Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0 - 10200

SEI INVESTMENTS COMPANY

(Exact name of registrant as specified in its charter)

| Pennsylvania | 23-1707341 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 1 Freedom Valley Drive, Oaks, Pennsylvania | 19456-1100 | |

| (Address of principal executive offices) | (Zip Code) |

610-676-1000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $.01 per share | The NASDAQ Stock Market LLC (The NASDAQ Global Select Market®) |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

(Cover page 1 of 2 pages)

Table of Contents

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting common stock held by non-affiliates of the registrant was approximately $2.7 billion based on the closing price of $18.04 as reported by NASDAQ on June 30, 2009 (the last business day of the registrant’s most recently completed second fiscal quarter). For purposes of making this calculation only, the registrant has defined affiliates as including all executive officers, directors and beneficial owners of more than ten percent of the common stock of the registrant.

The number of shares outstanding of the registrant’s common stock, as of the close of business on February 19, 2010:

| Common Stock, $.01 par value | 189,824,192 |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated by reference herein:

| 1. | The definitive proxy statement relating to the registrant’s 2010 Annual Meeting of Shareholders, to be filed within 120 days after the end of the fiscal year covered by this annual report, is incorporated by reference in Part III hereof. |

(Cover page 2 of 2 pages)

Table of Contents

Fiscal Year Ended December 31, 2009

TABLE OF CONTENTS

Page 1 of 97

Table of Contents

PART I

Forward Looking Statements

This Annual Report on Form 10-K contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve certain known and unknown risks, uncertainties and other factors, many of which are beyond our control, and are not limited to those discussed in Item 1A, “Risk Factors.” All statements that do not relate to historical or current facts are forward-looking statements. These statements may include words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” and other words and terms of similar meaning in connection with any discussion of future operating or financial performance. In particular, these include statements relating to present or anticipated products and markets, future revenues, capital expenditures, expansion plans, future financing and liquidity, personnel, and other statements regarding matters that are not historical facts or statements of current condition.

Any or all forward-looking statements contained within this Annual Report on Form 10-K may turn out to be wrong. They can be affected by inaccurate assumptions we might make, or by known or unknown risks and uncertainties. Many factors mentioned in the discussion below will be important in determining future results. Consequently, we cannot guarantee any forward-looking statements. Actual future results may vary materially.

We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. You are advised, however, to consult any further disclosures we make on related subjects in our filings with the U.S. Securities and Exchange Commission (SEC).

| Item 1. | Business. |

Overview

SEI (NASDAQ: SEIC) is a leading global provider of investment processing, fund processing, and investment management business outsourcing solutions that help corporations, financial institutions, financial advisors, and ultra-high-net-worth families create and manage wealth. As of December 31, 2009, through its subsidiaries and partnerships in which the company has a significant interest, SEI administers $391.7 billion in mutual fund and pooled assets, manages $158.8 billion in assets, and operates from numerous offices worldwide.

Our wealth management business solutions include:

| • | Investment processing and investment operations outsourcing solutions for banks, trust companies, independent wealth advisers, and investment managers; |

| • | Investment management programs to affluent individual investors and for institutional investors, including retirement plan sponsors, and not-for-profit organizations; and |

| • | Fund processing solutions for banks, investment management firms, and investment companies that sponsor and distribute mutual funds, hedge funds, and alternative investments. |

General Development of the Business

For over 40 years, SEI has been a leading provider of wealth management business solutions for the financial services industry.

We began doing business in 1968 by providing computer-based training simulations to instruct bank loan officers in credit lending practices.

1970s

We developed an investment accounting system for bank trust departments in 1972, and became a leading provider of investment processing outsourcing services to banks and trust institutions.

Page 2 of 97

Table of Contents

1980s

SEI became a public company in 1981. We entered the asset management business and launched a series of money market mutual funds for bank clients, and expanded our services to bank clients by offering mutual fund accounting services. We also began to provide investment operations outsourcing services.

1990s

We introduced our “Manager-of-Managers” investment process, and offered these programs to investment advisors who manage wealth for their high-net-worth clients. We entered the institutional investor market and began offering asset management programs to retirement plan sponsors and institutional investors in selected global markets, including the United States, Canada, the United Kingdom, continental Europe, South Africa and East Asia.

2000s

We delivered broader, more strategic solutions for clients and markets, including a complete life and wealth platform for operating an investment advisory business, a total operational outsourcing solution for investment managers, a fully-integrated pension management system for retirement plan sponsors, and a complete life and wealth solution for ultra-high-net-worth families. We introduced Global Wealth Services, a next generation business solution integrating investment processing technology, operating processes, and investment management programs.

Strategy

We seek to achieve growth in earnings and shareholder value by strengthening our position as a provider of global wealth management solutions. To achieve this objective, we have implemented these strategies:

Create broader solutions for wealth service firms. Banks, investment managers and financial advisors seek to enter new markets, expand their service offerings, provide a differentiated experience to their clients, improve efficiencies, reduce risks, and better manage their businesses. We have developed and continue to develop next generation business solutions integrating technology, operating processes, and financial products designed to help these institutions better serve their clients and provide opportunities to improve their business success.

Help institutional investors manage retirement plans and operating capital. Retirement plan sponsors, not-for-profit organizations, and other institutional investors strive to meet their financial objectives while reducing business risk. We deliver customized investment management solutions that enable investors to make better decisions about their investments and to manage their assets more effectively.

Help affluent individual investors manage their life and wealth goals. These investors demand a holistic wealth management experience that focuses on their life goals and provides them with an integrated array of financial services that includes substantially more than traditional wealth management offerings. We help these investors identify their goals and offer comprehensive life and wealth advisory services including life planning, investments, and other financial services.

Expand into global markets. Global markets are large and present significant opportunities for growth. We are evolving U.S. business models for the global wealth management marketplace, focusing on the needs of institutional investors, private banks, investment advisors, and affluent individual investors.

Fundamental Principles

We are guided by these fundamental principles in managing the business and adopting these growth strategies:

| • | Achieve organic growth in revenue and earnings. We seek to grow the business by providing additional services to clients, adding new clients, introducing new products, and adapting products for new markets. |

| • | Forge long-term client relationships. We strive to achieve high levels of customer satisfaction and to forge close and long lasting client relationships. We believe these relationships enable us to market additional services, and acquire knowledge and insights that fuel the product development process. |

| • | Invest in product development. We continually enhance products and services to keep pace with industry developments, regulatory requirements, and the emerging needs of markets and clients. We believe ongoing investments in research and development give us a competitive advantage in our markets. |

| • | Maintain financial strength. We adopt business models that generate recurring revenues and positive cash flows. Predictable cash flows serve as a source of funds for continuing operations, investments in new products, common stock repurchases, and dividend payments. |

Page 3 of 97

Table of Contents

| • | Leverage investments across the business. We create scalable, enterprise-wide solutions designed to serve the needs of multiple markets, potentially offering operating efficiencies that can benefit corporate profitability. |

| • | Create value for shareholders. The objective of achieving long-term sustainable growth in revenues and earnings strongly influences the management of the business. This philosophy guides corporate management practices, strategic planning activities, and employee compensation practices. |

Products and Services

Investment Processing

Investment processing solutions consist of application and business process outsourcing services, and transaction-based services. We deliver these solutions to banks, trust institutions, independent wealth advisers located in the United Kingdom, and financial advisors in Canada that provide wealth management services to their private and institutional clients. We also deliver these solutions, combined with our investment management programs, to investment advisors that provide wealth management services to their advisory clients.

