Attached files

| file | filename |

|---|---|

| 8-K - CENTER FINANCIAL CORPORATION 8-K - CENTER FINANCIAL CORP | a6184508.htm |

Exhibit 99.1

West Cost Bank CEO Forum San Francisco February 18, 2010

During the course of this presentation, the Company may make or present forward-looking statements. These forward-looking statements may be subject to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements, including statements related to the Company’s growth, market position and future performance are predictions based on factors as currently known to the Company. Actual events or results may differ materially. You are referred to the documents the Company files from time to time with the U.S. Securities and Exchange Commission, which review the risks and uncertainties that could cause actual results to differ materially from those contained in the Company’s projections or forward-looking statements. The historical results achieved by the company are not necessarily indicative of its future prospects. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

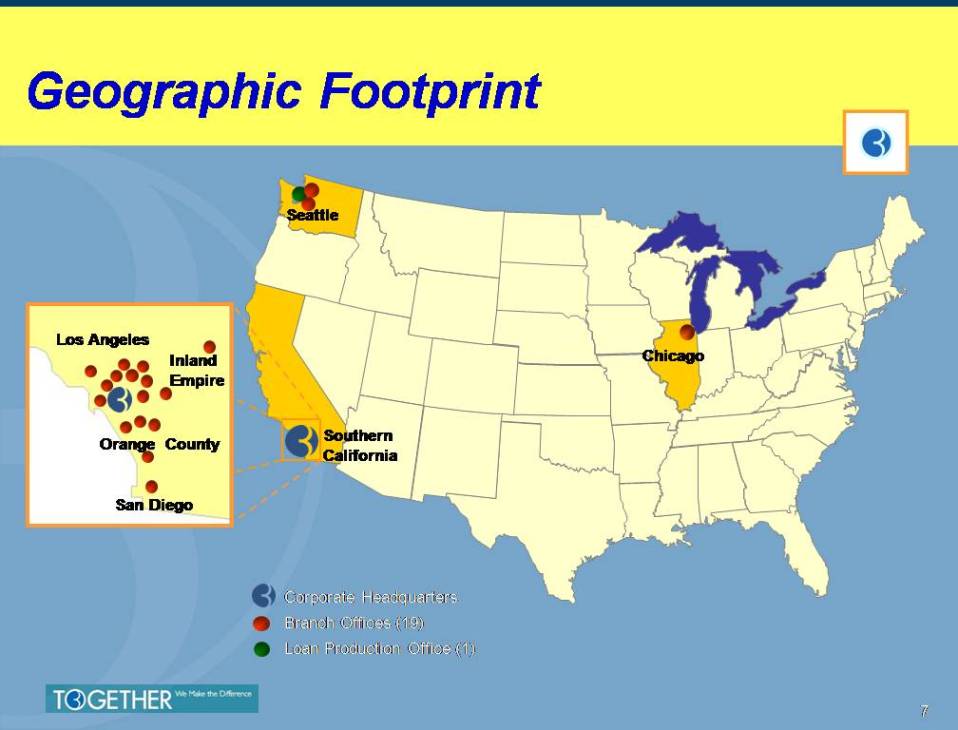

Center Bank – Corporate Profile 24 years of service as strong community business bankInternational trade finance expertiseNationally recognized SBA lender – 2006 Excellence in Lending Award based on highest asset qualityLeading provider of small business-oriented products & services – most comprehensive offering of cash management services in niche marketExceptional relationships in U.S. and Korea through Board and Management – insider holdings approximately 16.9% following recent capital raises20 offices across the nation19 full-service branches in Southern California, Seattle, ChicagoOne loan production office (LPO) in SeattleTotal assets of $2.19 billion (at 12/31/09)Headquartered in Los Angeles Largest Korean concentration outside Republic of Korea

Seasoned, Conservative Leadership Jae Whan (J.W.) Yoo, President & CEOSuccessfully resolved long-standing KEIC litigationFormer HAFC CEO who executed the acquisition of PUBBLonny Robinson, EVP & CFOIndustry veteran as both executive management and consultant to community banksJason Kim, SVP & CCORecognized for significant growth of SBA portfolio with exceptional credit quality; led Center to being named SBA’s 2006 “Lender of the Year”Lisa Kim Pai, EVP, CRO, GC & Corp SecretaryExtensive experience as GC for Korean-American community banks

