Attached files

| file | filename |

|---|---|

| 8-K - 8-K FOR 2009 EARNINGS RELEASE - TEMPLE INLAND INC | tin8k2009earnings20100209.htm |

| EX-99.3 - INVESTOR PRESENTATION MATERIALS - TEMPLE INLAND INC | tinex99320100209.htm |

| EX-99.1 - 2009 EARNINGS RELEASE - TEMPLE INLAND INC | tinex99120100209.htm |

13

Our

job is to be the best

14

This

presentation contains “forward-looking statements” within the meaning of the

federal

securities laws. These statements reflect management’s current views with respect to future

events and are subject to risk and uncertainties. We note that a variety of factors and uncertainties

could cause our actual results to differ significantly from the results discussed in the forward-

looking statements. Factors and uncertainties that might cause such differences include, but are

not limited to: general economic, market, or business conditions; the opportunities (or lack

thereof) that may be presented to us and that we may pursue; fluctuations in costs and expenses

including the costs of raw materials, purchased energy, and freight; changes in interest rates;

demand for new housing; accuracy of accounting assumptions related to impaired assets,

pension and postretirement costs, and contingency reserves; competitive actions by other

companies; changes in laws or regulations; our ability to execute certain strategic and business

improvement initiatives; the accuracy of certain judgments and estimates concerning the

integration of acquired operations and other factors, many of which are beyond our control.

Except as required by law, we expressly disclaim any obligation to publicly revise any forward-

looking statements contained in this presentation to reflect the occurrence of events after the date

of this presentation.

securities laws. These statements reflect management’s current views with respect to future

events and are subject to risk and uncertainties. We note that a variety of factors and uncertainties

could cause our actual results to differ significantly from the results discussed in the forward-

looking statements. Factors and uncertainties that might cause such differences include, but are

not limited to: general economic, market, or business conditions; the opportunities (or lack

thereof) that may be presented to us and that we may pursue; fluctuations in costs and expenses

including the costs of raw materials, purchased energy, and freight; changes in interest rates;

demand for new housing; accuracy of accounting assumptions related to impaired assets,

pension and postretirement costs, and contingency reserves; competitive actions by other

companies; changes in laws or regulations; our ability to execute certain strategic and business

improvement initiatives; the accuracy of certain judgments and estimates concerning the

integration of acquired operations and other factors, many of which are beyond our control.

Except as required by law, we expressly disclaim any obligation to publicly revise any forward-

looking statements contained in this presentation to reflect the occurrence of events after the date

of this presentation.

This

presentation includes non-GAAP financial measures. The

required reconciliations to

GAAP financial measures are included on our website, www.templeinland.com.

GAAP financial measures are included on our website, www.templeinland.com.

15

Net

income (loss) per share

Special

items

Net

income per share

excluding

special items

special items

• Cash provided by

operations of $640 million in 2009

• Long-term debt

reduced by $482 million in 2009

|

2009 |

2008 |

|

$ 1.89

|

$ (0.08)

|

|

(1.19)

