Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.1 - AURORA GOLD CORP | ex32_1.htm |

| EX-31.1 - EXHIBIT 31.1 - AURORA GOLD CORP | ex31_1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

x

|

ANNUAL

REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31,

2008

|

|

o

|

TRANSITION

REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM ____ TO

____

|

|

|

Commission

file number

|

0-24393

|

AURORA

GOLD CORPORATION

(Exact

Name of registrant as specified in its charter)

|

Delaware

|

13-3945947

|

|

(State

or other jurisdiction of incorporation or organization)

|

(I.R.S.

Employer Identification No.)

|

|

Baarerstrasse

10, 1st

Floor, Zug, Switzerland

|

6300

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

Registrant’s

telephone number, including area

code (+41) 7887-96966

Securities

registered under Section 12(b) of the Exchange Act:

None

Securities

registered under Section 12 (g) of the Exchange Act:

|

Common

stock, par value $0.001 per share

|

Pink

Sheets

|

|

Title

of each class

|

Name

of each exchange on which

registered

|

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.

o Yes

x No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.

o Yes

x No

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

x Yes

o

No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Website, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files).

x Yes

o

No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K.

o Yes

x

No

1

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company.

See the definitions of “large accelerated filer”, “accelerated filer” and

“smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large

accelerated filer: r

|

Accelerated

Filer: r

|

|

Non-accelerated

filer: r (Do not check if a smaller

reporting company)

|

Smaller

reporting company: þ

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act).

o Yes

x No

State the

aggregate market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the common equity was

sold, or the average bid and asked price of such common equity, as of the last

business day of the registrant’s most recently completed second fiscal

quarter.

$4,817,969

as of June 30, 2008

Indicate

the number of shares outstanding of each of the issuer’s classes of common

equity, as of the latest practicable date: 66,491,855 shares of Common Stock

were outstanding as of January 21, 2010.

2

PART

I

BUSINESS

This

annual report contains statements that plan for or anticipate the future and are

not historical facts. In this Report these forward looking statements are

generally identified by words such as “anticipate,” “plan,” “believe,” “expect,”

“estimate,” and the like. Because forward-looking statements involve future

risks and uncertainties, these are factors that could cause actual results to

differ materially from the estimated results. These risks and uncertainties are

detailed in Item 1. “Description of Business,” Item 2. “Description of

Properties,” Item 7. “Management’s Discussion and Analysis or Plan of

Operation,” Item 8. “Financial Statements” and Item. 13 “Certain Relationships

and Related Transactions and Director Independence”.

The

Private Securities Litigation Reform Act of 1995, which provides a “safe harbor”

for such statements, may not apply to this Report.

|

Item

1.

|

Description

of Business

|

Business

Development

We were

incorporated under the laws of the State of Delaware on October 10, 1995, under

the name "Chefs Acquisition

Corp." Initially formed for the purpose of engaging in the food

preparation business, we redirected our business efforts in late 1995 following

a change of control, which occurred on October 30, 1995, to the acquisition,

exploration and, if warranted, the development of mineral resource properties.

We changed our name to “Aurora

Gold Corporation” on August 20, 1996 to more fully reflect our resource

exploration business activities.

Our

general business strategy is to acquire mineral properties either directly or

through the acquisition of operating entities. Our continued

operations and the recoverability of mineral property costs is dependent upon

the existence of economically recoverable mineral reserves, confirmation of our

interest in the underlying properties, our ability to obtain necessary financing

to complete the development and upon future profitable production.

Since

1996 we have acquired and disposed of a number of properties. We have not been

successful in any of our exploration efforts to establish reserves on any of the

properties that we owned or in which we have or have had an

interest.

We

currently have interest in four (4) properties none of which contain any

reserves. Please refer to “Description of Properties.” We

have no revenues, have sustained losses since inception, have been issued a

going concern opinion by our auditors and rely upon the sale of our securities

to fund operations. We will not generate revenues even if any of our exploration

programs indicate that a mineral deposit may exist on our properties.

Accordingly, we will be dependent on future financings in order to maintain our

operations and continue our exploration activities.

We have

not been involved in any bankruptcy, receivership or similar

proceedings.

Our

Principal Products and Their Markets

We are a

junior mineral exploration company. Our strategy is to concentrate our

investigations into: (i) existing operations where an infrastructure already

exists; (ii) properties presently being developed and/or in advanced stages of

exploration which have potential for additional discoveries; and (iii)

grass-roots exploration opportunities.

3

We are

currently concentrating our property exploration activities in Brazil and

Canada. We are also examining data relating to the potential acquisition of

other exploration properties in the USA, Latin America and South

America.

Our

properties are in the exploration stage only and are without a known body of

mineral reserves. Development of the properties will follow only if satisfactory

exploration results are obtained. Mineral exploration and development involves a

high degree of risk and few properties that are explored are ultimately

developed into producing mines. There is no assurance that our

mineral exploration and development activities will result in any discoveries of

commercially viable bodies of mineralization. The long-term profitability of our

operations will be, in part, directly related to the cost and success of our

exploration programs, which may be affected by a number of factors. Please refer to “Item 1A Risk

Factors”

Significant

Developments in fiscal 2008 and Subsequent Events

For the

year ended December 31, 2008 we recorded exploration expenses of $77,273

compared to $2,033,875 in fiscal 2007. The following is a breakdown of the

exploration expenses by property: Brazil $74,723 (2007 - $2,031,700) and Canada,

Kumealon property $2,550 (2007 - $2,175).