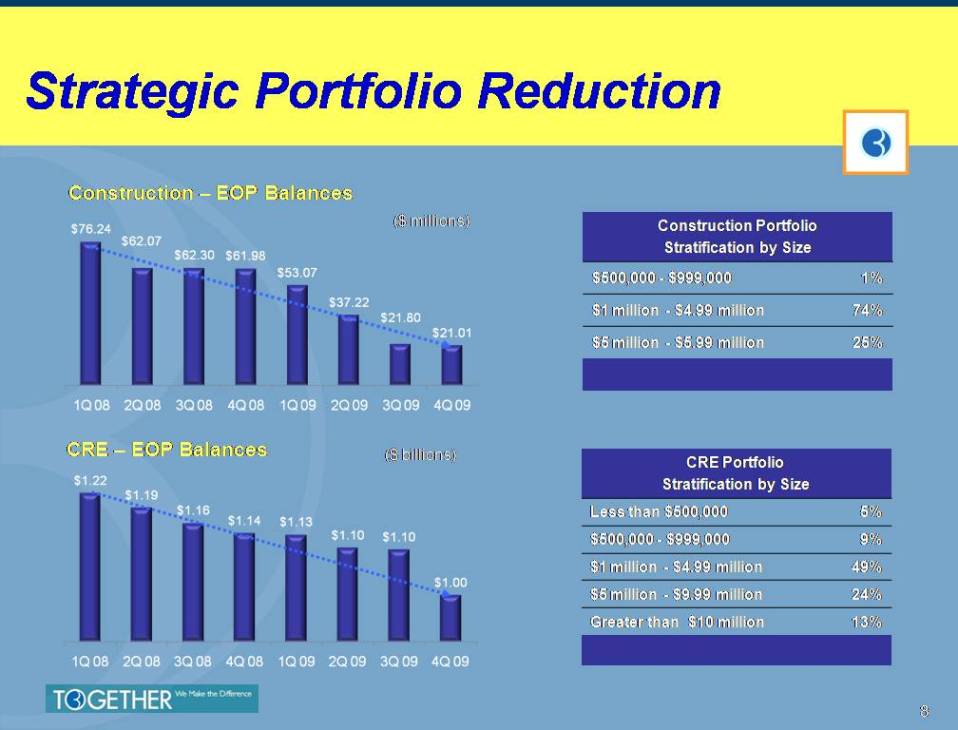

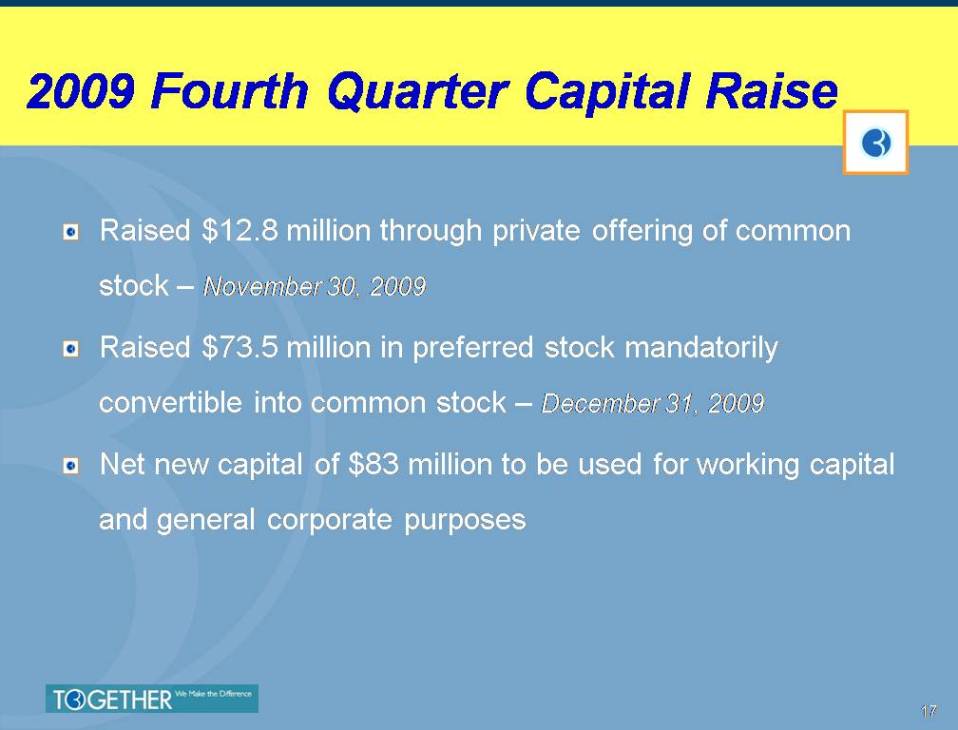

Strategic Management Initiatives Enhance operational efficiencies 25% reduction in core operating expense structure 4Q09 vs. 1Q08Successfully resolved long standing KEIC litigation eliminating rising legal feesFTE count lowered from peak of 366 as of 3/31/08 to 265 as of 12/31/09Commenced deleveraging strategy at the close of 1Q08Real estate construction portfolio reduced 72% from peak at 1Q08 to $21.0 million at 12/31/09CRE portfolio down-sized by $214.6 million from 1Q08 to $1.0 billion at 12/31/09Proactive balance sheet managementLoans reduced by $334 million, deposits increased by $70 million 1Q08 to 4Q09FHLB advances reduced by 27% Q3 to Q3Mitigate potential credit risk Speedy resolution of problem credits - $130 million of note sales in 2009Aggressively built loan loss reservesStrengthen capital position to capitalize on opportunities aheadRaised $12.8 million in a private offering that closed on November 30Raised $73.5 million of mandatorily convertible private placement Cleanse the balance sheet and address all open credit issues during 4Q09

