Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - MAINSOURCE FINANCIAL GROUP | a2197150zex-21.htm |

| EX-32.1 - EXHIBIT 32.1 - MAINSOURCE FINANCIAL GROUP | a2197150zex-32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - MAINSOURCE FINANCIAL GROUP | a2197150zex-31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - MAINSOURCE FINANCIAL GROUP | a2197150zex-31_2.htm |

| EX-23.1 - EXHIBIT 23.1 - MAINSOURCE FINANCIAL GROUP | a2197150zex-23_1.htm |

| EX-99.1 - EXHIBIT 99.1 - MAINSOURCE FINANCIAL GROUP | a2197150zex-99_1.htm |

| EX-32.2 - EXHIBIT 32.2 - MAINSOURCE FINANCIAL GROUP | a2197150zex-32_2.htm |

| EX-99.2 - EXHIBIT 99.2 - MAINSOURCE FINANCIAL GROUP | a2197150zex-99_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

For the fiscal year ended December 31, 2009

Commission file number 0-12422

MAINSOURCE FINANCIAL GROUP, INC.

(Exact name of registrant as specified in its charter)

| Indiana (State or other jurisdiction of incorporation or organization) |

35-1562245 (I.R.S. Employer Identification No.) |

|

2105 North State Road 3 Bypass Greensburg, Indiana 47240 (Address of principal executive offices) (Zip code) |

||

Registrant's telephone number, including area code: (812) 663-6734 |

||

Securities registered pursuant to Section 12(b) of the Act: |

||

Title of each class Common shares, no par value |

Name of each exchange on which registered The NASDAQ Stock Market LLC |

|

Securities registered pursuant to Section 12(g) of the Act: None |

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the previous 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer", "accelerated filer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value (not necessarily a reliable indication of the price at which more than a limited number of shares would trade) of the voting stock held by non-affiliates of the registrant was $149,411,806 as of June 30, 2009.

As of March 10, 2010, there were outstanding 20,136,362 common shares, without par value, of the registrant.

DOCUMENTS INCORPORATED BY REFERENCE

Documents

|

Part of Form 10-K Into Which Incorporated |

|

|---|---|---|

| Definitive Proxy Statement for Annual Meeting of Shareholders to be held April 28, 2010 |

Part III (Items 10 through 14) |

Pursuant to General Instruction G, the information called for by Items 10-14 is omitted by MainSource Financial Group, Inc. since MainSource Financial Group, Inc. will file with the Commission a definitive proxy statement to shareholders pursuant to Regulation 14A not later than 120 days after the close of the fiscal year containing the information required by Items 10-14.

2

(Dollar amounts in thousands except per share data)

General

MainSource Financial Group, Inc. ("MainSource" or the "Company") is a financial holding company based in Greensburg, Indiana. As of December 31, 2009, the Company operated one banking subsidiary: MainSource Bank ("the Bank"), an Indiana state chartered bank. During 2009, three wholly owned subsidiaries, MainSource Bank of Illinois, MainSource Bank — Ohio and MainSource Bank — Hobart, were merged into MainSource Bank. Through its non-bank affiliates, the Company provides services incidental to the business of banking. Since its formation in 1982, the Company has acquired and established various institutions and financial services companies and may acquire additional financial institutions and financial services companies in the future. For further discussion of the business of the Company see Management's Discussion and Analysis in Part II, Item 7.

As of December 31, 2009, the Company operated 85 branch banking offices in Indiana, Illinois, Ohio, and Kentucky as well as twelve insurance offices in Indiana and one in Illinois. As of December 31, 2009, the Company had consolidated assets of $2,906,530, consolidated deposits of $2,270,650 and shareholders' equity of $294,462.

Through the Bank, the Company offers a broad range of financial services, including: accepting time and transaction deposits; making consumer, commercial, agribusiness and real estate mortgage loans; renting safe deposit facilities; providing general agency personal and business insurance services; providing personal and corporate trust services; and providing other corporate services such as letters of credit and repurchase agreements.

The lending activities of the Bank are separated into primarily the categories of commercial/agricultural, real estate and consumer. Loans are originated by the lending officers of the Bank subject to limitations set forth in lending policies. The Board of Directors of the Bank reviews loans up to the Bank's legal lending limits, monitors concentrations of credit, problem and past due loans and charge-offs of uncollectible loans, and formulates loan policy. The Bank maintains conservative loan policies and underwriting practices in order to address and manage loan risks. These policies and practices include granting loans on a sound and collectible basis, serving the legitimate needs of the community and the general market area while obtaining a balance between maximum yield and minimum risk, ensuring that primary and secondary sources of repayment are adequate in relation to the amount of the loan, developing and maintaining adequate diversification of the loan portfolio as a whole and of the loans within each category and developing and applying adequate collection policies.

Commercial loans include secured and unsecured loans, including real estate loans, to individuals and companies and to governmental units predominantly within the market area of the Bank for a myriad of business purposes.

Agricultural loans are generated in the Bank's markets. Most of the loans are real estate loans on farm properties. Loans are also made for agricultural production and such loans are generally reviewed annually.

Residential real estate lending has been the largest component of the loan portfolio for many years. The Bank generates residential mortgages for its own portfolio. However, the Company elects to sell the majority of its fixed rate mortgages into the secondary market while maintaining the servicing of such loans. At December 31, 2009, the Company was servicing a $726 million residential real estate loan portfolio. By originating loans for sale in the secondary market, the Company can more fully satisfy customer demand for fixed rate residential mortgages and increase fee income, while reducing the risk of loss caused by rising interest rates.

The principal source of revenues for the Company is interest and fees on loans, which accounted for 63.2% of total revenues in 2009, 67.9% in 2008 and 69.1% in 2007.

The Company's investment securities portfolio is primarily comprised of U. S. Treasuries, federal agencies, state and municipal bonds, U. S. government sponsored entity's mortgage-backed securities and corporate securities. The Company has classified its entire investment portfolio as available for sale, with fair value changes reported separately in shareholders' equity. Funds invested in the investment portfolio generally represent funds not immediately required to meet loan demand. Income related to the Company's investment portfolio accounted for 14.8% of total revenues in 2009, 15.0% in 2008 and 14.2% in 2007. As of December 31, 2009, the Company had not identified any securities as being "high risk" as defined by the FFIEC Supervisory Policy Statement on Securities Activities.

The primary source of funds for the Bank is deposits generated in local market areas. To attract and retain stable depositors, the Bank markets various programs for demand, savings and time deposit accounts. These programs include interest and non-interest bearing demand and individual retirement accounts.

3

Currently, national retailing and manufacturing subsidiaries, brokerage and insurance firms and credit unions are fierce competitors within the financial services industry. Mergers between financial institutions within Indiana and neighboring states, which became permissible under the Interstate Banking and Branching Efficiency Act of 1994, have also added competitive pressure.

The branches of the Bank are located in predominantly non-metropolitan areas and the Bank's business is centered in loans and deposits generated within markets considered largely rural in nature. In addition to competing vigorously with other banks, thrift institutions, credit unions and finance companies located within their service areas, we also compete, directly and indirectly, with all providers of financial services.

Employees

As of December 31, 2009, the Company and its subsidiaries had 934 full-time equivalent employees to whom it provides a variety of benefits and with whom it enjoys excellent relations. None of our employees are subject to collective bargaining agreements.

