Attached files

| file | filename |

|---|---|

| 8-K - RHB IR PRESENTATION 4Q09 APRIL 7, 2010 - REHABCARE GROUP INC | eightk4q09present4710.htm |

Investor Presentation

Fourth Quarter 2009

Exhibit 99

Company Overview

n Headquartered in St. Louis, Missouri

n Established in 1982

n Largest contract manager of

rehabilitation services in hospitals and

long-term care settings, with nearly

1,300 locations in 41 states

rehabilitation services in hospitals and

long-term care settings, with nearly

1,300 locations in 41 states

n Fourth largest post-acute hospital

operator and third largest long-term

acute care hospital (LTACH) provider

in U.S.

operator and third largest long-term

acute care hospital (LTACH) provider

in U.S.

n Completed acquisition of Triumph

HealthCare, a leading operator of

LTACHs, on Nov. 24, 2009

HealthCare, a leading operator of

LTACHs, on Nov. 24, 2009

Geographic Presence

Hospital Rehabilitation Services (HRS) Division

Skilled Nursing Rehabilitation Services (SRS) Division

Hospital Division

1

Division Overviews

Skilled Nursing Rehabilitation

Services (SRS)

n $496 mm - 39% of pro forma

revenue

revenue

n 1,118 SNF/long-term care

programs in 37 states

programs in 37 states

n 8.1 mm annual patient visits

n Polaris Group - consulting for

long-term care facilities

long-term care facilities

n VTA Management Services -

therapy and nurse staffing for

New York

therapy and nurse staffing for

New York

$1.3 billion pro forma operating revenues for FYE 2009

Hospital Rehabilitation

Services (HRS)

n $178 mm - 14% of pro forma

revenue

revenue

n 145 hospital-based programs in

32 states

32 states

n 44,000 IRF discharges/year

n 1.3 mm annual outpatient visits

n $588 mm - 47% of pro forma

revenue

revenue

n 28 LTACHs, 6 IRFs; 13 states

n 19 FS LTACHs, 9 HIHs; 4 FS

IRFs, 2 HIHs

IRFs, 2 HIHs

n 1,593 licensed LTACH beds; 243

IRF beds

IRF beds

n 406,000 annual patient days

LTACHs = Long-Term Acute Care Hospitals

IRFs = Inpatient Rehabilitation Facilities

SNFs = Skilled Nursing Facilities

FS = Freestanding

HIH = Hospital in Hospital

Hospital Division

2

13%

Patient Discharge Destination1

LTACH / SNF

IRF

No post-

acute care

acute care

Hospice/Home Health

65%

Acute care

hospital

hospital

3

Market Overview

2MedPAC Data Book, June 2009; does not include Home Health or

Medicare Advantage

Medicare Advantage

3Avalere Health LLC, April 2009; does not include Home Health or

Medicare Advantage

Medicare Advantage

Medicare Post-Acute Spending (in billions)

$

n Large, growing and highly fragmented market

n Positive demographic trends, with first wave of Baby Boomers entering Medicare in 2011

n Medicare expenditures for post-acute services (excluding home health) projected to increase 113%

from 2007 to 2021

from 2007 to 2021

n RehabCare delivers services across the post-acute continuum of care, providing the

most appropriate discharge destination for acute patients

most appropriate discharge destination for acute patients

Projected3

Actual2

Hospital Division

Overview

Overview

Competitive Landscape

1MedPAC, March 2010 Report to the Congress

2Does not include additional Triumph facility scheduled to open April 2010

n Post Triumph merger, RehabCare is the third largest LTACH operator in the U.S., the largest

provider of long-term acute care in Houston and the dominant provider of LTACH services in

9 of its 13 markets

provider of long-term acute care in Houston and the dominant provider of LTACH services in

9 of its 13 markets

n RehabCare pursues joint venture hospital partnerships (nine currently, representing 14

locations) with market-leading acute care providers and physician groups, in addition to its

wholly owned facilities

locations) with market-leading acute care providers and physician groups, in addition to its

wholly owned facilities

Market Size1: 221 IRFs

(Freestanding and HIHs)

