Attached files

| file | filename |

|---|---|

| 8-K - BRYN MAWR BANK CORPORATION -- FORM 8-K - BRYN MAWR BANK CORP | d8k.htm |

Bryn

Mawr Bank Corporation NASDAQ: BMTC Fourth Quarter 2009 Update Exhibit 99.1 |

2 This presentation contains certain forward-looking statements. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include the words believe, expect, anticipate, intend, plan, estimate or words of similar meaning. Forward-looking statements, by their nature, are subject to risks and uncertainties. A number of factors, many of which are beyond Bryn Mawr Bank Corporation's (“the Corporation”) control could cause actual conditions, events or results to differ significantly from those described in the forward looking statements. Forward- looking statements speak only as of the date they are made. The Corporation does not undertake to update forward-looking statements. Safe Harbor |

3 Where to Find More Information About the First Keystone Financial, Inc. Merger The Corporation has filed with the Securities and Exchange Commission

("SEC") a Registration Statement on Form S-4 concerning

the proposed merger of First Keystone Financial, Inc. into the Corporation

(the “Merger”). The Registration Statement includes a prospectus for the offer and sale of the Corporation’s Common Shares to First Keystone Financial, Inc.'s

shareholders as well as a proxy statement for the solicitation of proxies from First Keystone Financial,

Inc.'s shareholders for use at the meeting at which the Merger will be voted

upon. The combined prospectus and proxy statement and other documents filed

by the Corporation with the SEC contain important information about the

Corporation, First Keystone Financial, Inc., and the Merger. We urge

investors and First Keystone Financial, Inc.'s shareholders to read carefully the combined prospectus and proxy statement and other documents filed with the SEC,

including any amendments or supplements also filed with the SEC. First

Keystone Financial, Inc.'s shareholders in particular should read the

combined prospectus and proxy statement carefully before making a decision

concerning the Merger. Investors and shareholders may obtain a free copy of the combined prospectus and proxy statement – along with other filings containing information about the Corporation – at the SEC’s website at http://www.sec.gov. Copies of the combined prospectus and proxy statement, and the filings with the SEC incorporated by reference in the

combined prospectus and proxy statement, can also be obtained free of charge

by directing a request to Bryn Mawr Bank Corporation, 801 Lancaster Avenue, Bryn Mawr, PA 19010, attention Robert

Ricciardi, Secretary, telephone (610) 526-2059 |

4 Bryn Mawr Bank Corporation Profile Founded in 1889 – 120 year history A unique business model with a traditional commercial bank ($1.2 billion) and a trust company ($2.9 billion) under one roof Wholly owned subsidiary – The Bryn Mawr Trust Company Located on Philadelphia’s affluent “Main Line”

|

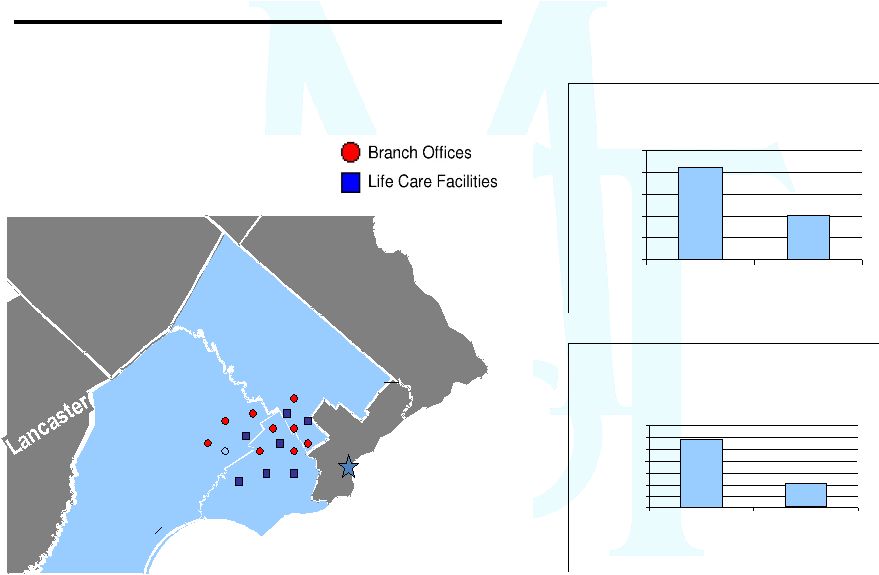

5 Chester Bucks Montgomery Berks State of Delaware Philadelphia New Jersey Delaware New Jersey The Franchise Footprint 9 Full Service Branches/ 7 Life Care Facilities Source: Public School Review Average Household Income $84,600 $41,000 $- $20,000 $40,000 $60,000 $80,000 $100,000 BMTC Target Market Penna. State Average Percent of Population with College Degree 0% 20% 40% 60% 70% BMTC Target Market Penna. State Average 10% 30% 50% 59% 22% |

