Attached files

| file | filename |

|---|---|

| EX-10.1 - EXHIBIT 10.1 - TREX CO INC | dex101.htm |

| EX-32 - EXHIBIT 32 - TREX CO INC | dex32.htm |

| EX-23 - EXHIBIT 23 - TREX CO INC | dex23.htm |

| EX-31.1 - EXHIBIT 31.1 - TREX CO INC | dex311.htm |

| EX-31.2 - EXHIBIT 31.2 - TREX CO INC | dex312.htm |

| EX-21 - EXHIBIT 21 - TREX CO INC | dex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-14649

Trex Company, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 54-1910453 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 160 Exeter Drive, Winchester, Virginia | 22603-8605 | |

| (Address of principal executive offices) | (Zip Code) | |

(540) 542-6300

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Name of each exchange on which registered: | |

| Common Stock, par value $0.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posed pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes ¨ No þ

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting Company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting Company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer þ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting Company) | Smaller reporting Company ¨ |

Indicate by check mark whether the registrant is a shell Company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the registrant’s common equity held by non-affiliates of the registrant at June 30, 2009, which was the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $191.0 million based on the closing price of the common stock as reported on the New York Stock Exchange on such date and assuming, for purposes of this computation only, that the registrant’s directors, executive officers and beneficial owners of 10% or more of the registrant’s common stock are affiliates.

The number of shares of the registrant’s common stock outstanding on March 9, 2010 was 15,452,256.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated by reference in this Form 10-K as indicated herein:

| Document |

Part of 10-K into which incorporated | |

| Proxy Statement relating to Registrant’s 2010 Annual Meeting of Stockholders |

Part III |

TABLE OF CONTENTS

| Page | ||||

| PART I | ||||

| Item 1. |

1 | |||

| Item 1A. |

10 | |||

| Item 1B. |

13 | |||

| Item 2. |

13 | |||

| Item 3. |

13 | |||

| PART II | ||||

| Item 5. |

15 | |||

| Item 6. |

17 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

19 | ||

| Item 7A. |

28 | |||

| Item 8. |

28 | |||

| Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

28 | ||

| Item 9A. |

28 | |||

| Item 9B. |

31 | |||

| PART III | ||||

| Item 10. |

32 | |||

| Item 11. |

32 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

32 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

32 | ||

| Item 14. |

32 | |||

| PART IV | ||||

| Item 15. |

33 | |||

| F-1 | ||||

i

NOTE ON FORWARD-LOOKING STATEMENTS

This report, including the information it incorporates by reference, contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. We intend our forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in these sections. All statements regarding our expected financial position and operating results, our business strategy, our financing plans, forecasted demographic and economic trends relating to our industry and similar matters are forward-looking statements. These statements can sometimes be identified by our use of forward-looking words such as “believe,” “may,” “will,” “anticipate,” “estimate,” “expect” or “intend.” We cannot promise you that our expectations in such forward-looking statements will turn out to be correct. Our actual results could be materially different from our expectations because of various factors, including the factors discussed under “Risk Factors” in this report.

ii

Some of the information contained in this report concerning the markets and industry in which we operate is derived from publicly available information and from industry sources. Although we believe that this publicly available information and the information provided by these industry sources are reliable, we have not independently verified the accuracy of any of this information.

| Item 1. | Business |

General

Trex Company, Inc., (the “Company”), founded as a Delaware corporation in 1999, is the largest U.S. manufacturer of wood-alternative decking, railing, fencing and trim products, which are marketed under the brand name Trex®. Our principal executive offices are located at 160 Exeter Drive, Winchester, Virginia 22603, and our telephone number at that address is (540) 542-6300.

Products

We offer a comprehensive set of aesthetically durable, low maintenance product offerings in the decking, railing, fencing and trim categories. We believe that the range and variety of our product offerings allow consumers to design much of their outdoor living space using Trex brand products.

The majority of our products are made in a proprietary process that combines waste wood fibers and reclaimed polyethylene. Our decking, railing, fencing and trim products are provided in a wide selection of popular sizes and lengths and are available with several finishes and/or numerous colors.

We market our decking products under seven brand names:

| • | Trex Accents®, which offers a smooth surface on one side and subtle wood grain on the other; |

| • | Trex Accents Fire Defense®, which is a deck board that meets stringent new fire resistant requirements for certain areas of the Western United States; |

| • | Trex Brasilia®, which replicates the look of tropical hardwoods with a smooth surface and subtle, random color variations; |

| • | Trex Contours®, which has a deep, wood grain surface; |

| • | Trex Escapes®, which is an ultra-low maintenance cellular PVC deck board; |

| • | Trex Origins®, which features a smooth surface; and |

| • | Trex TranscendTM , which features a protective shell for enhanced protection against fading, staining and scratching. |

We also have Trex Hideaway®, which is a hidden fastening system for specially grooved boards.

Our two railing products are Trex Designer Series Railing® and Trex TranscendTM Railing. Our Designer Series Railing system consists of a decorative top and bottom rail, refined balusters, our Trex RailPost™, and post caps and skirts. In addition to its styling benefits for consumers, this railing is fast and easy to construct for contractors that use our TrexExpress™ assembly tool and system. The Designer railing is available in our smooth Trex Origins finish and color palette, as well as in the Trex Brasilia finish and colors. Trex Transcend Railing is available in a white finish that makes it appropriate for use with Trex decking products as well as other decking materials, which we believe will enhance the sales prospects of our railing business, and in the colors of Trex Transcend decking. This railing product is manufactured with Fibrex® material, which is a patented technology that we license from Andersen Corporation.

1

We offer two fencing products. Each product consists of structural posts, bottom rail, pickets, top rail and decorative post caps. The Trex Seclusions® fencing product uses interlocking pickets for privacy, and the Trex Surroundings® fencing uses traditional pickets. These systems have been well received by fencing installers and provide the homeowner a superior combination of low maintenance, durability and premium aesthetics which are designed to complement the outdoor living experience provided by Trex decking and railing products.

Our TrexTrim™ product is a low maintenance cellular PVC residential exterior trim product that offers exceptional workability, durability, visual appeal and a low level of required maintenance.

Trex products offer a number of significant aesthetic advantages over wood while eliminating many of wood’s major functional disadvantages, which include warping, splitting and other damage from moisture. Our products require no staining, are resistant to moisture damage, provide a splinter-free surface and need no chemical treatment against rot or insect infestation. These features eliminate most of the on-going maintenance requirements for a wood deck and make Trex products less costly than wood over the life of the deck. Like wood, Trex products are slip-resistant (even when wet), can be painted or stained and are less vulnerable to damage from ultraviolet rays. Special characteristics (including resistance to splitting, the ability to bend, and ease and consistency of machining and finishing) facilitate deck, railing, fencing and trim installation, reduce contractor call-backs and afford customers a wide range of design options. Trex products do not have the tensile strength of wood and, as a result, are not used as primary structural members in posts, beams or columns used in a deck’s substructure.

We have received product building code listings from the major U.S. and Canadian building code listing agencies for both our decking and railing systems. Our listings facilitate the acquisition of building permits by deck builders and promote consumer and industry acceptance of our products as an alternative to wood in decking. In addition, Trex Seclusions privacy fencing has passed the Miami/Dade County wind load testing, a widely regarded standard for assessing a fencing product’s performance under extreme environmental conditions.