Investment processing solutions include TRUST 3000®, a comprehensive trust accounting and investment system that provides securities processing and investment accounting for all types of domestic and global securities, and support for multiple account types, including personal trust, corporate trust, institutional trust, and non-trust investment accounts.

In 2007, we introduced Global Wealth Services to the U.K. market. Global Wealth Services is a next-generation business solution that integrates investment processing technology, operating processes, and investment management programs. This solution provides the strategic infrastructure to help banks and other wealth management organizations grow and keep pace with a rapidly changing wealth management industry.

An integral component of the Global Wealth Services solution is the Global Wealth Platform, an investment accounting and securities processing system with capabilities that include global securities processing, trade-date and multi-currency accounting and reporting. The Global Wealth Platform offers enhanced client experience capabilities and improved operating efficiencies, and enables us to enter new markets in the United Kingdom, continental Europe and the United States. The platform is designed around the client and portfolio management processes. This enables banks to institutionalize their client processes around an investor’s investment objectives, facilitating a transition to model-based portfolio management, providing an improved client experience, while minimizing the expense and risk associated with investment operations.

Revenues from investment processing services are earned as monthly fees from contracted services including software licenses, information processing, and investment operations. These revenues are recognized in Information processing and software servicing fees on the accompanying Consolidated Statements of Operations, and are primarily earned based upon the type and number of investor accounts serviced. Investment processing revenues may also be earned as a percentage of assets under management and administration. Professional services revenues are earned from contracted, project-oriented services related to client implementations, and are recognized in Information processing and software servicing fees on the accompanying Consolidated Statements of Operations. Transaction-based revenues are earned from securities valuation and trade execution services, and are recognized as Transaction-based and trade execution fees on the accompanying Consolidated Statements of Operations.

Investment Management Programs

Investment management programs consist of money market, fixed-income and equity mutual funds and other collective investment products, alternative investment portfolios, and separately managed accounts. We serve as the administrator and investment advisor for many of these products. We distribute these programs primarily through investment advisory firms, including investment advisors and banks, and directly to institutional or individual investors.

We have expanded these investment management programs to include other consultative, operational, and technology components, and have created comprehensive solutions tailored to the needs of a specific market. These components may include investment strategies, consulting services, administrative and processing services, and technology tools.

Investors in our investment programs typically follow a customized investment strategy, and invest in a globally diversified portfolio that consists of multiple classes and investment styles, constructed according to our disciplined investment process. Our investment process is based on five principles: asset allocation and appropriate diversification, both of which are important to investment performance; portfolio construction that consists of multiple managers with complementary approaches to achieve diversification of risk and returns; manager selection, where

Page 4 of 97

Table of Contents

SEI acts as a manager-of-managers, selecting some of the best style-specific money managers from a global network of money managers; continuous portfolio management, to ensure each manager’s investment approach remains consistent with the objectives of the portfolio; and tax management, for an emphasis on after-tax returns.

As of December 31, 2009, we managed $106.3 billion in assets including: $82.9 billion invested in fixed-income and equity funds, or through separately managed account programs; $11.8 billion invested in liquidity or money market funds; and $11.6 billion invested in collective trust fund programs. An additional $52.5 billion in assets is managed by our affiliate LSV Asset Management (LSV).

Revenues from investment management programs are primarily earned as a contractual percentage of net assets under management. These revenues are recognized in Asset management, administration and distribution fees on the accompanying Consolidated Statements of Operations.

Fund Processing

Fund processing solutions include a full range of administration and distribution support services for traditional investment products such as mutual funds, collective investment trusts, exchange-traded funds, and institutional and separate accounts. Administrative services include fund administration, portfolio and fund accounting; cash administration and treasury services; trustee and custodial services; legal, audit and tax support; and investor and distribution services. Distribution support services may include market and industry analyses to identify distribution opportunities.

We also provide comprehensive solutions to investment managers worldwide that sponsor and distribute alternative investments such as hedge funds, funds of hedge funds, and private equity funds, across both registered and partnership structures. We also offer operational outsourcing solutions for the administration and management of separately managed account programs, as well as total operational outsourcing solutions for investment management firms.

As of December 31, 2009, we administered $232.9 billion in client-sponsored assets for traditional and alternative investment products.

Revenues from fund processing are primarily earned based upon a contractual percentage of net assets under administration. These revenues are recognized in Asset management, administration and distribution fees on the accompanying Consolidated Statements of Operations.

Business Segments

Business segments are generally organized around our target markets. Financial information about each business segment is contained in Note 13 to the Consolidated Financial Statements. Our business segments are:

Private Banks – provides investment processing and investment management programs to banks and trust institutions worldwide, independent wealth advisers located in the United Kingdom, and financial advisors in Canada;

Investment Advisors – provides investment management programs to affluent investors through a network of independent registered investment advisors, financial planners, and other investment professionals in the United States;

Institutional Investors – provides investment management programs and administrative outsourcing solutions to retirement plan sponsors and not-for-profit organizations worldwide;

Investment Managers – provides investment processing, fund processing, and operational outsourcing solutions to investment managers, fund companies and banking institutions located in the United States, and to investment managers worldwide of alternative asset classes such as hedge funds, funds of hedge funds, and private equity funds across both registered and partnership structures;

Investments in New Businesses – provides investment management programs to ultra-high-net-worth families residing in the United States through the SEI Wealth Network®; and

LSV Asset Management – is a registered investment advisor that provides investment advisory services to institutions, including pension plans and investment companies.

Page 5 of 97

Table of Contents

The percentage of consolidated revenues generated by each business segment for the last three years was:

| 2009 | 2008 | 2007 | |||||||

| Private Banks |

34 | % | 33 | % | 30 | % | |||

| Investment Advisors |

16 | % | 18 | % | 19 | % | |||

| Institutional Investors |

16 | % | 16 | % | 15 | % | |||

| Investment Managers |

13 | % | 11 | % | 10 | % | |||

| Investments in New Businesses |

1 | % | 1 | % | 1 | % | |||

| LSV |

20 | % | 21 | % | 25 | % | |||

| 100 | % | 100 | % | 100 | % | ||||

Private Banks

The Private Banks segment delivers investment processing services and investment management programs to banks and trust institutions worldwide, independent wealth advisers located in the United Kingdom, and financial advisors in Canada.

Our investment processing services enable banks and trust institutions to reduce risk, improve quality, and gain operational efficiency thus enabling them to focus on growing their business and serving client needs. Investment processing solutions are delivered via two primary business models: the Global Wealth Technology Services (GWTS) model and the Global Wealth Services (GWS) model. In both models, we own, maintain and operate the software applications and information processing facilities.

Banks using our GWTS model outsource investment processing technology software and computer processing, but retain responsibility for investment operations, client administration, and investment management. Clients operate our GWTS solution remotely while fully supported by our data center using dedicated telecommunications networks. The GWTS model includes a dedicated relationship team that supports our client’s business. We assist our clients with strategically evaluating their systems and process needs as their businesses change.

The GWS model is an extension of our GWTS solution. It was designed for private banks and other trust organizations that prefer to outsource their entire investment operation. With the GWS solution, we assume the entire back-office processing function. The GWS model includes: investment processing; account access and reporting; audit, compliance and regulatory support data generation; custody and safekeeping of assets; income collections; securities settlement; and other related trust activities.

