Attached files

| file | filename |

|---|---|

| 10-K - THE YORK WATER COMPANY 10K 12-31-09 - YORK WATER CO | form10k123109.htm |

| EX-23 - CONSENT OF PARENTEBEARD LLC - YORK WATER CO | exhibit23-123109.htm |

| EX-31.1 - YWC CERTIFICATION OF CEO - YORK WATER CO | exhibit311-123109.htm |

| EX-31.2 - YWC CERTIFICATION OF CFO - YORK WATER CO | exhibit312-123109.htm |

| EX-32.1 - YWC SECTION 906 CERTIFICATION OF CEO - YORK WATER CO | exhibit321-123109.htm |

| EX-32.2 - YWC SECTION 906 CERTIFICATION OF CFO - YORK WATER CO | exhibit322-123109.htm |

EXHIBIT 13

| 1 | |

| 2 | |

| 4 | |

| 14 | |

| 15 | |

| 16 | |

| 17 | |

| 19 | |

| 20 | |

| 21 | |

| 22 |

(In

thousands of dollars, except per share amounts)

|

Summary

of Operations

|

|||||

|

For

the Year

|

2009

|

2008

|

2007

|

2006

|

2005

|

|

Water

operating revenue

|

$37,043

|

$32,838

|

$31,433

|

$28,658

|

$26,805

|

|

Operating

expenses *

|

19,655

|

18,158

|

17,333

|

15,754

|

14,049

|

|

Operating

income *

|

17,388

|

14,680

|

14,100

|

12,904

|

12,756

|

|

Interest

expense

|

4,780

|

4,112

|

3,916

|

3,727

|

3,423

|

|

Other

income (expenses), net *

|

(517)

|

(509)

|

(78)

|

110

|

(117)

|

|

Income

before income taxes

|

12,091

|

10,059

|

10,106

|

9,287

|

9,216

|

|

Income

taxes

|

4,579

|

3,628

|

3,692

|

3,196

|

3,383

|

|

Net

income

|

$

7,512

|

$

6,431

|

$

6,414

|

$

6,091

|

$

5,833

|

|

Per

Share of Common Stock

|

|||||

|

Book

value

|

$6.92

|

$6.14

|

$5.97

|

$5.84

|

$4.85

|

|

Basic

earnings per share

|

0.64

|

0.57

|

0.57

|

0.58

|

0.56

|

|

Dividends

declared per share

|

0.506

|

0.489

|

0.475

|

0.454

|

0.424

|

|

Weighted

average number of shares

|

|||||

|

outstanding

during the year

|

11,695,155

|

11,298,215

|

11,225,822

|

10,475,173

|

10,359,374

|

|

Utility

Plant

|

|||||

|

Original

cost,

|

|||||

|

net

of acquisition adjustments

|

$259,839

|

$245,249

|

$222,354

|

$202,020

|

$181,756

|

|

Construction

expenditures

|

12,535

|

24,438

|

18,154

|

20,678

|

15,562

|

|

Other

|

|||||

|

Total

assets

|

$248,837

|

$240,442

|

$210,969

|

$196,064

|

$172,296

|

|

Long-term

debt

|

|||||

|

including

current maturities

|

77,568

|

86,353

|

70,505

|

62,335

|

51,874

|

*Certain

prior year amounts have been reclassified to conform to the 2009

presentation.

For

Management's Discussion and Analysis of Financial Condition and Results of

Operations, please refer to page 4.

Market

for Common Stock and Dividends

The

common stock of The York Water Company is traded on the NASDAQ Global Select

Market (Symbol “YORW”). Quarterly price ranges and cash dividends per

share for the last two years follow:

|

2009

|

2008

|

|||||

|

High

|

Low

|

Dividend*

|

High

|

Low

|

Dividend*

|

|

|

1st

Quarter

|

$13.50

|

$9.74

|

$0.126

|

$16.28

|

$14.19

|

$0.121

|

|

2nd

Quarter

|

16.26

|

11.75

|

0.126

|

16.50

|

14.51

|

0.121

|

|

3rd

Quarter

|

17.95

|

13.75

|

0.126

|

15.00

|

6.23

|

0.121

|

|

4th

Quarter

|

15.24

|

13.65

|

0.128

|

13.31

|

10.25

|

0.126

|

*Cash

dividends per share reflect dividends declared at each dividend

date.

Prices

listed in the above table are sales prices as listed on the NASDAQ Global Select

Market. Shareholders of record (excluding individual participants in

securities positions listings) as of December 31, 2009 numbered approximately

1,516.

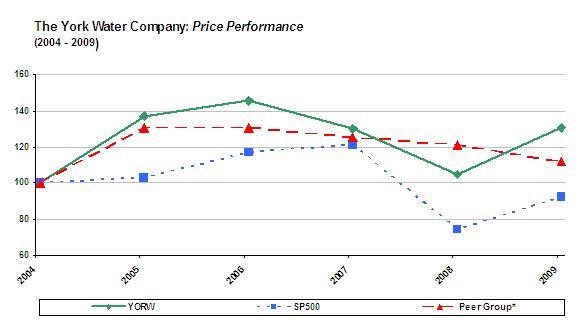

Performance

Graph

The

following line graph presents the annual and cumulative total shareholder return

for The York Water Company Common Stock over a five-year period from 2004

through 2009, based on the market price of the Common Stock and assuming

reinvestment of dividends, compared with the cumulative total shareholder return

of companies in the S&P 500 Index and a peer group made up of publicly

traded water utilities, also assuming reinvestment of dividends. The

peer group companies include: American States, Aqua America, Artesian

Resources, California Water Service, Connecticut Water Service, Middlesex Water,

Pennichuck Corporation, San Jose Water and Southwest Water.

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

|

|

The

York Water Company

|

100.00

|

136.99

|

145.72

|

129.93

|

105.04

|

130.61

|

|

S&P

500 Index

|

100.00

|

103.00

|

117.03

|

121.16

|

74.53

|

92.01

|

|

Peer

Group*

|

100.00

|

130.35

|

130.39

|

125.63

|

121.40

|

111.79

|

*ARTNA,

AWR, CTWS, CWT, MSEX, PNNW, SJW, SWWC, WTR

Source:

FactSet Research Systems Inc.

Dividend

Policy

Dividends

on the Company's common stock are declared by the Board of Directors and are

normally paid in January, April, July and October. Dividends are paid

based on shares outstanding as of the stated record date, which is ordinarily

the last day of the calendar month immediately preceding the dividend

payment.

The

dividend paid on the Company’s common stock on January 15, 2010 was the 556th

consecutive dividend paid by the Company. The Company has paid

consecutive dividends for its entire history, since 1816. The policy

of our Board of Directors is currently to pay cash dividends on a quarterly

basis. The dividend rate has been increased annually for thirteen

consecutive years. The Company’s Board of Directors declared dividend

number 557 in the amount of $0.128 per share at its January 2010

meeting. The dividend is payable on April 15, 2010 to shareholders of

record as of February 26, 2010. Future cash dividends will be

dependent upon the Company’s earnings, financial condition, capital demands and

other factors and will be determined by the Company’s Board of

Directors. See Note 4 to the Company’s financial statements included

herein for restrictions on dividend payments.

Financial

Reports and Investor Relations

Shareholders

may request, without charge, copies of the Company’s financial reports,

including Annual Reports, and Forms 8-K, 10-K and 10-Q filed with the Securities

and Exchange Commission (SEC). Such requests, as well as other

investor relations inquiries, should be addressed to:

|

Kathleen

M. Miller

|

The

York Water Company

|

(717)

845-3601

|

|

Chief

Financial Officer

|

P.

