Attached files

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM 10-K

x ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

fiscal year ended March 31, 2010

OR

o TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

transition period from

to .

Commission

file number 000-50601

SYNUTRA

INTERNATIONAL, INC.

|

DELAWARE

|

13-4306188

|

|

|

(State

or Other Jurisdiction of

Incorporation

or Organization)

|

I.R.S.

Employer

Identification

No.

|

|

|

2275

Research Blvd., Suite 500

Rockville,

Maryland 20850

|

||

|

(Address

of Principal Executive Offices, Zip Code)

|

||

|

(301)

840-3888

|

||

|

(Registrant’s

Telephone Number, Including Area

Code)

|

||

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which

Registered

|

|

Common

Stock $0.0001 Par Value

|

NASDAQ

Global Select Market

|

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes oNo x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Exchange Act. Yes oNo x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports) and (2) has been subject to such filing requirements for

the past 90 days. Yes x

No o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such

files). Yes o

No o

Indicate

by check mark if disclosure of delinquent filers in response to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer”, “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large

accelerated filer o

|

Accelerated

filer x

|

Non-accelerated

filer o

|

Smaller

reporting company o

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes oNo x

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant based on the closing sales price of the

registrant’s common stock on September 30, 2009 (the last business day of the

registrant’s most recently completed second fiscal quarter), as reported on the

NASDAQ Global Select Market, was $246.8 million. For purposes of this

disclosure, shares of common stock held by persons who hold more than 10% of the

outstanding shares of common stock and shares held by officers and directors of

the registrant have been excluded in that such persons may be deemed to be

affiliates. This determination is not necessarily conclusive for other

purposes.

As of June

1, 2010, there were 54,000,713 shares of the registrant’s common stock

outstanding.

TABLE

OF CONTENTS

Page

PART

I

|

Item

1. Business

|

2

|

|

Item

1A. Risk Factors

|

16

|

|

Item

1B. Unresolved Staff Comments

|

38

|

|

Item

2. Properties

|

38

|

|

Item

3. Legal Proceedings

|

39

|

|

Item

4. [Removed And Reserved]

|

40

|

|

PART

II

|

|

|

Item

5. Market for Registrant’s Common Equity, Related Stockholders Matters and

Issuer Purchases of Equity Securities

|

40

|

|

Item

6. Selected Financial Data

|

41

|

|

Item

7. Management’s Discussion and Analysis of Financial Condition and Results

of Operations

|

42

|

|

Item

7A. Quantitative and Qualitative Disclosures About Market

Risk

|

63

|

|

Item

8. Financial Statements and Supplementary Data

|

64

|

|

Item

9. Changes in and Disagreements With Accountants on Accounting and

Financial Disclosure

|

98

|

|

Item

9A. Controls and Procedures

|

98

|

|

Item

9B. Other Information

|

100

|

|

PART

III

|

|

|

Item

10. Directors, Executive Officers and Corporate Governance

|

101

|

|

Item

11. Executive Compensation

|

105

|

|

Item

12. Security Ownership of Certain Beneficial Owners and Management and

Related Stockholder Matters

|

108

|

|

Item

13. Certain Relationships and Related Transactions, and Director

Independence

|

110

|

|

Item

14. Principal Accounting Fees and Services

|

113

|

|

PART

IV

|

|

|

Item

15. Exhibits and Financial Statement Schedules

|

113

|

|

Signatures

|

114

|

i

CONVENTIONS

THAT APPLY TO THIS ANNUAL REPORT ON FORM 10-K

Except

where the context otherwise requires and for purposes of this Annual Report on

Form 10-K only:

|

·

|

“we,”

“us,” “our company,” “our,” and “Synutra” refer to Synutra International,

Inc., and its consolidated

subsidiaries;

|

|

·

|

“China”

or “PRC” refers to the People’s Republic of China, excluding Taiwan and

the Special Administrative Regions of Hong Kong and

Macau;

|

|

·

|

all

references to “ton” or “tons” are to “tonne” or “metric

ton”;

|

|

·

|

all

references to “Renminbi” or “RMB” are to the legal currency of China;

and

|

|

·

|

all

references to “U.S. dollars,” “dollars,” or “$” are to the legal currency

of the United States.

|

Amounts

may not always add to the totals due to rounding.

Unless

otherwise noted, all translations from Renminbi to U.S. dollars were made at the

mid rate published by the People’s Bank of China, or the mid rate, as of March

31, 2010, which was RMB6.8263 to $1.00. We make no representation that the

Renminbi amounts referred to in this Annual Report on Form 10-K could have been

or could be converted into U.S. dollars at any particular rate or at all. On

June 1, 2010, the mid rate was RMB 6.8279 to $1.00.

PART

I

This

Annual Report on Form 10-K, or Form 10-K, contains “forward-looking statements”

within the meaning of the Private Securities Litigation Reform Act of 1995, that

are based on our current expectations, assumptions, estimates and projections

about us and our industry. All statements other than statements of historical

fact in this Form 10-K are forward-looking statements. In some cases, these

forward-looking statements can be identified by words or phrases such as

“anticipate,” “believe,” “continue,” “estimate,” “expect,” “intend,” “is/are

likely to,” “may,” “plan,” “should,” “will,” “aim,” “potential,” “continue,” or

other similar expressions. The forward-looking statements included in this Form

10-K relate to, among others:

|

·

|

our

goals and strategies;

|

|

·

|

our

future business development, financial condition and results of

operations;

|

|

·

|

the

expected growth of the nutritional products and infant formula markets in

China;

|

|

·

|

market

acceptance of our products;

|

|

·

|

adverse

effects associated with the melamine contamination

incident;

|

|

·

|

our

expectations regarding demand for our

products;

|

|

·

|

our

ability to stay abreast of market trends and technological

advances;

|

|

·

|

competition

in the infant formula industry in

China;

|

|

·

|

PRC

governmental policies and regulations relating to the nutritional products

and infant formula industries; and

|

|

·

|

general

economic and business conditions in

China.

|

These

forward-looking statements involve various risks and uncertainties. Although we

believe that our expectations expressed in these forward-looking statements are

reasonable, our expectations may turn out to be

1

incorrect.

Our actual results could be materially different from our expectations.

Important risks and factors that could cause our actual results to be materially

different from our expectations are generally set forth in the “Item 1.

Business,” “Item 1A. Risk Factors,” “Item 7. Management’s Discussion and

Analysis of Financial Condition and Results of Operations,” and other sections

in this Form 10-K.

The

forward-looking statements are made as of the date of this Form 10-K. We

undertake no obligation to update any forward-looking statements to reflect

events or circumstances after the date on which the statements are made or to

reflect the occurrence of unanticipated events.

ITEM

1. BUSINESS

General

Development and Narrative Description of Business

We are a

leading infant formula company in China. We principally produce, market, and

sell our products under the “Shengyuan” or “Synutra” name, together with other

complementary brands. Our strategy is focused on selling premium infant formula

products, as well as more affordable infant formulas targeting the mass market

and other nutritional products and ingredients. We sell our products through an

extensive nationwide sales and distribution network, including independent

distributors, covering 30 provinces and provincial-level municipalities in

China. As of March 31, 2010, this network comprised over 540 independent

distributors and over 1,000 independent sub-distributors who sell our products

in over 71,000 retail outlets.

