Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - REGIONS FINANCIAL CORP | d8k.htm |

| EX-99.3 - VISUAL PRESENTATION - REGIONS FINANCIAL CORP | dex993.htm |

| EX-99.1 - PRESS RELEASE - REGIONS FINANCIAL CORP | dex991.htm |

Exhibit 99.2

|

FINANCIAL SUPPLEMENT TO FOURTH QUARTER 2010 EARNINGS RELEASE |

Summary

Quarterly profit of $0.03 per diluted share reflects improved core business performance; Progress continues

towards sustainable profitability; Account growth drives improved performance

| • | Significant fourth quarter drivers include: $333 million in securities gains, $26 million gain on sale of residential mortgages and $55 million loss on early extinguishment of debt |

| • | Inflow of non-performing loans declined 29% linked quarter |

| • | Pre-tax pre-provision net revenue, on an adjusted basis, totaled $461 million, 2% higher than prior quarter, 19% higher compared to the fourth quarter of 2009, and 4% higher for the full year 2010 versus 2009. |

Prudent de-risking of balance sheet continues; credit trends improving

| • | Non-performing loans, excluding loans held for sale, decreased $212 million or 6% linked quarter, and were the primary driver of an overall decline in non-performing assets |

| • | Net charge-offs decreased $77 million to $682 million, or an annualized 3.22% of loans as compared to third quarter’s 3.52%. |

| • | Allowance for loan losses increased 7 bps to 3.84%; loan loss provision essentially equaled net charge-offs |

| • | Allowance coverage ratio (ALL/NPL, excluding loans held for sale) rose to 1.01x as of December 31, 2010, as compared to 0.94x at September 30, 2010 and 0.89x at December 31, 2009 |

Continued emphasis on the customer; lending remains a primary focus

| • | Opened approximately 1,000,000 new business and consumer checking accounts for the second year in a row |

| • | Independent research by TNS ranks Regions’ brand favorability the highest of 11 major banks tested within our market which places Regions in a strong position to gain market share. |

| • | Customer retention remains well above the industry norm and is at a historical high |

| • | Gallup continues to identify Regions as a top-decile performer in customer loyalty |

| • | Loans outstanding declined $1.6 billion or 2% linked quarter, and reflects de-risking efforts, particularly involving investor real estate, which decreased $1.6 billion in the third quarter. Also impacted by $965 million sale of residential mortgage loans. |

| • | Commercial & industrial period end loans, primarily middle market, increased $1 billion or 5% linked quarter. Notably, the increase was more broadly distributed across the company’s footprint, and in more industries than the prior quarter. |

Net interest margin expansion driven by funding mix and improving loan yields

| • | Net interest income increased $9 million linked quarter and $97 million for the full year 2010 versus 2009 |

| • | Improving deposit costs continue to benefit the net interest margin, which rose 4 basis points linked quarter to 3.00% |

| • | Average low-cost deposits increased $1.4 billion linked quarter or $7 billion for the full year 2010 |

| • | Total deposit costs declined 6 bps linked quarter to 0.64%; down 51 basis points year-over-year |

| • | Loan yields increased 5 basis points linked quarter to 4.34%; company remains disciplined with pricing of new loans |

Strong non-interest revenue; Modest increase in non-interest expenses

| • | Non-interest income increased $463 million linked quarter; however, on an adjusted basis, after excluding $333 million in securities gains, $26 million gain on sale of mortgage loans and $59 million in leveraged lease terminations gains, non-interest revenue increased $47 million or 6% linked quarter. |

| • | Securities gains in 4Q10 reflect the sale of approximately $8.1 billion of agency mortgage-backed securities. The proceeds were reinvested in similar securities with slightly longer durations. |

| • | Non-interest expenses increased 9% linked quarter, however after adjusting for current quarter’s $55 million loss on early extinguishment of debt, non-interest expenses increased 4% driven by professional and legal fees and revenue-based incentives |

Strong capital and liquidity profile

| • | Tier 1 capital ratio of 12.4% (1); |

| • | Tier 1 common ratio of 7.9% (1) |

| • | As the rules are currently being interpreted, Basel III is expected to have a minimal impact to Regions |

| • | Tangible common stockholders’ equity to tangible assets of 6.04% |

| • | Loan to deposit ratio of 88% |

| (1) | estimated |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 2

Regions Financial Corporation and Subsidiaries

Consolidated Balance Sheets

(Unaudited)

| ($ amounts in millions) |

||||||||||||||||||||

| 12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | ||||||||||||||||

| Assets: |

||||||||||||||||||||

| Cash and due from banks |

$ | 1,643 | $ | 1,898 | $ | 2,097 | $ | 2,252 | $ | 2,052 | ||||||||||

| Interest-bearing deposits in other banks |

4,880 | 3,852 | 4,562 | 4,295 | 5,580 | |||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

396 | 1,137 | 752 | 324 | 379 | |||||||||||||||

| Trading account assets |

1,116 | 1,580 | 1,261 | 1,238 | 3,039 | |||||||||||||||

| Securities available for sale |

23,289 | 23,555 | 24,166 | 24,219 | 24,069 | |||||||||||||||

| Securities held to maturity |

24 | 26 | 28 | 30 | 31 | |||||||||||||||

| Loans held for sale |

1,485 | 1,587 | 1,162 | 1,048 | 1,511 | |||||||||||||||

| Loans, net of unearned income |

82,864 | 84,420 | 85,945 | 88,174 | 90,674 | |||||||||||||||

| Allowance for loan losses |

(3,185 | ) | (3,185 | ) | (3,185 | ) | (3,184 | ) | (3,114 | ) | ||||||||||

| Net loans |

79,679 | 81,235 | 82,760 | 84,990 | 87,560 | |||||||||||||||

| Other interest-earning assets |

1,219 | 1,043 | 1,082 | 819 | 734 | |||||||||||||||

| Premises and equipment, net |

2,569 | 2,564 | 2,588 | 2,637 | 2,668 | |||||||||||||||

| Interest receivable |

421 | 512 | 466 | 503 | 468 | |||||||||||||||

| Goodwill |

5,561 | 5,561 | 5,561 | 5,559 | 5,557 | |||||||||||||||

| Mortgage servicing rights (MSRs) |

267 | 204 | 220 | 270 | 247 | |||||||||||||||

| Other identifiable intangible assets |

385 | 414 | 443 | 472 | 503 | |||||||||||||||

| Other assets |

9,417 | 8,330 | 8,192 | 8,574 | 7,920 | |||||||||||||||

| Total Assets |

$ | 132,351 | $ | 133,498 | $ | 135,340 | $ | 137,230 | $ | 142,318 | ||||||||||

| Liabilities and Stockholders’ Equity: |

||||||||||||||||||||

| Deposits: |

||||||||||||||||||||

| Non-interest-bearing |

$ | 25,733 | $ | 25,300 | $ | 22,993 | $ | 23,391 | $ | 23,204 | ||||||||||

| Interest-bearing |

68,881 | 69,678 | 73,257 | 74,941 | 75,476 | |||||||||||||||

| Total deposits |

94,614 | 94,978 | 96,250 | 98,332 | 98,680 | |||||||||||||||

| Borrowed funds: |

||||||||||||||||||||

| Short-term borrowings: |

||||||||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

2,716 | 2,451 | 1,929 | 1,687 | 1,893 | |||||||||||||||

| Other short-term borrowings |

1,221 | 1,210 | 1,035 | 997 | 1,775 | |||||||||||||||

| Total short-term borrowings |

3,937 | 3,661 | 2,964 | 2,684 | 3,668 | |||||||||||||||

| Long-term borrowings |

13,190 | 14,335 | 15,415 | 15,683 | 18,464 | |||||||||||||||

| Total borrowed funds |

17,127 | 17,996 | 18,379 | 18,367 | 22,132 | |||||||||||||||

| Other liabilities |

3,876 | 3,361 | 3,248 | 2,893 | 3,625 | |||||||||||||||

| Total Liabilities |

115,617 | 116,335 | 117,877 | 119,592 | 124,437 | |||||||||||||||

| Stockholders’ equity: |

||||||||||||||||||||

| Preferred stock, Series A |

3,380 | 3,370 | 3,360 | 3,351 | 3,343 | |||||||||||||||

| Preferred stock, Series B |

— | — | — | 259 | 259 | |||||||||||||||

| Common stock |

13 | 13 | 13 | 12 | 12 | |||||||||||||||

| Additional paid-in capital |

19,050 | 19,047 | 19,038 | 18,781 | 18,781 | |||||||||||||||

| Retained earnings (deficit) |

(4,047 | ) | (4,070 | ) | (3,849 | ) | (3,502 | ) | (3,235 | ) | ||||||||||

| Treasury stock, at cost |

(1,402 | ) | (1,405 | ) | (1,405 | ) | (1,407 | ) | (1,409 | ) | ||||||||||

| Accumulated other comprehensive income (loss), net |

(260 | ) | 208 | 306 | 144 | 130 | ||||||||||||||

| Total Stockholders’ Equity |

16,734 | 17,163 | 17,463 | 17,638 | 17,881 | |||||||||||||||

| Total Liabilities and Stockholders’ Equity |

$ | 132,351 | $ | 133,498 | $ | 135,340 | $ | 137,230 | $ | 142,318 | ||||||||||

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 3

Regions Financial Corporation and Subsidiaries

Consolidated Statements of Operations

(Unaudited)

