Attached files

| file | filename |

|---|---|

| 8-K - 8-K_03-03-2010 INVESTOR UPDATE - NORTHWESTERN CORP | ek_030310.htm |

Investor

Update

San

Francisco, CA

March

3 - 4, 2010

2

forward-looking

statement…

During

the course of this presentation, there will be forward-looking

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

statements within the meaning of the “safe harbor” provisions of the

Private Securities Litigation Reform Act of 1995. Forward-looking

statements often address our expected future business and financial

performance, and often contain words such as “expects,” “anticipates,”

“intends,” “plans,” “believes,” “seeks,” or “will.”

The

information in this presentation is based upon our current

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason. Although

our expectations and beliefs are based on reasonable assumptions, actual

results may differ materially. The factors that may affect our results are

listed in certain of our press releases and disclosed in the Company’s

public filings with the SEC.

expectations as of the date hereof unless otherwise noted. Our actual

future business and financial performance may differ materially and

adversely from our expectations expressed in any forward-looking

statements. We undertake no obligation to revise or publicly update our

forward-looking statements or this presentation for any reason. Although

our expectations and beliefs are based on reasonable assumptions, actual

results may differ materially. The factors that may affect our results are

listed in certain of our press releases and disclosed in the Company’s

public filings with the SEC.

3

who we

are…

Above

data as of 12/31/09

(1) Book

capitalization calculated as total debt, excluding capital leases, plus

shareholders’ equity.

¾ 661,000

customers

» 396,000

electric

» 265,000 natural

gas

¾ Approximately

123,000 square

miles of service territory in

Montana, South Dakota, and Nebraska

miles of service territory in

Montana, South Dakota, and Nebraska

» 32,000 miles of

electric T&D lines

» 8,400 miles of

natural gas T&D pipelines

» 18 Bcf natural gas

storage

¾ Total

generation (mostly

base load coal)

» MT

- 222 MW - regulated beginning 1/1/09

» SD

- 312 MW - regulated

¾ Total

Assets: $2,795 MM

¾ Total

Capitalization: $1,774 MM(1)

¾ Total

Employees: 1,354

Located

in states with relatively stable economies with potential grid

expansion in the Northwest region.

expansion in the Northwest region.

¾ Solid

operations

» Cost

competitive

» Above-average

reliability

» Award-winning

customer service

¾ Improving

credit ratings and strong balance sheet and liquidity

» Secured

and unsecured investment grade ratings

» Moody’s

has us on “positive” outlook

¾ Positive

earnings and ROE trend

» Colstrip

Unit 4 into rates effective January 1, 2009

» Delivery

services rate cases for Montana electric and natural gas

¾ Strong

cash flows

» NOLs

and repair tax deduction provide an effective tax shield until likely

2014

¾ Competitive

dividend

» Current

yield approximately 5.2%

¾ Improving

regulatory environment

¾ Realistic

growth prospects

4

NorthWestern’s

attributes…

improving credit

ratings…

5

6

strong

balance sheet and liquidity…

¾ Debt

/ Total capitalization of 55.6% (12/31/09)