We

currently have three reportable segments which are:

|

·

|

the

powdered formula segment, which includes powdered infant and adult formula

products sold under our Super, U-Smart, Mingshan and Helanruniu

sub-brands;

|

|

·

|

the

baby food segment, which includes prepared foods for babies and children

sold under our Huiliduo sub-brand;

and

|

|

·

|

the

nutritional ingredients and supplements segment, which includes the

production and sale of nutritional ingredients and supplements such as

chondroitin sulfate, microencapsulated Docosahexanoic Acid (“DHA”) and

Arachidonic Acid (“ARA”).

|

Our other

business includes non-core operations such as toll packaging, toll drying

service and sales of ingredients and materials to industrial customers. A major

portion of other business for the fiscal year ended March 31, 2010 consist of

sales of surplus industrial milk powder which generated immediate cash flow for

us. Sales from our other business comprised approximately 32.6% of our net sales

for the fiscal year ended March 31, 2010.

On

September 16, 2008, we announced a compulsory recall on certain lots of U-Smart

products and a voluntary recall of other products that were contaminated or

suspected to be contaminated by melamine, a substance not approved for use in

food that is linked to illnesses among infants and children in China. The cost

of this recall during the fiscal year ended March 31, 2009 was $101.5 million,

including the cost of product replacement of $48.1 million in cost of sales, the

write-down and write-off of affected inventory of $48.5 million in cost of

sales, the net amount of $2.3 million to a compensation fund set up by China

Dairy Industry Association to settle existing and potential claims arising in

China from families of infants affected by melamine contamination in general and

administrative expenses, and freight charges of $2.6 million in selling and

distribution expenses, of which $4.5 million was recorded as a product recall

provision in the consolidated balance sheet as of March 31, 2009. During the

fiscal year ended March 31, 2010, we reversed recall expense of $0.9 million,

mostly for overestimated product replacement cost. We believe that the product

recall has been substantially completed and based on current information, we

believe that there should be no further material product recall costs incurred

relating to the melamine contamination incident. We believe that our fast

response to the melamine crisis, as well as recall efforts, including

instituting a voluntary recall were well recognized by the public and helped us

to maintain our reputation, brand recognition and relationships with our

distributors and suppliers.

There

have been certain legal proceedings brought against us in connection with the

melamine contamination incident, which may have an adverse effect on our results

of operations, see Part I - Item 1A. Risk Factors—Risks

2

Related

to Our Business—Product

liability claims against us could result in adverse publicity and potential

significant monetary damages. Although management is not aware of any

additional significant issues associated with the melamine contamination

incident, there can be no assurance that additional issues will not be

identified in the future and this may have an adverse effect on our results of

operations. See Part I - Item 1A. Risk Factors—Risks Related to Our

Business—We are highly

dependent upon consumers’ perception of the safety and quality of our products.

Any ill effects, product liability claims, recalls, adverse publicity or

negative public perception regarding particular ingredients or products or our

industry in general could harm our reputation and damage our brand and adversely

affect our results of operations.

Due to

the lingering impact of the product recall carried out in late calendar year

2008 and a greater proportion of rebates and discounts to distributors, our net

sales for the fiscal year ended March 31, 2010 decreased by 6.6% to $291.9

million from $312.5 million for the prior fiscal year. Our gross profit for the

fiscal year ended March 31, 2010 increased by 56.1% to $83.4 million from $53.4

million for the prior fiscal year. Our net loss attributable to Synutra

International, Inc. common shareholders for the fiscal year ended March 31, 2010

was $24.6 million, as compared to net loss attributable to Synutra

International, Inc. common shareholders of $100.5 million for the prior fiscal

year.

Our

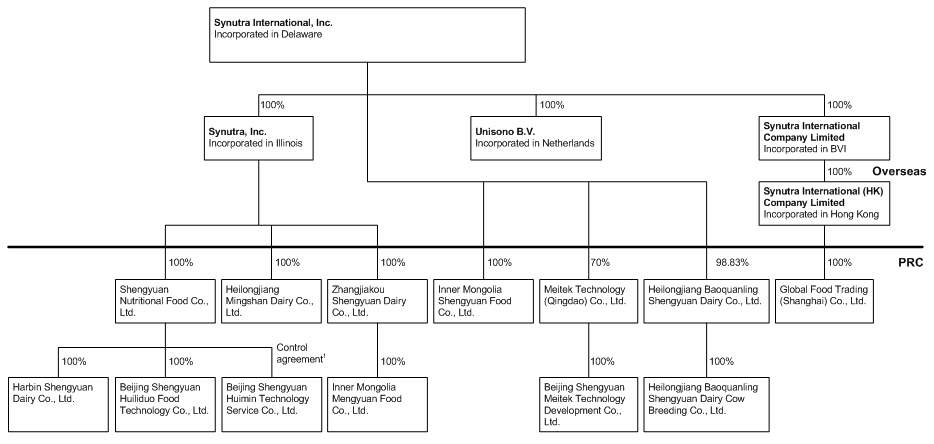

Corporate Structure and History

Synutra

International, Inc is a Delaware holding company that conducts its business

through its operating subsidiaries in China. It owns all or majority of the

equity interests in its operating subsidiaries, directly or indirectly, through

Synutra, Inc., or Synutra Illinois, an intermediate holding company, and Synutra

International Company Limited. Synutra Illinois was incorporated in Illinois in

2000 and has no other significant assets and operations of its own. Our

corporate structure reflects common practice for companies with operations in

the PRC where separate legal entities are often used for tax or administrative

reasons.

On July

15, 2005, Synutra Illinois completed a reverse acquisition transaction with

Vorsatech Ventures, Inc., or Vorsatech. Upon the consummation of this share

exchange transaction, Vorsatech’s total issued and outstanding common stock

equaled 50,000,713 shares, including 48,879,500 shares issued pursuant to the

reverse acquisition transaction and 1,121,213 shares owned by Vorsatech’s

existing stockholders. Thereafter, Synutra Illinois became Vorsatech’s wholly

owned subsidiary and Vorsatech became the reporting entity for our business. We

subsequently changed the name of the reporting entity to Synutra International,

Inc.

On May

24, 2007, we entered into a Common Stock Purchase Agreement with Warburg Pincus

Private Equity IX, L.P., or Warburg, pursuant to which we sold 4,000,000 shares

of our common stock for an aggregate purchase price of $66 million. The closing

of the transaction took place on June 15, 2007.