| ($ amounts in millions, except per share data) |

Quarter Ended | |||||||||||||||||||

| 12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | ||||||||||||||||

| Interest income on: |

||||||||||||||||||||

| Loans, including fees |

$ | 911 | $ | 919 | $ | 930 | $ | 945 | $ | 981 | ||||||||||

| Securities: |

||||||||||||||||||||

| Taxable |

193 | 214 | 224 | 242 | 256 | |||||||||||||||

| Tax-exempt |

— | — | — | 1 | 1 | |||||||||||||||

| Total securities |

193 | 214 | 224 | 243 | 257 | |||||||||||||||

| Loans held for sale |

12 | 10 | 9 | 8 | 12 | |||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

1 | 1 | 1 | — | 1 | |||||||||||||||

| Trading account assets |

12 | 8 | 9 | 12 | 30 | |||||||||||||||

| Other interest-earning assets |

7 | 6 | 7 | 7 | 7 | |||||||||||||||

| Total interest income |

1,136 | 1,158 | 1,180 | 1,215 | 1,288 | |||||||||||||||

| Interest expense on: |

||||||||||||||||||||

| Deposits |

152 | 167 | 194 | 242 | 280 | |||||||||||||||

| Short-term borrowings |

2 | 3 | 2 | 3 | 9 | |||||||||||||||

| Long-term borrowings |

105 | 120 | 128 | 139 | 149 | |||||||||||||||

| Total interest expense |

259 | 290 | 324 | 384 | 438 | |||||||||||||||

| Net interest income |

877 | 868 | 856 | 831 | 850 | |||||||||||||||

| Provision for loan losses |

682 | 760 | 651 | 770 | 1,179 | |||||||||||||||

| Net interest income (loss) after provision for loan losses |

195 | 108 | 205 | 61 | (329 | ) | ||||||||||||||

| Non-interest income: |

||||||||||||||||||||

| Service charges on deposit accounts |

290 | 294 | 302 | 288 | 299 | |||||||||||||||

| Brokerage, investment banking and capital markets |

312 | 257 | 254 | 236 | 257 | |||||||||||||||

| Mortgage income |

51 | 66 | 63 | 67 | 46 | |||||||||||||||

| Trust department income |

50 | 49 | 49 | 48 | 48 | |||||||||||||||

| Securities gains (losses), net |

333 | 2 | — | 59 | (96 | ) | ||||||||||||||

| Other |

177 | 82 | 88 | 114 | 164 | |||||||||||||||

| Total non-interest income |

1,213 | 750 | 756 | 812 | 718 | |||||||||||||||

| Non-interest expense: |

||||||||||||||||||||

| Salaries and employee benefits |

601 | 582 | 560 | 575 | 566 | |||||||||||||||

| Net occupancy expense |

108 | 110 | 110 | 120 | 114 | |||||||||||||||

| Furniture and equipment expense |

76 | 75 | 79 | 74 | 74 | |||||||||||||||

| Other-than-temporary impairments |

— | 1 | — | 1 | — | |||||||||||||||

| Regulatory charge |

— | — | 200 | — | — | |||||||||||||||

| Other |

481 | 395 | 377 | 460 | 465 | |||||||||||||||

| Total non-interest expense |

1,266 | 1,163 | 1,326 | 1,230 | 1,219 | |||||||||||||||

| Income (loss) before income taxes |

142 | (305 | ) | (365 | ) | (357 | ) | (830 | ) | |||||||||||

| Income tax expense (benefit) |

53 | (150 | ) | (88 | ) | (161 | ) | (287 | ) | |||||||||||

| Net income (loss) |

$ | 89 | $ | (155 | ) | $ | (277 | ) | $ | (196 | ) | $ | (543 | ) | ||||||

| Net income (loss) available to common shareholders |

$ | 36 | $ | (209 | ) | $ | (335 | ) | $ | (255 | ) | $ | (606 | ) | ||||||

| Weighted-average shares outstanding-during quarter: |

||||||||||||||||||||

| Basic |

1,257 | 1,257 | 1,200 | 1,194 | 1,191 | |||||||||||||||

| Diluted |

1,259 | 1,257 | 1,200 | 1,194 | 1,191 | |||||||||||||||

| Actual shares outstanding-end of quarter |

1,256 | 1,256 | 1,256 | 1,192 | 1,193 | |||||||||||||||

| Earnings (loss) per common share (1): |

||||||||||||||||||||

| Basic |

$ | 0.03 | $ | (0.17 | ) | $ | (0.28 | ) | $ | (0.21 | ) | $ | (0.51 | ) | ||||||

| Diluted |

$ | 0.03 | $ | (0.17 | ) | $ | (0.28 | ) | $ | (0.21 | ) | $ | (0.51 | ) | ||||||

| Cash dividends declared per common share |

$ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||

| Taxable-equivalent net interest income from continuing operations |

$ | 886 | $ | 876 | $ | 863 | $ | 839 | $ | 857 | ||||||||||

| (1) | Includes preferred stock dividends. |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 4

Regions Financial Corporation and Subsidiaries

Consolidated Statements of Operations

(Unaudited)

| ($ amounts in millions, except per share data) |

Twelve Months Ended December 31 |

|||||||

| 2010 | 2009 | |||||||

| Interest income on: |

||||||||

| Loans, including fees |

$ | 3,705 | $ | 4,199 | ||||

| Securities: |

||||||||

| Taxable |

873 | 966 | ||||||

| Tax-exempt |

1 | 19 | ||||||

| Total securities |

874 | 985 | ||||||

| Loans held for sale |

39 | 55 | ||||||

| Federal funds sold and securities purchased under agreements to resell |

3 | 3 | ||||||

| Trading account assets |

41 | 62 | ||||||

| Other interest-earning assets |

27 | 28 | ||||||

| Total interest income |

4,689 | 5,332 | ||||||

| Interest expense on: |

||||||||

| Deposits |

755 | 1,277 | ||||||

| Short-term borrowings |

10 | 54 | ||||||

| Long-term borrowings |

492 | 666 | ||||||

| Total interest expense |

1,257 | 1,997 | ||||||

| Net interest income |

3,432 | 3,335 | ||||||

| Provision for loan losses |

2,863 | 3,541 | ||||||

| Net interest income (loss) after provision for loan losses |

569 | (206 | ) | |||||

| Non-interest income: |

||||||||

| Service charges on deposit accounts |

1,174 | 1,156 | ||||||

| Brokerage, investment banking and capital markets |

1,059 | 989 | ||||||

| Mortgage income |

247 | 259 | ||||||

| Trust department income |

196 | 191 | ||||||

| Securities gains, net |

394 | 69 | ||||||

| Other |

461 | 1,091 | ||||||

| Total non-interest income |

3,531 | 3,755 | ||||||

| Non-interest expense: |

||||||||

| Salaries and employee benefits |

2,318 | 2,269 | ||||||

| Net occupancy expense |

448 | 454 | ||||||

| Furniture and equipment expense |

304 | 311 | ||||||

| Other-than-temporary impairments (1) |

2 | 75 | ||||||

| Regulatory charge |

200 | — | ||||||

| Other |

1,713 | 1,642 | ||||||

| Total non-interest expense (2) |

4,985 | 4,751 | ||||||

| Income (loss) before income taxes |

(885 | ) | (1,202 | ) | ||||

| Income tax benefit |

(346 | ) | (171 | ) | ||||

| Net income (loss) |

(539 | ) | (1,031 | ) | ||||

| Net income (loss) available to common shareholders |

($763 | ) | ($1,261 | ) | ||||

| Weighted-average shares outstanding-year-to-date: |

||||||||

| Basic |

1,227 | 989 | ||||||

| Diluted |

1,227 | 989 | ||||||

| Actual shares outstanding-end of period |

1,256 | 1,193 | ||||||

| Earnings (loss) per common share (3): |

||||||||

| Basic |

$ | (0.62 | ) | $ | (1.27 | ) | ||

| Diluted |

$ | (0.62 | ) | $ | (1.27 | ) | ||

| Cash dividends declared per common share |

$ | 0.04 | $ | 0.13 | ||||

| Taxable equivalent net interest income from continuing operations |

$ | 3,464 | $ | 3,367 | ||||

| (1) | Includes $266 million of gross charges, net of $191 million noncredit related portion recognized in other comprehensive income (loss), in 2009. The corresponding 2010 amounts are immaterial. |

| (2) | The securities for which noncredit other-than-temporary impairments were taken in 2Q09 were sold in 4Q09. Realized losses on the sales are reported with securities gains (losses), net. |

| (3) | Includes preferred stock dividends. |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 5

Regions Financial Corporation and Subsidiaries

Consolidated Average Daily Balances and Yield/Rate Analysis

| Quarter Ended | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ($ amounts in millions; yields on |

Average Balance |

Income/ Expense |

Yield/ Rate |

Average Balance |

Income/ Expense |

Yield/ Rate |

Average Balance |

Income/ Expense |

Yield/ Rate |

Average Balance |

Income/ Expense |

Yield/ Rate |

Average Balance |

Income/ Expense |

Yield/ Rate |

|||||||||||||||||||||||||||||||||||||||||||||

| Assets |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest-earning assets: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

$ | 952 | $ | 1 | 0.42 | % | $ | 1,096 | $ | 1 | 0.36 | % | $ | 345 | $ | 1 | 1.16 | % | $ | 373 | $ | — | — | % | $ | 364 | $ | 1 | 1.09 | % | ||||||||||||||||||||||||||||||

| Trading account assets |

1,255 | 13 | 4.11 | 1,214 | 9 | 2.94 | 1,186 | 9 | 3.04 | 1,288 | 13 | 4.09 | 2,827 | 31 | 4.35 | |||||||||||||||||||||||||||||||||||||||||||||

| Securities: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Taxable |

23,878 | 193 | 3.21 | 23,863 | 214 | 3.56 | 23,862 | 224 | 3.77 | 23,811 | 242 | 4.12 | 23,061 | 256 | 4.40 | |||||||||||||||||||||||||||||||||||||||||||||

| Tax-exempt |

47 | — | — | 39 | — | — | 41 | — | — | 51 | 1 | 7.95 | 135 | 2 | 5.88 | |||||||||||||||||||||||||||||||||||||||||||||

| Loans held for sale |

1,486 | 12 | 3.20 | 1,213 | 10 | 3.27 | 1,031 | 9 | 3.50 | 1,392 | 8 | 2.33 | 1,494 | 12 | 3.19 | |||||||||||||||||||||||||||||||||||||||||||||

| Loans, net of unearned income |

84,108 | 920 | 4.34 | 85,616 | 926 | 4.29 | 87,266 | 936 | 4.30 | 89,723 | 952 | 4.30 | 91,766 | 986 | 4.26 | |||||||||||||||||||||||||||||||||||||||||||||

| Other interest-earning assets |

5,188 | 6 | 0.46 | 4,308 | 6 | 0.55 | 6,745 | 8 | 0.48 | 5,973 | 7 | 0.48 | 5,566 | 7 | 0.50 | |||||||||||||||||||||||||||||||||||||||||||||

| Total interest-earning assets |

116,914 | 1,145 | 3.89 | 117,349 | 1,166 | 3.94 | 120,476 | 1,187 | 3.95 | 122,611 | 1,223 | 4.04 | 125,213 | 1,295 | 4.10 | |||||||||||||||||||||||||||||||||||||||||||||

| Allowance for loan losses |

(3,164 | ) | (3,223 | ) | (3,215 | ) | (3,144 | ) | (2,772 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash and due from banks |

2,069 | 2,059 | 2,112 | 2,181 | 2,206 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other non-earning assets |

17,515 | 17,544 | 17,912 | 17,917 | 16,486 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 133,334 | $ | 133,729 | $ | 137,285 | $ | 139,565 | $ | 141,133 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Liabilities and Stockholders’ Equity |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Savings accounts |

$ | 4,622 | 1 | 0.09 | $ | 4,517 | 1 | 0.09 | $ | 4,478 | 1 | 0.09 | $ | 4,215 | 1 | 0.10 | $ | 4,064 | 1 | 0.10 | ||||||||||||||||||||||||||||||||||||||||

| Interest-bearing transaction accounts |

12,690 | 6 | 0.19 | 13,606 | 7 | 0.20 | 15,651 | 8 | 0.21 | 15,709 | 11 | 0.28 | 14,279 | 11 | 0.31 | |||||||||||||||||||||||||||||||||||||||||||||

| Money market accounts |

28,273 | 23 | 0.32 | 28,088 | 22 | 0.31 | 27,302 | 32 | 0.47 | 25,715 | 40 | 0.63 | 23,808 | 38 | 0.63 | |||||||||||||||||||||||||||||||||||||||||||||

| Time deposits |

23,369 | 122 | 2.07 | 25,161 | 137 | 2.16 | 26,933 | 153 | 2.28 | 29,779 | 190 | 2.59 | 32,046 | 230 | 2.85 | |||||||||||||||||||||||||||||||||||||||||||||

| Total interest-bearing deposits (1) |

68,954 | 152 | 0.87 | 71,372 | 167 | 0.93 | 74,364 | 194 | 1.05 | 75,418 | 242 | 1.30 | 74,197 | 280 | 1.50 | |||||||||||||||||||||||||||||||||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