We

initially had 10 properties under Memorandum of Understanding (“MOU”) or under option of which we

currently have retained three (3) properties, São Domingos, São João and

Comandante Araras in the Tapajos Gold Province, State of Pará,

Brazil.

Between

December 21, 2005 and May 26, 2006 we signed four MOUs covering the Piranhas

(option since relinquished) , Branca de Neve (agreement cancelled),

Bigode (option since relinquished) and Santa Lúcia (agreement cancelled)

properties in the Municipality of Itaituba, Tapajos gold province, State of

Para, Brazil. During the first quarter of 2007 we signed a MOU covering the

Comandante Araras property. The MOUs provide us with a review period, ranging

from two months to six months, to access the mineral potential of the

properties.

Between

January 1, 2006 and March 31, 2006 the Company signed five option agreements

covering the Novo Porto, Ouro Mil, Santa Isabel, São Domingos and São João

mineral exploration licenses located in the Municipality of Itaituba, in the

Tapajos gold province of the State of Para, Brazil. The Company relinquished its

options on the Novo Porto and Ouro Mil properties in 2006 and the Santa Isabel

property in 2007.

Access to

all of the property areas in which we have an interest is by airstrips, rivers

in season and the Trans Garimpeiro Highway. Regional infrastructure

to the property areas is serviced from our offices in the city of Itaituba and

the field office located at the Sao Domingos property.

São

Domingos

The São

Domingos property covers an area of 6.100 hectares and is located approximately

250km south of the regional centre of Itaituba and approximately 40 km north of

our previous Santa Isabel property.

São

João

The São

João property area is located approximately 20km west of our São Domingos

property and covers an area of approximately 5.160 hectares.

4

Santa

Isabel – option since relinquished

The Santa

Isabel Property lies in the southwestern region of the Tapajos Gold Province,

Para State, Brazil and comprises an area of 3.650 hectares.

In March

2007 we decided not to follow up our preliminary exploration program on the

Santa Isabel property and have decided not to exercise our option to acquire the

property.

Novo

Porto - option since relinquished

The Novo

Porto property lies approximately 180km south of Itaituba and covered an area of

approximately 6.600 hectares. Due to changes in the Government land

management the area that encompassed the Nova Porto project and our property

interest was deemed to be in a non active commercial mining zone.

In March

2006 we decided not to follow-up our preliminary exploration program on the Novo

Porto property and have decided not to exercise our option to acquire the

property.

Ouro

Mil - option since relinquished

The Ouro

Mil property is located approximately 20 km south of Santa Isabel property area

and approx 300km South of Itaituba, and covers an area of 9.794

hectares.

In

October 2006 we decided not to follow up our preliminary exploration program on

the Ouro Mil property and have decided not to exercise our option to acquire the

property.

Branca de Neve

- option since

relinquished

The

Branca de Neve property adjoins the Piranhas property and is located

approximately 50 km NE of our São Domingos property, and covers an area of

approximately 2.210 hectares

The

Company has decided not to follow up our preliminary exploration program on the

Branca de Neve property and have decided not to exercise our option to acquire

the property.

Piranhas

– option since relinquished

The

Piranhas property adjoins the South western boundary of our Branca de Neve

property and covers an area of approximately 9.341 hectares.

The

Company has decided not to follow up our preliminary exploration program on the

Piranhas property and have decided not to exercise our option to acquire the

property.

Bigode

- option since relinquished

The 4.150

hectare Bigode property adjoins the southeast portion of the São Domingos

property, and is approximately 30 km north of our Santa Isabel

property. The Company has decided not to follow up our preliminary

exploration program on the Bigode property and have decided not to exercise our

option to acquire the property.

Santa

Lúcia - option since

relinquished

The 1.600

hectare Santa Lúcia property is located 1,270 km SSW of the main regional centre

of Itaituba. The property is located 10 km south west of the

Santa Isabel property.

5

The

Company has decided not to follow up our preliminary exploration program on the

Santa Lucia property and have decided not to exercise our option to acquire the

property.

Comandante

Araras

The 2.750

hectare Comandante Araras property is located 10 km west of the São João

property.

British

Columbia, Canada

The 741

acre Kumealon limestone project is located on the north shore of Kumealon Inlet,

54 kilometres south-southeast of Prince Rupert, British Columbia,

Canada.

Subsequent

Events

|

In September 2009,

convertible notes payable and related accrued interest aggregating US

$739,151.69 (AUD $850,479.45) were settled through the issuance of

5,000,000 shares of common stock of the

Company.

|

|

During

the month of September 2009, the Company raised $300,000 through a private

placement of 3,000,000 shares at a price of $0.10 per share. The shares

have not yet been issued. The Company’s agent will be paid a commission of

420,000 shares of common stock of the Company. Proceeds from the private

placement will be used for general working

capital.

|

In

November 2009, the Company signed a letter agreement with Global Minerals

Limited to acquire an initial 70% interest in the Front Range Gold Project

located in Boulder County, Colorado. The Company paid $100,000 on signing the

letter agreement. A further $400,000 is due on signing of the formal agreement

on or before February 28, 2010.

Distribution

Methods of Our Products and Services

We are a

mineral exploration company and are not in the business of distributing any

products or services.

Status

of Any Publicly Announced New Product or Service

We have

no plans for new products or services that we do not already offer.