6 Investment Considerations A great brand & franchise Solid financial fundamentals Excellent overall credit quality Outstanding target market demographics New business initiatives driving growth Well-capitalized |

7 2009 2008 2007 Net Interest Income (in millions) $40.8 $37.1 $34.2 Net Interest Margin 3.85% 3.63% 4.11% Net Income (in millions) $10.3 $9.3 $13.6 Diluted EPS $1.17 $1.08 $1.58 ROA 0.88% 0.89% 1.59% ROE 10.55% 10.01% 15.87% Financial Highlights |

8 Financial Highlights - continued 2009 2008 2007 Portfolio Loans & Leases (in millions) $887 $900 $803 Wealth Assets in Total (in billions) $2.87 $2.26 $2.28 Nonperforming loans % of loan portfolio 0.80% 0.65% 0.25% Tangible Book Value Per Share $10.40 $9.55 $10.60 Tangible Common Equity Ratio 7.51% 7.19% 9.02% Dividends Declared $0.56 $0.54 $0.50 |

9 Consistent 2009 Quarterly Results Net Income ($ in millions) Basic Earnings Per Common Share Diluted Earnings Per Common Share Dividend Declared Per Share 4 th Qtr 2009 $2.64 $0.30 $0.30 $0.14 3 rd Qtr 2009 2.62 0.30 0.30 0.14 2 nd Qtr 2009 2.45 0.28 0.28 0.14 1 st Qtr 2009 2.63 0.31 0.31 0.14 |

10 2009 Results Robust in-market residential mortgage originations Strong rebound in wealth management assets to $2.9 billion Improving margin: 3.85% (Q42009) vs. 3.63% (Q42008) Strong deposit growth Solid Bank investment portfolio performance with realized gains of approximately $2.0 million No OTTI charges in 2007, 2008 or 2009 |

11 2009 Results - continued Lease portfolio charge-offs have declined each quarter in 2009 (Q4 2009: $763 thousand vs. Q4 2008: $1.6 million) Loan quality strong with nonperforming loans and leases of 80 basis points at 12/31/2009 FDIC insurance and special assessment added to 2009 non-interest expense Merger related expenses and professional fees increased due to First Keystone Financial Inc. merger agreement and other initiatives

|

12 2010 Strategies Protect the net interest margin Complete the First Keystone merger and introduce Bryn Mawr Trust services to its customers Expand our Wealth Management offerings Control expenses Use banking industry turmoil to attract new clients Opportunistic expansion Raise capital as needed Maintain strong capital and liquidity programs |

New

Business Initiatives |

14 Announced acquisition of First Keystone Financial, Inc. Announced on November 2, 2009 $525 million in assets Expands footprint in Delaware and Chester counties with 8 branches New opportunities for BMTC Wealth Management, Business Banking, Retail Banking and Mortgage Banking BMTC of Delaware The Delaware Advantage Generation Skipping Trusts Directed Trusts $386 million in assets at December 31, 2009 Growth Initiatives |

15 Bryn Mawr Asset Management “Lift out” strategy Two investment advisers hired, approximately $90 million in new assets Additional opportunities being evaluated Branch Office Expansion and Modernization West Chester Regional Banking Center Branch Wayne branch modernization completed Paoli branch modernization nearing completion Havertown branch modernization scheduled Growth Initiatives - continued |