Regulation and Supervision

The Company is a financial holding company ("FHC") within the meaning of the Bank Holding Company Act of 1956, as amended. As a financial holding company, the Company is subject to regulation by the Federal Reserve Board ("FRB"). The Bank is an Indiana state chartered bank subject to supervision and regulation by the Federal Deposit Insurance Corporation ("FDIC") and the Indiana Department of Financial Institutions. The following is a discussion of material statutes and regulations affecting the Company and the Bank. The discussion is qualified in its entirety by reference to such statutes and regulations.

Bank Holding Company Act of 1956, as amended (the "BHC Act").

Generally, the BHC Act governs the acquisition and control of banks and nonbanking companies by bank holding companies. A bank holding company is subject to regulation under the BHC Act and is required to register with the FRB under the BHC Act. The BHC Act requires a bank holding company to file an annual report of its operations and such additional information as the FRB may require. The FRB has issued regulations under the BHC Act requiring a bank holding company to serve as a source of financial and managerial strength to its subsidiary banks. It is the policy of the FRB that, pursuant to this requirement, a bank holding company should stand ready to use its resources to provide adequate capital funds to its subsidiary banks during periods of financial stress or adversity.

The acquisition of 5% or more of the voting shares of any bank or bank holding company generally requires the prior approval of the FRB and is subject to applicable federal and state law, including the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 ("Riegle-Neal") for interstate transactions. The FRB evaluates acquisition applications based on, among other things, competitive factors, supervisory factors, adequacy of financial and managerial resources, and banking and community needs considerations.

The BHC Act also prohibits, with certain exceptions, a bank holding company from acquiring direct or indirect ownership or control of more than 5% of the voting shares of any "nonbanking" company unless the nonbanking activities are found by the FRB to be "so closely related to banking . . . as to be a proper incident thereto." Under current regulations of the FRB, a bank holding company and its nonbank subsidiaries are permitted, among other activities, to engage in such banking-related business ventures as consumer finance, equipment leasing, data processing, mortgage banking, financial and investment advice, and securities brokerage services. The BHC Act does not place territorial restrictions on the activities of a bank holding company or its nonbank subsidiaries.

Federal law prohibits acquisition of "control" of a bank or bank holding company without prior notice to certain federal bank regulators. "Control" is defined in certain cases as the acquisition of as little as 10% of the outstanding shares of any class of voting stock. Furthermore, under certain circumstances, a bank holding company may not be able to purchase its own stock, where the gross consideration will equal 10% or more of the company's net worth, without obtaining approval of the FRB. Under the Federal Reserve Act, banks and their affiliates are subject to certain requirements and restrictions when dealing with each other (affiliate transactions include transactions between a bank and its bank holding company).

Gramm-Leach-Bliley Financial Modernization Act of 1999.

The Gramm-Leach-Bliley Financial Modernization Act of 1999 (the "Modernization Act") was enacted on November 12, 1999. The Modernization Act, which amended the BHC Act, provides the following:

- •

- it allows bank holding companies that qualify as "financial holding companies" to engage in a broad range of financial and

related activities;

- •

- it allows insurers and other financial services companies to acquire banks;

4

- •

- it removes various restrictions that applied to bank holding company ownership of securities firms and mutual fund

advisory companies; and

- •

- it establishes the overall regulatory structure applicable to bank holding companies that also engage in insurance and securities operations.

The Company initially qualified as a financial holding company in December, 2004. Thus the Company is authorized to operate as a financial holding company and is eligible to engage in, or acquire companies engaged in, the broader range of activities that are permitted by the Modernization Act. These activities include those that are determined to be "financial in nature," including insurance underwriting, securities underwriting and dealing, and making merchant banking investments in commercial and financial companies. If a banking subsidiary ceases to be "well capitalized" or "well managed" under applicable regulatory standards, the FRB may, among other things, place limitations on our ability to conduct these broader financial activities or, if the deficiencies persist, require us to divest the banking subsidiary. In addition, if a banking subsidiary receives a rating of less than satisfactory under the Community Reinvestment Act of 1977 ("CRA"), we would be prohibited from engaging in any additional activities other than those permissible for bank holding companies that are not financial holding companies.

Bank Secrecy Act and USA Patriot Act

In 1970, Congress enacted the Currency and Foreign Transactions Reporting Act, commonly known as the Bank Secrecy Act (the "BSA"). The BSA requires financial institutions to maintain records of certain customers and currency transactions and to report certain domestic and foreign currency transactions, which may have a high degree of usefulness in criminal, tax, or regulatory investigations or proceedings. Under this law, financial institutions are required to develop a BSA compliance program.

In 2001, the President signed into law comprehensive anti-terrorism legislation known as the USA Patriot Act. Title III of the USA Patriot Act requires financial institutions, including the Company and the Bank, to help prevent and detect international money laundering and the financing of terrorism and prosecute those involved in such activities. The Department of the Treasury has adopted additional requirements to further implement Title III.

Under these regulations, a mechanism has been established for law enforcement officials to communicate names of suspected terrorists and money launderers to financial institutions to enable financial institutions to promptly locate accounts and transactions involving those suspects. Financial institutions receiving names of suspects must search their account and transaction records for potential matches and report positive results to the U.S. Department of the Treasury Financial Crimes Enforcement Network ("FinCEN"). Each financial institution must designate a point of contact to receive information requests. These regulations outline how financial institutions can share information concerning suspected terrorist and money laundering activity with other financial institutions under the protection of a statutory safe harbor if each financial institution notifies FinCEN of its intent to share information. The Department of the Treasury has also adopted regulations intended to prevent money laundering and terrorist financing through correspondent accounts maintained by U.S. financial institutions on behalf of foreign banks. Financial institutions are required to take reasonable steps to ensure that they are not providing banking services directly or indirectly to foreign shell banks. In addition, banks must have procedures in place to verify the identity of the persons with whom they deal.

FDIC Improvement Act of 1991

The Federal Deposit Insurance Corporation Improvement Act of 1991 ("FDICIA") requires, among other things, federal bank regulatory authorities to take "prompt corrective action" with respect to banks which do not meet minimum capital requirements. For these purposes, FDICIA establishes five capital tiers: well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized and critically undercapitalized. The FDIC has adopted regulations to implement the prompt corrective action provisions of FDICIA.

"Undercapitalized" banks are subject to growth limitations and are required to submit a capital restoration plan. A bank's compliance with such plan is required to be guaranteed by the bank's parent holding company. If an "undercapitalized" bank fails to submit an acceptable plan, it is treated as if it is significantly undercapitalized. "Significantly undercapitalized" banks are subject to one or more restrictions, including an order by the FDIC to sell sufficient voting stock to become adequately capitalized, requirements to reduce total assets and cease receipt of deposits from correspondent banks, and restrictions on compensation of executive officers. "Critically undercapitalized" institutions may not, beginning 60 days after becoming "critically undercapitalized," make any payment of principal or interest on certain subordinated debt or extend credit for a highly leveraged transaction or enter into any transaction outside the ordinary course of business. In addition, "critically undercapitalized" institutions are subject to appointment of a receiver or conservator.

A "well capitalized" institution is one that has a total risk-based capital ratio of at least 10%, a Tier 1 risk-based capital ratio of at least 6%, a leverage ratio of at least 5% and is not subject to regulatory direction to maintain a specific level for any capital measure. An "adequately capitalized" institution is one that has ratios greater than 8%, 4% and 4%. An institution is "undercapitalized" if its respective ratios are less than 8%, 4% and 4%. "Significantly undercapitalized" institutions have ratios of

5

less than 6%, 3% and 3%. An institution is deemed to be "critically undercapitalized" if it has a ratio of tangible equity to total assets that is 2% or less.

