal mines and power plants, or power plant cooling water, this would likely have an adverse effect on the cost, beneficial use and sales of CCPs.

Coal-fueled electric utilities are highly regulated under federal and state law. HRI relies on the production of CCPs by coal-fueled electric utilities. HRI has occasionally experienced delays and other problems in obtaining high-value CCPs from its suppliers and may in the future be unable to obtain high-value CCPs on the scale and within the time frames required by HRI to meet customers’ needs.

The Clean Air Act (“CAA”) and EPA implementing regulations, as well as corresponding state laws and regulations, limit the emission of air pollutants such as sulfur oxides (“SOx”), nitrogen oxides (“NOx”) and particulate matter. The coal industry is directly affected by CAA permitting and emissions control requirements. Because coal-burning electric utilities emit SOx, NOx (a precursor to ozone) and particulate matter, our utility clients are subject to CAA implementation measures of EPA and the states, as well as additional emission control measures required by state law.

Following the judicial invalidation in 2008 of the EPA’s Clean Air Mercury Rule under the CAA, additional control technologies at power plants may be required by future regulation or legislation, to reduce in mercury emissions that could negatively affect fly ash quality. The EPA has announced that it intends to propose new regulations to control hazardous air pollutant emissions (including mercury emissions) from power plants in 2011. For example, future regulations could require activated carbon to be injected into power plant exhaust gases to capture mercury. This process may increase the carbon collected with the fly ash and may make the fly ash undesirable for concrete. Carbon removal processes for fly ash are technically challenging and expensive.

Increasing concerns about greenhouse gases (“GHG”) or other emissions from burning coal at electricity generation plants could lead to federal or state regulations that encourage or require utilities to burn less or eliminate coal in the production of electricity. In 2010, Congress and the Obama administration attempted to develop federal legislation to reduce GHG emissions which, among other things, could establish a cap and trade system for GHG, including carbon dioxide emitted by coal burning power plants and requirements for electric utilities to increase their use of renewable energy, such as wind and solar power. The federal legislation did not pass in 2010, but could be re-proposed in the future. In addition, several states have taken steps to adopt cap and trade or other systems to limit GHG emissions from power plants. For example, in December 2010, the California Air Resources Board approved greenhouse gas cap-and-trade and Mandatory Reporting rules.

The EPA has taken several regulatory actions to reduce GHG emissions, including its finding of “endangerment” to public health and welfare from GHG, its promulgation of the Mandatory Reporting of Greenhouse Gases rule (which requires large sources, including coal burning power plants, to annually report GHG emissions to the EPA starting in 2011), and its promulgation of the

Prevention of Significant Deterioration and Title V Greenhouse Gas Tailoring rule (which requires large industrial facilities, including coal burning power plants, to obtain permits to emit, and to use best available control technology to control GHG). Some states have also adopted or are developing climate change legislation and regulations as well. Such legislation and regulations could reduce the supply of fly ash and other CCPs.

At the same time, opponents of GHG regulation have initiated litigation, as well as introduced legislation in Congress, to delay, limit or eliminate EPA’s and possibly state action to regulate GHG. At this time it is not possible to predict the ultimate form, timing, extent or impact on our business of future regulation of GHG.

HRI manages a number of landfill and pond operations that may be affected by new Clean Water Act requirements. In 2009, the EPA released a report concluding that effluent discharges from fly ash storage ponds and wastewater discharges from coal-fired power plants have adversely affected aquatic life. The EPA is revising its Clean Water Act effluent limitation guidelines to address these discharges and is required by consent decree to publish a proposed rule in 2012 and a final rule in 2014. EPA has also indicated it will propose new criteria and standards for cooling water intake structures for power plants in 2011. If EPA adopts new Clean Water Act requirements, compliance obligations would increase. However, in light of the early stage of EPA’s consideration of new Clean Water Act regulations, their effect on HRI cannot be ascertained at this time.

In addition, the EPA is addressing water quality impacts from coal mining operations which could affect the availability and cost of coal for power generation. In April 2010, the EPA issued new guidance on Clean Water Act permits for mountaintop removal and surface mining. This guidance is being challenged in court. In October 2010, the EPA’s independent Science Advisory Board published a report concluding that mountaintop removal damages Appalachian streams. In January 2011, the EPA vetoed a federal mountaintop-removal mining permit issued by the Army Corps of Engineers in 2007 asserting the mine would use unsustainable mining practices.

