Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DORCHESTER MINERALS, L.P. | d8k.htm |

Dorchester Minerals, LP

1

Dorchester Minerals, LP

Annual Meeting

May 12, 2010

Exhibit 99.1 |

Dorchester Minerals, LP

2

Forward-Looking Statements

•

Portions of this document may constitute "forward-looking

statements" as defined by federal law. Such statements are

subject to certain risks, uncertainties and assumptions.

Should one or more of these risks or uncertainties

materialize, or should underlying assumptions prove

incorrect, actual results may vary materially from those

anticipated, estimated or projected. Examples of such

uncertainties and risk factors include, but are not limited to,

changes in the price or demand for oil and natural gas,

changes in the operations on or development of the

Partnership’s properties, changes in economic and industry

conditions and changes in regulatory requirements (including

changes in environmental requirements) and the

Partnership’s consolidated financial position, business

strategy and other plans and objectives for future operations.

These and other factors are set forth in the Partnership's

filings with the Securities and Exchange Commission.

|

Dorchester Minerals, LP

3

•

Overview of 2009

–

Distributions and Financial Results

–

Production and Reserves

–

Peer Group Analysis

–

Royalty Cash Receipts

•

Maecenas Minerals Acquisition

•

Property Highlights

–

Portfolio Overview

–

Royalty Properties

–

Net Profits Interests

•

Developing Plays

Presentation Outline |

Dorchester Minerals, LP

4

Overview of 2009 Results |

Dorchester Minerals, LP

5

2009 Distributions

Royalty

Revenue

$37.3 MM

Total Revenue

$50.2 MM

Other

Revenue

$0.9 MM

NPI

Revenue

$12.0 MM

LP

Distribution

$43.3 MM

GP

Distribution

$1.4 MM

Total

Expenses

$5.5 MM

•

Cash Distributions Paid in Calendar 2009

–

Reflects Q4 2008 to Q3 2009 activity |

Dorchester Minerals, LP

6

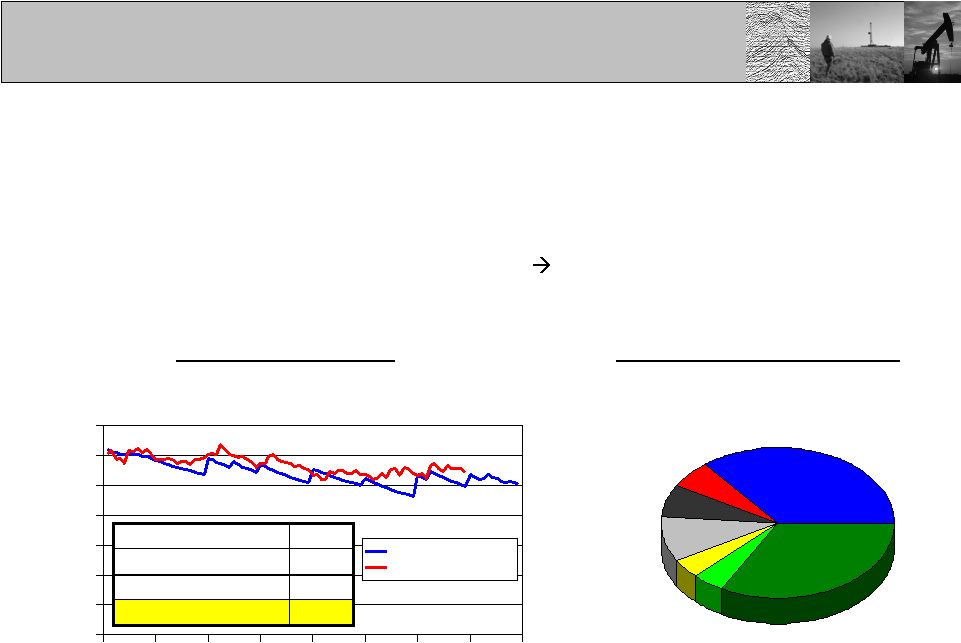

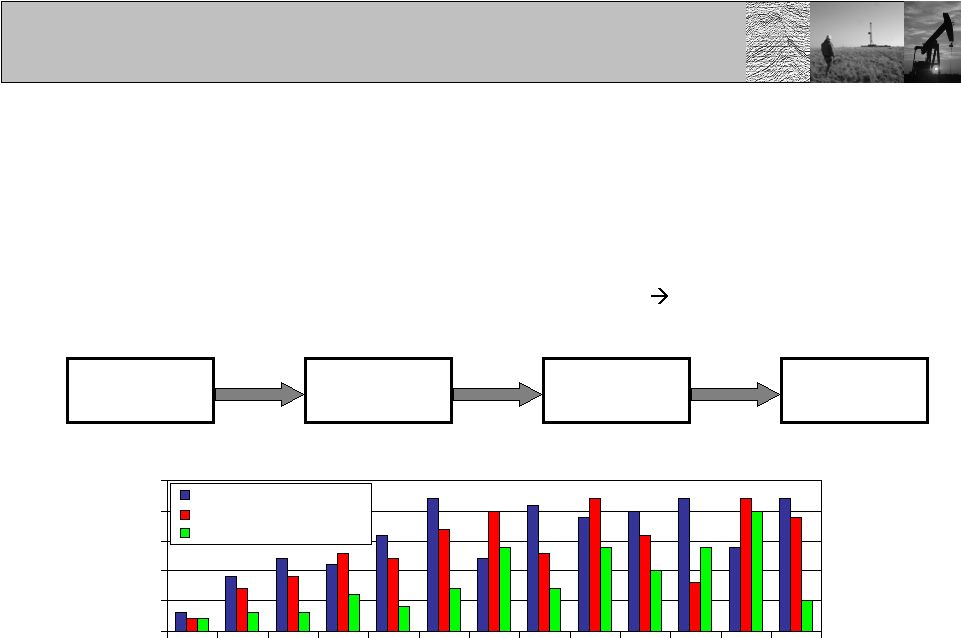

2009 Financial Results

$49.2

$56.8

$79.8

$74.9

$65.4

Operating Revenue ($MM)

Gas Price ($/Mcf)

Distributions ($/unit)

•

Revenue –

Price –

Distributions

