Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - OMNICARE INC | form8k-jpm.htm |

JP Morgan 29th Annual

Healthcare Conference

Healthcare Conference

January 12, 2011

Exhibit 99.1

Forward-Looking Statements

Except for historical information discussed, the statements made today are

forward-looking statements that involve risks and uncertainties. Investors

are cautioned that such statements are only predictions and that actual

events or results may differ materially.

forward-looking statements that involve risks and uncertainties. Investors

are cautioned that such statements are only predictions and that actual

events or results may differ materially.

These forward-looking statements speak only as of this date. We undertake

no obligation to publicly release the results of any revisions to the forward-

looking statements made today, to reflect events or circumstances after

today or to reflect the occurrence of unanticipated events.

no obligation to publicly release the results of any revisions to the forward-

looking statements made today, to reflect events or circumstances after

today or to reflect the occurrence of unanticipated events.

To facilitate comparisons and enhance understanding of core operating

performance, certain financial measures have been adjusted from the

comparable amount under Generally Accepted Accounting Principles

(GAAP). A detailed reconciliation of adjusted numbers to GAAP is posted

the Investor Relations section of our Web site at http://ir.omnicare.com.

performance, certain financial measures have been adjusted from the

comparable amount under Generally Accepted Accounting Principles

(GAAP). A detailed reconciliation of adjusted numbers to GAAP is posted

the Investor Relations section of our Web site at http://ir.omnicare.com.