Market Size1: 386 LTACHs

IRFs

LTACHs

4

Source: Information available from public filings or

from company websites

from company websites

2

99

95

83

34

23

19

16

14

8

4

Triumph Acquisition

Strategic rationale

Strategic rationale

n Combination provides immediate economies of scale

n Creates stronger, more comprehensive continuum of care, better positioning RehabCare for

potential changes in reimbursement (e.g., bundling)

potential changes in reimbursement (e.g., bundling)

n Additional growth potential through LTACH and IRF development opportunities

n All LTACH business now under Triumph management

n Meaningfully accretive to 2010 EPS; strong cash flow and ability to quickly deleverage

n More diversified business lines, reducing reliance on management contracts for revenue and EBITDA

streams

streams

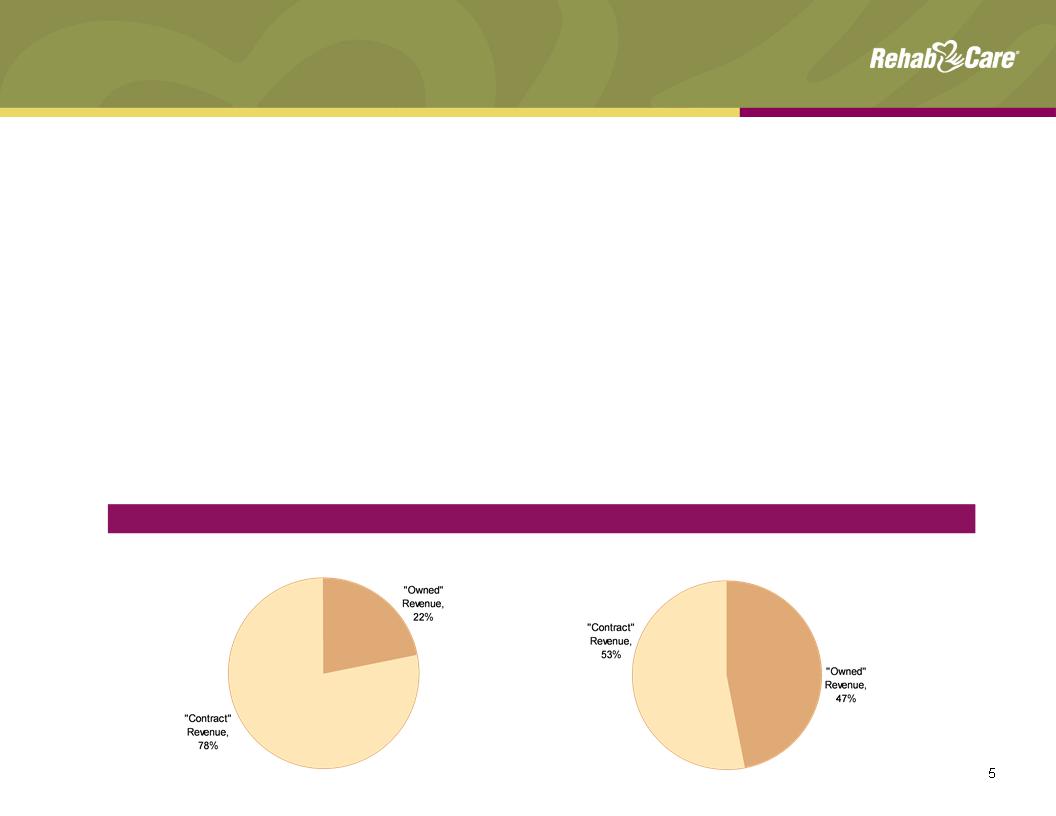

FYE 2009 “Owned” Revenue vs. “Contract” Revenue

RehabCare

Pro Forma

n Division historically has been impacted by de novo start-up losses and infrastructure investments;

Triumph merger provides level of critical mass as well as ability to adopt proven operational

strengths

Triumph merger provides level of critical mass as well as ability to adopt proven operational

strengths

n Expect total year 2010 revenue of $650.0 - $675.0 mm and EBITDA of $90.0 - $100.0 mm

n Reaffirm breakeven operating earnings run rate for 13 legacy hospitals by the end of the second

quarter of 2010 and breakeven operating earnings for FY2010; Dallas LTACH on track to be

accretive by end of Q210

quarter of 2010 and breakeven operating earnings for FY2010; Dallas LTACH on track to be

accretive by end of Q210

n Triumph impacted by softer volumes and compliance with 25-day length of stay for six hospitals in

Jan. and Feb.; EBITDA margin expected to be at historical level of 18 - 20% in Mar. 2010

Jan. and Feb.; EBITDA margin expected to be at historical level of 18 - 20% in Mar. 2010