¾ October

2009

» $55

million, 30 year First Mortgage Bonds issued at 5.71%

¾ June

2009

» Extended

unsecured revolver maturity to June 30, 2012

» Increased

size from $200 million to $250 million

¾ March

2009

» $250

million, 10 year First Mortgage Bonds issued at 6.34%

¾ Total

liquidity currently in the $230 million range

¾ Nearly

all long-term debt matures after 2014

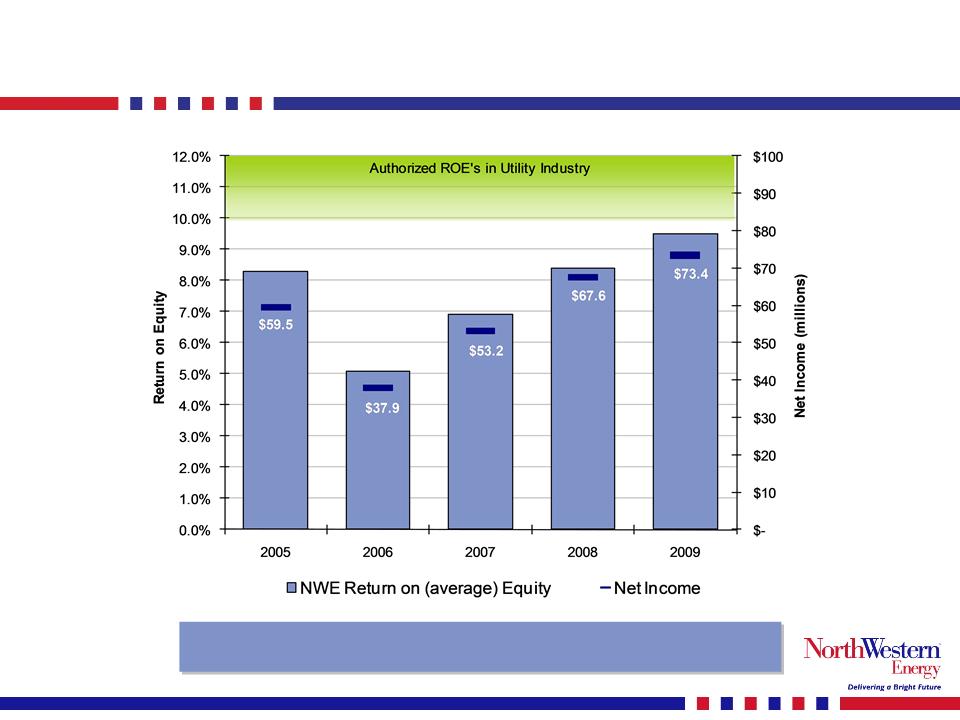

positive earnings

and ROE trend…

Recent authorized

ROE’s: Mill Creek (10.25%)

and Colstrip Unit 4 (10.00%).

and Colstrip Unit 4 (10.00%).

7

8

strong

cash flows…

Earnings growth, NOLs, and repairs tax

deduction provide strong

cash flows to fund future growth projects.

cash flows to fund future growth projects.

pension

funding and expense…

9

2009

return in excess of 20%. Moved

from 62% funded at

12/31/2008 to 94% funded at 12/31/2009.

12/31/2008 to 94% funded at 12/31/2009.

competitive

dividend…

10

Goal

for dividend payout ratio of 60% - 70%.

Current dividend yield about 5.2%.

Current dividend yield about 5.2%.

11

regulatory

update…

¾ Montana

» Rate

cases filed October 2009 requesting $17.5 million revenue increase

♦ November

2009 the MPSC determined the initial filing failed to comply with MPSC

applicable minimum filing requirements, primarily related to allocated cost of

service and rate design

applicable minimum filing requirements, primarily related to allocated cost of

service and rate design

♦ On

February 2, 2010 our supplemental filing was accepted as compliant

♦ Final

order and rate adjustment now expected by October 11, 2010

» Mill

Creek Generation Station filed with MPSC

♦ MPSC

approved in 2Q 2009

♦ Under

construction with $84.7 million capitalized CWIP as of 12/31/09

» Colstrip

Unit 4 placed into rate base starting January 2009

¾ South

Dakota / Nebraska

» Evaluate

whether to file natural gas rate cases during late 2010

¾ FERC

» Working

with FERC for MSTI rate design

♦ FERC

encouraged Company to develop MSTI on a cost of service basis

by requesting appropriate tariff waivers from existing OATT

by requesting appropriate tariff waivers from existing OATT

» FERC

approved 230kV Renewable Collector System open season

Establishing

positive regulatory regulations in all jurisdictions.