2

Omnicare Today

Omnicare Today…

A Leading Provider of Pharmacy Services

A Leading Provider of Pharmacy Services

• Long-term care pharmacy

– Pharmacy services for skilled nursing,

assisted living, chronic care and other settings

assisted living, chronic care and other settings

– 47 states, District of Columbia and Canada

– Dispenses over 110 million prescriptions/year

– Industry leader

• Specialty care

– Supports patients, providers, care-givers,

nurses, physicians and pharma-bio

companies

nurses, physicians and pharma-bio

companies

– Dispenses over 8 million prescriptions/year

– Emerging provider with growth rates

outpacing industry average

outpacing industry average

Instituting a renewed emphasis on customer service while

transitioning to an “operations-focused” company

4

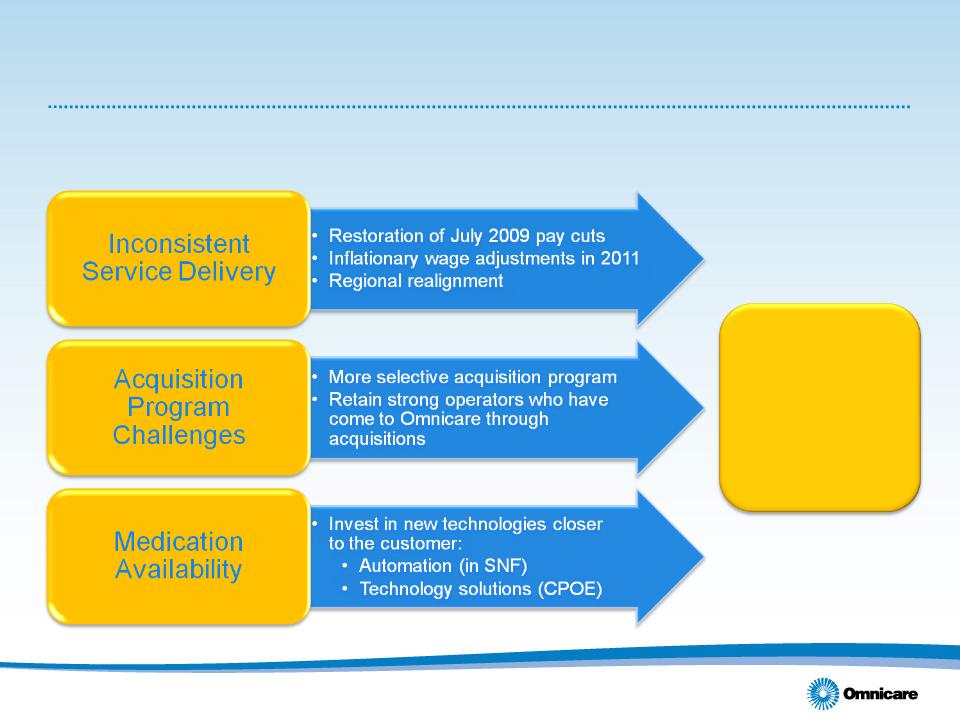

Customer retention issues have been driven largely by inconsistent service

delivery efforts, acquisition program challenges and medication availability

issues (impacted by changing admission schedules to SNFs)

delivery efforts, acquisition program challenges and medication availability

issues (impacted by changing admission schedules to SNFs)

Pay cut - July 2009

Focus on Customer Service

Operational Issues Have Inhibited Customer Growth

Operational Issues Have Inhibited Customer Growth

5

Focus on Customer Service

Elements to Improving Customer Service

Elements to Improving Customer Service

Net Bed

Growth

Growth

Problem

Solution

Result

6

Management Team Changes

New Team Focused on Execution and Growth

New Team Focused on Execution and Growth

• Appointment of John Figueroa as CEO

– President of McKesson’s U.S. Pharmaceutical Group

($90 billion business)

($90 billion business)

– Strong operations background, motivating leader

– Has deep understanding of Omnicare through McKesson relationship

and a broad appreciation for the industry

and a broad appreciation for the industry

– Successful track record

• Additional talent added to Omnicare team

– President of Specialty Care

– SVP of Finance

– SVP of Human Resources

– SVP of Trade Relations

– Promoted five operators to lead newly defined LTC divisions

7

Transitioning to an Operations-Driven Company

• Focus on corporate culture

– Management team changes

– Instill collaborative environment,

encourage employee innovation

encourage employee innovation

– Organization-wide focus on the customer

– Reinforce a commitment to compliance

• Reallocation of resources

– Align employee interests

– Reshape the organization to bring it

closer to the customer

closer to the customer

– Improve accountability with divisional

realignment

realignment

8

Transitioning to an Operations-Driven Company

Initiatives Focused on Organic Growth

Initiatives Focused on Organic Growth

• Enhance the customer experience

– Align customer retention with incentive programs

– Reposition leading technology offering

– Invest in new technologies closer to

the customer

the customer

• Improve selling effectiveness

– Re-engage sales consulting group

– Improve coordination of selling process

– Revamped incentive programs

9

Transitioning to an Operations-Driven Company

Productivity Improvements

Productivity Improvements

• Drug purchasing

• Strategic sourcing

• Operating initiatives

10

Industry Outlook

Regulatory Environment

Current Issues

Current Issues

• RUG-IV

– Medicare reimbursement changes impacting SNFs

– Effective 10/1/10

– Intent is to drive up acuity levels in nursing homes

(through a greater mix of clinically complex residents)

(through a greater mix of clinically complex residents)

– May have the effect of increasing average length of stay within the Part A patient

population

population

• Federal Upper Limit (“FUL”) definitions

– No less than 175% of the weighted average manufacturer’s price (“AMP”) based

on utilization

on utilization

– Effective 10/1/10 (the first FUL list has not yet been published)

– Some Medicaid, facility contracts impacted (Part D contracts restructured to

another reimbursement benchmark)

another reimbursement benchmark)

– In most cases, new FULs would have to be lower than MACs to impact

reimbursement for relevant payers

reimbursement for relevant payers

12

Regulatory Environment

Current Issues

Current Issues

• Short-cycle dispensing

– Weekly dispensing for branded drugs dispensed under Part D

– Effective 1/1/12 (although currently in 60-day

comment period)

comment period)