Competitive

Business Conditions and Our Competitive Position in the Industry and Methods of

Competition

Vast

areas of Brazil have been explored and in some cases staked through mineral

exploration programs. Vast areas also remain unexplored. The cost of

staking and re-staking new mineral claims and the costs of most phase one

exploration programs are relatively modest. Additionally, in many more

prospective areas, extensive literature is readily available with respect to

previous exploration activities. These facts make it possible for a junior

mineral exploration company such as ours to be very competitive with other

similar companies. In effect, we are also competitive with senior companies who

are doing grass roots exploration. In the event our exploration activities

uncover prospective mineral showings, we anticipate being able to attract the

interest of better financed industry partners to assist on a joint venture basis

in more extensive exploration. We are at a competitive disadvantage compared to

established mineral exploration companies when it comes to being able to

complete extensive exploration programs on claims which we hold or may hold in

the future. If we are unable to raise capital to pay for extensive claim

exploration, we will be required to enter into joint ventures with industry

partners which will result in our interest in our claims being substantially

diluted. Currently, we do not have sufficient funds for further

exploration.

6

As long

as management of our company remains committed to building a portfolio of

mineral exploration properties principally through their own efforts, we will be

able to continue operating on modest cash reserves for an extended period of

time. We are one small company in a large competitive industry with many other

junior exploration companies who are evaluating and re-evaluating prospective

mineral properties in Brazil.

Sources

and Availability of Raw Materials and the Names of Principal

Suppliers

As a

mineral exploration company, we do not require sources of raw materials and do

not have principal suppliers in the way which applies to manufacturing

companies. Our raw materials are, in effect, mineral exploration

properties which we may stake or acquire from third parties. Our management team

seeks to assemble a portfolio of quality mineral exploration properties in

Brazil. Initially, we will operate in the field with our president,

Technical director and various consultants on an as needed basis. This

will enable us to assemble a portfolio of properties through grass roots

exploration and staking. We will also acquire new properties through

option agreements where new properties can be acquired on favorable

terms.

Dependence

on One or a Few Major Customers

We are in

the business of mining exploration. We are not selling any product or

service and therefore have no dependence on one or a few major

customers.

Patents,

Trademarks, Licenses, Franchises, Concessions, Royalty Agreements or Labor

Contracts, Including Duration

Our

Company does not own any patents or trademarks. We are not party to any

labor agreements or contracts. Licenses, franchises, concessions and

royalty agreements are not part of our business.

Need

for any government approval of principal products or services

As a

mineral exploration company, we are not in a business which requires extensive

government approvals for principal products or services. The Department

National Production Minerals (DNPM) of Brazil outlines and governs the work that

can be done on mining claims in Brazil.

In the

event mining claims which we acquire in the future prove to host viable ore

bodies, we would likely sell or lease the deposit to a company whose business is

the extraction and treatment of ore. This company would undertake the sale

of metals or concentrates and pay us a net smelter royalty as specified in a

future lease agreement. All responsibility for government approvals

pertaining to mining methods, environmental impacts and reclamation would be the

responsibility of this contractor. All costs to obtain the necessary

government approvals would be factored into technical and viability studies in

advance of a decision being made to proceed with development of an ore

body.

The

mining industry in Brazil is highly regulated. Our president and Technical

director have extensive industry experience and are familiar with government

regulations respecting the initial acquisition and early exploration of mining

claims in Brazil. The Company is required under law to meet government

standards relating to the protection of land and waterways, safe work practices

and road construction. We are unaware of any proposed or probable

government regulations which would have a negative impact on the mining industry

in Brazil. We propose to adhere strictly to the regulatory framework which

governs mining operations in Brazil.

7

Effect

of existing or probable governmental regulations on our business.

Management

is unaware of any existing or probable government regulations which would have a

positive or negative impact on our company's business.

Costs

and effects of compliance with environmental laws (federal, state and

local)

At the

present time, our costs of compliance with environmental laws are minimal.

In the event that claims which we may acquire in the future host a viable

ore body, the costs and affects of compliance with environmental laws will be

incorporated in the exploration plan for these claims. These exploration

plans will be prepared by qualified mining engineers.

Number

of total employees and number of full time employees

As of

January 19, 2009 there were three part time employees.

|

Item

1A.

|

Risk

Factors

|

We

are an exploration stage company and have incurred substantial losses since

inception.

We have

never earned any revenues. In addition, we have incurred net losses of

$13,691,702 for the period from our inception (October 10, 1995) through

December 31, 2008 and, based upon our current plan of operation, we expect that

we will incur losses for the foreseeable future.

Potential

investors should be aware of the difficulties normally encountered by mineral

exploration companies and the high rate of failure of such companies. We are

subject to all of the risks inherent to an exploration stage business

enterprise, such as limited capital mineralized materials, lack of manpower, and

possible cost overruns associated with our exploration programs. Potential

investors must also weigh the likelihood of success in light of any problems,

complications, and delays that may be encountered with the exploration of our

properties.

Because

we are small and do not have much capital, we must limit our exploration

activity. As such we may not be able to complete an exploration program that is

as thorough as we would like. In that event, an existing ore body may go

undiscovered. Without an ore body, we cannot generate revenues and you will lose

your investment.

Because

we do not have any revenues, we expect to incur operating losses for the

foreseeable future.