16 First Keystone Financial, Inc. – Transaction Summary (1) Based upon BMTC’s average daily closing price for twenty consecutive trading

days ending 10/30/2009 ($16.76) Acquiror: Bryn Mawr Bank Corporation (NASDAQ: BMTC) Seller: First Keystone Financial, Inc. (NASDAQ: FKFS) Consideration: Each share of FKFS common stock will be exchanged for 0.6973 BMTC shares (1) and $2.06 in cash Transaction Value: $34 million Merger Consideration Adjustment: Per Share Merger Consideration subject to downward adjustment based on the rise of FKFS delinquencies above a specified level one month prior to close Board Representation: Donald Guthrie (Chairman of the FKFS Board of Directors) will join the BMTC Bank and Holding Company Boards as a Director Closing Condition: Aggregate amount of FKFS delinquencies must be less than $16.5 million Required Approvals: Customary Regulatory and FKFS Shareholders Expected Closing: Q3 2010 – Shareholder vote scheduled March 2, 2010 Acquiror: Bryn Mawr Bank Corporation (NASDAQ: BMTC) Seller: First Keystone Financial, Inc. (NASDAQ: FKFS) Consideration: Each share of FKFS common stock will be exchanged for 0.6973 BMTC shares (1) and $2.06 in cash Transaction Value: $34 million (approximate at announcement) Merger Consideration Adjustment: Per Share Merger Consideration subject to downward adjustment based on the rise of FKFS delinquencies above a specified level one month prior to close Board Representation: Donald Guthrie (Chairman of the FKFS Board of Directors) will join the BMTC Bank and Holding Company Boards as a Director Closing Condition: Aggregate amount of FKFS delinquencies must be less than $16.5 million Required Approvals: Customary Regulatory and FKFS Shareholders Expected Closing: |

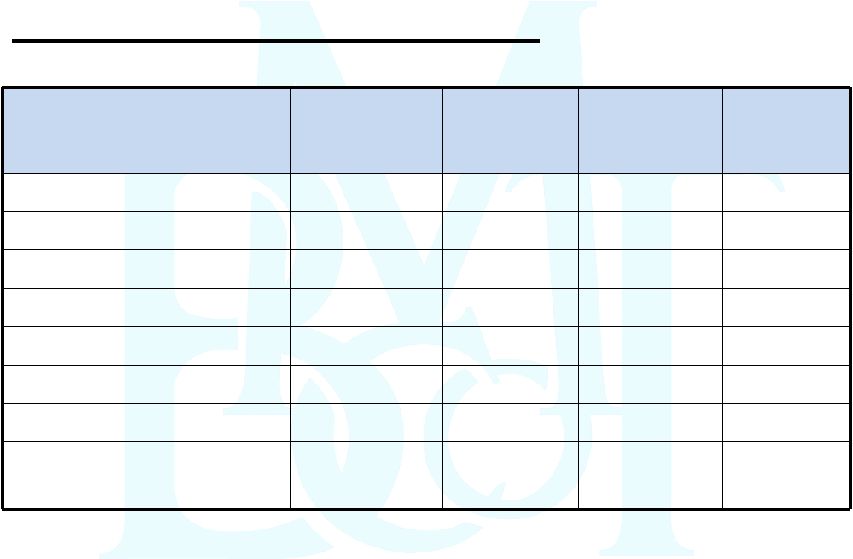

17 Merger Consideration Adjustment FKF Delinquencies At Month- End Preceding Closing Adjusted Amount Of BMBC Stock To Be Received For Each FKF Share Adjusted Per Share Cash Consideration For Each FKF Share Less Than $10.5 million 0.6973 $2.06 $10.5 - $12.5 million 0.6834 $2.02 $12.5 - $14.5 million 0.6718 $1.98 $14.5 - $16.5 million 0.6589 $1.95 $16.5 million or more 0.6485 $1.92 Delinquencies are defined in the merger agreement as all loans delinquent 30 days or

more, non-accruing loans, other real estate owned, troubled debt

restructurings and the aggregate amount of loans charged-off between 10/31/2008 and the month-end preceding closing in excess of $2.5 million. FKF delinquencies at

12/31/2009 were $12.4 million. |

18 First Keystone Financial Inc. - Transaction Highlights Expands branch footprint into the attractive demographic markets of Delaware and Chester County, Pennsylvania Important component of strategic plan Enhances long-term franchise value Complementary business mix Both banks have a “community focus” Significant potential synergies identified in wealth management services and residential

mortgage originations Low risk Transaction Extensive due diligence performed Conservative credit mark estimated Achievable cost savings identified Material earnings per share accretion after expensing merger related costs Attractive internal rate of return Pro Forma capital ratios remain significantly above “well capitalized” levels |

