Attached files

| file | filename |

|---|---|

| 8-K - Eagle Bulk Shipping Inc. | d1130325_8-k.htm |

EXHIBIT 99.1

EAGLE BULK SHIPPING INC.

EAGLE BULK SHIPPING INC.

Jefferies

7th Global Shipping Conference

8 September 2010

EAGLE BULK SHIPPING INC.

2

Forward Looking Statements

This presentation contains certain statements that may be deemed to be “forward-looking statements” within the

meaning of the Securities Acts. Forward-looking statements reflect management’s current views with respect to

future events and financial performance and may include statements concerning plans, objectives, goals,

strategies, future events or performance, and underlying assumptions and other statements, which are other

than statements of historical facts. The forward-looking statements in this presentation are based upon various

assumptions, many of which are based, in turn, upon further assumptions, including without limitation,

management's examination of historical operating trends, data contained in our records and other data available

from third parties. Although Eagle Bulk Shipping Inc. believes that these assumptions were reasonable when

made, because these assumptions are inherently subject to significant uncertainties and contingencies which

are difficult or impossible to predict and are beyond our control, Eagle Bulk Shipping Inc. cannot assure you that

it will achieve or accomplish these expectations, beliefs or projections. Important factors that, in our view, could

cause actual results to differ materially from those discussed in the forward-looking statements include the

strength of world economies and currencies, general market conditions, including changes in charterhire rates

and vessel values, changes in demand that may affect attitudes of time charterers to scheduled and

unscheduled drydocking, changes in our vessel operating expenses, including dry-docking and insurance costs,

or actions taken by regulatory authorities, ability of our counterparties to perform their obligations under sales

agreements, charter contracts, and other agreements on a timely basis, potential liability from future litigation,

domestic and international political conditions, potential disruption of shipping routes due to accidents and

political events or acts by terrorists. Risks and uncertainties are further described in reports filed by Eagle Bulk

Shipping Inc. with the US Securities and Exchange Commission.

meaning of the Securities Acts. Forward-looking statements reflect management’s current views with respect to

future events and financial performance and may include statements concerning plans, objectives, goals,

strategies, future events or performance, and underlying assumptions and other statements, which are other

than statements of historical facts. The forward-looking statements in this presentation are based upon various

assumptions, many of which are based, in turn, upon further assumptions, including without limitation,

management's examination of historical operating trends, data contained in our records and other data available

from third parties. Although Eagle Bulk Shipping Inc. believes that these assumptions were reasonable when

made, because these assumptions are inherently subject to significant uncertainties and contingencies which

are difficult or impossible to predict and are beyond our control, Eagle Bulk Shipping Inc. cannot assure you that

it will achieve or accomplish these expectations, beliefs or projections. Important factors that, in our view, could

cause actual results to differ materially from those discussed in the forward-looking statements include the

strength of world economies and currencies, general market conditions, including changes in charterhire rates

and vessel values, changes in demand that may affect attitudes of time charterers to scheduled and

unscheduled drydocking, changes in our vessel operating expenses, including dry-docking and insurance costs,

or actions taken by regulatory authorities, ability of our counterparties to perform their obligations under sales

agreements, charter contracts, and other agreements on a timely basis, potential liability from future litigation,

domestic and international political conditions, potential disruption of shipping routes due to accidents and

political events or acts by terrorists. Risks and uncertainties are further described in reports filed by Eagle Bulk

Shipping Inc. with the US Securities and Exchange Commission.

EAGLE BULK SHIPPING INC.

3

Agenda

§ Investment Thesis

§ Results and Highlights

§ The Fleet

§ Industry

§ Financials

§ Conclusion

Investment Thesis

EAGLE BULK SHIPPING INC.