Our

independent auditors have added an explanatory paragraph to their audit opinion

issued in connection with the consolidated financial statements for the years

ended December 31, 2008 and 2007 relative to our ability to continue as a going

concern. Our ability to obtain additional funding will determine our ability to

continue as a going concern. Our consolidated financial statements do not

include any adjustments that might result from the outcome of this

uncertainty.

We have

never generated revenues and we have never been profitable. Prior to completing

exploration on our mineral properties, we anticipate that we will incur

increased operating expenses without realizing any revenues. We therefore expect

to incur significant losses into the foreseeable future. If we are unable to

generate financing to continue the exploration of our properties, we will fail

and you will lose your entire investment.

8

None

of the properties in which we have an interest or the right to earn an interest

have any known reserves.

We

currently have an interest or the right to earn an interest in four properties,

none of which have any reserves. Based on our exploration activities through the

date of this Form 10-K, we do not have sufficient information upon which to

assess the ultimate success of our exploration efforts. If we do not

establish reserves we may be required to curtail or suspend our operations, in

which case the market value of our common stock may decline and you may lose all

or a portion of your investment.

We have

only completed the initial stages of exploration of our properties, and thus

have no way to evaluate whether we will be able to operate our business

successfully. To date, we have been involved primarily in organizational

activities, acquiring interests in properties and in conducting preliminary

exploration of properties. We have not earned any revenues and have not achieved

profitability as of the date of this Form 10-K.

We

are subject to all the risks inherent to mineral exploration, which may have an

adverse affect on our business operations.

Potential

investors should be aware of the difficulties normally encountered by mineral

exploration companies and the high rate of failure of such enterprises. The

likelihood of success must be considered in light of the problems, expenses,

difficulties, complications and delays encountered in connection with the

exploration of the mineral properties that we plan to undertake. These potential

problems include, but are not limited to, unanticipated problems relating to

exploration and additional costs and expenses that may exceed current estimates.

If we are unsuccessful in addressing these risks, our business will likely fail

and you will lose your entire investment.

We are

subject to the numerous risks and hazards inherent to the mining industry and

resource exploration including, without limitation, the following:

|

|

·

|

interruptions

caused by adverse weather

conditions;

|

|

|

·

|

unforeseen limited sources

of supplies resulting

in shortages of materials, equipment and

availability of

experienced manpower.

|

The

prices and availability of such equipment, facilities, supplies and manpower may

change and have an adverse effect on our operations, causing us to suspend

operations or cease our activities completely.

It

is possible that our title for the properties in which we have an interest will

be challenged by third parties.

We have

not obtained title insurance for our properties. It is possible that

the title to the properties in which we have our interest will be challenged or

impugned. If such claims are successful, we may lose our interest in such

properties.

Our

failure to compete with our competitors in mineral exploration for financing,

acquiring mining claims, and for qualified managerial and technical employees

will cause our business operations to slow down or be suspended.

Our

competition includes large established mineral exploration companies with

substantial capabilities and with greater financial and technical mineralized

materials than we have. As a result of this competition, we may be unable to

acquire additional attractive mining claims or financing on terms we consider

acceptable. We may also compete with other mineral exploration companies in the

recruitment and retention of qualified managerial and technical employees. If we

are unable to successfully compete for financing or for qualified employees, our

exploration programs may be slowed down or suspended.

9

Compliance

with environmental regulations applicable to our operations may adversely affect

our capital liquidity.

All

phases of our operations in Brazil and Canada, where our properties are located,

will be subject to environmental regulations. Environmental

legislation in Brazil and Canada is evolving in a manner which will require

stricter standards and enforcement, increased fines and penalties for

non-compliance, more stringent environmental assessments of proposed projects

and a heightened degree of responsibility for companies and their officers,

directors and employees. It is possible that future changes in environmental

regulation will adversely affect our operations as compliance will be more

burdensome and costly.

Because

we have not allocated any money for reclamation of any of our mining claims, we

may be subject to fines if the mining claims are not restored to its original

condition upon termination of our activities.

Our

executive officers devote and will continue to devote only a limited amount of

time to our business activities.

Mr.

Pearl, our president and chief executive officer is engaged in other business

activities and devotes only a limited amount of his time (approximately 50%) to

our business. As we expand our activities, a need for full time

management may arise. In such an event, should Mr. Pearl be unwilling

to dedicate more of his time to our business or if we fail to hire additional

personnel, our business and results of operations would suffer a material

adverse effect.

Our

directors may face conflicts of interest in connection with our participation in

certain ventures because they are directors of other mineral mineralized

material companies.

Mr.

Montgomery, who serves as a director, may also be a director of other companies

(including mineralized material exploration companies) and, if those other

companies participate in ventures in which we may participate, our directors may

have a conflict of interest in negotiating and concluding terms respecting the

extent of such participation. It is possible that due to our

directors’ conflicting interests, we may be precluded from participating in

certain projects that we might otherwise have participated in, or we may obtain

less favourable terms on certain projects than we might have obtained if our

directors were not also directors of other participating mineral mineralized

materials companies. In an effort to balance their conflicting

interests, our directors may approve terms equally favourable to all of their

companies as opposed to negotiating terms more favourable to us but adverse to

their other companies. Additionally, it is possible that we may not

be afforded certain opportunities to participate in particular projects because

those projects are assigned to our directors’ other companies for which the

directors may deem the projects to have a greater benefit.