Growth Strategies

Our long-term goal is to perpetuate our position as the leading producer of branded superior wood-alternative outdoor living products by increasing our market share and expanding into new product categories and geographic markets. To attain this goal, we intend to employ the following long-term strategies:

| • | Innovation: Bring to the market new products that address unmet consumer and trade professional needs. Provide a compelling value proposition through ease of installation, low maintenance, long-term durability and superior aesthetics. |

| • | Brand: Continue to build preference and commitment for the Trex brand with both the consumer and trade professional. Deliver on the brand’s promise of superior quality, functionality, aesthetics and overall performance in the outdoor living space. |

| • | Channels: Achieve comprehensive market segment and geographic coverage for Trex products by increasing the number of stocking dealers and retailers, thereby making our products available wherever our customers choose to purchase their decking, railing, and fencing and trim products. |

| • | Quality: Continuously advance the quality of all operational and business processes, with the goal of achieving superior product quality and service levels, thereby giving our Company a sustainable competitive advantage. |

| • | Cost: Through capital investments and process engineering, continuously seek to lower the cost to manufacture Trex products. Investments in plastic recycling capabilities will allow us to expand our ability to use a wider breadth of waste streams and, as a result, lower our raw material costs. We plan to concentrate on improving the productivity of our production process, from raw materials preparation through extrusion into finishing and packaging. |

2

Customers and Distribution

We distribute and/or sell our products through wholesale distribution and sell our products primarily to retail lumber dealers, retail building material specialty builders, Home Depot and Lowe’s.

Wholesale Distributors. In 2009, we generated the majority of our net sales through our wholesale distribution network by selling Trex products to wholesale companies. Our distributors, in turn, marketed our products to retail lumber outlets across North America. Although our dealers sell to both homeowners and contractors, they primarily direct their sales at professional contractors, remodelers and homebuilders.

We believe that attracting wholesale distributors, who are committed to our products and marketing approach and can effectively sell higher value products to contractor-oriented lumber yards and other retail outlets, is important to our future growth. Our distributors are able to provide value-added service in marketing our products because they sell premium wood decking products and other innovative building materials that typically require product training and personal selling efforts.

We typically appoint a distributor on a non-exclusive basis to distribute Trex products within a specified area. The distributor generally purchases our products at prices in effect at the time we ship the product to the distributor.

Based on our 2009 gross sales, sales to two of our distributors, Boise Cascade Corporation and Capital Lumber, exceeded 10% of our gross sales.

Retail Lumber Dealers. Our products are sold in independent lumber yards that emphasize sales to contractors. Although there is demand for our products from both the “do-it-yourself” homeowner and contractor, our sales efforts historically have emphasized the contractor-installed market. Contractor-installed decks generally are larger installations with professional craftsmanship. Our retail dealers generally provide sales personnel trained in Trex products, contractor training, inventory commitment and point-of-sale display support.

Retail Building Material Specialty Dealers. Composite decking is increasingly being sold through dealers that specialize in specific product lines instead of general lumber sales. These dealers include roofing and siding supply companies. We are focusing more attention on these distribution channels as we seek to make our products available at any retail location where contractor, builder or homeowner customers choose to purchase their decking.

Home Depot and Lowe’s. We sell our products through Home Depot and Lowe’s stores. Although Home Depot and Lowe’s serve the contractor market, the largest part of their sales are to “do-it-yourself” homeowner customers that shop for their materials at Home Depot and Lowe’s stores rather than at retail lumber dealers. We believe that brand exposure through Home Depot and Lowe’s distribution promotes consumer acceptance and generates sales to contractors that purchase from independent dealers.

Manufacturing Process

We have manufacturing facilities in Winchester, Virginia and Fernley, Nevada, which had floor space of approximately 265,000 square feet and 250,000 square feet, respectively, at December 31, 2009. In September 2007, we suspended operations at our Olive Branch facility and consolidated all of our manufacturing operations into our Winchester and Fernley sites. Our manufacturing capacity utilization rate was 32%, excluding the Olive Branch facility, during the year ended December 31, 2009.

Trex products are primarily manufactured from waste wood fiber and reclaimed polyethylene, which we sometimes refer to as “PE material” in this report. Our primary manufacturing process involves mixing wood particles with plastic, heating and finally extruding, or forcing, the highly viscous and abrasive material through a profile die. We have many proprietary and skill-based advantages in this process.

3

Production of a non-wood decking alternative such as ours requires significant capital investment, special process expertise and time to develop. We have continuously invested the capital necessary to expand our manufacturing capacity and improve our manufacturing processes. We have obtained, and continue to seek, patents with respect to our manufacturing process. We have also broadened the range of raw materials that we can use to produce a consistent and high-quality finished product. We maintain research and development operations in the Trex Technical Center adjacent to our Winchester, Virginia manufacturing facilities. In connection with our building code listings, we maintain a quality control testing program that is monitored by an independent inspection agency.

In 2005, we initiated Company-wide training and implementation of Six Sigma practices and in 2006 began implementation of Standard Lean Manufacturing methodology within our plant operations. These initiatives were significantly reenergized and expanded in 2008 and 2009. We are incorporating the use of these tools throughout our Company in the planning and execution of those projects that are the most important to our success.

Suppliers

The production of most of our products requires the supply of waste wood fiber and PE material.

The Company fulfills requirements for raw materials under both purchase orders and supply contracts. In the year ended December 31, 2009, the Company purchased substantially all of its waste wood fiber requirements under purchase orders, which do not involve long-term supply commitments. Substantially all of the Company’s PE material purchases are under short-term supply contracts that average two years, for which pricing is negotiated as needed. The PE material supply contracts have not had a material adverse effect on the Company’s business.

Waste Wood Fiber. Woodworking plants or mills are our preferred suppliers of waste wood fiber because the waste wood fiber produced by these operations contains little contamination and is low in moisture. These facilities generate waste wood fiber as a byproduct of their manufacturing operations.

If the waste wood fiber meets our specifications, our waste wood fiber supply contracts generally require us to purchase at least a specified minimum and at most a specified maximum amount of waste wood fiber each year. Depending on our needs, the amount of waste wood fiber that we actually purchase within the specified range under any supply contract may vary significantly from year to year.

PE Material. The PE material we consumed in 2009 was primarily composed of recovered plastic bags and plastic film. Approximately two billion pounds of polyethylene resin are used in the manufacture of plastic bags and stretch film in the United States each year. We will continue to seek to meet our future needs for plastic from the expansion of our existing supply sources and the development of new sources, including post-industrial waste and plastic coatings. We believe our use of multiple sources provides us with a cost advantage and facilitates an environmentally responsible approach to our procurement of PE material.

Our ability to source and use a wide variety of PE material is important to our cost strategy. We maintain this ability through the continued expansion of our plastic reprocessing operations in combination with the advancement of our proprietary material preparation and extrusion processes.

We own a 35% equity interest in a joint venture, called Denplax S.A., which operates a plant in El Ejido, Spain. Our joint venture partners are a local Spanish Company responsible for public environmental programs in southern Spain and an Italian equipment manufacturer. The plant is designed to recycle waste polyethylene generated primarily from agricultural and post-consumer sources. The plant delivered approximately 12% of the total PE material we purchased during 2009.

4

Third-Party Manufacturing. The Company outsources the production of certain products to third-party manufacturers under supply contracts that commit the Company to purchase minimum levels for each year extending through 2011. The Company is subject to monetary penalties if it fails to purchase a minimum volume as specified in the contracts.

Competition

In decking, we compete with wood and other manufacturers of wood alternative decking products. Many of the conventional lumber suppliers with which we compete have established ties to the building and construction industry and have well-accepted products. In railing, we compete with wood and other manufacturers of composite, non-wood and plastic products, as well as with railings using metal, glass, vinyl and other materials. In privacy fencing, we compete with wood, vinyl and other manufacturers of composites. In trim, we compete against wood, engineered wood, fiber cement, and other manufacturers of cellular PVC and similar plastic products.