– Expected to impact approximately

6 million scripts, or 5% of prescriptions

dispensed

6 million scripts, or 5% of prescriptions

dispensed

– We believe the automation within

our pharmacies creates an advantage

over competitors not using automation

over competitors not using automation

13

Demographic Trends

Aging Population Shaping Healthcare

Aging Population Shaping Healthcare

• Life expectancy continues to lengthen

• Significant population mix shift towards seniors

Source: U.S. Census Bureau

14

Pharmaceutical Market

Trends

Trends

• Branded drugs

• Major market shift to generic drugs

• Development and utilization of

specialty drugs increasing

specialty drugs increasing

15

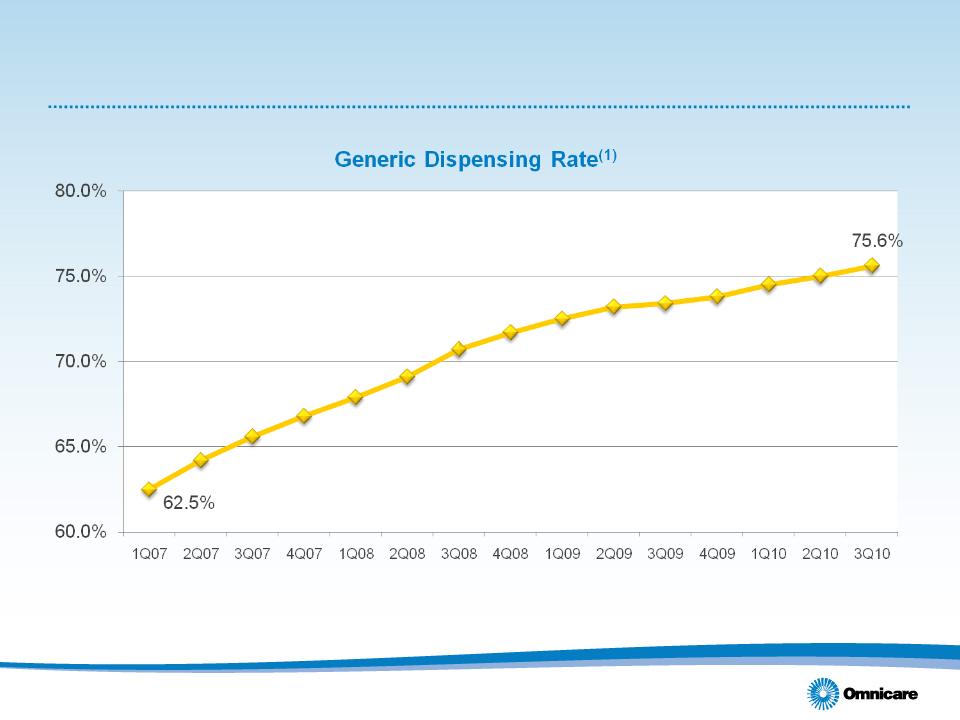

Brand to Generic Drugs

Increasing Utilization of Generics

Increasing Utilization of Generics

(1) Omnicare’s generic prescriptions dispensed as a percent of total scripts

16

Major Shift to Generic Drugs

Benefits

Benefits

• Omnicare’s sourcing abilities create

unique opportunity within industry

unique opportunity within industry

• Reduces sales, but increases gross

profit - both dollars and margins