O. Box 15089

|

(800)

750-5561

|

|

York,

PA 17405-7089

|

kathym@yorkwater.com

|

The

Annual Report as well as reports filed with the SEC and other information about

the Company can also be found on the Company's website at: www.yorkwater.com.

of

Financial Condition and Results of Operations

(In

thousands of dollars, except per share amounts)

Forward-looking

Statements

This

Annual Report contains certain matters which are not historical facts, but which

are forward-looking statements. Words such as "may," "should,"

"believe," "anticipate," "estimate," "expect," "intend," "plan" and similar

expressions are intended to identify forward-looking statements. The

Company intends these forward-looking statements to qualify for safe harbor from

liability established by the Private Securities Litigation Reform Act of

1995. These forward-looking statements include certain information

relating to the Company's business strategy; statements including, but not

limited to:

|

|

·

|

expected

profitability and results of

operations;

|

|

|

·

|

goals,

priorities and plans for, and cost of, growth and

expansion;

|

|

|

·

|

strategic

initiatives;

|

|

|

·

|

availability

of water supply;

|

|

|

·

|

water

usage by customers; and

|

|

|

·

|

ability

to pay dividends on common stock and the rate of those

dividends.

|

The

forward-looking statements in this Annual Report reflect what the Company

currently anticipates will happen. What actually happens could differ

materially from what it currently anticipates will happen. The

Company does not intend to make any public announcement when forward-looking

statements in this Annual Report are no longer accurate, whether as a result of

new information, what actually happens in the future or for any other

reason. Important matters that may affect what will actually happen

include, but are not limited to:

|

|

·

|

changes

in weather, including drought

conditions;

|

|

|

·

|

levels

of rate relief granted;

|

|

|

·

|

the

level of commercial and industrial business activity within the Company's

service territory;

|

|

|

·

|

construction

of new housing within the Company's service territory and increases in

population;

|

|

|

·

|

changes

in government policies or

regulations;

|

|

|

·

|

the

ability to obtain permits for expansion

projects;

|

|

|

·

|

material

changes in demand from customers, including the impact of conservation

efforts which may impact the demand of customers for

water;

|

|

|

·

|

changes

in economic and business conditions, including interest rates, which are

less favorable than expected;

|

|

|

·

|

the

ability to obtain financing; and

|

|

|

·

|

other

matters set forth in Item 1A, “Risk Factors,” of the Company's Annual

Report on Form 10-K for the year ended December 31,

2009.

|

Overview

The

Company is the oldest investor-owned water utility in the United States and is

duly organized under the laws of the Commonwealth of

Pennsylvania. The Company has operated continuously since

1816. The business of the Company is to impound, purify to meet or

exceed safe drinking water standards and distribute water. The

Company operates within its franchised territory, which covers 39 municipalities

within York County, Pennsylvania and seven municipalities within Adams County,

Pennsylvania. The Company is regulated by the Pennsylvania Public

Utility Commission, or PPUC, in the areas of billing, payment procedures,

dispute processing, terminations, service territory, debt and equity financing

and rate setting. The Company must obtain PPUC approval before

changing any practices associated with the aforementioned

areas. Water service is supplied through the Company's own

distribution system. The Company obtains its water supply from both

the South Branch and East Branch of the Codorus Creek, which together have an

average daily flow of 73.0 million gallons per day. This combined

watershed area is approximately 117 square miles. The Company has two

reservoirs, Lake Williams and Lake Redman, which together hold up to

approximately 2.2 billion gallons of water. The Company has a 15-mile

pipeline from the Susquehanna River to Lake Redman which provides access to an

additional supply of 12.0 million gallons of untreated water per

day. As of December 31, 2009, the Company's average daily

availability was 35.0 million gallons, and daily consumption was approximately

18.2 million gallons. The Company's service territory had an

estimated population of 180,000 as of December 31, 2009. Industry

within the Company's service territory is diversified, manufacturing such items

as fixtures and furniture, electrical machinery, food products, paper, ordnance

units, textile products, air conditioning systems, laundry detergent, barbells

and motorcycles.

The

Company's business is somewhat dependent on weather conditions, particularly the

amount of rainfall. Revenues are particularly vulnerable to weather

conditions in the summer months. Prolonged periods of hot and dry

weather generally cause increased water usage for watering lawns, washing cars,

and keeping golf courses and sports fields irrigated. Conversely,

prolonged periods of dry weather could lead to drought restrictions from

governmental authorities. Despite the Company's adequate water

supply, customers may be required to cut back water usage under such drought

restrictions which would negatively impact our revenues. The Company

has addressed some of this vulnerability by instituting minimum customer charges

which are intended to cover fixed costs of operations under all likely weather

conditions. In 2009, reduced water consumption, rainfall patterns and

a sluggish economy have combined to reduce per capita consumption by industrial,

commercial and residential customers by approximately 5.7% compared to

2008. If this downward trend continues, the Company's revenues would

be diminished in the short term, making timely and adequate rate filings even

more important.

The

Company's business does not require large amounts of working capital and is not

dependent on any single customer or a very few customers for a material portion

of its business. In 2009, operating revenue was derived from the

following sources and in the following percentages: residential, 63%; commercial

and industrial, 29%; and other, 8%, which is primarily from the provision for

fire service. Increases in revenues are generally dependent on the

Company's ability to obtain rate increases from regulatory authorities in a

timely manner and in adequate amounts and to increase volumes of water sold

through increased consumption and increases in the number of customers

served. The Company continuously looks for acquisition and expansion

opportunities both within and outside its current service

territory. The Company also looks for additional opportunities to

enter into bulk water contracts with municipalities and other entities to supply

water.

During

the five-year period ended December 31, 2009, the Company has maintained an

increasing growth in the number of customers and distribution facilities as

demonstrated by the following chart:

|

2009

|

2008

|

2007

|

2006

|

2005

|

|

|

Average

daily consumption (gallons per day)

|

18,233,000

|

18,298,000

|

19,058,000

|

18,769,000

|

18,657,000

|

|

Miles

of mains at year-end

|

938

|

884

|

845

|

817

|

786

|

|

Additional

distribution

mains

installed/acquired (ft.)

|

286,326

|

206,140

|

147,803

|

159,330

|

212,702

|

|

Number

of customers at year-end

|

62,186

|

61,527

|

58,890

|

57,578

|

55,731

|

|

Population

served at year-end

|

180,000

|

176,000

|

171,000

|

166,000

|

161,000

|

Performance

Measures

Company

management uses financial measures including operating revenues, net income,

earnings per share and return on equity to evaluate its financial

performance. Additional statistical measures including number of

customers, customer complaint rate, annual customer rates and the efficiency

ratio are used to evaluate performance quality. These measures are

calculated on a regular basis and compared with historical information, budget

and the other publicly-traded water companies.

The

Company's 2009 performance was strong under most of the above

measures. Effective October 9, 2008, the PPUC authorized an increase

in rates which allowed the Company to recover some of the increasing expenses

and offset some of the declining per capita water usage by our

customers. In 2009, we issued 1,070,000 additional shares of common

stock through an underwritten public offering. Despite an increase in

net income in 2009 over 2008 of 16.8%, return on equity on year end common

equity fell due to dilution.