Our primary competition consists of wood products, which constituted a substantial majority of 2009 decking and railing sales, as measured by linear feet of lumber. A majority of the lumber used in wooden decks is pressure-treated lumber. Southern yellow pine and fir have a porosity that readily allows the chemicals used in the pressure treating process to be absorbed. The same porosity makes southern yellow pine susceptible to taking on moisture, which causes the lumber to warp, crack, splinter and expel fasteners. In addition to pine and fir, other segments of wood material for decking include redwood, cedar and tropical hardwoods, such as ipe, teak and mahogany. These products are often significantly more expensive than pressure-treated lumber, but do not eliminate many of the disadvantages of other wood products.

Industry studies indicate that we have the leading market share of the wood/plastic composite segment of the decking and railing market. Our principal competitors in the wood/plastic composite decking and railing market include Advanced Environmental Recycling Technologies, Inc., Fiber Composites, LLC, Tamko Building Products, Inc., Timbertech Limited, and Universal Forest Products, Inc.

We also compete with decking products made from 100% plastic lumber that utilizes polyethylene, fiberglass and PVC as raw materials. Although there are several companies in the United States that manufacture 100% plastic lumber, this segment accounted for only a very small percentage of 2009 decking sales. We believe a number of factors have limited the success of 100% plastic lumber manufacturers, including poor product aesthetics and physical properties not considered suitable for decking, such as higher thermal expansion and contraction and poor slip resistance. We believe that Trex Escapes, an ultra-low maintenance cellular PVC deck board, is superior, both in terms of product aesthetics and physical properties, to 100% plastic lumber products available in the market.

Our ability to compete depends, in part, on a number of factors outside our control, including the ability of our competitors to develop new non-wood decking and railing alternatives that are competitive with our products. We believe that the principal competitive factors in the decking and railing market include product quality, price, aesthetics, maintenance cost, distribution and brand strength. We believe we compete favorably with respect to these factors. We believe that our products offer aesthetic and cost advantages over the life of a deck when compared to other types of decking and railing materials. Although a contractor-installed deck built with Trex products in 2009 using a pressure-treated wood substructure generally costs more than a deck made entirely from pressure-treated wood, Trex products eliminate most of the on-going maintenance required for a pressure-treated deck and are, therefore, less costly over the life of the deck. We believe that our manufacturing process and utilization of relatively low-cost raw material sources provide us with a competitive cost advantage relative to other wood/plastic composite and 100% plastic decking products. The scale of our operations also confers cost efficiencies in manufacturing, sales and marketing.

5

Government Regulation

We are subject to federal, state and local environmental regulation. The emissions of particulates and other substances from our manufacturing facilities must meet federal and state air quality standards implemented through air permits issued to us by the Department of Environmental Quality of the Commonwealth of Virginia, the Division of Environmental Protection of Nevada’s Department of Conservation and Natural Resources and the Mississippi Department of Environmental Quality. Our facilities are regulated by federal and state laws governing the disposal of solid waste and by state and local permits and requirements with respect to wastewater and storm water discharge. Compliance with environmental laws and regulations has not had a material adverse effect on our business, operating results or financial condition.

Our operations also are subject to work place safety regulation by the U.S. Occupational Safety and Health Administration, the Commonwealth of Virginia, the State of Nevada and the State of Mississippi. Our compliance efforts include safety awareness and training programs for our production and maintenance employees.

Intellectual Property

Our success depends, in part, upon our intellectual property rights relating to our products, production processes and other operations. We rely upon a combination of trade secret, nondisclosure and other contractual arrangements, and patent, copyright and trademark laws, to protect our proprietary rights. We have made substantial investments in manufacturing process improvements that have enabled us to increase manufacturing line production rates, facilitated our development of new products, and produced improvements in our existing products’ dimensional consistency, surface texture and color uniformity.

Intellectual property rights may be challenged by third parties and may not exclude competitors from using the same or similar technologies, brands or works. We seek to secure effective rights for our intellectual property, but cannot provide assurance that third parties will not successfully challenge, or avoid infringing, our intellectual property rights.

We have obtained two patents for complementary methods of preparing the raw materials for the manufacturing phase of production, one patent on an apparatus for implementing one of the methods, and one patent on a tool for use with the installation of the decking board. We intend to maintain our existing patents in effect until they expire, beginning in 2015, as well as to seek additional patents as we consider appropriate.

We consider our trademarks to be of material importance to our business plans. The U.S. Patent and Trademark Office has granted us federal registrations for many of our trademarks. Federal registration of trademarks is effective for as long as we continue to use the trademarks and renew their registrations. We do not generally register any of our copyrights with the U.S. Copyright Office, but rely on the protection afforded to such copyrights by the U.S. Copyright Act. This law provides protection to authors of original works, whether published or unpublished, and whether registered or unregistered. We enter into confidentiality agreements with our employees and limit access to and distribution of our proprietary information. If it is necessary to disclose proprietary information to third parties for business reasons, we require that such third parties sign a confidentiality agreement prior to any disclosure.

See “Legal Proceedings” in Item 3 of this report for information about a lawsuit involving intellectual property to which we were a party.

Employees

At December 31, 2009, we had approximately 520 full-time employees, approximately 375 of whom were employed in our manufacturing operations. Our employees are not covered by collective bargaining agreements. We believe that our relationships with our employees are good.

6

Web Sites and Additional Information

The SEC maintains an Internet web site at www.sec.gov that contains reports, proxy statements, and other information regarding our Company. In addition, we maintain an Internet corporate web site at www.trex.com. We make available through our web site our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after we electronically file or furnish such material with or to the SEC. We do not charge any fees to view, print or access these reports on our web site. The contents of our web site are not a part of this report.

Executive Officers and Directors

The table below sets forth information concerning our executive officers and directors as of February 15, 2010.

| Name |

Age | Positions with Company | ||

| Ronald W. Kaplan |

58 | President and Chief Executive Officer; Director | ||

| James E. Cline |

58 | Vice President and Chief Financial Officer | ||

| J.Mitchell Cox |

51 | Vice President, Sales | ||

| William R. Gupp |

50 | Chief Administrative Officer, General Counsel and Secretary | ||

| F. Timothy Reese |

57 | Vice President, Operations | ||

| Andrew U. Ferrari |

63 | Chairman | ||

| William F. Andrews |

78 | Director | ||

| Paul A. Brunner |

74 | Director | ||

| Jay M. Gratz |

57 | Director | ||

| Frank H. Merlotti, Jr. |

59 | Director | ||

| Richard E. Posey |

63 | Director | ||

| Patricia B. Robinson |

57 | Director |

Ronald W. Kaplan has served as a director and President and Chief Executive Officer of the Company since January 2008. From February 2006 through December 2007, Mr. Kaplan served as Chief Executive Officer of Continental Global Group, Inc., a manufacturer of bulk material handling systems. From July 2005 to February 2006, Mr. Kaplan was an independent consultant. From 1979 to July 2005, Mr. Kaplan was employed by Harsco Corporation, an international industrial services and products company, at which he served in a number of capacities, including as Senior Vice President-Operations, and, from 1994 through June 2005, as President of Harsco’s Gas Technologies Group, which manufactures containment and control equipment for the global gas industry. Mr. Kaplan received a B.A. degree in economics from Alfred University and an M.B.A. degree from the Wharton School of Business, University of Pennsylvania.

