Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Wendy's Co | form8-k_030410.htm |

EXHIBIT 99.1

Fourth

Quarter and Full-Year 2009

Earnings Call

Earnings Call

March

4, 2010

Opening

Comments

John

Barker

SVP and Chief Communications Officer

SVP and Chief Communications Officer

2

§ Business

Highlights - Roland Smith

− Fourth

quarter

− Full-year

2009

§ Financial

Results - Steve Hare

− Fourth

quarter consolidated financial overview

− Full-year

2009 results

− G&A

synergies

− Cash flow and

debt capitalization

− Dividend and

stock repurchase program

§ 2010 Overview

- Steve Hare & Roland Smith

§ Q&A

Agenda

3

Wendy’s/Arby’s

Group Reported Today:

§ Fourth

Quarter and Full-Year 2009 Results

− Q4

2009

− Full-year

2009 is not comparable to 2008 due to the merger

§ Balance Sheet

Highlights

§ Adjusted

EBITDA Compared to Pro-forma Adjusted EBITDA

§ Selected

Financial Highlights for Each Brand

§ Form

10-K

Fourth

Quarter 2009

4

Forward-Looking

Statements and

Regulation G

Regulation G

This

presentation, and certain information that management may discuss in connection

with this

presentation, may contain statements that are not historical facts, including, importantly,

information concerning possible or assumed future results of our operations. Those statements

constitute “forward-looking statements” within the meaning of the Private Securities Litigation

Reform Act of 1995 (the “Reform Act”). For all our forward-looking statements, we claim the

protection of the safe harbor for forward-looking statements contained in the Reform Act.

presentation, may contain statements that are not historical facts, including, importantly,

information concerning possible or assumed future results of our operations. Those statements

constitute “forward-looking statements” within the meaning of the Private Securities Litigation

Reform Act of 1995 (the “Reform Act”). For all our forward-looking statements, we claim the

protection of the safe harbor for forward-looking statements contained in the Reform Act.

Many

important factors could affect our future results and could cause those results

to differ

materially from those expressed in or implied by our forward-looking statements. Such factors,

all of which are difficult or impossible to predict accurately, and many of which are beyond our

control, include but are not limited to those identified under the caption “Forward-Looking

Statements” in our most recent earnings press release and in the “Special Note Regarding

Forward-Looking Statements and Projections” and “Risk Factors” sections of our most recent

Form 10-K and subsequent Form 10-Qs.

materially from those expressed in or implied by our forward-looking statements. Such factors,

all of which are difficult or impossible to predict accurately, and many of which are beyond our

control, include but are not limited to those identified under the caption “Forward-Looking

Statements” in our most recent earnings press release and in the “Special Note Regarding

Forward-Looking Statements and Projections” and “Risk Factors” sections of our most recent

Form 10-K and subsequent Form 10-Qs.

In addition,

this presentation and certain information management may discuss in

connection

with this presentation reference non-GAAP financial measures, such as earnings before

interest, taxes, depreciation and amortization, or EBITDA. Reconciliations of non-GAAP

financial measures to the most directly comparable GAAP financial measure are in the

Appendix to this presentation, and are included in the earnings release and posted on the

Investor Relations section of our website.

with this presentation reference non-GAAP financial measures, such as earnings before

interest, taxes, depreciation and amortization, or EBITDA. Reconciliations of non-GAAP

financial measures to the most directly comparable GAAP financial measure are in the

Appendix to this presentation, and are included in the earnings release and posted on the

Investor Relations section of our website.

Fourth

Quarter and

Full-Year 2009 Highlights

Full-Year 2009 Highlights

Roland

Smith

President & Chief Executive Officer

President & Chief Executive Officer

6

§ Delivered

Strong Earnings Growth

– Adjusted

EBITDA* increased 16%

§ Produced

Margin Improvement at Wendy’s

– 330 basis

point improvement in company-operated stores

– Ahead of

schedule on improving Wendy’s restaurant margins by 500

basis points by end of 2011

basis points by end of 2011

§ Achieved Cost

Savings Ahead of Schedule

§ Repositioned

Wendy’s Brand

§ Drove Product

Innovation at Both Brands

§ Implemented

Improved Value Strategies at Both Brands

§ Formed

Wendy’s Purchasing Co-op

§ Delivered

Strong Cash Flow and Financial Flexibility

*See

Appendix.

2009

Key Accomplishments

7

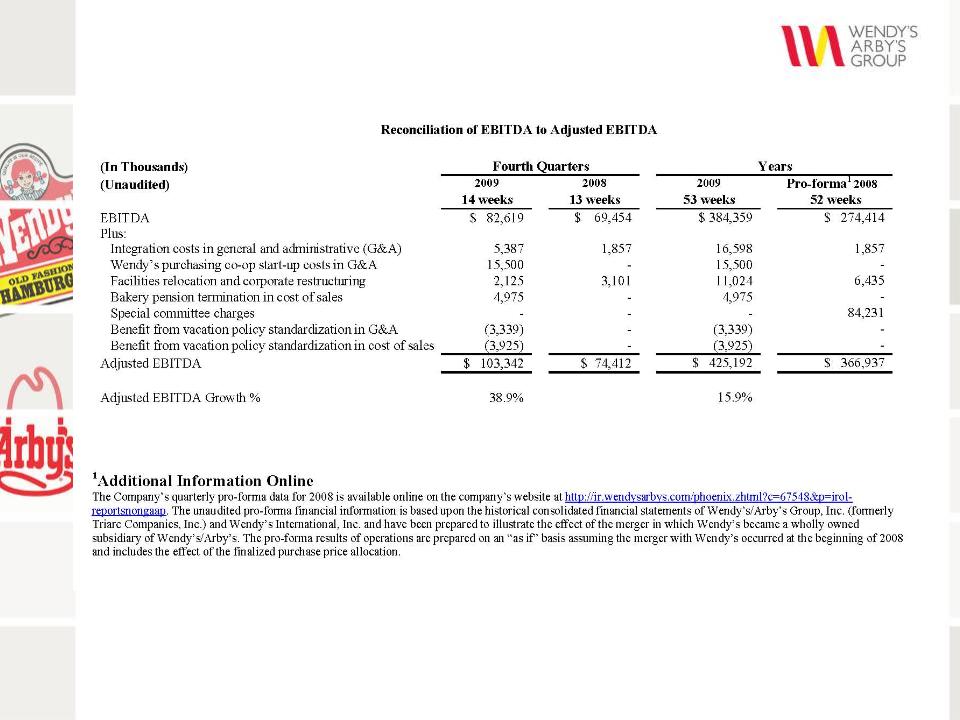

§ Adjusted

EBITDA* Grew 39% to $103.3 Million,

Including Effect of Additional Week in the Quarter

Including Effect of Additional Week in the Quarter

§ Strong Margin

Improvement at Wendy’s

− 420 basis

points improvement in company-operated stores

§ Sales and

Margins Declined at Arby’s

− Expanded

Everyday Value platform in Company units

*See

Appendix.