The

following is a brief description of our major operating subsidiaries in

China.

|

·

|

Shengyuan

Nutritional Food Co., Ltd., or Shengyuan Nutrition, formerly known as

Qingdao St. George Dairy Co., Ltd., located in Qingdao, Shandong, China,

was established by Synutra Illinois in September 2001 and is engaged in

the dry-blending, packaging, shipping and distribution of all of our

powdered formula products; in addition, it plans to provide diagnostic

services for pregnant women pursuant to a series of control agreements and

an entrustment agreement with related

parties.

|

|

·

|

Heilongjiang

Mingshan Dairy Co., Ltd., or Mingshan, formerly known as Luobei Shengyuan

Dairy Co., Ltd., located in Luobei, Heilongjiang, China, was established

in April 2001 and is engaged in raw milk processing and the production of

powdered formula. Synutra Illinois acquired 67% and 33% of the ownership

interest in Mingshan from Sheng Zhi Da Dairy Group Corporation (“Sheng Zhi

Da”) and Xiuqing Meng, the wife of Liang Zhang, our chairman and chief

executive officer, respectively, in January

2005.

|

|

·

|

Zhangjiakou

Shengyuan Dairy Co., Ltd., or

Zhangjiakou, located in Zhangjiakou, Hebei, China, was established in

March 2004 with Synutra Illinois and Sheng Zhi Da holding 40% and 60%,

respectively, of its equity interests and is engaged in raw milk

processing and the production of powdered formula. Synutra Illinois

acquired the remaining 60% ownership interest in Zhangjiakou from Sheng

Zhi Da in April 2005.

|

3

|

·

|

Inner

Mongolia Shengyuan Food Co., Ltd., or Inner Mongolia Shengyuan, located in

Zhenglanqi, Inner Mongolia, China, was established in September 2006 and

has been constructing its production facilities since its

establishment.

|

|

·

|

Inner

Mongolia Mengyuan Food Co., Ltd., or Mengyuan, located in Fengzhen, Inner

Mongolia, China, commenced operations in July 2007 and is engaged in raw

milk processing. Mengyuan was acquired by Zhangjiakou from its then

shareholders in November 2006.

|

|

·

|

Meitek

Technology (Qingdao) Co., Ltd., or Meitek, formerly known as Mei Tai

Technology (Qingdao) Co, Ltd., located in Qingdao, Shandong, China, was

established in November 2006 to produce certain nutritional supplements

and ingredients. Meitek began operations in October

2008.

|

|

·

|

Heilongjiang

Baoquanling Shengyuan Dairy Co., Ltd., or Baoquanling, located in

Junchuan, Heilongjiang, China, is engaged in raw milk processing and the

production of powdered formula. On September 9, 2009, we sold the two milk

processing factories of Baoquanling and three dairy farms of Heilongjiang

Baoquanling Shengyuan Dairy Cow Breeding Co., Ltd. (“Cow Breeding”), a

wholly owned subsidiary of Baoquanling, to Heilongjiang Wondersun Dairy

Co., Ltd. (“Wondersun”).

|

|

·

|

Harbin

Shengyuan Dairy Co., Ltd., or Harbin, located in Harbin, Heilongjiang,

China, is acquired in July 2008 and has been constructing its production

facilities since the acquisition.

|

|

·

|

Beijing

Shengyuan Huiliduo Food Technology Co., Ltd., or Huiliduo, located in

Beijing, China, was established in July 2008 to produce prepared baby

food. Huiliduo began operations in March

2009.

|

|

·

|

Beijing

Shengyuan Huimin Technology Service Co., Ltd., or Huimin, a variable

interest entity which was incorporated on July 10, 2008, plans to provide

diagnostic services for pregnant women through medical institutions.

Huimin was still in the pre-operation stage as of March 31,

2010.

|

|

·

|

Global

Food Trading (Shanghai) Co., Ltd., or Global Food, was acquired in June

2009 and is engaged in the sales and distribution of Helanruniu brand

products.

|

The

following chart reflects our organizational structure as of March 31,

2010.

4

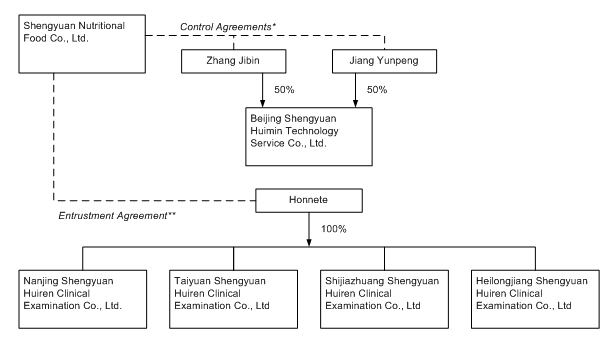

The

following chart shows the structure of our control agreements and the affiliated

entities consolidated into our group consolidated financial results as a result

of the control agreements:

|

|

*

|

Control

Agreements include:

|

|

|

(a)

|

Exclusive

Consulting and Service Agreement entered into by and between Nutritional

and Huimin;

|

|

|

(b)

|

Business

Operating Agreement entered into by and among Nutritional, Huimin, Zhang

Jibin (who is our Director of Loans) and Jiang Yunpeng (who is our

Director of Strategic

Acquisitions);

|

|

|

(c)

|

Call

Option Agreement entered into by and among Nutritional, Huimin, Zhang

Jibin and Jiang Yunpeng;

|

|

|

(d)

|

Pledge

Agreement entered into by and among Nutritional, Zhang Jibin and Jiang

Yunpeng; and

|

|

|

(e)

|

Entrustment

Agreement entered into by and among Nutritional, Zhang Jibin and Jiang

Yunpeng.

|

|

|

**

|

Entrustment

Agreement entered into by and among Nutritional, Zhang Jibin, Jiang

Yunpeng and Honnete.

|

For a

more detailed description of the control agreements, see “Item 13. Certain

Relationships and Related Transactions, and Director Independence.”

Our

Brands

We

primarily market our products under the Synutra, or Shengyuan, name which has

been associated with infant formula products in China for more than 10 years. In

addition to the Synutra, or Shengyuan name, our products are marketed in China

under brands that we have developed through our national sales and marketing

efforts.

Synutra

Family of Brands

The

Synutra family of brands includes several of China’s leading infant formula and

children’s nutrition brands, including Super and U-Smart. We have positioned the

Synutra family of brands as high quality brands, which provide unique,

clinically supported health and developmental benefits. The Synutra family of

brands features products that include DHA and ARA, which support brain, visual

and nervous system development of infants. Building upon the strength of our

brand equity, we are extending the Synutra family of brands into the fast

growing children’s nutrition market, such as prepared baby foods.

5

Complementary

Brands

In

addition to the Synutra family of brands, we market several other brands

targeted at various consumer segments and designed to meet the nutritional needs

of the broader consumer population in China. These brands include the Mingshan

(powdered formula), Helanruniu or Holsteina (adult formula), Meitek (nutritional

supplements), and Huiliduo (prepared baby foods).

Our

Products

Our

nutritional products are grouped by category of production process and usage as

well as internal resources allocation: (1) powdered formula, (2) baby foods, (3)

nutritional ingredients and supplements, and (4) other business. Sales of

powdered formula, baby foods, nutritional ingredients and supplements comprised

approximately 66.6%, 0.3%, 0.5% of our net sales for the fiscal year ended March

31, 2010. Sales from our other business comprised approximately 32.6% of our net

sales for the fiscal year ended March 31, 2010. A major portion of other

business for the fiscal year ended March 31, 2010 consist of sales of surplus

industrial milk powder.

Powdered

Formula Products

Powdered

formula segment covers the sale of powdered infant and adult formula products.