3,162 | — | — | 2,176 | 1 | 0.18 | 1,798 | 1 | 0.22 | 1,989 | 1 | 0.20 | 3,089 | 5 | 0.64 | |||||||||||||||||||||||||||||||||||||||||||||

| Other short-term borrowings |

1,056 | 2 | 0.75 | 866 | 2 | 0.92 | 847 | 1 | 0.47 | 1,086 | 2 | 0.75 | 1,849 | 4 | 0.86 | |||||||||||||||||||||||||||||||||||||||||||||

| Long-term borrowings |

14,006 | 105 | 2.97 | 14,878 | 120 | 3.20 | 15,933 | 128 | 3.22 | 17,417 | 139 | 3.24 | 18,326 | 149 | 3.23 | |||||||||||||||||||||||||||||||||||||||||||||

| Total interest-bearing liabilities |

87,178 | 259 | 1.18 | 89,292 | 290 | 1.29 | 92,942 | 324 | 1.40 | 95,910 | 384 | 1.62 | 97,461 | 438 | 1.78 | |||||||||||||||||||||||||||||||||||||||||||||

| Net interest spread |

2.71 | 2.65 | 2.55 | 2.42 | 2.32 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-interest-bearing deposits (1) |

25,688 | 23,706 | 23,688 | 22,817 | 22,149 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other liabilities |

3,422 | 3,349 | 3,063 | 3,040 | 3,275 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Stockholders’ equity |

17,046 | 17,382 | 17,592 | 17,798 | 18,248 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 133,334 | $ | 133,729 | $ | 137,285 | $ | 139,565 | $ | 141,133 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net interest income/margin FTE basis |

$ | 886 | 3.00 | % | $ | 876 | 2.96 | % | $ | 863 | 2.87 | % | $ | 839 | 2.77 | % | $ | 857 | 2.72 | % | ||||||||||||||||||||||||||||||||||||||||

| (1) | Total deposit costs may be calculated by dividing total interest expense on deposits by the sum of interest-bearing deposits and non-interest bearing deposits. The rates for total deposit costs equal 0.64%, 0.70%, 0.79%, 1.00% and 1.15% for the quarters ended December 31, 2010, September 30, 2010, June 30, 2010, March 31, 2010 and December 31, 2009, respectively. |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 6

Regions Financial Corporation and Subsidiaries

Consolidated Average Daily Balances and Yield/Rate Analysis

| Twelve Months Ended December 31 | ||||||||||||||||||||||||

| 2010 | 2009 | |||||||||||||||||||||||

| ($ amounts in millions; yields on taxable equivalent basis) |

Average Balance |

Revenue/ Expense |

Yield/ Rate |

Average Balance |

Revenue/ Expense |

Yield/ Rate |

||||||||||||||||||

| Assets |

||||||||||||||||||||||||

| Interest-earning assets: |

||||||||||||||||||||||||

| Federal funds sold and securities purchased under agreements to resell |

$ | 694 | $ | 3 | 0.43 | % | $ | 503 | $ | 3 | 0.60 | % | ||||||||||||

| Trading account assets |

1,236 | 44 | 3.56 | 1,599 | 65 | 4.07 | ||||||||||||||||||

| Securities: |

||||||||||||||||||||||||

| Taxable |

23,854 | 873 | 3.66 | 20,221 | 966 | 4.78 | ||||||||||||||||||

| Tax-exempt |

44 | 1 | 2.27 | 460 | 29 | 6.30 | ||||||||||||||||||

| Loans held for sale |

1,281 | 39 | 3.04 | 1,655 | 55 | 3.32 | ||||||||||||||||||

| Loans, net of unearned income |

86,660 | 3,734 | 4.31 | 94,523 | 4,218 | 4.46 | ||||||||||||||||||

| Other earning assets |

5,548 | 27 | 0.49 | 6,927 | 28 | 0.40 | ||||||||||||||||||

| Total interest-earning assets |

119,317 | 4,721 | 3.96 | 125,888 | 5,364 | 4.26 | ||||||||||||||||||

| Allowance for loan losses |

(3,187 | ) | (2,240 | ) | ||||||||||||||||||||

| Cash and due from banks |

2,105 | 2,245 | ||||||||||||||||||||||

| Other non-earning assets |

17,720 | 16,866 | ||||||||||||||||||||||

| $ | 135,955 | $ | 142,759 | |||||||||||||||||||||

| Liabilities and Stockholders’ Equity |

||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||

| Savings accounts |

$ | 4,459 | 4 | 0.09 | $ | 3,984 | 5 | 0.13 | ||||||||||||||||

| Interest-bearing transaction accounts |

14,404 | 32 | 0.22 | 14,347 | 40 | 0.28 | ||||||||||||||||||

| Money market accounts |

27,354 | 117 | 0.43 | 22,573 | 184 | 0.82 | ||||||||||||||||||

| Time deposits |

26,290 | 602 | 2.29 | 32,739 | 1,047 | 3.20 | ||||||||||||||||||

| Other |

— | — | — | 312 | 1 | 0.32 | ||||||||||||||||||

| Total interest-bearing deposits (1) |

72,507 | 755 | 1.04 | 73,955 | 1,277 | 1.73 | ||||||||||||||||||

| Federal funds purchased and securities sold under agreements to repurchase |

2,284 | 3 | 0.13 | 3,166 | 12 | 0.38 | ||||||||||||||||||

| Other short-term borrowings |

963 | 7 | 0.73 | 5,229 | 42 | 0.80 | ||||||||||||||||||

| Long-term borrowings |

15,547 | 492 | 3.16 | 18,588 | 666 | 3.58 | ||||||||||||||||||

| Total interest-bearing liabilities |

91,301 | 1,257 | 1.38 | 100,938 | 1,997 | 1.98 | ||||||||||||||||||

| Net interest spread |

2.58 | 2.28 | ||||||||||||||||||||||

| Non-interest bearing deposits (1) |

23,982 | 20,657 | ||||||||||||||||||||||

| Other liabilities |

3,228 | 3,391 | ||||||||||||||||||||||

| Stockholders’ equity |

17,444 | 17,773 | ||||||||||||||||||||||

| $ | 135,955 | $ | 142,759 | |||||||||||||||||||||

| Net interest income/margin FTE basis |

$ | 3,464 | 2.90 | % | $ | 3,367 | 2.67 | % | ||||||||||||||||

| (1) | Total deposit costs may be calculated by dividing total interest expense on deposits by the sum of interest-bearing deposits and non-interest bearing deposits. |

The rates for total deposit costs equal 0.78% and 1.35% for the twelve months ended December 31, 2010 and 2009, respectively.

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 7

Regions Financial Corporation and Subsidiaries

Selected Ratios

| As of and for Quarter Ended | ||||||||||||||||||||

| 12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | ||||||||||||||||

| Return on average assets (non-GAAP)* |

0.11 | % | (0.62 | %) | (0.98 | %) | (0.74 | %) | (1.70 | %) | ||||||||||

| Return on average assets, excluding regulatory charge |

0.11 | % | (0.62 | %) | (0.40 | %) | (0.74 | %) | (1.70 | %) | ||||||||||

| Return on average common equity* |

1.04 | % | (5.91 | %) | (9.62 | %) | (7.28 | %) | (16.40 | %) | ||||||||||

| Return on average tangible common equity |

1.78 | % | (10.00 | %) | (16.36 | %) | (12.29 | %) | (27.16 | %) | ||||||||||

| Return on average tangible common equity, excluding |

1.78 | % | (10.00 | %) | (6.60 | %) | (12.29 | %) | (27.16 | %) | ||||||||||

| Efficiency Ratio (non-GAAP) (4) |

72.0 | % | 71.6 | % | 69.5 | % | 74.3 | % | 75.4 | % | ||||||||||

| Common equity per share |

$ | 10.62 | $ | 10.98 | $ | 11.23 | $ | 11.77 | $ | 11.97 | ||||||||||

| Tangible common book value per share (non-GAAP) (3) |

$ | 6.09 | $ | 6.42 | $ | 6.65 | $ | 6.93 | $ | 7.11 | ||||||||||

| Stockholders’ equity to total assets |

12.64 | % | 12.86 | % | 12.90 | % | 12.85 | % | 12.56 | % | ||||||||||

| Tangible common stockholders’ equity to tangible assets (non-GAAP) (3) |

6.04 | % | 6.31 | % | 6.45 | % | 6.28 | % | 6.22 | % | ||||||||||

| Tier 1 Common risk-based ratio (non-GAAP) (1) |

7.9 | % | 7.6 | % | 7.7 | % | 7.1 | % | 7.1 | % | ||||||||||

| Tier 1 Capital (1) |

12.4 | % | 12.1 | % | 12.0 | % | 11.7 | % | 11.5 | % | ||||||||||

| Total Risk-Based Capital (1) |

16.4 | % | 16.0 | % | 15.9 | % | 15.8 | % | 15.8 | % | ||||||||||

| Allowance for credit losses as a percentage of loans, net of unearned income (2) |

3.93 | % | 3.86 | % | 3.79 | % | 3.69 | % | 3.52 | % | ||||||||||

| Allowance for loan losses as a percentage of loans, net of unearned income |

3.84 | % | 3.77 | % | 3.71 | % | 3.61 | % | 3.43 | % | ||||||||||

| Allowance for loan losses to non-performing loans, excluding loans held for sale |

1.01x | 0.94x | 0.92x | 0.86x | 0.89x | |||||||||||||||

| Net interest margin (FTE) |

3.00 | % | 2.96 | % | 2.87 | % | 2.77 | % | 2.72 | % | ||||||||||

| Loans, net of unearned income, to total deposits |

87.6 | % | 88.9 | % | 89.3 | % | 89.7 | % | 91.9 | % | ||||||||||

| Net charge-offs as a percentage of average loans* |

3.22 | % | 3.52 | % | 2.99 | % | 3.16 | % | 2.99 | % | ||||||||||

| Non-performing assets (excluding loans 90 days past due) as a percentage of loans and other real estate |

4.70 | % | 4.98 | % | 4.94 | % | 5.15 | % | 4.83 | % | ||||||||||

| Non-performing assets (including loans 90 days past due) as a percentage of loans and other real estate |

5.40 | % | 5.68 | % | 5.65 | % | 5.94 | % | 5.59 | % | ||||||||||

| * | Annualized |

| (1) | Current quarter Tier 1 Common, Tier 1 and Total Risk-Based Capital ratios are estimated |

| (2) | The allowance for credit losses reflects the allowance related to both loans on the balance sheet and exposure related to unfunded commitments and standby letters of credit |

| (3) | Beginning in 4th quarter 2010, tangible ratios are computed net of deferred tax liabilities associated with intangible assets. See the Reconciliation to GAAP Financial Measures on page 27. Prior periods have been revised to conform with the current presentation. |

| (4) | Efficiency ratio is shown on an operating basis and excludes adjustments as noted on page 26 in the Reconciliation to GAAP Financial Measures schedule |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 8

