Attached files

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

Commission file number 1-13879

INNOSPEC INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 98-0181725 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| Innospec Manufacturing Park Oil Sites Road Ellesmere Port Cheshire United Kingdom |

CH65 4EY | |

| (Address of principal executive offices) |

(Zip Code) | |

Registrant’s telephone number, including area code: 011-44-151-355-3611

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| N/A |

N/A |

Securities registered pursuant to Section 12 (g) of the Act: Common stock, par value $0.01 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Yes |

| |

| No |

X |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Yes |

| |

| No |

X |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days.

| Yes |

X | |

| No |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| Yes |

| |

| No |

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

| |

| Accelerated filer | X | |

| Non-accelerated filer |

| |

| Smaller reporting company |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

| Yes |

| |

| No |

X |

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of the most recently completed second fiscal quarter (June 30, 2009) was approximately $138 million, based on the closing price of the common shares on the NASDAQ Stock Market on June 30, 2009. Shares of common stock held by each officer and director and by each beneficial owner who owns 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for any other purpose.

As of February 11, 2010, 23,664,053 shares of the registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Innospec Inc.’s Proxy Statement for the Annual Meeting of Stockholders to be held on May 12, 2010 are incorporated by reference into Part III of this Form 10-K.

Table of Contents

1

Table of Contents

CAUTIONARY STATEMENT RELATIVE TO FORWARD-LOOKING STATEMENTS

FORWARD-LOOKING STATEMENTS

This Form 10-K contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical facts included or incorporated herein may constitute forward-looking statements. Such forward-looking statements include statements (covered by words like “expects”, “anticipates”, “may”, “believes” or similar words or expressions), for example, which relate to operating performance, events or developments that we expect or anticipate will or may occur in the future (including, without limitation, any of the Company’s guidance in respect of sales, gross margins, net income, growth potential and other measures of financial performance). Although forward-looking statements are believed by management to be reasonable when made, caution should be exercised not to place undue reliance on such statements because they are subject to certain risks, uncertainties and assumptions, including in respect of the general business environment, regulatory actions or changes. If the risks or uncertainties materialize or assumptions prove incorrect or change, our actual performance or results may differ materially from those expressed or implied by such forward-looking statements and assumptions. You are urged to carefully review and consider the cautionary statements and other disclosures made in those filings, specifically those under the heading “Risk Factors”. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

2

Table of Contents

| Item 1 | Business |

When we use the terms the “Corporation”, “Company”, “Registrant”, “we”, “us”, and “our” unless otherwise indicated or the context otherwise requires, we are referring to Innospec Inc. and its consolidated subsidiaries (“Innospec”).

General

Innospec develops, manufactures, blends and markets fuel additives and other specialty chemicals. Our products are sold primarily to oil refineries and other chemical and industrial companies throughout the world. Our fuel additives help improve fuel efficiency, boost engine performance and reduce harmful emissions. Our specialty chemicals provide effective technology-based solutions for our customers’ processes or products focused in the Personal Care; Household, Industrial & Institutional; and Fragrance Ingredients markets.

Our principal executive offices are in Ellesmere Port, United Kingdom. We became an independent company on May 22, 1998, when we were spun off from our then parent corporation Chemtura Corporation, previously known as Great Lakes Chemical Corporation. We changed our name from Octel Corp. to Innospec Inc. on January 30, 2006. On March 21, 2006 we transferred the listing of our common stock from the New York Stock Exchange (“NYSE”) to the Nasdaq Stock Market (“NASDAQ”).

Segmental Information

Innospec divides its business into three distinct segments for both management and reporting purposes: Fuel Specialties, Active Chemicals and Octane Additives. The Fuel Specialties and Active Chemicals businesses both operate in markets where we actively seek growth opportunities albeit their end customers are very different. The Octane Additives business is characterized by substantial declining demand.

Fuel Specialties

Our Fuel Specialties business develops, manufactures, blends and markets a range of specialty chemical products used as additives to a wide range of fuels. The business specializes in supplying fuel additives that help improve fuel efficiency, boost engine performance and reduce harmful emissions. The business’ products are used in the efficient operation of automotive, marine and aviation engines, power station generators, and heating and diesel particulate filter systems.

Historically, through to the end of 2004, the business had grown through a program of acquisitions. More recently growth in the Fuel Specialties business has been driven by new product development to address what we believe are the key drivers in demand for fuel additives. These key drivers are legislation, population affluence, and energy price and availability. We have devoted substantial resources to the development of new and improved

3

Table of Contents

products that may be used to improve fuel efficiency. Accordingly in our Fuel Specialties segment 43% of our sales in 2009 were derived from products developed during the previous five years.

Active Chemicals

Our Active Chemicals business provides effective technology-based solutions for our customers’ processes or products focused in the Personal Care; Household, Industrial & Institutional; and Fragrance Ingredients markets.

Historically the business has grown through a program of acquisitions. This program has included the acquisition of Finetex, Inc. in January 2005, Innospec Widnes Limited (previously known as Aroma Fine Chemicals Limited) in August 2004, and Innospec Leuna GmbH in June 2004. Effective January 1, 2007 the businesses of Finetex, Inc. and ProChem Chemicals, Inc. were merged into Innospec Active Chemicals LLC (previously known as Innospec Performance Chemicals U.S. Co.).

The focus for our Active Chemicals business is to develop high performance products from its technology base in a focused number of markets.

Octane Additives

Our Octane Additives business is the world’s only producer of tetra ethyl lead (“TEL”). The Octane Additives business comprises sales of TEL for use in automotive gasoline and trading in respect of our environmental remediation business.

TEL was first developed in 1928 and introduced into the European market for internal combustion engines to boost octane levels in gasoline allowing it to burn more efficiently and eliminating engine knock. It also acts as a lubricity aid reducing engine wear and preventing valve seat recession. Worldwide use of TEL has declined since 1973 following the enactment of the U.S. Clean Air Act of 1970 and similar legislation in other countries. The trend of countries exiting the leaded gasoline market has resulted in an average rate of decline in volume terms in demand for TEL in the last five years of approximately 35% per annum. Sales of the Octane Additives business are now concentrated in a relatively small number of customers. Accordingly, volume decline experienced in any one financial period may be greater or less than this average rate of decline and remaining sales in this business may decline with unpredictable volatility and severity.

We intend to manage the decrease in the sales of TEL for use in automotive gasoline to maximize the cash flow through the decline. Continuous cost improvement measures have been, and will continue to be, taken to respond to declining market demand.

Our environmental remediation business assists customers to manage the clean up of the associated redundant plants as refineries complete the move from leaded fuel.

4

Table of Contents

Strategy

Our strategy is to develop new and improved technologies to continue to strengthen and increase our market positions within our Fuel Specialties and Active Chemicals businesses. In addition to the average organic revenue growth of 11% per annum, and average operating income growth of 35% per annum, in these combined businesses since 2005, we also actively continue to assess potential strategic acquisitions, partnerships and other opportunities that would enhance our customer offering. We focus on opportunities that would extend our technology base, geographical coverage or product portfolio. We believe that focusing on the Fuel Specialties and Active Chemicals sectors in which our businesses operate provides the opportunity for positive returns on investment while lowering operating risk by investing in markets where the Company has existing experience, expertise and knowledge.