–

Royalty properties contributed 77% to total operating revenues

–

Gross Revenue

63% gas sales, 36% oil sales, 1% other revenue

–

NPI and lease bonuses have become a smaller portion of revenues

$89.9

$43.6

Note: Gross Revenue does not reflect production costs or other expenses

incorporated in calculating the net profits interest payments to LP distributions

$0

$20

$40

$60

$80

$100

2003

2004

2005

2006

2007

2008

2009

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

Royalties

NPI

Lease Bonus

Gas Price ($/Mcf)

2003

2004

2005

2006

2007

2008

2009

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

Distributions

Gas Price ($/Mcf) |

Dorchester Minerals, LP

7

2009 Production Overview

Geographic Breakdown

Fayetteville

Shale (RI)

4%

Mid-Continent

(Other)

6%

West TX/

SE NM

7%

Gulf Coast/

South TX

10%

Miscellaneous

33%

Mid-Continent

(Hugoton NPI)

36%

Daily Production (MMcfepd)

1.6%

Annualized Decline

10.5%

Decline Since Inception

1.4%

3-year Decline Rate

(1.2%)

1-year Decline Rate

Production Profile

•

Total Production of 10.33 Bcfe

–

82% of total production was natural gas, 18% oil and condensate

–

High quality properties + Diverse portfolio

Low decline rate

–

Year-over-year production rate increased 1.2%

Note: Total production on wellhead basis, daily production on sales basis,

gas-oil equivalency based on 6:1 ratio Barnett

Shale

4%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2003

2004

2005

2006

2007

2008

2009

2010

2011

Forecasted Prod.

Actual Prod. |

Dorchester Minerals, LP

8

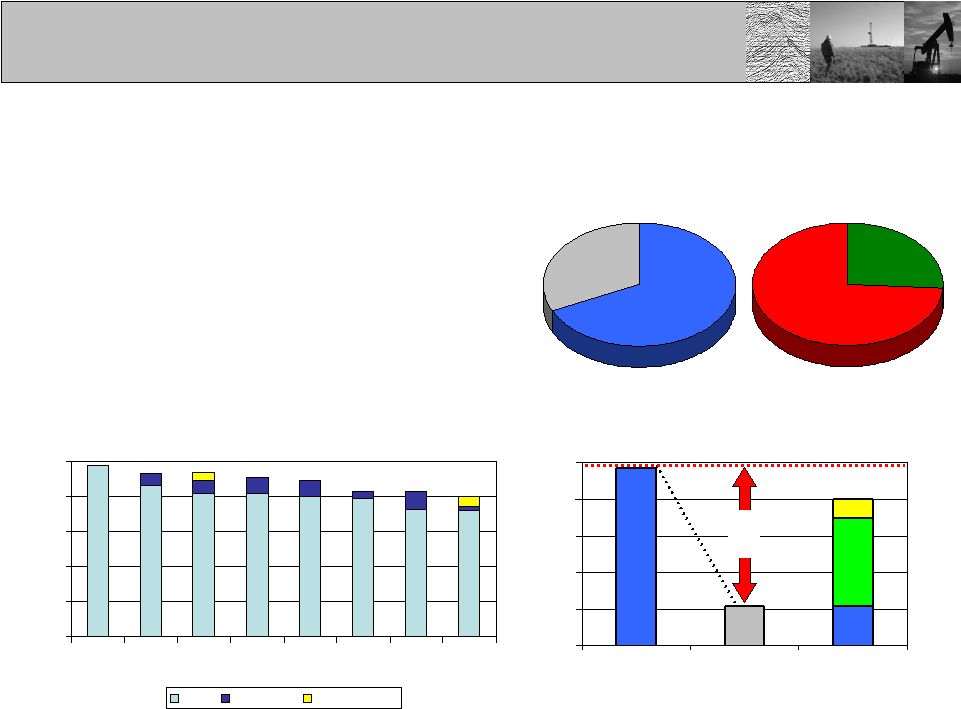

2009 Reserves Overview

•

Total Proved Reserves of 79.9 Bcfe

on 12/31/09

Gas &

NGL

75%

Oil

25%

NPI

32%

Royalty

68%

Year-end Reserves (Bcfe)

0

20

40

60

80

100

Actual

01/31/2003

Projected

12/31/2009

Actual

12/31/2009

79.9

97.0

21.5

Cumulative Reserve Revisions (Bcfe)

2003-2009

Production

(75.5 Bcfe)

–

All reported reserves are Proved Developed

–

Demonstrated history of positive revisions

–

Revisions and acquisitions account

for

73% of current reserves

–

Driven by new plays, field

extensions,

infill drilling, new technology, etc.