James E. Cline has served as Vice President and Chief Financial Officer of the Company since March 2008. Mr. Cline served from July 2005 through December 2007 as the President of Harsco GasServ, a subsidiary of Harsco Corporation and a manufacturer of containment and control equipment for the global gas industry. From January 2008 through February 2008, in connection with the purchase of Harsco GasServ by Taylor-Wharton International LLC, which is owned by Windpoint Partners Company, Mr. Cline served as a consultant to the buyers by providing transition management and financial services. From April 1994 through June 2005, Mr. Cline served as the Vice President and Controller of Harsco GasServ. Mr. Cline served in various capacities with Huffy Corporation from June 1976 to February 1994, including as the Director of Finance of its True Temper Hardware subsidiary, a manufacturer of lawn care and construction products with nine manufacturing locations in the United States, Canada and Ireland. Mr. Cline received a B.S.B.A. degree in accounting from Bowling Green State University.

J. Mitchell Cox has served as Vice President, Sales of the Company since September 2005. From 1981 to August 2005, Mr. Cox was employed by Kraft Foods Inc., an international manufacturer of packaged food and

7

beverage products, at which he served in a number of capacities, including Region Vice President from 1996 to August 2005; Director of Category Management from 1994 to 1996; and Division Sales Manager Metro New York/New Jersey from 1992 to 1994. Mr. Cox received a B.A. degree in English from the University of North Carolina at Chapel Hill.

William R. Gupp has served as Chief Administrative Officer, General Counsel and Secretary of the Company since October 2009. From May 2001 to October 2009, Mr. Gupp served as Vice President and General Counsel of the Company. From March 1993 to May 2001, Mr. Gupp was employed by Harsco Corporation, an international industrial services and products Company, most recently as Senior Counsel and Director-Corporate Development. From August 1985 to March 1993, Mr. Gupp was employed by the law firm of Harter, Secrest & Emery. Mr. Gupp received a B.S. degree in accounting from Syracuse University and a J.D. from the University of Pennsylvania Law School.

F. Timothy Reese has served as Vice President, Operations of the Company since February 2008. From March 2007 through January 2008, Mr. Reese served as Operations Director for the Americas Region of DuPont Teijin Films, a DuPont Teijin Films U.S. Limited Partnership and producer of polyester films. From 1979 to March 2007, Mr. Reese served in various positions with DuPont, including Global Director, Business and Integrated Operations, DuPont High Performance Films, from November 1995 through November 1998; Director/Plant Manager, Global Operations, Cyrel® Packaging Graphics Products, from December 1998 through May 2000; Director, Global Operations and Six Sigma Champion, Cyrel® Packaging Graphics Products, from June 2000 through February 2001; and Director/Plant Manager in multiple assignments from March 2001 through February 2007, including in Corporate Operations, Human Resources and DuPont Chemical Solutions Enterprise. Mr. Reese served in the U.S. Navy and received a B.S. in ocean engineering with an emphasis on mechanical engineering from the U.S. Naval Academy.

Andrew U. Ferrari has served as a director of the Company since September 1998 and as Chairman since January 2008. Mr. Ferrari served as Chief Executive Officer of the Company from August 2007 through December 2007, and as President and Chief Operating Officer of the Company from August 2005 through July 2007. From March 2003 through August 2005, Mr. Ferrari was a marketing and business development consultant. Mr. Ferrari served as Executive Vice President of Marketing and Business Development of the Company from October 2001 through March 2003, and of TREX Company, LLC, which was the Company’s wholly-owned subsidiary until December 31, 2002, from October 2001 through December 2002. He served as Executive Vice President of Sales and Marketing of the Company from September 1998 to October 2001 and of TREX Company, LLC from August 1996 to October 2001. From 1989 to 1996, Mr. Ferrari held various positions with Mobil Chemical, including Director of Sales and Marketing of the Composite Products Division, New Business Manager, and Marketing Director of the Consumer Products Division. Mr. Ferrari received a B.A. degree in economics from Whitman College and an M.B.A. degree from Columbia University.

William F. Andrews has served as a director of the Company since April 1999. Mr. Andrews has served as Chairman of Katy Industries, Inc., a manufacturer of maintenance and electrical products, since October 2001, and as Chairman of the Singer Sewing Company, a manufacturer of sewing machines, since 2004. Mr. Andrews served as Chairman of Corrections Corporation of America from 2000 to 2008 and is now the Chairman of the Executive Committee of the Board. Mr. Andrews has been a Principal of Kohlberg & Company, a venture capital firm, since 1994, and served as Chairman of Allied Aerospace Company from 2000 to 2006. Prior to 2002, he served in various positions, including Chairman of Scovill Fasteners Inc.; Chairman of Northwestern Steel and Wire Company; Chairman of Schrader-Bridgeport International, Inc.; Chairman, President and Chief Executive Officer of Scovill Manufacturing Co., where he worked for over 28 years; Chairman and Chief Executive Officer of Amdura Corporation; Chairman of Utica Corporation; and Chairman, President and Chief Executive Officer of Singer Sewing Company. Mr. Andrews also serves as a director of Black Box Corporation and O’Charley’s Restaurants. Mr. Andrews received a B.S. degree in business administration from the University of Maryland and an M.B.A degree in marketing from Seton Hall University.

8

Paul A. Brunner has served as a director of the Company since February 2003. Mr. Brunner is President and Chief Executive Officer of Spring Capital Inc., a merchant bank, which he founded in 1985. From 1982 to 1985, Mr. Brunner served as President and Chief Executive Officer of U.S. Operations of Asea-Brown Boveri, a multi-national Swiss manufacturer of high technology products. In 1967, he joined Crouse Hinds Company, a manufacturer of electronics and electronic equipment, and through 1982 held various positions with that company, including President and Chief Operating Officer, Executive Vice President of Operations, Vice President of Finance and Treasurer, and Director of Mergers and Acquisitions. Mr. Brunner served as a director of Johnson Controls, Inc. from 1983 through 2007, and as Chairman of its Audit Committee from 1989 to 2005. From 1959 to 1967, he worked for Coopers & Lybrand, an international accounting firm, as an audit supervisor. Mr. Brunner is a Certified Public Accountant. He received a B.S. degree in accounting from the University of Buenos Aires and an M.B.A. degree in management from Syracuse University.

Jay M. Gratz has served as a director of the Company since February 2007. Mr. Gratz has been a partner in Tatum LLC, a national executive services and consulting firm that focuses on the needs of the Office of the CFO since February 2010. From October 2007 through February 2010, Mr. Gratz was an independent consultant. From 1999 through October 2007, Mr. Gratz served as Executive Vice President and Chief Financial Officer of Ryerson Inc., a metals processor and distributor, and as President of Ryerson Coil Processing Division from November 2001 through October 2007. Mr. Gratz served as Vice President and Chief Financial Officer of Inland Steel Industries from 1994 through 1998 and served in various other positions, including Vice President of Finance, at that company since 1975. Mr. Gratz is a Certified Public Accountant. He received a B.A. degree in economics from the State University of New York in Buffalo and an M.B.A. degree from Northwestern University Kellogg Graduate School of Management.