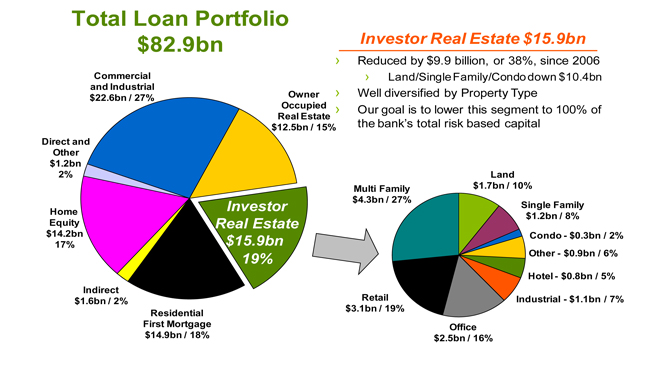

Loans

| Loan Portfolio - Period End Data |

||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | 12/31/10 vs. 9/30/10 |

12/31/10 vs. 12/31/09 |

|||||||||||||||||||||||||||||

| Commercial and industrial |

$ | 22,540 | $ | 21,501 | $ | 21,096 | $ | 21,220 | $ | 21,547 | $ | 1,039 | 4.8 | % | $ | 993 | 4.6 | % | ||||||||||||||||||

| Commercial real estate mortgage - owner-occupied |

12,046 | 11,850 | 11,967 | 12,028 | 12,054 | 196 | 1.7 | % | (8 | ) | -0.1 | % | ||||||||||||||||||||||||

| Commercial real estate construction - owner-occupied |

470 | 522 | 547 | 598 | 751 | (52 | ) | -10.0 | % | (281 | ) | -37.4 | % | |||||||||||||||||||||||

| Total commercial |

35,056 | 33,873 | 33,610 | 33,846 | 34,352 | 1,183 | 3.5 | % | 704 | 2.0 | % | |||||||||||||||||||||||||

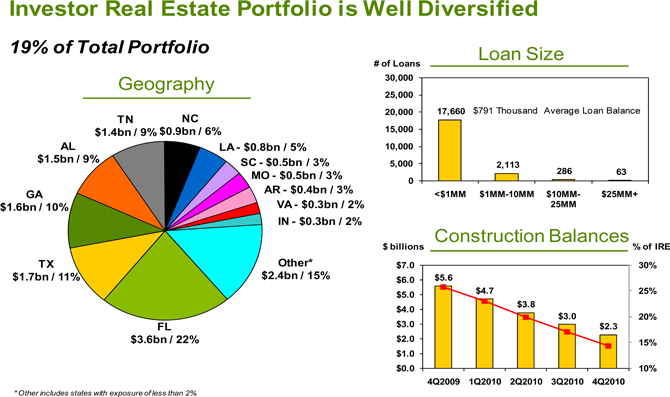

| Commercial investor real estate mortgage |

13,621 | 14,489 | 15,152 | 15,702 | 16,109 | (868 | ) | -6.0 | % | (2,488 | ) | -15.4 | % | |||||||||||||||||||||||

| Commercial investor real estate construction |

2,287 | 2,975 | 3,778 | 4,703 | 5,591 | (688 | ) | -23.1 | % | (3,304 | ) | -59.1 | % | |||||||||||||||||||||||

| Total investor real estate |

15,908 | 17,464 | 18,930 | 20,405 | 21,700 | (1,556 | ) | -8.9 | % | (5,792 | ) | -26.7 | % | |||||||||||||||||||||||

| Residential first mortgage |

14,898 | 15,723 | 15,567 | 15,592 | 15,632 | (825 | ) | -5.2 | % | (734 | ) | -4.7 | % | |||||||||||||||||||||||

| Home equity |

14,226 | 14,534 | 14,802 | 15,066 | 15,381 | (308 | ) | -2.1 | % | (1,155 | ) | -7.5 | % | |||||||||||||||||||||||

| Indirect |

1,592 | 1,657 | 1,900 | 2,162 | 2,452 | (65 | ) | -3.9 | % | (860 | ) | -35.1 | % | |||||||||||||||||||||||

| Other consumer |

1,184 | 1,169 | 1,136 | 1,103 | 1,157 | 15 | 1.3 | % | 27 | 2.3 | % | |||||||||||||||||||||||||

| $ | 82,864 | $ | 84,420 | $ | 85,945 | $ | 88,174 | $ | 90,674 | $ | (1,556 | ) | -1.8 | % | $ | (7,810 | ) | -8.6 | % | |||||||||||||||||

| Loan Portfolio - Average Balances |

||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Commercial and industrial |

$ | 21,956 | $ | 21,313 | $ | 21,109 | $ | 21,429 | $ | 21,570 | $ | 643 | 3.0 | % | $ | 386 | 1.8 | % | ||||||||||||||||||

| Commercial real estate mortgage - owner-occupied |

11,944 | 11,944 | 12,005 | 12,056 | 12,127 | — | 0.0 | % | (183 | ) | -1.5 | % | ||||||||||||||||||||||||

| Commercial real estate construction - owner-occupied |

503 | 516 | 563 | 686 | 819 | (13 | ) | -2.5 | % | (316 | ) | -38.6 | % | |||||||||||||||||||||||

| Total commercial |

34,403 | 33,773 | 33,677 | 34,171 | 34,516 | 630 | 1.9 | % | (113 | ) | -0.3 | % | ||||||||||||||||||||||||

| Commercial investor real estate mortgage |

14,223 | 15,090 | 15,586 | 16,220 | 16,292 | (867 | ) | -5.7 | % | (2,069 | ) | -12.7 | % | |||||||||||||||||||||||

| Commercial investor real estate construction |

2,649 | 3,477 | 4,340 | 5,071 | 6,145 | (828 | ) | -23.8 | % | (3,496 | ) | -56.9 | % | |||||||||||||||||||||||

| Total investor real estate |

16,872 | 18,567 | 19,926 | 21,291 | 22,437 | (1,695 | ) | -9.1 | % | (5,565 | ) | -24.8 | % | |||||||||||||||||||||||

| Residential first mortgage |

15,620 | 15,632 | 15,537 | 15,567 | 15,521 | (12 | ) | -0.1 | % | 99 | 0.6 | % | ||||||||||||||||||||||||

| Home equity |

14,389 | 14,684 | 14,947 | 15,237 | 15,515 | (295 | ) | -2.0 | % | (1,126 | ) | -7.3 | % | |||||||||||||||||||||||

| Indirect |

1,606 | 1,776 | 2,028 | 2,310 | 2,601 | (170 | ) | -9.6 | % | (995 | ) | -38.3 | % | |||||||||||||||||||||||

| Other consumer |

1,218 | 1,184 | 1,151 | 1,147 | 1,176 | 34 | 2.9 | % | 42 | 3.6 | % | |||||||||||||||||||||||||

| $ | 84,108 | $ | 85,616 | $ | 87,266 | $ | 89,723 | $ | 91,766 | $ | (1,508 | ) | -1.8 | % | $ | (7,658 | ) | -8.3 | % | |||||||||||||||||

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 9

Deposits

| Deposit Portfolio - Period End Data |

||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | 12/31/10 vs. 9/30/10 |

12/31/10 vs. 12/31/09 |

|||||||||||||||||||||||||||||

| Customer Deposits |

||||||||||||||||||||||||||||||||||||

| Interest-free deposits |

$ | 25,733 | $ | 25,300 | $ | 22,993 | $ | 23,391 | $ | 23,204 | $ | 433 | 1.7 | % | $ | 2,529 | 10.9 | % | ||||||||||||||||||

| Interest-bearing checking |

13,423 | 12,409 | 15,148 | 15,715 | 15,791 | 1,014 | 8.2 | % | (2,368 | ) | -15.0 | % | ||||||||||||||||||||||||

| Savings |

4,668 | 4,544 | 4,475 | 4,394 | 4,073 | 124 | 2.7 | % | 595 | 14.6 | % | |||||||||||||||||||||||||

| Money market - domestic |

27,420 | 27,983 | 26,773 | 26,196 | 23,291 | (563 | ) | -2.0 | % | 4,129 | 17.7 | % | ||||||||||||||||||||||||

| Money market - foreign |

569 | 509 | 502 | 635 | 766 | 60 | 11.8 | % | (197 | ) | -25.7 | % | ||||||||||||||||||||||||

| Low-cost deposits |

71,813 | 70,745 | 69,891 | 70,331 | 67,125 | 1,068 | 1.5 | % | 4,688 | 7.0 | % | |||||||||||||||||||||||||

| Time deposits |

22,784 | 24,177 | 26,298 | 27,939 | 31,468 | (1,393 | ) | -5.8 | % | (8,684 | ) | -27.6 | % | |||||||||||||||||||||||

| Total customer deposits |

94,597 | 94,922 | 96,189 | 98,270 | 98,593 | (325 | ) | -0.3 | % | (3,996 | ) | -4.1 | % | |||||||||||||||||||||||

| Corporate Treasury Deposits |

||||||||||||||||||||||||||||||||||||

| Time deposits |

17 | 56 | 61 | 62 | 87 | (39 | ) | -69.6 | % | (70 | ) | -80.5 | % | |||||||||||||||||||||||

| Total Deposits |

$ | 94,614 | $ | 94,978 | $ | 96,250 | $ | 98,332 | $ | 98,680 | $ | (364 | ) | -0.4 | % | $ | (4,066 | ) | -4.1 | % | ||||||||||||||||

| Deposit Portfolio - Average Balances |

||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Customer Deposits |

||||||||||||||||||||||||||||||||||||

| Interest-free deposits |

$ | 25,688 | $ | 23,706 | $ | 23,688 | $ | 22,817 | $ | 22,149 | $ | 1,982 | 8.4 | % | $ | 3,539 | 16.0 | % | ||||||||||||||||||

| Interest-bearing checking |

12,690 | 13,606 | 15,651 | 15,709 | 14,279 | (916 | ) | -6.7 | % | (1,589 | ) | -11.1 | % | |||||||||||||||||||||||

| Savings |

4,622 | 4,517 | 4,478 | 4,215 | 4,064 | 105 | 2.3 | % | 558 | 13.7 | % | |||||||||||||||||||||||||

| Money market - domestic |

27,767 | 27,574 | 26,670 | 24,961 | 22,956 | 193 | 0.7 | % | 4,811 | 21.0 | % | |||||||||||||||||||||||||

| Money market - foreign |

506 | 514 | 632 | 754 | 852 | (8 | ) | -1.6 | % | (346 | ) | -40.6 | % | |||||||||||||||||||||||

| Low-cost deposits |

71,273 | 69,917 | 71,119 | 68,456 | 64,300 | 1,356 | 1.9 | % | 6,973 | 10.8 | % | |||||||||||||||||||||||||

| Time deposits |

23,347 | 25,100 | 26,872 | 29,707 | 31,961 | (1,753 | ) | -7.0 | % | (8,614 | ) | -27.0 | % | |||||||||||||||||||||||

| Total customer deposits |

94,620 | 95,017 | 97,991 | 98,163 | 96,261 | (397 | ) | -0.4 | % | (1,641 | ) | -1.7 | % | |||||||||||||||||||||||

| Corporate Treasury Deposits |

||||||||||||||||||||||||||||||||||||

| Time deposits |

22 | 61 | 61 | 72 | 85 | (39 | ) | -63.9 | % | (63 | ) | -74.1 | % | |||||||||||||||||||||||

| Total Deposits |

$ | 94,642 | $ | 95,078 | $ | 98,052 | $ | 98,235 | $ | 96,346 | $ | (436 | ) | -0.5 | % | $ | (1,704 | ) | -1.8 | % | ||||||||||||||||

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 10

Pre-Tax Pre-Provision Net Revenue (“PPNR”) and Adjusted PPNR (non-GAAP)

The table below presents computations of pre-tax pre-provision net revenue excluding certain adjustments (non-GAAP). Regions believes that the exclusion of these adjustments provides a meaningful base for period-to-period comparisons, which management believes will assist investors in analyzing the operating results of the Company and predicting future performance. These

non-GAAP financial measures are also used by management to assess the performance of Regions’ business. It is possible that the activities related to the adjustments may recur; however, management does not consider the activities related to the adjustments to be indications of ongoing operations. Regions believes that presentation of these non-GAAP financial measures will permit investors to assess the performance of the Company on the same basis as that applied by management. Non-GAAP financial measures have inherent limitations, are not required to be uniformly applied and are not audited. Although these non-GAAP financial measures are frequently used by stakeholders in the evaluation of a company, they have limitations as analytical tools, and should not be considered in isolation, or as a substitute for analyses of results as reported under GAAP. In particular, a measure of earnings that excludes certain adjustments does not represent the amount that effectively accrues directly to stockholders.