profit - both dollars and margins

• Favorable impact on working capital

17

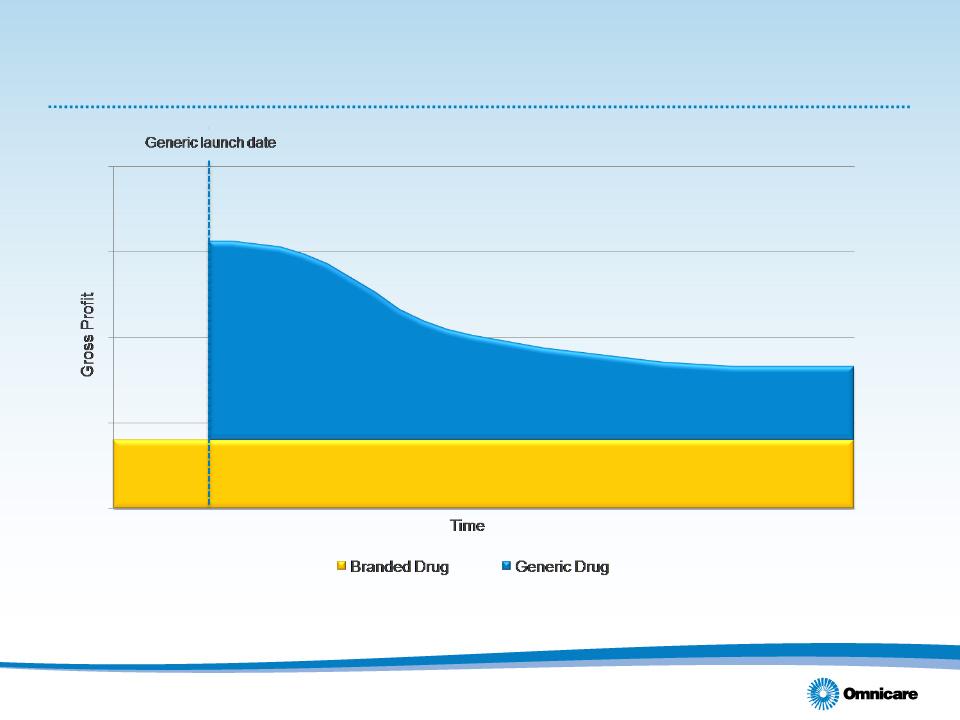

Major Shift to Generic Drugs

Typical Generic Drug Life Cycle

Typical Generic Drug Life Cycle

NOTE: Graph is for illustrative purposes only. Not representative of every generic drug, as each generic drug has unique characteristics.

18

(1) All generic launches are subject to change due to litigation or pediatric exclusivity.

(2) Drugs already launched shown in gray and italics

|

2010

|

2011

|

2012

|

2013

|

|

Arimidex

|

Fazaclo

|

Actos

|

Aciphex

|

|

Cozaar

|

Femara

|

Diovan

|

Asacol

|

|

Effexor ER

|

Gabitril

|

Geodon

|

Avodart

|

|

Exelon Caps

|

Levaquin

|

Invega

|

Cymbalta

|

|

Flomax

|

Lipitor

|

Lexapro

|

Humalog

|

|

Lovenox

|

Tricor

|

Lidoderm

|

Lupron Depot

|

|

Merrem Inj.

|

Uroxatrol

|

Plavix

|

Niaspan SR

|

|

Mirapex

|

Vancocin Caps

|

Seroquel

|

Oxycontin

|

|

Prevacid Soltabs

|

Xalatan

|

Singulair

|

Renagel

|

|

Aricept

|

Zyprexa

|

Xopenex

|

Travatan

|

2010-2013 Potential Patent Expirations(1),(2)