Working Capital

The nature of our customers’ businesses requires us to hold appropriate amounts of inventory in order to respond quickly to customers’ needs. We therefore require corresponding amounts of working capital for normal operation. However, we do not believe that this is materially different from our competitors.

The decline in our sales of TEL for use in automotive gasoline, and the purchase of large tranches of raw materials in our Fuel Specialties business does create some significant variation in working capital requirements, but these are planned and well managed by the business.

We do not believe that our terms of sale, or terms of purchase, differ markedly from those of our competitors.

Raw Materials and Product Supply

We use a variety of raw materials and chemicals in our manufacturing and blending processes and believe the sources of these are adequate for our current operations. Our major purchases are ethylene, sodium, lead, cetane number improvers, ethyl chloride, dibromoethane and various solvents.

These purchases account for a substantial portion of the Company’s variable manufacturing costs. These materials are, with the exception of ethylene in Germany, readily available from more than one source. Although ethylene is, in theory, available from several sources, it is no longer permissible to transport ethylene by road in Germany. As a result, our source is piped directly from a neighboring site, and is therefore effectively a single source. Ethylene is used as a primary raw material in products representing approximately 5% of the Company’s sales.

We use long-term contracts (generally with fixed costs and escalation terms) to help ensure availability, continuity of supply and manage the risk of cost increases. For some raw materials the risk of cost increases is managed with commodity swaps.

5

Table of Contents

The chemical industry, in general, is experiencing some tightness in the supply of certain commodity materials. We continue to monitor the situation and adjust our procurement strategies as we deem appropriate. The Company forecasts its raw material requirements substantially in advance, and builds long-term relationships and contractual positions with supply partners to safeguard its raw material positions. In addition, the Company operates an extensive risk management program which seeks to source all key raw materials from multiple sources, and to develop other contingency plans.

Intellectual Property

Our intellectual property, including trademarks, patents and licenses, forms a significant part of the Company’s competitive strength, particularly in the Fuel Specialties and Active Chemicals businesses. The Company does not however consider its business as a whole to be dependent on any one trademark, patent or license.

The Company has a portfolio of trademarks and patents, granted and in the application stage, covering products and processes in several jurisdictions. The majority of these patents were developed by the Company and, subject to maintenance obligations including the payment of renewal fees, have at least ten years’ life remaining.

The trademark Innospec and the Innospec device in Classes 1, 2 and 4 of the “International Classification of Goods and Services for the Purposes of the Registration of Marks” are registered in all countries or jurisdictions in which the Company has a significant market presence. The Company also has trademark registrations in all countries or jurisdictions in which it has a significant market presence for the following: Stadis® (a range of conductivity improvers), Ortholeum® (a range of lubricant additives), Valvemaster® (a range of anti valve seat recession additives), Legal Diesel® (a range of diesel fuel additives), Satacen® (a range of iron-based organo-metallic fuel borne catalysts), Enviomet® (a range of biodegradable chelating agents), Natrlquest® (a range of biodegradable chelants for personal care), Iselux™ (a range of innovative, sulfate-free surfactants for personal care) and Finsolv® (a range of benzoate esters for personal care and cosmetic products).

We actively protect our inventions, new technologies, and product developments by filing patent applications and maintaining trade secrets. In addition, we vigorously participate in patent opposition proceedings around the world, where necessary, to secure a technology base free from infringement of our intellectual property.

Customers

Fuel Specialties: Our customers are multinational oil companies and fuel retailers. Traditionally, a large portion of the total market was captive to oil companies that had fuel additives divisions providing supplies directly to their respective refinery customers. Many refineries are increasingly looking to purchase their fuel additive requirements on the open market. This trend is creating new opportunities for independent additive marketers such as ourselves.

6

Table of Contents

Active Chemicals: Customers range from large multinational companies and manufacturers of personal care and household products, to specialty chemical manufacturers operating in niche industries.

Octane Additives: Sales of TEL for use in automotive gasoline are made principally to the retail refinery market which comprises state owned refineries focused in the Middle East and Africa. Selling prices to major customers are usually negotiated under long-term supply agreements with varying prices and terms of payment. Our environmental remediation business then serves these customers to manage the clean up of the associated redundant plants as refineries complete the move away from leaded fuel.

In 2009 the Company had one significant customer in the Fuel Specialties business, Royal Dutch Shell plc and its affiliates (“Shell”), which accounted for $76.1 million (13%) of net group sales. In 2008 and 2007, Shell accounted for $84.6 million (13%) and $66.2 million (11%) of net group sales, respectively. The Company does not have any other such significant customers which alone account for more than 5% of net group sales.

Competition

Fuel Specialties: The Fuel Specialties market is fragmented and characterized by a small number of competitors in each submarket. The competitors in each submarket differ with no one company holding a dominant position. We consider our competitive strengths to be our proven technical development capacity, independence from major oil companies and strong long-term relationships with refinery customers.

Active Chemicals: We operate in three principal markets within Active Chemicals – Personal Care; Household, Industrial & Institutional; and Fragrance Ingredients. The Personal Care and Household, Industrial & Institutional markets are both highly fragmented, and the Company experiences substantial competition from a large number of multinational and specialty chemical suppliers in each geographical region in which we operate. The Fragrance Ingredients market is more concentrated, with our principal competitors being Givaudan SA, Firmenich International SA and International Flavors & Fragrances Inc.. Our competitive position in all three markets is based on supplying a superior, diverse product portfolio which solves particular customer problems or enhances the performance of new or existing products. In a number of Specialty Chemicals markets, we also supply niche product lines, where we enjoy market-leading positions.

Octane Additives: Our Octane Additives business is the world’s only producer of TEL and accordingly is the only supplier of TEL for use in automotive gasoline. The business therefore competes with marketers of products and processes that provide alternative ways of enhancing octane performance in automotive gasoline.

Research, Development, Testing and Technical Support

Research, product/application development and technical support (“R&D”) provide the basis for the growth of our Fuel Specialties and Active Chemicals businesses. Accordingly, the

7

Table of Contents

Company’s R&D activity has been, and will continue to be, focused on the development of new products and formulations. Technical support is provided for all of our business segments.

Our principal R&D facilities are located in Ellesmere Port, United Kingdom and Newark, Delaware. Expenditures to support R&D services to customers were $16.4 million, $14.8 million, and $13.6 million in 2009, 2008, and 2007, respectively.

We consider that our proven technical capability provides us with a significant competitive advantage. In the last three years, the Fuel Specialties business has developed new detergent, cold flow, stabilizers, anti-foulants, lubricity and combustion improver products, in addition to the introduction of many new cost effective fuel additive packages. We are now leveraging this proven technical capability within our Active Chemicals business.

Health, Safety and Environmental Matters

We are subject to environmental laws in all of the countries in which we conduct business. Management believes that the Company is in material compliance with all applicable environmental laws and has made appropriate provision for the continued costs of compliance with environmental laws. Nevertheless, there can be no assurance that changes in existing environmental laws, or the discovery of additional liabilities associated with our current or former operations, will not have a material adverse effect on our business, results of operations or financial and competitive position.