12

near-term potential

earnings drivers…

¾ 2010

» Expecting

modest growth in volumes and economic activity

♦ Due

to higher mix of residential/commercial vs. industrial customers as

compared to other utilities

compared to other utilities

● Electric:

69% Residential & Commercial, 31% Industrial

● Natural

Gas: 99% Residential & Commercial, 1% Industrial

» Montana

rate adjustment expected to take effect last quarter of 2010

¾ 2011

» In

2011 we anticipate:

♦ Full

year effect of Montana rate adjustment

♦ Potential

South Dakota and Nebraska natural gas rate adjustments

♦ Mill

Creek in rate base

● Approximately

$10 million annualized contribution to net income

Near-term

earnings drivers independent of

transmission

projects.

projects.

longer-term

potential earnings drivers…

¾ Distribution

system enhancements

» Exploring

incremental rate based investment (early

stages)

¾ Energy

supply

» Mill

Creek Generation Station

» South

Dakota peaking generation

» Natural

gas reserves (early

stages)

» Wind

projects and other renewable projects (early

stages)

» Big

Stone pollution control equipment (early

stages)

¾ Transmission

projects

» Colstrip

500 kV upgrade

» 230

kV Renewable Collector System

» Mountain

States Transmission Intertie (MSTI)

» Electric

Transmission America (ETA) (early

stages)

» Green

Power Express (ITC) (early

stages)

13

Balanced

growth opportunities across the business.

14

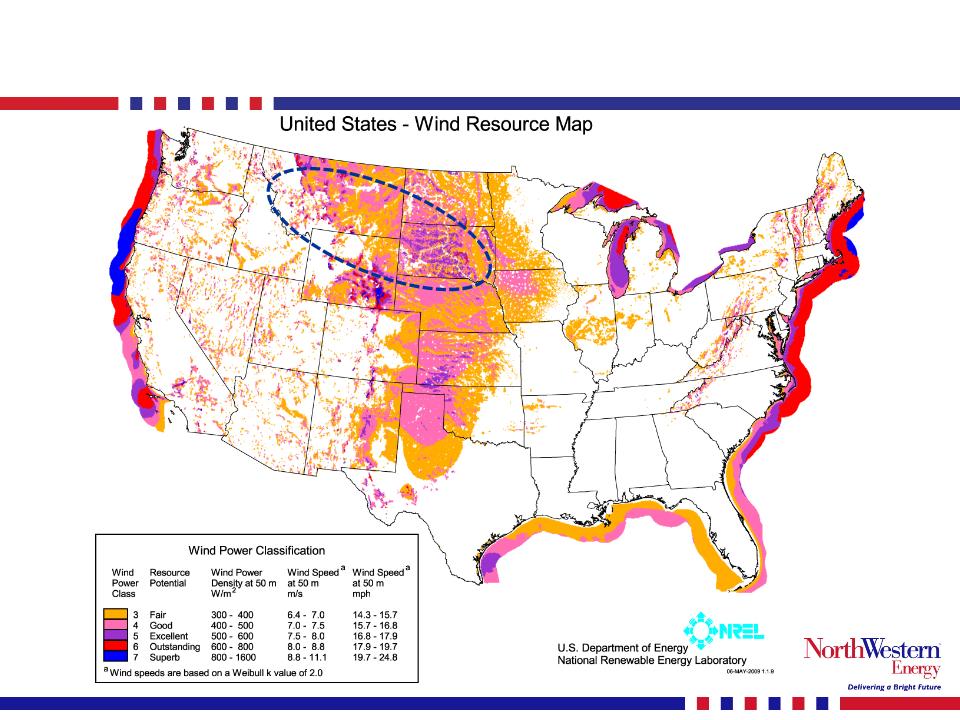

great

wind potential in our service territory…

15

service

territory is a link between supply…

16

and

demand…

17

our

proposed transmission projects…

18

capex

spending - next few years…

Additional

equity not

anticipated until we proceed

with MSTI or other major

investments not shown here.

anticipated until we proceed

with MSTI or other major

investments not shown here.

We

will move forward with

the funding of these projects

only when they make

economic sense.

the funding of these projects

only when they make

economic sense.

MSTI

project is now slated for

early 2015 and capex has

been modified accordingly.

Capital still shown at 100%

but still evaluating partners.

early 2015 and capex has

been modified accordingly.

Capital still shown at 100%

but still evaluating partners.

Utility

Maintenance

Capex is funded 100%

by free cash flow.