New clients undergo a business transformation process which can take a few months for smaller institutions and up to 15 months or more for larger institutions. During the transformation process, we collaborate with new clients to understand their strategic goals and objectives. During this transformation, systems, operations, and business processes are evaluated and optimized to meet client objectives. We typically earn a one-time implementation fee for these business transformation services.

Client contracts have initial terms that are generally three to seven years in length. At December 31, 2009, we had significant relationships with 127 banks and trust institutions in the United States, including trust departments of 9 of the 20 largest U.S. banks.

The Global Wealth Services solution will be further enhanced through the Global Wealth Platform. Target markets for this enhanced solution include private banks and independent wealth advisers in the United Kingdom, as well as community, regional, and national private banks in the United States. We believe the enhanced Global Wealth Services solution enabled by the new infrastructure will improve the client experience and place our clients in a superior position to serve the changing needs of their clients.

Our principal competitors in the investment processing business for this segment are: Odyssey Technologies; Fidelity National Information Services, Inc. (formerly Metavante Corporation); SunGard Data Systems Inc.; Temenos Group AG; and Pershing LLC, a subsidiary of The Bank of New York Mellon Corporation. Many large financial institutions develop, operate and maintain proprietary investment and trust accounting systems. We also consider these “in-house” solutions to be a form of competition.

Our investment management programs for banks and distribution partners are offered worldwide. At December 31, 2009, there were approximately 360 investment management clients worldwide. We also had single-product relationships with approximately 150 additional banks and trust institutions. The principal competitors for this

Page 6 of 97

Table of Contents

business are: Dimensional Fund Advisors; Federated Investors, Inc.; LPL Financial Corporation; Russell Investment Group, a subsidiary of The Northwestern Mutual Life Insurance Company; discretionary portfolio managers and various multi-manager investment programs offered by other firms. We also consider “in-house” internal asset management capabilities to be a form of competition.

Investment Advisors

The Investment Advisors segment offers wealth management solutions to registered investment advisors, many of whom are affiliated with or are registered as independent broker-dealers, financial planners, and life insurance agents located throughout the United States. These wealth management solutions include our investment management programs and back-office investment processing outsourcing services. We also help advisors manage and grow their businesses by giving them access to our marketing support programs, business assessment assistance and recommended management practices. Our solutions aim to help investment advisors reduce risk, improve quality, and gain operational efficiency to devote more of their resources to servicing their clients.

Advisors are responsible for the investor relationship which includes creating financial plans, implementing investment strategies and educating and servicing their customers. Advisors may customize portfolios to include separate account managers provided through our programs as well as SEI-sponsored mutual funds. Our wealth and investment programs are designed to be attractive to affluent or high-net-worth individual investors with over $250 thousand of investable assets and small to medium-sized institutional plans.

We continually enhance our offering to meet the emerging needs of our advisors and their end clients. For example, in 2009, we introduced a new goals-based statement package rated by DALBAR, Inc. as one of the best in the mutual fund industry.

Although we have agreements with over 5,700 financial advisors, our business is based primarily on approximately 1,100 clients who, at December 31, 2009, had at least $5.0 million each in customer assets invested in our mutual funds and separately managed accounts. Revenues are earned largely as a percentage of average assets under management.

The principal competition for our investment management products is from other money managers and mutual fund companies. In the advisor distributor channel, the principal competitors include AssetMark Investment Services Inc., Brinker Capital, EnvestNet Asset Management, Inc., Fidelity Investments, Lockwood Advisors, Inc., a subsidiary of The Bank of New York Mellon, Charles Schwab & Co., Inc., and other broker-dealers.

Institutional Investors

The Institutional Investors segment offers investment management programs and administrative outsourcing solutions for retirement plan sponsors and not-for-profit organizations globally. Clients can outsource their entire investment management needs and the administration for defined benefit plans, defined contribution plans, endowments, foundations and other balance sheet assets, as well as the administration of endowment and foundation asset pools.

The outsourcing program provides a strategic platform integrating the Manager-of-Managers investment process, plan administration services, and consulting services. Plan administration services include trustee, custodial, benefit payment services, record-keeping services, and donor administration. Consulting services include actuarial services, asset liability modeling, and the customization of an asset allocation plan that is designed to meet long-term objectives.

By outsourcing retirement plan services, we believe clients benefit from an investment approach built around an investment plan designed to meet the client’s long-term business and plan objectives and an investment process that removes the responsibility of manager selection. This approach is designed to reduce business risk, provide ongoing due diligence, and increase operational efficiency. Nonprofit organizations can manage volatility through more diversified portfolios and focus more resources on achieving their overall mission. Healthcare organizations benefit from customized asset allocations that help provide improved balance sheet protection and overall financial risk management.

Fees are primarily earned as a percentage of average assets under management. At December 31, 2009, we had relationships with approximately 525 institutional investor clients. The principal competitors for this segment are Frank Russell Company, a subsidiary of The Northwestern Mutual Life Insurance Company, and Northern Trust Corporation.

Page 7 of 97

Table of Contents

Investment Managers

The Investment Manager Services segment provides comprehensive operations outsourcing solutions to investment managers globally. This array of back-, middle- and front-office investment processing services integrate best-in-class industry tools and technology to support a manager’s diverse business needs across multiple products and asset classes. Our clients are retail and institutional investment managers with global offerings that span the investment management industry. We offer managers support for traditional investment products such as mutual funds, collective investment trusts, exchange-traded funds, and institutional and separate accounts, by providing outsourcing services including accounting, administration, reconciliation, investor servicing and client reporting. We also provide comprehensive solutions to managers focused on alternative investments who manage hedge funds, funds of hedge funds, and private equity funds, across both registered and partnership structures.

By applying operating services, technologies, and business and regulatory knowledge, our solutions help investment managers focus on their core competencies of portfolio management and investor relations. This allows them to better manage their business risk, improve accuracy and efficiency, and, through our proprietary and best of breed systems, receive tools and analytics through which to gain insight about, and better manage, their business.

Contracts for our outsourcing and investment processing services generally have terms ranging from one to five years. Fees are primarily earned as a percentage of average assets under management and administration. At December 31, 2009, we had relationships with approximately 180 investment management companies and alternative investment managers. Our competitors for this segment include GlobeOp Financial Services, Citco, and State Street Bank and Trust Company.

Investments in New Businesses

The Investments in New Businesses segment represents other business ventures intended to expand our investment solutions to include ultra-high-net-worth families who reside in the United States. The family wealth management solution offers flexible family-office type services through a highly personalized solution while utilizing the Manager-of-Managers investment process.

The principal competitors for the family wealth solution are diversified financial services providers focused on the ultra-high-net-worth market.

LSV Asset Management

LSV is a registered investment advisor that provides investment advisory services to institutions, including pension plans and investment companies. LSV is a value-oriented, contrarian money manager offering a deep-value investment alternative utilizing a proprietary equity investment model to identify securities generally considered to be out of favor by the market. LSV is currently one of the specialist advisors to a number of our equity mutual funds. In addition, LSV is a portfolio manager to a portion of our global investment products. At December 31, 2009, LSV managed approximately $52.5 billion in total assets, of which approximately $1.6 billion were assets in our mutual funds.