The principal sites giving rise to environmental remediation liabilities are the former Octane Additives manufacturing sites at Paimboeuf in France, Doberitz and Biebesheim in Germany, together with the Ellesmere Port site in the United Kingdom, which is the last ongoing manufacturer of TEL. Remediation work is substantially complete at Paimboeuf, Doberitz and Biebesheim. At Ellesmere Port there is a continuing remediation program related to those manufacturing units that have been closed. We regularly review the future costs of remediation and the current estimate is reflected in Note 12 of the Notes to the Consolidated Financial Statements.

We record environmental liabilities relating to the retirement of assets and environmental clean up when they are probable and costs can be estimated reasonably. This involves anticipating the program of work and the associated future costs, and so involves the exercise of judgment by management.

New laws and regulations may be introduced in the future that could result in additional compliance costs and prevent or inhibit the development, distribution and sale of our products. The European Union (“EU”) has approved additional legislation known as the Registration, Evaluation and Authorization of Chemical Substances Regulations (“REACH”) which requires most of the Company’s products to be registered with the European Chemicals Agency. Under this legislation the Company has to demonstrate the continuing safety of its products. During this registration period the Company will incur expense to test and register its products. The Company estimates that the cost of complying with REACH will be approximately $8 million over the next 3 to 4 years. While the Company expects that its

8

Table of Contents

products will be approved for registration after testing it is possible that certain products may not be registered if the test data proves unsatisfactory. In such an outcome some of the Company’s products may be restricted or prohibited in the EU.

Employees

The Company has 790 employees as at December 31, 2009.

Available Information

We file with the Securities and Exchange Commission (“SEC”) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, proxy statements and other documents. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet website at www.sec.gov that contains reports, proxy and information statements and other information that registrants, including the Company, file electronically with the SEC.

Our corporate website is www.innospecinc.com. We make available, free of charge, on or through this website our annual, quarterly and current reports, and any amendments to those reports, as soon as reasonably practicable after electronically filing such material with, or furnishing it to, the SEC. In addition, Innospec’s Corporate Governance Guidelines, Code of Ethics and Director Independence standards, and the written charters for the committees of Innospec’s Board of Directors are available on this website under “Investor Relations – Corporate Governance” and in print upon request by writing to: Corporate Secretary, Innospec Inc., Innospec Manufacturing Park, Oil Sites Road, Ellesmere Port, Cheshire, United Kingdom, CH65 4EY.

None of the above available information forms part of this filing on Form 10-K, unless specifically incorporated by reference elsewhere in this Form 10-K.

| Item 1A | Risk Factors |

Our business is subject to many factors that could materially adversely affect our future performance and cause our actual results to differ materially from those experienced or implied by forward-looking statements made in this Annual Report on Form 10-K. Investing in our securities involves risks and accordingly investors should carefully evaluate these risks including the factors discussed below before deciding to invest in our securities. Except as otherwise indicated, these factors may or may not occur and we cannot predict the likelihood of any such factor occurring. Other risk factors may exist that we do not consider significant based on information that is currently available to us. In addition, new risks may emerge at any time, and we cannot predict those risks or estimate the extent to which they may affect our future performance.

9

Table of Contents

We may have to pay substantial fines and penalties if we are fined by the U.S. or United Kingdom governments in connection with their investigations regarding our activities related to the United Nations Oil for Food Program (“OFFP”) and U.S. Foreign Corrupt Practices Act (“FCPA”) matters.

As discussed in more detail in Item 3 of Part I (“Legal Proceedings”), the Company is currently the subject of investigations by the U.S. and United Kingdom government authorities in connection with potential violations under the OFFP, the FCPA and other laws.

Because of the uncertainties associated with the ultimate outcome of these investigations, and the costs to the Company of responding and participating in them, no assurance can be given that the ultimate costs incurred will correspond to the amounts accrued. In addition, sanctions that may be imposed may have a material adverse impact on the Company’s results of operations, financial position and cash flows.

We may be required to make additional cash contributions to the defined benefit pension plan that we operate in the United Kingdom and recognize greater pension charges.

The Company operates a contributory defined benefit pension plan (the “Plan”) in the United Kingdom. The Plan is closed to new entrants without trustee discretion, but has a large number of deferred and current pensioners. A full triennial actuarial valuation of the Plan was performed as at December 31, 2008 and an update performed as at December 31, 2009, the results of which are reflected in these consolidated financial statements. At December 31, 2009 the underlying plan asset value and Projected Benefit Obligation (“PBO”) were $671.8 million and $796.0 million, respectively, resulting in a deficit of $124.2 million.

Movements in the underlying plan asset value and PBO are dependent on actual return on investments and pay awards as well as our assumptions in respect of the discount rate, annual member mortality rates, future return on assets, future pay escalation, future pension increases and future inflation. A change in any one of these assumptions could impact the plan asset value, PBO and pension cost recognized in the income statement. Such changes could adversely impact our results of operations and financial position.

The Company has announced closure of the Plan to future service accrual with effect from March 31, 2010 and accordingly we anticipate a curtailment charge of approximately $10 million will be recognized in 2010. The Company is in negotiations with the trustees to fund the Plan deficit over a number of years, but currently expects its annual cash contribution for 2010 to increase to approximately $20 million.

In addition, should future investment returns prove insufficient to meet future obligations, or should future obligations increase due to actuarial factors or changes in pension legislation, then the Company may be required to make additional cash contributions. This could adversely impact our results of operations, financial position and cash flows.

10

Table of Contents

We may have additional tax liabilities.

We are subject to income taxes and state taxes in the U.S., as well as numerous foreign jurisdictions. Significant judgment is required in determining our worldwide provision for income taxes. In the ordinary course of our business, there are many transactions and calculations where the ultimate tax determination is uncertain. We are currently under tax audit by the United Kingdom tax authority. Although we believe our tax estimates are reasonable, the final determination of tax audits and any related litigation could be materially different than that which is reflected in our consolidated financial statements. Should any tax authority take issue with our estimates, this could adversely impact our results of operations, financial position and cash flows.

Our reliance on a small number of significant customers may have a material adverse impact on our results of operations.

Our principal customers are major multinational and state owned oil companies, and large multinational manufacturers of personal care and household products. These industries are characterized by concentration of a few large participants. The loss of a significant customer, a material reduction in purchases by a significant customer, or non-renewal of a significant customer contract, could adversely impact our results of operations, financial position and cash flows.

Our success depends on our management team and other key personnel, the loss of any of whom could disrupt our business operations.

Our future success will depend in substantial part on the continued services of our senior management. The loss of the services of one or more of our key personnel could impede implementation of our business plan and result in reduced profitability. Our future success will also depend on the continued ability to attract, retain and motivate highly-qualified technical sales and support staff. We cannot guarantee that we will be able to retain our key personnel or that we will be able to attract, assimilate or retain qualified personnel in the future. If we are unsuccessful in our efforts in this regard this could adversely impact our results of operations, financial position and cash flows.

Strikes or other forms of work stoppage or slowdown could disrupt our business and lead to increased costs.

Adverse labor relations or contract negotiations that do not result in an agreement could result in strikes or slowdowns. These disruptions may decrease our production and sales or impose additional costs to resolve disputes and adversely impact our results of operations, financial position and cash flows.