5

Eagle Bulk, Global Leader in the Supramax Class

|

Transformational Growth

|

||||

|

|

September, 2005

|

September, 2010

|

% Change

|

|

|

Fleet

|

Number of vessels

|

11

|

47

|

+327.3%

|

|

Total DWT

|

540,456

|

2,552,800

|

+372.3%

|

|

|

OTW Average Age (years)

|

5.8

|

4.6

|

-20.7%

|

|

|

Commercial

Current Year Chartering Strategy |

Fixed

|

100%

|

60%

|

-

|

|

Indexed

|

0%

|

20%

|

-

|

|

|

Open

|

0%

|

20%

|

-

|

|

|

Operational

|

Fleet Utilization

|

99.6%

|

99.9%

|

-

|

|

Technical Managers

|

1

|

4 (including in-house)

|

-

|

|

|

Financial

|

Enterprise Value

|

$509m

|

$1,272m

|

+149.9%

|

Growth Delivered

EAGLE BULK SHIPPING INC.

6

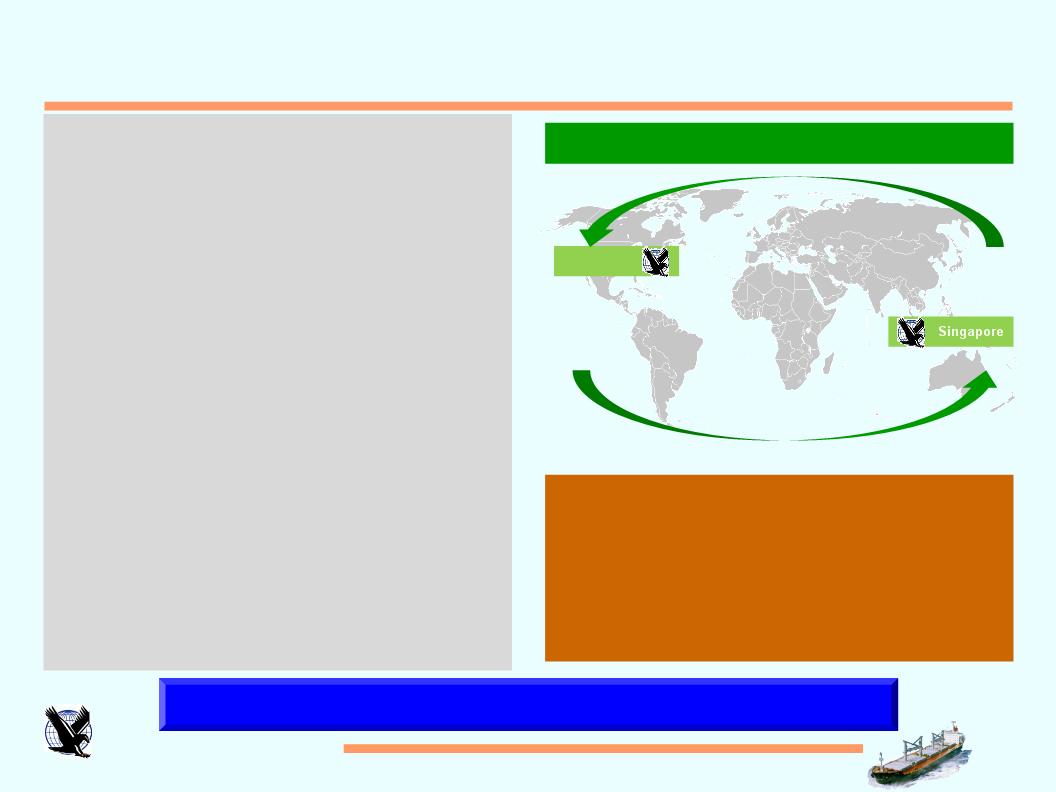

Eagle Bulk Establishes Trading Capabilities

Capturing value in all shipping cycles

Eagle Bulk Pte Ltd:

§Freight Trading division setup by Eagle Bulk

Shipping Inc.

Shipping Inc.

§ Headed by Keith Denholm,

ex-Commercial Director at Pacific Carriers

Limited (Singapore) and Malaysian Bulk

Carriers Berhad.

ex-Commercial Director at Pacific Carriers

Limited (Singapore) and Malaysian Bulk

Carriers Berhad.

§Objective:

§ Leverage the Company’s growing scale in

order to generate excess-returns in all

shipping cycles.

order to generate excess-returns in all

shipping cycles.