The Sarbanes-Oxley Act

The Sarbanes-Oxley Act of 2002 ("Sarbanes-Oxley Act"), which became law on July 30, 2002, added new legal requirements for public companies affecting corporate governance, accounting and corporate reporting. The Sarbanes-Oxley Act provides for, among other things:

- •

- a prohibition on personal loans made or arranged by the issuer to its directors and executive officers (except for loans

made by a bank subject to Regulation O);

- •

- independence requirements for audit committee members;

- •

- independence requirements for company auditors;

- •

- certification of financial statements on Forms 10-K and 10-Q reports by the chief executive

officer and the chief financial officer;

- •

- the forfeiture by the chief executive officer and chief financial officer of bonuses or other incentive-based compensation

and profits from the sale of an issuer's securities by such officers in the twelve-month period following initial publication of any financial statements that later require restatement due to

corporate misconduct;

- •

- disclosure of off-balance sheet transactions;

- •

- two-business day filing requirements for insiders filing Form 4s;

- •

- disclosure of a code of ethics for financial officers and filing a Form 8-K for a change in or waiver

of such code;

- •

- the reporting of securities violations "up the ladder" by both in-house and outside attorneys;

- •

- restrictions on the use of non-GAAP financial measures in press releases and SEC filings;

- •

- the formation of a public accounting oversight board; and

- •

- various increased criminal penalties for violations of securities laws.

The SEC has been delegated the task of enacting rules to implement various provisions of the Sarbanes-Oxley Act. In addition, each of the national stock exchanges developed new corporate governance rules, including rules strengthening director independence requirements for boards, the adoption of corporate governance codes and charters for the nominating, corporate governance and audit committees.

Deposit Insurance Fund

The deposits of the Bank are insured to the maximum extent permitted by law by the Deposit Insurance Fund ("DIF") of the FDIC, which was created in 2006 as the result of the merger of the Bank Insurance Fund and the Savings Association Insurance Fund in accordance with the Federal Deposit Insurance Reform Act of 2005 (the "FDI Act"). The FDI Act provided for several additional changes to the deposit insurance system, including adjusting the deposit insurance limits every 5 years beginning in 2011 based on an inflation index, increasing the insurance limit for retirement accounts from $100 to $250, and allocating an aggregate of $4.7 billion of one-time credits to banks to offset the insurance premiums charged to such banks by the FDIC.

During the second quarter of 2009, the FDIC levied an industry-wide special assessment charge on insured financial institutions as part of the agency's efforts to rebuild the DIF. In November 2009, the FDIC amended regulations that required insured institutions to prepay their estimated quarterly risk-based assessments for the fourth quarter of 2009 and for all of the years 2010-2012. The prepaid assessments will be applied against future quarterly assessments (as they may be so revised) until the prepaid assessment is exhausted or the balance of the prepayment is returned, whichever occurs first.

In addition, on January 12, 2010, the FDIC announced that it would seek public comment on whether financial institutions with compensation plans that encourage risky behavior should be charged higher deposit assessment rates than such financial institutions would otherwise be charged. The FDIC is not precluded from changing assessment rates or from further revising the risk-based assessment system during the prepayment period or thereafter. Thus, the Company may also be required to pay significantly higher FDIC insurance assessment premiums in the future because market developments have significantly depleted the DIF and reduced the ratio of reserves to insured deposits.

6

Dividends

The Company is a legal entity separate and distinct from the Bank. There are various legal limitations on the extent to which the Bank can supply funds to the Company. The principal source of the Company's funds consists of dividends from the Bank. State and Federal law restricts the amount of dividends that may be paid by banks. In addition, the Bank is subject to certain restrictions on extensions of credit to the Company, on investments in the stock or other securities of the Company and in taking such stock or securities as collateral for loans.

Recent Legislative and Regulatory Initiatives to Address Financial and Economic Crises

Congress, the United States Department of the Treasury ("Treasury") and the federal banking regulators, including the FDIC, have taken broad action since early September 2008 to address volatility in the U.S. banking system and financial markets.

In October 2008, the Emergency Economic Stabilization Act of 2008 ("EESA") was enacted. The EESA authorizes Treasury to purchase from financial institutions and their holding companies up to $700 billion in mortgage loans, mortgage-related securities and certain other financial instruments, including debt and equity securities issued by financial institutions and their holding companies in a troubled asset relief program ("TARP"). The purpose of TARP is to restore confidence and stability to the U.S. banking system and to encourage financial institutions to increase their lending to customers and to each other. As part of TARP, Treasury has allocated $250 billion towards the Capital Purchase Program. Under the Capital Purchase Program, Treasury will purchase debt or equity securities from participating institutions. Participants in the Capital Purchase Program are subject to executive compensation limits and are encouraged to expand their lending and mortgage loan modifications. EESA also increased FDIC deposit insurance on most accounts from $100 to $250.

Following a systemic risk determination, on October 14, 2008, the FDIC established a Temporary Liquidity Guarantee Program ("TLGP"). The TLGP includes the Transaction Account Guarantee Program ("TAGP"), which provides unlimited deposit insurance coverage for noninterest-bearing transaction accounts (typically business checking accounts) and certain funds swept into noninterest-bearing savings accounts. As originally enacted, the TAGP expired on December 31, 2009, and banks participating in the TAGP paid a 10 basis point fee (annualized) on the balance of each covered account in excess of $250. On October 1, 2009, the FDIC extended the TAGP for six months until June 30, 2010. Any insured depository institution that was participating in the TAGP program as of October 1, 2009 was permitted to continue in the TAGP during the extension period. The annual assessment rate that applies to participating institutions during the extension period is either 15 basis points, 20 basis points or 25 basis points, depending on the "Risk Category" assigned to the institution under the FDIC's risk-based premium system. Any institution participating in the TAGP program as of October 1, 2009 that desired to opt out of the TAGP extension was required to submit its opt-out election to the FDIC on or before November 2, 2009. The Company elected to participate in the TAGP through December 31, 2009, but did not elect to participate in the extension of the program.

The TLGP also includes the Debt Guarantee Program ("DGP"), under which the FDIC guaranteed certain senior unsecured debt of FDIC-insured institutions and their holding companies issued on or after October 14, 2008 and not later than June 30, 2009. The guarantee is effective through the earlier of the maturity date or June 30, 2012. The DGP coverage limit is generally 125% of the entity's eligible debt outstanding on September 30, 2008 and scheduled to mature on or before June 30, 2009 or, for certain insured institutions, 2% of their total liabilities as of September 30, 2008. Depending on the term of the debt maturity, the nonrefundable DGP fee ranges from 50 to 100 basis points (annualized) for covered debt outstanding until the earlier of maturity or June 30, 2012. The DGP is in effect for all eligible entities, unless the entity opted out on or before December 5, 2008. The Company did not opt out of the DGP, although it does not have any eligible debt and therefore will not pay any premium associated with the DGP.

On February 17, 2009, President Barack Obama signed the American Recovery and Reinvestment Act of 2009 ("ARRA"), more commonly known as the economic stimulus or economic recovery package. ARRA includes a wide variety of programs intended to stimulate the economy and provide for extensive infrastructure, energy, health and education needs. In addition, ARRA imposes new executive compensation and corporate governance limits on current and future participants in the Treasury's Capital Purchase Program ("CPP"), including the Company, which are in addition to those previously announced by Treasury. The new limits remain in place until the participant has redeemed the preferred stock sold to Treasury, which is now permitted under ARRA without penalty and without the need to raise new capital, subject to Treasury's consultation with the recipient's appropriate federal regulator. On June 10, 2009, Treasury released an interim final rule, effective June 15, 2009, that provided guidance on the compensation and governance standards for participants in the CPP, and promulgated regulations to implement the restrictions and standards set forth in ARRA. Among other things, Treasury's final rule and ARRA significantly expanded the executive compensation restrictions previously imposed by EESA.

