Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ZIONS BANCORPORATION, NATIONAL ASSOCIATION /UT/ | form_8k.htm |

1

February 1, 2011

Morgan Stanley U.S. Financial

Conference

Conference

2

Forward-Looking Statements

This presentation contains statements that relate to the projected performance of

Zions Bancorporation and elements of or affecting such performance, including

statements with respect to the beliefs, plans, objectives, goals, guidelines,

expectations, anticipations and estimates of management. These statements

constitute forward-looking information within the meaning of the Private Securities

Litigation Reform Act. Actual facts, determinations, results or achievements may

differ materially from the statements provided in this presentation since such

statements involve significant known and unknown risks and uncertainties.

Factors that might cause such differences include, but are not limited to:

competitive pressures among financial institutions; economic, market and

business conditions, either nationally or locally in areas in which Zions

Bancorporation conducts its operations, being less favorable than expected;

changes in the interest rate environment reducing expected interest margins;

changes in debt, equity and securities markets; adverse legislation or regulatory

changes; and other factors described in Zions Bancorporation’s most recent

annual and quarterly reports. In addition, the statements contained in this

presentation are based on facts and circumstances as understood by management

of the company on the date of this presentation, which may change in the future.

Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking

statements included herein to reflect future events, developments, determinations

or understandings.

Zions Bancorporation and elements of or affecting such performance, including

statements with respect to the beliefs, plans, objectives, goals, guidelines,

expectations, anticipations and estimates of management. These statements

constitute forward-looking information within the meaning of the Private Securities

Litigation Reform Act. Actual facts, determinations, results or achievements may

differ materially from the statements provided in this presentation since such

statements involve significant known and unknown risks and uncertainties.

Factors that might cause such differences include, but are not limited to:

competitive pressures among financial institutions; economic, market and

business conditions, either nationally or locally in areas in which Zions

Bancorporation conducts its operations, being less favorable than expected;

changes in the interest rate environment reducing expected interest margins;

changes in debt, equity and securities markets; adverse legislation or regulatory

changes; and other factors described in Zions Bancorporation’s most recent

annual and quarterly reports. In addition, the statements contained in this

presentation are based on facts and circumstances as understood by management

of the company on the date of this presentation, which may change in the future.

Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking

statements included herein to reflect future events, developments, determinations

or understandings.

3

Agenda

|

Overview of Zions

Key Performance Drivers

–Capital

–Credit Quality

–Revenue

Outlook Summary

|

|

|

4

A Collection of Great Banks

Asset and deposit balances as of 3Q 2010

5

Multi-Bank Business Model: Competitive

Strengths

Strengths

§ Direct customer access to local decision makers

§ Cross-pollination of ideas between banks

– CEOs & division managers meet frequently to compare best

practices, opportunities, and resolve “intramural” issues

practices, opportunities, and resolve “intramural” issues

§ Community bank feel - local marketing and branding

§ Superior lending capacity relative to community banks

§ Centralization of processing and other non-customer

facing elements of the business

facing elements of the business

§ Established market-leading small business lender

– Leading SBA Lender

• Largest SBA portfolio relative to overall size of loan book

– Superior treasury management products & services (Greenwich

survey)

survey)

§ Local “ownership” of market opportunities and

challenges

challenges

6

Small Business Banking:

National Awards:

• Overall Satisfaction

• Overall Treasury Management

Regional Awards:

• Overall Satisfaction - West

• Overall Satisfaction - Treasury

Management - West

Management - West

What Others Say About Us

2010 Greenwich Excellence Awards

in Small Business and Middle Market Banking

Middle Market Banking

National Awards:

• Overall Satisfaction

• Relationship Manager Performance

• Credit Policy

• Overall Treasury Management

• Accuracy of Operations

• Customer Service

• Treasury Product Capabilities

• Treasury Sales Specialist Performance

Regional Awards:

• Overall Satisfaction - West

• Overall Satisfaction - Treasury

Management - West

Management - West

7

*Includes FDIC supported assets

Strong Focus on Business Banking - Loan Mix

Loan Portfolio

as of 4Q10

as of 4Q10

§Commercial and

CRE Loans: 80%

CRE Loans: 80%

§Retail & Other

Loans: 20%

Loans: 20%

8

Agenda

|

Overview of Zions

Key Performance Drivers

–Capital

–Credit Quality

–Revenue

Outlook Summary

|

|

|

9

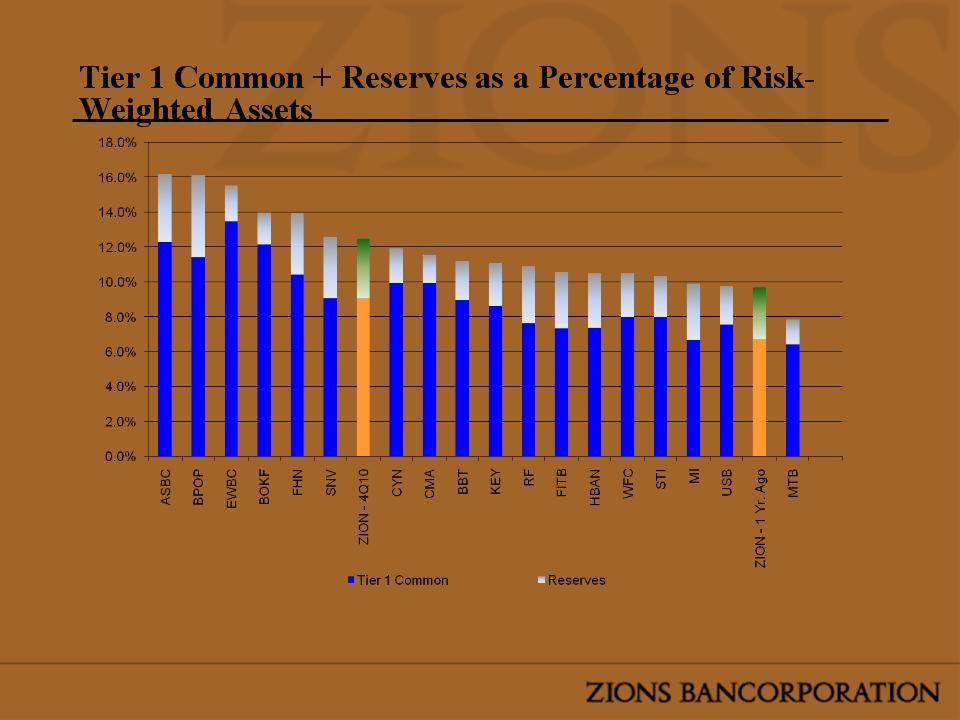

Zion as of 4Q 2010, peers as of 3Q 2010

Note: Peer group includes U.S. regional banks with assets greater than $20 billion and less than $200 billion plus footprint competitors WFC and

USB

USB

Source: SNL

10

Basel III New Capital Proposal

B3 estimated capital ratios for Zions assumes elimination of trust preferred securities and other comprehensive income from Tier 1 capital, and

adjusts for deferred tax asset limits.

adjusts for deferred tax asset limits.

Tier 1 Common

9.08%

Total RBC

17.36%

Tier 1 RBC

15.01%

7.8%

15.0%

12.6%

7.6%

9.3%

7.0%

10.5%

8.5%

11.7%

11

Agenda

|

Overview of Zions

Key Performance Drivers

–Capital

–Credit Quality

–Revenue

Outlook Summary

|

|

|

12

Credit Quality Trends

*Annualized

Zions excludes FDIC supported assets

Note: Peer group includes U.S. publicly traded regional banks with assets greater than $20 billion and less than $200 billion plus