Capex is funded 100%

by free cash flow.

19

growth

project potential…

Opportunity

to double and diversify earnings as compared with

our existing $1.5 billion rate base.

our existing $1.5 billion rate base.

20

growth

project milestones ’10 & ’11…

2010

Mill

Creek

¾Test

“fire” the turbines

Q3

¾Periodic

filings with MPSC

Qtrly

¾Complete

Construction

Q4

¾Commercial

operation date

Q4

500

kV Upgrade

¾Finalize

commercial terms with partners

Q4

¾WECC

phase 1 planning process completed

Q4

¾Decision

point on proceeding w/construction

Q4

230

kV Collector System

¾Open

season information meeting

Q1

¾Collector open

season commences

Q2

¾LGIA

tendered to qualified participants

Q4

MSTI

¾Draft

EIS

Q1

¾Phase

1 of open season

Q2

¾Phase

2 of open season

Q3

¾EIS

Record of Decision

Q4

|

2011

|

|

|

Mill

Creek

|

|

|

¾Providing

regulating services

¾Tariffs

filed for rates

¾MPSC

prudence review filing

|

Q1

Q1

Q1

|

|

500

kV Upgrade

|

|

|

¾WECC

phase 2 rating

|

Q3

|

|

¾Construction

begins

|

Q3

|

|

230

kV Collector System

|

|

|

¾Open

season results posted

|

Q1

|

|

¾Customers

provide full credit support

|

Q1

|

|

¾FERC

approvals of OATT waivers

|

Q2

|

|

¾WECC

regional planning approval

|

Q4

|

|

MSTI

|

|

|

¾Open

season results posted

|

Q1

|

|

¾FERC

approvals of OATT waivers

|

Q1

|

|

¾Customers

provide full credit support

|

Q2

|

|

¾Begin

right of way procurement

|

Q4

|

21

in

summary…

¾ Solid

operations

¾ Improving

credit ratings and strong balance

sheet and liquidity

sheet and liquidity

¾ Positive

earnings and ROE trend

¾ Strong

cash flows

¾ Competitive

dividend

¾ Improving

regulatory environment

¾ Realistic

growth prospects

22

Appendix

23

income

statement…

Appendix

24

2008 -

2009 earnings bridge…

Prior

earnings

guidance for 2009 of

$1.75 - $1.85 was

revised upward to

$1.95 - $2.05 on

October 28, 2009 due

to repairs tax

deduction.

guidance for 2009 of

$1.75 - $1.85 was

revised upward to

$1.95 - $2.05 on

October 28, 2009 due

to repairs tax

deduction.

Appendix

2009 -

2010 earnings bridge…

25

Appendix

balance

sheet…

26

Appendix

cash

flow…

27

Appendix

28

MPSC

rate request…

¾ Requested

revenue increase of $17.5 million

» Electric

T&D = $15.5 million (6.98%)

» Natural

gas T&D = $2.0 million (1.89%)

» Expect

decision by October 11, 2010

» Interim

rates requested

» Increase

primarily due to pension and wage increases

¾ Requested

for both Electric and Natural Gas Cases

» ROE

of 10.90%

» Ratio

of 50.55% debt / 49.45% equity

» Cost

of debt of 5.76%

» Resulting

cost of capital of 8.30%

» Electric

and Natural Gas rate base of $632 million and $257 million,

respectively

Rate

request excludes Colstrip Unit 4 generation and the

under-construction Mill Creek Generation Plant.

under-construction Mill Creek Generation Plant.

Appendix

29

repairs

tax deduction impact…

As

pre-tax income increases the repairs tax deduction benefit, as a % of

the

effective tax rate, decreases.

effective tax rate, decreases.

Appendix

Sample

calculation

30

Montana

rate filing…

The

above demonstrates the impact of our repairs tax deduction on our current

rate

filing in Montana. The reduction in our income tax expense has been passed through

to customers in the form of a lower rate request while leaving NorthWestern “whole”.

filing in Montana. The reduction in our income tax expense has been passed through

to customers in the form of a lower rate request while leaving NorthWestern “whole”.

Appendix