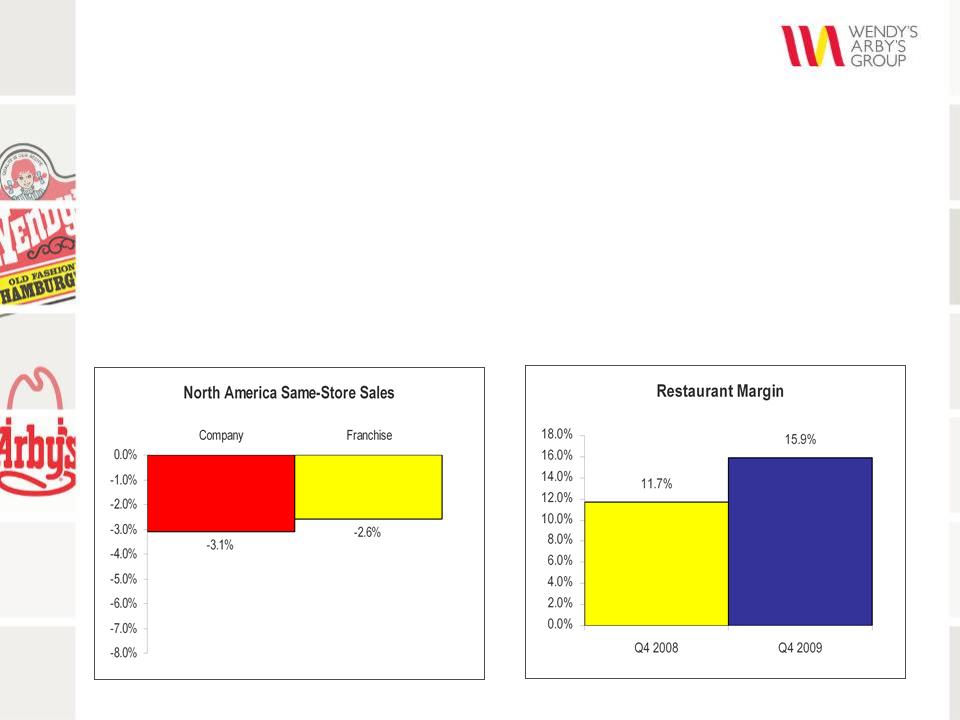

2009

Q4 Business Overview

8

Wendy’s

2009 Q4 Results

§ North America

Systemwide Same-Store Sales Declined 3%

− SSS among

strongest in the industry

− Impacted by

challenging economic trends and strong Q4 2008

SSS of +3.7%

SSS of +3.7%

§ 420 bps

Margin Increase Driven by Operations, Pricing and

Favorable Commodities

Favorable Commodities

* Excludes

the effect (-1.0%) of fewer restaurants serving breakfast.

*

9

Wendy’s

Full-Year 2009 Results

§ North America

Systemwide Same-Store Sales Declined 0.7%

− Among the

best in the industry during a challenging year

§ Strong Margin

Increase of 330 bps Driven by Operations

Improvements and Pricing with No Impact from Commodities

Improvements and Pricing with No Impact from Commodities

* Excludes

the effect (-1.4%) of fewer restaurants serving breakfast.

*

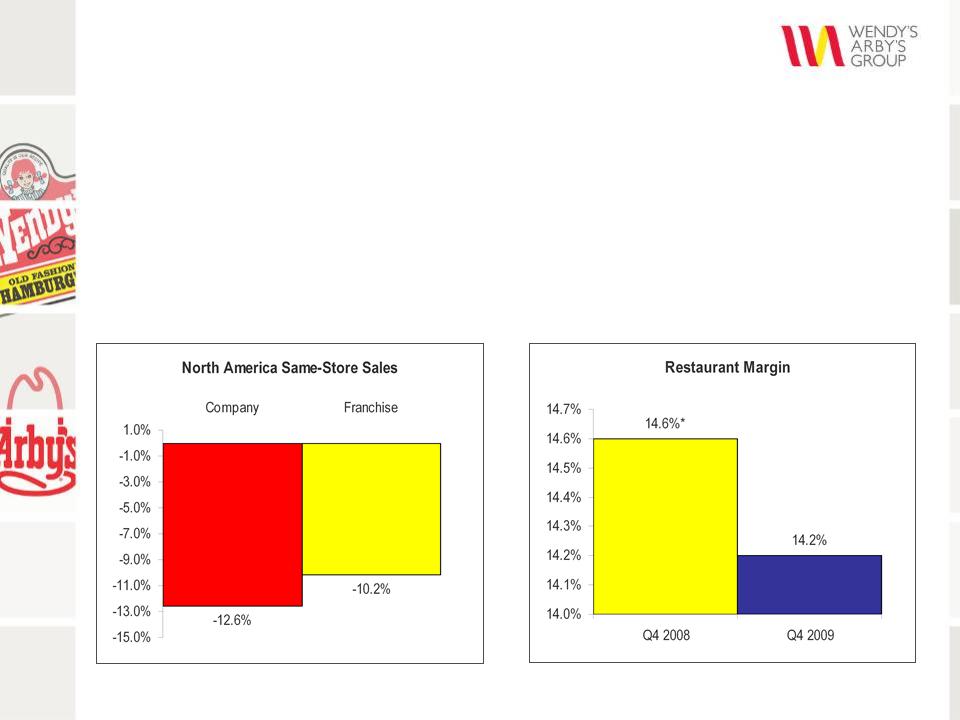

110

Arby’s

2009 Q4 Results

§ North America

Systemwide Same-Store Sales Declined 11%

− Impacted by

significant competitor discounting and challenging

economic trends

economic trends

§ Margin

Decreased Due to Sales Deleveraging

* Restaurant

Margin includes benefit of vacation policy

standardization (150 bps)

standardization (150 bps)