footprint competitors WFC and USB

footprint competitors WFC and USB

Source: SNL

NPAs + Greater than 90

Days Delinquent /

Loans + OREO

Days Delinquent /

Loans + OREO

Net Charge-

offs as a % of

Loans*

offs as a % of

Loans*

13

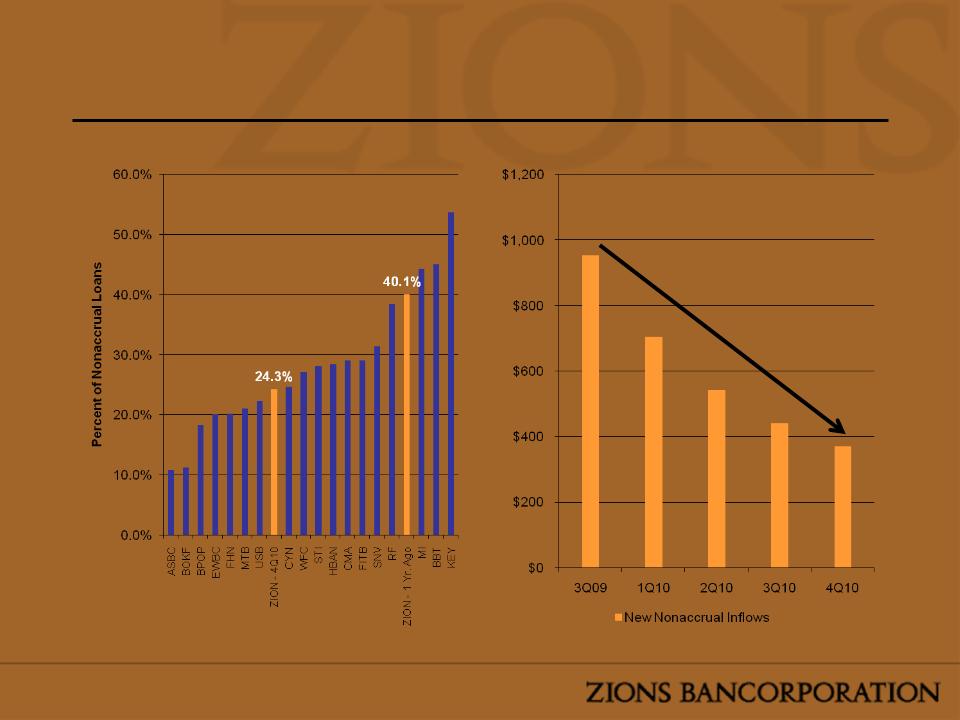

Source: SNL. Peer data as of 3Q10. Nonaccrual inflows from Form FR Y-9C, schedule HC-N, line M.7.

Nonaccrual Inflows

Millions

14

Note: Peer group includes U.S. publicly traded regional banks with assets greater than $20 billion and less than $200 billion plus footprint

competitors WFC and USB

competitors WFC and USB

Source: ZION, company documents as of YTD 2010, Peer group, SNL YTD 3Q10

Net Charge Offs - By Loan Type

Percentage of

Zions Total Loans

Zions Total Loans

10.4% 9.4% 5.7% 2.8% 19.5% 20.3% 26.6% 5.3%

15

SCAP Completed: ZION vs. More Adverse Scenario

•Although ZION was

not officially subject

to the SCAP stress

tests, we applied

the midpoint of

ratios given to the

largest 19 banks to

our loan portfolio.

not officially subject

to the SCAP stress

tests, we applied

the midpoint of

ratios given to the

largest 19 banks to

our loan portfolio.

•While the credit

cycle is not

complete, the two-

year period for

SCAP is complete.

cycle is not

complete, the two-

year period for

SCAP is complete.

•Results are not as

severe as many

expected.

severe as many

expected.

Dollars in

millions

millions

16

Source: Company earnings press release

Trends: Nonaccrual and Net Charge-Offs

Construction & Land Development

Construction & Land Development

§ Fourth quarter charge-offs elevated due to total resolution volume 1.5x higher than historical quarterly

resolution rate (36% of beginning classified loan balance versus average of 23%).

resolution rate (36% of beginning classified loan balance versus average of 23%).

17

Source: Company earnings press release

Favorable Resolutions vs. Net Charge-Offs

Construction & Land Development

Construction & Land Development

18

Source: Company earnings press release

Trends: Nonaccrual and Net Charge Offs

Term CRE & Owner Occupied

Term CRE & Owner Occupied

§ Fourth quarter charge-offs elevated due to total resolution volume 1.5x higher than historical quarterly resolution

rate (36% of beginning classified loan balance versus average of 23%).

rate (36% of beginning classified loan balance versus average of 23%).