19 Pro Forma Deposit Market Share – Delaware County, PA 2009 Total 2009 Deposits Total in Market Branch Market Share Rank Institution (ST) Count ($M) (%) 1 Wells Fargo & Co. (CA) 21 1,630 15.3 2 Royal Bank of Scotland Group 23 1,585 14.9 3 Toronto-Dominion Bank 14 1,360 12.8 4 Citigroup Inc. (NY) 3 1,040 9.8 5 PNC Financial Services Group (PA) 11 929 8.7 6 Banco Santander S.A. 13 830 7.8 Pro Forma 14 563 5.3 7 Beneficial Mutual Bncp (MHC) (PA) 7 386 3.6 8 Alliance Bancorp of Penn (MHC) (PA) 8 338 3.2 9 First Keystone Financial (PA) 7 337 3.2 10 Bryn Mawr Bank Corp. (PA) 7 226 2.1 Top 10 114 8,662 81.3 Market Total 180 10,651 100.0 Bryn Mawr Bank Corp. (16) First Keystone Financial, Inc. (8) Expanding Southeast PA Footprint ($ in millions) BMTC FKFS Pro Forma Assets $1,196 $525 $1,721 Loans 886 317 1,203 Deposits 899 354 1,253 Branches 16 (1) 8 24 Pro Forma Financials Source: SNL Financial Pro forma financials do not include merger adjustments BMTC data as of 9/30/2009; FKFS data as of 6/30/2009 (1) Includes 7 limited service retirement community branches |

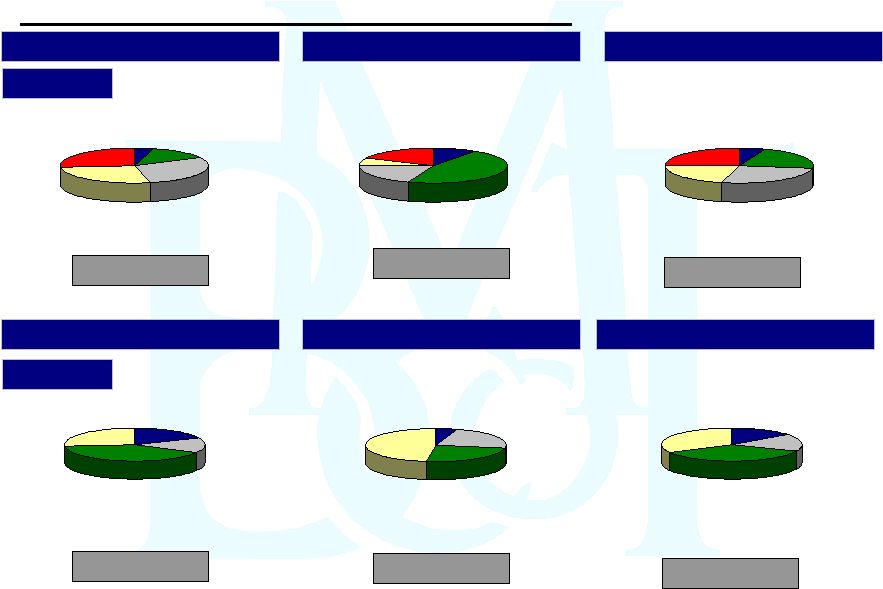

20 Time Deposits 32.7% NOW & Other Trans. Accts. 16.7% MMDA, Savings, & Other 35.8% Demand Deposits 14.8% Consumer & Other 24.5% Commercial & Industrial 21.6% Residential R.E. 22.0% Commercial R.E. 26.4% Construction R.E. 5.6% Consumer & Other 26.8% Commercial & Industrial 26.8% Residential R.E. 13.3% Commercial R.E. 28.9% Construction R.E. 4.2% Pro Forma Loans and Deposits Source: Company filings FKFS loan and deposit data as of 6/30/2009 BMTC stand alone loan and deposit data as of 9/30/2009 Time Deposits 26.8% NOW & Other Trans. Accts. 14.3% MMDA, Savings, & Other 40.2% Demand Deposits 18.7% Deposits Loans BMTC Stand Alone Total: $886M Total: $1.2B Total: $899M Total: $1.3B Consumer & Other 18.0% Commercial & Industrial 7.0% Residential R.E. 46.1% Commercial R.E. 19.4% Construction R.E. 9.6% Time Deposits 47.7% NOW & Other Trans. Accts. 22.7% MMDA & Savings 24.4% Demand Deposits 5.1% Total: $317M Total: $354M BMTC Stand Alone FKFS Stand Alone BMTC Pro Forma FKFS Stand Alone BMTC Pro Forma |