–

2.8% of reserves from Fayetteville Shale (RI only)

Reserve

Revisions

(48.0 Bcfe)

Reserve

Acquisitions

(10.4 Bcfe)

Reserve

Base

(21.5 Bcfe)

Note: 10.4 Bcf

of acquired reserves at time transactions closed.

0

20

40

60

80

100

'Feb

2003

2003

2004

2005

2006

2007

2008

2009

Base

Revisions

Acquisitions |

Dorchester Minerals, LP

9

Peer Group Comparison

30

40

50

60

70

80

90

100

110

120

2003

2004

2005

2006

2007

2008

2009

Normalized Reserves (Indexed to 2003)

30

40

50

60

70

80

90

100

110

120

2003

2004

2005

2006

2007

2008

2009

Normalized Production (Indexed to 2003)

•

Reserves and Production Performance

–

DMLP is a cross between a royalty trust with 100% net profits interests (SJT) and

one with 100% royalties (SBR), plus the upside of a large non-producing

mineral portfolio with potential for future drilling and development

–

DMLP has the ability to expand its portfolio of assets through acquisitions

DMLP

HGT

SJT

PBT

MTR

CRT

SBR

Source: SEC 10-K filings |

Dorchester Minerals, LP

10

Peer Group Comparison

80

90

100

110

120

130

140

150

160

Jan

Feb

Mar

Apr

YTD 2010 Normalized Returns (reinvested)

0

100

200

300

400

500

600

700

2003

2004

2005

2006

2007

2008

2009

2010

2003-2009 Normalized Returns (reinvested)

•

Market Performance

–

Pure

royalties

lack

operating

leverage

inherent

in

net

profits

interests

Less

volatility

•

Underperforming in high price environment (mid-2008)

•

Outperforming in low price environment (mid-2009) due to lower fixed cost

structure DMLP

HGT

SJT

PBT

MTR

CRT

SBR

Note: Dist. reinvested on last day of quarter |

Dorchester Minerals, LP

11

Royalty Cash Receipts

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Oil and Gas

Produced

Cash

receipts

begin

1st Quarter

Distribution

declared

Dist. Paid

(Feb-Mar cash)

2nd Quarter

Distribution

declared

Dist. Paid

(Apr-Jun cash)

LP distribution of all cash attributable to January production

may occur as late as August , a 7-month time lag

•

Long delay between production and cash distribution

–

Cash receipts extend over multiple months due to adjustments, releases, etc.

–

Prices

can

change

dramatically

between

production

and

payment

of

distribution

–

Example of a typical cash receipt cycle : |

Dorchester Minerals, LP

12

Royalty Cash Receipts

•

Long delay between production and cash distribution

–

Peak cash receipt month was June 2008

–

Peak distribution was paid in November 2008

–

Actual cash receipts, distributions and gas price:

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan-07

Jan-08

Jan-09

Jan-10

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

Total Cash Receipts

Cash Distributions

Gas Price (HSC)

Cash Receipts/Distribution ($MM)

HSC Gas Price ($/Mcf) |

Dorchester Minerals, LP

13

Maecenas Minerals

Acquisition |

Dorchester Minerals, LP

14

Maecenas Minerals Acquisition

•

Minerals

and

Royalties

–

206

counties

in

17

states

–

Closed transaction on 03/31/10 as a non-taxable exchange for 835,000

units –

Assets concentrated in Texas and North Dakota with increased exposure to oil

plays •

Permian Basin

Seminole

(San

Andres),

Goldsmith,

Wolfberry

potential

•

Williston Basin

Cedar

Hills

South

Unit,

Bakken

and

Three

Forks/Sanish

potential

–

DMLP already

owns

interests

in

all

acquired

properties

–

no

additional

overhead

–

Simple integration into existing accounting and land systems

–

Portfolio includes significant undeveloped acreage with upside potential

–

Analysis of Q1 2010 cash receipts:

$0.468

$0.406

Cash per Unit

$0.39 MM

$12.13 MM

Cash to LP

835,000

29,840,431

Units

15.3%

Maecenas Minerals

DMLP (stand-alone)

Accretion |

Dorchester Minerals, LP

15

Maecenas Minerals Acquisition

•

Goldsmith

Andector

Unit

–

Ector

County,

Texas

–

Representative of assets in the Maecenas portfolio

–

Substantial

production

from

large

multi-well

units

with

little

concentration

of

risk

–

Long-life

reserves

+

Diversified

base

+

Development

potential

Stable

decline

profile

–

Adding

high

quality

properties

improves

DMLP’s

decline

curve

Gross Daily Oil Rate (boepd)