19

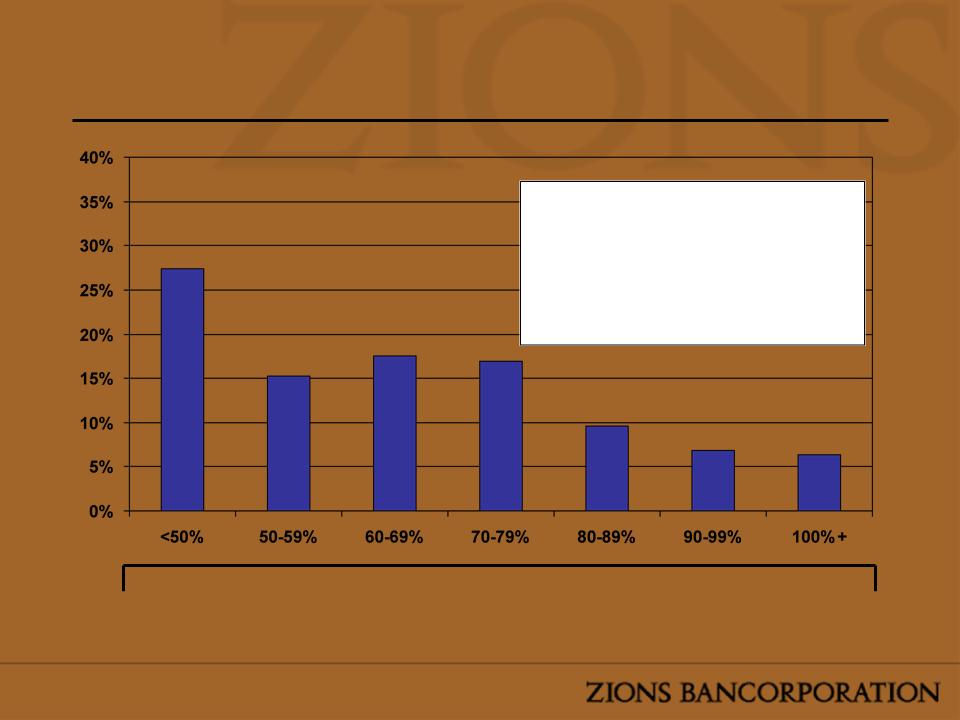

Term CRE

Updated LTV Stratification

Updated LTV Stratification

The MIT Transaction Based Index is a national index that has been applied to Zions’ mostly regional CRE Portfolio

Zions loan data as of 4Q10 and TBI data as of 3Q10

|

Percentage of Loans within each bucket that are Non-Accrual

|

||||||

|

2.2%

|

3.2%

|

1.7%

|

4.4%

|

6.2%

|

3.8%

|

5.8%

|

• By attaching each loan to

the TBI index as of the

date of the loans last

appraisal we can see an

estimate of the updated

LTV ratios of the portfolio

the TBI index as of the

date of the loans last

appraisal we can see an

estimate of the updated

LTV ratios of the portfolio

20

Agenda

|

Overview of Zions

Key Performance Drivers

–Capital

–Credit Quality

–Revenue

Outlook Summary

|

|

|

21

Core net income excludes items that are one time or non-recurring in nature. Incorporated in the Appendix of this presentation is the detail which

supports our core net income before tax calculations. 2Q09 - 4Q09 included material gains from loan portfolio swaps. Swaps are used to manage

interest rate risk and were generally added near the peak in the rate cycle. As hedges became ineffective, gains were realized.

supports our core net income before tax calculations. 2Q09 - 4Q09 included material gains from loan portfolio swaps. Swaps are used to manage

interest rate risk and were generally added near the peak in the rate cycle. As hedges became ineffective, gains were realized.

Generally Stable Core Pre-Tax, Pre-Credit

Income

Income

22

Core Net Interest Margin - 4Q10

Zions’ net interest margin excludes non-cash sub debt amortization expense and accretion on FDIC-acquired loans. Peer group net interest margin

adjusted for accretion of interest income on FDIC acquired loans, where applicable.

adjusted for accretion of interest income on FDIC acquired loans, where applicable.

Source: SNL as of 4Q 2010, Zions calculations.

Strong NIM

Driven in part by Strong

Demand Deposits

Demand Deposits

N/A

N/A

N/A

23

Core NIM Trends

• Zions expects net interest

sensitive income to increase

between an estimated 3.7% and

6.7% if interest rates were to

rise 200 bps* in the first year

sensitive income to increase

between an estimated 3.7% and

6.7% if interest rates were to

rise 200 bps* in the first year

• Core NIM (excludes discount

accretion) has been generally

stable

accretion) has been generally

stable

– 2010 core NIM compression

attributable to a greater drag from

cash balances

attributable to a greater drag from

cash balances

– 1Q09 experienced a temporary dip

partially due to an intentional build

-up of excess liquidity during the

significant turmoil during late

2008/early 2009

partially due to an intentional build

-up of excess liquidity during the

significant turmoil during late

2008/early 2009

– Large senior note issuance in

September 2009 had about 8 bps

adverse impact on the core NIM in

4Q09

September 2009 had about 8 bps

adverse impact on the core NIM in

4Q09

(1) Cash drag refers to the adverse impact on the net interest margin due to the total balance of cash held in interest-bearing accounts. Assumptions

used to compute the cash drag include investing the cash at a rate of 4.5%, similar to the rate achieved on recent loan production. Liquidity targets and

loan demand are factors that may prevent fully deploying such cash; the cash drag is shown for illustrative purposes only.

used to compute the cash drag include investing the cash at a rate of 4.5%, similar to the rate achieved on recent loan production. Liquidity targets and

loan demand are factors that may prevent fully deploying such cash; the cash drag is shown for illustrative purposes only.