Our reliance on a small number of significant stockholders may have a material adverse impact on our stock price.

Almost fifty percent of the Company’s common stock is held by three stockholders. A decision by any of these stockholders to sell all or a significant part of its holding in the

11

Table of Contents

Company, or a sudden or unexpected disposition of Company stock, could result in a significant decline in the Company’s stock price which could in turn adversely impact our ability to access equity markets which in turn could adversely impact our results of operations, financial position and cash flows.

Approximately twenty percent of the Company’s common stock has been held or controlled by Tontine Capital Partners, L.P., Tontine 25 Overseas Master Fund, L.P., Tontine Capital Management L.L.C., Tontine Capital Overseas Master Fund, L.P., Tontine Capital Overseas GP, L.L.C. and Jeffrey L. Gendell (collectively “Gendell et al”). On both November 10, 2008, and October 22, 2009, Gendell et al jointly filed a Schedule 13D with the SEC in which they reported that they are exploring alternatives for the disposition of their equity interests in the Company’s common stock which aggregated to 4,828,345 shares at both dates. On February 1, 2010, Gendell et al jointly filed a further Schedule 13D with the SEC in which they reported that they had reallocated their equity interests in the Company’s common stock amongst themselves, Tontine Capital Overseas Master Fund II, L.P. and Tontine Asset Associates, L.L.C.. Following this reallocation their equity interests in the Company’s common stock remained 4,828,345 shares.

Competition and market conditions may adversely affect our operating results.

Certain markets in which the Company’s businesses operate are subject to significant competition. The Company competes on the basis of a number of factors including, but not limited to, product quality and properties, specialized product lives, customer relationships and service, and regulatory and toxicological expertise. For some of our products our competitors are larger than us and may have greater access to financial, technological and other resources. As a result, these competitors may be better able to adapt to changes in conditions within the industries in which the Company operates, fluctuations in the costs of raw materials or changes in global economic conditions. Competitors may also be able to introduce new products with enhanced features that may cause a decline in the demand and sales of our products. Consolidation of customers or competitors, or economic problems of customers, in the market areas in which the Company operates may cause a loss of market share for the Company’s products, place downward pressure on prices, result in payment delays or non-payment and declining plant utilization rates. Any of these risks could adversely impact our results of operations, financial position and cash flows.

We could be adversely affected by technological changes in our industry.

Our ability to maintain or enhance our technological capabilities, develop and market products and applications that meet changing customer requirements, and successfully anticipate or respond to technological changes in a cost effective and timely manner will likely impact our future business success. The Company competes on the basis of a number of factors including, but not limited to, product quality and properties. For some products our competitors are larger than us and may have greater access to financial, technological and other resources. Competitors may be able to introduce new products with enhanced features that may cause a decline in the demand and sales of the Company’s products, and accordingly could adversely impact our results of operations, financial position and cash flows.

12

Table of Contents

Continuing adverse global economic conditions could materially affect our current and future businesses.

The global economy and capital and credit markets have recently experienced severe disruptions. Ongoing concerns about the systemic impact of potential long-term and wide-spread national recessions, volatile energy costs, geopolitical issues, the availability, cost and terms of credit, declining consumer and business confidence, substantially increased unemployment and the crisis in the global housing and mortgage markets have contributed to increased market volatility and diminished expectations for both established and emerging economies, including those in which we operate. In the second half of 2008, added concerns fuelled by government interventions in financial systems led to increased market uncertainty and instability in both U.S. and international capital and credit markets. These conditions have contributed to substantial economic uncertainty.

Concern about the stability of the markets generally and the strength of counterparties specifically has led many lenders and institutional investors to reduce, and in many cases cease to provide, credit to businesses and consumers. These factors have led to a substantial and continuing decrease in spending by businesses and consumers, and a corresponding decrease in global infrastructure spending. The availability, cost and terms of credit have been, and may continue to be, adversely affected by the foregoing factors and these circumstances have produced, and may in the future result in, illiquid markets and wider credit spreads. Continued turbulence in the U.S. and international markets and economies, the generally restricted environment for credit, and prolonged declines in business and consumer spending could adversely impact our results of operations, financial position and cash flows.

We are exposed to fluctuations in foreign exchange rates, which may adversely affect our results of operations.

The Company generates a portion of its revenues and incurs some operating costs in currencies other than the U.S. dollar. In addition, the financial position and results of operations of some of our foreign subsidiaries are reported in the relevant local currency and then translated to U.S. dollars at the applicable currency exchange rate, for inclusion in our consolidated financial statements. Fluctuations in exchange rates between these foreign currencies and the U.S. dollar will affect the recorded levels of our assets and liabilities, to the extent such figures reflect the inclusion of foreign assets and liabilities that are translated into U.S. dollars for presentation in our financial statements, as well as our results of operations.

The primary foreign currencies in which we have exchange rate fluctuation exposure are the European Union euro and British pound sterling. We cannot accurately predict the nature or extent of future exchange rate variability amongst these currencies or relative to the U.S. dollar. While the Company takes steps to manage currency exposure, including entering into hedging transactions, it cannot eliminate all exposure to future exchange rate variability. Exchange rates between these currencies and the U.S. dollar have fluctuated significantly in recent years and may continue to do so in the future, which could adversely impact our results of operations, financial position and cash flows.

13

Table of Contents

A disruption in the supply of raw materials or transportation services would have a material adverse impact on our results of operations.

The chemical industry and transportation industry are in a situation where the supply and demand for both transportation services and raw materials are currently broadly in balance. When we identify a situation where an imbalance may occur or is occurring we may build certain product inventories of strategic importance. Any significant disruption in the supply of either of these could affect our ability to obtain raw materials or transportation services at accessible costs, if at all, which could adversely impact our results of operations, financial position and cash flows.

Sharp and unexpected fluctuations in the cost of our raw materials and energy could adversely affect our profit margins.

We use a variety of raw materials, chemicals and energy in our manufacturing and blending processes. Many of the raw materials that we use are derived from petrochemical-based feedstocks which can be subject to periods of rapid and significant cost instability. These fluctuations in cost can be caused by political instability in oil producing nations and elsewhere, or other factors influencing global supply and demand of these materials, over which we have little or no control. We use long-term contracts (generally with fixed costs and escalation terms) to help ensure availability, continuity of supply and manage the risk of cost increases and have entered hedging arrangements for certain raw materials, but do not typically enter into hedging arrangements for all raw materials, chemicals or energy costs. Should the costs of raw materials, chemicals or energy increase, and should the Company’s businesses not be able to pass on these cost increases to our customers, then operating margins and cash flows from operating activities would be adversely impacted. Should raw material costs increase significantly, then the Company’s need for working capital could also increase. Any of these risks could adversely impact our results of operations, financial position and cash flows.

We face risks related to our foreign operations that may adversely affect our business.

We serve global markets and accordingly operate in certain countries which do not have stable economies or governments. Specifically, we trade in countries experiencing political and economic instability in the Middle East and Asia Pacific regions. Our international operations are subject to international business risks including, but not limited to, unsettled political conditions, risk of expropriation, import and export restrictions, exchange controls, national and regional labor strikes, high or unexpected taxes, government royalties and restrictions on repatriation of earnings or proceeds from liquidated assets of foreign subsidiaries. The occurrence or imposition of any, or a combination, of these factors could adversely impact our results of operations, financial position and cash flows.