|

0.19

|

|

$ 0.70

|

$ 0.11

|

2009

Consolidated Results

16

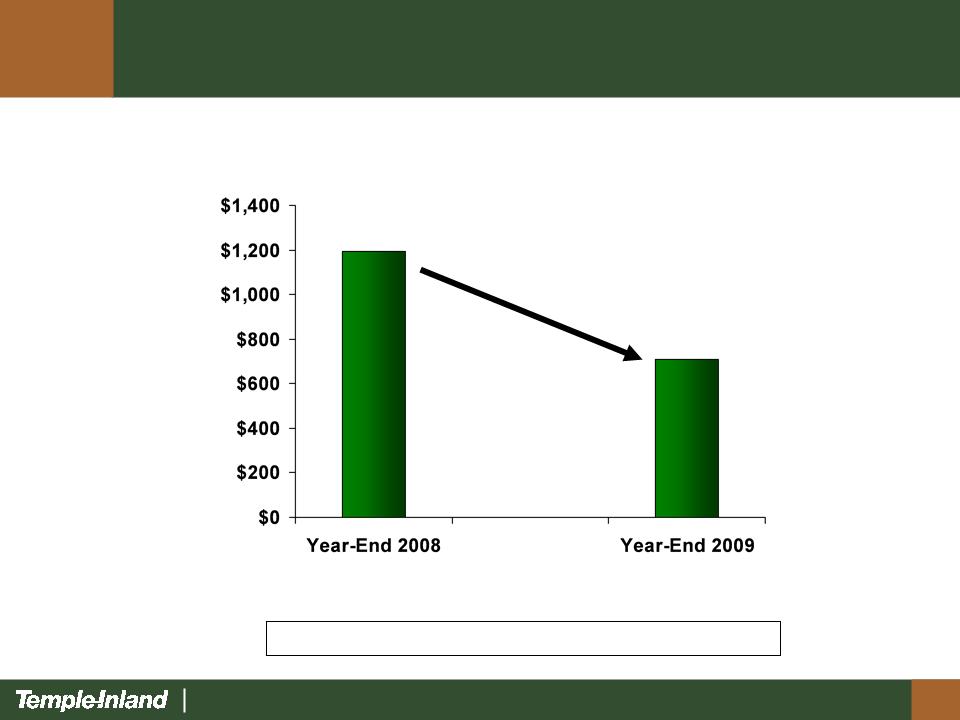

$482

$710

$1,192

Long-term

debt reduced by $482 million in 2009

2009

Long-Term Debt Reduction

17

|

|

2009

|

2008

|

|

Revenues

|

$

3,001

|

$

3,190

|

|

Costs and

expenses

|

2,654

|

2,965

|

|

Segment

operating income

|

$ 347

|

$ 225

|

($ in

Millions)

• Record annual

operating earnings

• 16.5% ROI - fourth

consecutive year of returns in excess of cost of capital

• Highest return in

peer group

Corrugated Packaging

Segment

18

($ in

Millions)

(Box

plant

transformation,

PBL and lower

mill costs)

transformation,

PBL and lower

mill costs)

(Lower

input

costs and lower

box pricing)

costs and lower

box pricing)

Corrugated Packaging

Segment Earnings

19

|

|

2009

|

2008

|

|

Revenues

|

$

576

|

$

694

|

|

Costs and

expenses

|

(603)

|

(734)

|

|

Segment

operating income (loss)

|

$ (27)

|

$ (40)

|

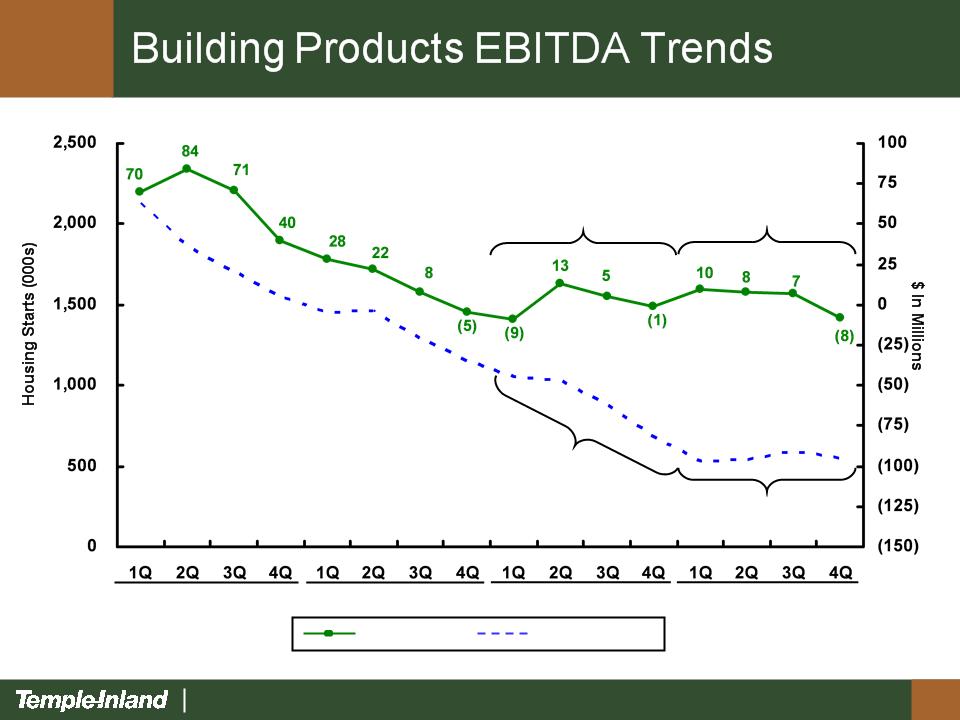

($ in

Millions)