*Assumes a parallel shift in the yield curve; key assumptions include a slow and a fast deposit repricing response (i.e. if deposit rates are slow to

increase Zions expects a 6.7% increase in interest sensitive income, and if deposits were to reprice quickly Zions expects a 3.7% increase in interest

sensitive income); sensitivity analysis based on November 2010 data.

increase Zions expects a 6.7% increase in interest sensitive income, and if deposits were to reprice quickly Zions expects a 3.7% increase in interest

sensitive income); sensitivity analysis based on November 2010 data.

Due to the extinguishment/ reissuance of subordinated debt in June 2009, Zions experiences non-cash discount accretion, which increases interest

expense, reducing GAAP NIM

expense, reducing GAAP NIM

|

|

1Q0

9 |

2Q0

9 |

3Q0

9 |

4Q0

9 |

1Q1

0 |

2Q1

0 |

3Q1

0 |

4Q1

0 |

|

|

Cash Drag (1)

|

|

24

bps |

17

bps |

16

bps |

24

bps |

20

bps |

35

bps |

46

bps |

45

bps |

24

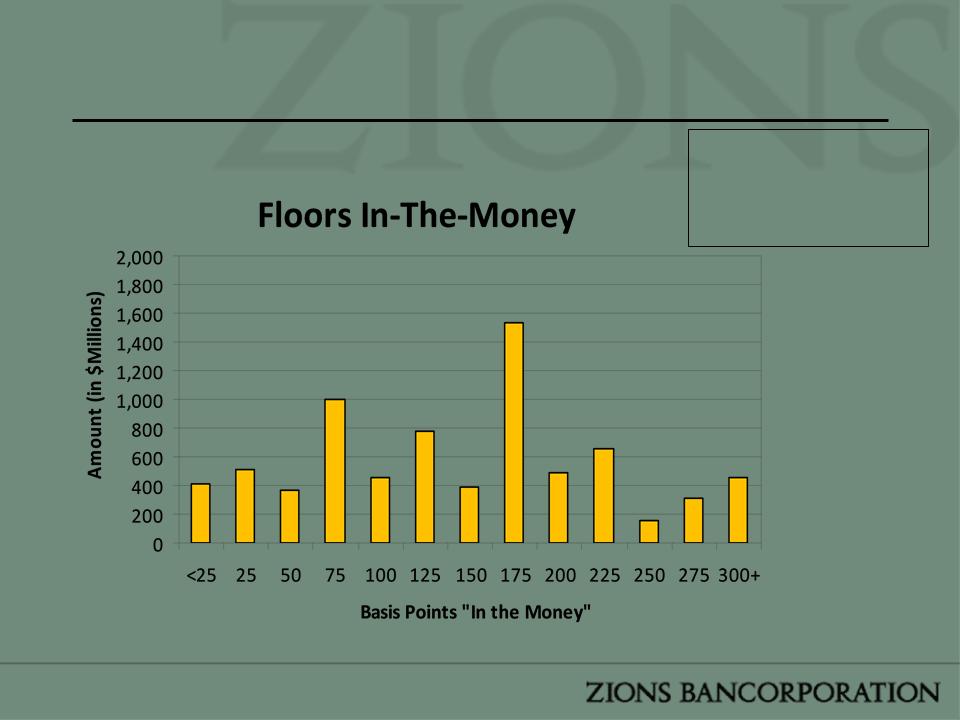

Loans with Floors (as of 12/31/10)

§ The total amount of loans

with floors that are in-the

-money equal

approximately $7.5B

with floors that are in-the

-money equal

approximately $7.5B

§ Weighted average in-the-

money floor: 148 bps

money floor: 148 bps

25

Interest Rate Risk Simulation - “Slow

Response”

Response”

§ 12-month simulated impact - a static balance sheet, and is based on regression analysis comparing

deposit repricing changes against similar duration benchmark indices (e.g. Libor, U.S. Treasuries); it also

includes management input across all major geographies in which Zions does business, intended to adjust

for local market conditions(1). Assumes reduction of DDA of approximately $3 billion and a

commensurate reduction in cash balances. Change does not reflect cost savings associated with FDIC

premium expense on a lower asset base.

deposit repricing changes against similar duration benchmark indices (e.g. Libor, U.S. Treasuries); it also

includes management input across all major geographies in which Zions does business, intended to adjust

for local market conditions(1). Assumes reduction of DDA of approximately $3 billion and a

commensurate reduction in cash balances. Change does not reflect cost savings associated with FDIC

premium expense on a lower asset base.