The

efficiency ratio, which is calculated as net income divided by revenues, is used

by management to evaluate its ability to keep expenses in line. Over

the five previous years, our ratio averaged 21.3%. In 2009, the ratio

fell slightly to 20.3% due to reduced per capita water usage by our customers

which caused water usage revenues to decline, but not expenses, and increased

expenses, some of which had not yet been included in rates charged to

customers. Despite the reduction in the efficiency ratio, management

is confident that our ratio will again exceed that of our peers. Management continues to

look for ways to decrease expenses and increase efficiency as well as to file

for rate increases promptly when needed.

Results

of Operations

2009

Compared with 2008

Net

income for 2009 was $7,512, an increase of $1,081, or 16.8%, from net income of

$6,431 for 2008. The primary contributing factors to the increase in

net income were higher water revenues which were partially offset by increased

depreciation, higher pension cost, reduced interest capitalized, increased

interest expense on debt and higher salary and wage expense.

Water

operating revenues for the year increased $4,205, or 12.8%, from $32,838 for

2008 to $37,043 for 2009. The primary reasons for the increase in

revenues were a rate increase of 17.9% effective October 9, 2008 and growth in

the customer base. The average number of customers served in 2009

increased as compared to 2008 by 2,414 customers, from 59,483 to 61,897

customers. Approximately 2,050 of the additional customers were due

to the Asbury Pointe and West Manheim acquisitions. Despite this

increase in customers, the total per capita volume of water sold in 2009

decreased compared to 2008 by approximately 5.7%. The largest decline

occurred in the industrial category followed by the commercial and residential

categories. The reduction is attributed to, among other things, a

sluggish economy and rainfall patterns. The Company expects revenues

to remain consistent as the impact of new customers is expected to be offset by

the decline in per capita consumption. Drought warnings or

restrictions as well as regulatory actions could impact results.

Operating

expenses for the year increased $1,497, or 8.2%, from $18,158 for 2008 to

$19,655 for 2009. The increase was primarily due to higher

depreciation of $790 due to increased plant investment, increased pension

expense of $487, higher salary and wage expense of $229 due mainly to the

increased vacation accrual discussed in Note 1 (Reclassifications) and higher

distribution system maintenance expense, chemical expense, power costs, rate

case expense, provision for doubtful accounts, banking fees, realty taxes and

other expenses aggregating approximately $482. The increase was

partially offset by reduced health insurance costs, increased capitalized

overhead, lower transportation expenses and reduced software support and legal

expenses aggregating approximately $491. Depreciation expenses are

expected to continue to rise due to investment in plant and other operating

expenses are expected to increase at a moderate rate as costs to serve customers

and to extend our distribution system continue to rise.

Interest

on debt for 2009 increased $231, or 4.9%, from $4,759 for 2008 to $4,990 for

2009. Interest on the Company's long-term debt increased by $706 due

to an increase in the amount of long-term debt outstanding from new debt issued

on October 15, 2008 in the aggregate principal amount of $15,000 at an interest

rate of 6%. The increased expenses were partially offset by lower

interest on the $12,000 variable rate bonds of approximately $69 due to lower

variable interest rates. Interest on the Company's lines of credit

decreased by $346 due to lower interest rates. The average interest

rate on the lines of credit was 1.41% for 2009 compared to 3.61% for

2008. The average debt outstanding under the lines of credit was

$16,848 for 2009 and $16,128 for 2008. Other long-term interest

decreased $60.

Allowance

for funds used during construction decreased $437, from $647 for 2008 to $210 in

2009, due to a lower volume of eligible construction. Eligible 2008

construction expenditures included an investment in a large water treatment

replacement and expansion project and a main extension to West Manheim Township

that was placed in service in December, 2008.

Other

income (expenses), net for 2009 reflects increased expenses of $8 as compared to

2008. The increase was primarily due to increased charitable

contributions, higher debt cost amortization and other expenses which were

partially offset by reduced retirement expenses.

Income

taxes for 2009 increased by $951, or 26.2%, compared to 2008, primarily due to

an increase in taxable income. The Company's effective tax rate was

37.9% in 2009 and 36.1% in 2008. The increase in the effective tax

rate was due to taxable gains on the surrender of life insurance policies and

bonus depreciation initially being taxable for state tax purposes.

2008

Compared with 2007

Net

income for 2008 was $6,431, an increase of $17, or 0.3%, from net income of

$6,414 for 2007. The primary contributing factors to the increase in

net income were higher water operating revenues partially offset by increased

operating and retirement expenses.

Water

operating revenues for the year increased $1,405, or 4.5%, from $31,433 for 2007

to $32,838 for 2008. The primary reasons for the increase in revenues

were a rate increase effective October 9, 2008, an increased distribution

surcharge through the first three quarters and growth in the customer

base. The average number of customers served in 2008 increased as

compared to 2007 by 993 customers, from 58,490 to 59,483 customers due to growth

in the Company's service territory. The total number of customers

added during the year was approximately 2,600 with approximately 250 of those

customers added in November due to the Asbury Pointe acquisition and

approximately 1,800 customers added in December due to the West Manheim

acquisition. Despite this increase in customers, the total per capita

volume of water sold in 2008 decreased compared to 2007 by approximately

4.1%. Reduced consumption is attributed to a sluggish economy and

increased rainfall.

Operating

expenses for the year increased $825, or 4.8%, from $17,333 for 2007 to $18,158

for 2008. Higher depreciation expense of approximately $395 due to

increased plant investment, increased health insurance costs of approximately

$136, higher banking fees of approximately $103 related to lockbox processing

and credit enhancement, increased pension expense of approximately $96 and

higher salaries of approximately $87 due to wage increases were the principal

reasons for the increase. Higher power costs, legal fees, realty

taxes, transportation costs, director fees and other expenses aggregating

approximately $353 also added to the increase. The increase in

expenses was partially offset by lower software support expenses of

approximately $209, reduced chemical expenses of approximately $89 and lower

shareholder costs of approximately $47.

Interest

on debt for 2008 increased $615, or 14.8%, from $4,144 for 2007 to $4,759 for

2008. Interest on the Company's lines of credit increased by $329 due

to increased borrowings to fund operations and construction. The

average interest rate on the lines of credit was 3.61% for 2008 compared to

5.96% for 2007. The average debt outstanding under the lines of

credit was $16,128 for 2008 and $3,898 for 2007. Interest on the

Company's long-term debt increased by $192 due to an increase in the amount of

long-term debt outstanding from new debt issued on October 15, 2008 in the

aggregate principal amount of $15,000 at an interest rate of

6%. Interest on the $12,000 variable rate bonds increased $58 and

other long-term interest increased $36.

Allowance

for funds used during construction increased $419, from $228 in 2007 to $647 in

2008, due to an increased volume of construction

expenditures. Eligible 2008 construction expenditures included an

investment in a large water treatment replacement and expansion project and a

main extension to West Manheim Township.

Other

income (expenses), net for 2008 reflects increased expenses of $431 as compared

to 2007. The increase was primarily due to higher retirement expenses

of approximately $479. The additional expense resulted from changes

to the plans to make them compliant with Internal Revenue Code Section 409A and

a reduction in the discount rate used in recording the present value of the

benefits. The increase in expenses was partially offset by higher

interest income in 2008 of approximately $53 on water district notes

receivable. Interest income on water district notes receivable in the

first nine months of 2007 included a negative adjustment (expense) due to the

recalculation of a note. Decreased charitable contributions of

approximately $25 also reduced other expenses.

Income

taxes for 2008 decreased by $64, or 1.7%, compared to 2007 primarily due to a

decrease in taxable income. The Company's effective tax rate was

36.1% in 2008 and 36.5% in 2007.