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Net Interest Income (GAAP) |

$ | 877 | $ | 868 | $ | 856 | $ | 831 | $ | 850 | $ | 9 | 1.0 | % | $ | 27 | 3.2 | % | ||||||||||||||||||

| Non-Interest Income (GAAP) |

1,213 | 750 | 756 | 812 | 718 | 463 | 61.7 | % | 495 | 68.9 | % | |||||||||||||||||||||||||

| Total Revenue (GAAP) |

2,090 | 1,618 | 1,612 | 1,643 | 1,568 | 472 | 29.2 | % | 522 | 33.3 | % | |||||||||||||||||||||||||

| Non-Interest Expense (GAAP) |

1,266 | 1,163 | 1,326 | 1,230 | 1,219 | 103 | 8.9 | % | 47 | 3.9 | % | |||||||||||||||||||||||||

| Pre-tax Pre-provision Net Revenue (GAAP) |

$ | 824 | $ | 455 | $ | 286 | $ | 413 | $ | 349 | 369 | 81.1 | % | 475 | 136.1 | % | ||||||||||||||||||||

| Adjustments: |

||||||||||||||||||||||||||||||||||||

| Regulatory charge, net of tax |

— | — | 200 | — | — | — | NM | — | — | |||||||||||||||||||||||||||

| Securities (gains) losses, net |

(333 | ) | (2 | ) | — | (59 | ) | 96 | (331 | ) | NM | (429 | ) | -446.9 | % | |||||||||||||||||||||

| Gain on sale of mortgage loans |

(26 | ) | — | — | — | — | (26 | ) | NM | (26 | ) | NM | ||||||||||||||||||||||||

| Leveraged lease termination gains |

(59 | ) | — | — | (19 | ) | (71 | ) | (59 | ) | NM | 12 | -16.9 | % | ||||||||||||||||||||||

| Loss on extinguishment of debt |

55 | — | — | 53 | — | 55 | NM | 55 | NM | |||||||||||||||||||||||||||

| Securities impairment, net |

— | 1 | — | 1 | — | (1 | ) | NM | — | — | ||||||||||||||||||||||||||

| Branch consolidation costs (1) |

— | — | — | 8 | 12 | — | — | (12 | ) | NM | ||||||||||||||||||||||||||

| Total adjustments |

(363 | ) | (1 | ) | 200 | (16 | ) | 37 | (362 | ) | NM | (400 | ) | -1081.1 | % | |||||||||||||||||||||

| Adjusted PPNR (non-GAAP) |

$ | 461 | $ | 454 | $ | 486 | $ | 397 | $ | 386 | $ | 7 | 1.5 | % | $ | 75 | 19.4 | % | ||||||||||||||||||

| (1) | Includes $7 million of net occupancy expense and $1 million in valuation charges in 1Q10 and $3 million of net occupancy expense, $6 million of salary expense and $3 million in valuation charges in 4Q09. |

Categorization of Income (Loss) Related to

Mortgage Servicing Rights (MSRs) (2)

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Net interest income (3) |

$ | — | $ | — | $ | — | $ | 3 | $ | 20 | — | — | (20 | ) | NM | |||||||||||||||||||||

| Brokerage, investment banking and capital markets (4) |

— | — | — | 4 | 5 | — | — | (5 | ) | NM | ||||||||||||||||||||||||||

| Mortgage income (loss) (5) |

(13 | ) | 2 | 12 | 16 | (4 | ) | (15 | ) | NM | (9 | ) | NM | |||||||||||||||||||||||

| $ | (13 | ) | $ | 2 | $ | 12 | $ | 23 | $ | 21 | (15 | ) | NM | (34 | ) | -161.9 | % | |||||||||||||||||||

| (2) | This table details the impact of changes in valuation of mortgage servicing rights and related hedging instruments on various categories in the consolidated statements of operations. |

| (3) | Interest earned on trading securities used to hedge MSRs. |

| (4) | Mark-to-market impact of trading securities used to hedge MSRs. |

| (5) | Net effect of mark-to-market impact of MSRs and derivatives used to hedge MSRs. |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 11

Non-Interest Income and Expense

| Non-Interest Income and Expense | ||||||||||||||||||||||||||||||||||||

| Non-Interest Income | ||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Service charges on deposit accounts |

$ | 290 | $ | 294 | $ | 302 | $ | 288 | $ | 299 | $ | (4 | ) | -1.4 | % | $ | (9 | ) | -3.0 | % | ||||||||||||||||

| Brokerage, investment banking and capital markets |

312 | 257 | 254 | 236 | 257 | 55 | 21.4 | % | 55 | 21.4 | % | |||||||||||||||||||||||||

| Mortgage income |

51 | 66 | 63 | 67 | 46 | (15 | ) | -22.7 | % | 5 | 10.9 | % | ||||||||||||||||||||||||

| Trust department income |

50 | 49 | 49 | 48 | 48 | 1 | 2.0 | % | 2 | 4.2 | % | |||||||||||||||||||||||||

| Securities gains (losses), net |

333 | 2 | — | 59 | (96 | ) | 331 | NM | 429 | NM | ||||||||||||||||||||||||||

| Insurance income |

25 | 25 | 26 | 27 | 25 | — | 0.0 | % | — | 0.0 | % | |||||||||||||||||||||||||

| Leveraged lease termination gains |

59 | — | — | 19 | 71 | 59 | NM | (12 | ) | -16.9 | % | |||||||||||||||||||||||||

| Gain on sale of mortgage loans |

26 | — | — | — | — | 26 | NM | 26 | NM | |||||||||||||||||||||||||||

| Other |

67 | 57 | 62 | 68 | 68 | 10 | 17.5 | % | (1 | ) | -1.5 | % | ||||||||||||||||||||||||

| Total non-interest income |

$ | 1,213 | $ | 750 | $ | 756 | $ | 812 | $ | 718 | $ | 463 | 61.7 | % | $ | 495 | 68.9 | % | ||||||||||||||||||

| Non-Interest Expense | ||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Salaries and employee benefits |

$ | 601 | $ | 582 | $ | 560 | $ | 575 | $ | 566 | $ | 19 | 3.3 | % | $ | 35 | 6.2 | % | ||||||||||||||||||

| Net occupancy expense |

108 | 110 | 110 | 120 | 114 | (2 | ) | -1.8 | % | (6 | ) | -5.3 | % | |||||||||||||||||||||||

| Furniture and equipment expense |

76 | 75 | 79 | 74 | 74 | 1 | 1.3 | % | 2 | 2.7 | % | |||||||||||||||||||||||||

| Professional and legal fees |

92 | 71 | 75 | 66 | 108 | 21 | 29.6 | % | (16 | ) | -14.8 | % | ||||||||||||||||||||||||

| Marketing expense |

14 | 22 | 18 | 15 | 18 | (8 | ) | -36.4 | % | (4 | ) | -22.2 | % | |||||||||||||||||||||||

| Amortization of core deposit intangible |

26 | 27 | 27 | 28 | 29 | (1 | ) | -3.7 | % | (3 | ) | -10.3 | % | |||||||||||||||||||||||

| Other real estate owned expense |

61 | 65 | 41 | 42 | 64 | (4 | ) | -6.2 | % | (3 | ) | -4.7 | % | |||||||||||||||||||||||

| Other-than-temporary impairments, net |

— | 1 | — | 1 | — | (1 | ) | NM | — | 0.0 | % | |||||||||||||||||||||||||

| FDIC premiums |

52 | 51 | 58 | 59 | 54 | 1 | 2.0 | % | (2 | ) | -3.7 | % | ||||||||||||||||||||||||

| Valuation charges associated with branch consolidations |

— | — | — | 1 | 3 | — | — | (3 | ) | NM | ||||||||||||||||||||||||||

| Loss on early extinguishment of debt |

55 | — | — | 53 | — | 55 | NM | 55 | NM | |||||||||||||||||||||||||||

| Regulatory charge |

— | — | 200 | — | — | — | — | — | 0.0 | % | ||||||||||||||||||||||||||

| Other |

181 | 159 | 158 | 196 | 189 | 22 | 13.8 | % | (8 | ) | -4.2 | % | ||||||||||||||||||||||||

| Total non-interest expense |

$ | 1,266 | $ | 1,163 | $ | 1,326 | $ | 1,230 | $ | 1,219 | $ | 103 | 8.9 | % | $ | 47 | 3.9 | % | ||||||||||||||||||

| • | Non-interest income increased $463 million linked quarter; however, on an adjusted basis, after excluding $333 million in securities gains, $26 million gain on sale of mortgage loans and $59 million in leveraged lease termination gains, non-interest revenue increased $47 million or 6% linked quarter |

| • | Service charges income declined $4 million or 1% linked quarter, despite the impact from Regulation E. This quarter reflected solid interchange income due to increased debit card volume and fee-based account growth. The actual impact from Regulation E changes was $57 million, in-line with the previous estimate of between $50 - $60 million for the second half of 2010. |

| • | Brokerage income increased $55 million to $312 million, driven by an increase in investment banking revenue and continued strength in private client revenue |

| • | Mortgage income declined $15 million linked quarter, primarily reflecting the impact of a reduced benefit from mortgage servicing rights and related hedging activities. Origination volumes increased approximately $227 million to $2.6 billion in the fourth quarter and totaled $8.2 billion for the full year. |

| • | Securities gains in 4Q10 reflect the sale of approximately $8.1 billion of agency mortgage-backed securities. The proceeds were reinvested in similar securities with slightly longer durations. |

| • | Non-interest income reflects a $59 million gain recorded as a result of Regions unwinding certain leveraged lease transactions. However, this gain was offset by $56 million in increased tax expense, resulting in a nominal impact to net income. |

| • | Non-interest expenses increased 9% linked quarter, however after adjusting for current quarter’s $55 million loss on early extinguishment of debt, non-interest expenses increased 4% driven by professional and legal fees and revenue-based incentives |

| • | Salaries and benefits expense increased 3% linked quarter, driven by higher incentive-based compensation related to Morgan Keegan |

| • | The Company prepaid approximately $500 million of Federal Home Loan Bank advances, realizing a $55 million loss on the early extinguishment of debt |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 12