Our

future performance is dependent on our ability to retain key personnel, loss of

which would adversely affect our success and growth.

Our

performance is substantially dependent on performance of our senior

management. In particular, our success depends on the continued

efforts of Mr. Pearl. The loss of his services could have a material adverse

effect on our business, results of operations and financial condition as our

potential future revenues would most likely dramatically decline and our costs

of operations would rise. We do not have employment agreements in

place with any of our officers or our key employees, nor do we have key person

insurance covering our employees.

10

The

value and transferability of our shares may be adversely impacted by the limited

trading market for our shares.

There is

only a limited trading market for our common stock on the Pink Sheets. This may

make it more difficult for you to sell your stock if you so desire.

Our

common stock is a penny stock and because "penny stock” rules will apply, you

may find it difficult to sell the shares of our common stock.

Our

common stock is a “penny stock” as that term is defined under Rule 3a51-1 of the

Securities Exchange Act of 1934. Generally, a "penny stock" is a common stock

that is not listed on a national securities exchange and trades for less than

$5.00 a share. Prices often are not available to buyers and sellers and the

market may be very limited. Penny stocks in start-up companies are among the

riskiest equity investments. Broker-dealers who sell penny stocks must provide

purchasers of these stocks with a standardized risk-disclosure document prepared

by the Securities and Exchange Commission. The document provides information

about penny stocks and the nature and level of risks involved in investing in

the penny stock market. A broker must also give a purchaser, orally or in

writing, bid and offer quotations and information regarding broker and

salesperson compensation, make a written determination that the penny stock is a

suitable investment for the purchaser, and obtain the purchaser's written

agreement to the purchase. Consequently, the rule may affect the ability of

broker-dealers to sell our securities and also may affect the ability of

purchasers of our stock to sell their shares in the secondary

market. It may also cause fewer broker dealers to make a market in

our stock.

Many

brokers choose not to participate in penny stock transactions. Because of the

penny stock rules, there is less trading activity in penny stock and you are

likely to have difficulty selling your shares.

In

addition to the "penny stock" rules promulgated by the Securities and Exchange

Commission, FINRA has adopted rules that require that in recommending an

investment to a customer, a broker-dealer must have reasonable grounds for

believing that the investment is suitable for that customer. Prior to

recommending speculative low-priced securities to their non-institutional

customers, broker-dealers must make reasonable efforts to obtain information

about the customer's financial status, tax status, investment objectives and

other information. Under interpretations of these rules, FINRA believes that

there is a high probability that speculative low priced securities will not be

suitable for at least some customers. FINRA requirements make it more difficult

for broker-dealers to recommend that their customers buy our common stock, which

may limit your ability to buy and sell our stock and have an adverse effect on

the market for our shares.

Future

sales of shares by us may reduce the value of our stock.

If

required, we will seek to raise additional capital through the sale of our

common stock. Future sales of shares by us could cause the market

price of our common stock to decline and may result in further dilution of the

value of the shares owned by our stockholders.

|

Item

1B.

|

Unresolved

Staff Comments

|

Not

Applicable.

|

Item

2.

|

Description

of Properties

|

Office

Premises

We

conduct our activities from our principal and technical office located at

Baarerstrasse 10, 1st

Floor, Zug, 6300, Switzerland. These offices are provided to us on a month to

month basis. We believe that these offices are adequate for our

purposes. We do not own any real property or significant assets.

Management believes that this space will meet our needs for the next 12

months.

11

Mining

Properties

Our

properties are in the preliminary exploration stage and do not contain any known

bodies of ore.

We

conduct exploration activities from our principal and technical office located

at Baarerstrasse 10, 1st

Floor, Zug, 6300, Switzerland. The telephone number is (+41)

7887-96966. We believe that these offices are adequate for our

purposes and operations.

Our

strategy is to concentrate our efforts on: (i) existing operations where an

infrastructure already exists; (ii) properties presently being developed and/or

in advanced stages of exploration which have potential for additional

discoveries; and (iii) grass-roots exploration opportunities.

We are

currently concentrating our property exploration activities in Brazil and

Canada. We are also examining data relating to the potential acquisition of

other exploration properties in Latin America, South America.

Our

properties are in the exploration stage only and are without a known body of

mineral reserves. Development of the properties will follow only if satisfactory

exploration results are obtained. Mineral exploration and development involves a

high degree of risk and few properties that are explored are ultimately

developed into producing mines. There is no assurance that our

mineral exploration and development activities will result in any discoveries of

commercially viable bodies of mineralization. The long-term profitability of our

operations will be, in part, directly related to the cost and success of our

exploration programs, which may be affected by a number of factors. Please refer to “Item 1A. Risk

Factors.”

We

currently have an interest in three (3) projects located in Tapajos gold

province in Para State, Brazil and one property located in British Columbia,

Canada. We have conducted only preliminary exploration activities to

date and may discontinue such activities and dispose of the properties if

further exploration work is not warranted.