Rate

Developments

From time

to time, the Company files applications for rate increases with the PPUC and is

granted rate relief as a result of such requests. The most recent

rate request was filed by the Company on May 16, 2008 and sought an increase of

$7,086, which would have represented a 19.6% increase in

rates. Effective October 9, 2008, the PPUC authorized an increase in

rates designed to produce approximately $5,950 in additional annual

revenues. The Company anticipates that it will file a rate increase

request in 2010.

Acquisitions

See Note

2 to the Company's financial statements included herein for a discussion of our

acquisitions.

Capital

Expenditures

During

2009, the Company invested $12,535 in construction expenditures for routine

items as well as an additional standpipe and booster station, various

replacements of aging infrastructure, and a main extension to support our

westward expansion. In addition to construction projects, we invested

approximately $2,236 for the acquisition of West Manheim and Beaver Creek

Village water systems and additional expenditures relating to the Asbury Pointe

water system. The Company was able to fund operating activities and

construction expenditures using internally-generated funds, borrowings against

the Company's lines of credit, an underwritten common stock offering, proceeds

from its stock purchase plans (see Note 5 to the Company's financial statements

included herein), customer advances and the distribution surcharge (DSIC)

allowed by the PPUC. The distribution surcharge allows the Company to

add a charge to customers’ bills for qualified replacement costs of certain

infrastructure without submitting a rate filing.

The

Company anticipates construction and acquisition expenditures for 2010 and 2011

of approximately $12,740 and $13,926, respectively. In addition to

routine transmission and distribution projects, a portion of the anticipated

2010 and 2011 expenditures will be for additional standpipes, further upgrades

to water treatment facilities, reinforcement of one of our dams, and various

replacements of aging infrastructure. We intend to use

internally-generated funds for at least half of our anticipated 2010 and 2011

construction and fund the remainder through line of credit borrowings, proceeds

from our stock purchase plans or public offerings, possible long-term debt

offerings, the DSIC and customer advances and contributions (see Note 1 to the

Company's financial statements included herein). Customer advances

and contributions are expected to account for approximately 5% of funding

requirements in 2010 and 15% of funding requirements in 2011. We

believe we will have adequate access to the capital markets, if necessary during

2010, to fund anticipated construction and acquisition

expenditures.

Liquidity

and Capital Resources

Cash

Although

the Company is able to generate funds internally through customer bill payments,

we have not historically maintained cash on the balance sheet. The

Company manages its cash through a cash management account that is directly

connected to a line of credit. Excess cash generated automatically

pays down outstanding borrowings under the line of credit

arrangement. If there are no outstanding borrowings, the cash is

automatically invested in an interest-bearing account

overnight. Likewise, if additional funds are needed, besides what is

generated internally, for payroll, to pay suppliers, or to pay debt service,

funds are automatically borrowed under the line of credit. The cash

management facility has historically provided the necessary liquidity and

funding for our operations and we expect that to continue to be the case for the

foreseeable future.

Internally-generated

Funds

The

amount of internally-generated funds available for operations and construction

depends on our ability to obtain timely and adequate rate relief, our customers’

water usage, weather conditions, customer growth and controlled

expenses. In 2009, we generated $15,801 internally as compared to

$11,527 in 2008 and $10,040 in 2007. A successful rate increase

request, the addition of approximately 2,600 customers and increased

depreciation and deferred income taxes, which are non-cash expenses, helped to

increase cash flow from operating activities during 2009. In addition

to internally-generated funds, we used our bank lines of credit and proceeds

from an underwritten common stock offering to help fund operations and

construction.

Credit

Lines

Historically,

the Company has borrowed $15,000 to $20,000 under its lines of credit before

refinancing with long-term debt or equity capital. As of December 31,

2009, the Company maintained unsecured lines of credit aggregating $33,000 with

three banks. One line of credit includes a $4,000 portion which is

payable upon demand and carries an interest rate of 4.00% or LIBOR plus 0.70%,

whichever is greater, and a $13,000 committed portion with a revolving 2-year

maturity (currently May 2011), which carries an interest rate of LIBOR plus

0.70%. In January 2010, we signed a renewal for this line of credit

which eliminated the 4.00% interest rate floor on the on-demand portion and

raised the interest rate on both portions to LIBOR plus 2.00%. The

Company had $3,054 in outstanding borrowings under the committed portion and no

on-demand borrowings under this line of credit as of December 31,

2009. The second line of credit, in the amount of $11,000, is a

committed line of credit, which matures in May 2010 and carries an interest rate

of LIBOR plus 1.50%. This line of credit has a compensating balance

requirement of $500. The Company had $3,000 in outstanding borrowings

under this line of credit as of December 31, 2009. The third line of

credit, in the amount of $5,000, is a committed line of credit, which matures in

April 2010 and carries an interest rate of LIBOR plus 2.00%. The

Company had $2,000 in outstanding borrowings under this line of credit as of

December 31, 2009. The weighted average interest rate on line of

credit borrowings as of December 31, 2009 was 1.56% compared to 2.32% as of

December 31, 2008. The Company plans to renew the lines of credit

that expire in 2010 under similar terms and conditions.

The

credit and liquidity crisis which began in 2008 has caused substantial

volatility and uncertainty in the capital markets and in the banking industry

resulting in increased borrowing costs and reduced credit

availability. While actual interest rates are currently low, one of

our banks has recently increased the interest rate on our line of credit from

LIBOR plus 70 basis points to LIBOR plus 200 basis points. Although

we have taken steps to manage the risk of reduced credit availability such as

maintaining primarily committed lines of credit that cannot be called on demand

and obtaining a 2-year revolving maturity, there is no guarantee that we will be

able to obtain sufficient lines of credit with favorable terms in the

future. In addition, if we are unable to refinance our line of credit

borrowings with long-term debt or equity when necessary, we may have to

eliminate or postpone capital expenditures. We believe we will have

adequate capacity under our current lines of credit to meet our financing needs

throughout 2010.

Long-term

Debt

The

Company's loan agreements contain various covenants and

restrictions. We believe we are currently in compliance with all of

these restrictions. See Note 4 to the Company's financial statements

included herein for additional information regarding these

restrictions.

The 3.6%

Industrial Development Authority Revenue Refunding Bonds, Series 1994, had a

mandatory tender date of May 15, 2009. The Company retired the $2,700

bonds using funds available under its lines of credit. The 3.75%

Industrial Development Authority Revenue Refunding Bonds, Series 1995, have a

mandatory tender date of June 1, 2010. The Company currently plans to meet its

$4,300 obligation using funds available under its lines of credit or a potential

debt issuance.

The

Company's debt (long-term debt plus current portion of long-term debt) as a

percentage of the total capitalization, defined as total common stockholders’

equity plus long-term debt (including current portion of long-term debt), was

47.2% as of December 31, 2009, compared with 55.3% as of December 31,

2008. While our debt load has trended upward over the years, we have

historically matched increasing debt with increasing equity so that our debt to

total capitalization ratio was nearly fifty percent. This capital

structure has historically been acceptable to the PPUC in that prudent debt

costs and a fair return have been granted by the PPUC in rate

filings. The economic downturn during the latter part of 2008 delayed

the matching increase in equity, resulting in a higher debt ratio and increased

borrowings under our lines of credit. The improved market conditions

in 2009 allowed the Company to complete an underwritten common stock offering

and reduce the percentage of debt in its capital structure. See Note

4 to the Company's financial statements included herein for the details of our

long-term debt outstanding as of December 31, 2009.