It includes the brands of Super, U-Smart, Mingshan which was launched in October

2008 and Helanruniu, or Holsteina, which was launched in December 2008. Infant

formula is our primary product line in the powdered formula segment, accounting

for 92.8%, 85.9% and 84.8% of our total net sales in the powdered formula

segment for the fiscal years ended March 31, 2010, 2009, and 2008,

respectively.

Each of

our Super, U-Smart and Mingshan product lines has multiple formulations designed

to meet nutritional requirements and help promote a baby or child’s healthy

growth at each developmental stage. We endeavor to bring our infant formula

products closer to the quality of breast milk. We have devoted resources to

extensively adjust our product portfolio, upgrade our product lines, and add new

products or line extensions to respond to market needs and target a wider group

of consumers. To meet consumer expectations, we also periodically upgrade our

product concepts, packaging, and pricing of our products.

We

supplement our powdered infant formula products with other nutritional products

for both adults and children. Our products are targeted at, and come in

formulations that are developed to address specific types of consumer profiles,

such as middle-aged and elderly consumers with cardiologic health issues,

diabetic conditions, and calcium deficiency. Furthermore, we have developed a

product specially designed for young adults to address their calcium and other

nutrient fortification needs. Our products for women and young adults have also

undergone product extensions and upgrades to further clarify the health and

nutritional message and product image we intend to convey.

We

continue to improve our rice cereal products as supplemental and functional

foods to our powdered infant and children formula products. These improvements

included upgrades to packaging as well as product extensions with new

functionalities, new tastes and flavors, and new protein sources such as fish

and chicken.

Baby

Food Products

Baby food

segment covers the sale of prepared baby food for babies and children. It

includes the brand of Huiliduo which was launched in the quarter ended March 31,

2009. These products are designed to be part of a child’s healthy diet with

enhanced nutrition value at different stages of development.

Nutritional

Ingredients and Supplements

Nutritional

ingredients and supplements segment covers the production and sale of

nutritional ingredients and supplements such as chondroitin sulfate,

microencapsulated DHA and ARA. In the past, we had sourced and exported

chondroitin sulfate, a nutrient for joint health, to U.S. industrial customers

through our exclusive third-party agent. With the completion of our Meitek

facilities in October 2008, we are now able to produce chondroitin sulfate

ourselves. In addition, our Meitek facilities can produce microencapsulated DHA

and ARA powders and other nutritional ingredients and supplements for our own

use and for external industrial customers.

6

Production

Powdered

Formula Processing

In the

fiscal year ended March 31, 2010, all of our milk powder used for our Super,

U-Smart and Holsteina brands is imported from Fonterra Co-operative Group

(“Fonterra”) in New Zealand.

Currently,

milk powder produced at our own facilities is primarily used for commercial

resale for our other business. Only the Mingshan series of products continues to

use locally produced raw milk. Raw milk is collected from dairy farmers. Local

dairy farmers bring their dairy cattle to collection stations owned by us where

raw milk is automatically received using fully enclosed, stainless-steel vacuum

milking machines. These collection stations collect and transport the raw milk

to our production facilities which are located within 100 kilometers of these

milk collection stations, except for our Qingdao facility. Although raw milk can

remain fresh for up to 72 hours, we normally process it within 24

hours. Once received, the raw milk is processed with refrigeration

equipment that cools the raw milk to approximately four degrees Celsius. The raw

milk is then stored in air-tight tanks in preparation for advanced processes,

which include milk fat separation, sterilization and spray-drying. At our

Mingshan facilities, sterilized raw milk is mixed with whey protein powder and

other nutrients to the specifications of product formula through a wet mixing

method. The resulting mixture is then spray dried into milk powder and

transported to our Qingdao facility for final packaging.

At the

Qingdao facility, dried milk powder is mixed in large automated mechanical

mixers with whey protein powder and other additives in a method known as

dry-blending. Our dry-blending equipment can automatically adjust the level of

ingredients to achieve the complex formulations required by our premium

products. The resulting milk powder is then checked to ensure proper granule

size before packaging and distribution.

Packaging

The bulk

of our powdered formula and other nutritional products come in three types of

retail packaging: tin canisters, standup/display pouches, or sealed packages in

a box. All packaging labels carry product information, nutritional profile, user

instructions, product tracing data and shelf life date, product certification

status, quality control and assurance remarks, manufacturer contact information,

as well as customer service information that comply with PRC labeling

requirements. Selected products are also retail-packaged in single-use sizes.

Before any product leaves our packaging facility to distributors, we generally

engage in an extensive testing and inspection of the final product.

Production

and Packaging Facilities

Our

processing and packaging facilities, which are all owned by us, are located in

various locations in China, including Beijing, Qingdao, Luobei, Zhangjiakou,

Fengzhen and Zhenglanqi. These facilities encompass approximately 77,990 square

meters of office, plant, and warehouse space. Our distribution center located in

Qingdao includes over 14,116 square meters of owned office space. All of our

production facilities are built based on the GMP standard, with equipment

imported from Europe and all of our facilities that have commenced operation

have ISO9000 and HACCP series qualifications with some also being ISO14000

certified.

We

currently own and operate four processing facilities and one packaging facility

for our powdered formula production. As of March 31, 2010, we had raw milk

processing capacity of 32,600 tons per year, packaging capacity of 82,000 tons

per year and dry-blending processing capacity of 73,000 tons per

year.

Our

Qingdao facility serves as our dry-blending and packaging plant. Various

ingredients, such as milk powder, whey protein powder and nutritional additives

arrive at our Qingdao facility from our production facilities and our suppliers,

and are mixed using the dry-blending method. Qingdao facility repackages the

mixed ingredients into retail-size tin canisters or stand up/display pouches or

sealed packages in boxes. This packaging facility also provides inventory

control and logistics management, product quality monitoring and product

development assistance.

7

Our

production facility for prepared baby foods is located in Beijing and

Zhenglanqi. As of March 31, 2010, the Beijing facility had a processing capacity

of 4.8 million jars (approximately 540 tons) per year, and the Zhenglanqi

facility is planned to have a processing capacity of 18,000 tons per year upon

completion.

Our

production facility for nutritional ingredients and supplements is located in

Qingdao. As of March 31, 2010, this facility had a processing capacity of 700

tons per year for chondroitin sulfate, 1,000 tons per year for collagen protein,

and 700 tons for microencapsulated DHA and ARA powders and other nutritional

ingredients.

For

information with respect to the installed capacity, location and function of our

processing and packaging facilities, see “Item 2.

Properties”.

Raw

Materials and Suppliers

Raw

Materials

Our

business depends on maintaining a regular and adequate supply of high-quality

raw materials. In the aftermath of the melamine contamination incident, we

decided to use imported milk powder for the production of our higher end

powdered formula products. We currently source approximately 90% of milk powder

used in our production from New Zealand. We also pay market prices or premium

prices in certain regions in China for our raw milk. Our milk suppliers are

primarily dairy farmers located throughout Heilongjiang and Hebei provinces and

in Inner Mongolia.

Whey

protein powder is the other key ingredient used in the production of our

powdered infant formula products and our other dairy-based products. Like all

powdered milk producers, we use whey protein powder as the active ingredient to

help reconstituted dairy-based formula to mimic the consistency of breast milk,

which can constitute approximately 55% of the final powdered infant formula

product by weight. Whey protein powder is a byproduct of cheese-making

processes, and is difficult and costly to produce as a stand-alone product.