On May 20, 2009, the Helping Families Save Their Homes Act of 2009, which extended the temporary increase in the standard maximum deposit insurance amount provided by the FDIC to $250 per depositor through December 31, 2013, was signed into law. This extension of the temporary $250 coverage limit (pursuant to EESA) became effective immediately upon the President's

7

signature. The legislation provides that the standard maximum deposit insurance amount provided by the FDIC will return to $100 on January 1, 2014.

On October 22, 2009, the Federal Reserve issued a comprehensive proposal on incentive compensation policies (the "Incentive Compensation Proposal") intended to ensure that the incentive compensation policies of banking organizations do not undermine the safety and soundness of such organizations by encouraging excessive risk-taking. This guidance sets expectations for banking organizations concerning their incentive compensation arrangements and related risk-management, control and governance processes. The Incentive Compensation Proposal, which covers all employees that have the ability to materially affect the risk profile of an organization, either individually or as part of a group, is based upon three primary principles: (i) balanced risk-taking incentives, (ii) compatibility with effective controls and risk management, and (iii) strong corporate governance. Any deficiencies in compensation practices that are identified may be incorporated into the organization's supervisory ratings, which can affect its ability to make acquisitions or perform other actions. In addition, under the Incentive Compensation Proposal, the Federal Reserve in appropriate circumstances may take enforcement action against a banking organization.

On January 14, 2010, the current administration announced a proposal to impose a fee (the "Financial Crisis Responsibility Fee") on those financial institutions that benefited from recent actions taken by the U.S. government to stabilize the financial system. If implemented as initially proposed, the Financial Crisis Responsibility Fee will be applied to firms with over $50 billion in consolidated assets, and, therefore, by its terms would not apply to the Company. The Financial Crisis Responsibility Fee would be collected by the Internal Revenue Service and would be approximately fifteen basis points, or 0.15%, of an amount calculated by subtracting a covered institution's Tier 1 capital and FDIC-assessed deposits (and/or an adjustment for insurance liabilities covered by state guarantee funds) from such institution's total assets. The Financial Crisis Responsibility Fee, if implemented as proposed by the current administration, would go into effect on June 30, 2010 and remain in place for at least ten years. The U.S. Treasury would be asked to report after five years on the effectiveness of the Financial Crisis Responsibility Fee as well as its progress in repaying projected losses to the U.S. government as a result of TARP. If losses to the U.S. government as a result of TARP have not been recouped after ten years, the Financial Crisis Responsibility Fee would remain in place until such losses have been recovered.

Other Regulations

In addition to the statutes and regulations discussed above, the Company and the Bank are subject to additional regulation of their activities, including a variety of consumer protection regulations affecting lending, deposit and collection activities and regulations affecting secondary mortgage market activities.

Capital Requirements

As discussed above, the Company and the Bank must meet certain minimum capital requirements mandated by each of their state or federal regulators. These regulatory agencies require BHCs and banks to maintain certain minimum ratios of primary capital to total assets and total capital to total assets. The FRB requires BHCs to maintain a minimum Tier 1 leverage ratio of 3% capital to total assets; however, for all but the most highly rated institutions which do not anticipate significant growth, the minimum Tier 1 leverage ratio is 3% plus an additional cushion of 100 to 200 basis points. As of December 31, 2009, the Company's leverage ratio of capital to total assets was 8.8%. The FRB and FDIC each have approved the imposition of "risk-adjusted" capital ratios on BHCs and financial institutions. The Company's Tier 1 Capital to Risk-Weighted Assets Ratio was 13.5% and its Total Capital to Risk-Weighted Assets Ratio was 14.8% at December 31, 2009. The Bank had capital to asset ratios and risk- adjusted capital ratios at December 31, 2009, in excess of the applicable minimum regulatory requirements.

In addition to the other information contained in this report, the following risks may affect us. If any of these risks actually occur, our business, financial condition or results of operations may suffer. As a result, the price of our common shares could decline.

Risks Related to the Company's Business

Difficult conditions in the capital markets and the economy generally may materially adversely affect our business and results of operations.

Our results of operations are materially affected by conditions in the capital markets and the economy generally. The capital and credit markets continue to experience extreme volatility and disruption. In many cases, these markets have produced downward pressure on stock prices of, and credit availability to, certain companies without regard to those companies' underlying financial strength. The impact of this situation, together with concerns regarding the financial strength of financial institutions, has led to distress in financial markets and issues relating to liquidity among financial institutions. As a result, and because of concerns about the stability of the financial markets generally, the resulting credit availability issues, the lack of confidence in the financial sector, the increased volatility in the financial markets and the reduced business activity could have a material adverse effect on the

8

Company's ability to access capital and manage liquidity. If current levels of financial market volatility and disruption continue or worsen, there can be no assurance that the Company's business, financial condition and results of operations will not be materially and adversely affected.

There can be no assurance that actions of the U.S. government, Federal Reserve and other governmental and regulatory bodies for the purpose of stabilizing the financial markets will achieve the intended effect.

In response to the financial crises affecting the banking system and financial markets and going concern threats to investment banks and other financial institutions, on October 3, 2008, President Bush signed EESA into law. Pursuant to EESA, the Treasury has the authority to utilize up to $700 billion to purchase distressed assets from financial institutions or infuse capital into financial institutions for the purpose of stabilizing the financial markets. The Treasury announced the Capital Purchase Program under EESA pursuant to which it has purchased and will continue to purchase senior preferred stock in participating financial institutions such as the Company. Then, on February 17, 2009, President O'Bama signed ARRA as a sweeping economic recovery package intended to stimulate the economy and provide for broad infrastructure, energy, health and education needs. There can be no assurance as to the actual impact that EESA or its programs, including the Capital Purchase Program and ARRA, will have on the financial markets or on us. The failure of these programs to help stabilize the financial markets and a continuation or worsening of current financial market conditions could materially and adversely affect our business, financial condition, results of operations, access to credit or the trading price of our common stock.

The federal government, Federal Reserve, FDIC, SEC and other governmental and regulatory bodies have taken, or are considering taking, other actions to address the financial crisis. There can be no assurance as to what impact such actions will have on the financial markets, including the extreme levels of volatility currently being experienced. Such continued volatility could materially and adversely affect our business, financial condition and results of operations, or the trading price of our common stock.

Like most banking organizations, a significant portion of our assets consists of loans, which if not repaid could result in losses to the Company.

As a lender, we are exposed to the risk that our customers will be unable to repay their loans according to their terms and that the collateral securing the payment of their loans (if any) may not be sufficient to assure repayment. Credit losses could have a material adverse effect on our operating results.

As of December 31, 2009, our total loan portfolio was approximately $1,885,447 or 65% of our total assets. Three major components of the loan portfolio are loans principally secured by real estate, approximately $1,553,076 or 82% of total loans; other commercial loans, approximately $237,398 or 13% of total loans; and consumer loans, approximately $94,973 or 5% of total loans. Our credit risk with respect to our consumer installment loan portfolio and commercial loan portfolio relates principally to the general creditworthiness of individuals and businesses within our local market area. Our credit risk with respect to our residential and commercial real estate mortgage and construction loan portfolio relates principally to the general creditworthiness of individuals and businesses and the value of real estate serving as security for the repayment of the loans. A related risk in connection with loans secured by commercial real estate is the effect of unknown or unexpected environmental contamination, which could make the real estate effectively unmarketable or otherwise significantly reduce its value as security. Credit issues, particularly within our residential and commercial real estate mortgage and construction loan portfolio, may continue to broaden during 2010 depending on the severity and duration of the declining economy and the current credit cycle.