Resilient Koreatown Factors supporting influx of Korean immigrants and funds Ratification of Visa-Waiver status Ratification of US-Korea FTA Liberation of currency controls Mid-Wilshire financial district Symbolic for growth in LA’s Korean-American community

(Gp:) Seattle Chicago Geographic Footprint Corporate Headquarters Branch Offices (19) Loan Production Office (1) Southern California Inland Empire Los Angeles Orange County San Diego

Strategic Portfolio Reduction Construction – EOP Balances ($ millions) ($ billions) CRE – EOP Balances

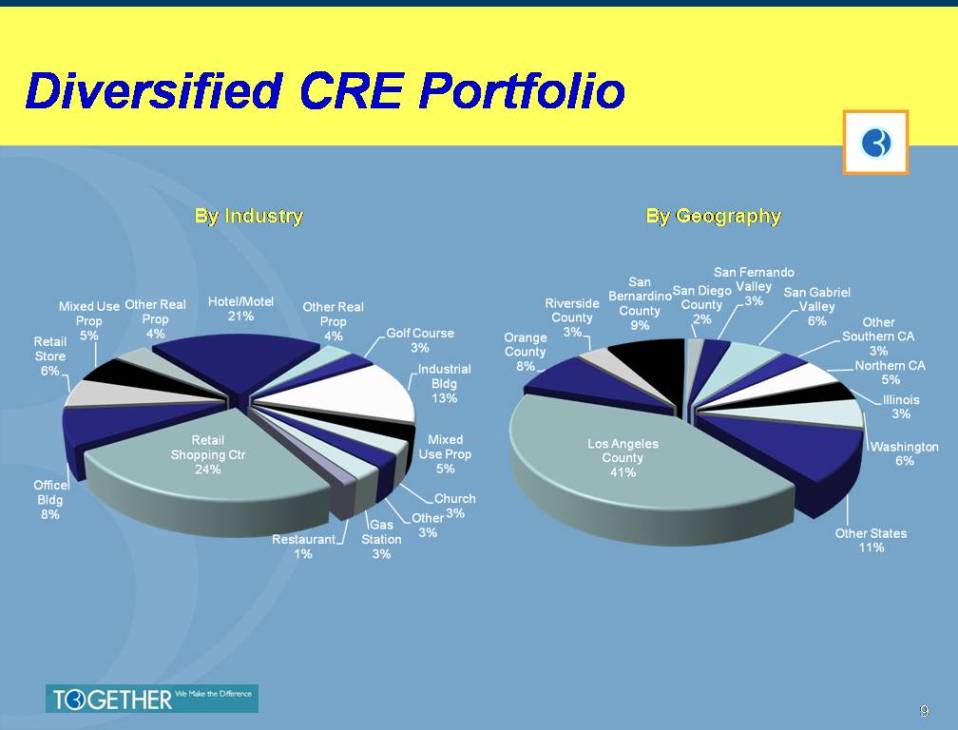

Diversified CRE Portfolio By Industry By Geography

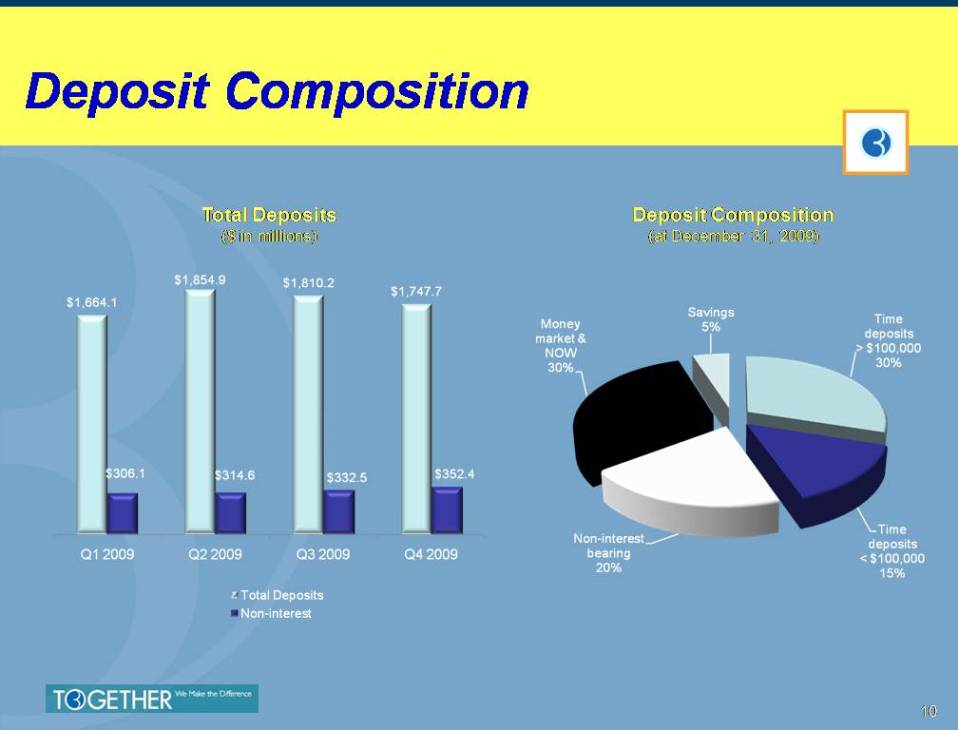

Deposit Composition Total Deposits ($ in millions) Deposit Composition (at December 31, 2009)

Vigilance to Credit Quality Fully understanding the market Extensive management experience directly in marketplace Balancing marketing and credit quality Regular reviews of loan portfolio Recent completion of Deep Dive External Loan Review Annual self stress testing of portfolio sampling expanded to quarterly stress test of 100% of loan portfolio Semi-annual external loan review of 70% of loan portfolio Ongoing credit training Stringent underwriting standards and guidelines