• Housing starts

declined 39% in 2009 vs. 2008

• 2009 EBITDA of $17

million, an improvement of $9 million vs. 2008

Building Products

Segment

20

Housing

Starts

TIN

EBITDA

2006

2007

2008

2,127

2009

906

554

$8

$17

21

Net

income (loss) per share

Special

items

Net

income (loss) per share

excluding

special items

special items

|

Q4

2009

|

Q4

2008

|

Q3

2009

|

|

$ 0.34

|

$

(0.06)

|

$ 0.61

|

|

(0.41)

|

0.17

|

(0.37)

|

|

$(0.07)

|

$ 0.11

|

$ 0.24

|

• Cash provided by

operations of $200 million

• Long-term debt down

$169 million

• Share-based

compensation expense increased $37 million vs. Q4 2008 and

$6 million vs. Q3 2009 due to increase in share price

$6 million vs. Q3 2009 due to increase in share price

Fourth

Quarter 2009 Consolidated Results

22

($ in

Millions)

|

|

Q4

2009

|

Q4

2008

|

Q3

2009

|

|

Revenues

|

$

715

|

$

819

|

$

734

|

|

Costs and

expenses

|

(658)

|

(751)

|

(640)

|

|

Segment

operating income

|

$ 57

|

$ 68

|

$ 94

|

• 10.8%

ROI

• Highest return in

peer group

Corrugated Packaging

Segment

23

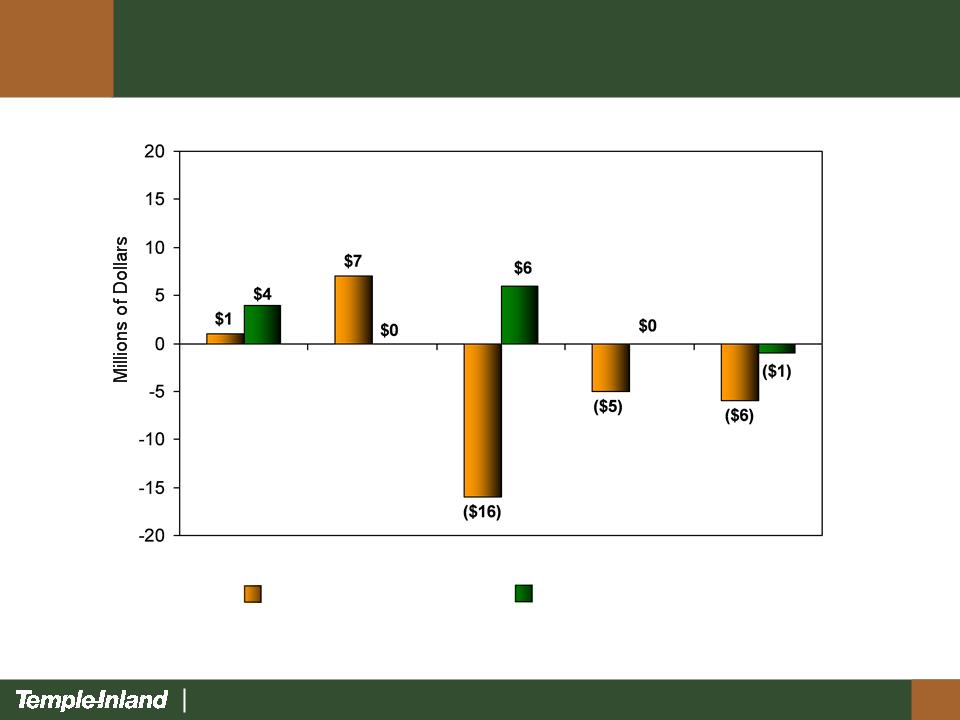

Q4 2009

vs. Q4 2008 Q4 2009

vs. Q3 2009

Virgin

Fiber OCC Energy Chemicals Freight

Key

Input Cost Changes

24

TIN

Average Box Price *

* Average

box price realization includes the impact of mix of business

2008

Q4 Q1 Q2 Q3 Q4

2009

Corrugated Packaging

Segment

25

Box

Shipments

*

Source: Fibre Box Association

2008

2009

Corrugated Packaging

Segment

26

Matching Production

to our Demand

• Q4 2009

downtime

– 23,000 tons

maintenance related

– 16,000 tons weather

related

• Q1 2010

– 27,000 tons

maintenance related

27

($ in

Millions)

|

|

Q4

2009

|

Q4

2008

|

Q3

2009

|

|

Revenues

|

$

130

|

$

154

|

$ 151

|

|

Costs and

expenses

|

(148)