§Strategy:

§ Develop value-added relationships with

major industrial producers and users of

drybulk commodities.

major industrial producers and users of

drybulk commodities.

§ Capitalize on market opportunities for both

vessels (i.e. tonnage) and cargoes;

monitor global markets 24/7.

vessels (i.e. tonnage) and cargoes;

monitor global markets 24/7.

Eagle Bulk Pte Ltd Core Activities

§ Trading spot

§ Contracts of Affreightment

§ Timecharter-In/Out

§ Paper derivatives

§ Risk Management

New York

Global Market Coverage 24/7

Results and Highlights

EAGLE BULK SHIPPING INC.

8

1H 2010 Results and YTD Highlights

Results:

§ Net Income of $15.6 million or $0.25 per share.

§ Revenues, net of commissions, of $119.9 million.

§ EBITDA* of $74.6 million.

§ Fleet utilization of 99.5%.

Highlights:

§ Took delivery of 12 newbuilding Supramaxes, expanding fleet by 44.4% to 39:

§ 1Q- 6 vessels

§ 2Q- 3 vessels

§ 3Q- 3 vessels to-date

*EBITDA, as defined by the Company’s credit agreement, is calculated as net income plus interest exp., depreciation, amortization, and exceptional items

The Fleet

EAGLE BULK SHIPPING INC.

10

|

|

Vessel

|

DWT

|

Year

Built |

|

Vessel

|

DWT

|

Year

Built |

|

Vessel

|

DWT

|

Year

Built |

|

1

|

Martin

|

57,776

|

2010

|

14

|

Bittern

|

57,809

|

2009

|

27

|

Kittiwake

|

53,146

|

2002

|

|

2

|

Kingfisher

|

57,776

|

2010

|

15

|

Stellar Eagle

|

55,989

|

2009

|

28

|

Goldeneye

|

52,421

|

2002

|

|

3

|

Jay

|

57,802

|

2010

|

16

|

Crested Eagle

|

55,989

|

2009

|

29

|

Osprey I

|

50,206

|

2002

|

|

4

|

Ibis Bulker

|

57,775

|

2010

|

17

|

Crowned Eagle

|

55,940

|

2008

|

30

|

Heron

|

52,827

|

2001

|

|

5

|

Grebe Bulker

|

57,809

|

2010

|

18

|

Woodstar

|

53,390

|

2008

|

31

|

Falcon

|

51,268

|

2001

|

|

6

|

Gannet Bulker

|

57,809

|

2010

|

19

|

Wren

|

53,349

|

2008

|

32

|

Peregrine

|

50,913

|

2001

|

|

7

|

Imperial Eagle

|

55,989

|

2010

|

20

|

Redwing

|

53,411

|

2007

|

33

|

Condor

|

50,296

|

2001

|

|

8

|

Avocet

|

53,462

|

2010

|

21

|

Cardinal

|

55,362

|

2004

|

34

|

Harrier

|

50,296

|

2001

|

|

9

|

Thrasher

|

53,360

|

2010

|

22

|

Jaeger

|

52,248

|

2004

|

35

|

Hawk I

|

50,296

|

2001

|

|

10

|

Golden Eagle

|

55,989

|

2010

|

23

|

Kestrel I

|

50,326

|

2004

|

36

|

Merlin

|

50,296

|

2001

|

|

11

|

Egret Bulker

|

57,809

|

2010

|

24

|

Skua

|

53,350

|

2003

|

37

|

Sparrow

|

48,225

|

2000

|

|

12

|

Crane

|

57,809

|

2010

|

25

|

Shrike

|

53,343

|

2003

|

38

|

Kite

|

47,195

|

1997

|

|

13

|

Canary

|

57,809

|

2009

|

26

|

Tern

|

50,200

|

2003

|

39

|

Griffon

|

46,635

|

1995

|

On-the-water Fleet

|

TOTAL VESSEL COUNT

|

39

|

TOTAL DWT

|

2,093,700

|

AVERAGE AGE (by DWT)

|

4.6yrs

|

One of the largest and most modern Supramax fleets in the world

EAGLE BULK SHIPPING INC.