Frank H. Merlotti, Jr. has served as a director of the Company since February 2006. Since October 2006, Mr. Merlotti has served as President of Steelcase Design Group, the North American business unit of Steelcase, Inc., a manufacturer of office furniture and furniture systems, and served as President of Steelcase North America from September 2002 through September 2006. Mr. Merlotti served as President and Chief Executive Officer of G&T Industries, a manufacturer and distributor of fabricated foam and soft-surface materials for the marine, office furniture and commercial building industries, from August 1999 to September 2002. From 1991 through 1999, Mr. Merlotti served as President and Chief Executive Officer of Metropolitan Furniture Company, a Steelcase Design Partnership Company. From 1985 through 1999, Mr. Merlotti served as General Manager of the Business Furniture Division of G&T Industries.

Richard E. Posey has served as a director of the company since May 2009. He served as President and Chief Executive Officer of Moen Incorporated, a leading manufacturer in the global faucet market, for six years before retiring in 2007. Prior to joining Moen, Mr. Posey was President and Chief Executive Officer of Hamilton Beach / Proctor Silex, Inc. for five years. Mr. Posey began his career at S.C. Johnson & Son, where for 22 years he served in a series of increasingly responsible management positions, both overseas and in the U.S., culminating with Executive Vice President, Consumer Products, North America. Mr. Posey currently serves on the Board of Directors of The Colman Group, a supply equipment company, is a member of the Visiting Committee, The Ross School of Business, The University of Michigan, and is a Founding Trustee, Virginia Commonwealth University School of Engineering Foundation. He received a B.A. degree in English from The University of Southern California and an M.B.A. degree from The University of Michigan.

Patricia B. Robinson has served as a director of the Company since November 2000. Ms. Robinson has been an independent consultant since 1999. From 1977 to 1998, Ms. Robinson served in a variety of positions with Mead Corporation, a forest products company, including President of Mead School and Office Products, Vice President of Corporate Strategy and Planning, President of Gilbert Paper, Plant Manager of a specialty machinery facility and Product Manager for new packaging product introductions. Ms. Robinson received a B.A. degree in economics from Duke University and an M.B.A. degree from the Darden School at the University of Virginia.

9

| Item 1A. | Risk Factors |

Our business is subject to a number of risks, including the following:

We may not be able to grow unless we increase market acceptance of our products and develop new products and applications.

Our primary competition consists of wood products, which constitute a substantial majority of decking and railing sales. Our ability to grow will depend largely on our success in converting the current demand for wood in decking, railing, fencing, and trim applications into a demand for Trex products. To increase our market share, we must overcome:

| • | the consumer lack of awareness of the value of non-wood decking, railing, fencing and trim alternatives in general and Trex brand products in particular; |

| • | the resistance of many consumers and contractors to change from well-established wood products; |

| • | the greater initial expense of Trex decking, railing, fencing and trim compared to wood; |

| • | the established relationships existing between suppliers of wood decking, railing, fencing and trim products and contractors and homebuilders; and |

| • | the competition from other wood alternative manufacturers. |

In addition to the above, substantially all of our revenues are derived from sales of our proprietary wood/plastic composite material. Although we have developed, and continue to develop, new products made from other materials, if we should experience significant problems, real or perceived, with product quality or acceptance of the Trex wood/polyethylene composite material, our lack of product diversification could have a significant adverse impact on our net sales levels.

Our prospects for sales growth and profitability may be adversely affected if we fail to maintain product quality and product performance at an acceptable cost.

We will be able to expand our net sales and to sustain and enhance profitable operations only if we succeed in maintaining the quality and performance of our products. If we should not be able to produce high-quality products at standard manufacturing rates and yields, unit costs may be higher. A lack of product performance would negatively affect our profitability by impeding acceptance of our products in the marketplace and by leading to higher product replacement and consumer relations expenses. In recent periods, we have experienced significant increases in product replacement and consumer relations expenses related to a small portion of our production at our Fernley, Nevada manufacturing facility and have increased our warranty reserve accordingly. Because the establishment of reserves is an inherently uncertain process involving estimates of the number of future claims and the cost to settle claims, our ultimate losses may exceed our warranty reserve. Future increases to the warranty reserve would have an adverse effect on our profitability in the periods in which we make such increases. Increases we made to the warranty reserve in 2007 had a material adverse effect on 2007 profitability and payments for related claims had a material adverse effect on our cash flow in 2007, 2008 and 2009.

Our sales and reputation may be affected by product liability claims or litigation in relation to our products.

Our products are used outdoors and are sometimes subject to heavy use and harsh exposure to the environment. Although our Limited Warranty excludes any conditions attributable to “any act of God (such as flooding, hurricane, earthquake, lighting, etc., ), environmental condition (such as air pollution, mold, mildew, etc.), staining from foreign substances (such as dirt, grease, oil, etc.), or normal weathering (defined as exposure to sunlight, weather and atmosphere which will cause any colored surface to gradually fade, chalk, or accumulate dirt or stains”), to the extent that our products are affected in any way, this may lead to an increased risk of product liability claims or litigation. Such claims could cause adverse publicity which in turn could result in a

10

loss of consumer confidence in our products and also reduce our sales. Product liability claims could increase our expenses and have a material adverse effect on demand for our products and, consequently, reduce our sales, net income and liquidity.

Our business is subject to risks in obtaining the raw materials we use at acceptable prices.

The production of our product requires substantial amounts of wood fiber and PE material. Our business strategy is to create a substantial cost advantage over our competitors by using recycled plastic and reclaimed wood. Our business could suffer from the termination of significant sources of raw materials, the payment of higher prices for raw materials or the failure to obtain sufficient additional raw materials to meet planned increases in production. Our ability to obtain adequate supplies of PE material depends on our success in developing new sources that meet our quality requirements, entering into long-term arrangements with suppliers and managing the collection of supplies from geographically dispersed distribution centers and off-shore sources.

The demand for our products is influenced by general economic conditions and could be adversely affected by economic downturns.

The demand for our products is correlated to changes in the health of the economy in general, and the level of activity in home improvements and, to a much lesser extent, new home construction. These activity levels, in turn, are affected by such factors as home equity values, consumer spending habits, employment, interest rates and inflation. Market conditions in the housing industry have slowed significantly in recent periods, particularly in new home construction. Home equity values in many markets have decreased significantly, adversely affecting the availability of home equity withdrawals, which have resulted in decreased home improvement spending. In 2008, the U.S. economy entered into a recession. We cannot predict how long the recession will last and whether the downward trend in home remodeling and new home construction will continue or worsen. Any continued economic downturn could reduce consumer income or equity capital available for spending on discretionary items such as decking, railing, fencing or trim, which could adversely affect the demand for our products.

Our performance may suffer if we do not compete effectively in the highly competitive decking, railing, fencing and trim markets.

We must compete with an increasing number of companies in the wood/plastic composites segment of the decking, railing, fencing and trim markets and with wood producers that currently have more production capacity than is required to meet the demand for such products. Our failure to compete successfully in such markets could have a material adverse effect on our ability to replace wood or increase the market share of wood/plastic composites compared to wood. Many of the conventional lumber suppliers with which we compete have established ties to the building and construction industry and have well-accepted products. Many of our competitors in the decking, railing, fencing and trim markets that sell wood products have significantly greater financial, technical and marketing resources than we do. Our ability to compete depends, in part, upon a number of factors outside our control, including the ability of competitors to develop new non-wood alternatives that are more competitive with Trex products.

We have significant capital invested in property, plant and equipment that may become obsolete or impaired and result in a charge to our earnings.