1,000

10,000

100,000

2003

2004

2005

2006

2007

2008

2009

2010

174 Wells

291 Wells |

Dorchester Minerals, LP

16

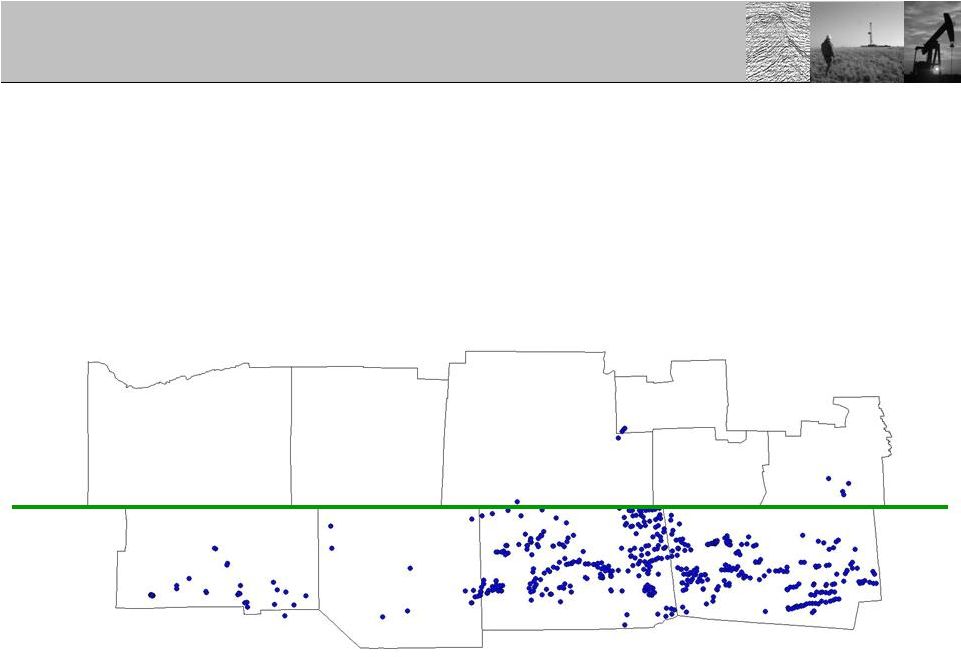

Property Highlights

Royalty Properties |

Dorchester Minerals, LP

17

Property Highlights

Williston

101,810 net acres

Mid-Continent

35,223 net acres

Texas

141,581 net acres

Gulf Coast

18,819 net acres

Eastern

25,273 net acres

Appalachia

23,834 net acres

Other

3,783 net acres

Rockies

5,369 net acres

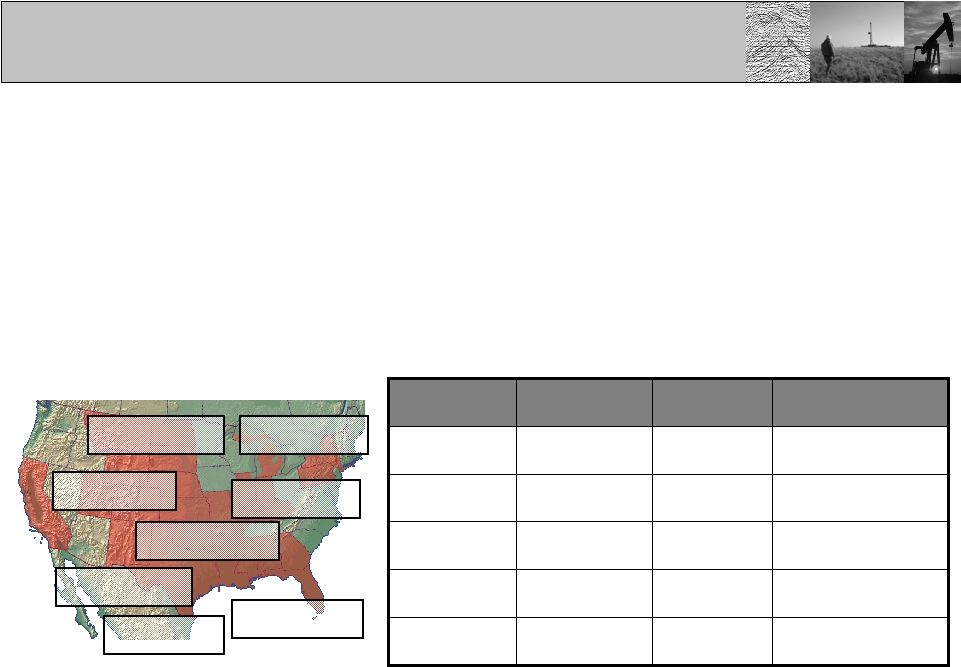

•

Mineral Portfolio Overview

–

355,692 net acres (3,122,867 gross acres) –

574 counties in 25 states

–

Majority of acreage is undeveloped

–

Wide geographic spread including most major producing basins

–

Assets range from mature legacy production to areas with exploratory

potential Expansion

Potential

Ongoing

Development

Legacy

Production

Basin/Area

Three Forks

Sanish

Bakken

Red River

Nesson

Anticline

Williston

Basin

Marcellus/Utica

Upper Devonian

Appalachia

Horizontal

Granite Wash

Fayetteville

Hugoton

Mid-Continent

Horizontal Wilcox

Bob West

Jeffress

McAllen Ranch

Gulf Coast

South Texas

Delaware Basin

West TX Overthrust

Wolfberry

Denver Unit

Wasson

West Texas

Southeast NM

Note: Acreage count as of 12/31/2009, excludes Maecenas transaction

|

Dorchester Minerals, LP

18

Royalty Properties

•

Leasing and Development Activity

–

Consummated 53 leases/elections on 1,724 net acres in 22 counties/

parishes in four states

–

Lease bonus payments up to $1,200/acre

–

Initial royalty terms up to 30%

–

92 active lease offers as of May 2010

–

Identified 353 new wells on royalty properties in 11 states

–

Fayetteville Shale activity continued to ramp up in 2009

–

Low price environment reduced infill drilling and redevelopment on

legacy properties |

Dorchester Minerals, LP

19

Property Highlights

Barnett Shale

|

Dorchester Minerals, LP

20

Royalty Properties

•

Barnett

Shale

–

Tarrant

County,

Texas

–

Closed transaction on 06/30/09 as a non-taxable

exchange for 1,600,000 units

–

Producing and non-producing royalty and ORRI’s

–

100% undivided mineral interest in 6 tracts totaling 1,824

acres and overriding royalty interests in 2 of these tracts

–

NRIs

range from 0.5% to 20%

–

High quality, long-life reserves with development potential

–

Properties integrated into DMLP royalty system with

minimal additional overhead

–

New play adds diversification to DMLP’s

existing portfolio

–

Analysis of Q2 2009 to Q1 2010 cash receipts:

$1.675

$1.278

Cash per Unit

$2.68 MM

$36.09 MM

Cash to LP

1,600,000

28,240,431

Units

31.1%

Barnett Shale

DMLP (stand-alone)

Accretion |

Dorchester Minerals, LP

21

1,000

10,000

100,000

2005

2006

2007