Since China is not a large consumer or producer of cheese and cheese products,

we and other domestic producers typically obtain whey protein powder in volume

from overseas sources, such as France.

Based on

our experience, prices of milk powder and whey protein powder can fluctuate over

relatively short periods of time depending on market conditions. Our sourcing

team monitors price movements and makes major purchases at times when prices are

attractive, subject to projected customer order flow and other

factors.

Some of

our powdered milk products, including our powdered infant formulas, also include

additives such as DHA and ARA fatty acids and other nutritional additives. DHA

and ARA fatty acids are long-chain poly-unsaturated fatty acids found in breast

milk that are believed to aid in the development of an infant’s brain, eyes and

nervous system. Studies have suggested that DHA and ARA fortification can

replicate some of the nutritional benefits of breast milk in infant formulas.

Currently we are producing microencapsulated DHA and ARA powders at our Meitek

facility which began operations in October 2008 for both internal use and

external sales.

We use

vegetable oils in our dry-spraying powder infant formula production processes as

a binder for the dry ingredients, helping diminish the occurrence of “lumpiness”

or uneven texture when reconstituting powdered infant formula.

We

purchase animal cartilage from third-party suppliers, including overseas

slaughtering houses, for the production of chondroitin sulfate, a substance that

provides nutrients for joints, tendon, ligaments and bones, in our Meitek

facility.

Suppliers

and Supplier Arrangements

Prior to

September 2008, we were able to meet our milk powder production needs by

purchasing raw milk on the open market in established dairy regions in northern

and northeastern China. We generally negotiate the purchase price of raw milk

with many dairy farmers and cooperatives.

8

In the

fiscal year ended March 31, 2010, we have been purchasing approximately 90% of

our milk powder from Fonterra in New Zealand. We generally negotiate the prices

for each separate purchase on spot and do not sign long term contracts with our

suppliers.

Prior to

June 2007, we obtained our supply of whey protein powder from Honnete, a large

volume importer of processed dairy products in China. Honnete, a company

controlled by Liang Zhang, our chairman and chief executive officer, is a major

supplier of China’s whey protein powder. Beginning in June 2007, we began

sourcing our whey protein powder directly from Eurosérum S.A.S (“Eurosérum”),

Honnete’s supplier in France.

Sales

and Distribution

Sales

We

generally sell our products directly to distributors and in limited

circumstances directly to retailers. Our recent marketing efforts for our

nutritional products have focused on extending retail coverage in terms of

geography and market sectors. Our sales and marketing approach combines

advertising, brand-building and store-level promotions. Our sales team of more

than 300 employees use our customer relations management, or CRM, database in

order to acquire, process, and manage targeted customer

information.

We have

built a sales network that currently covers 30 provinces and provincial-level

municipalities. Our sales group is divided into multiple sub-sales regions. Each

sub-sales region covers between eight to 20 urban sales areas which acts as an

independent operating unit, while each urban sales area covers three to 20

county sales areas. As of March 31, 2010, we had a sales and marketing force of

more than 3,300 employees, complemented by more than 18,000 commissioned field

nutrition consultants or retail site promoters employed by our distributors and

sub-distributors to promote and sell our products.

Although

we sell primarily to our distributors and a few resellers, our sales teams work

directly with each retail outlet to manage the sales process and to collect

customer and purchasing related data. We use multiple criteria to select our

distributors, including reviewing each potential distributor’s financial

condition. We intend to expand our sales organization into additional cities and

municipalities that we do not currently serve. City managers are rotated

periodically among various cities. We have recently set up a sales budget

management team to manage our sales expenses and to supervise the execution of

our budgeting plan. This team reports directly to the president of marketing and

sales.

We

compensate our sales personnel through a combination of fixed salaries and

bonuses based on sales growth. Our targeted sales incentive programs compensate

our sales personnel on a product-specific level, thereby enabling us to

incentivize our sales personnel to focus their sales and promotion efforts on

certain product lines, such as our premium product lines or larger product

packages.

Distribution

We

primarily work directly with over 540 independent distributors, who in turn work

with over 1,000 independent sub-distributors, and more than 71,000 retail

outlets. Our packaging subsidiary, Shengyuan Nutrition, also serves as our

national distribution center for our distributors in China. From the beginning

of 2007, prior to the melamine contamination incident, we only offered credit

for our products to a few selected distributors. In light of the financial

difficulties experienced by our distributors as a result of the melamine

contamination incident, we extended credit to more distributors and increased

the amount of credit we granted to distributors whom we had previously extended

credit to. We ask our distributors to provide monthly inventory reports which

allows us to monitor their inventory levels. Our sales personnel also regularly

inspect distributors’ inventories to identify and control any potential

inventory buildup by our distributors. We employ trucking companies locally and

nationally to distribute retail packaged products to various regional and

provincial distributors.

Distributors

normally have exclusive distribution rights in their respective regions and

cities to distribute our products, and are also responsible for developing the

sub-distributors in their own region and cities. We typically enter into a

contract with each of our distributors that establishes the range of sales

obligations and their respective pricing ranges. However, our obligation to sell

and the distributor’s obligation to purchase arise only at the time

a

9

purchase

order is accepted. We seek to carefully manage our distributors through an

evaluation system that monitors and grades each distributor with respect to

performance criteria such as monthly sales and investment in promotional

activities. We seek to incentivize well-performing distributors by providing

discounts, larger sales territory and other incentives. While we do not directly

manage our sub-distributors, we do track sub-distributor performance through

coordinated efforts between our own sales personnel in the field and

distributors. Our distributors generally have the right to return products due

to package damage.

We

currently distribute our nutritional products across China. Our logistics center

in our Qingdao facilities occupies an area of 14,000 square meters. This

logistics center can currently dispatch 6,900 tons of our products for shipment

to our distributors per month. Our Qingdao facility also has the capability to

respond to urgent requests for product shipments within an average of five

days.

We

currently work with approximately 22 transportation companies that transport our

goods directly from our Qingdao facilities to distributors in a timely and

efficient manner.

We have

an enterprise resource planning system, or ERP system, which is a financial

information system with an inventory module that manages and records inventory

transactions.

Seasonality

Our

business experiences some seasonal fluctuations. Summer time is typically a slow

time for the infant formula market because the population generally consumes

less food during the summer. Furthermore, Chinese parents tend to choose the

summer time to switch from milk feeding to more concrete food for their babies.

As a result, we generally experience weaker sales in our first and second fiscal

quarters.

Marketing,

Advertising and Promotion

Advertising

We

advertise through various media, including television, print media and the

Internet. Additionally, we conduct promotional activities with supermarket

chains and entertainment companies in order to reach our target

market.

We

started nationwide television advertising coverage in September 2006. In certain

cases, we supplement our nationwide television coverage with local television

coverage. We also pursue advertising over the Internet. Our advertising spending

was $16.7 million, $72.8 million and $30.3 million for the fiscal years ended

March 31, 2010, 2009 and 2008, respectively. Our advertising spending has

enabled us to secure prime-time placements with China Central Television and

other premium regional or satellite television stations. After an aggressive

advertising and promotional campaign from October 2008 to March 2009 to regain

market share in the aftermath of the melamine contamination incident, we slowed

down our advertising and promotional expenses in the fiscal year ended March 31,

2010 to better utilize our resources. We plan to resume more active advertising

activities in the near future and we expect our advertising expenditure will

increase in the fiscal year ending March 31, 2011.