Heightened Credit Risk Management Asset quality task force Proactive executive management involvement Bi-weekly review of delinquent loans greater than $500,000 Action plan initiated from day one of delinquency Internal stress testing mechanisms Deployment of new program enabling more regular testing Quarterly stress test being applied to 100% of loan portfolio Capital burn down analysis assuming significant CRE devaluation Minimizing portfolio risk Strategic sales and run-off of construction and CRE portfolios Revitalize SBA lending pipeline Allows for growth with minimal risk given 90% guarantee Low levels of loan loss provision needed

Deep Dive External Review in 4Q09 Body: Crowe Horwath reviewed 200 largest relationships 75%+ of total CRE loan portfolio, including 8 of 20 largest C&I loans Reviewed based on current LTV, DSC and Cap Rate conditions Review consistent with evolving regulatory standards Minimal to no credit for borrower guarantees, other changing criteria Including prior review by Cabrera & Associates, 90%+ of total portfolio reviewed in 2009 Review and resulting provision creates foundation for profitable 2010

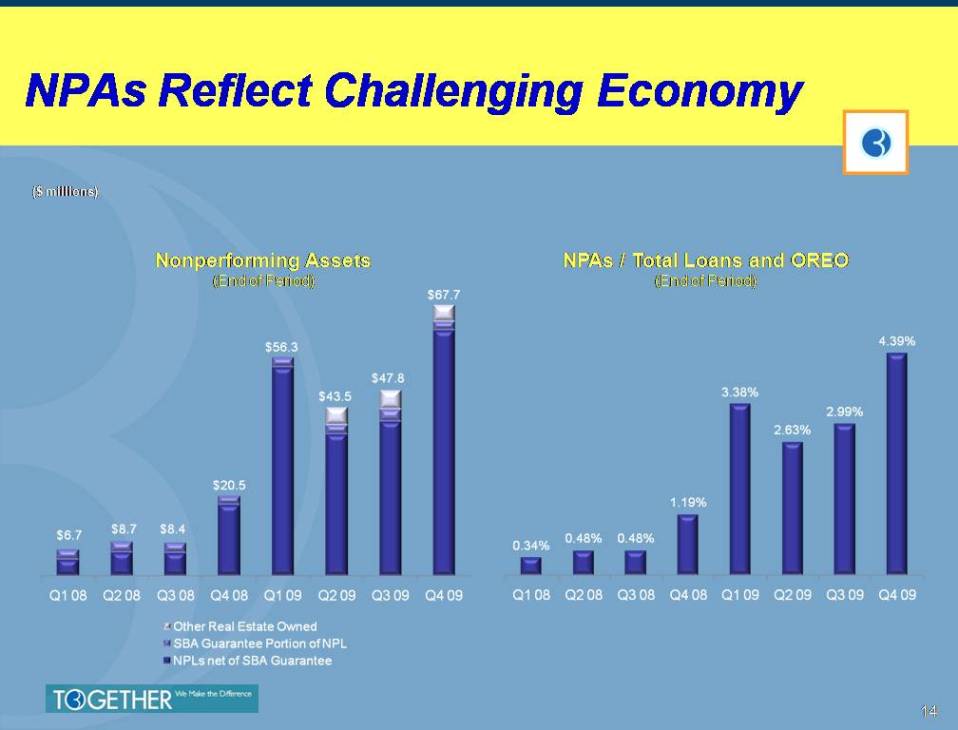

NPAs Reflect Challenging Economy Nonperforming Assets (End of Period) NPAs / Total Loans and OREO (End of Period) ($ millions)