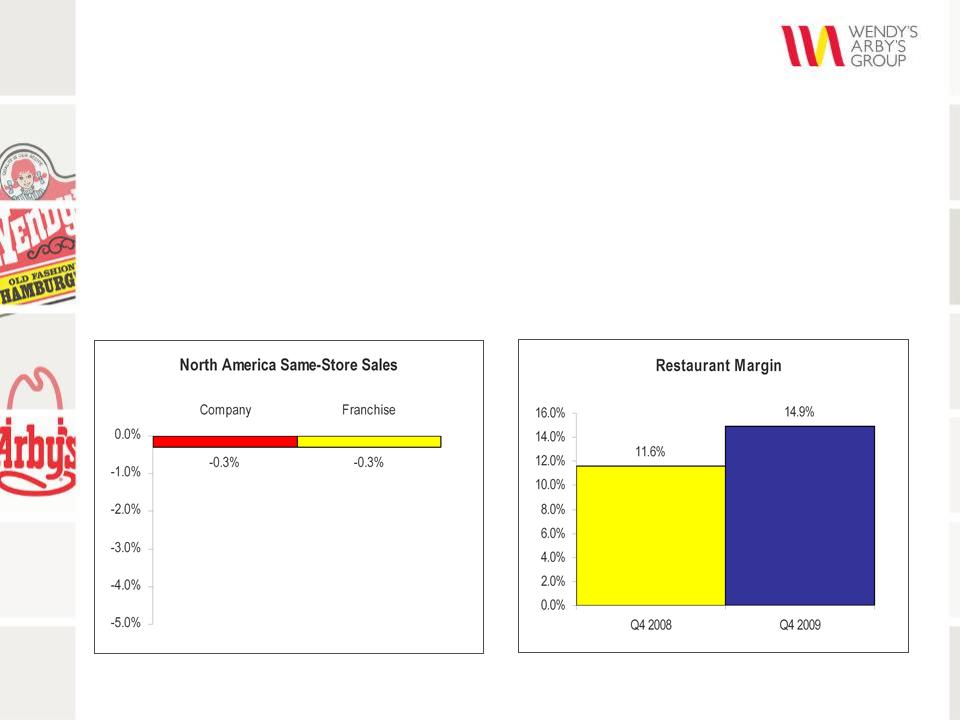

11

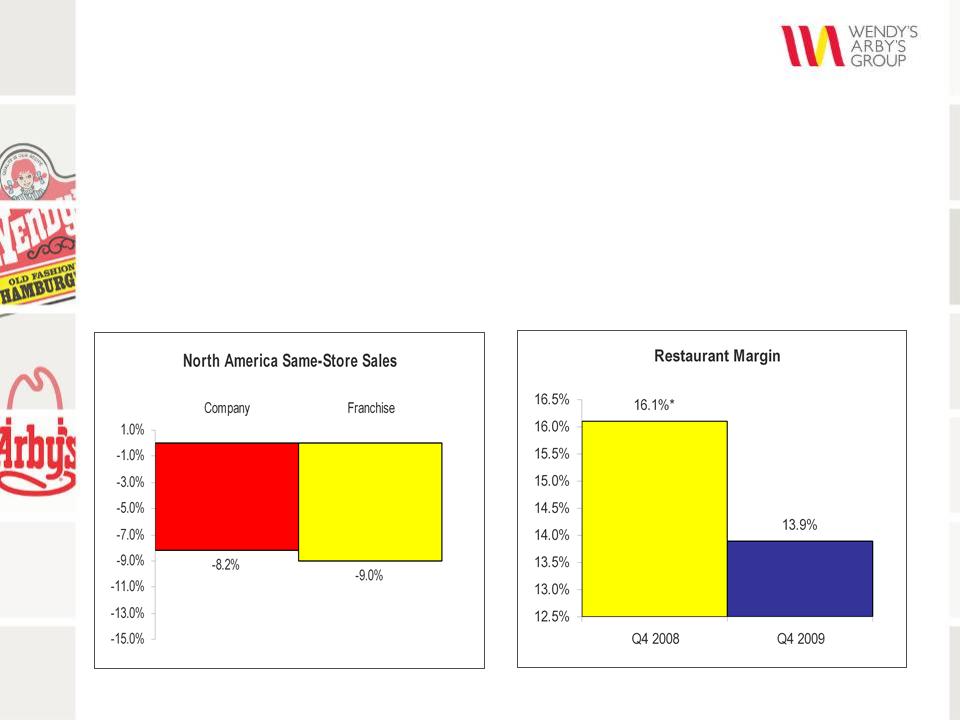

Arby’s

Full-Year 2009 Results

* Restaurant

Margin includes benefit of vacation policy

standardization (40 bps)

standardization (40 bps)