Marketing

and Promotion

As part

of our sales and marketing approach, our sales force works with more than 14,000

healthcare facilities across China to provide maternity, infant nutrition and

health education programs. We have also established a national customer service

call center providing live assistance and a toll-free line to provide consumers

with prenatal, nursing, baby care education, product information, and address

complaints and dispute resolution.

We

provide displays, posters and other promotional print to retail outlets and

sales consultants employed by our distributors at each point of sale. We also

pay entry fees to various retail outlets to place our products within such

outlets. We collect customer information through surveys voluntarily provided by

each customer via the point of sale or via mailed forms provided to our

customers in each product package. We also have promotional activities with

supermarket chains and entertainment companies in order to reach our target

market.

10

Quality

Control

We place

primary importance on quality. We have established quality control and food

safety management systems for the purchase of raw materials, raw milk checks,

raw milk processing, packaging, storage and transportation. We use commercial

strength 25KG poly kraft bags for packaging before shipping the formula products

to our retail packaging and distribution facilities. Additionally, we maintain

cold storage areas at each of our three raw milk processing facilities to store

fluid milk. All of our processing facilities are equipped with in-house

laboratories for quality assurance and quality control purposes. Our laboratory

in Qingdao has been qualified as a National Standard Laboratory by the China

National Accreditation Service for Conformity Assessment.

In order

to ensure the quality and safety of our ingredients and products, we have also

installed testing equipment and have implemented control procedures at each

stage of production, including at the initial raw material purchase stage. There

are over 1,100 quality control points throughout the entire production process,

including 24 quality control points at the milk collection stations. We employ

strict internal procedures and monitoring by highly trained employees during

production, transportation and storage. Additionally, we have been increasing

our investment in quality control equipment and training. All policies relating

to quality control are subject to PRC laws and regulations.

Highlights

of our quality control procedures are summarized below, organized by the main

stages of production:

Imported

Milk Powder and Whey Protein:

|

·

|

Procurement

staff inspects the Certificate of Analysis to ensure the products are

manufactured and tested according to production countries’ national

standard;

|

|

·

|

Entry-Exit

Inspection and Quarantine of the People’s Republic of China performs

quality test to ensure the products are up to national standard and issue

a Sanitary Certificate; and

|

|

·

|

Central

Lab staff of the Company performs detailed test on quality and nutritional

ingredients of the products before using them in

production.

|

Purchase

of Raw Milk:

|

·

|

Raw

milk procurement manager conducts pre-purchase assessment of dairy farmers

and requests issuance of clean bill of health for dairy

cows;

|

|

·

|

Procurement

staff conducts on-site inspection in compliance with our quality standards

and rejects nonconforming supply;

|

|

·

|

Inspection

of specimen—sampling in the process of raw milk collection for inspection

at our facilities pursuant to national standards;

and

|

|

·

|

Sterilization

of equipment for raw milk

collection.

|

Milk

Powder Production:

|

·

|

Compliance

with production process control procedure, HACCP Plan implemented at all

plants;

|

|

·

|

All

raw materials are subject to prior

inspection;

|

|

·

|

Detailed

process designed for all parts of the production process including

pretreatment, vaporization, drying, powder receiving, cooling and

packaging;

|

|

·

|

Maintain

hygiene standards for staff, equipment, environment and any other object;

and

|

|

·

|

Inspection

conducted throughout the production

process.

|

11

Packaging,

Storage and Transport:

|

·

|

Establishment

and practice of total process management with respect to product

identification and traceability;

|

|

·

|

Inspection

before warehousing of products;

|

|

·

|

Maintain

hygiene standards in the course of transport and storage;

and

|

|

·

|

Products

must be positioned according to their category during transport and

storage.

|

In the

fiscal year ended March 31, 2010, we have been importing approximately 90% of

our milk powder from New Zealand. There are three steps of quality control for

imported milk powder: (1) the exporters conduct their own quality control before

they ship the milk powder; (2) all of our milk powder imports are inspected by

China’s import-export inspection and quarantine authorities at landing, pursuant

to a national standard of inspection, and (3) our Qingdao laboratory tests each

batch of imported milk powder using strict standards for quality

assurance.

Research

and Development

Our

research and development activities focus on new product formulation, new

ingredient development, creation of new methods to incorporate certain nutrients

in our products, and improvement in product tastes and ingredient shelf

stabilities. We engage in regular product refinement and new product development

for our dairy-based formula products, as well as other forms of foods and

nutritional supplements.

We

utilize our research and development facilities to engage in the development of

bringing our infant formula products closer to the quality of breast milk and

promote our brand image. We also engage third-party research institutions to

research and develop such trial products for us.

We seek

to leverage our research and development resources in order to extend our new

product pipeline. We believe we can accomplish this goal with new formulations

and product concepts in dairy-based formula products as well as other

nutritional food products and supplements.

In

addition to new formulations and products, we have also developed a variety of

delivery systems such as orally delivered supplements in a pill format and

single use packages which can provide the formula to the end-user in convenient

single packets instead of bulky large canisters.

We also

plan to open a new research and development facility in Beijing, which we plan

to be operational by late calendar year 2010.

During

each of the fiscal years ended March 31, 2010, 2009 and 2008, we spent

approximately 0.2% of net sales per year on research and

development.

Competition

The

infant formula industry in China is highly competitive. We generally compete

with both multinational and domestic infant formula producers. Competitive

factors include brand recognition, distribution network, quality, advertising,

formulation, packaging and price. Many of our competitors have significant

market share in the markets we compete in. Our principal competitors can be

classified generally into the following two groups:

Multinational

Producers

|

·

|

Abbot

Laboratories’ Ross Products Division, a U.S. producer and distributor of

infant formulas marketed under the brand names of Similac and Enfalac

family of formulas;

|

|

·

|

Mead

Johnson Nutrition Co., or Mead Johnson, formerly a Bristol-Myers Squibb

Company Division, a U.S. producer and distributor of the Enfamil family of

formulas;

|

12

|

·

|

Groupe

Danone SA’s Numico division, or Numico, a Dutch producer of baby foods,

which sells and markets infant formula products in China under the Dumex

brand;

|

|

·

|

Nestlé

Suisse SA, or Nestlé, a Swiss producer and distributor of starter and

follow-up formulas, milk, cereals, oral supplements and performance foods

marketed under Nestlé brands such as Carnation;

and

|

|

·

|

Wyeth,

a U.S. producer and distributor of infant formula sold under private label

brands.

|

Domestic

Producers

|

·

|

Inner

Mongolia Yili Industrial Group Co., Ltd., or Yili, a PRC producer and

distributor of liquid and powdered milk under their Yili

brand;

|

|

·

|

Beingmate

Group Company Limited, or Beingmate, a PRC producer and distributor of

infant formula products under their Beingmate

brand;

|

|

·

|

Guangdong

Yashili Group Co., Ltd., or Yashili, a PRC consumer brand marketer which

sells a line of infant formula products under their Yashili brand;

and

|

|

·

|

American

Dairy, Inc., a PRC producer and distributor of milk formula products under

their Feihe brand.

|

According

to data collected by the PRC National Commercial Information Center, or CIC, an

entity affiliated with the PRC General Chamber of Commerce responsible for

collecting retail sales data, the top ten brands accounted for 83.0% of total

infant formulas sold in China in calendar year 2009.