If HRI is unable to obtain CCPs or if it experiences a delay in the delivery of high-value or quality CCPs, HRI will have a reduced supply of CCPs to sell or may be forced to incur significant unanticipated expenses to secure alternative sources or to otherwise maintain supply to customers. More stringent regulation of coal combustion emissions, water discharges, and mining operations could increase the cost of coal and coal combustion for utilities and thus reduce coal use, adversely impacting the availability and cost of fly ash for HRI’s CCP activities. Revenues could be adversely affected if CCP sales volumes or pricing cannot be maintained.

HRI primarily sells fly ash for use in concrete; if use of fly ash does not increase, HRI may not grow.

HRI’s growth has been and continues to be dependent upon the increased use of fly ash in the production of concrete. HRI’s marketing initiatives emphasize the environmental, cost and performance advantages of replacing portland cement with fly ash in the production of concrete. If HRI’s marketing initiatives are not successful, HRI may not be able to sustain its growth.

Further, utilities are switching fuel sources, changing boiler operations and introducing activated carbon and ammonia into the exhaust gas stream in an effort to decrease costs and/or to meet increasingly stringent emissions control regulations. All of these factors can have a negative effect on fly ash quantity and quality, including an increase in the amount of unburned carbon in fly ash and the presence of ammonia slip. We are attempting to address these challenges with the development and/or commercialization of two technologies: carbon fixation, which pre-treats unburned carbon particles in fly ash in order to minimize the particles’ adverse effects, and ammonia slip mitigation, which counteracts the impact of ammonia contaminants in fly ash. Decreased quantity and quality of fly ash may impede the use of fly ash in the production of concrete, which would adversely affect HRI’s revenue.

If the EPA decides to regulate CCPs as hazardous waste, there would likely be an adverse effect on beneficial use and sales of CCPs and HRI’s relationship with utilities. Even though the EPA proposes to continue to exempt beneficial uses of CCPs from hazardous waste rules, users of fly ash and other CCPs are likely to attach a stigma to material that is identified as “hazardous waste” and may seek alternative products. Moreover, some environmental groups are urging the EPA to restrict some beneficial uses of CCPs, such as in cement, concrete and road base, alleging contaminants may leach into the environment. This could reduce the demand for fly ash and other CCPs which would have an adverse affect on Headwaters’ CCP revenues.

If portland cement or competing replacement products are available at lower prices than fly ash, our sales of fly ash as a replacement for portland cement in concrete products could suffer, causing a decline in HRI’s revenues and net income.

Approximately 70% of HRI’s revenues for the fiscal year ended September 30, 2010 were derived from the sale of fly ash as a replacement for portland cement in concrete products. At times, there may be an overcapacity of cement in regional markets, causing potential price decreases. The markets for HRI’s products are regional, in part because of the costs of transporting CCPs, and HRI’s business is affected by the availability and cost of competing products in the specific regions where it conducts business. If competing products become available at prices equal to or less than fly ash, HRI’s revenues and net income could decrease.

Because demand for CCPs sold by HRI is affected by fluctuations in weather and construction cycles, HRI’s revenues and net income could decrease significantly as a result of unexpected or severe weather.

HRI manages and markets CCPs and uses CCPs to produce building products. Utilities produce CCPs year-round. In comparison, sales of CCPs are generally keyed to construction market demands that tend to follow national trends in construction with predictable increases during temperate seasons and decreases during periods of severe weather. HRI’s CCP sales have historically reflected these seasonal trends, with the largest percentage of total annual revenues being realized in the quarters ended June 30 and September 30. Low seasonal demand normally results in reduced shipments and revenues in the quarters ended December 31 and March 31. The seasonal impact on HRI’s revenue, together with the seasonal impact on HRI’s revenues may result in negative cash flows for the winter months of 2010 and 2011.

The profitability of HES depends upon the operational success of our coal cleaning business.