Research and Development

We are devoting significant resources to research and development, including expenditures for new technology platforms, enhancements to existing technology platforms, and new investment products and services. We spent approximately $103.9 million in 2009, $117.5 million in 2008, and $141.9 million in 2007, of which we capitalized approximately $43.9 million in 2009, $56.2 million in 2008, and $61.4 million in 2007 relating to the development of new technology platforms. Total research and development expenditures as a percentage of revenues were 12.2 percent in 2009, 11.9 percent in 2008, and 13.9 percent in 2007. All percentages exclude the revenues of LSV.

The majority of our research and development spending is related to building our Global Wealth Platform (GWP). GWP combines business service processing with asset management and distribution services. The platform offers to our customers a client-centric, rather than an account-centric, process with model-based portfolio management providing services through a single platform. The platform utilizes our proprietary applications with those built by third-party providers, and integrates them into a single technology solution, providing a common user experience. This integration supports straight-through business processing and enables the transformation of our clients’ trust services from operational investment processing services to client value-added services.

The solution will serve U.K., European and U.S. markets. GWP provides the technology platform for the business solutions now being marketed to private banks and independent wealth adviser organizations in the United Kingdom. The TRUST 3000® platform does not meet certain requirements of U.K. and European markets such as trade-date

Page 8 of 97

Table of Contents

reporting, trade-date investment accounting, and multi-lingual reporting. In U.S. markets, we believe the demand for the advanced capabilities of the new platform will enable us to market our services to global wealth managers and existing clients in the Private Banks segment and improve the services we offer in the Investment Advisors segment. It is our current expectation that GWP will be deployed in the United States in 2012.

GWP will eventually be used at some level by all business segments, except LSV. The front-end components will be used by us and by our clients to manage customer administration and portfolio management. The back-office components will streamline all investment-related activities and will eliminate manual processes and perform trade order execution and settlement activities.

Marketing and Sales

Our business solutions are directly marketed to potential clients in our target markets. We employ approximately 100 sales representatives who operate from offices located throughout the United States, Canada, the United Kingdom, continental Europe, South Africa, Asia and other locations.

Customers

In 2009, no single customer accounted for more than ten percent of revenues in any business segment.

Personnel

At January 31, 2010, we had approximately 2,220 full-time and 70 part-time employees. None of our employees is unionized. Management considers employee relations to be generally good.

Regulatory Considerations

Our principal wholly-owned subsidiaries are SEI Investments Distribution Co., or SIDCO, SEI Investments Management Corporation, or SIMC, SEI Private Trust Company, or SPTC, SEI Trust Company, or STC, and SEI Investments (Europe) Limited, or SIEL. SIDCO is a broker-dealer registered with the SEC under the Securities and Exchange Act of 1934 and is a member of the Financial Industry Regulatory Authority, Inc. SIMC is an investment advisor registered with the SEC under the Investment Advisers Act of 1940. SPTC is a limited purpose federal thrift chartered and regulated by the United States Office of Thrift Supervision. STC is a Pennsylvania trust company, regulated by the Pennsylvania Department of Banking. SIEL is an investment manager and financial institution subject to regulation by the Financial Services Authority of the United Kingdom. In addition, various SEI subsidiaries are subject to the jurisdiction of regulatory authorities in Canada, the Republic of Ireland and other foreign countries. The Company has a minority ownership interest in LSV, which is also an investment advisor registered with the SEC.

SIDCO and SIMC are subject to various federal and state laws and regulations that grant supervisory agencies, including the SEC, broad administrative powers. In the event of a failure to comply with these laws and regulations, the possible sanctions that may be imposed include the suspension of individual employees, limitations on the permissibility of SIDCO, SIMC, SEI, and our other subsidiaries to engage in business for specified periods of time, the revocation of applicable registration as a broker-dealer or investment advisor, as the case may be, censures, and fines. SPTC and STC are subject to laws and regulations imposed by federal and state banking authorities. In the event of a failure to comply with these laws and regulations, restrictions, including revocation of applicable banking charter, may be placed on the business of these companies and fines or other sanctions may be imposed. Additionally, the securities and banking laws applicable to us and our subsidiaries provide for certain private rights of action that could give rise to civil litigation. Any litigation could have significant financial and non-financial consequences including monetary judgments and the requirement to take action or limit activities that could ultimately affect our business.

Compliance with existing and future regulations and responding to and complying with recent regulatory activity affecting broker-dealers, investment advisors, investment companies and their service providers and financial institutions could have a significant impact on us. We periodically undergo regulatory examinations and respond to regulatory inquiries and document requests. As a result of these examinations, inquiries and requests, we review our compliance procedures and business operations, and make changes as we deem necessary, some of which may result in increased expense or may reduce revenues.

We offer investment and banking products that also are subject to regulation by the federal and state securities and banking authorities, as well as foreign regulatory authorities, where applicable. Existing or future regulations that affect these products could lead to a reduction in sales of these products.

Page 9 of 97

Table of Contents

Our bank clients are subject to supervision by federal and state banking authorities concerning the manner in which such clients purchase and receive our products and services. Our plan sponsor clients and our subsidiaries providing services to those clients are subject to supervision by the Department of Labor and compliance with employee benefit regulations. Investment advisor and broker-dealer clients are regulated by the SEC and state securities authorities. Existing or future regulations applicable to our clients may affect our clients’ purchase of our products and services.

In addition, see the discussion of governmental regulations in Item 1A “Risk Factors” for a description of the risks that proposed regulatory changes may present for our business.

Available Information

We maintain a website at www.seic.com and make available free of charge through the Investors section of this website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. We include our website in this Annual Report on Form 10-K only as an inactive textual reference and do not intend it to be an active link to our website. The material on our website is not part of this Annual Report on Form 10-K.

| Item 1A. | Risk Factors. |

We believe that the risks and uncertainties described below are those that impose the greatest threat to the sustainability of our business. However, there are other risks and uncertainties that exist that may be unknown to us or, in the present opinion of our management, do not currently pose a material risk of harm to us. The risk and uncertainties facing our business, including those described below, could materially adversely affect our business, results of operations, financial condition and liquidity.

Our revenues and earnings are affected by changes in capital markets. A majority of our revenues are earned based on the value of assets invested in investment products that we manage or administer. Significant fluctuations in securities prices may materially affect the value of these assets and may also influence an investor’s decision to invest in and maintain an investment in a mutual fund or other investment product. As a result, our revenues and earnings derived from assets under management and administration could be adversely affected.

A majority of the securities held by our investment products are valued using quoted prices from active markets gathered by external pricing services. Securities for which market prices are not readily available are valued in accordance with procedures applicable to that investment product. These procedures may utilize unobservable inputs that are not gathered from any active markets and involve considerable judgment. If these valuations prove to be inaccurate, our revenues and earnings from assets under management could be adversely affected.

We are exposed to product development risk. We continually strive to increase revenues and meet our customers’ needs by introducing new products and services. As a result, we are subject to product development risk, which may result in loss if we are unable to develop and deliver fully functional products to our target markets that address our clients’ needs and that are developed on a timely basis and reflect an attractive value proposition. New product development is primarily for the purpose of enhancing our competitive position in the industry. In the event that we fail to develop products or services at an acceptable cost or on a timely basis or if we fail to deliver functional products and services which are of sound, economic value to our clients and our target markets, or an inability to support the product in a cost-effective manner, we could suffer significant financial loss.