(1) “Slow Response” refers to an assumption that market rates on deposits will adjust at a moderate rate (i.e. supply of deposits exceeds demand for

loans)

loans)

26

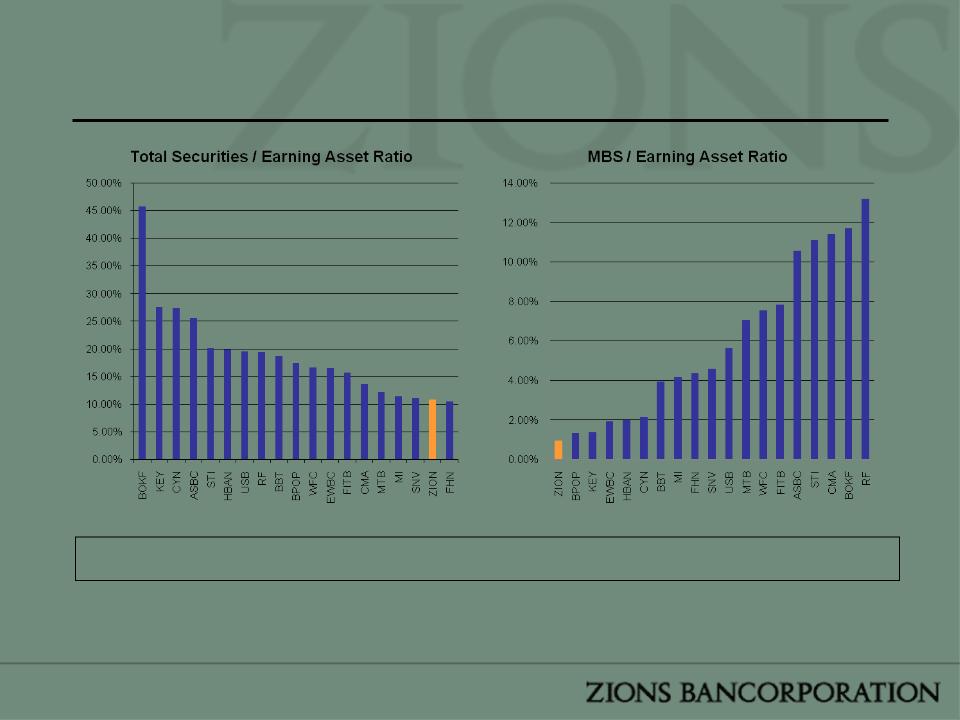

Securities Portfolio Comparison

Source: SNL. Zion as of 4Q 2010, peer data as of 3Q 2010

MBS securities include residential mortgage pass-through investments that are not guaranteed by the U.S. Government