Our allowance for loan losses may not be sufficient to cover actual loan losses, which could adversely affect our earnings.

We maintain an allowance for loan losses at a level estimated by management to be sufficient to cover probable incurred loan losses in our loan portfolio. Loan losses will likely occur in the future and may occur at a rate greater than we have experienced to date. In determining the size of the allowance, our management makes various assumptions and judgments about the collectability of our loan portfolio, including the diversification by industry of our commercial loan portfolio, the effect of changes in the local real estate markets on collateral values, the results of recent regulatory examinations, the effects on the loan portfolio of current economic indicators and their probable impact on borrowers, the amount of charge-offs for the period, the amount of nonperforming loans and related collateral security, and the evaluation of our loan portfolio by an external loan review. If our assumptions and judgments prove to be incorrect, our current allowance may not be sufficient and adjustments may be necessary to allow for different economic conditions or adverse developments in our loan portfolio. Additionally, continuing deterioration in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside the Company's control, may require an increase in the allowance for loan losses. Federal and state regulators also periodically review our allowance for loan losses and may require us to increase our provision for loan losses or recognize further loan charge-offs, based on judgments different than those of our management. Any increase in our allowance for loan losses or loan charge-offs could have an adverse effect on our operating results and financial condition. There can be no assurance that our

9

monitoring procedures and policies will reduce certain lending risks or that our allowance for loan losses will be adequate to cover actual losses.

If we foreclose on collateral property, we may be subject to the increased costs associated with ownership of real property, resulting in reduced revenues and earnings.

We may have to foreclose on collateral property to protect our investment and may thereafter own and operate such property, in which case we will be exposed to the risks inherent in the ownership of real estate. The amount that we, as a mortgagee, may realize after a default is dependent upon factors outside of our control, including, but not limited to: (i) general or local economic conditions; (ii) neighborhood values; (iii) interest rates; (iv) real estate tax rates; (v) operating expenses of the mortgaged properties; (vi) environmental remediation liabilities; (vii) ability to obtain and maintain adequate occupancy of the properties; (viii) zoning laws; (ix) governmental rules, regulations and fiscal policies; and (x) acts of God. Certain expenditures associated with the ownership of real estate, principally real estate taxes, insurance, and maintenance costs, may adversely affect the income from the real estate. Therefore, the cost of operating real property may exceed the income earned from such property, and we may have to advance funds in order to protect our investment, or we may be required to dispose of the real property at a loss. The foregoing expenditures and costs could adversely affect our ability to generate revenues, resulting in reduced levels of profitability.

Significant interest rate volatility could reduce our profitability.

Our results of operations are affected principally by net interest income, which is the difference between interest earned on loans and investments and interest expense paid on deposits and other borrowings. We cannot predict or control changes in interest rates. National, regional and local economic conditions and the policies of regulatory authorities, including monetary policies of the Board of Governors of the Federal Reserve System, affect market interest rates. While we have instituted policies and procedures designed to manage the risks from changes in market interest rates, at any given time our assets and liabilities will likely be affected differently by a given change in interest rates, principally because we do not match the maturities of our loans and investments precisely with our deposits and other funding sources. Changes in interest rates may also affect the level of voluntary prepayments on our loans and the level of financing or refinancing by customers. As of December 31, 2009, we had a negative interest rate gap of 18% of interest earning assets in the one-year time frame. Although this is within our internal policy limits, our earnings will be adversely affected in periods of rising interest rates because, during such periods, the interest expense paid on deposits and borrowings will generally increase more rapidly than the interest income earned on loans and investments. If such an interest rate increase occurred gradually, we would use our established procedures to attempt to mitigate the effects over time. However, if such an interest rate increase occurred rapidly, or interest rates exhibited volatile increases and decreases, we might be unable to mitigate the effects, and our net interest income could suffer significant adverse effects. While management intends to continue to take measures to mitigate interest rate risk, we cannot assure you that such measures will be entirely effective in minimizing our exposure to the risk of rapid changes in interest rates.

We may be required to pay significantly higher Federal Deposit Insurance Corporation (FDIC) premiums in the future.

Recent insured institution failures, as well as deterioration in banking and economic conditions, have significantly increased FDIC loss provisions, resulting in a decline in the designated reserve ratio to historical lows. The FDIC expects a higher rate of insured institution failures in the next few years compared to recent years; thus, the reserve ratio may continue to decline. In addition, EESA increased the limit on FDIC coverage of deposit accounts to $250. These developments will cause the premiums assessed to us by the FDIC to increase.

On December 16, 2008, the FDIC Board of Directors determined deposit insurance assessment rates for the first quarter of 2009 at 12 to 14 basis points of deposits. Beginning April 1, 2009, the rates increased to 12 to 16 basis points of deposits. Additionally, the FDIC implemented a 5 basis point special emergency assessment on June 30, 2009, payable September 30, 2009. These higher FDIC assessment rates and any future special assessments could have an adverse impact on our results of operations.

Future growth or operating results may require the Company to raise additional capital but that capital may not be available or it may be dilutive.

The Company is required by federal and state regulatory authorities to maintain adequate levels of capital to support its operations. To the extent the Company's future operating results erode capital or the Company elects to expand through loan growth or acquisition it may be required to raise capital. The Company's ability to raise capital will depend on conditions in the capital markets, which are outside of its control, and on the Company's financial performance. Accordingly, the Company cannot be assured of its ability to raise capital if needed or on favorable terms. If the Company cannot raise additional capital when needed, it will be subject to increased regulatory supervision and the imposition of restrictions on its growth and business. These could negatively impact the Company's ability to operate or further expand its operations through acquisitions or the establishment of additional

10

branches and may result in increases in operating expenses and reductions in revenues that could have a material adverse effect on its financial condition and results of operations.

We rely heavily on our management and other key personnel, and the loss of any of them may adversely affect our operations.

We are and will continue to be dependent upon the services of our management team. The loss of any of our senior managers could have an adverse effect on our growth and performance because of their skills, knowledge of the markets in which we operate and years of industry experience and the difficulty of promptly finding qualified replacement personnel. The loss of key personnel in a particular market could have an adverse effect on our performance in that market because it may be difficult to find qualified replacement personnel who are already located in or would be willing to relocate to a non-metropolitan market.

Our ability to retain key officers and employees may be further impacted by legislation and regulation affecting the financial services industry. On June 10, 2009, the U.S. Treasury released an interim final rule (the "IFR"), effective June 15, 2009, that provided guidance on the compensation and governance standards for participants in Treasury's Capital Purchase Program, and promulgated regulations to implement the restrictions and standards set forth in Section 7001 of ARRA. Among other things, the IFR and ARRA significantly expanded the executive compensation restrictions previously imposed by EESA. Such restrictions apply to any entity that has received or will receive financial assistance under the Capital Purchase Program, and shall generally continue to apply for as long as any obligation arising from such financial assistance, including preferred stock issued under the Capital Purchase Program, remains outstanding. These ARRA restrictions shall not apply to any participant during such time when the federal government (i) only holds any warrants to purchase common stock of such recipient or (ii) does not hold any preferred stock or warrants to purchase common stock of such recipient. As a result of our participation in the Capital Purchase Program, the restrictions and standards set forth in Section 7001 of ARRA, as well as the IFR promulgated by the U.S. Treasury, shall be applicable to us. Such restrictions and standards may further impact management's ability to compete with financial institutions that are not subject to the same limitations as we are under Section 7001 of ARRA and the IFR.