|

(168)

|

(155)

|

|

Segment

operating income (loss)

|

$( 18)

|

$( 14)

|

$

( 4)

|

• Seasonally

adjusted

housing

starts declined 16% in Q4 2009 vs. Q4 2008

• Actual housing

starts declined 24% in Q4 2009 vs. Q3 2009

• Non-cash inventory

adjustment and asset write-offs of $4 million

Building Products

Segment

28

Lumber

Price

2008

2009

Q4 Q1 Q2 Q3 Q4

Volume

2008

2009

Q4 Q1 Q2 Q3 Q4

Building Products

Segment

29

Gypsum

Volume

2008

2009

Q4 Q1 Q2 Q3 Q4

Price

Q4 Q1

Q2 Q3 Q4

2008

2009

Building Products

Segment

30

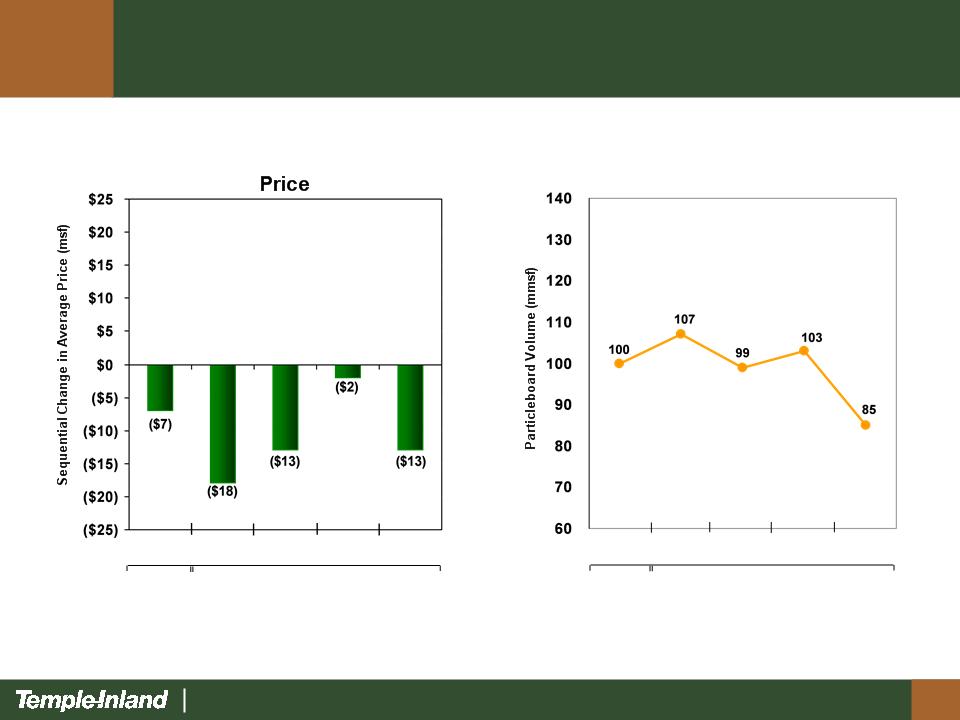

Particleboard

Volume

2008

2009

Q4 Q1 Q2 Q3 Q4

Q4 Q1

Q2 Q3 Q4

2008

2009

Building Products

Segment

31

2009

Fourth Quarter and Full Year

Financial Highlights

Financial Highlights

• Cash

Flow

- Cash

provided by operations $200 million in 4Q/2009 and

$640

million for the year

• Balance

Sheet

- Long-term

debt $710 million at year-end, down $482 million

vs.