21 First Keystone Financial Inc. - Due Diligence Extensive due diligence conducted by BMTC and third parties during September 2009. Extensive credit due diligence conducted BMTC and third party loan review Reviewed over 65% of commercial portfolio (CRE, C&I, and Construction) Multiple Construction / Commercial Real Estate sites visited Conservative credit mark estimated at 4% to 5% of total loans outstanding including existing Allowance for Loan Loss balance. Estimated securities portfolio Mark–to–Market KPMG conducted tax and accounting due diligence |

Financial Review Bryn Mawr Bank Corporation Only As of December 31, 2009 |

23 Diluted Earnings Per Share (1) Excludes $0.10 per share gain on sale of real estate |

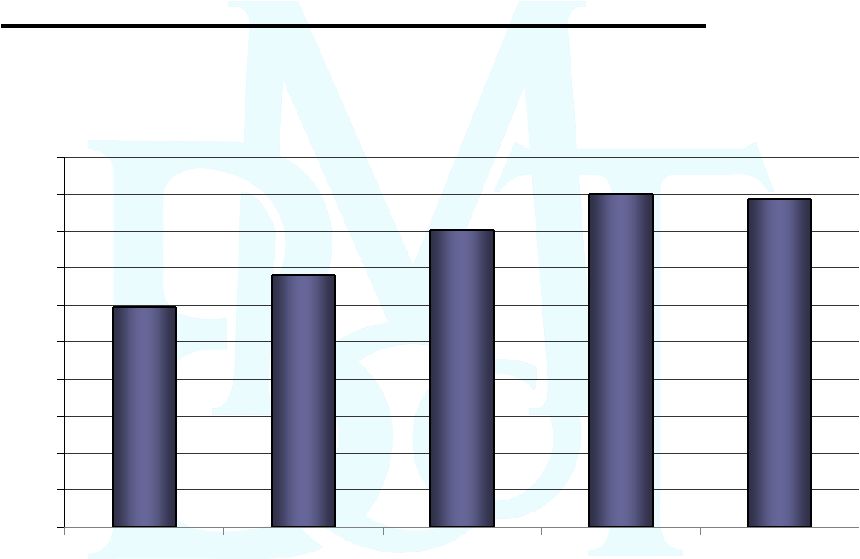

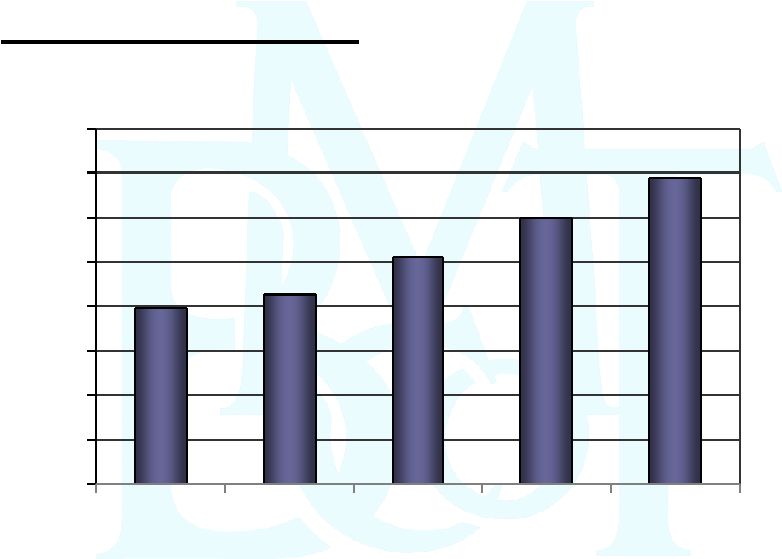

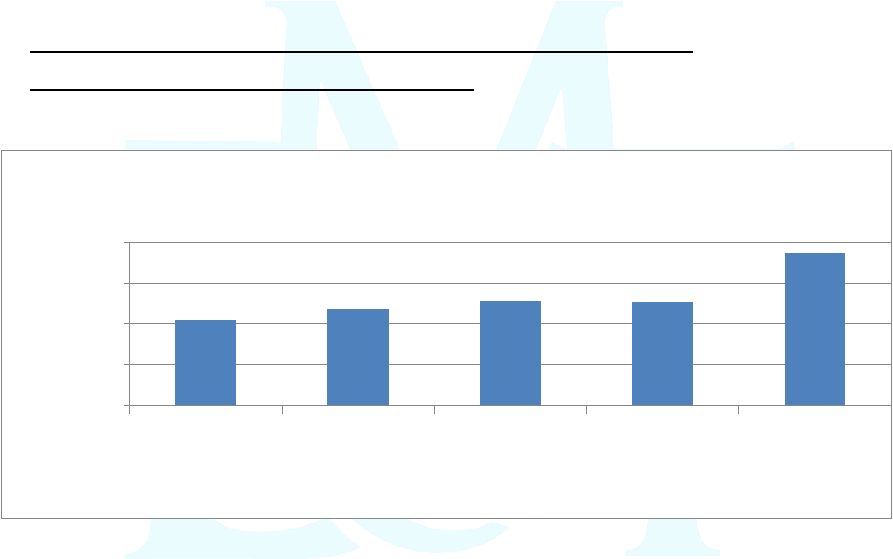

24 Portfolio Loan & Lease Growth Total Portfolio Loans & Leases Outstanding ($ in millions) CAGR : 10.5% (2005-2009) $595 $681 $803 $900 $887 $0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 2005 2006 2007 2008 2009 |