At December 31, 2009, we had $137.0 million of net property, plant and equipment. The improvement we seek to make to our manufacturing processes sometimes involves the implementation of new technology and replacement of equipment at our manufacturing facilities, which may result in charges to our earnings if the existing equipment is not fully depreciated. Of our net property, plant and equipment at December 31, 2009, approximately $14.2 million is located at our Olive Branch, Mississippi manufacturing facility. In September 2007, we suspended operations at our Olive Branch facility and consolidated all of our manufacturing operations into our Winchester and Fernley sites. In September 2009, we recorded a pre-tax impairment charge

11

of $23.3 million related to the long-lived assets held at the facility. Changes in the expected cash flows related to our facilities in the future may result in additional impairment charges and reduced earnings.

Our level of indebtedness could adversely affect our financial health and ability to compete.

As of December 31, 2009, we had $101.0 million of total indebtedness. Our level of indebtedness could have important consequences. For example, it may:

| • | increase our vulnerability to general adverse economic and industry conditions, including interest rate fluctuations; |

| • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

| • | limit our ability to borrow additional funds to alleviate liquidity constraints, as a result of financial and other restrictive covenants in our indebtedness; |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| • | place us at a competitive disadvantage relative to companies that have less indebtedness; and |

| • | limit our ability to refinance our principal secured indebtedness. |

In addition, our senior secured credit facility imposes operating and financial restrictions that may limit our discretion on some business matters, which could make it more difficult for us to expand, finance our operations and engage in other business activities that may be in our interest. These restrictions may limit our ability to:

| • | incur additional indebtedness and additional liens on our assets; |

| • | engage in mergers or acquisitions or dispose of assets; |

| • | enter into sale-leaseback transactions; |

| • | pay dividends or make other distributions; |

| • | voluntarily prepay other indebtedness; |

| • | enter into transactions with affiliated persons; |

| • | make investments; and |

| • | change the nature of our business. |

We may incur indebtedness in addition to our current indebtedness. Any additional indebtedness we may incur in the future could subject us to similar or even more restrictive conditions.

Our ability to refinance our indebtedness will depend on our ability in the future to generate cash flows from operations and to raise additional funds, including through the offering of equity or debt securities. We may not be able to generate sufficient cash flows from operations or to raise additional funds in amounts necessary for us to repay our indebtedness when such indebtedness becomes due and to meet our other cash needs.

Our ability to make scheduled principal and interest payments on our real estate loans, convertible notes, borrow and repay amounts under our revolving credit facility and continue to comply with our loan covenants will depend primarily on our ability to generate sufficient cash flow from operations. Our failure to comply with our loan covenants might cause our lenders to accelerate our repayment obligations under our credit facility, which may be declared payable immediately based on a default and which could result in a cross-default under our $97.5 million principal amount of outstanding convertible notes. Our ability to borrow under our revolving

12

credit facility is tied to a borrowing base that consists of specified receivables and inventory. To remain in compliance with our credit facility, and real estate loans, we must maintain specified financial ratios based on our levels of debt, capital, net worth, fixed charges, and earnings (excluding extraordinary gains and extraordinary non-cash losses) before interest, taxes, depreciation and amortization, all of which are subject to the risks of our business.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

We lease our corporate headquarters in Winchester, Virginia, which consists of 32,517 square feet of office space, under a lease that expires in March 2020. In anticipation of relocating our corporate headquarters to Dulles, Virginia, we entered into a lease agreement in 2005, which expires in 2019. The Dulles lease agreement provides for our initial occupancy of 55,047 square feet of office space, which will increase during the lease term to 80,071 square feet in mid-2012. We reconsidered our decision to relocate our corporate headquarters in 2005 and decided not to move. As of January 10, 2008, we had executed subleases for the entire space we currently lease. The terms of the existing subleases extend through years 2012 to 2015. For a description of our financial reporting in connection with the Dulles lease agreement, see Note 14 to our consolidated financial statements appearing elsewhere in this report.

We own approximately 74 contiguous acres of land in Winchester, Virginia and the buildings on this land. The site includes our original manufacturing facility, which contains approximately 115,000 square feet of space, our research and development technical facility, which contains approximately 30,000 square feet of space, a mixed-use building, which contains approximately 173,000 square feet of space, and an additional manufacturing facility, which contains approximately 150,000 square feet of space. We own the land and the manufacturing facility on the Fernley, Nevada site, which contains approximately 250,000 square feet of manufacturing space. Our Fernley site is located on approximately 37 acres, which includes outside open storage. We own approximately 102 acres of land in Olive Branch, Mississippi and the buildings on this land. The site contains four buildings with approximately 200,000 square feet for manufacturing and raw material handling operations. In September 2007, we suspended operations at our Olive Branch facility and consolidated all of our manufacturing operations into our Winchester and Fernley sites.

We lease a total of approximately 1.1 million square feet of storage warehouse space under leases with expiration dates ranging from 2010 to 2015. For information about these leases, see Note 11 to our consolidated financial statements appearing elsewhere in this report.

The equipment and machinery we use in our operations consist principally of plastic and wood conveying and processing equipment. We own all of our manufacturing equipment. We lease substantially all of our forklift equipment at our facilities under operating leases.

We regularly evaluate our various facilities and equipment and make capital investments where necessary. In 2009, we spent a total of $6.9 million on capital expenditures, primarily to make process and productivity improvements. We estimate that our capital expenditures in 2010 will be approximately $10 million. We expect to use these expenditures principally to make process and productivity improvements and upgrade systems.

| Item 3. | Legal Proceedings |

On October 16, 2006, Ron Nystrom commenced a lawsuit against the Company in the United States District Court for the Eastern District of Virginia, Norfolk Division, which also named Home Depot, Inc. and Snavely Forest Products, Inc. as defendants. Mr. Nystrom alleged that the Company’s Accents® product and other new

13

products introduced after the commencement of a prior patent infringement action infringed his patent. Mr. Nystrom also alleged that the Company’s Contours® product infringed a second patent owned by him and that the Company was engaged in contributory infringement by recommending third party hidden fastening systems that infringe such patent. In January 2008, Mr. Nystrom added an additional allegation that the Company’s Trex HideawayTM hidden fastening system also infringed such patent. On May 16, 2008, the District Court granted summary judgment to the Company with respect to Mr. Nystrom’s claims on the first patent. On April 29, 2008, the District Court issued an order severing all claims associated with the second patent and consolidating them into a separate case.

On September 25, 2008, the Company commenced a lawsuit against Mr. Nystrom in Virginia Circuit Court for various causes of action, including defamation. On September 26, 2008, Mr. Nystrom filed a Notice of Appeal to the United States Court of Appeals for the Federal Circuit appealing the District Court’s grant of summary judgment to the Company with respect to Mr. Nystrom’s claims on the first patent. On October 16, 2008, the Company and Mr. Nystrom signed a Dismissal and Tolling Agreement which provided that the Federal District Court action relating to the second patent and the Company’s action in Virginia Circuit Court would both be dismissed without prejudice pending the decision of the Federal Court of Appeals on the District Court’s decision relating to the first patent. On September 8, 2009, the Federal Court of Appeals affirmed the District Court’s grant of summary judgment, in favor of the Company. Pursuant to the Dismissal and Tolling Agreement, this ended all pending litigation between the parties.

On January 19, 2009, a purported class action case was commenced against the Company in the Superior Court of California, Santa Cruz County, by Eric Ross and Bradley S. Hureth generally alleging certain product defects in the Company’s products, and that the Company has failed to provide adequate remedies for defective products. On February 13, 2009, the Company removed this case to the United States District Court, Northern District of California. On January 21, 2009, a purported class action case was commenced against the Company in the United States District Court, Western District of Washington by Mark Okano making similar allegations. The Okano case was subsequently transferred by the Washington Court to the California Court as a related case to the Ross/Hureth case. On July 30, 2009, the U.S. District Court for the Northern District of California preliminary approved a settlement of the claims of the Ross/Hureth lawsuit involving surface flaking of the Company’s product. A hearing for final approval of the settlement occurred on October 30, 2009. As of the date of this report, the District Court has not issued its final ruling. The Company believes that both lawsuits are without merit.