11

Fleet Expansion Contributing to Cash Flow

|

2010 Newbuilding Charters

|

|||||

|

|

Vessel

|

Delivery

|

TC Expiration

|

TC Rate

|

Minimum Contracted

Revenue |

|

1

|

Crane

|

1Q10

|

2019

|

$18,850

|

$60m*

|

|

2

|

Egret Bulker

|

1Q10

|

2013

|

$17,650

|

$19m*

|

|

3

|

Golden Eagle

|

1Q10

|

2011

|

indexed to BSI

|

market

|

|

4

|

Thrasher

|

1Q10

|

2019

|

$18,400

|

$59m*

|

|

5

|

Avocet

|

1Q10

|

2019

|

$18,400

|

$59m*

|

|

6

|

Imperial Eagle

|

1Q10

|

2011

|

indexed to BSI

|

market

|

|

7

|

Gannet Bulker

|

2Q10

|

2013

|

$17,650

|

$19m*

|

|

8

|

Grebe Bulker

|

2Q10

|

2013

|

$17,650

|

$19m*

|

|

9

|

Ibis Bulker

|

2Q10

|

2013

|

$17,650

|

$19m*

|

|

10

|

Jay

|

3Q10

|

2018

|

$18,500

|

$56m*

|

|

11

|

Kingfisher

|

3Q10

|

2018

|

$18,500

|

$56m*

|

|

12

|

Martin

|

3Q10

|

2017

|

$18,400

|

$44m

|

|

TOTAL

|

$410m**

|

||||

*Excludes profit-sharing revenue- Egret Bulker, Gannet Bulker, Grebe Bulker, Ibis Bulker, Jay, and Kingfisher profit shares are in effect.

**Excludes both profit-sharing and indexed revenue.

Long-term Visibility

EAGLE BULK SHIPPING INC.

12

§ One vessel to be delivered in 4Q 2010

charter-free.

charter-free.

§ Seven additional vessels to be

delivered in 2011.

delivered in 2011.

§ All have fixed charters which are

expected to generate combined

minimum contracted revenues of

$200m.

expected to generate combined

minimum contracted revenues of

$200m.

Eagle vessel-owned days, CAGRe > 25%

Newbuildings funded from existing cash, facility, and operations

Fleet Expansion Contributing to Cash Flow

EAGLE BULK SHIPPING INC.

13

Supramax Versatility

*Includes alumina, copper, fertilizers, salt, and other.

65% of cargoes carried in 2Q 2010 were “Capesize and Panamax cargoes”

Eagle Bulk 2Q10 Cargoes

§ 3.4m MT carried in the quarter, +47.1% y/y.

|

Drybulks

|

Cargoes Carried by Asset Class

|

|||

|

Handymax /

Supramax |

Panamax

|

Capesize

|

||

|

1

|

Iron Ore

|

yes

|

yes

|

yes

|

|

2

|

Coal

|

yes

|

yes

|

yes

|

|

3

|

Grains / Soybeans

|

yes

|

yes

|

|

|

4

|

Other Ores

|

yes

|

|

|

|

5

|

Cement

|

yes

|

|

|

|

6

|

Coke

|

yes

|

|

|

|

7

|

Steels

|

yes

|

|

|

|

8

|

Scrap Iron

|

yes

|

|

|

|

9

|

Aggregates

|

yes

|

|

|

|

10

|

Sugar

|

yes

|

|

|

|

11

|

Miscellaneous*

|

yes

|

|

|

EAGLE BULK SHIPPING INC.

14

Eagle Bulk Historic Cargoes

CAGR= 58.2%

Industry

EAGLE BULK SHIPPING INC.

16

Power Generation to Dominate Drybulk Trade

Source: CNEA, Peabody

Electricity Usage per Capita

|

Coal-fueled plants coming online in 2010

|

||

|

Region

|

Coal required

(m MT) |

%

|

|

China

|

212

|

58.1%

|

|

India

|

80

|

21.9%

|

|

Other Asia

|

34

|

9.3%

|

|

U.S.

|

25

|

6.9%

|

|

Other

|

14

|

3.8%

|

|

Total

|

365

|

100.0%

|

§ Met coal seaborne trade expected to reach

265m MT in 2010, representing a 17%

increase y/y.