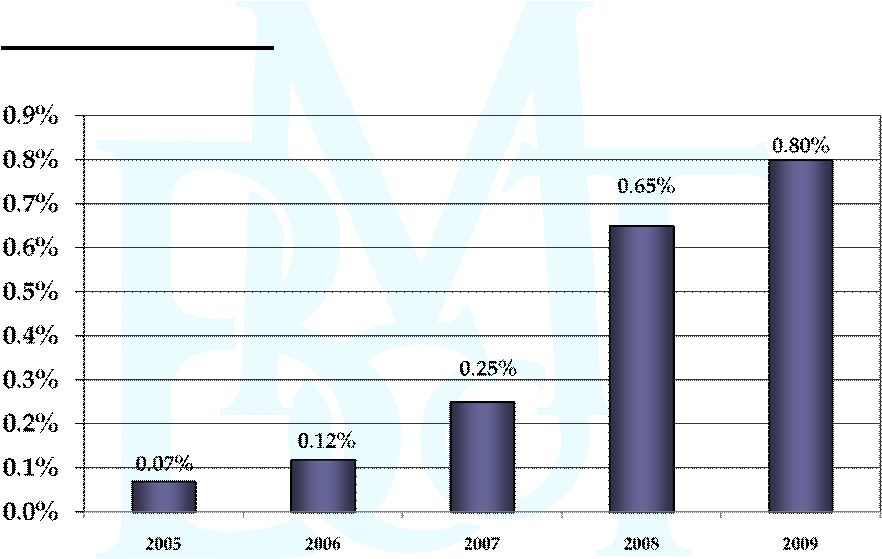

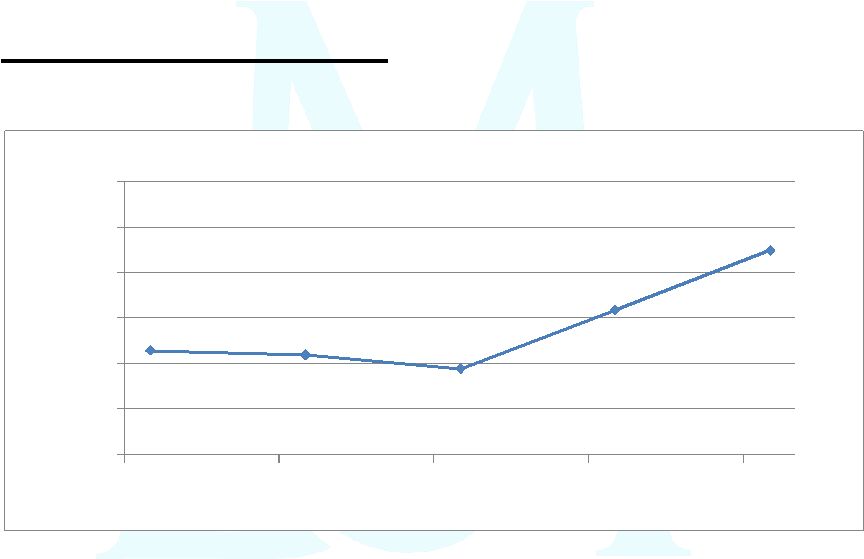

25 Asset Quality Nonperforming loans and leases as a % of portfolio loans and leases

|

26 Loan Composition at December 31, 2009 $265 $233 $191 $111 $38 $48 Commercial Mortgages Commercial & Industrial Home Equity Lines & Loans & Consumer Loans Residential Mortgages Construction Leases ($ in millions) |

27 Small Ticket National Leasing Business “Lift out” strategy Leases outstanding: $47.7 million at 12/31/2009 Lease portfolio reduced by design - $11.6 million since 12/31/2008 Average yield 10.54% Quarterly lease charge-offs have continuously decreased since 12/31/2008 Changes made in underwriting standards and collection process have improved results |