The majority of our efforts pertains to the development and deployment of the Global Wealth Platform (GWP). In 2007, the initial version of GWP was offered to private banks in the United Kingdom. We intend to implement enhancements and upgrades to the platform through a series of releases that will eventually provide the full functionality of GWP to clients across numerous jurisdictions. Future releases may include enhancements that could replace significant components that currently exist in the platform. If this occurs, we may incur significant costs due to the requirement to immediately expense the remaining net book value of previously capitalized development costs of those components that were replaced.

Consolidation within our target markets may affect our business. Merger and acquisition activity between banks and other financial institutions could reduce the number of existing and prospective clients or reduce the amount of revenue we receive from retained clients. Consolidation activities may also cause larger institutions to internalize some or all of our services. These factors may negatively impact our ability to generate future growth in revenues and earnings.

We are dependent upon third-party service providers in our operations. We utilize numerous third-party service providers in our operations, in the development of new products, and in the maintenance of our proprietary systems.

Page 10 of 97

Table of Contents

A failure by a third-party service provider could expose us to an inability to provide contractual services to our clients in a timely basis. Additionally, if a third-party service provider is unable to provide these services, we may incur significant costs to either internalize some of these services or find a suitable alternative.

During the past 18 months, the financial services industry has faced an extremely difficult economic environment. Many of the challenges posed by this environment have raised serious concerns related to the financial health of banks. We utilize the services of banks in our operations. Although we have undertaken measures to reduce the potential disruption to our operations and the delivery of services to our clients in the event that any of these banks should fail, our revenues and earnings could be significantly affected if the financial health of certain banks continues to deteriorate or if they become insolvent.

Poor fund performance may affect our revenues and earnings. Our ability to maintain our existing clients and attract new clients may be negatively affected if the performance of our mutual funds and other investment products, relative to market conditions and other comparable competitive investment products, is lower. Investors may decide to place their investable funds elsewhere which would reduce the amount of assets we manage resulting in a decrease in our revenues.

The Company and our clients are subject to extensive governmental regulation. Our various business activities are conducted through entities which may be registered with the Securities and Exchange Commission (SEC) as an investment advisor, a broker-dealer, a transfer agent, an investment company or with the United States Office of Thrift Supervision or state banking authorities as a trust company. Our broker-dealer is also a member of the Financial Industry Regulatory Authority and is subject to its rules and oversight. In addition, some of our foreign subsidiaries are registered with, and subject to the oversight of, regulatory authorities primarily in the United Kingdom and the Republic of Ireland. Many of our clients are subject to substantial regulation by federal and state banking, securities or insurance authorities or the Department of Labor. Compliance with existing and future regulations and responding to and complying with recent regulatory activity affecting broker-dealers, investment advisors, investment companies and their service providers and financial institutions could have a significant impact on us.

We offer investment and banking products that also are subject to regulation by the federal and state securities and banking authorities, as well as foreign regulatory authorities, where applicable. Existing or future regulations that affect these products could lead to a reduction in sales of these products or an increase in the cost of providing these products.

As a result of the recent economic and political developments, there has been an unusual amount of speculation about governmental regulation of financial institutions and financial products. Changes in laws or regulations and changes in the identity or policies of the regulators having jurisdiction over our regulated subsidiaries, products or clients could have a material impact on our markets, customers, solutions, revenues and costs.

We are exposed to systems and technology risks. Through our proprietary systems, we maintain and process data for our clients that is critical to their business operations. An unanticipated interruption of service may have significant ramifications, such as lost data, damaged software codes, or inaccurate processing of transactions. As a result, the costs necessary to rectify these problems may be substantial.

We are exposed to data security risks. A failure to safeguard the integrity and confidentiality of client data and our proprietary data from the infiltration by an unauthorized user that is either stored on or transmitted between our proprietary systems or to other third party service provider systems may lead to modifications or theft of critical and sensitive data pertaining to us or our clients. The costs incurred to correct client data and prevent further unauthorized access to our data or client data could be extensive.

We are dependent upon third party approvals. Many of the investment advisors through which we distribute our investment offerings are affiliated with independent broker-dealers or other networks, which have regulatory responsibility for the advisor’s practice. As part of the regulatory oversight, these broker-dealers or networks must approve the use of our investment products by affiliated advisors within their networks. Failure to receive such approval, or the withdrawal of such approval, could adversely affect the marketing of our investment products.

We are exposed to operational risks. Operational risk generally refers to the risk of loss resulting from our operations, including, but not limited to, improper or unauthorized execution and processing of transactions, deficiencies in our operating systems, business disruptions and inadequacies or breaches in our internal control processes. We operate different businesses in diverse markets and are reliant on the ability of our employees and systems to process large volumes of transactions often within short time frames. In the event of a breakdown or improper operation of systems, human error or improper action by employees, we could suffer financial loss, regulatory sanctions or damage to our reputation. In order to mitigate and control operational risk, we continue to enhance policies and procedures that are designed to identify and manage operational risk.

Page 11 of 97

Table of Contents

Changes in, or interpretation of, accounting principles could affect our revenues and earnings. We prepare our consolidated financial statements in accordance with generally accepted accounting principles. A change in these principles can have a significant effect on our reported results and may even retrospectively affect previously reported results.

Changes in, or interpretations of, tax rules and regulations may adversely affect our effective tax rates. Unanticipated changes in our tax rates could affect our future results of operations. Our future effective tax rates could be adversely affected by changes in tax laws or the interpretation of tax laws. We are subject to possible examinations of our income tax returns by the Internal Revenue Service and state and foreign tax authorities. We regularly assess the likelihood of outcomes resulting from these examinations to determine the adequacy of our provision for income taxes, however, there can be no assurance that the final determination of any examination will not have an adverse effect on our operating results or financial position.

Currency fluctuations could negatively affect our future revenues and earnings as our business grows globally. We operate and invest globally to expand our business into foreign markets. Our foreign subsidiaries use the local currency as the functional currency. As these businesses evolve, our exposure to changes in currency exchange rates may increase. Adverse movements in currency exchange rates may negatively affect our operating results, liquidity and financial condition.

We rely on our executive officers and senior management. Most of our executive officers and senior management personnel do not have employment agreements with us. The loss of these individuals may have a material adverse affect on our future operations.

| Item 1B. | Unresolved Staff Comments. |

None.

| Item 2. | Properties. |

Our corporate headquarters is located in Oaks, Pennsylvania and consists of nine buildings situated on approximately 90 acres. We own and operate the land and buildings, which encompass approximately 486,000 square feet of office space and 34,000 square feet of data center space. We lease other offices which aggregate 60,000 square feet. We also own a 3,400 square foot condominium that is used for business purposes in New York, New York.