§ North America

Systemwide Same-Store Sales Declined 9%

− Impacted by

competitor discounting and lack of a value menu

offering

offering

§ Margins

Decreased Driven by Deleveraging

Financial

Overview

Steve Hare

Chief Financial Officer

13

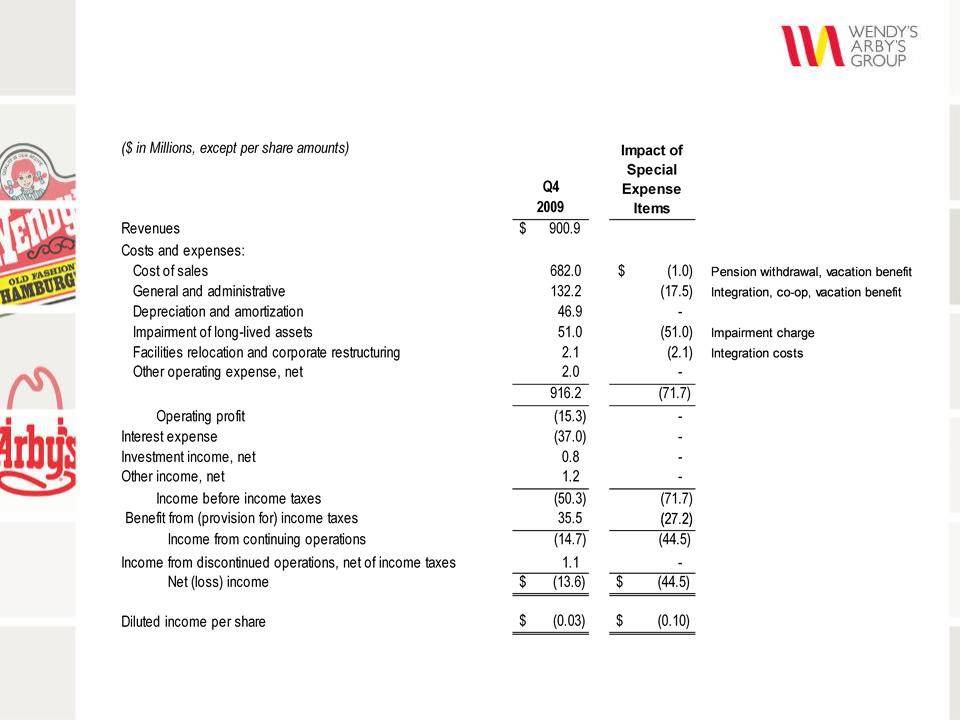

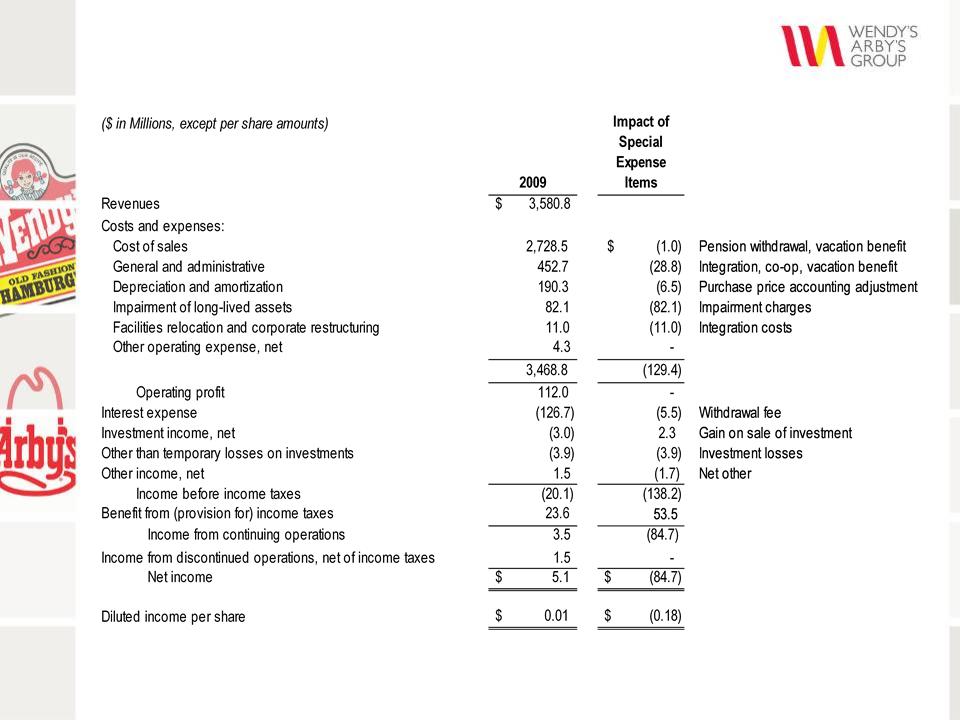

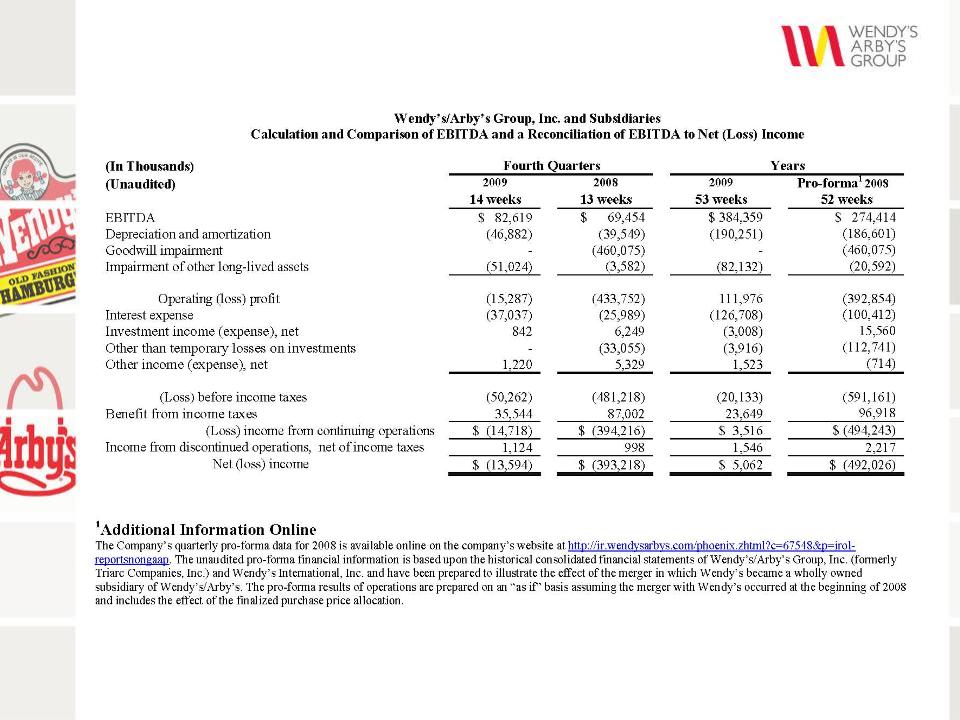

2009

Q4 Consolidated

Operating Results

Operating Results

14

*See

Appendix.

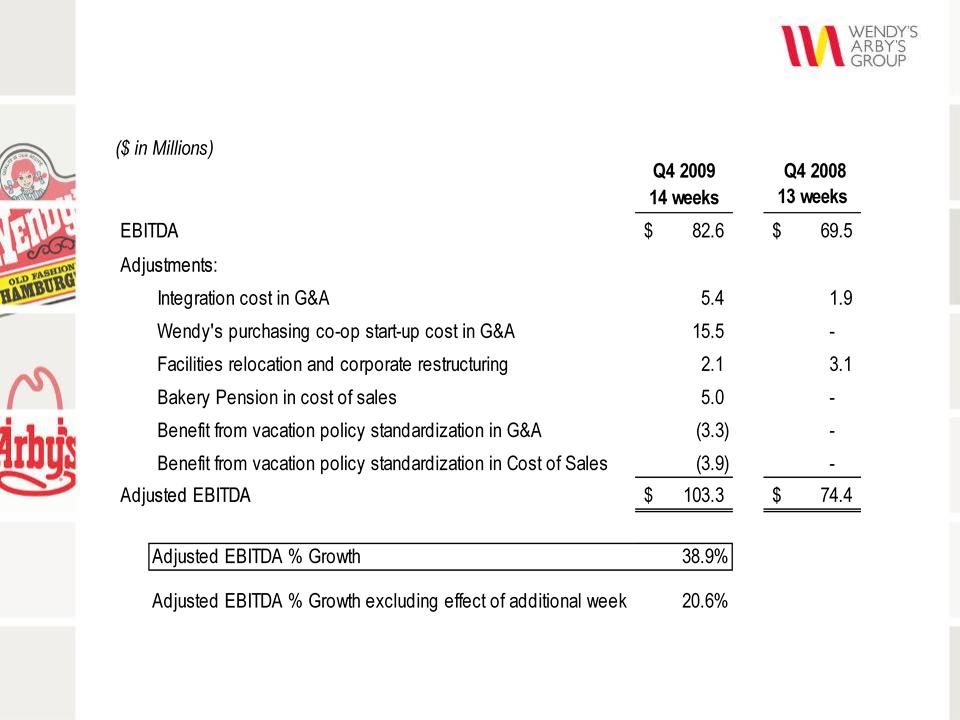

2009

Q4 EBITDA and

Adjusted EBITDA*

Adjusted EBITDA*

15

2009

Consolidated Operating Results

16

*See

Appendix.