Common

Stock

In

September 2009, the Company closed an underwritten public offering of 950,000

shares of its common stock. In October 2009, the underwriters

exercised an over-allotment of 120,000 shares. Boenning &

Scattergood, Inc. and J.J.B. Hilliard, W.L. Lyons, LLC were the underwriters in

the offering. The Company received net proceeds in the offering,

after deducting offering expenses and underwriter’s discounts and commissions,

of approximately $14.1 million. The net proceeds were used to repay a

portion of the Company's borrowings under its line of credit agreements incurred

to fund capital expenditures and acquisitions, and for general corporate

purposes.

Common

stockholders’ equity as a percent of the total capitalization was 52.8% as of

December 31, 2009, compared with 44.7% as of December 31, 2008. It is

the Company's intent to maintain a ratio near fifty percent. Economic

conditions in 2008 caused us to modify our plans to issue common stock due to a

reduced stock price, the potential inability to raise the needed funds and the

prospect of further dilution to our stock value. The improved market

conditions in 2009 allowed the Company to complete an underwritten common stock

offering and increase the percentage of common stockholders’ equity in its

capital structure. We have the ability to issue additional shares of

the Company's common stock in the future under a shelf Registration Statement on

Form S-3 filed with the Securities and Exchange Commission on April 28,

2009.

Credit

Rating

On March

26, 2009, Standard and Poor’s affirmed our credit rating at A-, with a stable

outlook. Our ability to maintain this rating depends, among other

things, on adequate and timely rate relief, which we have been successful in

obtaining, and our ability to fund capital expenditures in a balanced manner

using both debt and equity. In 2010, our objectives will be to

continue to maximize our funds provided by operations and maintain the equity

component of total capitalization.

Dividends

During

2009, the Company's dividend payout ratios relative to net income and cash

provided by operating activities were 80.5% and 37.0%,

respectively. During the fourth quarter of 2009, the Board of

Directors increased the dividend by 1.6% from $0.126 per share to $0.128 per

share per quarter. This was the thirteenth consecutive annual

dividend increase and the 194th consecutive year of paying

dividends.

The

Company's Board of Directors declared a dividend in the amount of $0.128 per

share at its January 2010 meeting. The dividend is payable on April

15, 2010 to shareholders of record as of February 26, 2010. While the

Company expects to maintain this dividend amount in 2010, future dividends will

be dependent upon the Company's earnings, financial condition, capital demands

and other factors and will be determined by the Company's Board of

Directors. See Note 4 to the Company's financial statements included

herein for restrictions on dividend payments.

Inflation

The

Company is affected by inflation, most notably by the continually increasing

costs incurred to maintain and expand its service capacity. The

cumulative effect of inflation results in significantly higher facility

replacement costs which must be recovered from future cash flows. The

ability of the Company to recover this increased investment in facilities is

dependent upon future rate increases, which are subject to approval by the

PPUC. The Company can provide no assurances that its rate increases

will be approved by the PPUC; and, if approved, the Company cannot guarantee

that these rate increases will be granted in a timely or sufficient manner to

cover the investments and expenses for which the rate increase was

sought.

Contractual

Obligations

The

following summarizes the Company's contractual obligations by period as of

December 31, 2009:

|

Payments

due by period

|

|||||||

|

Total

|

2010

|

2011

|

2012

|

2013

|

2014

|

Thereafter

|

|

|

Long-term

debt obligations (a)

|

$77,568

|

$4,341

|

$15,095

|

$42

|

$42

|

$43

|

$58,005

|

|

Interest

on long-term debt (b)

|

66,676

|

4,188

|

4,121

|

4,120

|

4,120

|

4,119

|

46,008

|

|

Short-term

borrowings (c)

|

5,000

|

5,000

|

-

|

-

|

-

|

-

|

-

|

|

Purchase

obligations (d)

|

1,756

|

1,756

|

-

|

-

|

-

|

-

|

-

|

|

Defined

benefit obligations (e)

|

1,218

|

1,218

|

-

|

-

|

-

|

-

|

-

|

|

Deferred

employee benefits (f)

|

4,489

|

229

|

224

|

236

|

226

|

235

|

3,339

|

|

Other

deferred credits (g)

|

1,161

|

343

|

241

|

154

|

99

|

57

|

267

|

|

Total

|

$157,868

|

$17,075

|

$19,681

|

$4,552

|

$4,487

|

$4,454

|

$107,619

|

|

(a)

|

Represents

debt maturities including current maturities. Included in the

table is a payment of $12,000 in 2011 on the variable rate bonds which

would only be due if the bonds were unable to be

remarketed. There is currently no indication of this

happening.

|

|

(b)

|

Excludes

interest on the $12,000 variable rate debt as these payments cannot be

reasonably estimated. The interest rate on this issue is reset

weekly by the remarketing agent based on then current market

conditions. Also excludes interest on the committed line of

credit due to the variability of both the outstanding amount and the

interest rate.

|

|

(c)

|

Represents

obligations under the Company's short-term lines of

credit.

|

|

(d)

|

Represents

an approximation of open purchase orders at year end.

|

|

(e)

|

Represents

contributions expected to be made to qualified defined benefit

plans. The amount of required contributions in 2011 and

thereafter is not currently determinable.

|

|

(f)

|

Represents

the obligations under the Company's Supplemental Retirement and Deferred

Compensation Plans for executives.

|

|

(g)

|

Represents

the estimated settlement payments to be made under the Company's interest

rate swap contract.

|

In

addition to these obligations, the Company makes refunds on Customers’ Advances

for Construction over a specific period of time based on operating revenues

related to developer-installed water mains or as new customers are connected to

and take service from such mains. The refund amounts are not included

in the above table because the timing cannot be accurately

estimated. Portions of these refund amounts are payable annually

through 2020 and amounts not paid by the contract expiration dates become

non-refundable and are transferred to Contributions in Aid of

Construction.

See Note

9 to the Company's financial statements included herein for a discussion of our

commitments.

Critical

Accounting Estimates

The

methods, estimates and judgments we use in applying our accounting policies have

a significant impact on the results we report in our financial

statements. Our accounting policies require us to make subjective

judgments because of the need to make estimates of matters that are inherently

uncertain. Our most critical accounting estimates include: regulatory

assets and liabilities, revenue recognition and accounting for our pension

plans.

Regulatory

Assets and Liabilities

Generally

accepted accounting principles define professional standards for companies whose

rates are established by or are subject to approval by an independent

third-party regulator. In accordance with the professional standards,

the Company defers costs and credits on its balance sheet as regulatory assets

and liabilities when it is probable that these costs and credits will be

recognized in the rate-making process in a period different from when the costs

and credits were incurred. These deferred amounts are then recognized

in the statement of income in the period in which they are reflected in customer

rates. If the Company later finds that these assets and liabilities

cannot be included in rate-making, they are adjusted

appropriately. See Note 1 for additional details regarding regulatory

assets and liabilities.

Revenue

Recognition

Revenues

include amounts billed to metered customers on a cycle basis and unbilled

amounts based on both actual and estimated usage from the latest meter reading

to the end of the accounting period. Estimates are based on average

daily usage for those particular customers. The unbilled revenue

amount is recorded as a current asset on the balance sheet. Actual

results could differ from these estimates and would result in operating revenues

being adjusted in the period in which the actual usage is

known. Based on historical experience, the Company believes its

estimate of unbilled revenues is reasonable.