| Item 3. | Legal Proceedings. |

One of SEI’s principal subsidiaries, SIDCO, has been named as a defendant in certain putative class action complaints (the Complaints) related to leveraged exchange traded funds (ETFs) advised by ProShares Advisors, LLC. To date, the Complaints have been filed in the United States District Court for the Southern District of New York and in the United States District Court for the District of Maryland although the three complaints filed in the District of Maryland have been voluntarily dismissed by the plaintiffs. Two of them were subsequently re-filed in the Southern District of New York. Two of the complaints filed in the Southern District of New York have been voluntarily dismissed by plaintiffs. The first complaint was filed on August 5, 2009. The Complaints are purportedly made on behalf of all persons that purchased or otherwise acquired shares in various ProShares leveraged ETFs pursuant or traceable to allegedly false and misleading registration statements, prospectuses and statements of additional information. The Complaints name as defendants ProShares Advisors, LLC; ProShares Trust; ProShares Trust II, SIDCO, and various officers and trustees to ProShares Advisors, LLC; ProShares Trust and ProShares Trust II. The Complaints allege that SIDCO was the distributor and principal underwriter for the various ProShares leveraged ETFs that were distributed to authorized participants and ultimately shareholders. The complaints allege that the registration statements for the ProShares ETFs were materially false and misleading because they failed adequately to describe the nature and risks of the investments. The Complaints allege that SIDCO is liable for these purportedly material misstatements and omissions under Section 11 of the Securities Act of 1933. The Complaints seek unspecified compensatory and other damages, reasonable costs and other relief. The cases are in the early stage, and the court has not yet appointed lead plaintiff(s). Defendants have moved to consolidate the complaints, which motion is pending. While the outcome of this litigation is uncertain given its early phase, SEI believes that it has valid defenses to plaintiffs’ claims and intends to defend the lawsuits vigorously.

SEI has also been named in three lawsuits that were filed in August 2009 in the 19th Judicial District Court for the Parish of East Baton Rouge, State of Louisiana. One of the three actions purports to set forth claims on behalf of a class and also names SPTC as a defendant. All three actions name various defendants besides

Page 12 of 97

Table of Contents

SEI, and, in all three actions, the plaintiffs purport to bring a cause of action against SEI under the Louisiana Securities Act. The putative class action also includes a claim against SEI for an alleged violation of the Louisiana Unfair Trade Practices Act. In addition, in December 2009, a group of six plaintiffs filed a lawsuit in the 23rd Judicial District Court for the Parish of Ascension, State of Louisiana, against SEI and other defendants asserting claims of negligence, breach of contract, breach of fiduciary duty, violations of the uniform fiduciaries law, negligent misrepresentation, detrimental reliance, violations of the Louisiana Securities Act, and Louisiana Racketeering Act and conspiracy. Further, SEI is aware that, in February 2010, two groups of plaintiffs amended petitions they had previously filed in the 19th Judicial District for the Parish of East Baton Rouge, State of Louisiana, to add claims against SEI and SPTC for alleged violations of the Louisiana Securities Act, the Louisiana Racketeering Act, and civil conspiracy. The underlying allegations in all six actions are purportedly related to the role of SPTC in providing data consolidation, securities processing, and other services to Stanford Trust Company. Two of the three actions filed in East Baton Rouge have been removed to federal court, and plaintiffs’ motions to remand are pending. These two cases were also transferred by the Judicial Panel on Multidistrict Litigation (MDL) to a MDL pending in the Northern District of Texas. The case filed in Ascension was also removed to federal court and transferred by the Judicial Panel on Multidistrict Litigation to the same MDL pending in the Northern District of Texas. The schedule for responding to that complaint has not yet been established. SEI and SPTC filed exceptions in the putative class action that remains pending in East Baton Rouge, which the Court granted in part and dismissed the claims under the Louisiana Unfair Trade Practices Act and denied, in part, as to the other exceptions. The response to that petition will be due ten days after the Court formally enters the order reflecting its ruling on the exceptions. The time for SEI and SPTC to respond to the two amended petitions adding claims has not yet run. While the outcome of this litigation is uncertain given its early phase, SEI and SPTC believe that they have valid defenses to plaintiffs’ claims and intend to defend the lawsuits vigorously.

| Item 4. | Submission of Matters to a Vote of Security Holders. |

There were no matters submitted to a vote of security holders during the fourth quarter of 2009.

Executive Officers of the Registrant

Information about our executive officers is contained in Item 10 of this report and is incorporated by reference into this Part I.

Page 13 of 97

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Price Range of Common Stock and Dividends:

Our common stock is traded on The Nasdaq Global Select Market® (NASDAQ) under the symbol “SEIC.” The following table shows the high and low sales prices for our common stock as reported by NASDAQ and the dividends declared on our common stock for the last two years. Our Board of Directors intends to declare future dividends on a semiannual basis.

| 2009 |

High | Low | Dividends | ||||||

| First Quarter |

$ | 16.25 | $ | 9.19 | $ | — | |||

| Second Quarter |

18.52 | 11.74 | .08 | ||||||

| Third Quarter |

20.00 | 16.66 | — | ||||||

| Fourth Quarter |

20.36 | 17.18 | .09 | ||||||

| 2008 |

High | Low | Dividends | ||||||

| First Quarter |

$ | 32.49 | $ | 22.99 | $ | — | |||

| Second Quarter |

26.93 | 22.84 | .08 | ||||||

| Third Quarter |

24.99 | 16.14 | — | ||||||

| Fourth Quarter |

23.77 | 11.64 | .08 | ||||||

As of January 31, 2010, we estimate that we had approximately 450 shareholders of record.

For information on our equity compensation plans, refer to Note 9 to the Consolidated Financial Statements and Item 12 of this Annual Report on Form 10-K.

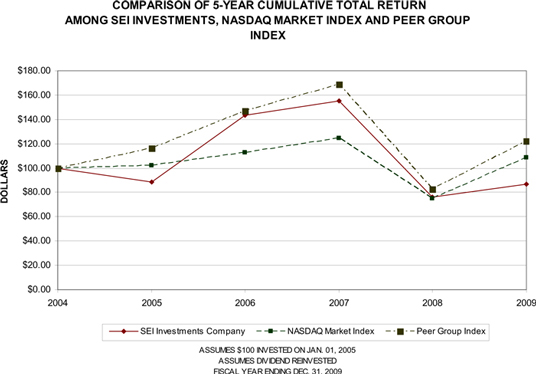

Comparison of Cumulative Total Return of Common Stock, Industry Index and Nasdaq Market Index:

Page 14 of 97

Table of Contents

Issuer Purchases of Equity Securities:

Our Board of Directors has authorized the repurchase of up to $1.63 billion of our common stock. Currently, there is no expiration date for our common stock repurchase program.

Information regarding the repurchase of common stock during the three months ended December 31, 2009 is:

| Period |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Program |

Approximate Dollar Value of Shares that May Yet Be Purchased Under the Program | ||||||

| October 1 – 31, 2009 |

235,000 | $ | 18.02 | 235,000 | $ | 46,262,000 | ||||

| November 1 – 30, 2009 |

525,000 | 17.75 | 525,000 | 36,945,000 | ||||||

| December 1 – 31, 2009 |

483,000 | 17.66 | 483,000 | 128,422,000 | ||||||

| Total |

1,243,000 | $ | 17.76 | 1,243,000 | ||||||

| Item 6. | Selected Financial Data. |

(In thousands, except per-share data)

This table presents selected consolidated financial information for the five-year period ended December 31, 2009. This data should be read in conjunction with the financial statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this Annual Report on Form 10-K.