year-end, 2008

• Liquidity

- Committed

credit facilities $1,075

- Unused

available borrowing capacity $890 million at

year-end

32

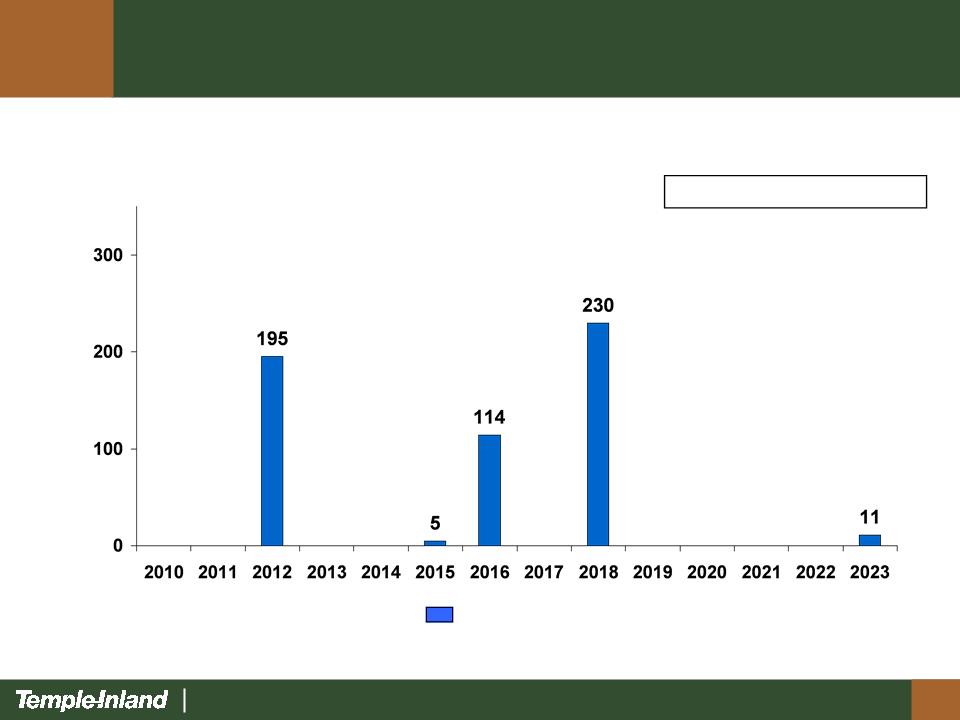

Term

debt

($ In

Millions)

Total

Term Debt = $555MM

Term

Debt Maturity Profile as of

Year-End 2009

Year-End 2009

33

($ In

Millions)

Year-End 2009

Liquidity Summary

Committed

facilities $1,075

Less: borrowings/commitments (185)

Unused

borrowing capacity $ 890

Covenants (as

specifically defined)

Debt/total

capital

43.0% 70%

max

Interest

coverage * 10.2x 3.0x

min

* Best

4 out of 5 trailing quarters

34

2009

Fourth Quarter and Full Year

Financial Highlights

Financial Highlights

• Expense related

items

– Interest expense $13

million in the fourth quarter,

down 43% vs. year ago

down 43% vs. year ago

– General &

administrative costs $70 million for 2009,

down 8% vs. year ago

down 8% vs. year ago

35

• Maintain high

integration level

• Drive for low

cost

• Improve mix and

margins

• Profitably grow

business

Corrugated Packaging

Strategic Initiatives

36

C

U

L

T

U

R

E

Lower

cost and higher margins

Corrugated Packaging

Strategic Initiatives

• Drive Low Cost and

Increase Asset

Utilization

Utilization

– Fewer

Plants

– Fewer

Machines

– Fewer

People

• Improve Mix &

Margins

37

Box

Plant Transformation I (2006-2010)

• EBIT (Lower

Costs)

$80MM/Year

– Fewer Plants

4

– Fewer Machines

88

– Fewer People

1,157

• Investment

$174MM

• ROI

46%

38

Box

Plant Transformation II (2010-2013)

• EBIT (Lower

Costs)

$100MM/Year

– Fewer Plants

12

– Fewer Machines

66

– Fewer People

917

• Investment

$250MM

• ROI

40%

39

2010

• Capital

Expenditures

- 2009 :

$130MM

- 2010 :

$200MM-$210MM

• Depreciation

- 2009 :

$200MM

- 2010 :

$198MM

• Pension

- No

required cash contribution in 2010

- Voluntary,

discretionary contribution in 2010 : $30MM

- Pension

expense in 2010 : $59MM

40

2010

• General and

administrative expenses

- 2009 :

$70MM

- 2010 :

$71 - $73MM

• Share-based and

long-term incentive compensation

- 2009 :

$58MM

- 2010 :

$32MM, $1 change in share price = $2.3 million

• Interest

expense

- 2009 :

$63MM

- 2010 :

$50 - $52 MM

• Income

tax

- 2010

effective tax rate = 39%

- 2010

remain a 20% cash tax payer

41

2010

Financial Priorities

• Return cash to

shareholders

– Maintained dividend

during 2009

– Q1 2010 dividend

increased 10% to annual

rate of $0.44 per share

rate of $0.44 per share

• Reduce

debt

• Invest in our

business

• Profitably

grow

42

Our

job is to be the best