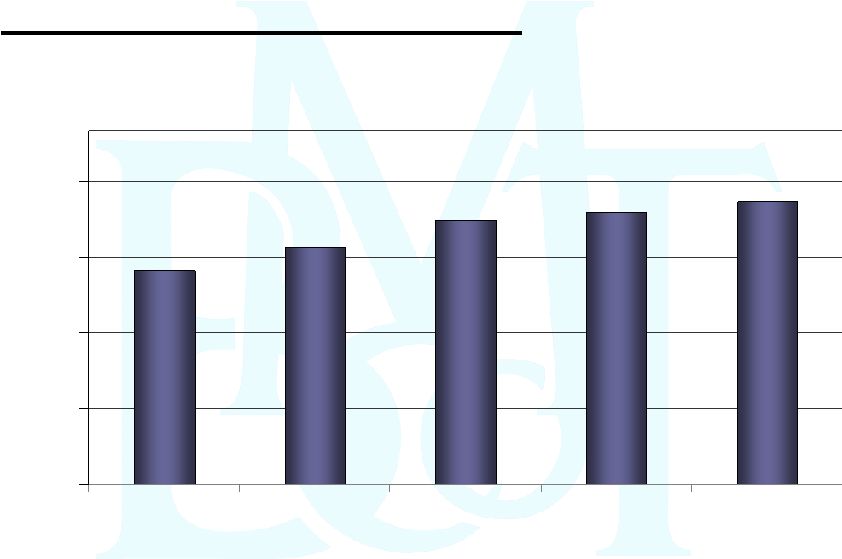

28 $31.3 $33.3 $34.2 $37.1 $40.8 $0 $10 $20 $30 $40 $50 2005 2006 2007 2008 2009 Net Interest Income CAGR: 6.9% (2005-2009) Note: Not on a tax-equivalent basis ($ in millions) |

29 3.63% 3.62% 3.59% 3.72% 3.85% 3.4% 3.5% 3.6% 3.7% 3.8% 3.9% 4.0% Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Net Interest Margin On a tax equivalent basis |

30 $596 $626 $709 $798 $888 $200 $300 $400 $500 $600 $700 $800 $900 $1,000 2005 2006 2007 2008 2009 Deposit Growth Average Annual Deposits ($ in millions) |

31 Average Deposits & Borrowed Funds Mix Fourth Quarter 2009 $185 $452 $162 $110 $148 $23 Non-Interest Bearing DDA Savings, NOW & Money Market Time Deposits Wholesale Deposits, IND & IDC Borrowed Funds Subordinated Debt ($ in millions) |