265m MT in 2010, representing a 17%

increase y/y.

§ Steel production to increase 50% by

2020.

2020.

§ Thermal coal seaborne trade expected to

reach 713m MT in 2010, representing a 4%

increase y/y.

reach 713m MT in 2010, representing a 4%

increase y/y.

§ Coal-fired power generation to grow

60% by 2020 to reach 1.4k GW.

60% by 2020 to reach 1.4k GW.

Seaborne trade to reach 1.2B MT by 2015,

+40% from current levels

Coal to Increase Ton-miles

5yr Import/Export Growth Projection (incremental trade)

Canada:

5m

5m

U.S.A.:

5m

5m

Colombia:

25m

25m

Atlantic:

(50m)

(50m)

Russia:

15m

15m

South Africa:

15m

15m

Australia:

170m

170m

India:

(150m)

(150m)

China:

(150m)

(150m)

Korea:

(40m)

(40m)

Japan:

(30m)

(30m)

Indonesia:

80m

80m

EXPORTS

IMPORTS

Demand to outstrip supply

17

EAGLE BULK SHIPPING INC.

18

Grains to contribute to 2H 2010 Supramax Earnings

§ China’s improving standard of living is leading to

increased demand for meat and dairy products:

increased demand for meat and dairy products:

§ Urban household incomes up 10% y/y.

Leading to:

Leading to:

§ Meat product and dairy demand expected to

grow at 7% and 10% per annum,

respectively, for the next 5 years.

grow at 7% and 10% per annum,

respectively, for the next 5 years.

§ Increasing feedstock required to meet

this growing demand.

this growing demand.

§ China imports over 50% of the world’s

soybean exports, demand growth

expected at 8% per annum for the next

three years.

soybean exports, demand growth

expected at 8% per annum for the next

three years.

§ Corn demand expected to grow 5% per

annum for the next five years.

annum for the next five years.

2010 Wheat Trade

Source: Cargill, Clarksons, JPM

§ Severe drought in the Baltic Sea region

has forced Russia to ban wheat exports

until December 31 2010.

has forced Russia to ban wheat exports

until December 31 2010.

§ U.S.D.A. predicts record harvest

for the year.

for the year.

§ Supply substitution will result in

increased ton-mile demand.

increased ton-mile demand.

§ Supramaxes have replaced

Panamaxes as prime beneficiary

on U.S. grain trade.

Panamaxes as prime beneficiary

on U.S. grain trade.

§ BHP Billiton’s bid for Potash

Corporation highlights the positive long-

term fundamentals for fertilizer, a key

requirement for meat and plant

production.

Corporation highlights the positive long-

term fundamentals for fertilizer, a key

requirement for meat and plant

production.

Fertilizers

EAGLE BULK SHIPPING INC.

19

Other Factors Affecting Drybulk

Congestion:

§ Inadequate port and in-land

infrastructure will continue to soak-up

tonnage in the market.

infrastructure will continue to soak-up

tonnage in the market.

§ Increasing global fleet will compete

for drydock services resulting in

bottlenecks/delays which will in-turn

affect utilization.

for drydock services resulting in

bottlenecks/delays which will in-turn

affect utilization.

Source: Clarksons, Peabody

Intra-China Seaborne Coal Trade Routes

Supramax Congestion Calculator

-One vessel > 9 voyages per year.

-Nine voyages = 18 ports of call.

-Assume 3 days delay per vessel for load/discharge

-18 ports of call * 3 delay days= 54 delay days

-54 delay days * 755 vessels= 40,770 total delay days

-40,770 delay days / 365 =

= 111 vessels (14.8% of fleet) per annum

§ This hidden demand is expected to reach 480m MT

in 2010, representing an additional 50% to reported

international seaborne coal trade volumes.

in 2010, representing an additional 50% to reported

international seaborne coal trade volumes.

EAGLE BULK SHIPPING INC.