Intellectual

Property

All of

our product formulations have been developed in-house and are proprietary. We

have not registered or applied for protections in China for most of our

intellectual property or proprietary technologies relating to the formulations

of our powdered infant formula. See Item 1A. Risk factors—Risks Related to Our

Business—Failure to adequately protect our intellectual property rights may

undermine our competitive position, and litigation to protect our intellectual

property rights may be costly. Although we believe that, as of today,

patents and copyrights have not been essential to maintaining our competitive

market position, we intend to assess in the future whether to seek patent and

copyright protections for those aspects of our business that provide significant

competitive advantages.

As of

March 31, 2010, we had 175 registered trademarks in China, one registered

trademark in Hong Kong, one registered trademark in the United States, and 3

registered trademarks in France. Additionally, we had 38 trademark applications

pending approval in China.

We rely

on trade secret protection and confidentiality agreements to protect our

proprietary information and know-how. Our management and each of our research

and development personnel have entered into annual employment contracts, each of

which includes a confidentiality clause and a clause acknowledging that all

inventions, designs, trade secrets, works of authorship, developments and other

processes generated by them on our behalf are our property, and assigning to us

any ownership rights that they may claim in those works. Despite our

precautions, it may be possible for third parties to obtain and use, without our

consent, intellectual property that we own or are licensed to use. Unauthorized

use of our intellectual property by third parties, and the expenses incurred in

protecting our intellectual property rights, may adversely affect our business.

See Item 1A. Risk factors—Risks Related to Our Business—Failure to

adequately protect our intellectual property rights may undermine our

competitive position, and litigation to protect our intellectual property rights

may be costly.

Environmental

Matters

Our

manufacturing facilities are subject to various pollution control regulations in

China with respect to noise, water and air pollution and the disposal of waste

and hazardous materials. We are also subject to periodic inspections by local

environmental protection authorities in China. We are not currently subject to

any pending actions alleging any violations of applicable PRC environmental

laws.

13

Our

Employees

As of

March 31, 2010, we employed approximately 5,800 employees in all of our

facilities, with approximately 140 head office management staff and research and

development employees, approximately 2,300 production employees, and

approximately 3,300 sales and marketing employees. Our employees are not

represented by a labor organization or covered by a collective bargaining

agreement. We have not experienced any work stoppages.

We offer

our employees both a base salary and a profit sharing program composed of

performance bonuses and rewards for exceptional performance. As required by PRC

regulations, we participate in various employee benefit plans that are organized

by municipal and provincial governments, including pension, work-related injury

benefits, maternity insurance, medical and unemployment benefit plans. We are

required under PRC law to make contributions to the employee benefit plans at

specified percentages of the salaries, bonuses and certain allowances of our

employees, up to a maximum amount specified by the local government from time to

time. Members of the retirement plan are entitled to a pension equal to a fixed

proportion of the member’s salary amount at the member’s retirement

date.

Regulation

The food

industry, of which nutritional and infant formula products form a part, and

medical institutions, are subject to extensive regulations in China. This

section summarizes the most significant PRC regulations governing our business

in China.

Food

Hygiene and Safety Laws and Regulations

As a

producer of nutritional products, and particularly dairy-based infant formula

products, in China, we are subject to a number of PRC laws and regulations

governing the manufacturing (including composition of ingredients), labeling,

packaging, safety and hygiene of food products:

|

·

|

the

PRC Product Quality Law;

|

|

·

|

the

PRC Food Safety Law;

|

|

·

|

the

Implementation Rules on the PRC Food Safety

Law;

|

|

·

|

the

Dairy Product Industrial Policies (2009

Version);

|

|

·

|

the

Regulation on the Supervision and Administration of the Quality and Safety

of Dairy Products;

|

|

·

|

The

Outlines of the Rectification and Revival of the Dairy

Industry;

|

|

·

|

the

Measures of the Administration on the New

Food-Additives;

|

|

·

|

the

Measures of the Filing of the Enterprise Standard of the Food

Safety;

|

|

·

|

the

Implementation Rules on the Administration and Supervision of Quality and

Safety in Food Producing and Processing

Enterprises;

|

|

·

|

the

Regulation on the Administration of Production Licenses for Industrial

Products;

|

|

·

|

the

General Standards for the Labeling of Prepackaged

Foods;

|

|

·

|

the

Implementation Measures on Examination of Dairy Product Production

Permits;

|

|

·

|

the

Standardization Law;

|

|

·

|

the

Raw Milk Collection Standard;

|

14

|

·

|

the

Whole Milk Powder, Skimmed Milk Powder, Sweetened Whole Milk Powder and

Flavored Milk Powder Standards; and

|

|

·

|

the

General Technical Requirements for Infant Formula Powder and Supplementary

Cereal for Infants and Children.

|

These

laws and regulations set out safety and hygiene standards and requirements for

various aspects of food production, such as the use of additives, production,

packaging, handling, labeling and storage, as well as facilities and equipment.

Failure to comply with these laws and regulations may result in confiscation of

our products and proceeds from the sales of non-compliant products, destruction

of our products and inventory, fines, suspension of production and operation,

product recalls, revocation of licenses, and, in extreme cases, criminal

liability.

As a

result of the melamine contamination incident, the PRC government authorities

have conducted extensive dairy industry inspections. In addition to the initial

22 companies implicated in the incident, these subsequent government inspections

have identified other companies with unacceptable contamination in their

products. On October 7, 2008, the State General Administration of Quality

Supervision, Inspection and Quarantine (“AQSIQ”) issued a national standard on

the detection of melamine in raw milk and dairy based products. On October 9,

2008, the State Council promulgated with immediate effect a Regulation for the

Quality and Safety Supervision of Dairy Based Products, which, among other

things, imposes more stringent requirements for inspection, production,

packaging, labeling and product recall on dairy product producers. This

regulation also established a “Black-List” system to ensure that illegal

business operators in the dairy production chain are timely disclosed and

severely punished.

Environmental

Regulations

We are

subject to various governmental regulations related to environmental protection.

The major environmental regulations applicable to us include:

|

·

|

the

Environmental Protection Law of the

PRC;

|

|

·

|

the

Law of PRC on the Prevention and Control of Water

Pollution;

|

|

·

|

Implementation

Rules of the Law of PRC on the Prevention and Control of Water

Pollution;

|

|

·

|

the

Law of PRC on the Prevention and Control of Air

Pollution;

|

|

·

|

Implementation

Rules of the Law of PRC on the Prevention and Control of Air

Pollution;

|

|

·

|

the

Law of PRC on the Prevention and Control of Solid Waste Pollution;

and

|

|

·

|

the

Law of PRC on the Prevention and Control of Noise

Pollution.

|

We are

periodically inspected by local environmental protection authorities. Our

operating subsidiaries have received certifications from the relevant PRC

government agencies in charge of environmental protection indicating that their

business operations are in compliance with the relevant PRC environmental laws

and regulations.