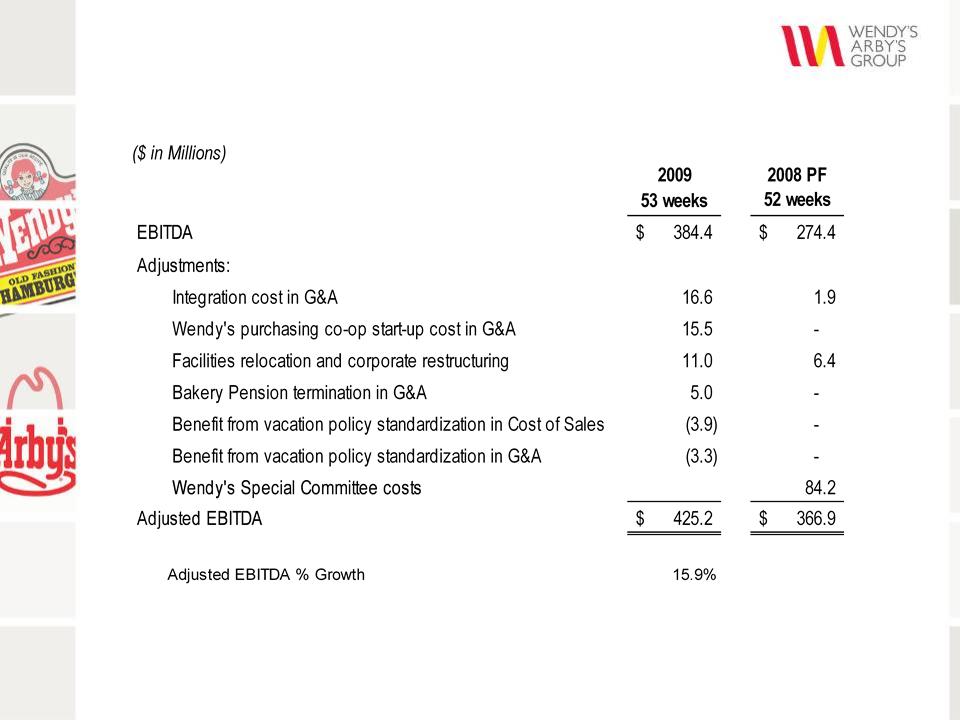

2009

EBITDA and Adjusted EBITDA*

17

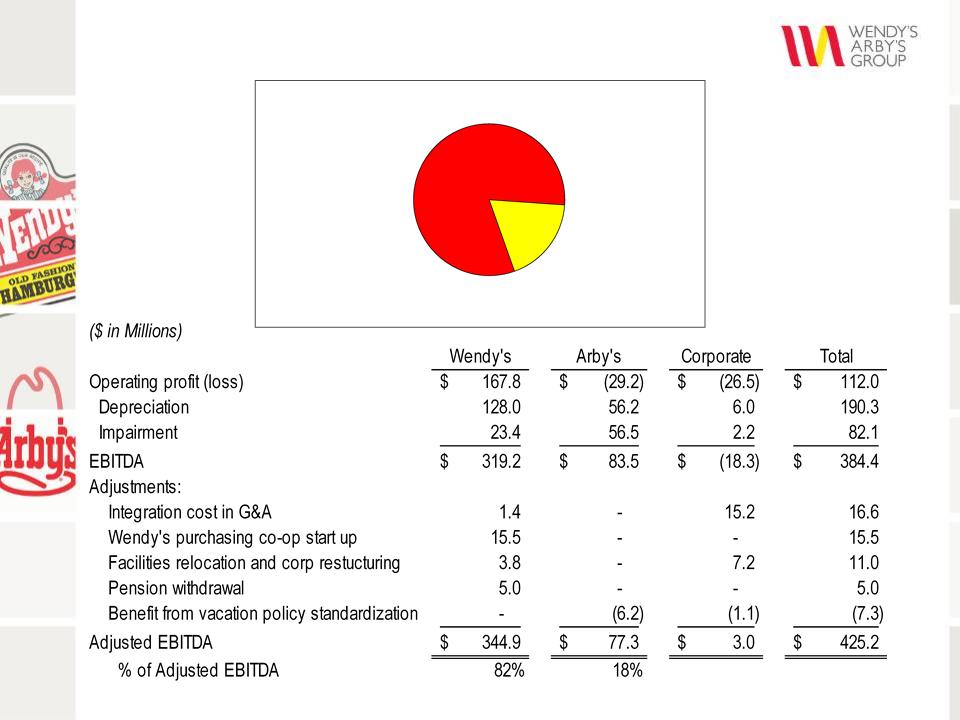

Wendy’s

Contributes Majority of Adjusted EBITDA

Wendy’s

82%

Arby’s

18%

%

of Consolidated Adjusted EBITDA

*See

Appendix.