12

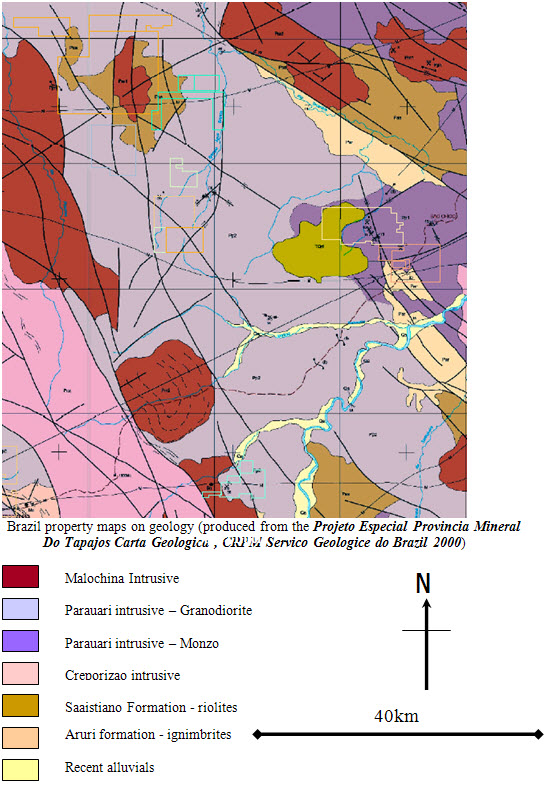

|

Figure

1.

|

Brazil,

South America

|

13

|

Figure

2.

|

Brazil

property maps on geology

|

14

Properties

Between

December 21, 2005 and May 26, 2006 we signed four MOUs covering the Piranhas,

Branca de Neve, Bigode and Santa Lúcia properties in the Municipality of

Itaituba, Tapajos gold province, State of Para, Brazil. During the first quarter

of 2007 we signed a MOU covering the Comandante Araras property. The MOUs

provided us with a review period, ranging from two months to six months, to

access the mineral potential of the properties.

Between

January 1 and March 31, 2006 we signed five option agreements covering the Novo

Porto, Ouro Mil, Santa Isabel, São Domingos and São João mineral exploration

licenses located in the Municipality of Itaituba, in the Tapajos gold province

of the State of Para, Brazil.

Brazil

Memorandum of Understandings, Option

Agreements and Property descriptions:

Piranhas – agreement

cancelled

Location

and access

The

project is located in the mid section of the Tapajos gold province of northern

Brazil, in the state of Para. Access is by light aircraft from the

regional centre of Itaituba, where the company maintains a small administration

centre. Further access is by unsealed roads linking up to the

unsealed Trans Garimpeiro Highway, which links to all national

highways.

Tenure

The

project covers an area of 9.341 hectares and was granted in 1993 and 1996 as

exploration license number 855.892/1996 to 856.289/1996 (Block 1) and 853.597 to

853.638/1993 (Block 2) by the Brazilian National department of Mineral

Production DNPM - Departamento Nacional de Produção Mineral, and expires in

April 2010.

Memorandum

of Understanding

The

Piranhas MOU provided us with a 180 day review period to access the gold

potential of the property. If we decided to proceed with acquiring a 100 percent

interest in the title to the mineral rights then we would have given notice to

the vendors of our intention to acquire title to the mineral rights at least

five days prior to the expiration of the aforementioned period. We would then

have entered into an option agreement with the property vendors for the

Assignment and transfer of the mineral rights.

Option

Agreement

The terms

of the Piranhas option agreement, as specified in the MOU, allowed us to perform

geological surveys and assessment work necessary to ascertain the existence of

possible mineral deposits which may be economically mined and to earn a 100%

interest in the Piranhas project mineral rights via structured cash

payments. The total option agreement payments for the license were

structured as follows:

|

June

30, 2006

|

–

USD $30,000 (paid)

|

|

July

21, 2006

|

–

USD $70,000 (paid and cancelled Block 1);

|

|

July

21, 2007

|

–

USD $120,000 (advanced R$10,000 in September 2007 and subsequently

relinquished option);

|

|

July

21, 2008

|

–

USD $180,000;

|

|

July

21, 2009

|

–

USD $1,600,000

|

|

Total

of USD $2,000,000.

|

|

15

The

vendor would have a 1.5% Net Smelter Royalty. The option agreement could be

terminated at any time upon written notice to the vendor and we would have been

free of any and all payment commitments yet to be due.

The

option agreement has been cancelled.

Geology

The

property is located within the Parauari Intrusive Suite. Limited

lithological inspection has shown the area to host mineralized quartz

veins. The dominant North and NNW structures are thought to represent

relicts of the original mineralizing event. The property is located

approx 50 km east of the Brazauro mineralized materials Corporation’s

Tocantinzinho property.

Branca

de Neve -

agreement cancelled

Location

and access

The

Branca de Neve project is located in mid section of the Tapajos Gold Province

and is accessed by light aircraft from Itaituba and from unsealed 4WD access

from the adjoining Piranhas property. The Transgarimpeiro highway

passes to the south of the property and provides seasonal heavy vehicle

access.

Tenure

The

project covers an area of 2.210 hectares and was granted in 2006 as exploration

license number 850.118/2006 by the Brazilian National department of Mineral

Production DNPM - Departamento Nacional de Produção Mineral, and expires in

2010. The area covering the property has since been incorporated into the

Brazilian government land management scheme which restricts all mining

activity.

Memorandum

of Understanding

The

Branca de Neve MOU provided us with a review period to access the gold potential

of the property. If we decided to proceed with acquiring a 100 percent interest

in the title to the mineral rights then we would have given notice to the

vendors of our intention to acquire title to the mineral rights at least five

days prior to the expiration of the aforementioned period. We would then have

entered into an option agreement with the property vendor for the assignment and

transfer of the mineral rights.