Hospital Division

Performance/outlook

Performance/outlook

Operating Earnings ($ in millions)

1Operating earnings excluding start-up & ramp-up losses and transaction and severance related

costs, see Appendix for reconciliation to GAAP

costs, see Appendix for reconciliation to GAAP

2Includes $39.7 million in revenue and operating earnings of $3.7 million generated by Triumph from

11/25/09 - 12/31/09

11/25/09 - 12/31/09

3Includes a $1.5 million pretax charge related to the cancellation of a planned acquisition and

development project

development project

2

New Hospitals: 1 0 1 1 21

4Q2008 1Q2009 2Q2009 3Q2009 4Q2009

6

Revenue ($ in millions) and Patient Days

2

1

3

Skilled Nursing Rehabilitation Services (SRS)

Division overview

Division overview

n Manages rehab programs for SNFs

n Each Medicare-certified SNF is required to provide physical, speech and occupational therapy,

but many lack the know-how and/or scale to effectively manage a program

but many lack the know-how and/or scale to effectively manage a program

n RehabCare provides a compelling value proposition to its SNF partners

n Access to advanced technology platform

n Broader array of services

n Better access to scarce therapist labor pool

Source: Information available from public filings or from company websites

¹Source: MedPAC Report to Congress, March 2010

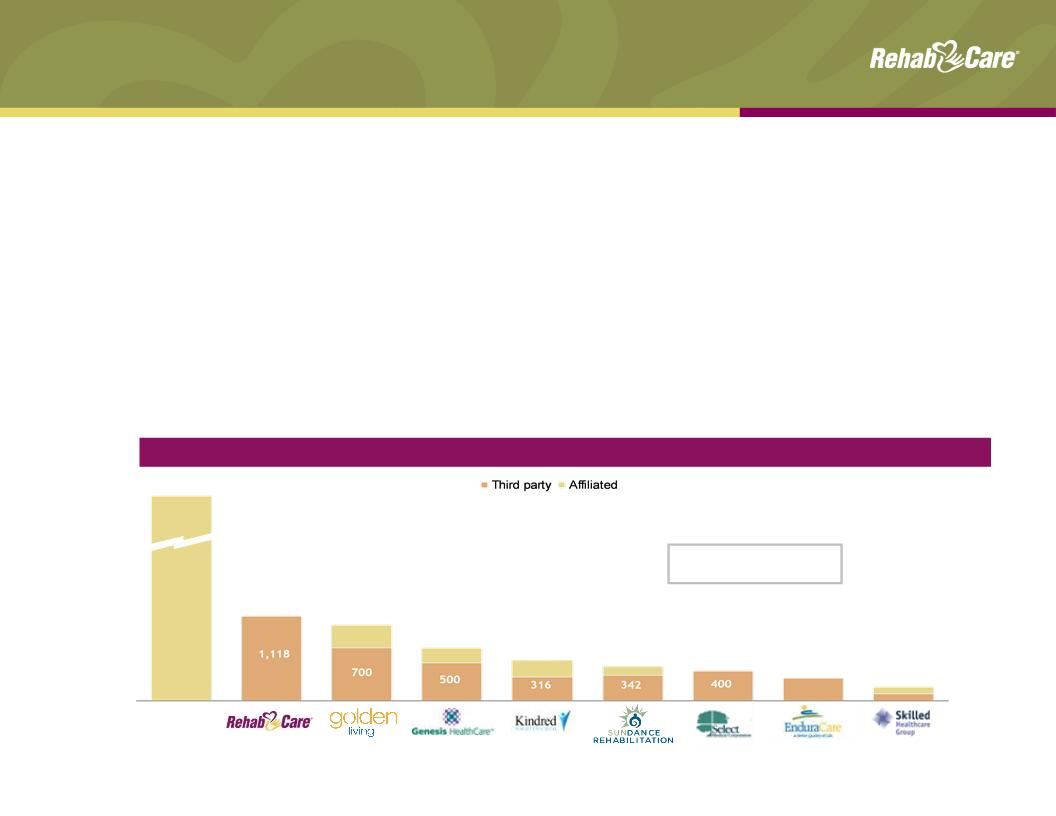

Competitive Landscape — # of facilities served

Self-

operated

11,000+

1,118

1,000

700

538

450

400

300

188

Market Size1: 15,000+

Medicare-certified SNFs

Medicare-certified SNFs

7

SRS Division

Performance/outlook

Performance/outlook

Revenue ($ in millions)