Geriatric Market

Geriatric Market

19

Specialty Pharmaceuticals

A Growth Industry

A Growth Industry

(1) Source: EvaluatePharma

Pharmaceutical Market Share(1) by Drug Type

Mail order specialty pharmacy

Outsourced services for

biotechnology firms

biotechnology firms

Omnicare’s institutional

pharmacies

pharmacies

Conventional

Drugs, 72%

Drugs, 72%

Other, 19%

Omnicare’s Positioning Within Specialty Pharmaceuticals…

20

Growth

Long-Term Care

• Skilled Nursing Facilities

– Selected acquisitions

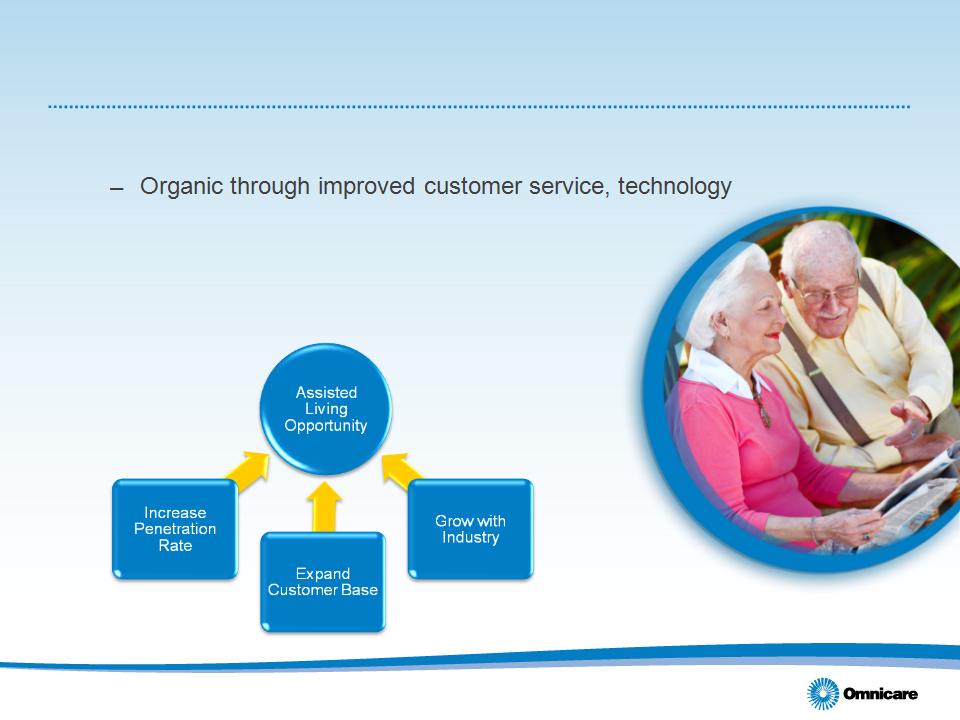

• Assisted Living Facilities

– Three-pronged growth opportunity

22

Specialty Care

Growth Outside Institutional Setting

Growth Outside Institutional Setting

Omnicare specialty care growth has been robust…and opportunities

exist to further accelerate growth through:

exist to further accelerate growth through:

•Addition of new leadership

•Tighter coordination of efforts

•Leveraging long-term care business and relationships to create new

opportunities

opportunities

•Penetrate additional disease states (for ACS)

– Primary disease states currently multiple sclerosis and oncology

•Potential additional acquisitions to fill-out portfolio in the future

Two-year CAGR(1) for Omnicare’s specialty care businesses = 28.1%

(1) Quarterly revenues based on third quarter 2010 results for Advanced Care Scripts, RxCrossroads

and excelleRx (as compared with third quarter 2008 results)

and excelleRx (as compared with third quarter 2008 results)