Option

Agreement

The terms

of the Branca de Neve option agreement, as specified in the MOU, allowed us to

perform geological surveys and assessment work necessary to ascertain the

existence of possible mineral deposits which may be economically mined and to

earn a 100% interest in the Branca de Neve property mineral rights via

structured cash payments. The total option agreement payments for the

license were structured as follows:

16

|

April

28, 2006

|

–

R$35,0001

(paid) (approximately USD $14,945 at 12/31/2008)

|

|

October

25, 2006

|

–

R$35,000

(paid) (approximately USD $14,945 at 12/31/2008)

|

|

April

25, 2007

|

–

R$35,000 (approximately USD $14,945 at 12/31/2008) (paid R$5,000 which is

approximately USD $2,135 at 12/31/2008 and cancelled option

agreement);

|

|

October

25, 2007

|

–

R$35,000 (approximately USD $14,945 at 12/31/2008);

|

|

April

25, 2008

|

–

R$35,000 (approximately USD $14,945 at 12/31/2008);

|

|

October

25, 2008

|

–

R$35,000 (approximately USD $14,945 at 12/31/2008);

|

|

April

25, 2009

|

–

R$35,000 (approximately USD $14,945 at 12/31/2008);

|

|

April

25, 2009

|

–

R$500,000 (approximately USD $213,500 at 12/31/2008)

|

|

Total

of R$745,000 (approximately USD $318,115 at

12/31/2008)

|

|

The

vendor would have a 0.75% Net Smelter Royalty. The Royalty payment could be

purchased at any time upon written notice to the vendor and payment of

R$500,000. The option agreement could be terminated at any time upon written

notice to the vendor and we would have been free of any and all payment

commitments yet to be due.

The

option agreement has been cancelled.

Geology

Locally

the Branca de Neve property geology is set in the highly prospective Pararui

Granite Intrusive suite and has a series of brittle deformation

events. North South trending regional faults dominate the property

and are considered to be related to the North West trending regional structures

noted in this area of the Tapajos, which extend from the São Domingos

property. We have completed limited soil sampling and rock chip

exploration. We are currently focusing on other projects which have a

higher current ranking.

Bigode

– agreement cancelled

Location

and access

The

Bigode project is located in the mid east of the Tapajos Gold province and

adjoins to the south east with the Company’s primary project at Sao

Domingo. Access is by light aircraft to the small township at Sao

Domingo and then by 4WD 5km to the target area.

Tenure

The

project covers an area of 4.150 hectares and was granted in 1997 as exploration

license number 751.228/1997 to 751.237/1997 and 755.311/1997 to 755.416/1997 by

the Brazilian National department of Mineral Production DNPM - Departamento

Nacional de Produção Mineral, and expires in 2012.

Memorandum

of Understanding

The

Bigode MOU provided us with a 180 day review period to access the gold potential

of the property. We are no longer negotiating with the property vendor to enter

into an option agreement. If we decided to proceed with acquiring a 100 percent

interest in the title to the mineral rights then we would have given notice to

the vendors of our intention to acquire title to the mineral rights at least

five days prior to the expiration of the aforementioned period. We would then

have entered into an option agreement with the property vendors for the

assignment and transfer of the mineral rights.

|

1

|

“Reals”

is the Brazilian currency. On December 31, 2008 the exchange rate was 1

Real equaled 0.427 US dollar.

|

17

Option

Agreement

The terms

of the Bigode option agreement, as specified in the MOU, allowed us to perform

geological surveys and assessment work necessary to ascertain the existence of

possible mineral deposits which may be economically mined and to earn a 100%

interest in the Bigode property mineral rights via structured cash

payments.

The total

option agreement payments for the license were structured as

follows:

|

October

30, 2006

|

–

USD $60,000 (paid);

|

|

October

30, 2007

|

–

USD $40,000 (paid);

|

|

October

31, 2007

|

–

USD $13,118 (paid);

|

|

January

30, 2008

|

–

USD $40,000 (paid and cancelled option agreement);

|

|

October

30, 2008

|

–

USD $90,000;

|

|

October

30, 2009

|

–

USD $100,000;

|

|

October

30, 2010

|

–

USD $1,000,000

|

|

Total

of USD $1,343,118.

|

|

The

vendor would have a 0.75% Net Smelter Royalty. The Royalty payment could be

purchased at any time upon written notice to the vendor and payment of

USD$500,000. The option agreement could be terminated at any time upon written

notice to the vendor and we would have been free of any and all payment

commitments yet to be due.

The

option agreement has been cancelled.

Geology

The

property is located within the highly prospective Parauari Intrusive Suite,

which is the host of several gold deposits and showings within the Southern

Tapajos. Limited lithological inspection has shown the area is host

to mineralized quartz veins. Similar to the Sao Domingos

property, the dominant North and NNW structures are thought to represent relicts

of the original mineralizing event. Preliminary investigation of the property

area has confirmed the existence of mineralized quartz veins and stockwork

systems within these Intrusive Granite Suites.

We

conducted an initial rock chip sampling program over an area recently being

excavated for free gold in alluvial systems and the weathered granitic

overburden via water canon and sluice. The sample results demonstrate

that the quartz vein systems are highly mineralized and can be traced across the

river valley for at least 200m.