Note: Includes Symphony acquisition as of July 1, 2006

1Same store analysis does not include Symphony

% Margin: 5.5% (0.3%) 1.7% 5.6% 7.6%

Operating Earnings ($ in millions)

8

YOY growth: 35.5% 49.9% 24.4% 5.6% 8.5%

Same store: 8.4% 1.0%¹ 7.1%1 12.4% 8.8%

n Significant same store revenue and margin growth since completion of Symphony

integration in 2007

integration in 2007

n Expect 6.5% - 7.5% operating earnings margins for the full year 2010, driven by mid-single

digit year-over-year same store revenue growth (reflects estimated impact of concurrent

therapy rules that go into effect Oct. 1, 2010); 50 to 75 net new units in 2010

digit year-over-year same store revenue growth (reflects estimated impact of concurrent

therapy rules that go into effect Oct. 1, 2010); 50 to 75 net new units in 2010

n First quarter impacted by Part B therapy caps; Senate cleared package of short-term

extenders on Mar. 4, which extended therapy cap exceptions process through Mar. 31,

2010; healthcare reform legislation extends through Dec. 31, 2010

extenders on Mar. 4, which extended therapy cap exceptions process through Mar. 31,

2010; healthcare reform legislation extends through Dec. 31, 2010

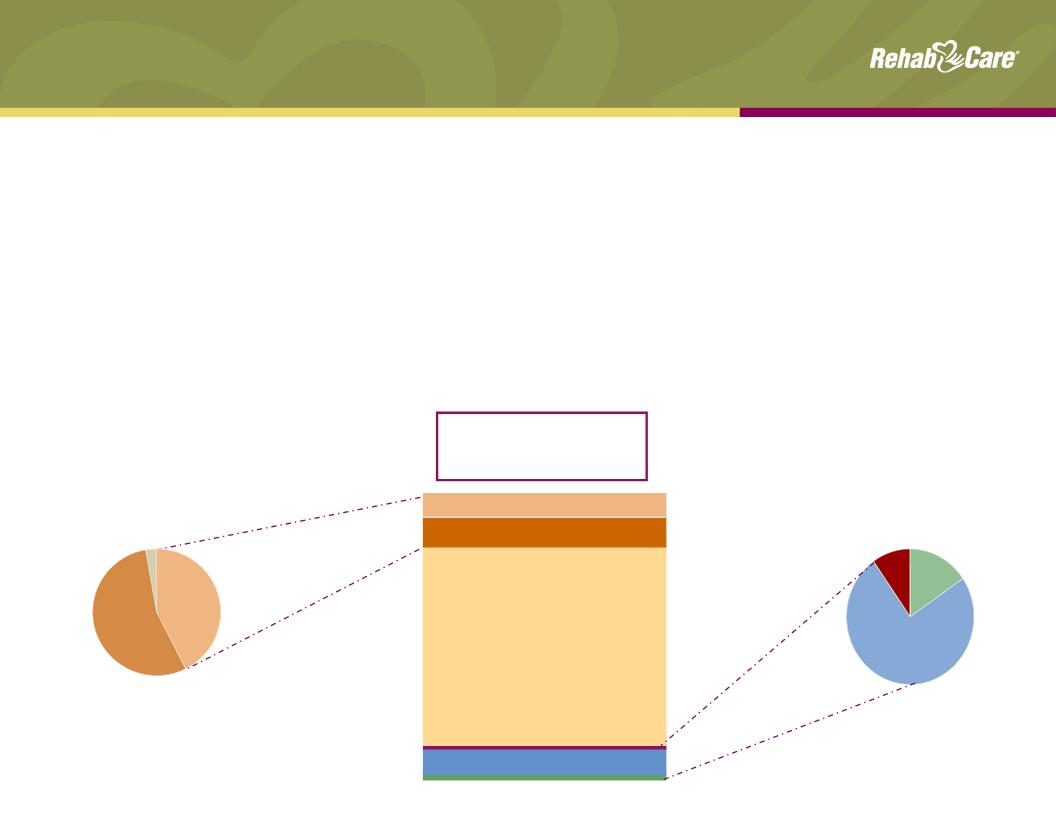

RehabCare, 9.1%

Horizon Health, 1.9%

Other, 0.9%

Hospital-based:

Self-op, 69.9%

Other, 9.9%

RehabCare, 0.5%

HealthSouth, 7.8%

Source: Information available from public filings or from

company websites

company websites

1MedPAC March 2010 Report to the Congress

Horizon Health

15.6%

15.6%

Other

9.8%

9.8%

RehabCare

74.6%

74.6%

Freestanding

Hospital-Based

3rd Party

3rd Party

HealthSouth

42.9%

42.9%

Other 54%

RehabCare

3.1%

3.1%

18.2%

11.9%

Hospital Rehabilitation Services (HRS)

Division overview

Division overview

n Manages hospital-based inpatient and outpatient therapy programs on a contract basis, providing

its partners with:

its partners with:

n Improved clinical outcomes

n Ability to attract ≈ 30% admissions from external sources

n Broader clinical programming (brain, stroke, spinal dysfunction)

n Better access to scarce therapist labor pool

n Better compliance (60% rule, RAC, 3-hour rule)

Market Size1: 1,202

hospital-based and

freestanding IRFs

hospital-based and

freestanding IRFs

9

10

HRS Division

Performance/outlook

Performance/outlook

n Revenue and earnings declined due to implementation of 75% Rule in 2004; freeze of rule

at 60% in January 2008 gave runway for revenue growth

at 60% in January 2008 gave runway for revenue growth

n Expect 15% - 17% operating earnings margin and 2 - 4% year-over-year growth in IRF

same store discharges for the full year 2010; unit count expected to decrease in first half of

year with recovery in second, resulting in flat unit growth for year

same store discharges for the full year 2010; unit count expected to decrease in first half of

year with recovery in second, resulting in flat unit growth for year

¹Includes $1.2 mm pretax charge from a bad debt write-down related to an

outpatient transaction

outpatient transaction

Revenue ($ in millions)

CAGR: (1.6%)

YOY growth: (0.5%) (5.3%) (8.7%) 0.9% 7.6%

IRFs: 120 115 107 113 106

Operating Earnings ($ in millions)

% Margin: 11.9% 13.2% 14.0% 13.3% 16.6%

1

Standalone and Pro Forma

Historical Key Financials

Historical Key Financials

Pro Forma

RehabCare

Diluted Earnings Per Share³

1RehabCare 2009 historical includes $39.7 million in revenue generated by Triumph;

excluding Triumph, RHB Y-o-Y growth would have been 12.8%

excluding Triumph, RHB Y-o-Y growth would have been 12.8%

2See Appendix for reconciliation to GAAP

3Represents net earnings per share from continuing operations, attributable to

RehabCare

RehabCare

Historical Operating Revenue¹ ($mm)

11

Historical Adjusted EBITDA² ($mm)

Historical Adjusted EBITDA Margin (%)

$1.88

4RehabCare 2009 historical includes transaction and severance related pre-tax

charges of $9.4 mm or $0.38 per diluted share. Pro forma 2009 historical includes

severance and other transaction related pre-tax charges of $10.7 mm or $0.27 per

diluted share. Excluding these charges, 2009 accretion would have been 31.1%.

charges of $9.4 mm or $0.38 per diluted share. Pro forma 2009 historical includes

severance and other transaction related pre-tax charges of $10.7 mm or $0.27 per

diluted share. Excluding these charges, 2009 accretion would have been 31.1%.

4

4

12

Consolidated Pro Forma

Balance Sheet

Balance Sheet

n Cash flow from operations was $48.0 mm for fiscal year 2009 consistent with 2008

n Days sales outstanding improved from 66 days at Dec. 31, 2008 to 60 days at Dec.

31, 2009 excluding Triumph

31, 2009 excluding Triumph

n Expect continued strong operating cash flow with DSO of approximately 60 - 65 days

n Capital expenditures anticipated to be $32.0 mm in 2010, consisting of $12.5 mm of

information system investments; $12.5 mm in expansion projects and $7.0 mm related

to maintenance

information system investments; $12.5 mm in expansion projects and $7.0 mm related

to maintenance

Cash and Cash Equivalents

Total Assets

Total Debt

Stockholders’ Equity

Noncontrolling Interests

Percent of Debt to Total Capital¹

Debt to Pro Forma Adjusted EBITDA²

($mm)

$ 24.7

1,110.0

455.3

437.3

22.3

50%

3.0x

12/31/09

1Total capital represents the sum of debt, stockholders’ equity and noncontrolling interests

2Represents Total Debt plus OID of $8.9 mm divided by 2009 Pro forma Adjusted EBITDA; see Appendix for reconciliation of Pro forma