23

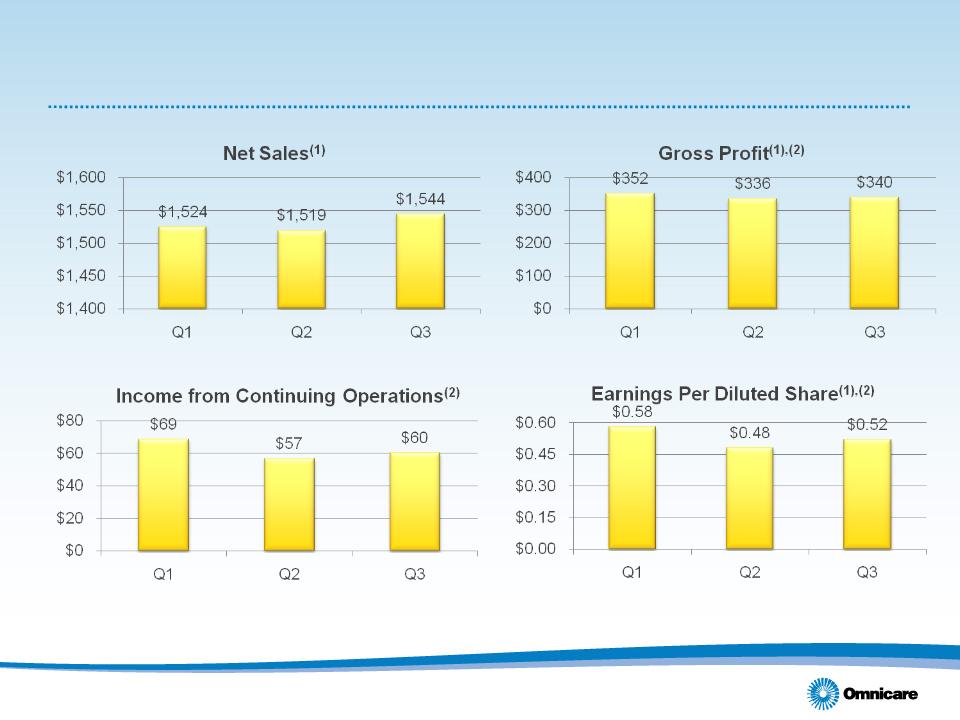

Financial Elements

(1) Excludes discontinued operations.

(2) Excludes special items. A reconciliation of this non-GAAP information is available on Omnicare’s Web site under ‘Supplemental Financial Information’ from

the ‘Investors’ page.

the ‘Investors’ page.

Financial Performance

2010 YTD (In $ millions, except per share data)

2010 YTD (In $ millions, except per share data)

25

Focus on Cash Flows

Demonstrates Quality of Earnings

Demonstrates Quality of Earnings

(2) Cash flows from continuing operations includes approximately $38 million of settlement payments in 2Q10, $21 million of settlement payments in 3Q10 and

$7 million of separation-related payments related to three former Omnicare executives in 3Q10.

$7 million of separation-related payments related to three former Omnicare executives in 3Q10.

(3) Excludes special items. A reconciliation of this non-GAAP information is available on Omnicare’s Web site under ‘Supplemental Financial Information’ from

the ‘Investors’ page.

the ‘Investors’ page.

YTD Cash Flows from Continuing Operations(1),(2) and Interest Expense vs.

YTD Adjusted EBITDA(1),(3) (in $ millions)

26

Capital Returned to Shareholders

2010 YTD (In $ millions)

2010 YTD (In $ millions)

(1) Cumulative % Returned = (YTD Dividends Paid + YTD Share Repurchases) / 12/31/09 Market Capitalization of $2,908.4 million.

34.1% of net operating cash flows returned to shareholders through share

repurchases and dividends during the first three quarters of 2010.

(1) Cumulative % Returned = (YTD Dividends Paid + YTD Share Repurchases) / 12/31/09 Market Capitalization of $2,908.4 million.

27

(1) Assumes convertible debentures due 2035 are put to the company in 2015 with related tax capture included.

(2) Debt amounts shown exclusive of unamortized debt discount.

(3) In $ millions

Capital Structure

Recent Initiatives Create More Flexibility for FCF

Recent Initiatives Create More Flexibility for FCF

Recent capital restructuring initiatives have extended maturities,

providing more flexibility for capital allocation strategies

28

Omnicare’s Fundamental Value Drivers

29

Outlook

2011 Drivers

|

Major 2011 Drivers

|

1st Half 2011

|

2nd Half 2011

|

|

• Brand-to-generic and drug price inflation

|

Positive

|

Positive

|

|

• Annualized pricing adjustments

|

Negative

|

Neutral

|

|

• Annualized impact of bed losses

|

Negative

|

Neutral

|

|

• Impact of payroll costs

|

Negative

|

Negative

|

|

• Productivity improvements

|

Positive

|

Positive

|

2011 drivers point to a weaker 1st half but stronger 2nd half.

2011 guidance expected to be provided on Q4 conference call.

31

Longer-Term Drivers

Omnicare: A Platform to Build Upon

Omnicare: A Platform to Build Upon

We believe investments made in 2011

will position the company for long-term

profitable growth in 2012 and beyond

will position the company for long-term

profitable growth in 2012 and beyond

2011

32

JP Morgan 29th Annual

Healthcare Conference

Healthcare Conference

January 12, 2011