Morgan Keegan

| Morgan Keegan | ||||||||||||||||||||||||||||||||||||

| Summary Income Statement (1) | ||||||||||||||||||||||||||||||||||||

| ($ amounts in millions) |

4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | 4Q10 vs. 3Q10 |

4Q10 vs. 4Q09 |

|||||||||||||||||||||||||||||

| Net interest income (3) |

$ | 21 | $ | 15 | $ | 15 | $ | 14 | $ | 14 | $ | 6 | 40.0 | % | $ | 7 | 50.0 | % | ||||||||||||||||||

| Non-interest income |

342 | 309 | 292 | 297 | 320 | 33 | 10.7 | % | 22 | 6.9 | % | |||||||||||||||||||||||||

| Non-interest expense |

320 | 289 | 275 | 272 | 305 | 31 | 10.7 | % | 15 | 4.9 | % | |||||||||||||||||||||||||

| Regulatory charge |

— | — | 200 | — | — | — | NM | — | NM | |||||||||||||||||||||||||||

| Pre-tax Income |

43 | 35 | (168 | ) | 39 | 29 | 8 | 22.9 | % | 14 | 48.3 | % | ||||||||||||||||||||||||

| Income tax expense (benefit) |

26 | 13 | 12 | 14 | 11 | 13 | 100.0 | % | 15 | 136.4 | % | |||||||||||||||||||||||||

| Net income (loss) |

$ | 17 | $ | 22 | $ | (180 | ) | $ | 25 | $ | 18 | (5 | ) | -22.7 | % | (1 | ) | -5.6 | % | |||||||||||||||||

Breakout of Revenue by Division (2)

| ($ amounts in millions) |

Private Client |

Fixed- Income Capital Markets |

Equity Capital Markets |

Investment Banking |

Regions MK Trust |

Asset Management |

Interest & Other |

|||||||||||||||||||||

| Three months ended |

||||||||||||||||||||||||||||

| December 31, 2010 |

||||||||||||||||||||||||||||

| $ amount of revenue |

$ | 124 | $ | 82 | $ | 15 | $ | 57 | $ | 56 | $ | 3 | $ | 30 | ||||||||||||||

| % of gross revenue |

33.8 | % | 22.3 | % | 4.1 | % | 15.5 | % | 15.3 | % | 0.8 | % | 8.2 | % | ||||||||||||||

| Three months ended |

||||||||||||||||||||||||||||

| September 30, 2010 |

||||||||||||||||||||||||||||

| $ amount of revenue |

$ | 119 | $ | 89 | $ | 12 | $ | 32 | $ | 54 | $ | 3 | $ | 19 | ||||||||||||||

| % of gross revenue |

36.3 | % | 27.1 | % | 3.7 | % | 9.8 | % | 16.5 | % | 0.9 | % | 5.7 | % | ||||||||||||||

| Year Ended |

||||||||||||||||||||||||||||

| December 31, 2010 |

||||||||||||||||||||||||||||

| $ amount of revenue |

$ | 476 | $ | 322 | $ | 55 | $ | 151 | $ | 211 | $ | 15 | $ | 89 | ||||||||||||||

| % of gross revenue |

36.1 | % | 24.4 | % | 4.2 | % | 11.4 | % | 16.0 | % | 1.1 | % | 6.8 | % | ||||||||||||||

| Year ended |

||||||||||||||||||||||||||||

| December 31, 2009 |

||||||||||||||||||||||||||||

| $ amount of revenue |

$ | 415 | $ | 360 | $ | 59 | $ | 104 | $ | 197 | $ | 39 | $ | 108 | ||||||||||||||

| % of gross revenue |

32.4 | % | 28.1 | % | 4.6 | % | 8.1 | % | 15.4 | % | 3.0 | % | 8.4 | % | ||||||||||||||

| (1) | Certain amounts in the prior periods have been reclassified to reflect current period presentation |

| (2) | “Breakout of Revenue by Division” has been adjusted to reflect changes in the company’s reporting structure |

| (3) | Net interest income in the Summary Income Statement is illustrated on a net basis, whereas the Breakout of Revenue by Division, revenue is illustrated on a gross basis. 4Q10, 3Q10, 2Q10, 1Q10 and 4Q09 in the Summary Income Statement exclude $3 million each quarter of gross interest income. |

| • | Morgan Keegan’s Investment Banking division revenue was aided by an improved market for investment banking, particularly in the division’s Technology, Healthcare and Public Finance groups. |

| • | Customer and trust assets under management increased $5.3 billion linked quarter to $157 billion |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 13

Credit Quality

| Credit Quality | ||||||||||||||||||||

| As of and for Quarter Ended | ||||||||||||||||||||

| ($ amounts in millions) |

12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | |||||||||||||||

| Allowance for credit losses (ACL) |

$ | 3,256 | $ | 3,256 | $ | 3,256 | $ | 3,250 | $ | 3,188 | ||||||||||

| Provision for loan losses |

682 | 760 | 651 | 770 | 1,179 | |||||||||||||||

| Provision for unfunded credit losses |

— | — | 5 | (8 | ) | 10 | ||||||||||||||

| Net loans charged-off:* |

||||||||||||||||||||

| Commercial and industrial |

128 | 89 | 87 | 92 | 76 | |||||||||||||||

| Commercial real estate mortgage - owner-occupied |

80 | 64 | 39 | 32 | 38 | |||||||||||||||

| Commercial real estate construction - owner-occupied |

4 | 3 | 3 | 14 | 9 | |||||||||||||||

| Total commercial |

212 | 156 | 129 | 138 | 123 | |||||||||||||||

| Commercial investor real estate mortgage |

202 | 254 | 203 | 207 | 210 | |||||||||||||||

| Commercial investor real estate construction |

99 | 171 | 133 | 150 | 159 | |||||||||||||||

| Total investor real estate |

301 | 425 | 336 | 357 | 369 | |||||||||||||||

| Residential first mortgage |

56 | 58 | 61 | 62 | 55 | |||||||||||||||

| Home equity |

92 | 102 | 106 | 116 | 113 | |||||||||||||||

| Indirect |

4 | 3 | 4 | 8 | 10 | |||||||||||||||

| Other consumer |

17 | 15 | 15 | 19 | 22 | |||||||||||||||

| Total |

$ | 682 | $ | 759 | $ | 651 | $ | 700 | $ | 692 | ||||||||||

| Net loan charge-offs as a% of average loans, annualized * |

||||||||||||||||||||

| Commercial and industrial |

2.31 | % | 1.66 | % | 1.65 | % | 1.74 | % | 1.39 | % | ||||||||||

| Commercial real estate mortgage - owner-occupied |

2.64 | % | 2.12 | % | 1.28 | % | 1.09 | % | 1.26 | % | ||||||||||

| Commercial real estate construction - owner-occupied |

3.54 | % | 1.95 | % | 2.17 | % | 8.41 | % | 4.45 | % | ||||||||||

| Total commercial |

2.44 | % | 1.83 | % | 1.53 | % | 1.64 | % | 1.41 | % | ||||||||||

| Commercial investor real estate mortgage |

5.63 | % | 6.67 | % | 5.22 | % | 5.17 | % | 5.11 | % | ||||||||||

| Commercial investor real estate construction |

14.91 | % | 19.57 | % | 12.33 | % | 12.00 | % | 10.26 | % | ||||||||||

| Total investor real estate |

7.09 | % | 9.09 | % | 6.77 | % | 6.80 | % | 6.52 | % | ||||||||||

| Residential first mortgage |

1.42 | % | 1.48 | % | 1.58 | % | 1.63 | % | 1.40 | % | ||||||||||

| Home equity |

2.53 | % | 2.74 | % | 2.84 | % | 3.07 | % | 2.89 | % | ||||||||||

| Indirect |

1.09 | % | 0.64 | % | 0.72 | % | 1.38 | % | 1.58 | % | ||||||||||

| Other consumer |

5.54 | % | 5.03 | % | 5.23 | % | 6.68 | % | 7.37 | % | ||||||||||

| Total |

3.22 | % | 3.52 | % | 2.99 | % | 3.16 | % | 2.99 | % | ||||||||||

| Non-accrual loans, excluding loans held for sale |

$ | 3,160 | $ | 3,372 | $ | 3,473 | $ | 3,706 | $ | 3,488 | ||||||||||

| Non-performing loans held for sale |

304 | 393 | 256 | 256 | 317 | |||||||||||||||

| Non-accrual loans, including loans held for sale |

$ | 3,464 | $ | 3,765 | $ | 3,729 | $ | 3,962 | $ | 3,805 | ||||||||||

| Foreclosed properties |

454 | 461 | 546 | 610 | 607 | |||||||||||||||

| Non-performing assets (NPAs) |

$ | 3,918 | $ | 4,226 | $ | 4,275 | $ | 4,572 | $ | 4,412 | ||||||||||

| Loans past due > 90 days* |

$ | 585 | $ | 593 | $ | 612 | $ | 700 | $ | 688 | ||||||||||

| Commercial loans restructured not included in categories above |

$ | 268 | $ | 173 | $ | 47 | $ | 48 | $ | 25 | ||||||||||

| Consumer loans restructured not included in categories above** |

$ | 1,215 | $ | 1,126 | $ | 1,192 | $ | 1,258 | $ | 1,583 | ||||||||||

| Total restructured loans not included in categories above |

$ | 1,483 | $ | 1,299 | $ | 1,239 | $ | 1,306 | $ | 1,608 | ||||||||||

| Credit Ratios: |

||||||||||||||||||||

| ACL/Loans, net |

3.93 | % | 3.86 | % | 3.79 | % | 3.69 | % | 3.52 | % | ||||||||||

| ALL/Loans, net |

3.84 | % | 3.77 | % | 3.71 | % | 3.61 | % | 3.43 | % | ||||||||||

| Allowance for loan losses to non-performing loans, excluding loans held for sale |

1.01x | 0.94x | 0.92x | 0.86x | 0.89x | |||||||||||||||

| NPAs (ex. 90+ past due)/Loans and foreclosed properties |

4.70 | % | 4.98 | % | 4.94 | % | 5.15 | % | 4.83 | % | ||||||||||

| NPAs (inc. 90+ past due)/Loans and foreclosed properties |

5.40 | % | 5.68 | % | 5.65 | % | 5.94 | % | 5.59 | % | ||||||||||

| * | See pages 14-17 for loan portfolio (risk view) breakout |

| ** | At 12/31/10, 67 percent of consumer loans restructured not included in categories above consist of residential first mortgages. |

| Allowance for Credit Losses | ||||||||

| ($ amounts in millions) |

Year Ended December 31 | |||||||

| 2010 | 2009 | |||||||

| Balance at beginning of year |

$ | 3,188 | $ | 1,900 | ||||

| Net loans charged-off |

(2,792 | ) | (2,253 | ) | ||||

| Provision for loan losses |

2,863 | 3,541 | ||||||

| Provision for unfunded credit commitments |

(3 | ) | — | |||||

| Balance at end of period |

$ | 3,256 | $ | 3,188 | ||||

| Components: |

||||||||

| Allowance for loan losses |

$ | 3,185 | $ | 3,114 | ||||

| Reserve for unfunded credit commitments |

71 | 74 | ||||||

| Allowance for credit losses |

$ | 3,256 | $ | 3,188 | ||||

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 14

Total Loan Portfolio

| 4Q2010 | 3Q2010 | 2Q2010 | 1Q2010 | 4Q2009 | ||||||||||||||||||||||||||||||||||||

| ($ millions) |

$ | % Total |

$ | % Total |

$ | % Total |

$ | % Total |

$ | % Total |

||||||||||||||||||||||||||||||

| Commercial and Industrial |

22,540 | 27.2 | % | 21,501 | 25.5 | % | 21,096 | 24.6 | % | 21,220 | 24.1 | % | 21,547 | 23.8 | % | |||||||||||||||||||||||||

| Commercial Real Estate Mortgage - OO |

12,046 | 14.5 | % | 11,850 | 14.0 | % | 11,967 | 13.9 | % | 12,028 | 13.6 | % | 12,054 | 13.3 | % | |||||||||||||||||||||||||

| Commercial Real Estate Construction - OO |

470 | 0.6 | % | 522 | 0.6 | % | 547 | 0.6 | % | 598 | 0.7 | % | 751 | 0.8 | % | |||||||||||||||||||||||||

| Total Commercial |

35,056 | 42.3 | % | 33,873 | 40.1 | % | 33,610 | 39.1 | % | 33,846 | 38.4 | % | 34,352 | 37.9 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Mortgage |