Dairy

Industry Access Conditions and Policies

In June

2009, the PRC National Development and Reform Commission, or the NDRC, and the

Ministry of Industry and Information Technology, or the MIIT, jointly

promulgated and issued Dairy Industry Policies (2009 Version), or the Policies.

The Policies set forth the conditions an entity must satisfy in order to engage,

or continue to engage, in the dairy products processing business, including

technique and equipment, product quality, energy and water consumption,

sanitation and environmental protection, as well as production safety. Any new

or continuing dairy products processing projects or enterprises will be required

to meet all the conditions and requirements set forth in the Policies. For

projects or enterprises that already commenced operations before the

promulgation of the Policies, improvements or rectification actions may need to

be taken in order to have such projects or enterprises meet the conditions

before the end of 2010.

15

The

Policies also set forth some requirements relating to the location, processing

capacity and raw milk source for any new or continuing dairy products processing

project or enterprise. Any new or continuing dairy products processing projects

or enterprises that fail to meet the requirements will not be able to procure

land, license, permits, loan facility and electricity necessary for the

processing of dairy products, and those projects or enterprises already in

operation before the promulgation of the Policies will be deregistered and

ordered to shut down if they fail to meet the conditions before the end of 2010.

We believe that all of our existing entities and facilities meet the

requirements under the Access Conditions. See Item 1A. Risk Factors—Risks

Associated with Doing Business in China—Changes in the regulatory

environment for dairy and infant nutrition products in China could negatively

impact our business.

Medical

Institutions

On

February 26, 1994, the State Council promulgated the Regulations of

Administration on Medical Institutions which established the regulations for

establishing, managing and supervision of medical institutions. In particular,

the regulations required a medical institution to be approved by and register

with the applicable administrative department of public health prior to

establishment. On December 14, 2009, the Ministry of Public Health promulgated

the Standards of Medical Inspection Laboratory which set forth the standards for

establishing and managing medical inspection laboratories.

Financial

Information About Segments and Geographic Areas

We have

three reportable segments, which are powdered formula, baby food and nutritional

ingredients and supplements. In addition, in the fiscal year ended March 31,

2010, sales from our other business which includes non-core operations accounted

for 32.6% of our net sales. Please refer to Note 18 to the Consolidated

Financial Statements for further discussion about segments and geographic

areas.

Available

Information

Our

Internet website address is www.synutra.com. We make

available at this address, free of charge, our Annual Reports on Form 10-K,

Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments

to those reports as soon as reasonably practicable after such material is

electronically filed with or furnished to the United States Securities and

Exchange Commission, or SEC. Information available on our website is not

incorporated by reference in and is not deemed a part of this Form 10-K. The

public may read and copy any materials we file with the SEC at the SEC’s Public

Reference Room at 100 F. Street, N.E., Washington, DC, 20549. The public may

obtain information on the operation of the Public Reference Room by calling the

SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports,

proxy and information statements, and other information regarding issues that

file electronically with the SEC at www.sec.gov.

ITEM

1A. RISK FACTORS

Because

of the following factors, as well as other factors affecting our financial

condition and operating results, past financial performance should not be

considered to be a reliable indicator of future performance, and investors

should not use historical trends to anticipate results or trends in future

periods.

You

should carefully consider the following risks and other information in this Form

10-K before making an investment decision with respect to our common stock. The

following risks and uncertainties could materially and adversely affect our

business, results of operations and financial condition. The risks described

below are not the only ones we face. Additional risks that we are not presently

aware of or that we currently believe are immaterial may also impair our

business operations.

16

Risks

Related to Our Business

We

are highly dependent upon consumers’ perception of the safety and quality of our

products. Any ill effects, product liability claims, recalls, adverse publicity

or negative public perception regarding particular ingredients or products or

our industry in general, could harm our reputation and damage our brand, and

adversely affect our results of operations.

We sell

products for human consumption, which involves risks such as product

contamination, spoilage and tampering. We may be subject to liability if the

consumption of any of our products causes injury, illness or death. Adverse

publicity or negative public perception regarding particular ingredients, our

products, our actions relating to our products, or our industry in general could

result in a substantial drop in demand for our products. This negative public

perception may include publicity regarding the safety or quality of particular

ingredients or products in general, of other companies or of our products or

ingredients specifically. Negative public perception may also arise from

regulatory investigations or product liability claims, regardless of whether

those investigations involve us or whether any product liability claim is

successful against us.

On

September 16, 2008, China’s Administration of Quality Supervision, Inspection

and Quarantine, or China AQSIQ, announced its finding that the formula products

of 22 Chinese formula producers, including certain lots of our U-Smart products,

were contaminated by melamine, a substance not approved for use in food and

linked to the illness and deaths of infants and children in China. To date,

there have been six reported deaths and approximately 300,000 children have

suffered kidney-related illnesses due to the contaminated infant formula of one

of our competitors. This contamination incident has resulted in significant

negative publicity for the entire domestic dairy and formula industries in China

and demand for domestically-produced dairy and formula products, including our

products, has declined significantly since September 2008 until late 2009. We

recalled our affected U-Smart products as well as all other products produced at

the same facilities in the Hebei and Inner Mongolia regions of China, where we

believe the contaminated milk supplies originated. We also suspended production

at our facilities in Qingdao, Hebei and Inner Mongolia for two weeks pending

government and internal investigations. The total cost of this action was $100.6

million which was recognized as a charge to cost of sales, selling and

distribution expenses and general and administrative expenses in our

consolidated statement of income for the two fiscal years ended March 31,

2010.

Although

we have not confirmed any cases of kidney-related or other illnesses caused by

our products, we cannot assure you that such cases will not surface in the

future. The Chinese government has provided medical screening, treatment, and

care for consumers affected by melamine contamination in infant formula

products. We have contributed a net amount of $2.3 million to a compensation

fund set up by China Dairy Industry Association to settle existing and potential

claims arising in China from families of infants affected by melamine

contamination. We cannot assure you that the Chinese government will not seek

further reimbursement from dairy and formula product manufacturers, including

us.

We

believe the melamine contamination incident negatively impacted our brand and

reputation in China. It also affected investor confidence in us as reflected by

the significant decrease in our stock price after September 16, 2008. We cannot

predict the long-term effect this recall and the negative publicity associated

with the melamine contamination incident will have on our reputation among our

customers, consumers and investors. Our results of operations and financial

position, may, in the future, continue to be severely impacted if our customers

and consumers cease to purchase our products as a result of lingering concerns

from the melamine contamination incident.

In the

past, there have also been occurrences of counterfeiting and imitation of

products in China that have been widely publicized. We cannot guarantee that

contamination or counterfeiting or imitation of our or similar products will not

occur in the future or that we will be able to detect it and deal with it

effectively. Any occurrence of contamination or counterfeiting or imitation

could negatively impact our corporate and brand image or consumers’ perception

of our products or similar nutritional products generally, particularly if the

counterfeit or imitation products cause injury or death to consumers. For

example, in April 2004, sales of counterfeit and substandard infant formula in

Anhui, China caused the deaths of 13 infants as well as harming many others.