Failure to protect our intellectual property rights could adversely affect our future performance and cash flows.

Our intellectual property, including trademarks, patents and licenses, forms a significant part of the Company’s competitive strengths. We therefore depend on our ability to develop and

14

Table of Contents

protect our intellectual property rights to distinguish our products from those of our competitors. Failure to develop or protect our intellectual property rights may result in the loss of valuable technologies, or our having to pay other companies for infringing on their intellectual property rights. Measures taken by us to protect our intellectual property may be challenged, invalidated, circumvented or rendered unenforceable. We may also face patent infringement claims from our competitors which may result in substantial litigation costs, claims for damages or a tarnishing of our reputation even if we are successful in defending against these claims, which may cause our customers to switch to our competitors. The occurrence of any, or a combination, of these events could adversely impact our results of operations, financial position and cash flows.

We are subject to extensive government regulation.

We are subject to regulation by local, state, federal and foreign governmental authorities. In some circumstances these authorities must approve our products, manufacturing processes and facilities before we may sell certain products. Many of the Company’s products are required to be registered with the U.S. Environmental Protection Agency (“EPA”) and with comparable governmental agencies in the European Union (“EU”) and elsewhere. We are also subject to ongoing reviews of our products, manufacturing processes and facilities by governmental authorities including the requirement to produce product data.

In order to obtain regulatory approval of certain new products we must, amongst other things, demonstrate to the relevant authorities that the product is safe and effective for its intended uses, and that we are capable of manufacturing the product in accordance with applicable regulations. This approval process can be costly, time consuming, and subject to unanticipated and significant delays. Accordingly, there can be no assurance that approvals will be granted on a timely basis, or at all. Any delay in obtaining, or any failure to obtain or maintain, these approvals would adversely affect our ability to introduce new products and to generate income from those products. New laws and regulations may be introduced in the future that could result in additional compliance costs and prevent or inhibit the development, distribution and sale of our products. While the Company expects that its products will obtain regulatory approval it is possible that certain products may not. In such an outcome some of the Company’s products may be restricted or prohibited in the jurisdiction where approval cannot be obtained, which could adversely impact our results of operations, financial position and cash flows.

Legal proceedings and other claims could impose substantial costs on us.

In addition to matters described in more detail in Item 3 of Part I (“Legal Proceedings”), we are occasionally involved in legal proceedings that result from, and are incidental to, the conduct of our business, including employee and product liability claims. We have insurance coverage to mitigate anticipated potential damages in a wide variety of such proceedings, however if our insurance did not cover such claims, this could adversely impact our results of operations, financial position and cash flows.

15

Table of Contents

Unexpected environmental matters could have a substantial adverse impact on our results of operations.

The Company operates a number of manufacturing sites. As such, it is subject to extensive federal, state, local and foreign environmental, health and safety laws and regulations concerning emissions to the air, discharges to land and water and the generation, handling, treatment and disposal of hazardous waste and other materials on these sites. The Company is also required to obtain various environmental permits and licenses many of which require periodic notification and renewal.

The Company’s historic operations, and the historic operations of companies that have previously operated on sites that the Company has acquired, pose the risk of environmental contamination on these sites should unexpected environmental contamination be found. Discovery of unexpected contamination may result in fines or criminal sanctions being imposed against the Company or may require the Company to pay material remediation or fines to address the effects and to remediate this contamination.

The Company further anticipates that certain production facilities may cease production over the medium to long-term. On closure of some of our production operations in the future, we expect to be subject to environmental laws that will require these facilities to be safely decommissioned and a degree of environmental remediation to be undertaken. The degree of environmental remediation required will depend on the plans for the future use of the operating sites that are affected and the environmental legislation in force at the time. The Company has currently made a decommissioning and remediation provision based on the Company’s current known obligations, the anticipated plans for those sites and existing environmental legislation. Should there be unexpected or unknown contamination at these facilities, or the Company’s future plans for the sites or environmental legislation change, then current provisions may prove inadequate and this could adversely impact our results of operations, financial position and cash flows.

The terms of our finance facility may restrict our ability to incur additional indebtedness or to otherwise expand our business.

The Company’s finance facility contains restrictive clauses which may constrain our activities and limit our operational and financial flexibility. The facility obliges the lenders to comply with a request for utilization of finance unless there is an event of default outstanding. Events of default are defined in the finance facility and include a material adverse change to our business, properties, assets, financial condition or results of operations. The facility also contains a number of restrictions that limit our ability, amongst other things, and subject to certain limited exceptions, to incur additional indebtedness, pledge our assets as security, guarantee obligations of third parties, make investments, undergo a merger or consolidation, dispose of assets, or materially change our line of business.

In addition, the finance facility requires the Company to meet certain financial ratios defined therein including net debt to EBITDA and net interest expense to EBITDA. The ability to meet these financial covenants depends upon the future successful operating performance of

16

Table of Contents

the businesses. If the Company fails to meet target covenants then it would be in technical default under the finance facility and the maturity of the Company’s outstanding debt could be accelerated unless we were able to obtain waivers from our lenders. If the Company were found to be in default under the finance facility, this could adversely impact our results of operations, financial position and cash flows.

We may not be able to consummate, finance or successfully integrate future acquisitions, partnerships or other opportunities into our business, which could hinder our strategy or result in unanticipated expenses and losses.

It is part of our stated strategy that we intend to pursue strategic acquisitions, partnerships and other opportunities to complement and expand our existing businesses. Our ability to implement this component of our strategy will be limited by our ability to identify appropriate acquisitions, partnerships or other opportunities and limited by financial resources, including our available cash and borrowing capacity and the financial markets. Moreover, as further described above, the availability of liquidity and credit to fund or support the continuation and expansion of business operations worldwide has reduced. As a result, many lenders and institutional investors have reduced and, in some cases, ceased to provide funding to borrowers. Continued disruption of the credit markets has affected and could adversely impact our ability to complete strategic acquisitions, partnerships and other opportunities which in turn could adversely impact our results of operations, financial position and cash flows.

The success of our strategic acquisitions, partnerships and other opportunities will depend on our ability to integrate assets and personnel acquired in these transactions, apply our internal controls processes to these acquired businesses, and cooperate with our strategic partners. The expense incurred in consummating acquisitions, partnerships or other opportunities, the time it takes to integrate an acquisition, or our failure to integrate businesses successfully, could result in unanticipated expenses and losses. The process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or expansion of existing operations. Furthermore, we may not realize the degree or timing of benefits we anticipate when we first enter a transaction. Any of these risks could adversely impact our results of operations, financial position and cash flows.

Our business is subject to the risk of production or transportation disruptions, the occurrence of any of which would adversely affect our results of operations.

We are subject to hazards common to chemical manufacturing, blending, storage, handling and transportation including fires, explosions, mechanical failure, transportation interruptions, remediation, chemical spills and the release or discharge of toxic or hazardous substances. These hazards could result in loss of life, property damage, environmental contamination and temporary or permanent production cessation. Any, or a combination, of these factors could adversely impact our results of operations, financial position and cash flows.