2009

Adjusted EBITDA* by Brand

18

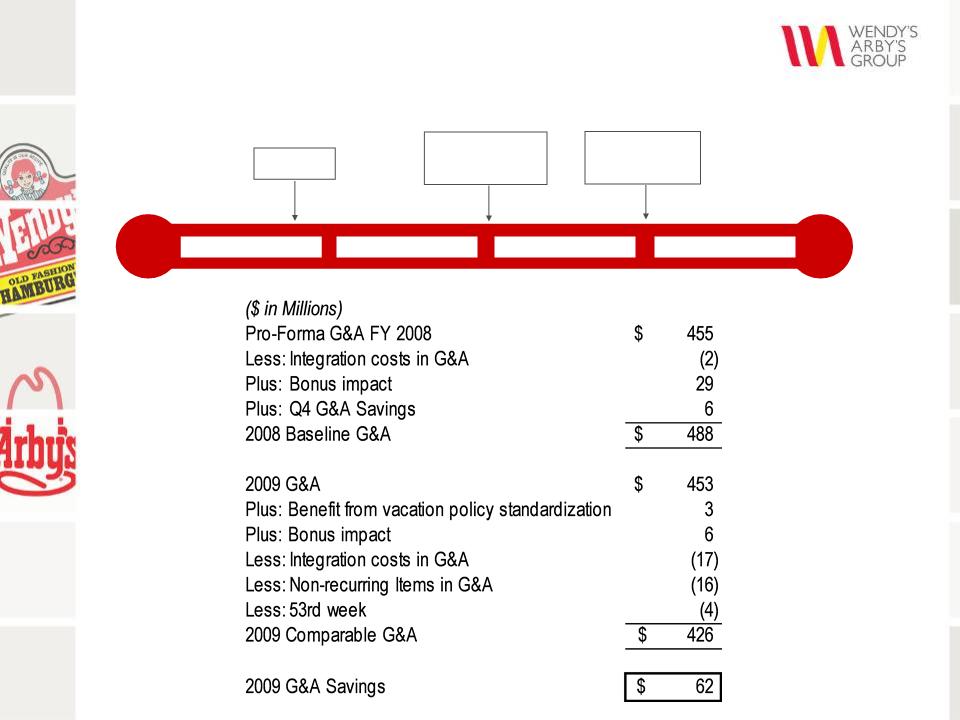

2008

2009

2010

2011

2009

Actual

$62

million

Plan

$60

million

Merger

Achieved

Targeted G&A

Synergies Ahead of Schedule

Synergies Ahead of Schedule

19

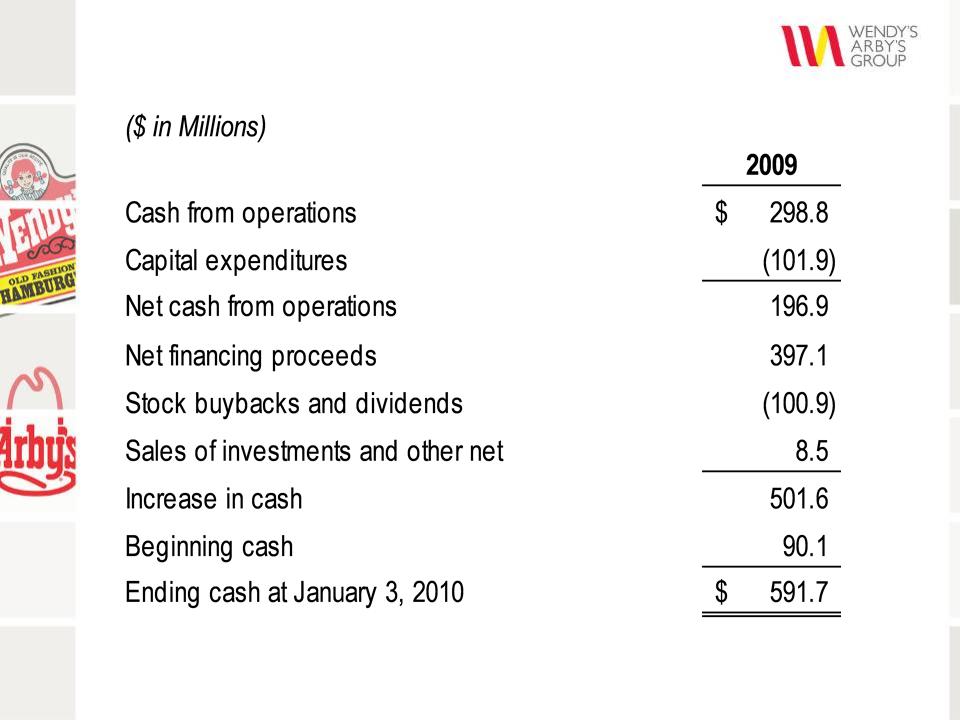

Strong

Cash Flow - 2009

20

(1)Adjusted EBITDA for 2008

is pro-forma. See appendix.

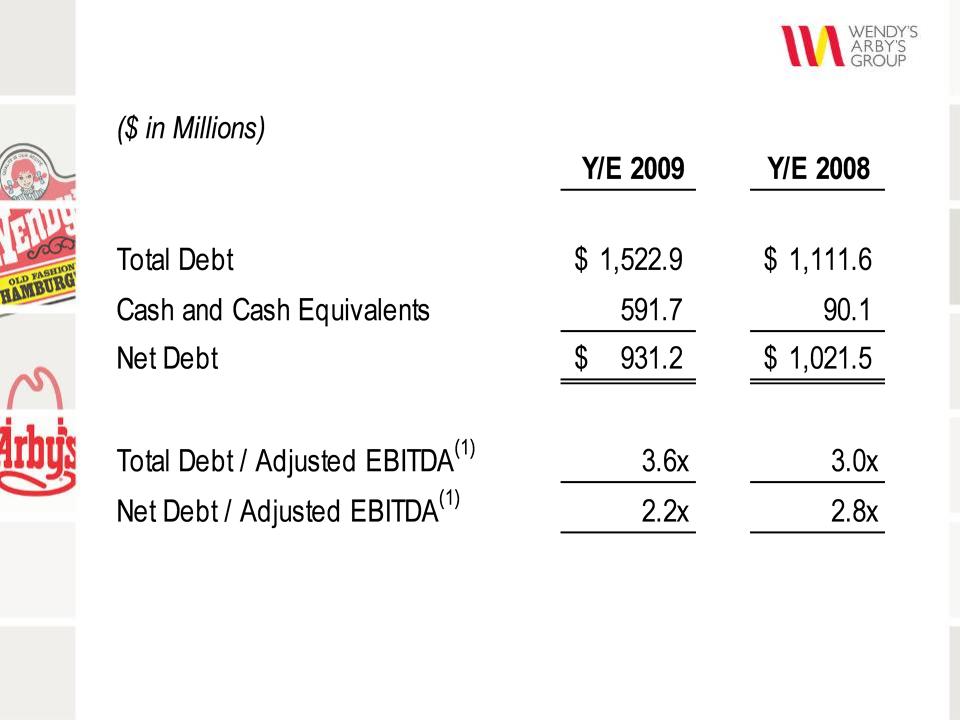

Debt

Capitalization

21

§ Board

Increased Stock Repurchase Authorization to

$200 Million

$200 Million

– Company

purchased $120.2 million of common stock as

of February 26, 2010

of February 26, 2010

– 26.1 million

shares for approximately $4.61 per share

– Company may

repurchase additional shares as market

conditions warrant through January 2, 2011

conditions warrant through January 2, 2011

§ Quarterly

Cash Dividend

– $0.015 per

share

– Payable on

March 15, 2010 to stockholders of record as

of March 1, 2010

of March 1, 2010

Recent

Board Actions

2010

Overview

23

Source: Bureau

of Labor Statistics.

Unemployment

rate

remains

high at 9.7%

No

job growth in

the

U.S.