Pension

Accounting

Accounting

for defined benefit pension plans requires estimates of future compensation

increases, mortality, the discount rate, and expected return on plan assets as

well as other variables. These variables are reviewed annually with

the Company's pension actuary. The Company selected its December 31,

2009 and 2008 discount rates based on the Citigroup Pension Liability

Index. This index uses the Citigroup spot rates for durations out to

30 years and matches them to expected disbursements from the plan over the long

term. The Company believes this index most appropriately matches its

pension obligations. The present values of the Company's future

pension obligations were determined using a discount rate of 6.0% at December

31, 2009 and 2008.

Choosing

a lower discount rate normally increases the amount of pension expense and the

corresponding liability. In the case of the Company, a reduction in

the discount rate would increase its liability, but would not have an impact on

its pension expense. The PPUC, in a previous rate settlement, agreed

to grant recovery of the Company's contribution to the pension plans in customer

rates. As a result, under the professional standards, expense in

excess of the Company's pension plan contribution is deferred as a regulatory

asset and will be expensed as contributions are made to the plans and the

contributions are recovered in customer rates. Therefore, changes in

the discount rate affect regulatory assets rather than pension

expense.

The

Company's estimate of the expected return on plan assets is primarily based on

the historic returns and projected future returns of the asset classes

represented in its plans. The target allocation of pension assets is

50% to 70% equity securities, 30% to 50% debt securities, and 0% to 10%

reserves. The Company used 7% as its estimate of expected return on

assets in both 2009 and 2008. If the Company were to reduce the

expected return, its liability would increase, but its expense would again

remain unchanged because the expense is equal to the Company's contribution to

the plans. The additional expense would instead be recorded as an

increase to regulatory assets.

Other

critical accounting estimates are discussed in the Significant Accounting

Policies Note to the Financial Statements.

Off-Balance

Sheet Transactions

The

Company does not use off-balance sheet transactions, arrangements or obligations

that may have a material current or future effect on financial condition,

results of operations, liquidity, capital expenditures, capital resources or

significant components of revenues or expenses. The Company does not

use securitization of receivables or unconsolidated entities. The Company does

not engage in trading or risk management activities, with the exception of the

interest rate swap agreement discussed in Note 4 to the financial statements,

does not use derivative financial instruments for speculative trading purposes,

has no lease obligations, no guarantees and does not have material transactions

involving related parties.

Impact

of Recent Accounting Pronouncements

See Note

1 to the Company's financial statements included herein for a discussion on the

effect of new accounting pronouncements.

Management’s

Report on Internal Control Over Financial Reporting

Management

of The York Water Company (the “Company”) is responsible for establishing and

maintaining adequate internal control over financial reporting. Internal control

over financial reporting is a process designed to provide reasonable assurance

regarding the reliability of financial reporting and the preparation of

financial statements for external purposes in accordance with generally accepted

accounting principles. A Company's internal control over financial reporting

includes those policies and procedures that pertain to the maintenance of

records that, in reasonable detail, accurately and fairly reflect the

transactions and dispositions of the assets of the company; provide reasonable

assurance that transactions are recorded as necessary to permit preparation of

financial statements in accordance with generally accepted accounting

principles, and that receipts and expenditures of the company are being made

only in accordance with authorizations of management and directors of the

company; and provide reasonable assurance regarding prevention or timely

detection of unauthorized acquisition, use, or disposition of the

company's assets that could have a material effect on the financial

statements.

Because

of its inherent limitations, internal control over financial reporting may not

prevent or detect misstatements. Also, projections of any evaluation of

effectiveness to future periods are subject to the risk that controls may become

inadequate because of changes in conditions, or that the degree of compliance

with the policies or procedures may deteriorate.

Management

evaluated the Company's internal control over financial reporting as of December

31, 2009. In making this assessment, management used the criteria set forth by

the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control-Integrated

Framework (COSO). As a result of this assessment and based on the

criteria in the COSO framework, management has concluded that, as of December

31, 2009, the Company’s internal control over financial reporting was

effective.

The

Company’s independent auditors, ParenteBeard LLC, have audited the Company’s

internal control over financial reporting. Their opinions on the Company’s

internal control over financial reporting and on the Company’s financial

statements appear on the following pages of this annual report.

|

/s/Jeffrey

R. Hines

|

/s/Kathleen

M. Miller

|

||

|

Jeffrey

R. Hines

|

Kathleen

M. Miller

|

||

|

President,

Chief Executive Officer

|

Chief

Financial Officer

|

March 11,

2010

Report

of Independent Registered Public Accounting Firm

To the

Board of Directors and

Stockholders

of The York Water Company

We have

audited The York Water Company’s internal control over financial reporting as of

December 31, 2009, based on criteria established in Internal Control—Integrated

Framework issued by the Committee of Sponsoring Organizations of the

Treadway Commission (COSO). The York Water Company’s management is

responsible for maintaining effective internal control over financial reporting

and for its assessment of the effectiveness of internal control over financial

reporting included in the accompanying Management’s Report on Internal Control

over Financial Reporting. Our responsibility is to express an opinion

on the Company’s internal control over financial reporting based on our

audit.

We

conducted our audit in accordance with the standards of the Public Company

Accounting Oversight Board (United States). Those standards require

that we plan and perform the audit to obtain reasonable assurance about whether

effective internal control over financial reporting was maintained in all

material respects. Our audit of internal control over financial

reporting included obtaining an understanding of internal control over financial

reporting, assessing the risk that a material weakness exists, and testing and

evaluating the design and operating effectiveness of internal control based on

the assessed risk. Our audit also included performing such other

procedures as we considered necessary in the circumstances. We

believe that our audit provides a reasonable basis for our opinion.

A

company’s internal control over financial reporting is a process designed to

provide reasonable assurance regarding the reliability of financial reporting

and the preparation of financial statements for external purposes in accordance

with generally accepted accounting principles. A company’s internal

control over financial reporting includes those policies and procedures that

(1) pertain to the maintenance of records that, in reasonable detail,

accurately and fairly reflect the transactions and dispositions of the assets of

the Company; (2) provide reasonable assurance that transactions are

recorded as necessary to permit preparation of financial statements in

accordance with generally accepted accounting principles, and that receipts and

expenditures of the Company are being made only in accordance with

authorizations of management and directors of the Company; and (3) provide

reasonable assurance regarding prevention or timely detection of unauthorized

acquisition, use, or disposition of the Company’s assets that could have a

material effect on the financial statements.

Because

of its inherent limitations, internal control over financial reporting may not

prevent or detect misstatements. Also, projections of any evaluation

of effectiveness to future periods are subject to the risk that controls may

become inadequate because of changes in conditions, or that the degree of

compliance with the policies or procedures may deteriorate.

In our

opinion, The York Water Company maintained, in all material respects, effective

internal control over financial reporting as of December 31, 2009, based on

criteria established in Internal Control—Integrated

Framework issued by the Committee of Sponsoring Organizations of the

Treadway Commission (COSO).

We have

also audited, in accordance with the standards of the Public Company Accounting

Oversight Board (United States), the balance sheets and the related statements

of income, common stockholders’ equity and comprehensive income, and cash flows

of The York Water Company, and our report dated March 11, 2010 expressed an

unqualified opinion.

/s/ParenteBeard

LLC

ParenteBeard

LLC

York,

Pennsylvania

March 11,

2010

Report

of Independent Registered Public Accounting Firm

To the

Board of Directors and

Stockholders

of The York Water Company

We have

audited the accompanying balance sheets of The York Water Company as of

December 31, 2009 and 2008, and the related statements of income, common

stockholders’ equity and comprehensive income, and cash flows for each of the

years in the three-year period ended December 31, 2009. The York

Water Company’s management is responsible for these financial

statements. Our responsibility is to express an opinion on these

financial statements based on our audits.