17

Table of Contents

Domestic or international natural disasters or terrorist attacks may disrupt our operations, decrease the demand for our products or otherwise have an adverse impact on our business.

Chemical related assets, and U.S. corporations such as ourselves, may be at greater risk of future terrorist attacks than other possible targets in the U.S., United Kingdom and throughout the world. Extraordinary events such as natural disasters may negatively affect local economies, including those of our customers or suppliers. The occurrence of such events cannot be predicted though they can be expected to continue to adversely impact the economy in general and our specific markets. The resulting damage from such an event could include loss of life, property damage or site closure. Any, or a combination, of these factors could adversely impact our results of operations, financial position and cash flows.

The inability of counterparties to meet their contractual obligations could have a substantial adverse impact on our results of operations.

The Company sells a range of specialty chemicals to customers around the world. Credit limits, ongoing credit evaluation and account monitoring procedures are used to minimize bad debt risk. Collateral is not generally required. The Company uses derivatives, including interest rate swaps, commodity swaps and foreign currency forward exchange contracts, in the normal course of business to manage market risks. The Company enters into derivative instruments with a diversified group of major financial institutions in order to monitor the exposure to non-performance of such instruments. The Company has in place a financing facility with a syndicate of banks.

The Company remains subject to market and credit risks including the ability of counterparties to meet their contractual obligations and the potential non-performance of counterparties to deliver contracted commodities or services at the contracted price. Due to the disruptions in the credit and global financial markets the ability of counterparties to meet their contractual obligations may be reduced and this could have an adverse impact on results of operations, financial position and cash flows.

Our Octane Additives business could decline faster than expected.

Worldwide use of TEL has declined since 1973, in particular following the enactment of the U.S. Clean Air Act of 1970 and similar legislation in other countries. The trend of countries exiting the leaded gasoline market has resulted in an average rate of decline in volume terms in demand for TEL in the last five years of approximately 35% per annum. Net sales and gross profit of our Octane Additives business accounted for approximately 8% and 8%, respectively, of our consolidated sales and gross profit in 2009. The remaining sales of the Octane Additives business are now concentrated in a relatively small number of customers and therefore may decline with unpredictable volatility and severity. Should one or more of these customers choose for economic, environmental, political or other reasons to cease using TEL as an octane enhancer earlier than has been anticipated, then the Company’s future results of operation, financial position and cash flows could be adversely impacted. There could also be an accelerated impairment of Octane Additives business goodwill as the forecast discounted cash flows from that business would be reduced. The Company anticipates that eventually all

18

Table of Contents

countries in the world will stop the use of TEL in automotive gasoline. The Company expects that it will cease all sales of TEL for use in automotive gasoline in 2012.

| Item 1B | Unresolved Staff Comments |

None.

| Item 2 | Properties |

A summary of the Company’s principal properties is shown in the following table. Each of these properties is owned by the Company except where otherwise noted:

| Location |

Business and Business Segment | Operations | ||

| Littleton, Colorado (1) | Innospec Fuel Specialties LLC – Fuel Specialties and Active Chemicals | American Headquarters Business Teams Sales/Administration | ||

| Ellesmere Port, United Kingdom | Innospec Inc. and Innospec Limited – Fuel Specialties, Active Chemicals and Octane Additives | European Headquarters Business Teams Sales/Manufacturing/Administration Research & Development Fuel Technology Center | ||

| Singapore, Singapore (1) | Innospec Asia Pacific Pte Ltd – Fuel Specialties and Active Chemicals | Asia-Pacific Headquarters Business Teams Sales/Administration | ||

| Widnes, United Kingdom | Innospec Widnes Limited – Active Chemicals | Manufacturing/Administration | ||

| Herne, Germany | Innospec Deutschland GmbH – Fuel Specialties | Sales/Manufacturing/Administration | ||

| Leuna, Germany | Innospec Leuna GmbH – Fuel Specialties and Active Chemicals | Sales/Manufacturing/Administration | ||

| Vernon, France | Innospec France SA – Fuel Specialties | Sales/Manufacturing/Administration | ||

| Zug, Switzerland (1) | Alcor Chemie Vertriebs GmbH – Octane Additives | Sales/Administration | ||

| Newark, Delaware (1) | Innospec Fuel Specialties LLC – Fuel Specialties | Sales/Administration Research & Development | ||

| High Point, North Carolina | Innospec Active Chemicals LLC – Active Chemicals | Manufacturing/Administration | ||

| Spencer, North Carolina | Innospec Active Chemicals LLC – Active Chemicals | Manufacturing/Administration | ||

| (1) | Leased property |

The corporate headquarters of Innospec Inc. is located at 220 Continental Drive, Newark, DE 19713. The principal executive offices of Innospec Inc. are located at Innospec Manufacturing Park, Oil Sites Road, Ellesmere Port, Cheshire, United Kingdom, CH65 4EY.

19

Table of Contents

Production Capacity

We believe that our plants and supply agreements are sufficient to meet expected future sales levels. Operating rates of the plants are generally flexible and varied with product mix and normal sales swings. We believe that all of our facilities are well maintained and in good operating condition though there remains an ongoing need for capital investment.

| Item 3 | Legal Proceedings |

United Nations Oil for Food Program (“OFFP”) and U.S. Foreign Corrupt Practices Act (“FCPA”) investigations

On February 7, 2006, the Securities and Exchange Commission (“SEC”) notified the Company that it had commenced an investigation to determine whether any violations of law had occurred in connection with certain transactions conducted by or involving the Company, including those conducted by its wholly owned indirect Swiss subsidiary, Alcor Chemie Vertriebs GmbH (“Alcor”), under the OFFP between June 1, 1999 and December 31, 2003. As part of its investigation, the SEC issued a subpoena requiring the production of certain documents, including documents relating to these transactions, by the Company and Alcor. Upon receipt of the SEC’s notification and initial subpoena, the Company undertook a review of its participation in the OFFP.

On October 10, 2007 and November 1, 2007, the SEC served two additional subpoenas on the Company. These additional subpoenas required the production of documents relating both to the OFFP, and also to transactions conducted by the Company or its subsidiaries with state owned or state controlled entities between June 1, 1999 and the date of such subpoenas, concerning the use of foreign agents and the possibility of extra-contractual payments to secure business with foreign governmental entities in the context of the FCPA and other laws. In a coordinated investigation, the Company was also notified by the U.S. Department of Justice (“DOJ”) regarding the possibility of violations by the Company or its subsidiaries arising under other laws stemming from matters covered by the SEC investigation as well as certain preliminary inquiries regarding compliance with anti-trust laws applicable to the U.S. and international tetra ethyl lead markets. The subjects into which the SEC and DOJ have inquired include areas that concern certain former and current executives of the Company, including our former CEO, who resigned on March 20, 2009. The Company, and its officers and directors are cooperating with the SEC and DOJ investigations.

On February 19, 2008, the Board of Directors of the Company formed a committee comprised of the chairmen of the Board, the Audit Committee and the Nominating and Governance Committee, all of whom were independent directors. (The chairman of the Nominating and Governance Committee retired as a director of the Company effective May 6, 2008, but his services were retained in an independent capacity as a member of the committee until October 1, 2009 when he resigned. Mr. Haubold did not resign as a result of any dispute or disagreement with the Company or the committee). External counsel to the Company, reporting to the committee has, on behalf of the committee, conducted and will continue to

20

Table of Contents

conduct an investigation into the circumstances giving rise to the SEC and DOJ investigations. External counsel reports directly to the committee and assists in connection with communications and interactions with the SEC and DOJ.