14

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market for Common Stock

Our common stock has been listed on the New York Stock Exchange, or NYSE since April 8, 1999. Between April 8, 1999 and November 22, 2009, it was listed under the symbol “TWP”. Effective November 23, 2009, the symbol changed to “TREX”. The table below shows the reported high and low sale prices of our common stock for each quarter during 2008 and 2009 as reported by the New York Stock Exchange:

| 2009 |

High | Low | ||||

| First Quarter |

$ | 19.50 | $ | 5.11 | ||

| Second Quarter |

14.85 | 7.24 | ||||

| Third Quarter |

21.22 | 11.51 | ||||

| Fourth Quarter |

20.98 | 15.46 | ||||

| 2008 |

High | Low | ||||

| First Quarter |

$ | 9.00 | $ | 6.42 | ||

| Second Quarter |

14.17 | 7.76 | ||||

| Third Quarter |

21.73 | 8.83 | ||||

| Fourth Quarter |

18.46 | 9.54 | ||||

Dividend Policy

We have never paid cash dividends on our common stock. We intend to retain future earnings, if any, to finance the development and expansion of our business and, therefore, do not anticipate paying any cash dividends on the common stock in the foreseeable future. Under the terms of our credit agreement there are restrictions on our ability to pay dividends.

15

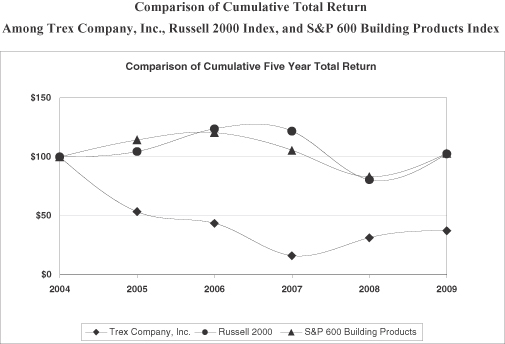

Stockholder Return Performance Graph

The following graph and table show the cumulative total stockholder return on Trex Company’s common stock for the last five fiscal years compared to the Russell 2000 Index and the Standard and Poor’s 600 Building Products Index. The graph assumes $100 was invested on December 31, 2004 in (1) Trex Company common stock, (2) the Russell 2000 Index and (3) the S&P 600 Building Products Index, and assumes reinvestment of dividends and market capitalization weighting as of December 31, 2005, 2006, 2007, 2008 and 2009.

| December 31, 2004 |

December 31, 2005 |

December 31, 2006 |

December 31, 2007 |

December 31, 2008 |

December 31, 2009 | |||||||||||||

| Trex Company |

$ | 100.00 | $ | 53.49 | $ | 43.65 | $ | 16.23 | $ | 31.39 | $ | 37.38 | ||||||

| Russell 2000 |

$ | 100.00 | $ | 104.55 | $ | 123.76 | $ | 121.82 | $ | 80.66 | $ | 102.58 | ||||||

| S&P 600 BPI |

$ | 100.00 | $ | 114.40 | $ | 120.59 | $ | 105.62 | $ | 83.15 | $ | 102.99 | ||||||

Other Stockholder Matters

As of March 5, 2010, there were approximately 241 holders of record of our common stock.

In 2009, we submitted to the NYSE in a timely manner the annual certification that our Chief Executive Officer was not aware of any violation by us of the NYSE corporate governance listing standards.

16

| Item 6. | Selected Financial Data |

The following table presents selected financial data as of December 31, 2005, 2006, 2007, 2008 and 2009 and for each of the years in the five-year period ended December 31, 2009.

The selected financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto appearing elsewhere in this report.

| Year Ended December 31, | ||||||||||||||||||||

| 2005 | 2006 | 2007 (1) | 2008 | 2009 (2) | ||||||||||||||||

| (In thousands, except share and per share data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Net sales |

$ | 294,133 | $ | 336,956 | $ | 328,952 | $ | 329,194 | $ | 272,286 | ||||||||||

| Cost of sales |

213,897 | 257,671 | 289,529 | 240,170 | 191,339 | |||||||||||||||

| Gross profit |

80,236 | 79,285 | 39,423 | 89,024 | 80,947 | |||||||||||||||

| Selling, general and administrative expenses |

77,378 | 73,223 | 119,439 | 66,958 | 65,257 | |||||||||||||||

| Impairment of long-lived assets |

— | — | — | — | 23,251 | |||||||||||||||

| Income (loss) from operations |

2,858 | 6,062 | (80,016 | ) | 22,066 | (7,561 | ) | |||||||||||||

| Interest expense, net |

2,626 | 3,011 | 11,503 | 15,282 | 14,699 | |||||||||||||||

| Income (loss) before income taxes |

232 | 3,051 | (91,519 | ) | 6,784 | (22,260 | ) | |||||||||||||

| Provision (benefit) for income taxes |

(2,019 | ) | 708 | (26,105 | ) | (750 | ) | (5,811 | ) | |||||||||||

| Net income (loss) |

$ | 2,251 | $ | 2,343 | $ | (65,414 | ) | $ | 7,534 | $ | (16,449 | ) | ||||||||

| Basic earnings (loss) per share |

$ | 0.15 | $ | 0.16 | $ | (4.39 | ) | $ | 0.50 | $ | (1.09 | ) | ||||||||

| Basic weighted average shares outstanding |

14,769,799 | 14,829,832 | 14,884,174 | 14,956,927 | 15,061,603 | |||||||||||||||

| Diluted earnings (loss) per share |

$ | 0.15 | $ | 0.16 | $ | (4.39 | ) | $ | 0.50 | $ | (1.09 | ) | ||||||||

| Diluted weighted average shares outstanding |

14,879,661 | 14,892,966 | 14,884,174 | 15,113,083 | 15,061,603 | |||||||||||||||

| Cash Flow Data: |

||||||||||||||||||||

| Cash provided by (used in) operating activities |

$ | 11,234 | $ | (4,038 | ) | $ | (1,163 | ) | $ | 33,042 | $ | 35,063 | ||||||||

| Cash used in investing activities |

(29,374 | ) | (27,743 | ) | (24,035 | ) | (8,594 | ) | (6,638 | ) | ||||||||||

| Cash provided by (used in) financing activities |

(4,432 | ) | 31,058 | 24,592 | (1,325 | ) | (32,100 | ) | ||||||||||||

| Other Data (unaudited): |

||||||||||||||||||||

| EBITDA (3) |

$ | 18,997 | $ | 26,324 | $ | (57,525 | ) | $ | 46,942 | $ | 38,592 | |||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents and restricted cash |

$ | 1,395 | $ | 672 | $ | 66 | $ | 23,189 | $ | 19,514 | ||||||||||

| Working capital |

40,061 | 29,559 | 48,385 | 65,085 | 60,645 | |||||||||||||||

| Total assets |

285,714 | 352,317 | 320,529 | 307,084 | 256,459 | |||||||||||||||

| Total debt (including derivatives) |

73,606 | 104,637 | 98,002 | 103,563 | 77,571 | |||||||||||||||

| Total stockholder’s equity |

$ | 164,708 | $ | 169,415 | $ | 128,385 | $ | 137,828 | $ | 125,579 | ||||||||||

| (1) | Year ended December 31, 2007 materially affected by increases to the warranty reserve, product returns and tax valuation allowance as disclosed in the Company’s previous filings. |