32 Wholesale Funding Totals Type December 31, 2009 % of Wholesale Funding December 31, 2008 % of Wholesale Funding Wholesale CD $ 15.2 6.5% $ 51.3 16.8% PLIGIT - - 40.0 13.1 FHLB Advances 144.8 61.7 154.9 50.7 CDARS 21.0 9.0 29.1 9.5 IND/IDC 53.6 22.8 30.5 10.0 Total Wholesale Funding $ 234.6 100.0% $ 305.8 100.0% Total Funding * $ 1,082.7 $ 1,024.4 Total Wholesale Funding/Total Funding 21.7% 29.9% * Total Funding = All deposits plus borrowings (includes wholesale

funding; excludes sub debt) ($ in millions) |

33 Additional Funding Sources at December 31, 2009 ($ in millions) Available Used Fed Funds Line of Credit (7 Banks) $ 75 $ 0 FHLB of Pittsburgh* $ 448 $145 Federal Reserve Bank – Discount Window Program $ 55 $ 0 Total $ 578 $ 145 Total (Percentage) 100% 25% * Additional FHLB of Pittsburgh common stock would need to be purchased to

utilize the unused availability |

34 Investment Portfolio as of December 31, 2009 ($ in thousands) Amortized Fair Unrealized SECURITY DESCRIPTION (AFS) Cost Value Gain / Loss U. S. Government Agency $ 85,462 $ 85,061 $

(401) State, County & Municipal 24,859

25,024

165

FNMA/FHLMC Mortgage Backed Securities 49,318

50,951

1,633 GNMA Mortgage Backed Securities 8,607

8,718

111

Foreign Debt Securities 1,500 1,499 (1) Bond – Mutual Funds 36,943 36,970 27 Total Investment Portfolio $ 206,689 $ 208,223 $ 1,534 Note: Other assets at December 31, 2009 include approximately $8 million of FHLB of Pittsburgh common stock at cost which is not paying a dividend and cannot be redeemed. |

35 Capital Considerations Bryn Mawr Bank Corporation elected not to take TARP Capital Maintains a “well capitalized” capital position Selectively add capital as needed to fund growth and acquisitions Additional earn out payments for Lau Associates at the end of 2010 and 2011 Active Dividend Reinvestment and Direct Stock Purchase Plan (DRIP/DSPP) |

36 Capital Position - Bryn Mawr Bank Corporation Regulatory Minimum to be Well Capitalized Actual 12/31/2009 Actual 12/31/2008 Tier I 6.00% 9.41% 8.81% Total (Tier II) 10.00% 12.53% 11.29% Tier I Leverage 5.00% 8.35% 8.03% Common Equity - 8.39% 8.03% Tangible Common Equity - 7.51% 7.13% |

37 Capital Position - Bryn Mawr Trust Company (“Bank”) Regulatory Minimum to be Well Capitalized Actual 12/31/2009 Actual 12/31/2008 Tier I 6.00% 9.06% 8.49% Total (Tier II) 10.00% 12.20% 10.98% Tier I Leverage 5.00% 8.03% 7.70% |

38 Capital Raised in 2009 $7.5 million in subordinated debt in April 2009 (Tier Two) $2.5 million in common stock in April 2009 DRIP/DSPP to provide an incremental stream of capital Request for Waiver Plan raised approximately $1.6 million over a two week period ($1.2 million in 2009 and $400 thousand in 2010). See Plan prospectus for additional information |

39 $2.04 $2.18 $2.28 $2.26 $2.87 $1.0 $1.5 $2.0 $2.5 $3.0 2005 2006 2007 2008 2009 Assets Under Management, Administration, Supervision and Brokerage (1) ($ in billions) (1) Excludes Community Banks 2005 - 2007 |

40 $11.5 $12.4 $13.5 $13.8 $14.2 $3 $6 $9 $12 $15 2005 2006 2007 2008 2009 Wealth Management Fees ($ in millions) CAGR: 5.4% (2005 – 2009) |

41 Summary Outstanding franchise in a vibrant, growing market Focus on Wealth Services, Business Banking and Private Banking Investing in growth opportunities today for earnings growth tomorrow Announced acquisition will expand footprint Solid 2010 strategy to succeed in current economic environment |

Thank

You Joseph Keefer, EVP 610- 581- 4869 jkeefer@bmtc.com Duncan Smith, CFO 610- 526 – 2466 jdsmith@bmtc.com Ted Peters, Chairman 610-581-4800 tpeters@bmtc.com Frank Leto, EVP 610-581-4730 fleto@bmtc.com |