On March 5, 2008, a letter was received by the Company from the DOJ in which a request for a wider and more detailed range of documents was made. A further letter was received from the DOJ on June 13, 2009 which contained requests for information made by the U.S. Office of Foreign Assets Control (“OFAC”). In addition to the voluntary disclosure made in relation to the Bycosin disposal OFAC is inquiring into business the Company may have conducted in countries in respect of which there are U.S. laws and regulations that restrict trade.

On July 31, 2009, the DOJ issued a press release in which it disclosed the arrest of an individual and the unsealing of an August 7, 2008 indictment in the U.S. District Court for the District of Columbia against the individual for certain FCPA violations relating to his alleged participation in an eight-year conspiracy to defraud the OFFP and to bribe Iraqi government officials on behalf of a publicly traded U.S. chemical company in connection with the sale of a chemical additive used in the refining of leaded fuel. This individual is the Company’s former agent for Iraq and certain other markets and the Company understands the indictment to relate to the matters that are the subject of the OFFP and FCPA investigations of the Company.

Separately, on May 21, 2008, the United Kingdom’s Serious Fraud Office (“SFO”) notified Innospec Limited, a wholly owned subsidiary of the Company, that it had commenced an investigation into certain contracts involving British companies under the OFFP. As part of this investigation, the SFO has asked the Company to produce documents in respect of the Company’s participation in the OFFP between January 1, 1996 and December 31, 2003. Following receipt of the SFO’s notice the Company has instructed external legal counsel to advise and assist in relation to the investigation and the Company and its directors and officers intend to cooperate with the SFO. On October 16, 2008, the Company was further notified that the scope of the SFO’s investigation would extend to matters relating to potential bribery involving overseas commercial agents that are already in the large part the subject of the ongoing DOJ and SEC investigations. This investigation by the SFO similarly includes areas that concern certain former and current executives of the Company.

The Company and its officers and directors intend to continue to cooperate with the SEC, DOJ and SFO.

The outcome of these investigations remains uncertain to the Company. Discussions with the SEC, DOJ and SFO are ongoing in an effort to resolve these investigations, including discussions with a view to settlement. The amount of any final settlement, including the final amount of probable disgorgement, penalties and/or fines that we may be subject to, has yet to be conclusively determined. The amount of any disgorgements, penalties and/or fines that the Company could face depends on a number of eventual factors which have yet to be finally resolved with the relevant government authorities, including findings by relevant authorities regarding the amount, nature and scope of any improper payments, the amount of any pecuniary gain involved, the Company’s ability to pay, and the level of cooperation provided

21

Table of Contents

to government authorities during the investigations. As previously disclosed, for accounting purposes, based on a potential settlement range of $18.3 million to $63.4 million in connection with the ongoing discussions with government authorities, we recorded in the third quarter of 2009 an $18.3 million accrual for potential global settlement of these investigations as required under U.S. GAAP. In the fourth quarter of 2009, we similarly recorded an additional accrual of $21.9 million for anticipated global settlement of this matter, bringing total accruals to $40.2 million, based on our assessment for accounting purposes of the best estimate within an anticipated settlement range of $28.8 million to $40.2 million. As these accruals are estimates, there is no assurance that final settlement amount will correspond to the accrued amounts.

Because of the uncertainties associated with the ultimate outcome of these investigations and the costs to the Company of responding and participating in them, no assurance can be given that the ultimate costs incurred and sanctions that may be imposed will not have a material adverse impact on the Company’s results of operations, financial position and cash flows.

As part of the Company’s commitment to cooperate and comply with the OFFP and FCPA investigations the Company has accrued and spent the following amounts in respect of estimated probable future legal and other professional expenses:

| (in millions) |

Accrued |

Spent |

Provision remaining at year end | |||||||

| Year ended December 31, 2006 |

$ | 1.2 | $ | (0.8 | ) | $ | 0.4 | |||

| Year ended December 31, 2007 |

4.6 | (1.3 | ) | 3.7 | ||||||

| Year ended December 31, 2008 |

15.5 | (15.8 | ) | 3.4 | ||||||

| Year ended December 31, 2009 |

12.9 | (13.6 | ) | $ | 2.7 | |||||

| $ | 34.2 | $ | (31.5 | ) | ||||||

These accruals have been made on the basis of the Company’s current best estimate, working in consultation with the committee of the Board of Directors, external legal counsel to the Company and its other professional advisors. Should any underlying assumptions prove incorrect or should any of the DOJ, SEC and/or the SFO alter the scope of the investigations, then the actual costs incurred by the Company could differ materially from current estimates. The Company continues to keep the amount of such accrual provisions under review.

Voluntary disclosure of possible violations of the Cuban Assets Control Regulations to the Office of Foreign Assets Control and other matters

Given the international scope of its operations, the Company is subject to laws of many different jurisdictions, including laws relating to the imposition of restrictions on trade and investment with various entities, persons and countries, some of which laws are conflicting. In 2004 the Company reviewed, as it does periodically, aspects of its operations in respect of such restrictions, and determined to dispose of certain non-core, non-U.S. subsidiaries of Bycosin AB. Bycosin’s non-U.S. subsidiaries had been engaged in transactions and activities

22

Table of Contents

involving Cuban persons and entities before the acquisition of the Bycosin Group by the Company in June 2001, and such subsidiaries were continuing to engage in such transactions and activities at the time of the disposal of the non-core Fuel Specialties business and related assets in November 2004. On November 15, 2004, Bycosin AB, a wholly-owned subsidiary of the Company organized under the laws of Sweden (now known as Innospec Sweden AB, the “Seller”), entered into a Business and Asset Purchase Agreement (the “Agreement”) with Pesdo Swedcap Holdings AB (the “Purchaser”), Håkan Byström and others as the Purchaser’s guarantors, and Octel Petroleum Specialties Limited (now known as Innospec Fuel Specialties Limited) as the Seller’s guarantor, and completed the all-cash transaction contemplated thereby (together with related transactions, the “Transaction”). The Agreement provided for, amongst other things: (i) the disposal of certain non-core Fuel Specialties business and related manufacturing and other assets of the Seller; and (ii) the supply and distribution of certain power products to certain geographic regions. The net consideration paid by the Purchaser was approximately $2.9 million.

Following completion of the Transaction, the Company made a voluntary disclosure to the U.S. Office of Foreign Assets Control (“OFAC”) regarding transactions and activities engaged in by certain non-U.S. subsidiaries of the Company. Disclosures, amongst other items, included that the aggregate monetary value of the transactions involving Cuban persons and entities conducted by the Company’s non-U.S. subsidiaries since January 1999 was approximately $26.6 million.