17

| (2) | Year ended December 31, 2009 materially affected by impairment of long-lived assets at the idle Olive Branch facility. |

| (3) | EBITDA represents net income before interest, income taxes, depreciation and amortization. EBITDA is not a measurement of financial performance under accounting principles generally accepted in the United States, or GAAP. The Company has included data with respect to EBITDA because management evaluates and projects the performance of the Company’s business using several measures, including EBITDA. Management considers EBITDA to be an important supplemental indicator of the Company’s operating performance, particularly as compared to the operating performance of the Company’s competitors, because this measure eliminates many differences among companies in capitalization and tax structures, capital investment cycles and ages of related assets, as well as some recurring non-cash and non-operating charges to net income or loss. For these reasons, management believes that EBITDA provides important supplemental information to investors regarding the operating performance of the Company and facilitates comparisons by investors between the operating performance of the Company and the operating performance of its competitors. Management believes that consideration of EBITDA should be supplemental, because EBITDA has limitations as an analytical financial measure. These limitations include the following: |

| • | EBITDA does not reflect the Company’s cash expenditures, or future requirements for capital expenditures, or contractual commitments; |

| • | EBITDA does not reflect the interest expense, or the cash requirements necessary to service interest or principal payments, on the Company’s indebtedness; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; |

| • | EBITDA does not reflect the effect of earnings or charges resulting from matters the Company considers not to be indicative of its ongoing operations; and |

| • | not all of the companies in the Company’s industry may calculate EBITDA in the same manner in which the Company calculates EBITDA, which limits its usefulness as a comparative measure. |

The Company compensates for these limitations by relying primarily on its GAAP results to evaluate its operating performance and by considering independently the economic effects of the foregoing items that are not reflected in EBITDA. As a result of these limitations, EBITDA should not be considered as an alternative to net income (loss), as calculated in accordance with GAAP, as a measure of operating performance, nor should it be considered as an alternative to cash flows as a measure of liquidity. The following table sets forth, for the years indicated, a reconciliation of EBITDA to net income (loss):

| Year Ended December 31, | |||||||||||||||||||

| 2005 | 2006 | 2007 | 2008 | 2009 | |||||||||||||||

| (In thousands) | |||||||||||||||||||

| Net income (loss) |

$ | 2,251 | $ | 2,343 | $ | (65,414 | ) | $ | 7,534 | $ | (16,449 | ) | |||||||

| Plus interest expense, net |

2,626 | 3,011 | 11,503 | 15,282 | 14,699 | ||||||||||||||

| Plus income tax provision (benefit) |

(2,019 | ) | 708 | (26,105 | ) | (750 | ) | (5,811 | ) | ||||||||||

| Plus depreciation and amortization |

16,139 | 20,262 | 22,491 | 24,876 | 22,902 | ||||||||||||||

| Plus impairment of long-lived assets |

— | — | — | — | 23,251 | ||||||||||||||

| EBITDA |

$ | 18,997 | $ | 26,324 | $ | (57,525 | ) | $ | 46,942 | $ | 38,592 | ||||||||

18

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This management’s discussion and analysis contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements regarding our expected financial position and operating results, our business strategy, our financing plans, forecasted demographic and economic trends relating to our industry and similar matters are forward-looking statements. These statements can sometimes be identified by our use of forward-looking words such as “may,” “will,” “anticipate,” “estimate,” “expect,” “intend” or similar expressions. We cannot promise you that our expectations in such forward-looking statements will turn out to be correct. Our actual results could be materially different from our expectations because of various factors, including the factors discussed under “Item 1A. Risk Factors.” These statements are also subject to risks and uncertainties that could cause the Company’s actual operating results to differ materially. Such risks and uncertainties include the extent of market acceptance of the Company’s products; the sensitivity of the Company’s business to general economic conditions; the Company’s ability to obtain raw materials at acceptable prices; the Company’s ability to maintain product quality and product performance at an acceptable cost; the level of expenses associated with product replacement and consumer relations expenses related to product quality; and the highly competitive markets in which the Company operates.

Overview

General. Trex Company, Inc., (the “Company”), is the largest U.S. manufacturer of wood-alternative decking, railing, fencing and trim products, which are marketed under the brand name Trex®. We offer a comprehensive set of aesthetically durable, low maintenance product offerings and believe that the range and variety of our product offerings allow consumers to design personal outdoor living space using Trex brand products.

We have seven decking products: Trex Contours®, Trex Origins®, Trex Accents®, Trex Accents Fire Defense®, Trex Brasilia® , Trex Escapes® and Trex TranscendTM;; two railing products: Trex Designer Series Railing® and Trex TranscendTM Railing two fencing products, Trex Seclusions® and Trex Surroundings® and a cellular PVC outdoor trim product, TrexTrim™. In addition, we offer Trex Hideaway®, which is a hidden fastening system for specially grooved boards.

Highlights related to the full year 2009 include:

| • | In 2009, we experienced decreased sales volume primarily as a result of the poor U.S. macroeconomic conditions. Customers and dealers continued to reduce their inventory levels and conserve working capital. |

| • | We continued our progress on process and productivity improvements. Those improvements and the effect of our 2009 price increase more than offset the impact of operating at significantly lower capacity utilization and the effect of the startup of the new Transcend production lines. |

| • | During the year, we continued to significantly reduce inventory. Since December of 2007 we have reduced inventory by 51% or $47 million, of which $24 million was in 2009. This reduction resulted in a favorable LIFO adjustment approximately equal to the benefit realized in 2008. In the third quarter of 2009, we also recorded a $7.2 million write-down to certain inventory manufactured prior to 2008. This write-down was entirely offset by a corresponding favorable LIFO adjustment. |

| • | We generated positive operating cash flow, despite reduced earnings. At the end of 2009 our cash balance was $20 million and we had no outstanding balance on our revolving lines of credit. In addition, we refinanced our outstanding debt and reduced the total amount of our outstanding debt. During the year we utilized cash on hand to pay in full $25 million Mississippi Business Finance Corporation Bonds and $5 million in term debt related to our Winchester Properties. |

| • | 2009 cash flows were negatively impacted by claims payments of $10.6 million from the warranty reserve for material previously produced at the Nevada facility that exhibited surface defects. |

19

Net Sales. Net sales consist of sales and freight, net of returns and discounts. The level of net sales is principally affected by sales volume and the prices paid for Trex products. Our branding and product differentiation strategy enables us to command premium prices over wood and to maintain price stability for Trex. To ensure adequate availability of product to meet anticipated seasonal consumer demand, we have historically provided our distributors and dealers incentives to build inventory levels before the start of the prime deck-building season. These incentives include prompt payment discounts or extended payment terms. In addition, from time to time we may offer price discounts on specified products and other incentives based on increases in distributor purchases as part of specific promotional programs. There are no product return rights granted to our distributors except those granted pursuant to the warranty provisions of our agreements with distributors.

Gross Profit. Gross profit represents the difference between net sales and cost of sales. Cost of sales consists of raw materials costs, direct labor costs, manufacturing costs and freight. Raw materials costs generally include the costs to purchase and transport waste wood fiber, reclaimed polyethylene, or “PE material,” and pigmentation for coloring Trex products. Direct labor costs include wages and benefits of personnel engaged in the manufacturing process. Manufacturing costs consist of costs of depreciation, utilities, maintenance supplies and repairs, indirect labor, including wages and benefits, and warehouse and equipment rental activities.