We

conducted our audits in accordance with the standards of the Public Company

Accounting Oversight Board (United States). Those standards require

that we plan and perform the audit to obtain reasonable assurance about whether

the financial statements are free of material misstatement. An audit

includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also includes

assessing the accounting principles used and significant estimates made by

management, as well as evaluating the overall financial statement

presentation. We believe that our audits provide a reasonable basis

for our opinion.

In our

opinion, the financial statements referred to above present fairly, in all

material respects, the financial position of The York Water Company as of

December 31, 2009 and 2008, and the results of its operations and its cash flows

for each of the years in the three-year period ended December 31, 2009 in

conformity with accounting principles generally accepted in the United States of

America.

We also

have audited, in accordance with the standards of the Public Company Accounting

Oversight Board (United States), The York Water Company’s internal control over

financial reporting as of December 31, 2009, based on criteria established in

Internal Control—Integrated

Framework issued by the Committee of Sponsoring Organizations of the

Treadway Commission (COSO), and our report dated March 11, 2010 expressed an

unqualified opinion.

/s/ParenteBeard

LLC

ParenteBeard

LLC

York,

Pennsylvania

March 11,

2010

|

Balance

Sheets

|

|||||||||

|

(In

thousands of dollars, except per share amounts)

|

|||||||||

| December 31 | |||||||||

|

2009

|

2008

|

||||||||

|

ASSETS

|

|||||||||

|

UTILITY

PLANT, at original cost

|

$ | 262,598 | $ | 246,613 | |||||

|

Plant

acquisition adjustments

|

(2,759 | ) | (1,364 | ) | |||||

|

Accumulated

depreciation

|

(38,364 | ) | (34,429 | ) | |||||

|

Net

utility plant

|

221,475 | 210,820 | |||||||

|

OTHER

PHYSICAL PROPERTY:

|

|||||||||

|

Net

of accumulated depreciation of $175 in 2009

|

|||||||||

|

and

$162 in 2008

|

554 | 562 | |||||||

|

CURRENT

ASSETS:

|

|||||||||

|

Restricted

cash-compensating balance

|

500 | - | |||||||

|

Receivables,

net of reserves of $225 in 2009 and $195 in 2008

|

2,938 | 3,243 | |||||||

|

Unbilled

revenues

|

2,451 | 2,687 | |||||||

|

Recoverable

income taxes

|

- | 131 | |||||||

|

Materials

and supplies inventories, at cost

|

716 | 741 | |||||||

|

Prepaid

expenses

|

387 | 412 | |||||||

|

Deferred

income taxes

|

154 | 133 | |||||||

|

Total

current assets

|

7,146 | 7,347 | |||||||

|

OTHER

LONG-TERM ASSETS:

|

|||||||||

|

Deferred

debt expense

|

1,906 | 2,013 | |||||||

|

Notes

receivable

|

476 | 536 | |||||||

|

Deferred

regulatory assets

|

14,010 | 15,972 | |||||||

|

Other

|

3,270 | 3,192 | |||||||

|

Total

other long-term assets

|

19,662 | 21,713 | |||||||

|

Total

Assets

|

$ | 248,837 | $ | 240,442 | |||||

|

The

accompanying notes are an integral part of these

statements.

|

|||||||||

|

THE

YORK WATER COMPANY

|

||||||||

|

Balance

Sheets

|

||||||||

|

(In

thousands of dollars, except per share amounts)

|

||||||||

| December 31 | ||||||||

|

2009

|

2008

|

|||||||

|

STOCKHOLDERS'

EQUITY AND LIABILITIES

|

||||||||

|

COMMON

STOCKHOLDERS' EQUITY:

|

||||||||

|

Common

stock, no par value, authorized 46,500,000 shares,

|

$ | 73,569 | $ | 57,875 | ||||

|

issued

and outstanding 12,558,724 shares in 2009

|

||||||||

|

and

11,367,248 shares in 2008

|

||||||||

|

Retained

earnings

|

13,353 | 11,891 | ||||||

|

Total

common stockholders' equity

|

86,922 | 69,766 | ||||||

|

PREFERRED

STOCK, authorized 500,000 shares, no shares issued

|

- | - | ||||||

|

LONG-TERM

DEBT, excluding current portion

|

73,227 | 83,612 | ||||||

|

COMMITMENTS

|

- | - | ||||||

|

CURRENT

LIABILITIES:

|

||||||||

|

Short-term

borrowings

|

5,000 | 6,000 | ||||||

|

Current

portion of long-term debt

|

4,341 | 2,741 | ||||||

|

Accounts

payable

|

892 | 2,011 | ||||||

|

Dividends

payable

|

1,393 | 1,192 | ||||||

|

Accrued

taxes

|

488 | 75 | ||||||

|

Accrued

interest

|

1,019 | 1,080 | ||||||

|

Other

accrued expenses

|

1,472 | 1,097 | ||||||

|

Total

current liabilities

|

14,605 | 14,196 | ||||||

|

DEFERRED

CREDITS:

|

||||||||

|

Customers'

advances for construction

|

16,188 | 18,258 | ||||||

|

Deferred

income taxes

|

22,507 | 19,549 | ||||||

|

Deferred

employee benefits

|

8,765 | 9,758 | ||||||

|

Other

deferred credits

|

1,679 | 2,789 | ||||||

|

Total

deferred credits

|

49,139 | 50,354 | ||||||

|

Contributions

in aid of construction

|

24,944 | 22,514 | ||||||

|

Total

Stockholders' Equity and Liabilities

|

$ | 248,837 | $ | 240,442 | ||||

|

The

accompanying notes are an integral part of these

statements.

|

||||||||

|

Statements

of Income

|

||||||||||||

|

(In

thousands of dollars, except per share amounts)

|

||||||||||||

|

Year

Ended December 31

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

WATER

OPERATING REVENUES:

|

||||||||||||

|

Residential

|

$ | 23,299 | $ | 20,572 | $ | 19,722 | ||||||

|

Commercial

and industrial

|

10,734 | 9,671 | 9,290 | |||||||||

|

Other

|

3,010 | 2,595 | 2,421 | |||||||||

| 37,043 | 32,838 | 31,433 | ||||||||||

|

OPERATING

EXPENSES:

|

||||||||||||

|

Operation

and maintenance

|

7,067 | 6,749 | 6,593 | |||||||||

|

Administrative

and general

|

7,101 | 6,685 | 6,506 | |||||||||

|

Depreciation

and amortization

|

4,412 | 3,622 | 3,227 | |||||||||

|

Taxes

other than income taxes

|

1,075 | 1,102 | 1,007 | |||||||||

| 19,655 | 18,158 | 17,333 | ||||||||||

|

Operating

income

|

17,388 | 14,680 | 14,100 | |||||||||

|

OTHER

INCOME (EXPENSES):

|

||||||||||||

|

Interest

on debt

|

(4,990 | ) | (4,759 | ) | (4,144 | ) | ||||||

|

Allowance

for funds used during construction

|

210 | 647 | 228 | |||||||||

|

Other

income (expenses), net

|

(517 | ) | (509 | ) | (78 | ) | ||||||

| (5,297 | ) | (4,621 | ) | (3,994 | ) | |||||||

|

Income

before income taxes

|

12,091 | 10,059 | 10,106 | |||||||||

|

Income

taxes

|

4,579 | 3,628 | 3,692 | |||||||||

|

Net

income

|

$ | 7,512 | $ | 6,431 | $ | 6,414 | ||||||

|

Basic

Earnings Per Share

|

$ | 0.64 | $ | 0.57 | $ | 0.57 | ||||||

|

Cash

Dividends Declared Per Share

|

$ | 0.506 | $ | 0.489 | $ | 0.475 | ||||||

|

The

accompanying notes are an integral part of these

statements.