2008

2009

2010

0

15

30

45

60

–

Current Development Activity (CHK Operated)

•

29 producing wells

•

7 wells drilling or waiting on pipeline

•

5 permitted locations

–

Upside potential in undeveloped acreage, downspacing

and improved stimulation

Royalty Properties

Gross Daily Gas Rate (Mcfepd)

Well Count

•

Barnett Shale –

Tarrant County, Texas

DMLP Acquired

Interest

41 wells/permits |

Dorchester Minerals, LP

22

Property Highlights

Net Profits Interests |

Dorchester Minerals, LP

23

Net Profits Interests

•

NPI Provides LP Exposure to Working Interest

Potential Without Generating UBTI

–

Four NPI groups were created at the time of formation in 2003

–

Capitalize on strong negotiating position to capture additional value

–

Leverage information franchise

–

Optional working interest participation in numerous leases

–

Minerals NPI represents the majority of new development activity

–

Elected to participated in 56 wells in Arkansas and Oklahoma

•

30 wells completed in 2009

•

11 wells in various stages of drilling or completion at year-end 2009

•

15 wells waiting to spud at year-end 2009 |

Dorchester Minerals, LP

24

1%

99%

Minerals NPI

Other NPI

Net Profits Interests

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

Historical NPI CAPEX ($MM)

2009 NPI CAPEX

•

Capital Expenditures Through Year-end 2009

–

$21.6 million of cumulative investments in all net profits interest

properties –

2009 capital investments virtually unchanged from 2008

–

Majority of CAPEX was used to drill new wells in the Minerals NPI

–

Continue to reinvest Minerals NPI cash flow |

Dorchester Minerals, LP

25

Net Profits Interests

•

Minerals NPI Performance

–

Production and reserves growing steadily since inception

–

204 wells/units producing in Q4 2009 (175 in pay status)

–

2.6 Bcfe

in production receipts through year-end 2009

–

Total

proved

reserves

of

3.4

Bcfe

at

year-end

2009,

a

43%

increase

over

2008

–

Minerals NPI production and reserves are not included in DMLP results

Note: Gas rate based on sales volumes

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2003

2004

2005

2006

2007

2008

2009

Proved Reserves (Bcfe)

Net Daily Gas Rate (Mcfd)

100

1,000

10,000

2003

2004

2005

2006

2007

2008

2009

2010 |

Dorchester Minerals, LP

26

Net Profits Interests

($4.0)

($3.0)

($2.0)

($1.0)

$0.0

$1.0

2003

2004

2005

2006

2007

2008

2009

2010

Investment

Net Operating Income

Surplus (Deficit)

($MM)

•

Minerals

NPI

Cash

Flow

–

Inception

through

Q1

2010

Cumulative Revenue

$19.1 MM

Cumulative Expense (LOE, taxes, etc)

($3.4 MM)

Cumulative Operating Income

$15.7 MM

Cumulative Investment

($18.7 MM)

Cumulative Surplus (Deficit)

($3.0 MM)