At this time, however, management believes that it would be speculative and potentially misleading for the Company to predict the specific nature or amount of penalties that OFAC might eventually assess against it. While penalties could be assessed on different bases, if OFAC assessed penalties against the Company on a “performance of contracts basis”, the applicable regulations provide for penalties, in the case of civil violations of the Cuban Assets Control Regulations (31 CFR. Part 515) (“CACR”), of the lesser of $65,000 per violation or the value of the contract. Since January 1999, non-U.S. subsidiaries of the Company have entered into 43 contracts with Cuban entities, each of which could be considered a separate violation of the CACR by OFAC. OFAC may take the position that the CACR should be interpreted or applied in a different manner, potentially even to permit the assessment of penalties equal to or greater than the value of the business conducted with Cuban persons or entities.

The Company has considered the range of possible outcomes and potential penalties payable. In accordance with the Company’s accounting policies, provision has been made for management’s current best estimate of the potential liability, including anticipated legal costs. However, should the underlying assumptions prove incorrect, the actual outcome could differ materially from management’s current expectations. Management is not able to estimate the amount of any additional loss, if any.

In addition to the voluntary disclosure made in relation to the Bycosin disposal, and as referred to in the Company’s disclosure relating to the investigations into its involvement in the OFFP and FCPA matters, OFAC is inquiring into business the Company may have

23

Table of Contents

conducted in countries in respect of which there are U.S. laws and regulations that restrict trade. The Company and its officers and directors intend to continue to cooperate with OFAC.

If the Company or its subsidiaries (current or former) were found not to have complied with the CACR, or other U.S. laws or regulations that restrict trade with certain countries, the Company believes that it could be subject to fines or other civil or criminal penalties which could be material.

Patent Actions

The Company is actively opposing certain third party patents in various regions of the world. The actions are part of the Company’s ongoing management of its intellectual property portfolio. The Company does not believe that any of these actions will have a material effect on the financial condition or results of operations of the Company.

Other Legal Matters

Except as disclosed elsewhere in this Form 10-K we are not involved in any other administrative or judicial proceedings arising under provisions enacted that regulate the discharge of materials into the environment or enacted for the purpose of protecting the environment involving a governmental authority as a party, which involves potential monetary sanctions which the Company reasonably believes will result in monetary sanctions of more than $100,000.

We are involved from time to time in claims and legal proceedings that result from, and are incidental to, the conduct of our business including business and commercial litigation, employee and product liability claims. There are no other material pending legal proceedings to which the Company or any of its subsidiaries is a party, or of which any of their property is subject, other than ordinary, routine litigation incidental to their respective businesses.

Whilst it is not possible to predict with certainty the outcome of any legal proceedings, it is our opinion based on our current knowledge that we will not suffer any material adverse effect on our results of operations, financial position or cash flows as a result of any actual or threatened litigation.

| Item 4 | Submission of Matters to a Vote of Security Holders |

No matter was submitted to a vote of security holders during the quarter ended December 31, 2009.

24

Table of Contents

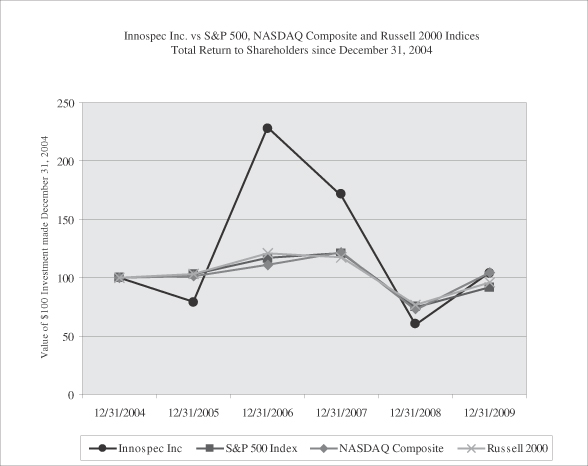

| Item 5 | Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities |

Market Information and Holders

The Company’s common stock is listed on the NASDAQ (symbol – IOSP). As of February 11, 2010 there were approximately 1,200 registered holders of the common stock. The following table shows the closing high and low prices of our common stock for each of the last eight quarters.

| First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter | |||||||||

| 2009 |

||||||||||||

| High |

$ | 6.31 | $ | 11.31 | $ | 15.63 | $ | 15.41 | ||||

| Low |

$ | 2.79 | $ | 3.95 | $ | 10.00 | $ | 8.89 | ||||

| 2008 |

||||||||||||

| High |

$ | 22.60 | $ | 25.29 | $ | 23.49 | $ | 11.05 | ||||

| Low |

$ | 14.10 | $ | 18.89 | $ | 11.60 | $ | 4.54 | ||||

Dividends

In line with its policy of semi-annual consideration of a dividend the Company declared the following cash dividends for the two years ended December 31, 2009.

| Date declared |

Stockholders of record |

Date paid |

Amount per share | |||

| February 22, 2008 |

March 14, 2008 |

April 4, 2008 | 5 cents | |||

| August 14, 2008 |

September 1, 2008 |

October 6, 2008 | 5 cents | |||

| February 23, 2009 |

March 16, 2009 |

April 6, 2009 | 5 cents | |||

On February 6, 2009 we entered into a new three-year finance facility which contains no restrictive covenants with respect to dividends and the Company is allowed to repurchase its own common stock provided that it does not affect compliance with the financial covenants in this facility.

Related Stockholder Matters

On June 12, 2009 the Board of Directors of the Company approved a stockholder rights plan (the “Plan”). In connection with the Plan a dividend was declared of one preferred stock (designated as Series B Junior Participating Preferred Stock) right for each outstanding share of Innospec Inc. common stock (each a “Right”). The Rights attached to all common stock certificates representing shares outstanding on June 26, 2009, the record date. Subject to certain exceptions, the Rights are exercisable only if a person or group acquires 15% or more of Innospec Inc.’s common stock, including through derivatives, or announces a tender or

25

Table of Contents

exchange offer which would result in ownership of 15% or more of the common stock (an “Acquiring Person”). Tontine Capital Partners, L.P. and its affiliates, which already own approximately 20% of the Company’s common stock, will not be treated as an Acquiring Person for the purposes of the Plan unless they purchase additional shares and as a result own 21% or more of the Company’s common stock, or unless another person or entity becomes affiliated or associated with them and together they own 21% or more of the Company’s common stock. Each Right entitles its holder to buy one one-thousandth of a share of Series B Junior Participating Preferred Stock at an exercise price of $55, subject to adjustment. Initially, the Rights are not exercisable and will be transferred with and only with the Company’s common stock. Following the acquisition of 15% or more of Innospec Inc. common stock by a person or group, the holders of the Rights (other than the Acquiring Person or group) will be entitled to purchase shares of common stock at one-half the market price of such shares, and, in the event of a subsequent merger or other acquisition of the Company, to buy shares of common stock of the acquiring entity at one-half of the market price of those shares.

Issuer Purchases of Equity Securities

No purchases of equity securities by the issuer or affiliated purchasers were made during the fourth quarter of 2009.

Repurchases of common stock are held as treasury shares unless reissued under equity compensation plans.

The Company has authorized securities for issuance under equity compensation plans. The information contained in the table entitled “Equity Compensation Plan Information” under the heading “Equity Compensation Plans” in the Proxy Statement is incorporated herein by reference. The current limit for the total amount of shares which can be issued or awarded under the Company’s five share option plans is 1,790,000.

The Company has not, within the last three years, made any sales of unregistered securities.

26