13,621 | 16.4 | % | 14,489 | 17.2 | % | 15,152 | 17.6 | % | 15,702 | 17.8 | % | 16,109 | 17.8 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Construction |

2,287 | 2.8 | % | 2,975 | 3.5 | % | 3,778 | 4.4 | % | 4,703 | 5.3 | % | 5,591 | 6.2 | % | |||||||||||||||||||||||||

| Total Investor Real Estate |

15,908 | 19.2 | % | 17,464 | 20.7 | % | 18,930 | 22.0 | % | 20,405 | 23.1 | % | 21,700 | 23.9 | % | |||||||||||||||||||||||||

| Residential First Mortgage |

14,898 | 18.0 | % | 15,723 | 18.6 | % | 15,567 | 18.1 | % | 15,592 | 17.7 | % | 15,632 | 17.2 | % | |||||||||||||||||||||||||

| Home Equity |

14,226 | 17.2 | % | 14,534 | 17.2 | % | 14,802 | 17.2 | % | 15,066 | 17.1 | % | 15,381 | 17.0 | % | |||||||||||||||||||||||||

| Direct |

838 | 1.0 | % | 828 | 1.0 | % | 799 | 0.9 | % | 774 | 0.9 | % | 783 | 0.9 | % | |||||||||||||||||||||||||

| Indirect |

1,592 | 1.9 | % | 1,657 | 2.0 | % | 1,900 | 2.2 | % | 2,162 | 2.5 | % | 2,452 | 2.7 | % | |||||||||||||||||||||||||

| Other Consumer |

346 | 0.4 | % | 341 | 0.4 | % | 337 | 0.4 | % | 329 | 0.4 | % | 374 | 0.4 | % | |||||||||||||||||||||||||

| Total Consumer |

31,900 | 38.5 | % | 33,083 | 39.2 | % | 33,405 | 38.9 | % | 33,923 | 38.5 | % | 34,622 | 38.2 | % | |||||||||||||||||||||||||

| Total Loans |

82,864 | 100.0 | % | 84,420 | 100.0 | % | 85,945 | 100.0 | % | 88,174 | 100.0 | % | 90,674 | 100.0 | % | |||||||||||||||||||||||||

OO = Owner Occupied

IRE = Investor Real Estate

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 15

Net Charge-Offs

| 4Q2010 | 3Q2010 | 2Q2010 | 1Q2010 | 4Q2009 | ||||||||||||||||||||||||||||||||||||

| ($ millions) |

$ | % | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||

| Commercial and Industrial |

128 | 2.31 | % | 89 | 1.66 | % | 87 | 1.65 | % | 92 | 1.74 | % | 76 | 1.39 | % | |||||||||||||||||||||||||

| Commercial Real Estate Mortgage - OO |

80 | 2.64 | % | 64 | 2.12 | % | 39 | 1.28 | % | 32 | 1.09 | % | 38 | 1.26 | % | |||||||||||||||||||||||||

| Commercial Real Estate Construction - OO |

4 | 3.54 | % | 3 | 1.95 | % | 3 | 2.17 | % | 14 | 8.41 | % | 9 | 4.45 | % | |||||||||||||||||||||||||

| Total Commercial |

212 | 2.44 | % | 156 | 1.83 | % | 129 | 1.53 | % | 138 | 1.64 | % | 123 | 1.41 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Mortgage |

202 | 5.63 | % | 254 | 6.67 | % | 203 | 5.22 | % | 207 | 5.17 | % | 210 | 5.11 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Construction |

99 | 14.91 | % | 171 | 19.57 | % | 133 | 12.33 | % | 150 | 12.00 | % | 159 | 10.26 | % | |||||||||||||||||||||||||

| Total Investor Real Estate |

301 | 7.09 | % | 425 | 9.09 | % | 336 | 6.77 | % | 357 | 6.80 | % | 369 | 6.52 | % | |||||||||||||||||||||||||

| Residential First Mortgage |

56 | 1.42 | % | 58 | 1.48 | % | 61 | 1.58 | % | 62 | 1.63 | % | 55 | 1.40 | % | |||||||||||||||||||||||||

| Home Equity |

92 | 2.53 | % | 102 | 2.74 | % | 106 | 2.84 | % | 116 | 3.07 | % | 113 | 2.89 | % | |||||||||||||||||||||||||

| Direct |

3 | 1.40 | % | 2 | 1.18 | % | 3 | 1.51 | % | 4 | 1.85 | % | 4 | 2.07 | % | |||||||||||||||||||||||||

| Indirect |

4 | 1.09 | % | 3 | 0.64 | % | 4 | 0.72 | % | 8 | 1.38 | % | 10 | 1.58 | % | |||||||||||||||||||||||||

| Other Consumer |

14 | 13.93 | % | 13 | 13.84 | % | 12 | 13.47 | % | 15 | 16.90 | % | 18 | 18.46 | % | |||||||||||||||||||||||||

| Total Consumer |

169 | 2.04 | % | 178 | 2.13 | % | 186 | 2.22 | % | 205 | 2.42 | % | 200 | 2.28 | % | |||||||||||||||||||||||||

| Total Net Charge-Offs |

682 | 3.22 | % | 759 | 3.52 | % | 651 | 2.99 | % | 700 | 3.16 | % | 692 | 2.99 | % | |||||||||||||||||||||||||

OO = Owner Occupied

IRE = Investor Real Estate

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 16

90+ Days Past Due Loans

| 4Q2010 | 3Q2010 | 2Q2010 | 1Q2010 | 4Q2009 | ||||||||||||||||||||||||||||||||||||

| ($ millions) |

$ | % | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||

| Commercial and Industrial |

9 | 0.04 | % | 5 | 0.03 | % | 7 | 0.03 | % | 24 | 0.11 | % | 24 | 0.11 | % | |||||||||||||||||||||||||

| Commercial Real Estate Mortgage - OO |

6 | 0.05 | % | 6 | 0.05 | % | 4 | 0.04 | % | 6 | 0.05 | % | 16 | 0.13 | % | |||||||||||||||||||||||||

| Commercial Real Estate Construction - OO |

1 | 0.12 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | 2 | 0.24 | % | |||||||||||||||||||||||||

| Total Commercial |

16 | 0.05 | % | 11 | 0.03 | % | 11 | 0.03 | % | 30 | 0.09 | % | 42 | 0.12 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Mortgage |

5 | 0.04 | % | 6 | 0.04 | % | 26 | 0.17 | % | 42 | 0.27 | % | 22 | 0.14 | % | |||||||||||||||||||||||||

| Commercial Investor Real Estate Construction |

1 | 0.04 | % | 2 | 0.05 | % | 4 | 0.10 | % | 6 | 0.14 | % | 8 | 0.14 | % | |||||||||||||||||||||||||

| Total Investor Real Estate |

6 | 0.04 | % | 8 | 0.04 | % | 30 | 0.16 | % | 48 | 0.24 | % | 30 | 0.14 | % | |||||||||||||||||||||||||

| Residential First Mortgage |

359 | 2.41 | % | 369 | 2.35 | % | 349 | 2.24 | % | 365 | 2.34 | % | 361 | 2.31 | % | |||||||||||||||||||||||||

| Home Equity |

198 | 1.39 | % | 198 | 1.36 | % | 215 | 1.45 | % | 249 | 1.65 | % | 241 | 1.57 | % | |||||||||||||||||||||||||

| Direct |

1 | 0.13 | % | 2 | 0.21 | % | 1 | 0.14 | % | 1 | 0.17 | % | 2 | 0.30 | % | |||||||||||||||||||||||||

| Indirect |

2 | 0.13 | % | 2 | 0.14 | % | 3 | 0.12 | % | 3 | 0.16 | % | 6 | 0.24 | % | |||||||||||||||||||||||||

| Other Consumer |

3 | 0.88 | % | 3 | 0.79 | % | 3 | 0.90 | % | 4 | 1.20 | % | 6 | 1.34 | % | |||||||||||||||||||||||||

| Total Consumer |

563 | 1.76 | % | 574 | 1.74 | % | 571 | 1.71 | % | 622 | 1.83 | % | 616 | 1.78 | % | |||||||||||||||||||||||||

| Total 90+ Days Past Due Loans |

585 | 0.71 | % | 593 | 0.70 | % | 612 | 0.71 | % | 700 | 0.79 | % | 688 | 0.76 | % | |||||||||||||||||||||||||

OO = Owner Occupied

IRE = Investor Real Estate

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 17

Non-Accrual Loans (excludes loans held for sale)

| 4Q2010 | 3Q2010 | 2Q2010 | 1Q2010 | 4Q2009 | ||||||||||||||||||||||||||||||||||||

| ($ millions) |

$ | % | $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||||

| Total Commercial & Industrial |

467 | 2.07 | % | 502 | 2.33 | % | 479 | 2.27 | % | 517 | 2.43 | % | 427 | 1.98 | % | |||||||||||||||||||||||||

| Total Commercial Real Estate Mortgage - OO |

606 | 5.03 | % | 616 | 5.20 | % | 680 | 5.68 | % | 623 | 5.18 | % | 560 | 4.65 | % | |||||||||||||||||||||||||

| Total Commercial Real Estate Construction - OO |

29 | 6.19 | % | 35 | 6.65 | % | 37 | 6.77 | % | 38 | 6.47 | % | 50 | 6.69 | % | |||||||||||||||||||||||||

| Total Commercial |

1,102 | 3.14 | % | 1,153 | 3.40 | % | 1,196 | 3.56 | % | 1,178 | 3.48 | % | 1,037 | 3.02 | % | |||||||||||||||||||||||||

| Total Commercial Investor Real Estate Mortgage |

1,265 | 9.28 | % | 1,347 | 9.30 | % | 1,286 | 8.49 | % | 1,343 | 8.55 | % | 1,203 | 7.47 | % | |||||||||||||||||||||||||

| Total Commercial Investor Real Estate Construction |

452 | 19.76 | % | 561 | 18.87 | % | 754 | 19.94 | % | 986 | 20.97 | % | 1,067 | 19.07 | % | |||||||||||||||||||||||||

| Total Investor Real Estate |

1,717 | 10.79 | % | 1,908 | 10.93 | % | 2,040 | 10.77 | % | 2,329 | 11.41 | % | 2,270 | 10.46 | % | |||||||||||||||||||||||||

| Residential First Mortgage |

285 | 1.92 | % | 267 | 1.70 | % | 212 | 1.36 | % | 199 | 1.28 | % | 180 | 1.15 | % | |||||||||||||||||||||||||

| Home Equity |

56 | 0.40 | % | 44 | 0.30 | % | 25 | 0.17 | % | — | 0.00 | % | 1 | 0.00 | % | |||||||||||||||||||||||||

| Direct |

— | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | |||||||||||||||||||||||||

| Indirect |

— | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | |||||||||||||||||||||||||

| Other Consumer |

— | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | |||||||||||||||||||||||||

| Total Consumer |

341 | 1.07 | % | 311 | 0.94 | % | 237 | 0.71 | % | 199 | 0.59 | % | 181 | 0.52 | % | |||||||||||||||||||||||||

| Total Non-Accrual Loans |

3,160 | 3.81 | % | 3,372 | 3.99 | % | 3,473 | 4.04 | % | 3,706 | 4.20 | % | 3,488 | 3.85 | % | |||||||||||||||||||||||||