Surplus balance must

be positive before the

Minerals NPI contributes

to LP distributions

Note: Figures provide on a cash basis |

Dorchester Minerals, LP

27

Net Profits Interests

•

Hugoton

Area

–

Operated

Properties

–

2009 production within 1% of projection

–

Year-over-year decline of 7.2%

–

World-class asset but limited upside potential

Gas Rate (Mcfepd)

Well Count

1,000

10,000

100,000

2003

2004

2005

2006

2007

2008

2009

2010

0

50

100

150

200

Note: Gas rate based on sales volumes |

Dorchester Minerals, LP

28

Property Highlights

Fayetteville Shale

|

Dorchester Minerals, LP

29

Fayetteville Shale

•

Eastern

Arkoma

Basin

–

Northern

Arkansas

–

Ownership summary

•

23,336 gross/11,464 net acres in trend

•

196 sections in 8 counties

–

“Hybrid”

leases in 179 sections (9,800 net acres)

•

Bonus and 25% royalty retained by DMLP

•

Participation option owned by the operating partnership

•

Option may be exercised on a well-by-well basis

•

Leverage data gained through mineral ownership

•

Working interests subject to Minerals NPI

2.6%

3.5%

111

Optional WI (NPI)

4.7%

0.0%

Avg. WI

4.7%

4

Unleased

MI (NPI)

2.1%

179

Royalty (DMLP)

Avg. NRI

Sections

Interest Type |

Dorchester Minerals, LP

30

Fayetteville Shale

•

Six County Core Area

–

Current development activity on DMLP acreage

•

142 wells completed as producers (110 in pay status)

•

58 wells in various stages of drilling or completion

•

27 wells permitted and/or proposed by operator

–

Drilling or permitting activity has occurred on 48% of DMLP sections (28% in

2008) Dorchester Acreage

Wells with IP > 6 MMcfd

Productive Fairway

2,264 Producing Wells

428 Active Permits

290 Locations

Note:

Data

from

HPDI,

“Active

Permit”

–

well

spud

but

not

completed,

“Location”

–

well

permitted

but

not

spud

227 wells/permits |

Dorchester Minerals, LP

31

Fayetteville Shale

–

Development activity remains at high levels, driven by SWN and CHK

–

Well spuds have been outpaced by well permits, a leading indicator

–

Substantial

time-lag

between

permit

and

first

payment

359

days

•

Permitting, Drilling and Payment History

First

Payment

First

Production

Well

Spud

Well

Permitted

54 days

118 days

187 days

Well Count

0

5

10

15

20

25

Q1

07

Q2

07

Q3

07

Q4

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

New Permits

New Wells Spud

1st Payment Received |

Dorchester Minerals, LP

32

•

Capital Expenditures

Fayetteville Shale

•

2009 Reserves

0.0

1.0

2.0

3.0

4.0

5.0

2006

2007

2008

2009

DMLP (RI)

Minerals NPI (WI)

Proved Reserves (Bcf)

–

Year-end reserves of 4.9 Bcf

(124 wells)

•

2.3 Bcf

(WI)

•

2.6 Bcf

(RI)

–

69% Year-over-year reserve increase

–

Only completed wells with test rates are

included in reserve estimates (no PUDs)

0.0

1.0

2.0

3.0

4.0

5.0

2006

2007

2008

2009

Capital Expenditures ($MM)

–

All expenditures within Minerals NPI

–

Total Fayetteville investments of

$10.4 MM through Q1 2010

–

Average $3.1 MM per well in 2009

–

Drilling and completion costs may

increase with longer lateral lengths |

Dorchester Minerals, LP

33

•

Well Performance

•

Production Results

Fayetteville Shale

Net Daily Production (Mcfd)

0

1,000

2,000

3,000

4,000

5,000

2006

2007

2008

2009

2010

Net RI Production

Net WI Production

–

123 wells producing at year-end 2009

•

2.4 MMcfd

(WI)

•

2.0 MMcfd

(RI)

–

91% Year-over-year rate increase

–

Produced 1.2 Bcf

in 2009

–

54% from working interest wells

Normalized Production Rate (Mcfd)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

2

4

6

8

10

12

2.0 Bcf (SEECO)

2.5 Bcf (SEECO)

3.0 Bcf (SEECO)

DMLP (2009 Avg)

Months on Production

–

Improved stimulation and longer laterals

have increased average initial rate

•

2006

1.9 MMcfd

(Max 2.9 MMcfd)

•

2007

1.7 MMcfd

(Max 3.5 MMcfd)

•

2008

2.4 MMcfd

(Max 5.5 MMcfd)

•

2009

3.1 MMcfd

(Max 5.9 MMcfd)

Note:

Volumes

from

AOGC,

1

st

point

on

DMLP

normalize

curve

based

on

estimates

from

partial

month

data

4.4 MMcfd |

Dorchester Minerals, LP

34

Property Highlights

Horizontal Bakken |

Dorchester Minerals, LP

35

Horizontal Bakken

•

Williston Basin –

Northwestern North Dakota

–

Diversified acreage position

•

70,390 gross acres/9,503 net acres

–

Operators: Continental, EOG, Whiting, Marathon

–

Elected non-consent option in 88 wells to date

•

Average royalty of all leases in unit (~15% royalty)