24

Consumer

Confidence Continues to

Run Below Healthy Economic Levels

Run Below Healthy Economic Levels

Source:

The Conference Board

Consumer

confidence

fell

10 points to a

10-month

low

Consumer

Confidence Index

25

Consumers

Continue to Pay Down Debt

Causing Less Consumer Spending

Causing Less Consumer Spending

Source: Federal

Reserve

Consumer

Revolving Credit Outstanding:

%

Change vs. Year Ago

26

§ Anticipate

Weak Economic Conditions to Continue

– High

unemployment

– Weak consumer

confidence

§ Positive SSS

at Wendy’s

§ Negative SSS

at Arby’s, but Improving Year-over-Year

§ Total Capital

Expenditure of $165 Million

– Open 12 new

Wendy’s

– Remodel 100

Wendy’s and 100 Arby’s

§ Low-to-Mid

Single Digit Growth in Adjusted EBITDA

– Excludes

effect of 53rd week ($14 million in 2009)

– Excludes

investment spending on Wendy’s breakfast

($9 million in 2010)

($9 million in 2010)

Financial

Outlook 2010

2010

Brand Overview

Roland

Smith

President & Chief Executive Officer

President & Chief Executive Officer

Wendy’s

Brand

29

§ Drive

Positive Same-Store Sales

– Balance

premium and value

– Continue

product innovation

– Reinforce

“Real” brand positioning

– Strategic

pricing project

§ Continue

Margin Improvement

§ Optimize New

Purchasing Co-op

§ Re-Launch

Breakfast Program and Expand to New Market

§ Execute

Remodeling Program

Wendy’s

Initiatives in 2010

30

Wendy’s

1st Quarter Calendar

January

February

March

99¢

Premium

Cod

31

Wendy’s

Strategic Pricing

§ Implementing

a Strategic Pricing Initiative to Drive

Same-Store Sales and Margins

Same-Store Sales and Margins

§ History:

– Wendy’s

priced on a national basis

– Over the past

two years, moved to regional pricing

§ New strategy

will price on a store-by-store basis

– Expect

benefit in 2011 and beyond

32

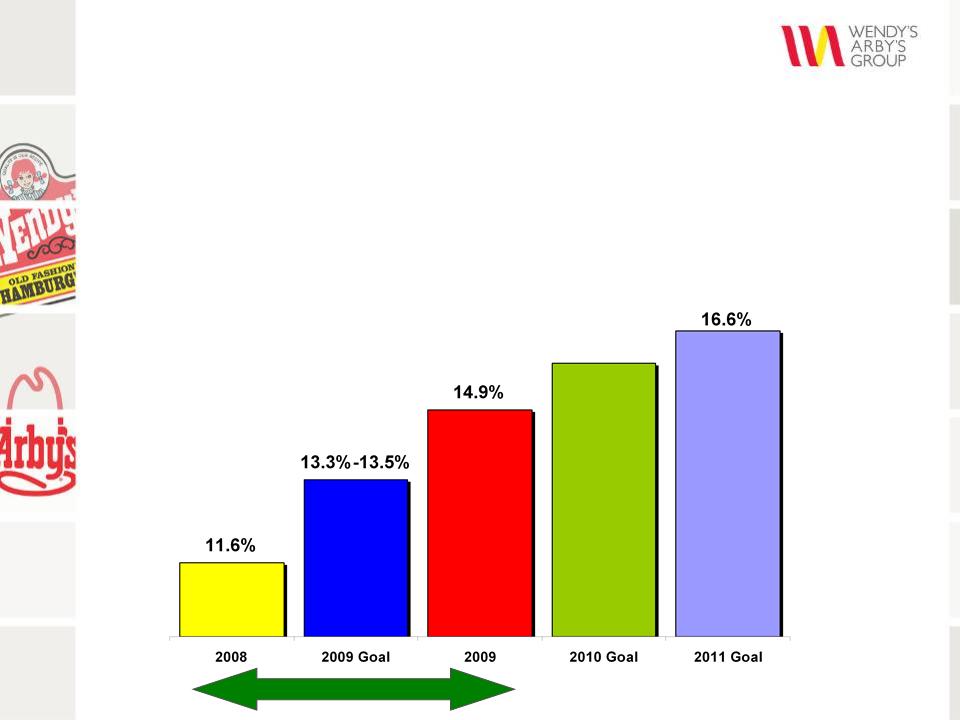

§ 2009: Goal was

160 to 180 bps Improvement

Achieved

330 bps Improvement

§ 2010: Goal is

to Continue Margin Expansion of 90 to 110 bps

(excluding incremental breakfast investment)

(excluding incremental breakfast investment)

§ 2011: Goal is

a Total Increase of 500 bps to 16.6%

330

bps 2009

15.8%-16.0%

Wendy’s

Margin Improvement

33

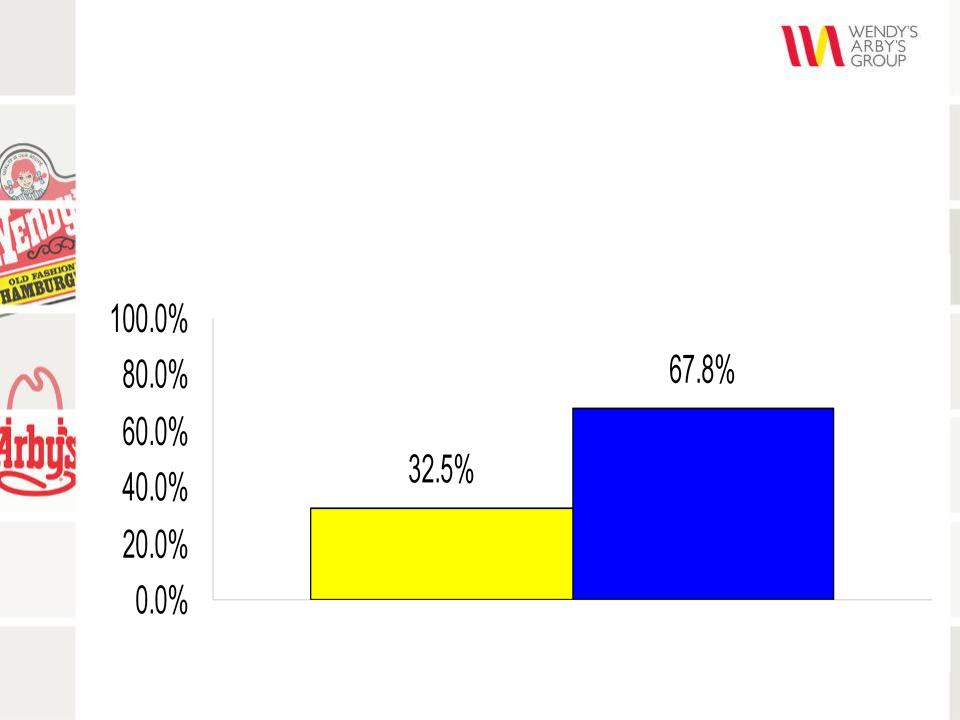

§ Steady

Improvement in Operations

– Number of “A”

and “B” stores increased by 35 points

Continue

to Improve Wendy’s

Restaurant

Operations

Q1

2008

Q4

2009

34

Optimize

Wendy’s New

Purchasing Co-op

Purchasing Co-op

§ Formed

National Supply Chain Co-op in January 2010

§ Co-op is

Managing Food and Related Product Purchases as

Well as Distribution Services

Well as Distribution Services

§ Offers Cost

Savings Opportunities While Maintaining the

Quality of the Wendy’s Brand

Quality of the Wendy’s Brand

35

§ 2010

Plan:

– Introduce new

menu and program in 3 existing markets

– Expand into

additional company and franchise markets

• $9 million

incremental investment spend

Introduce

Wendy’s New Breakfast

Program and Expand

Program and Expand

36

§ 2009: 90

Remodels Complete

§ 2010: 100

Remodels Planned

Curv

e

e

Tower

Wendy’s

Remodeling Plan

Arby’s

Brand

38

§ Recruit

Experienced Brand President

§ Execute

Turnaround Plan:

– Expand value

strategy

– Increase

media efficiency

– Validate

brand positioning

– Improve

advertising effectiveness

– Revitalize

product innovation

– Launch a

three-year remodeling program

Arby’s

2010 Initiatives

39

Arby’s

Unique Selling Proposition

§ Quality Food

Positioning

§ Unique,

Slow-Roasted and Freshly Sliced Roast Beef

Sandwiches

Sandwiches

§ A Menu that’s

an Alternative to Traditional Fast Food

Arby’s

Has One of the Highest

Check Averages in QSR

Check Averages in QSR

40

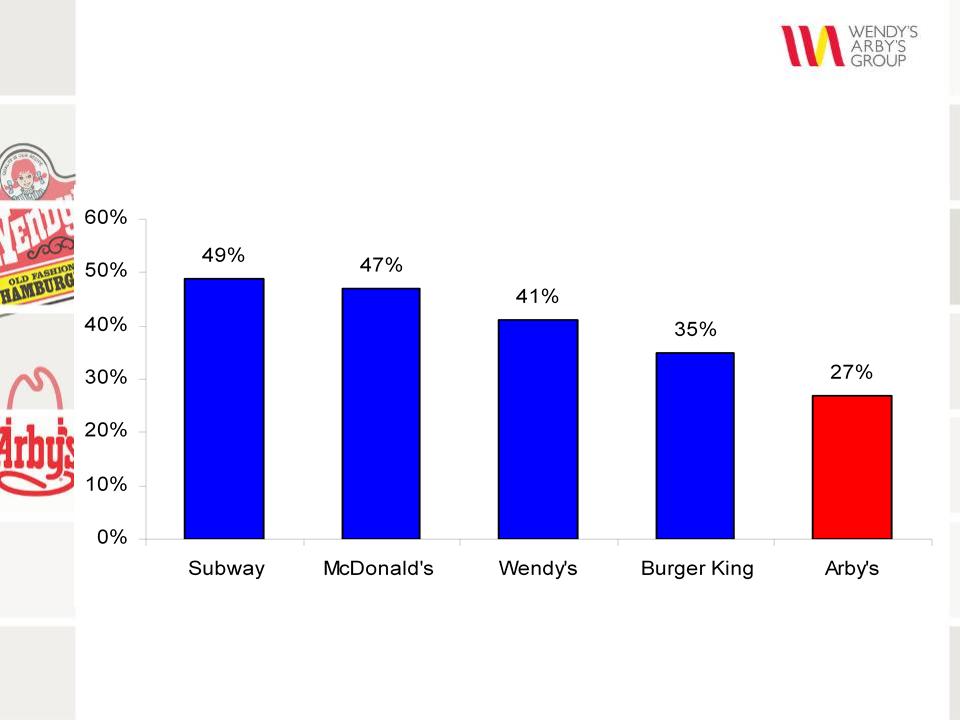

Arby’s

Rated Lowest in

“Worth

What You Pay for It”

Value

is Arby’s Biggest Issue

Source: Millward

Brown, Brand Tracking Study; represents % of consumers who agree “Worth What You

Pay for It”

41

STARTING

AT

§ National

Advertising for $1 Value begins in April

Arby’s

- Value Strategy

42

Arby’s

Media Efficiency and

Advertising Effectiveness

Advertising Effectiveness

§ Increase

National Media Weight

§ Franchisees

Approved National Media Rate Increase from

1.2% to 2.5% Effective April 1

1.2% to 2.5% Effective April 1

§ New

Advertising Campaign begins in March

§ National

Advertising on New Value Menu Starts in April

43

§ 56% of Arby’s

System is “Pinnacle”

§ Remodel

Program

– 3-Year Plan

to Invest ($75-100M)

– Goal is 75%

as Pinnacle Image

§ 100 Remodels

in 2010

Launching

Arby’s Three-Year

Remodel Program

Remodel Program

Pinnacle

Remodel

New

Pinnacle

International

45

§ 2009:

– Contractual

commitments for more than

300 new restaurants

300 new restaurants

§ 2010:

– Targeting

development agreements for

approximately 400 restaurants

approximately 400 restaurants

• Expand

existing markets

• Enter 4 new

countries

• Identify a

new partner for Japan

– New

openings

• 35-45 new

franchise units

• First

dual-branded unit opening in Dubai

in Q2

in Q2

§ Long-Term:

– Potential for

8,000 restaurants outside of

North America

North America

Singapore

1st Store Grand Opening

Artist

rendering of first dual-branded unit in the Middle East

International

Growth

46

§ Invest in

Future Growth

– Breakfast

expansion

– Remodeling

– International

§ Drive

Positive Same-Store Sales and Continue Margin

Improvement at Wendy’s

Improvement at Wendy’s

§ Turnaround

Arby’s and Improve Same-Store Sales

§ Continue to

Identify G&A Efficiencies

§ Leverage

Purchasing Power of Both Brands

§ Deliver

Low-to-Mid Single Digits Growth in 2010

Adjusted EBITDA

Adjusted EBITDA

§ Expect to

Return to Mid-Teens Adjusted EBITDA

Growth in 2011

Growth in 2011

2010

Summary

www.wendysarbys.com

Q&A

Appendix

49

50