Adjusted EBITDA to GAAP

Adjusted EBITDA to GAAP

Impact of Healthcare Reform

n Extends LTACH provisions of Medicare, Medicaid and SCHIP Extension Act (MMSEA) of 2007

through Dec. 31, 2012

through Dec. 31, 2012

n Maintains existing status related to 25% Rule and short-stay outliers

n Delays one-time budget neutrality adjustment (estimated at 3.75%)

n Continues moratorium on new LTACH beds while facility criteria is established

n Extends auto exception process for Part B therapy caps through Dec. 31, 2010

n Delays implementation of RUGs IV until Oct. 1, 2011; concurrent therapy rules take effect Oct.

1, 2010

1, 2010

n Establishes negative adjustments to annual market basket calculations for IRFs and LTACHs

of an average 32 bps/year beginning Apr. 1, 2010 through rate year 2019; no market basket

adjustments for SNFs; all sectors subject to productivity adjustments beginning in 2012

of an average 32 bps/year beginning Apr. 1, 2010 through rate year 2019; no market basket

adjustments for SNFs; all sectors subject to productivity adjustments beginning in 2012

n Establishes a national pilot program by 2013 to study effectiveness of bundled payment

system for hospital services, physician services and post-acute care delivered three days prior

to hospitalization through 30 days post-discharge

system for hospital services, physician services and post-acute care delivered three days prior

to hospitalization through 30 days post-discharge

n Implements payment penalties for hospitals with high readmission rates

n Beginning in 2012, allows providers organized as Accountable Care Organizations (ACOs) that

voluntarily meet quality thresholds to share in cost savings achieved in Medicare program

voluntarily meet quality thresholds to share in cost savings achieved in Medicare program

n Prohibits physician ownership of hospitals, effective Dec. 31, 2010, and creates new

transparency, reporting and expansion requirements for “grandfathered” hospitals

transparency, reporting and expansion requirements for “grandfathered” hospitals

13

Strategic Direction

n Enhance focus on clinical outcomes through cutting-edge technology and

commitment to excellence

commitment to excellence

n Advance to next generation in point-of-care technology

n Develop Centers of Excellence

n Provide oversight of clinical quality and outcomes through Quality and Patient

Safety Committee

Safety Committee

n Drive organic growth and continue to explore M&A opportunities in existing

businesses

businesses

n Improve profitability of Hospital division through Triumph merger

n Complete three scheduled hospital expansion projects; explore development

opportunities within Triumph facilities

opportunities within Triumph facilities

n Enhance client value proposition through new product offerings for ACOs,

critical access hospitals, etc.; bundling options and IT solutions

critical access hospitals, etc.; bundling options and IT solutions

n Utilize point-of-service technology to increase speed of referrals/admissions,

strengthen relationships with referrers and optimize performance

strengthen relationships with referrers and optimize performance

14

15

Safe Harbor

Forward-looking statements have been provided pursuant to the safe harbor

provisions of the Private Securities Litigation Reform Act of 1995. Such statements

are based on the Company’s current expectations and could be affected by

numerous factors, risks and uncertainties discussed in the Company’s filings with

the Securities and Exchange Commission, including its most recent annual report

on Form 10-K, subsequent quarterly reports on Form 10-Q and current reports on

Form 8-K. Do not rely on forward looking statements as the Company cannot

predict or control many factors that affect its ability to achieve the results

estimated. The Company makes no promise to update any forward looking

statements whether as a result of changes in underlying factors, new information,

future events or otherwise.

provisions of the Private Securities Litigation Reform Act of 1995. Such statements

are based on the Company’s current expectations and could be affected by

numerous factors, risks and uncertainties discussed in the Company’s filings with

the Securities and Exchange Commission, including its most recent annual report

on Form 10-K, subsequent quarterly reports on Form 10-Q and current reports on

Form 8-K. Do not rely on forward looking statements as the Company cannot

predict or control many factors that affect its ability to achieve the results

estimated. The Company makes no promise to update any forward looking

statements whether as a result of changes in underlying factors, new information,

future events or otherwise.