•

Back-in for 100% WI after payout + 50% penalty

•

Working interest subject to Minerals NPI

–

Historical activity trend:

0

5

10

15

20

Q1

07

Q2

07

Q3

07

Q4

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

New Permits

New Wells Spud

Wells Reaching Payout

Well Count |

Dorchester Minerals, LP

36

Horizontal Bakken

•

Six County Core Area

–

Current development activity on DMLP acreage

•

64 wells completed as producers (4 reached payout status)

•

14 wells in various stages of drilling or completion

•

10 wells permitted and/or proposed by operator

–

Rig count has increased 268% since May 2009

–

Three rigs currently drilling on DMLP acreage

Parshall,

Sanish

&

Stanley

fields

(426 nma)

Lila

1-36H

Owan-Nehring

27-34 1H

Harstad

1-18-19H

2.45%

0.42%

561

Lila 1-36H (Continental)

0.11%

1.65%

5.82%

2.47%

19.76%

APO

NRI

0.02%

0.21%

0.73%

0.52%

4.15%

BPO

NRI

Test Rate

(boepd)

Well Name (Operator)

1,476

McGregor 1-15H (Continental)

2,513

Owan-Nehring

27-34 1H (BEXP)

681

Harstad

18-19H (Fidelity)

1,639

Pederson 1-33H (EOG)

1,693

Austin 20-29H (EOG)

Pederson

1-33H

Austin

20-29H

McGregor

1-15H

88 wells/permits |

Dorchester Minerals, LP

37

Developing Play

Highlights |

Dorchester Minerals, LP

38

Developing Play Highlights

•

Devonian Shale (Appalachia)

–

New York and Pennsylvania

–

Concentrated acreage position

•

32,447 gross acres

•

24,774 net acres

•

70% in Allegany and Steuben Counties, NY

–

Challenging political environment in New York

–

Potential targets

•

Upper Devonian oil (shallow)

•

Marcellus/Devonian shale gas (middle)

•

Trenton-Black River gas (deep)