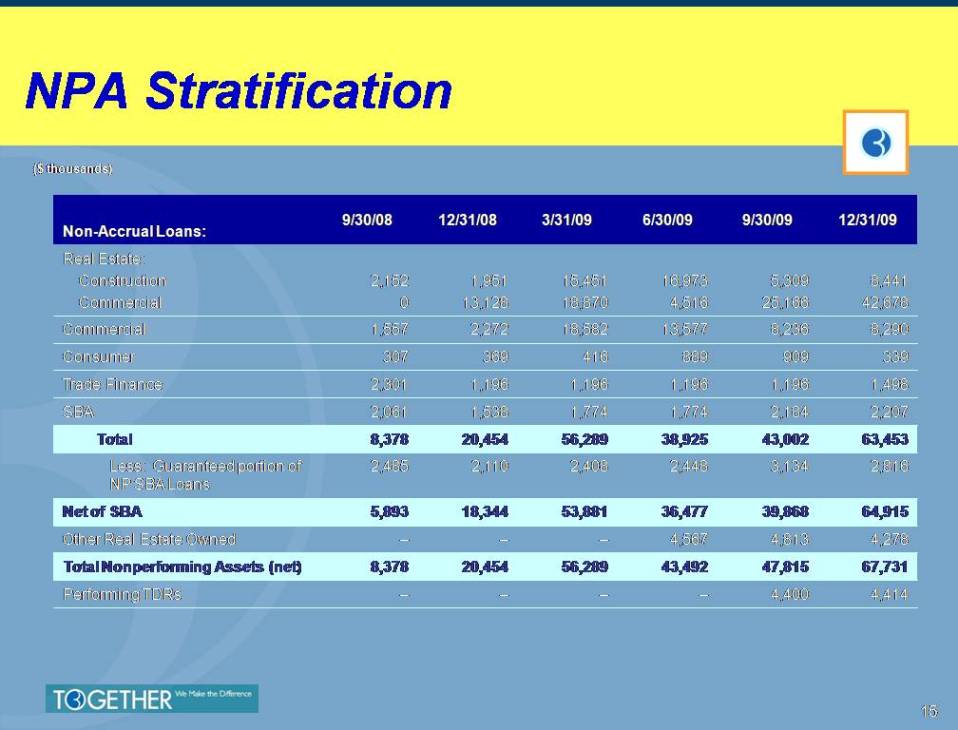

NPA Stratification($ thousands)

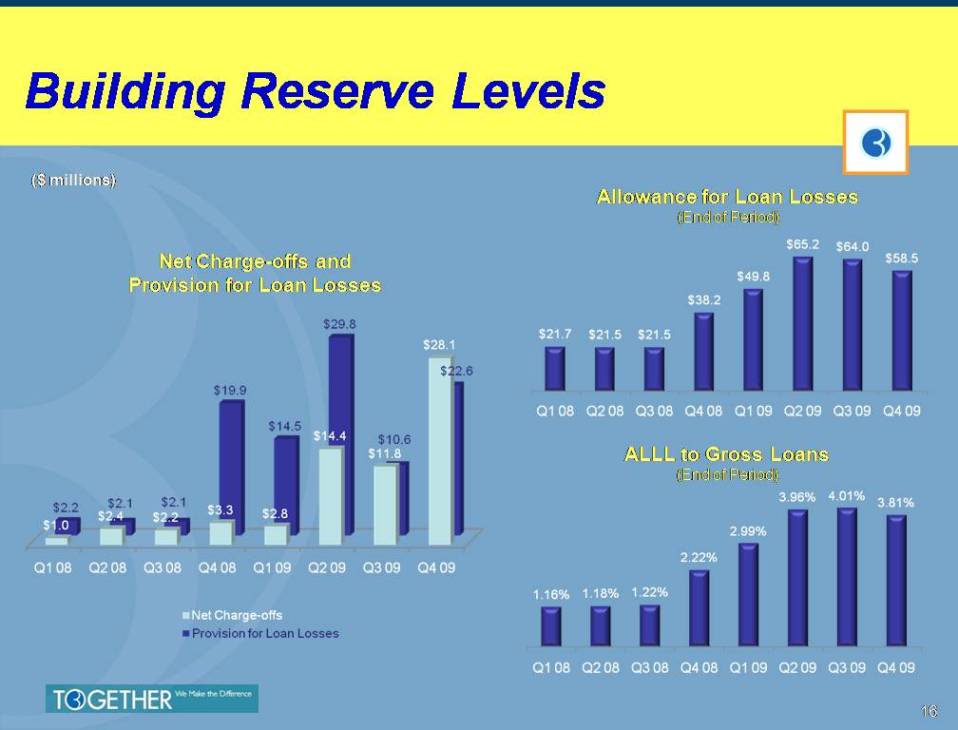

Building Reserve Levels Net Charge-offs and Provision for Loan Losses Allowance for Loan Losses (End of Period) ALLL to Gross Loans (End of Period) ($ millions)