The geographic concentration of our markets makes our business highly susceptible to local economic conditions.

Unlike larger banking organizations that are more geographically diversified, our operations are currently concentrated in 32 counties in Indiana, three counties in Illinois, two counties in Ohio, and three counties in Kentucky. As a result of this geographic concentration in four fairly contiguous markets, our financial results depend largely upon economic conditions in these market areas. A deterioration in economic conditions in one or all of these markets could result in one or more of the following:

- •

- an increase in loan delinquencies;

- •

- an increase in problem assets and foreclosures;

- •

- a decrease in the demand for our products and services; or

- •

- a decrease in the value of collateral for loans, especially real estate, in turn reducing customers' borrowing power, the value of assets associated with problem loans and collateral coverage.

If we do not adjust to rapid changes in the financial services industry, our financial performance may suffer.

We face substantial competition for deposit, credit and trust relationships, as well as other sources of funding in the communities we serve. Competing providers include other banks, thrifts and trust companies, insurance companies, mortgage banking operations, credit unions, finance companies, money market funds and other financial and nonfinancial companies which may offer products functionally equivalent to those offered by our banks. Competing providers may have greater financial resources than we do and offer services within and outside the market areas we serve. In addition to this challenge of attracting and retaining customers for traditional banking services, our competitors now include securities dealers, brokers, mortgage bankers, investment advisors and finance and insurance companies who seek to offer one-stop financial services to their customers that may include services that banks have not been able or allowed to offer to their customers in the past. The increasingly competitive environment is primarily a result of changes in regulation, changes in technology and product delivery systems and the accelerating pace of consolidation among financial service providers. If we are unable to adjust both to increased competition for traditional banking services and changing customer needs and preferences, it could adversely affect our financial performance and your investment in our common stock.

Our historical growth and financial performance trends may not continue if our acquisition strategy is not successful.

Growth in asset size and earnings through acquisitions has been an important part of our business strategy. As consolidation of the banking industry continues, the competition for suitable acquisition candidates may increase. We compete with other banking companies for acquisition opportunities, and many of these competitors have greater financial resources and acquisition experience than we do and may be able to pay more for an acquisition than we are able or willing to pay. We also may need additional debt or

11

equity financing in the future to fund acquisitions. We may not be able to obtain additional financing or, if available, it may not be in amounts and on terms acceptable to us. We may use our common stock as the consideration for an acquisition or we may issue additional common stock and use the proceeds for the acquisition. Our issuance of additional securities will dilute your equity interest in us and may have a dilutive effect on our earnings per share. If we are unable to locate suitable acquisition candidates willing to sell on terms acceptable to us, or we are otherwise unable to obtain additional debt or equity financing necessary for us to continue our acquisition strategy, we would be required to find other methods to grow our business and we may not grow at the same rate we have in the past, or at all.

Acquisitions entail risks which could negatively affect our operations.

Acquisitions involve numerous risks, including:

- •

- exposure to asset quality problems of the acquired institution;

- •

- maintaining adequate regulatory capital;

- •

- diversion of management's attention from other business concerns;

- •

- risks and expenses of entering new geographic markets;

- •

- potential significant loss of depositors or loan customers from the acquired institution; or

- •

- exposure to undisclosed or unknown liabilities of an acquired institution.

Any of these acquisition risks could result in unexpected losses or expenses and thereby reduce the expected benefits of the acquisition.

Unanticipated costs related to our acquisitions could reduce MainSource's future earnings per share.

MainSource believes it has reasonably estimated the likely costs of integrating the operations of the banks it acquires into MainSource and the incremental costs of operating such banks as a part of the MainSource family. However, it is possible that unexpected transaction costs such as taxes, fees or professional expenses or unexpected future operating expenses, such as increased personnel costs or increased taxes, as well as other types of unanticipated adverse developments, could have a material adverse effect on the results of operations and financial condition of MainSource. If unexpected costs are incurred, acquisitions could have a dilutive effect on MainSource's earnings per share. Current accounting guidance requires expensing of acquisition costs. In prior years, these costs could be capitalized. In other words, if MainSource incurs such unexpected costs and expenses as a result of its acquisitions, MainSource believes that the earnings per share of MainSource common stock could be less than they would have been if those acquisitions had not been completed.

MainSource may be unable to successfully integrate the operations of the banks it has acquired and may acquire in the future and retain employees of such banks.

MainSource's acquisition strategy involves the integration of the banks MainSource has acquired and may acquire in the future as MainSource subsidiary banks. The difficulties of integrating the operations of such banks with MainSource and its other subsidiary banks include:

- •

- coordinating geographically separated organizations;

- •

- integrating personnel with diverse business backgrounds;

- •

- combining different corporate cultures; or

- •

- retaining key employees.

The process of integrating operations could cause an interruption of, or loss of momentum in, the activities of one or more of MainSource, its subsidiary banks and the banks MainSource has acquired and may acquire in the future and the loss of key personnel. The integration of such banks as MainSource subsidiary banks requires the experience and expertise of certain key employees of such banks who are expected to be retained by MainSource. We cannot be sure, however, that MainSource will be successful in retaining these employees for the time period necessary to successfully integrate such banks' operations as subsidiary banks of MainSource. The diversion of management's attention and any delays or difficulties encountered in connection with the mergers, along with the integration of the banks as MainSource subsidiary banks, could have an adverse effect on the business and results of operation of MainSource.

12

Risks Relating to the Banking Industry

Changes in governmental regulation and legislation could limit our future performance and growth.

We are subject to extensive state and federal regulation, supervision and legislation that govern almost all aspects of our operations, as well as any acquisitions we may propose to make. Any change in applicable federal or state laws or regulations could have a substantial impact on us, our subsidiary banks and our operations. While we cannot predict what effect any presently contemplated or future changes in the laws or regulations or their interpretations would have on us, these changes could reduce the value of your investment.

Changes in regulation or oversight may have a material adverse impact on our operations.

We are subject to extensive regulation, supervision and examination by the Indiana Department of Financial Institutions, the Federal Deposit Insurance Corporation, the Board of Governors of the Federal Reserve System, the Securities and Exchange Commission and other regulatory bodies. Such regulation and supervision governs the activities in which we may engage. Regulatory authorities have extensive discretion in their supervisory and enforcement activities, including the imposition of restrictions on our operations, investigations and limitations related to our securities, the classification of our assets and determination of the level of our allowance for loan losses. In light of the current conditions in the U.S. financial markets and economy, Congress and regulators have increased their focus on the regulation of the financial services industry. Any change in such regulation and oversight, whether in the form of regulatory policy, regulations, legislation or supervisory action, may have a material adverse impact on our business, financial condition or results of operations.

The Company may be subject to future goodwill impairment charges

During 2009, the Company recorded $80,310 in goodwill impairment charges in the second and fourth quarters. While the Company does not currently anticipate that there will be additional impairment charges required in the future, it can make no guarantees that none will be taken. If more impairment is recorded, it will have a negative impact on future earnings.

Risks Related to the Company's Stock

We may not be able to pay dividends in the future in accordance with past practice.