–

Operators: Anadarko, Cabot, Chesapeake,

EOG, EXCO, Fortuna Energy, Range, XTO

–

No reserves booked in 2009

Allegany & Steuben

Counties |

Dorchester Minerals, LP

39

Developing Play Highlights

•

Southern Tier NY & Northern Tier PA

–

Regulatory

environment

in

New

York

has

limited

activity

relative

to

Pennsylvania

–

Prospectivity

of

acreage

in

Allegany

and

Steuben

Counties

is

undetermined

due

to

limited testing of potential shale gas zones

–

Continuing to monitor industry activity in the area

Allegany

13,216 nma

Steuben

4,714 nma

Chemung

308 nma

Schuyler

459 nma

Tioga

163 nma

Bradford

0 nma

Potter

846 nma

McKean

1,158 nma

Cattaraugus

0 nma

Tioga

41 nma

NY

PA

NY

PA |

Dorchester Minerals, LP

40

Developing Play Highlights

•

Granite Wash –

Texas Panhandle

–

Concentrated acreage position in Northeast Wheeler County

•

DMLP owns 5,444 gross/1,189 net acres

–

Substantial liquids component to production

–

Multiple active lease offers

Horizontal Wells/Permits

NFX: 10.1 MMcfd

NFX: 12.7 MMcfd

FST: 10.2 MMcfd

NFX: 16.1 MMcfd

CHK: 18.5 MMcfd

DVN: 18.0 MMcfd

NFX: 20.1 MMcfd

APA: 6.6 MMcfd |

Dorchester Minerals, LP

41

Dorchester Minerals, LP

Annual Meeting

May 12, 2010 |

Dorchester Minerals, LP

42

Appendix |

Dorchester Minerals, LP

43

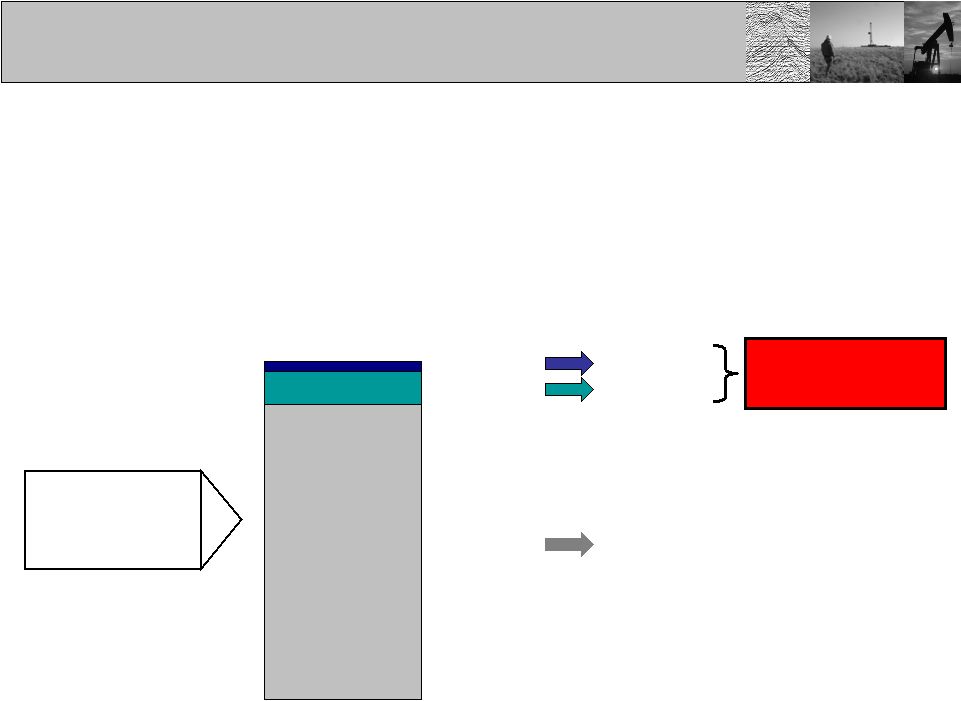

•

What is the Minerals NPI and How Does it Work?

Appendix

–

Upon its formation, Dorchester Minerals, LP (DMLP, the public partnership and owner

of the mineral interests) provided for future development opportunities on its

undeveloped mineral interests by the creation of the Minerals Net Profits

Interest (Minerals NPI). –

DMLP has negotiated and may continue to negotiate the right but not the obligation to

participate in development activity in addition to retaining a royalty

interest. –

This right may take the form of an optional heads-up (unpromoted) working

interest, carried working interest or reversionary (back-in) working

interest. In some instances, an unleased mineral interest may

be treated as a working interest subject to statutory non-consent

provisions. –

DMLP assigns this right to Dorchester Minerals Operating LP (the

operating partnership or DMOLP)

subject to the terms of the Minerals NPI.

–

DMOLP is an indirect wholly owned affiliate of DMLP’s

General Partner.

–

DMOLP funds all costs associated with this right, including drilling and completion

costs. –

DMLP and its partners are not liable for any costs or expenses.

–

DMOLP pays to DMLP 96.97% of the monthly “Net Proceeds”

attributable to the properties subject to the

Minerals NPI.

–

Net Proceeds is defined as total revenues less total expenses plus an amount

equivalent to interest at a prevailing rate on any prior period deficit

balance. In other words, DMOLP pays 100% of all costs, receives 100% of all

revenues plus interest, and thereafter (sometimes called “Payout”) pays 96.97% of

net cashflow

to DMLP.

–

LP distributions reflect 96% of royalty net cashflow

and 99% of NPI net cashflow

99% x 96.97% = 96%. |

Dorchester Minerals, LP

44

Appendix

DMLP

Lease to third party for

royalty and optional

participation right

Participation right

assigned to DMOLP

NPI payment

(96.97% of cash flow)

Distributable Cash

DMOLP pays 100% of costs

and receives 100% of revenue

plus interest equivalent on

total NPI basis

Royalty

(100% of cash flow)

General

Partner

4% of

royalties

1% of NPI’s

Limited

Partners

96% of

royalties

99% of NPI’s

•

What is the Minerals NPI and How Does it Work? |

Dorchester Minerals, LP

45

Appendix

•

Distribution Determinations

4% of Net Cash Receipts from Royalty Properties

$ --------

$1,309

96% of Net Cash Receipts from Royalty Properties

$31,416

$ --------

1% of Net Profits Interests Paid to our Partnership

$ --------

$120

Total Distributions

$43,299

$1,429

99% of Net Profits Interests Paid to our Partnership

$11,883

$ --------

Operating Partnership Share (3.03% of Net Proceeds)

$ --------

$375

Total General Partner Share

$1,804

% Total

96%

4%

Limited

Partners

General

Partner

–

Period from October 2008 through September 2009

($ thousands) |

Dorchester Minerals, LP

46

Appendix

2009 Cash

Distributions

$44.7 MM

Mgmt GP

Mgmt LP

Other LP

$1.4 MM

$3.6 MM

$39.7 MM

Mgmt LP is 2.6

times Mgmt GP

•

Alignment of GP and LP interests

–

GP has no incentive distribution rights –

fixed sharing ratio

–

Management’s LP interest exceeds its GP interest

–

Not incentivized to make dilutive transactions

88.8 %

8.1 %

3.1 % |

Dorchester Minerals, LP

47

•

Operating Leverage –

Royalty Interest vs. NPI

Appendix

Net Profits Interest

Royalty Interest

1,000 Mcf

$6.00/Mcf

$6,000

($0)

$6,000

25% Royalty

$1,500

1,000 Mcf

$7.80/Mcf

$7,800

($0)

$7,800

25% Royalty

$1,950

1,000 Mcf

$6.00/Mcf

$6,000

($1,000)

$5,000

25% NPI

$1,250

1,000 Mcf

$7.80/Mcf

$7,800

($1,000)

$6,800

25% NPI

$1,700

30% Increase in

Royalty Cash Flow

36% Increase in

NPI Cash Flow

30% Increase in Gas Price

Production Volume

Gas Price

Revenue

Fixed Production Costs

Operating Income

Net Interest

Net Cash Flow

Production Volume

Gas Price

Revenue

Fixed Production Costs

Operating Income

Net Interest

Net Cash Flow |