2009 Fourth Quarter Capital Raise Raised $12.8 million through private offering of common stock – November 30, 2009 Raised $73.5 million in preferred stock mandatorily convertible into common stock – December 31, 2009 Net new capital of $83 million to be used for working capital and general corporate purposes

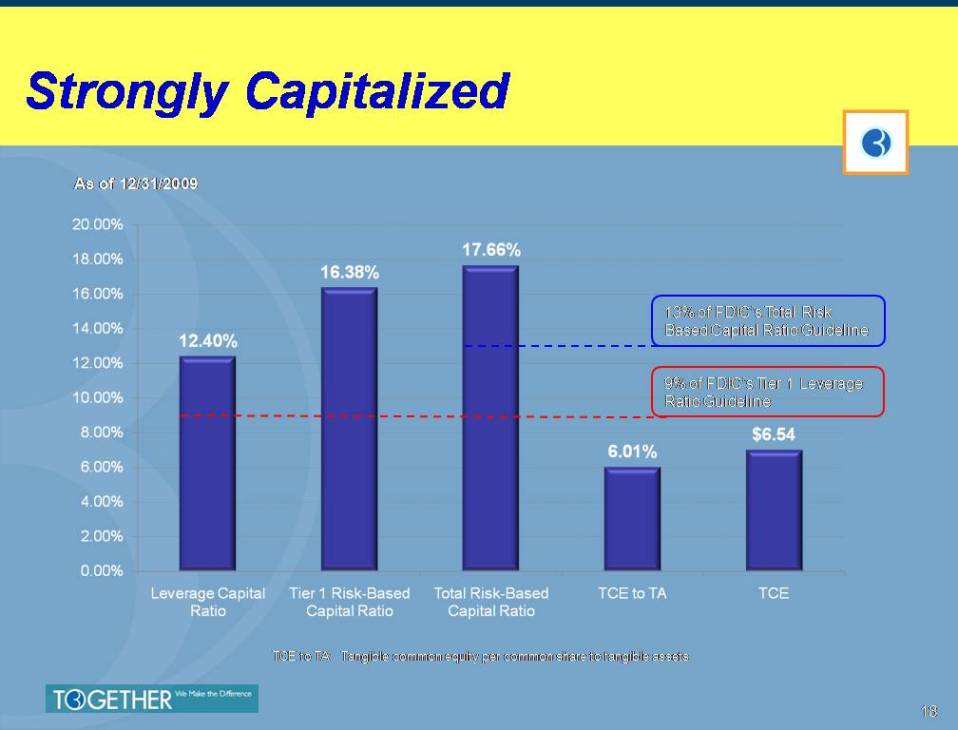

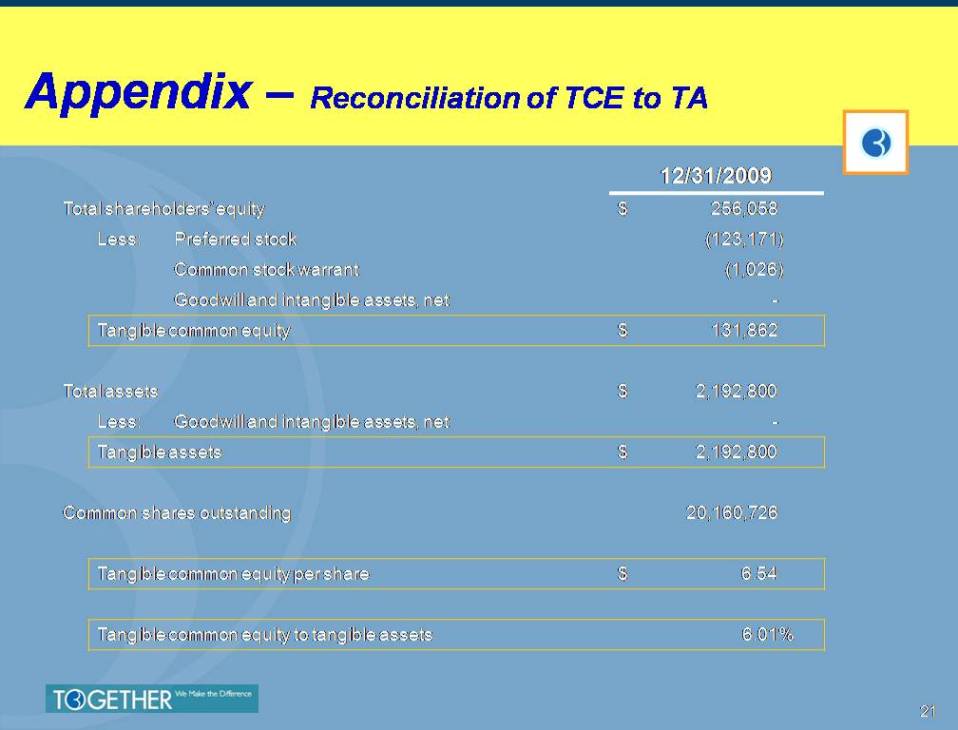

Strongly Capitalized TCE to TA: Tangible common equity per common share to tangible assets As of 12/31/2009 9% of FDIC’s Tier 1 Leverage Ratio Guideline 13% of FDIC’s Total Risk Based Capital Ratio Guideline

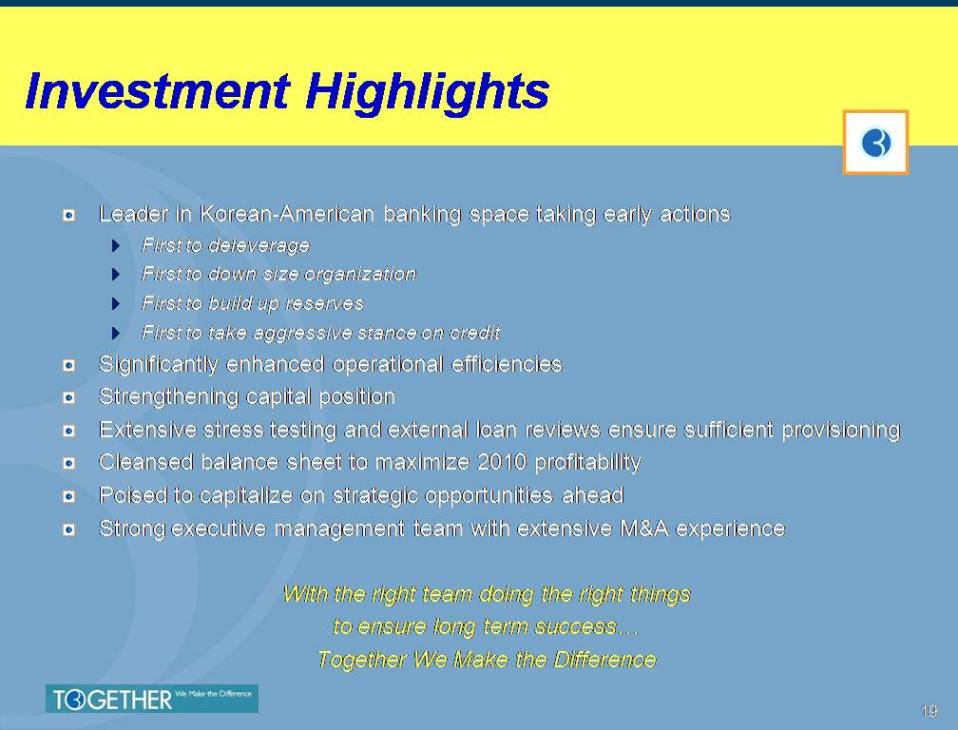

Investment Highlights Leader in Korean-American banking space taking early actions First to deleverage First to down size organization First to build up reserves First to take aggressive stance on credit Significantly enhanced operational efficiencies Strengthening capital position Extensive stress testing and external loan reviews ensure sufficient provisioning Cleansed balance sheet to maximize 2010 profitability Poised to capitalize on strategic opportunities ahead Strong executive management team with extensive M&A experience With the right team doing the right things to ensure long term success… Together We Make the Difference