The Company has traditionally paid a quarterly dividend to common stockholders. The payment of dividends is subject to legal and regulatory restrictions. Any payment of dividends in the future will depend, in large part, on the Company's earnings, capital requirements, financial condition and other factors considered relevant by the Company's Board of Directors. Starting in the second quarter of 2009 and continuing to the present, the Company reduced the amount of cash dividends paid. This reduction was made to preserve capital levels at the Company. The Company may also be limited in the amount of dividends paid out as a result of its participation in the Department of the Treasury Capital Purchase Program.

The price of the Company's common stock may be volatile, which may result in losses for investors.

General market price declines or market volatility in the future could adversely affect the price of the Company's common stock. In addition, the following factors may cause the market price for shares of the Company's common stock to fluctuate:

- •

- announcements of developments related to the Company's business;

- •

- fluctuations in the Company's results of operations;

- •

- sales or purchases of substantial amounts of the Company's securities in the marketplace;

- •

- general conditions in the Company's banking niche or the worldwide economy;

- •

- a shortfall or excess in revenues or earnings compared to securities analysts' expectations;

- •

- changes in analysts' recommendations or projections; and

- •

- the Company's announcement of new acquisitions or other projects.

13

The Company's participation in Treasury's Capital Purchase Program (CPP) may adversely affect the value of its common stock and the rights of its common stockholders.

The rights of the holders of the Company's common stock may be adversely affected by the Company's participation in the CPP. For example:

- •

- Prior to the earlier of January 16, 2012 and the date on which all of the Preferred Shares have been redeemed by

the Company or transferred by Treasury to third parties, the Company may not, without the consent of Treasury, subject to limited exceptions, redeem, repurchase, or otherwise acquire shares of the

Company's common stock or preferred stock.

- •

- The Company may not pay dividends on its common stock unless it has fully paid all required dividends on the Preferred

Shares. Although the Company fully expects to be able to pay all required dividends on the Preferred Shares, there is no guarantee that it will be able to do so.

- •

- As long as the Treasury owns the securities purchased from the Company under the CPP, the Company may not, without the

prior consent of the Treasury, increase the quarterly dividends it pays on its common stock above $0.145 per share.

- •

- The Preferred Shares will receive preferential treatment in the event of liquidation, dissolution, or winding up of the

Company.

- •

- The ownership interest of the existing holders of the Company's common stock will be diluted to the extent the warrant the Company issued to Treasury in conjunction with the sale to Treasury of the Preferred Shares is exercised.

In addition, terms of the Preferred Shares require that quarterly dividends be paid on the Preferred Shares at the rate of 5% per annum for the first five years and 9% per annum thereafter until the stock is redeemed by the Company. The payments of these dividends will decrease the excess cash the Company otherwise has available to pay dividends on its common stock and to use for general corporate purposes, including working capital.

The Company's charter documents and federal regulations may inhibit a takeover, prevent a transaction that may favor or otherwise limit the Company's growth opportunities, which could cause the market price of the Company's common stock to decline.

Certain provisions of the Company's charter documents and federal regulations could have the effect of making it more difficult for a third party to acquire, or of discouraging a third party from attempting to acquire, control of the Company. In addition, the Company must obtain approval from regulatory authorities before acquiring control of any other company.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

As of December 31, 2009, the Company leased an office building from one of its subsidiaries for use as its corporate headquarters. The Company's subsidiaries own, or lease, all of the facilities from which they conduct business. All leases are comparable to other leases in the respective market areas and do not contain provisions materially detrimental to the Company or its subsidiaries. As of December 31, 2009 the Company had 85 banking locations. In addition, the Company operates twelve insurance offices in Indiana and one in Illinois. At December 31, 2009, the Company had approximately $49,499 invested in premises and equipment.

The Company and its subsidiaries may be parties (both plaintiff and defendant) to ordinary litigation incidental to the conduct of business. Management is presently not aware of any material pending or contemplated legal proceedings.

ITEM 4. (REMOVED AND RESERVED)

14

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER'S PURCHASES OF EQUITY SECURITIES

Market Information

The Company's Common Stock is traded on the NASDAQ Stock Market under the symbol MSFG. The Common Stock was held by approximately 5,000 shareholders at March 10, 2010. The quarterly high and low closing prices for the Company's common stock as reported by NASDAQ and quarterly cash dividends declared and paid are set forth in the tables below. All per share data is retroactively restated for all stock dividends and splits.

The range of known per share prices by calendar quarter, based on actual transactions, excluding commissions, is shown below.

| |

Market Prices | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2009 |

Q1 |

Q2 |

Q3 |

Q4 |

|||||||||

High |

$ | 15.16 | $ | 10.35 | $ | 7.74 | $ | 7.04 | |||||

Low |

$ | 4.85 | $ | 7.00 | $ | 5.64 | $ | 4.45 | |||||

2008 |

Q1 |

Q2 |

Q3 |

Q4 |

|||||||||

High |

$ | 16.51 | $ | 17.59 | $ | 21.27 | $ | 21.02 | |||||

Low |

$ | 12.15 | $ | 13.45 | $ | 13.98 | $ | 12.74 | |||||

| |

Cash Dividends | ||||||||||||

2009 |

Q1 |

Q2 |

Q3 |

Q4 |

|||||||||

|

$ | 0.145 | $ | 0.050 | $ | 0.050 | $ | 0.010 | |||||

2008 |

Q1 |

Q2 |

Q3 |

Q4 |

|||||||||

|

$ | 0.140 | $ | 0.145 | $ | 0.145 | $ | 0.145 | |||||

It is expected that the Company will continue to pay its reduced dividend for the foreseeable future, until the Company determines that its results of operations, its capital levels and other external factors beyond management's control make it prudent to raise the dividend, and until the Company determines that its earnings are sufficient to repurchase the preferred shares held by the U.S. Treasury pursuant to Treasury's Capital Purchase Program. As a participant in the U.S. Treasury's Capital Purchase Program, the Company is prohibited from increasing cash dividends on common stock above $0.145 per share per quarter without prior government permission for a period of three years from the date of participation, which was January 16, 2009, unless the preferred shares issued to Treasury are no longer held by Treasury. Additionally, no dividends may be paid on the common stock unless and until all accrued and unpaid dividends for all past dividend periods owed to the Treasury on the preferred shares are fully paid. See Note 27 to the Consolidated Financial Statements for additional details on the Company's participation in the Capital Purchase Program.

Equity Compensation Plan Information

The following table sets forth information regarding securities authorized for issuance under the Company's equity compensation plans as of December 31, 2009:

| Plan category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights (a) |

Weighted-average exercise price of outstanding options, warrants and rights (b) |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

Equity compensation plans approved by security holders |

429,608 | $ | 13.30 | 453,833 | ||||||

Equity compensation plans not approved by security holders |

— | — | — | |||||||

Total |

429,608 | $ | 13.30 | 453,833 | ||||||

15

Stock Performance Graph

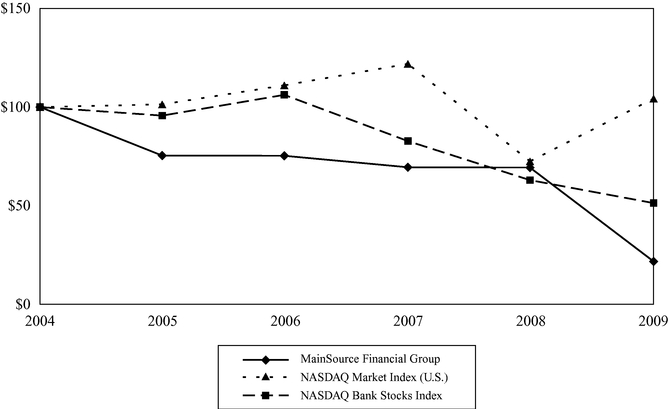

The following performance graph compares the performance of our common shares to the performance of the NASDAQ Market Index (U.S.) and the NASDAQ Bank Stocks Index for the 60 months ended December 31, 2009. The graph assumes an investment of $100 in each of the Company's common shares, the NASDAQ Market Index (U.S.) and the NASDAQ Bank Stocks Index on December 31, 2004.