Appendix

16

17

Primary Post-Acute Settings

Overview

Overview

|

|

Long Term Acute Care Hospitals

|

Skilled Nursing Facilities

|

Inpatient Rehab Facilities

|

|

Medicare

Spending 2009 |

$4.6 billion

|

$25.5 billion

(est. $6 billion rehab) |

$5.8 billion

|

|

Patients Served

2008 |

130,869 Medicare discharges

|

2.6 million Medicare admissions

|

370,048 Medicare discharges

|

|

Type of Patient

|

High acuity, at least 25 days

|

Low to moderate acuity, may

require some rehab |

High acuity, requires extensive

rehab (min 3 hrs/day) |

|

Avg. Length of

Stay |

At least 25 days

|

27 days

|

13.2 days

|

|

Medicare

Reimbursement |

LTACH PPS - Receive a single payment

when Medicare beneficiary is discharged for all services rendered |

SNF PPS - Receive a per diem

payment under both Medicare Part A and state Medicaid programs |

IRF PPS- Receive a single

payment when Medicare beneficiary is discharged for all services rendered |

|

Medicare

Requirements |

• Patients must have an average length

of stay of >25 days • 25% rule: no more than 25% of

patients may be referred from a single source (fixed at 50% through 2012) • Moratorium on new LTACH beds until

2013 |

Medicare covers up to 100 days

of SNF care following an acute hospital stay of at least 3 days |

60% Rule: 60% of patients

must satisfy one of 13 defined conditions |

Source: MedPAC

Standalone and Pro Forma Historical

Financial Reconciliations

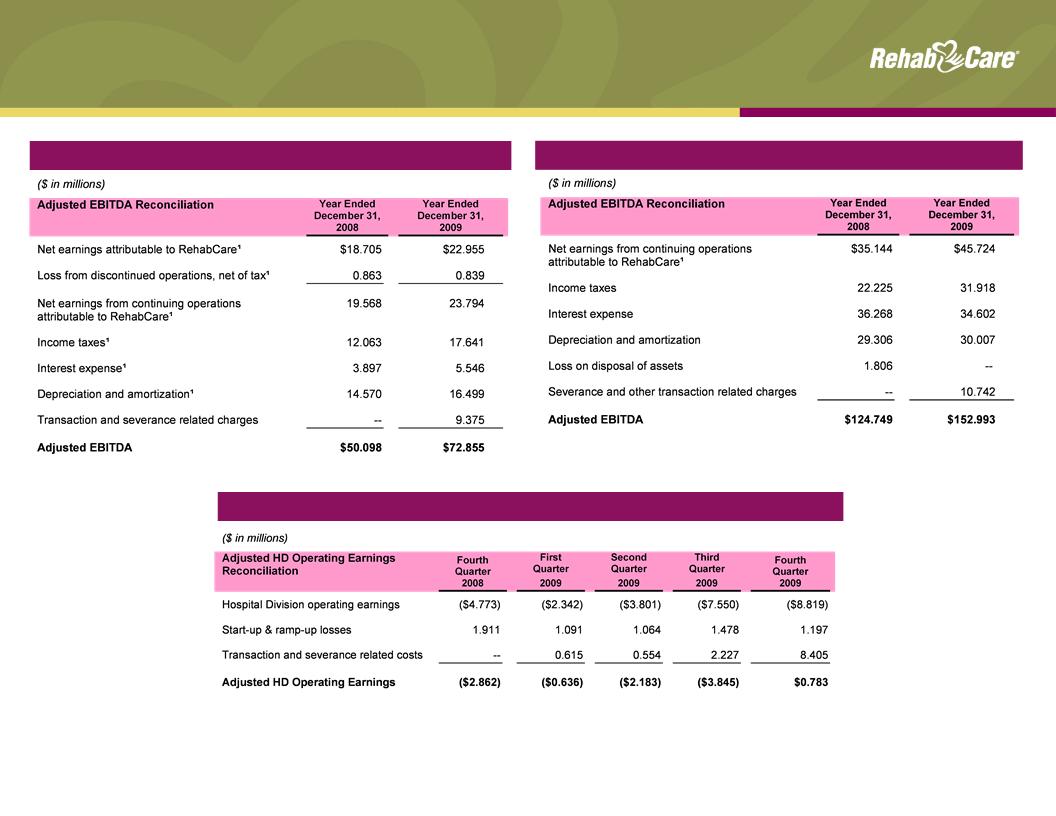

Financial Reconciliations

RehabCare Adjusted EBITDA

Pro Forma Adjusted EBITDA

1As reflected in the Company’s 2009 Form 10-K financial statements and footnotes

18

Hospital Division Adjusted Operating Earnings