By December 2008, HES had acquired or completed construction on 11 coal cleaning facilities. To be successful, HES must overcome operational issues. This is a relatively new business, and in some cases, HES has experienced difficulty in securing and maintaining strategic relationships with coal companies, landowners, and others that host our coal cleaning facilities. These relationships provide HES with access to the coal cleaning facilities, truck and rail loadouts, and other material handling and transportation facilities, as well as on-site coal piles, impoundments, and surface mines, and existing mine site permits. For some facilities, unfavorable contracts, strained relationships, and reduced access has had a detrimental impact on the availability of adequate coal feedstock at a reasonable price, efficient material handling and transportation, operating permits, and product marketing services. In the future, HES will likely need to undertake the significant disruption and expense of relocating facilities and entering into new strategic relationships where feedstock is exhausted, contracts are unfavorable, or other critical arrangements come to an end. In addition, HES continues to address the operability of its coal cleaning equipment to achieve efficient separation of minerals including ash, sulfur, and mercury, as well as product moisture and Btu content in order to achieve customer product specifications. At some facilities HES has experienced difficulty in extracting its full requirements of feedstock in part because of dredging and slurry piping that is more difficult to operate than we expected, increasing the overall costs of operations. We have not achieved our planned economies of scale based upon budgeted full production. To date, our coal cleaning facilities have not consistently operated at a cost that is less than the revenues generated. In 2010 we recorded a non-cash impairment charge relating to the value of certain coal cleaning assets because of weaker than expected cash flow projections. If operational results do not improve, we may be required to record additional impairment charges relating to our coal cleaning assets. The profitability of HES depends on the ability of HES to increase production and sales of cleaned coal. If these facilities operate at low production levels or cannot produce fuel at a cost and quality satisfactory to customers, these operations may not become profitable.

The revenues of HES have been adversely affected by decreased demand for our coal and may not improve to levels that could make HES profitable.

Coal is a commodity that can be produced and shipped worldwide. The U.S. and worldwide economic slowdown has reduced energy requirements including the demand for steam coal in the markets in which we operate. In addition, the economic slowdown has reduced the demand and production of steel. Some of our clean coal revenues come from the sale of metallurgical grade coal used in steel making. This reduced demand has caused an over-supply of coal, reduced prices for coal, and increased competition among coal producers. Selling our finished product, which is generally of smaller particle size (called fines), is often more difficult than selling run-of-mine coal produced by our competitors. We have experienced softness in demand for our coal and in the prices for which we have been able to sell coal, particularly steam coal, adversely affecting our revenues. As a result, we have curtailed operations at three facilities, leaving eight in operation at this time. While we believe that an economic recovery will increase the demand for energy and steel, including our coal products, there is no assurance that demand will increase to levels that could make HES profitable in the future.

Regulatory changes could reduce the demand for coal which may decrease the price for which HES can sell its clean coal product.

Our clean coal revenues are dependent upon the demand for coal, including use as a fuel for the production of electricity. Increasing concerns about greenhouse gas or other air emissions, toxic materials in wastewater discharges, certain coal mining practices and the hazardousness of coal combustion waste from burning coal at power generation plants could lead to federal or state regulations that encourage or require utilities to burn less or eliminate coal in the production of electricity. Such regulations could reduce the demand for coal, which would adversely affect the prices at which HES could sell its clean coal product and decrease our revenues.

HES may not qualify for tax credits under Section 45, which will adversely affect our profitability.

Section 45 provides a tax credit for the production and sale of refined coal. Based on the language of Section 45 and available public guidance, HES believes that the coal cleaning facilities are eligible for Section 45 refined coal tax credits. However, the ability to claim tax credits is dependent upon a number of conditions, including, but not limited to:

| • | Placing facilities in service on or before December 31, 2010; |

| • | Producing a fuel from coal that is lower in NOx and either SOx or mercury emissions by the specified amount as compared to the emissions of the feedstock; |

| • | For most facilities placed in service prior to January 1, 2009, producing a fuel at least 50% more valuable than the feedstock; and |

| • | Sale of the fuel to a third-party for the purpose of producing steam. |

In September 2010, the Internal Revenue Service (“IRS”) issued Notice 2010-54 (“Notice”) giving some public guidance about how this tax credit program will be administered and some of the restrictions on the availability of such credits. Among other things, the Notice requires that for coal cleaning operations to qualify for Section 45 credits, the facilities must have been put into service for the purpose of producing refined coal and must produce refined coal from waste coal. In addition, the Notice gives guidance about the testing that must be conducted to certify the emissions reduction required by Section 45.