Slide: 20

Appendix – Reconciliation of TCE to TA

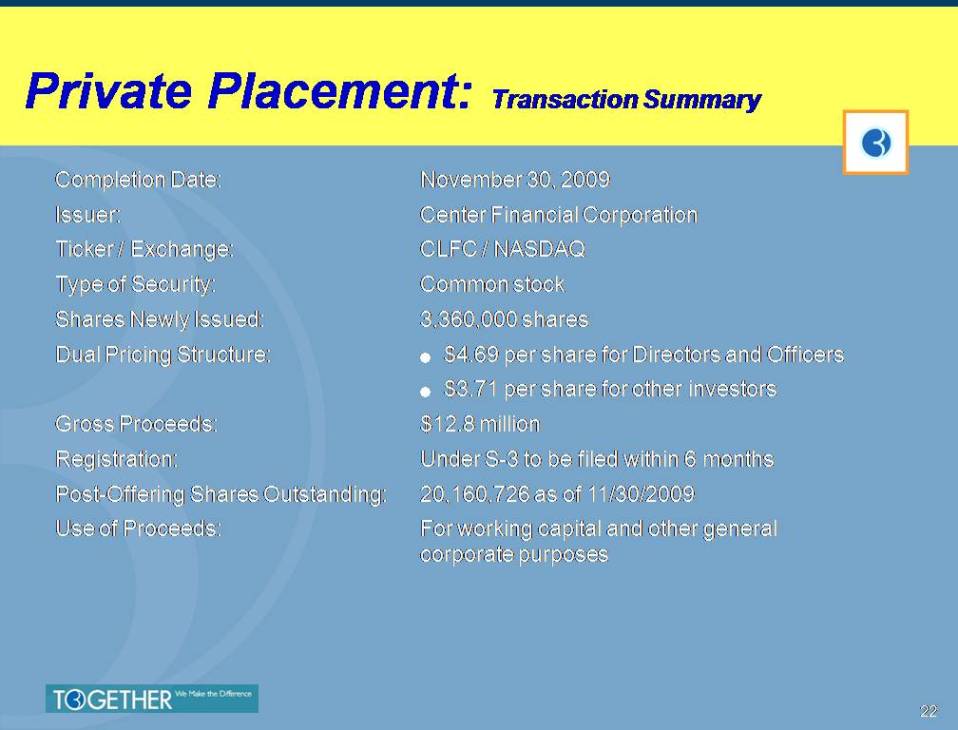

Private Placement: Transaction Summary Completion Date: November 30, 2009 Issuer: Center Financial Corporation Ticker / Exchange: CLFC / NASDAQ Type of Security: Common stock Shares Newly Issued: 3,360,000 shares Dual Pricing Structure: ? $4.69 per share for Directors and Officers ? $3.71 per share for other investors Gross Proceeds: $12.8 million Registration: Under S-3 to be filed within 6 months Post-Offering Shares Outstanding: 20,160,726 as of 11/30/2009 Use of Proceeds: For working capital and other general corporate purposes

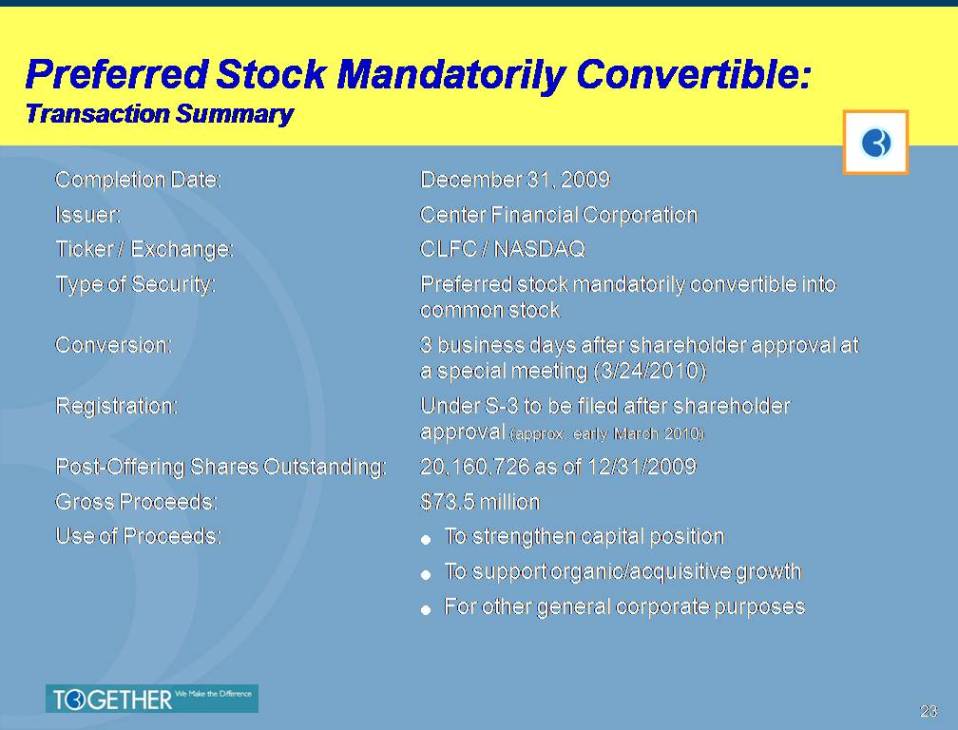

Preferred Stock Mandatorily Convertible: Transaction Summary Completion Date: December 31, 2009 Issuer: Center Financial Corporation Ticker / Exchange: CLFC / NASDAQ Type of Security: Preferred stock mandatorily convertible into common stock Conversion: 3 business days after shareholder approval at a special meeting (3/24/2010) Registration: Under S-3 to be filed after shareholder approval (approx. early March 2010) Post-Offering Shares Outstanding: 20,160,726 as of 12/31/2009 Gross Proceeds: $73.5 million Use of Proceeds: ? To strengthen capital position ? To support organic/acquisitive growth ? For other general corporate purposes