Takeaway - no material NIM compression risk from

MBS repricing

MBS repricing

27

• Zions’ asset sensitivity

implies a potentially stronger

net interest margin in a

rising rate environment

implies a potentially stronger

net interest margin in a

rising rate environment

• Near term pressure on loan

pricing may adversely affect

the net interest margin

pricing may adversely affect

the net interest margin

28

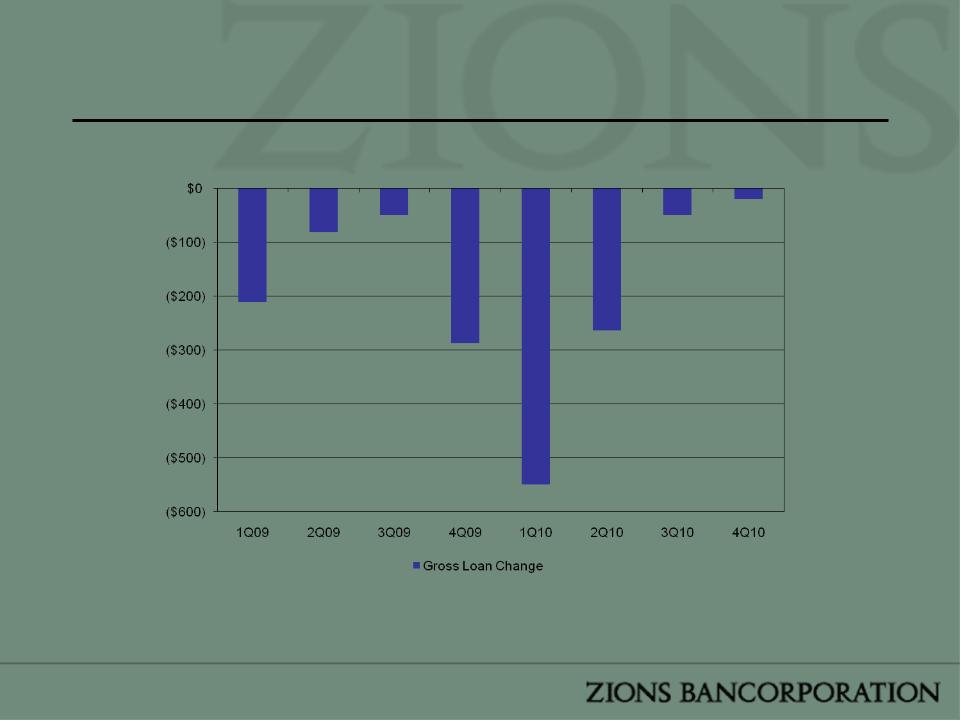

Loan Growth Trend

Excludes CRE C&D and FDIC-supported Loans

Excludes CRE C&D and FDIC-supported Loans

29

Agenda

|

Overview of Zions

Key Performance Drivers

–Capital

–Credit Quality

–Revenue

Outlook Summary

|

|

|

30

Near Term Objectives

§ Reduce problem credits

– Continued intense focus on workouts

– On the margin, increase the use of A/B note structure

§ Increase lending activity

– Additional emphasis on government guaranteed lending

programs

programs

– C&I pipelines strengthening in most markets,

particularly small and middle-market enterprises

(SMEs)

particularly small and middle-market enterprises

(SMEs)

§ Reduce excess cash balances

– Lower interest rates on non-relationship interest bearing

accounts

accounts

– Marginally increase investments in agency securities

31

Outlook Summary

|

|

Moderating

Decline |

|

Loan Balances

|

|

|

Declining

|

|

Nonperforming Assets

|

|

|

Declining

|

|

Credit Costs

|

|

|

Generally Low

|

|

OTTI

|

|

|

Generally

Stable |

|

Core Net Interest Margin

|

|

|

Generally

Stable |

|

Core Non-interest Expense

|

|

|

Generally

Stable |

|

Capital Ratios

|

32

Appendix

33

Asset Sensitivity

§ Fixed-rate loans:

– Approximately one quarter of portfolio

– Duration of about 1.5 years

§ Variable-rate loans:

– Approximately three quarters of portfolio

– Roughly 30% of variable-rate loans are intermediate

term resets (>12 months)

term resets (>12 months)

– Floors on approximately 55% of variable-rate loans

– Swaps: $570 million (Pay Floating, Receive Fixed), up

from $520 million in the prior quarter

from $520 million in the prior quarter

As of November 2010

34

CDO Portfolio Summary

§ Credit-related OTTI losses in 4Q10: $12.3 million

– Credit-related impairment from bank and insurance trust

preferred CDOs for 4Q10 was only $5.3 million (compared to

$20.9 million in 3Q10 and $86.8 million in 4Q09).

preferred CDOs for 4Q10 was only $5.3 million (compared to

$20.9 million in 3Q10 and $86.8 million in 4Q09).

§ Noncredit-related losses on securities in 4Q10: $2.9 million

– Recognized in OCI

*Table includes $2.1 billion par value of CDOs that are backed predominantly by bank trust preferred securities. The par value of all Bank & Insurance