|

||||||||||||

|

Statements

of Common Stockholders' Equity and Comprehensive Income

|

||||||||||||||||

|

(In

thousands of dollars, except per share amounts)

|

||||||||||||||||

|

For

the Years Ended December 31, 2009, 2008 and 2007

|

||||||||||||||||

|

Accumulated

|

||||||||||||||||

|

Other

|

||||||||||||||||

|

Common

|

Retained

|

Comprehensive

|

||||||||||||||

|

Stock

|

Earnings

|

Income

(Loss)

|

Total

|

|||||||||||||

|

Balance,

December 31, 2006

|

$ | 55,558 | $ | 9,904 | $ | (101 | ) | $ | 65,361 | |||||||

|

Net

income

|

- | 6,414 | - | 6,414 | ||||||||||||

|

Other

comprehensive income (loss):

|

||||||||||||||||

|

Unrealized

loss on interest rate swap,

|

||||||||||||||||

|

net

of $125 income tax

|

- | - | (183 | ) | (183 | ) | ||||||||||

|

Reclassification

adjustment for amounts

|

||||||||||||||||

|

recognized

in income, net of $3 income tax

|

- | - | 4 | 4 | ||||||||||||

|

Comprehensive

income

|

6,235 | |||||||||||||||

|

Dividends

($0.475 per share)

|

- | (5,332 | ) | - | (5,332 | ) | ||||||||||

|

Issuance

of common stock under

|

||||||||||||||||

|

dividend

reinvestment and

|

||||||||||||||||

|

employee

stock purchase plans

|

1,008 | - | - | 1,008 | ||||||||||||

|

Balance,

December 31, 2007

|

56,566 | 10,986 | (280 | ) | 67,272 | |||||||||||

|

Net

income

|

- | 6,431 | - | 6,431 | ||||||||||||

|

Other

comprehensive income (loss):

|

||||||||||||||||

|

Reclassification

adjustment for unrealized loss

|

||||||||||||||||

|

on

interest rate swap to regulatory asset,

|

||||||||||||||||

|

net

of $191 income tax

|

- | - | 280 | 280 | ||||||||||||

|

Comprehensive

income

|

6,711 | |||||||||||||||

|

Dividends

($0.489 per share)

|

- | (5,526 | ) | - | (5,526 | ) | ||||||||||

|

Issuance

of common stock under

|

||||||||||||||||

|

dividend

reinvestment, direct stock and

|

||||||||||||||||

|

employee

stock purchase plans

|

1,309 | - | - | 1,309 | ||||||||||||

|

Balance,

December 31, 2008

|

57,875 | 11,891 | - | 69,766 | ||||||||||||

|

Net

income

|

- | 7,512 | - | 7,512 | ||||||||||||

|

Dividends

($0.506 per share)

|

- | (6,050 | ) | - | (6,050 | ) | ||||||||||

|

Issuance

of 1,070,000 shares of common stock

|

14,094 | - | - | 14,094 | ||||||||||||

|

Issuance

of common stock under

|

||||||||||||||||

|

dividend

reinvestment, direct stock and

|

||||||||||||||||

|

employee

stock purchase plans

|

1,600 | - | - | 1,600 | ||||||||||||

|

Balance,

December 31, 2009

|

$ | 73,569 | $ | 13,353 | $ | - | $ | 86,922 | ||||||||

|

The

accompanying notes are an integral part of these

statements.

|

||||||||||||||||

|

Statements

of Cash Flows

|

|||||||||||||

|

(In

thousands of dollars, except per share amounts)

|

|||||||||||||

|

Year

Ended December 31

|

|||||||||||||

|

2009

|

2008

|

2007

|

|||||||||||

|

CASH

FLOWS FROM OPERATING ACTIVITIES:

|

|||||||||||||

|

Net

income

|

$ | 7,512 | $ | 6,431 | $ | 6,414 | |||||||

|

Adjustments

to reconcile net income to net cash provided by operating

activities:

|

|||||||||||||

|

Depreciation

and amortization

|

4,412 | 3,622 | 3,227 | ||||||||||

|

Increase

in deferred income taxes

|

2,515 | 1,911 | 1,143 | ||||||||||

|

Other

|

39 | (166 | ) | (71 | ) | ||||||||

|

Changes

in assets and liabilities:

|

|||||||||||||

|

(Increase)

decrease in accounts receivable, unbilled revenues and recoverable income

taxes

|

440 | (816 | ) | (216 | ) | ||||||||

|

(Increase)

decrease in materials and supplies and prepaid expenses

|

50 | 105 | (38 | ) | |||||||||

|

Increase

in accounts payable, accrued expenses, regulatory

|

|||||||||||||

|

and

other liabilities, and deferred employee benefits and

credits

|

666 | 870 | 103 | ||||||||||

|

Increase

(decrease) in accrued interest and taxes

|

352 | 221 | (52 | ) | |||||||||

|

Increase

in regulatory and other assets

|

(185 | ) | (651 | ) | (470 | ) | |||||||

|

Net

cash provided by operating activities

|

15,801 | 11,527 | 10,040 | ||||||||||

|

CASH

FLOWS FROM INVESTING ACTIVITIES:

|

|||||||||||||

|

Utility

plant additions, including debt portion of allowance for funds used

during

|

|||||||||||||

|

construction

of $117 in 2009, $427 in 2008 and $127 in 2007

|

(12,535 | ) | (24,438 | ) | (18,154 | ) | |||||||

|

Acquisitions

of water systems

|

(2,236 | ) | (259 | ) | (896 | ) | |||||||

|

Increase

in compensating balance

|

(500 | ) | - | - | |||||||||

|

Decrease

in notes receivable

|

60 | 74 | 858 | ||||||||||

|

Net

cash used in investing activities

|

(15,211 | ) | (24,623 | ) | (18,192 | ) | |||||||

|

CASH

FLOWS FROM FINANCING ACTIVITIES:

|

|||||||||||||

|

Customers'

advances for construction and contributions in aid of

construction

|

443 | 804 | 2,447 | ||||||||||

|

Repayments

of customer advances

|

(926 | ) | (1,489 | ) | (1,469 | ) | |||||||

|

Proceeds

of long-term debt issues

|

23,659 | 52,308 | 8,210 | ||||||||||

|

Debt

issuance costs

|

- | (950 | ) | - | |||||||||

|

Repayments

of long-term debt

|

(32,444 | ) | (36,460 | ) | (40 | ) | |||||||

|

Borrowings

(repayments) under short-term line of credit agreements

|

(1,000 | ) | 3,000 | 3,000 | |||||||||

|

Changes

in cash overdraft position

|

(167 | ) | 34 | 277 | |||||||||

|

Issuance

of common stock

|

15,694 | 1,309 | 1,008 | ||||||||||

|

Dividends

paid

|

(5,849 | ) | (5,460 | ) | (5,281 | ) | |||||||

|

Net

cash (used in) provided by financing activities

|

(590 | ) | 13,096 | 8,152 | |||||||||

|

Net

change in cash and cash equivalents

|

- | - | - | ||||||||||

|

Cash