| |

12/31/04 |

12/31/05 |

12/31/06 |

12/31/07 |

12/31/08 |

12/31/09 |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MainSource Financial Group |

$ | 100.00 | $ | 75.41 | $ | 75.30 | $ | 69.48 | $ | 69.31 | $ | 21.72 | |||||||

NASDAQ MARKET INDEX (U.S.) |

100.00 | 101.37 | 111.03 | 121.92 | 72.49 | 104.31 | |||||||||||||

NASDAQ Bank Stocks Index |

100.00 | 95.67 | 106.20 | 82.76 | 62.96 | 51.31 | |||||||||||||

16

ITEM 6. SELECTED FINANCIAL DATA

Selected Financial Data

(Dollar amounts in thousands except per share data)

| |

2009 |

2008 |

2007 |

2006 |

2005 |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Results of Operations |

||||||||||||||||||

Net interest income |

$ | 98,008 | $ | 87,525 | $ | 74,397 | $ | 68,268 | $ | 53,648 | ||||||||

Provision for loan losses |

46,310 | 20,918 | 5,745 | 1,819 | 1,040 | |||||||||||||

Noninterest income |

40,050 | 29,697 | 28,126 | 23,039 | 17,332 | |||||||||||||

Noninterest expense |

167,532 | 72,773 | 68,020 | 59,642 | 48,576 | |||||||||||||

Income (loss) before income tax |

(75,784 | ) | 23,531 | 28,758 | 29,846 | 21,364 | ||||||||||||

Income tax (benefit) |

(11,645 | ) | 4,379 | 6,888 | 7,605 | 5,172 | ||||||||||||

Net income (loss) |

(64,139 | ) | 19,152 | 21,870 | 22,241 | 16,192 | ||||||||||||

Preferred dividends and accretion |

(2,919 | ) | — | — | — | — | ||||||||||||

Net income (loss) available to common shareholders |

(67,058 | ) | 19,152 | 21,870 | 22,241 | 16,192 | ||||||||||||

Dividends paid on common stock |

5,135 | 11,133 | 10,392 | 8,944 | 6,514 | |||||||||||||

Per Common Share* |

||||||||||||||||||

Earnings (loss) per share (basic) |

$ | (3.33 | ) | $ | 1.00 | $ | 1.17 | $ | 1.30 | $ | 1.23 | |||||||

Earnings (loss) per share (diluted) |

(3.33 | ) | 1.00 | 1.17 | 1.29 | 1.23 | ||||||||||||

Dividends paid |

0.255 | 0.575 | 0.555 | 0.529 | 0.495 | |||||||||||||

Book value — end of period |

11.84 | 14.90 | 14.22 | 13.50 | 11.39 | |||||||||||||

Market price — end of period |

4.78 | 15.50 | 15.56 | 16.94 | 17.00 | |||||||||||||

At Year End |

||||||||||||||||||

Total assets |

$ | 2,906,530 | $ | 2,899,835 | $ | 2,536,437 | $ | 2,429,773 | $ | 1,645,605 | ||||||||

Investment securities |

714,607 | 513,310 | 489,739 | 485,259 | 450,814 | |||||||||||||

Loans, excluding held for sale |

1,885,447 | 1,995,601 | 1,693,678 | 1,574,384 | 957,995 | |||||||||||||

Allowance for loan losses |

46,648 | 34,583 | 14,331 | 12,792 | 10,441 | |||||||||||||

Total deposits |

2,270,650 | 2,009,324 | 1,901,829 | 1,859,689 | 1,352,697 | |||||||||||||

Federal Home Loan Bank advances |

222,265 | 433,167 | 257,099 | 208,443 | 41,547 | |||||||||||||

Subordinated debentures |

49,966 | 49,816 | 41,239 | 41,239 | 29,898 | |||||||||||||

Shareholders' equity |

294,462 | 299,949 | 264,102 | 253,247 | 161,069 | |||||||||||||

Financial Ratios |

||||||||||||||||||

Return on average assets |

(2.19 | )% | 0.73 | % | 0.90 | % | 1.06 | % | 1.04 | % | ||||||||

Return on average common shareholders' equity |

(22.61 | ) | 6.90 | 8.49 | 10.39 | 11.27 | ||||||||||||

Allowance for loan losses to total loans (year end, excluding held for sale) |

2.47 | 1.73 | 0.85 | 0.81 | 1.09 | |||||||||||||

Allowance for loan losses to total non-performing loans (year end) |

58.05 | 58.31 | 69.93 | 73.18 | 102.19 | |||||||||||||

Shareholders' equity to total assets (year end) |

10.13 | 10.34 | 10.41 | 10.42 | 9.79 | |||||||||||||

Average equity to average total assets |

11.59 | 10.57 | 10.57 | 10.13 | 9.18 | |||||||||||||

Dividend payout ratio |

NM | 58.13 | 47.52 | 40.21 | 40.23 | |||||||||||||

- *

- Adjusted

for stock split and dividends

- NM

- Not meaningful

17

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management's Discussion and Analysis

(Dollar amounts in thousands except per share data)

Forward-Looking Statements

Except for historical information contained herein, the discussion in this Annual Report includes certain forward-looking statements based upon management expectations. Actual results and experience could differ materially from the anticipated results or other expectations expressed in the Company's forward-looking statements. The Company disclaims any intent or obligation to update such forward looking statements. Factors which could cause future results to differ from these expectations include the following: general economic conditions; legislative and regulatory initiatives; monetary and fiscal policies of the federal government; deposit flows; the cost of funds; general market rates of interest; interest rates on competing investments; demand for loan products; demand for financial services; changes in accounting policies or guidelines; changes in the quality or composition of the Company's loan and investment portfolios; the Company's ability to integrate acquisitions, the impact of our continuing acquisition strategy, and other factors, including the risk factors set forth in Item 1A of this Annual Report on Form 10-K and in other reports we file from time to time with the Securities and Exchange Commission. The Company intends the forward looking statements set forth herein to be covered by the safe harbor provisions for forward looking statements contained in the Private Securities Litigation Reform Act of 1995.

Overview

MainSource Financial Group, Inc. ("MainSource" or the "Company") is a financial holding company whose principal activity is the ownership and management of its wholly owned subsidiary bank: MainSource Bank headquartered in Greensburg, Indiana (the "Bank"). The Bank operates under an Indiana state charter and is subject to regulation by the Indiana Department of Financial Institutions and the Federal Deposit Insurance Corporation. Non-banking subsidiaries include MainSource Insurance, LLC and MainSource Title, LLC. Both of these subsidiaries are subject to regulation by the Indiana Department of Insurance.

Business Strategy

The Company operates under the broad tenets of a long-term strategic plan ("Plan") designed to improve the Company's financial performance, expand its competitive position and enhance long-term shareholder value. The Plan is premised on the belief of the Company's Board of Directors that it can best promote long-term shareholder interests by pursuing strategies which will continue to preserve its community-focused philosophy. The dynamics of the Plan assure continually evolving goals, with the enhancement of shareholder value being the constant, overriding objective. The extent of the Company's success will depend upon how well it anticipates and responds to competitive changes within its markets, the interest rate environment and other external forces.

Results of Operations