backed CDOs is approximately $2.6 billion

backed CDOs is approximately $2.6 billion

35

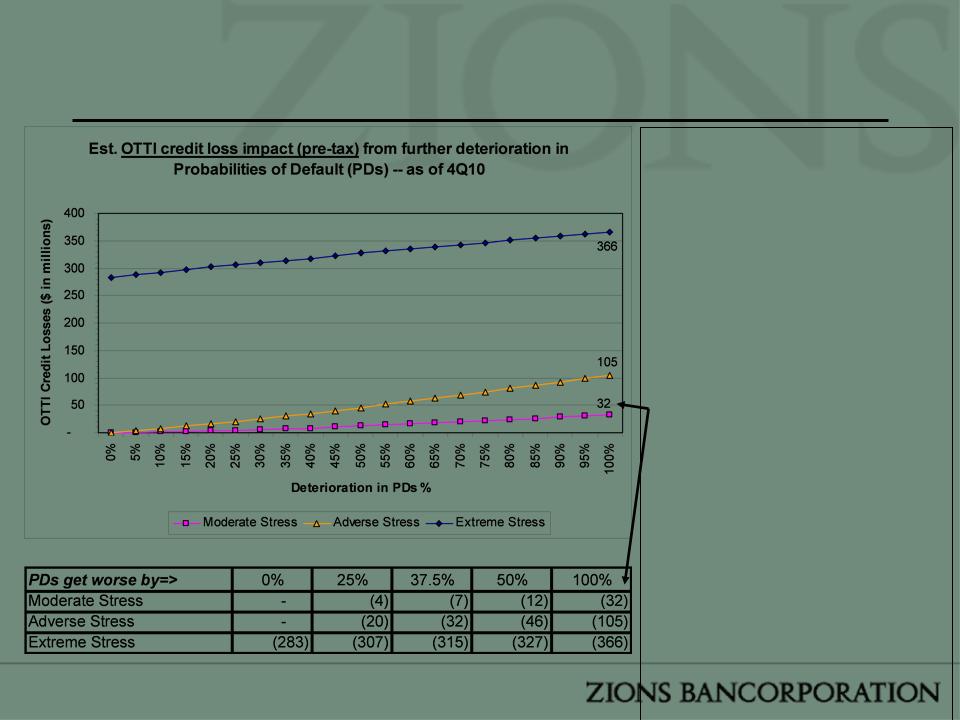

CDO Stress Testing - OTTI

§“Deterioration in PDs %” means that

the default curve applied to the

performing collateral of each deal is

made worse by the percentage

indicated. Thus a deal with a default

curve of 5% stressed to a 25%

“Deterioration in PDs %” would have a

6.25% default probability curve applied

to it, a deal with 20% would go to 25%

and so forth. A “Deterioration in PDs

%” stress of 100% would double the

PD curve being applied to a deal's

collateral.

the default curve applied to the

performing collateral of each deal is

made worse by the percentage

indicated. Thus a deal with a default

curve of 5% stressed to a 25%

“Deterioration in PDs %” would have a

6.25% default probability curve applied

to it, a deal with 20% would go to 25%

and so forth. A “Deterioration in PDs

%” stress of 100% would double the

PD curve being applied to a deal's

collateral.

§Moderate Stress - The PD curve that

was applied to the performing

collateral of each CDO deal in the

pricing run is increased by the %

indicated and the resultant values

were used to estimate OTTI losses.

The Moderate Stress Scenario at

100% would result in approximately

$32 million of pre-tax OTTI losses.

was applied to the performing

collateral of each CDO deal in the

pricing run is increased by the %

indicated and the resultant values

were used to estimate OTTI losses.

The Moderate Stress Scenario at

100% would result in approximately

$32 million of pre-tax OTTI losses.

§Adverse Stress - Incorporates all of

the deterioration of PDs applied to the

performing collateral, but also stresses

the PDs applied to collateral in deferral

by the same deterioration

percentages. PDs on deferring

collateral are used to estimate the

value of the potential for this collateral

to cure in the future through recovery

or re-performance.

the deterioration of PDs applied to the

performing collateral, but also stresses

the PDs applied to collateral in deferral

by the same deterioration

percentages. PDs on deferring

collateral are used to estimate the

value of the potential for this collateral

to cure in the future through recovery

or re-performance.

§Extreme Stress - This is a very

severe stress scenario that uses the

“Moderate Stress” assumptions for

performing collateral, but also

immediately defaults all deferring

collateral instantly with no recovery

and no probability to re-perform in the

future.

severe stress scenario that uses the

“Moderate Stress” assumptions for

performing collateral, but also

immediately defaults all deferring

collateral instantly with no recovery

and no probability to re-perform in the

future.

36

CDO Stress Testing - Capital

§ Under various stress

scenarios, Zions’

modeling indicates

that OCI

(accumulated other

comprehensive

income) would

erode, although at a

significantly lower

amount than OTTI

(other than

temporary

impairment).

scenarios, Zions’

modeling indicates

that OCI

(accumulated other

comprehensive

income) would

erode, although at a

significantly lower

amount than OTTI

(other than

temporary

impairment).

§ Under the moderate

stress scenario at

100% greater PDs,

OTTI incurred would

be approximately $32

million pre-tax (see

previous slide).

Under that same

moderate stress

scenario at 100%

greater PDs, OCI

would only

deteriorate by

approximately $11

million after-tax.

stress scenario at

100% greater PDs,

OTTI incurred would

be approximately $32

million pre-tax (see

previous slide).

Under that same

moderate stress

scenario at 100%

greater PDs, OCI

would only

deteriorate by

approximately $11

million after-tax.

37

As of 11-26-11

38

Core Net Income Before Tax Detail

39