20

Sub-Panamax: Oldest Fleet / Greatest Slippage

Source: Clarksons, ICAP, SSY

Drybulk Fleet Over 25yrs of Age

Scrapping, currently at low levels, can positively impact the market

2010e Newbuilding Delivery Slippage

1,572

vessels

vessels

70

vessels

vessels

262

vessels

vessels

Financials

EAGLE BULK SHIPPING INC.

22

1H 2010 Earnings

|

Period ending June 30th

(in $000’s,except per share data)

|

|||

|

|

1H 2010

|

1H 2009

|

|

|

REVENUES, net of commissions

|

$119,856

|

$108,999

|

|

|

EXPENSES

|

|

|

|

|

|

Vessel expenses

|

31,530

|

26,005

|

|

|

Depreciation and amortization

|

29,243

|

21,234

|

|

|

General and administrative expenses

|

19,852

|

17,944

|

|

|

Total operating expenses

|

80,625

|

65,183

|

|

OPERATING INCOME

|

$39,231

|

$43,816

|

|

|

|

Interest expense

|

23,785

|

13,302

|

|

|

Interest income

|

(140)

|

(70)

|

|

|

Net interest expense

|

23,645

|

13,232

|

|

NET INCOME

|

$15,586

|

$30,584

|

|

|

EBITDA

|

$68,474

|

$65,050

|

|

|

|

|

|

|

|

EPS (Basic and Diluted)

|

$0.25

|

$0.62

|

|

|

|

|

|

|

|

Weighted average shares outstanding

|

|

|

|

|

Basic

|

62,215,915

|

49,656,431

|

|

|

Diluted

|

62,366,183

|

49,626,359

|

|

EAGLE BULK SHIPPING INC.

23

Balance Sheet

As of: June 30, 2010

(in $000’s)

(in $000’s)

Cash and Restricted Cash

$120,410

Other current assets

14,702

Vessels, net

1,409,038

Advances for vessel construction

240,592

Other assets

28,023

Total assets

$1,812,765

Current liabilities

$33,714

Long-term debt

1,080,241

Other liabilities

54,708

Stockholder’s equity

644,102

Total liabilities and stockholder’s equity

$1,812,765

EAGLE BULK SHIPPING INC.

24

2010 Estimated Cash Break-Even Levels

|

Daily Cash Expenses

|

|

|

Vessel

|

$5,116

|

|

Technical Management

|

307

|

|

G&A

|

1,521

|

|

Cash Interest (net)

|

3,850

|

|

Drydocking

|

603

|

|

Break-Even

|

$11,397

|

$11,397 per day cash break-even cost for 2H 2010

Vessel expenses are comprised of the following items: crew wages and related, insurance, repair and maintenance, stores, spares, and

related inventory, tonnage taxes, newbuilding pre-operating costs (associated with taking delivery of vessels). Eagle anticipates higher

costs relating to crewing and oil based supplies, including lubes and paints. The Company makes an allowance for drydocking

constraints (i.e. decreased drydock capacity drives up costs).

related inventory, tonnage taxes, newbuilding pre-operating costs (associated with taking delivery of vessels). Eagle anticipates higher

costs relating to crewing and oil based supplies, including lubes and paints. The Company makes an allowance for drydocking

constraints (i.e. decreased drydock capacity drives up costs).

Conclusion

EAGLE BULK SHIPPING INC.

26

|

Supramax:

Best

Asset Class |

§ Most versatile and flexible vessels in drybulk.

§ Stable earnings.

|

|

Fleet

|

§ One of the largest and most modern Supramax fleets in the world.

§ Average age of 4.6 years.

|

|

Commercial

|

§ Fixed charter coverage on existing fleet and newbuilds provide for strong

and long-term cash flow visibility. § Open/Indexed exposure allow for upside to earnings.

§ Trading activities to capture value in all shipping cycles.

|

|

Operational

|

§ In-house technical management allows for benchmarking (of third-party

managers) and improved control/costs. § Superior fleet utilization, almost 100% for 2Q 2010.

|

|

Company

|

§ Headquartered in New York City

|

Key Takeaways