| Year Ended December 31, |

2009 | 2008 | 2007 | 2006 (A) | 2005 | |||||||||||||||

| Revenues |

$ | 1,060,548 | $ | 1,247,919 | $ | 1,369,028 | $ | 1,175,749 | $ | 773,007 | ||||||||||

| Total expenses |

696,841 | 751,570 | 775,053 | 677,298 | 557,915 | |||||||||||||||

| Income from operations |

363,707 | 496,349 | 593,975 | 498,451 | 215,092 | |||||||||||||||

| Other (expense) income |

(1,389 | ) | (142,119 | ) | (8,556 | ) | 7,267 | 83,256 | ||||||||||||

| Income before income taxes |

362,318 | 354,230 | 585,419 | 505,718 | 298,348 | |||||||||||||||

| Income taxes |

89,886 | 86,703 | 151,182 | 123,218 | 107,778 | |||||||||||||||

| Net income |

272,432 | 267,527 | 434,237 | 382,500 | 190,570 | |||||||||||||||

| Less: Net income attributable to the noncontrolling interest |

(98,097 | ) | (128,273 | ) | (174,428 | ) | (145,510 | ) | (2,226 | ) | ||||||||||

| Net income attributable to SEI Investments |

174,335 | 139,254 | 259,809 | 236,990 | 188,344 | |||||||||||||||

| Basic earnings per common share |

$ | 0.91 | $ | 0.73 | $ | 1.32 | $ | 1.20 | $ | 0.94 | ||||||||||

| Shares used to calculate basic earnings per common share |

190,821 | 192,057 | 196,120 | 197,364 | 200,742 | |||||||||||||||

| Diluted earnings per common share |

$ | 0.91 | $ | 0.71 | $ | 1.28 | $ | 1.17 | $ | 0.91 | ||||||||||

| Shares used to calculate diluted earnings per common share |

191,783 | 195,233 | 202,231 | 203,266 | 206,276 | |||||||||||||||

| Cash dividends declared per common share |

$ | .17 | $ | .16 | $ | .14 | $ | .12 | $ | .11 | ||||||||||

| Financial Position as of December 31, |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 590,877 | $ | 416,643 | $ | 360,921 | $ | 286,948 | $ | 130,128 | ||||||||||

| Total assets |

$ | 1,533,808 | $ | 1,341,715 | $ | 1,252,365 | $ | 1,079,705 | $ | 657,147 | ||||||||||

| Long-term debt (including current portion) |

$ | 253,552 | $ | 31,532 | $ | 51,971 | $ | 80,638 | $ | 14,389 | ||||||||||

| SEI Investments Shareholders’ equity |

$ | 909,723 | $ | 769,152 | $ | 756,383 | $ | 630,512 | $ | 421,688 | ||||||||||

| (A) | Beginning in 2006, our financial information includes the consolidation of LSV and LSV Employee Group as well as the impact of stock-based compensation charges. In prior periods, our proportionate share in the earnings of LSV earnings was reported in Equity in earnings of unconsolidated affiliate which was a component of other income (See Notes 2 and 9 to the Consolidated Financial Statements for information regarding LSV and LSV Employee Group and stock-based compensation, respectively). |

Page 15 of 97

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

(In thousands, except per-share data)

This discussion reviews and analyzes the consolidated financial condition at December 31, 2009 and 2008, the consolidated results of operations for the years ended December 31, 2009, 2008, and 2007, and other factors that may affect future financial performance. This discussion should be read in conjunction with the Selected Financial Data included in Item 6 of this Annual Report and the Consolidated Financial Statements and Notes to the Consolidated Financial Statements included in Item 8 of this Annual Report.

Overview

Our Business and Business Segments

We are a leading global provider of investment processing, fund processing, and investment management business outsourcing solutions that help corporations, financial institutions, financial advisors, and ultra-high-net-worth families create and manage wealth. Investment processing fees are earned as monthly fees for contracted services, including computer processing services, software licenses, and trust operations services, as well as transaction-based fees for providing securities valuation and trade-execution. Fund processing and investment management fees are earned as a percentage of average assets under management or administration. As of December 31, 2009, through our subsidiaries and partnerships in which we have a significant interest, we administer $391.7 billion in mutual fund and pooled assets, manage $158.8 billion in assets, and operate from numerous offices worldwide.

Our reportable business segments are:

Private Banks – provides investment processing and investment management programs to banks and trust institutions worldwide, independent wealth advisers located in the United Kingdom, and financial advisors in Canada and accounts for 34 percent of consolidated revenues in 2009;

Investment Advisors – provides investment management programs to affluent investors through a network of independent registered investment advisors, financial planners, and other investment professionals in the United States and accounts for 16 percent of consolidated revenues in 2009;

Institutional Investors – provides investment management programs and administrative outsourcing solutions to retirement plan sponsors and not-for-profit organizations worldwide and accounts for 16 percent of consolidated revenues in 2009;

Investment Managers – provides investment processing, fund processing, and operational outsourcing solutions to investment managers, fund companies, and banking institutions located in the United States, and to investment managers worldwide of alternative asset classes such as hedge funds, funds of hedge funds, and private equity funds across both registered and partnership structures and accounts for 13 percent of consolidated revenues in 2009;

Investments in New Businesses – provides investment management programs to ultra-high-net-worth families residing in the United States through the SEI Wealth Network®. This segment accounts for one percent of consolidated revenues in 2009; and

LSV Asset Management – is a registered investment advisor that provides investment advisory services to institutions, including pension plans and investment companies. This segment accounts for 20 percent of consolidated revenues in 2009.

Page 16 of 97

Table of Contents

Results of Operations

Revenues, Expenses, and Operating Profit (Loss) by business segment for the year ended 2009 compared to the year ended 2008, and for the year ended 2008 compared to the year ended 2007 are:

| Year Ended December 31, |

2009 | 2008 | Percent Change |

2007 | Percent Change |

|||||||||||||

| Private Banks: |

||||||||||||||||||

| Revenues |

$ | 361,273 | $ | 408,500 | (12 | )% | $ | 413,922 | (1 | )% | ||||||||

| Expenses |

309,300 | 326,661 | (5 | )% | 330,923 | (1 | )% | |||||||||||

| Operating Profit |

51,973 | 81,839 | (36 | )% | 82,999 | (1 | )% | |||||||||||

| Investment Advisors: |

||||||||||||||||||

| Revenues |

166,097 | 223,164 | (26 | )% | 259,288 | (14 | )% | |||||||||||

| Expenses |

109,418 | 122,231 | (10 | )% | 124,942 | (2 | )% | |||||||||||

| Operating Profit |

56,679 | 100,933 | (44 | )% | 134,346 | (25 | )% | |||||||||||

| Institutional Investors: |

||||||||||||||||||

| Revenues |

177,721 | 198,154 | (10 | )% | 199,593 | (1 | )% | |||||||||||

| Expenses |

99,924 | 112,866 | (11 | )% | 121,365 | (7 | )% | |||||||||||

| Operating Profit |

77,797 | 85,288 | (9 | )% | 78,228 | 9 | % | |||||||||||

| Investment Managers: |

||||||||||||||||||

| Revenues |

139,004 | 147,968 | (6 | )% | 143,375 | 3 | % | |||||||||||

| Expenses |

93,074 | 101,078 | (8 | )% | 101,401 | — | ||||||||||||

| Operating Profit |

45,930 | 46,890 | (2 | )% | 41,974 | 12 | % | |||||||||||

| Investments in New Businesses: |

||||||||||||||||||

| Revenues |

4,492 | 6,865 | (35 | )% | 7,205 | (5 | )% | |||||||||||

| Expenses |

11,625 | 15,795 | (26 | )% | 19,670 | (20 | )% | |||||||||||

| Operating Loss |

(7,133 | ) | (8,930 | ) | (20 | )% | (12,465 | ) | (28 | )% | ||||||||

| LSV: |

||||||||||||||||||

| Revenues |

211,961 | 263,268 | (19 | )% | 345,645 | (24 | )% | |||||||||||

| Expenses(1) |

136,580 | 164,783 | (17 | )% | 213,926 | (23 | )% | |||||||||||

| Operating Profit |

75,381 | 98,485 | (23 | )% | 131,719 | (25 | )% | |||||||||||

| Totals: |

||||||||||||||||||

| Revenues |

1,060,548 | 1,247,919 | (15 | )% | 1,369,028 | (9 | )% | |||||||||||

| Expenses |

759,921 | 843,414 | (10 | )% | 912,227 | (8 | )% | |||||||||||

| Corporate overhead expenses |

36,529 | 38,955 | (6 | )% | 42,045 | (7 | )% | |||||||||||

| Noncontrolling interest reflected in segments |

(106,905 | ) | (138,079 | ) | (23 | )% | (186,500 | ) | (26 | )% | ||||||||

| LSV Employee Group Expenses |

7,296 | 7,280 | — | 7,281 | — | |||||||||||||

| Income from operations |

$ | 363,707 | $ | 496,349 | (27 | )% | $ | 593,975 | (16 | )% | ||||||||

| (1) | For the years ended December 31, 2009, 2008 and 2007, includes $105,471, $135,251 and $181,591, respectively, of noncontrolling interest of the other partners of LSV. |

Page 17 of 97

Table of Contents

Asset Balances

This table presents assets of our clients, or of our clients’ customers, for which we provide management or administrative services. These assets are not included in our balance sheets because we do not own them.

| Asset Balances (In millions) |

As of December 31, | ||||||||||||||

| 2009 | 2008 | Percent Change |

2007 | Percent Change |

|||||||||||

| Private Banks: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 12,690 | $ | 10,573 | 20 | % | $ | 21,160 | (50 | )% | |||||

| Collective trust fund programs |

1,067 | 1,145 | (7 | )% | 1,007 | 14 | % | ||||||||

| Liquidity funds |

6,035 | 9,194 | (34 | )% | 8,886 | 3 | % | ||||||||

| Total assets under management |

$ | 19,792 | $ | 20,912 | (5 | )% | $ | 31,053 | (33 | )% | |||||

| Client proprietary assets under administration |

11,213 | 10,622 | 6 | % | 14,235 | (25 | )% | ||||||||

| Total assets |

$ | 31,005 | $ | 31,534 | (2 | )% | $ | 45,288 | (30 | )% | |||||

| Investment Advisors: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 25,392 | $ | 21,631 | 17 | % | $ | 36,378 | (41 | )% | |||||

| Collective trust fund programs |

2,423 | 2,606 | (7 | )% | 2,295 | 14 | % | ||||||||

| Liquidity funds |

1,929 | 3,436 | (44 | )% | 2,079 | 65 | % | ||||||||

| Total assets under management |

$ | 29,744 | $ | 27,673 | 7 | % | $ | 40,752 | (32 | )% | |||||

| Institutional Investors: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 44,322 | $ | 34,966 | 27 | % | $ | 44,833 | (22 | )% | |||||

| Collective trust fund programs |

684 | 942 | (27 | )% | 897 | 5 | % | ||||||||

| Liquidity funds |

3,370 | 4,582 | (26 | )% | 3,629 | 26 | % | ||||||||

| Total assets under management |

$ | 48,376 | $ | 40,490 | 19 | % | $ | 49,359 | (18 | )% | |||||

| Investment Managers: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 4 | $ | 8 | (50 | )% | $ | 24 | (67 | )% | |||||

| Collective trust fund programs |

7,428 | 5,974 | 24 | % | 6,651 | (10 | )% | ||||||||

| Liquidity funds |

412 | 869 | (53 | )% | 325 | 167 | % | ||||||||

| Total assets under management |

$ | 7,844 | $ | 6,851 | 14 | % | $ | 7,000 | (2 | )% | |||||

| Client proprietary assets under administration |

221,680 | 234,628 | (6 | )% | 215,124 | 9 | % | ||||||||

| Total assets |

$ | 229,524 | $ | 241,479 | (5 | )% | $ | 222,124 | 9 | % | |||||

| Investments in New Businesses: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 520 | $ | 519 | — | $ | 929 | (44 | )% | ||||||

| Liquidity funds |

75 | 153 | (51 | )% | 74 | 107 | % | ||||||||

| Total assets under management |

$ | 595 | $ | 672 | (11 | )% | $ | 1,003 | (33 | )% | |||||

| LSV: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 52,488 | $ | 37,714 | 39 | % | $ | 67,599 | (44 | )% | |||||

| Consolidated: |

|||||||||||||||

| Equity and fixed-income programs |

$ | 135,416 | $ | 105,411 | 28 | % | $ | 170,923 | (38 | )% | |||||

| Collective trust fund programs |

11,602 | 10,667 | 9 | % | 10,850 | (2 | )% | ||||||||

| Liquidity funds |

11,821 | 18,234 | (35 | )% | 14,993 | 22 | % | ||||||||

| Total assets under management |

$ | 158,839 | $ | 134,312 | 18 | % | $ | 196,766 | (32 | )% | |||||

| Client proprietary assets under administration |

232,893 | 245,250 | (5 | )% | 229,359 | 7 | % | ||||||||

| Total assets under management and administration |

$ | 391,732 | $ | 379,562 | 3 | % | $ | 426,125 | (11 | )% | |||||

Page 18 of 97

Table of Contents

Assets under management are total assets of our clients or their customers invested in our equity and fixed-income investment programs, collective trust fund programs, and liquidity funds for which we provide asset management services. Assets under management and administration are total assets of our clients or their customers for whom we provide administrative services, including client proprietary fund balances for which we provide administration and/or distribution services.

General Overview

After experiencing the worst contraction in economic activity of the post-World War II period, the U.S. financial markets began to stabilize during the second quarter of 2009 and continued to improve for the balance of the year. The S&P 5001 and the Dow Jones Industrial Average2 rebounded by 24 percent and 19 percent, respectively, in 2009 after posting severe declines of over 35 percent and 30 percent, respectively, in 2008. Since capital market levels trended higher in the first half of 2008 than in all of 2009, we suffered decreased revenues from Asset management, administration and distribution fees of 19 percent, and an overall reduction in total revenues of 15 percent in 2009.

We continued to feel the negative impact of the depressed economic environment on sales of new business. As the pervasive effects of the severe market uncertainty lessened during the latter half of 2009, the pace of our new business activity began to strengthen, particularly in the Institutional Investors and Investment Managers segments. However, this new business activity contributed only modest increases in revenues as compared to the overall decrease in revenues from market depreciation of assets under management and administration.

In contrast to the flight-to-quality strategies employed during the extreme market volatility in late 2008 and early 2009, investors gradually rotated out of money market funds and other liquid investments and into our higher margin investment products, such as equity and fixed-income funds, as the year progressed. This shift in investments helped to offset losses in revenues due to the capital market depreciation, most notably from U.S. investors in our Private Banks and Investment Advisors segments.