OO = Owner Occupied

IRE = Investor Real Estate

| FINANCIAL SUPPLEMENT TO FOURTH QUARTER 2010 EARNINGS RELEASE PAGE 18 |

| FINANCIAL SUPPLEMENT TO FOURTH QUARTER 2010 EARNINGS RELEASE PAGE 19 |

| FINANCIAL SUPPLEMENT TO FOURTH QUARTER 2010 EARNINGS RELEASE PAGE 20 |

| FINANCIAL SUPPLEMENT TO FOURTH QUARTER 2010 EARNINGS RELEASE PAGE 21 |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 22

Home Equity Lending Net Charge-off Analysis

| 4Q10 | 3Q10 | 2Q10 | 1Q10 | 4Q09 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ($ in millions) |

1st Lien |

2nd Lien |

Total | 1st Lien |

2nd Lien |

Total | 1st Lien |

2nd Lien |

Total | 1st Lien |

2nd Lien |

Total | 1st Lien |

2nd Lien |

Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Florida | Net Charge-off%* | 2.26 | % | 6.46 | % | 4.81 | % | 2.37 | % | 6.83 | % | 5.09 | % | 3.12 | % | 7.10 | % | 5.57 | % | 2.92 | % | 7.96 | % | 6.04 | % | 3.17 | % | 7.47 | % | 5.83 | % | |||||||||||||||||||||||||||||||

| $Losses | $ | 11.9 | $ | 52.2 | $ | 64.2 | $ | 12.6 | $ | 56.6 | $ | 69.2 | $ | 16.5 | $ | 59.7 | $ | 76.2 | $ | 15.4 | $ | 68.2 | $ | 83.6 | $ | 17.4 | $ | 66.4 | $ | 83.8 | ||||||||||||||||||||||||||||||||

| Balance | $ | 2,074.3 | $ | 3,166.4 | $ | 5,240.7 | $ | 2,090.0 | $ | 3,253.6 | $ | 5,343.6 | $ | 2,098.0 | $ | 3,333.3 | $ | 5,431.3 | $ | 2,126.5 | $ | 3,424.9 | $ | 5,551.4 | $ | 2,169.7 | $ | 3,485.5 | $ | 5,655.2 | ||||||||||||||||||||||||||||||||

| Original LTV | 65.0 | % | 75.5 | % | 71.3 | % | 65.0 | % | 75.4 | % | 71.3 | % | 65.7 | % | 76.1 | % | 72.1 | % | ||||||||||||||||||||||||||||||||||||||||||||

| All Other States | Net Charge-off %* | 0.75 | % | 1.60 | % | 1.21 | % | 0.98 | % | 1.71 | % | 1.38 | % | 0.75 | % | 1.67 | % | 1.26 | % | 0.74 | % | 1.85 | % | 1.35 | % | 0.93 | % | 1.39 | % | 1.18 | % | |||||||||||||||||||||||||||||||

| $ Losses | $ | 7.9 | $ | 19.8 | $ | 27.7 | $ | 10.5 | $ | 21.8 | $ | 32.3 | $ | 8.0 | $ | 21.6 | $ | 29.6 | $ | 7.9 | $ | 24.0 | $ | 31.9 | $ | 10.4 | $ | 18.8 | $ | 29.2 | ||||||||||||||||||||||||||||||||

| Balance | $ | 4,138.7 | $ | 4,846.2 | $ | 8,984.9 | $ | 4,187.6 | $ | 5,002.4 | $ | 9,190.0 | $ | 4,250.3 | $ | 5,120.4 | $ | 9,370.7 | $ | 4,306.0 | $ | 5,208.4 | $ | 9,514.4 | $ | 4,394.8 | $ | 5,330.6 | $ | 9,725.4 | ||||||||||||||||||||||||||||||||

| Original LTV | 66.8 | % | 79.2 | % | 73.4 | % | 66.9 | % | 79.2 | % | 73.5 | % | 67.7 | % | 79.8 | % | 74.2 | % | ||||||||||||||||||||||||||||||||||||||||||||

| Totals | Net Charge-off %* | 1.26 | % | 3.52 | % | 2.53 | % | 1.45 | % | 3.72 | % | 2.74 | % | 1.53 | % | 3.81 | % | 2.84 | % | 1.46 | % | 4.27 | % | 3.07 | % | 1.67 | % | 3.79 | % | 2.89 | % | |||||||||||||||||||||||||||||||

| $ Losses | $ | 19.8 | $ | 72.1 | $ | 91.9 | $ | 23.1 | $ | 78.4 | $ | 101.5 | $ | 24.5 | $ | 81.3 | $ | 105.8 | $ | 23.3 | $ | 92.2 | $ | 115.5 | $ | 27.8 | $ | 85.2 | $ | 113.0 | ||||||||||||||||||||||||||||||||

| Balance | $ | 6,213.0 | $ | 8,012.6 | $ | 14,225.6 | $ | 6,277.6 | $ | 8,256.0 | $ | 14,533.6 | $ | 6,348.3 | $ | 8,453.7 | $ | 14,802.0 | $ | 6,432.5 | $ | 8,633.3 | $ | 15,065.8 | $ | 6,564.5 | $ | 8,816.1 | $ | 15,380.6 | ||||||||||||||||||||||||||||||||

| Original LTV | 66.2 | % | 77.7 | % | 72.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| * | 22% Florida second lien concentration driving results |

| * | Second lien, Florida net charge-offs represent 57% of 4Q10 net charge-offs but just 22% of outstanding balances. |

| * | Net charge-offs in Florida approximately 4 times non-Florida net charge-off rate |

| * | Current quarter’s origination quality is solid with an average FICO of 777 and an average LTV of 64%; Property value declines driving losses |

Notes: * Recoveries are pro-rated based on charge-off balances.

| * | Balances shown on an ending basis. Net loss rates calculated using average balances |

| * | Original LTVs shown for current period only; prior period LTVs not materially different |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 23

| (in millions) |

4Q09 | 1Q10 | 2Q10 | 3Q10 | 4Q10 | |||||||||||||||

| Net Charge-offs |

||||||||||||||||||||

| IRE Valuation Losses |

$ | 215 | $ | 198 | $ | 142 | $ | 132 | $ | 110 | ||||||||||

| Investor Real Estate (IRE) |

55 | 59 | 74 | 73 | 95 | |||||||||||||||

| Commercial |

107 | 128 | 117 | 143 | 197 | |||||||||||||||

| Consumer Real Estate |

168 | 177 | 167 | 160 | 148 | |||||||||||||||

| Other Consumer |

32 | 28 | 19 | 18 | 21 | |||||||||||||||

| Net Charge-offs excluding charge-offs from Sales / Transfers to HFS |

577 | 590 | 519 | 526 | 571 | |||||||||||||||

| Sales/Transfer to HFS |

115 | 110 | 132 | 233 | 111 | |||||||||||||||

| Total Net Charge-offs |

$ | 692 | $ | 700 | $ | 651 | $ | 759 | $ | 682 | ||||||||||

| Net Loss / (Gain) - HFS Sales |

2 | 6 | (9 | ) | (2 | ) | (7 | ) | ||||||||||||

| HFS Write-downs (1) |

9 | 10 | 5 | 7 | 21 | |||||||||||||||

| OREO expense |

65 | 42 | 40 | 65 | 61 | |||||||||||||||

| Total Credit Costs |

$ | 768 | $ | 758 | $ | 687 | $ | 829 | $ | 757 | ||||||||||

| (1) | Reflects write-downs subsequent to initial move to held for sale and write-downs upon transfer to OREO |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 24

Gross and Net NPA Migration

| ($ in millions) |

4Q 2009 | 1Q 2010 | 2Q 2010 | 3Q 2010 | 4Q 2010 | |||||||||||||||

| Beginning Non-Performing Assets1 |

$ | 4,099 | $ | 4,412 | $ | 4,572 | $ | 4,275 | $ | 4,226 | ||||||||||

| Additions |

$ | 1,383 | $ | 1,303 | $ | 865 | $ | 1,410 | $ | 1,021 | ||||||||||

| Payments |

(89 | ) | (127 | ) | (139 | ) | (155 | ) | (208 | ) | ||||||||||

| Returned to Accruing Status |

(44 | ) | (55 | ) | (58 | ) | (100 | ) | (140 | ) | ||||||||||

| Charge-Offs / OREO Write-Downs |

(509 | ) | (473 | ) | (458 | ) | (497 | ) | (576 | ) | ||||||||||

| Net Additions |

$ | 741 | $ | 648 | $ | 210 | $ | 658 | $ | 97 | ||||||||||

| Non-Accrual Asset Sales |

(300 | ) | (386 | ) | (336 | ) | (511 | ) | (309 | ) | ||||||||||

| OREO Sales |

(128 | ) | (102 | ) | (171 | ) | (196 | ) | (96 | ) | ||||||||||

| Ending Non-Performing Assets1 |

$ | 4,412 | $ | 4,572 | $ | 4,275 | $ | 4,226 | $ | 3,918 | ||||||||||

| Change Versus Previous Quarter |

$ | 313 | $ | 160 | ($297 | ) | ($49 | ) | ($308 | ) | ||||||||||

| 1 | Includes Loans Held for Sale |

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 25

Additional Financial and Operational Data

| 12/31/10 | 9/30/10 | 6/30/10 | 3/31/10 | 12/31/09 | ||||||||||||||||

| Associate headcount |

27,829 | 27,898 | 27,895 | 28,213 | 28,509 | |||||||||||||||

| Total branch outlets |

1,772 | 1,774 | 1,774 | 1,774 | 1,895 | |||||||||||||||

| ATMs |

2,148 | 2,150 | 2,162 | 2,198 | 2,304 | |||||||||||||||

| Morgan Keegan offices |

321 | 329 | 325 | 321 | 324 | |||||||||||||||

FINANCIAL SUPPLEMENT TO

FOURTH QUARTER 2010 EARNINGS RELEASE

PAGE 26

Reconciliation to GAAP Financial Measures