Santa

Lúcia - agreement cancelled

Location

and access

Access to

the property area is by light aircraft direct to the property or by river

utilizing the Surubim River, a tributary of the Tapajos, which connects to the

Amazon and to all major ports and the seaport of Belem. Road access

is by the Trans Garimpeiro Highway via the Trans Amazon highway and ferry river

crossings.

18

Tenure

The

project covers an area of 1.600 hectares and was granted in 1993 as exploration

license number 854.001/1993 to 854.032/1993 by the Brazilian National department

of Mineral Production DNPM - Departamento Nacional de Produção Mineral, and

expires in 2102.

Memorandum

of Understanding

The Santa

Lúcia MOU provided us with a 90 day review period to access the gold potential

of the property. If we decided to proceed with acquiring a 100 percent interest

in the title to the mineral rights then we would have given notice to the

vendors of our intention to acquire title to the mineral rights at least five

days prior to the expiration of the aforementioned period. We would then have

entered into an option agreement with the property vendors for the assignment

and transfer of the mineral rights.

Option

Agreement

The terms

of the Santa Lúcia option agreement, as specified in the MOU, allowed us to

perform geological surveys and assessment work necessary to ascertain the

existence of possible mineral deposits which may be economically mined and to

earn a 100% interest in the Santa Lúcia property mineral rights via structured

cash payments.

The total

option agreement payments for the license were structured as

follows:

|

September

1, 2006

|

–

USD $20,000 (paid and cancelled option agreement);

|

|

March

1, 2007

|

–

USD $50,000;

|

|

March

1, 2008

|

–

USD $60,000;

|

|

March

1, 2009

|

–

USD $70,000;

|

|

September

1, 2009

|

–

USD $500,000

|

|

Total

of USD $700,000.

|

|

The

vendor would have a 1.5% Net Smelter Royalty. The Royalty payment could be

purchased at any time upon written notice to the vendor and payment in Reals

(Brazilian currency) of the equivalent of USD $1,000,000. The option agreement

could be terminated at any time upon written notice to the vendor and we would

have been free of any and all payment commitments yet to be due.

The

option agreement was cancelled.

Geology

Granites

of the Pararui Intrusive Suite, long known to host significant precious metal

mineralisation, dominate the local geology, with occasional later granitic

stocks of the Maloquinha intrusive suite. Sub vertical mineralized

quartz veins with widths from 20 cm to 60 cm strike between 310 and 330,

mimicking the regional structural trend. Recent samples of these

veins assayed between 17 and 25.9 g/t Gold.

Previous

work on the project is limited to alluvial mining of the tributaries of the

Surubim, and many areas of primary mineralization of pyrite associated with gold

have been uncovered as a result.

The

Surubim River Valley, connecting the Santa Lúcia and Santa Isabel properties,

was the focus of intense alluvial mining with an estimated 200,000 m3 of

alluvial material grading greater than 1g/t, with material near the Santa Isabel

border grading up to 3g/t. These figures are more than triple the

grades generally mined by artisanal methods in the Tapajos, suggesting a

high-grade proximal source.

19

Novo

Porto – agreement cancelled

Location

and access

The Nova

Porto property is located in the north eastern area of the Southern Tapajos Gold

Province. Access to the property area is by light aircraft direct to

the property or by river via tributaries of the Tapajos

River. Further access is available on unsealed seasonal

roads.

Tenure

The

project covered an area of 6.600 hectares. The area covering the

property has since been incorporated into the Brazilian government land

management scheme which restricts all mining activity. We have since

not carried on our commitments to the property.

Option

Agreement

The Novo

Porto option agreement allowed us to perform geological surveys and assessment

work necessary to ascertain the existence of possible mineral deposits which may

be economically mined and to earn a 100% interest in the Novo Porto property

mineral rights via structured cash payments.

The total

option agreement payments for the license were structured as

follows:

|

December

25, 2005

|

–

USD $2,500 (paid);

|

|

January

15, 2006

|

–

USD $10,000 (paid);

|

|

May

30, 2006

|

–

USD $37,500;

|

|

May

30, 2007

|

–

USD $50,000;

|

|

May

30, 2008

|

–

USD $75,000;

|

|

May

30, 2009

|

–

USD $1,850,000

|

|

Total

of USD $2,025,000.

|

|

The

agreement was not formally executed until 2006 and the initial payment of $2,500

due December 25, 2005 was not paid until 2006. The option agreement could be

terminated at any time upon written notice to the vendor and we would have been

free of any and all payment commitments yet to be due.

In March

2006 we decided not to follow-up our preliminary exploration program on the Novo

Porto property and have decided not to exercise our option to acquire the

property and the option agreement was cancelled.

Geology

The Novo

Porto property, as noted on the CPRM (Servico Geologico Do Brazil) 1:250,000

geology maps, as a large alluvial area, which has produced gold over an unknown

period. These alluvial workings lie in a NW trending river valley

formed on the faulted contact between the Pararui Intrusive Suite to the west

and the later Maloquinha Intrusive Suite to the west. Else where in

the region the Pararui Intrusive Suite is host to many other gold

deposits.

Ouro

Mil – agreement cancelled

Location

and access

The Ouro

Mil property is located in the south western area of the Southern Tapajos Gold

Province. Access to the property area is by light aircraft direct to

the property or by river via the Surubim River which forms one of the

tributaries of the Tapajos River. Further access is available on

unsealed seasonal roads.

20

Tenure

The

project covers an area of 9.794 hectares and was granted in 1995 and 2006 as

exploration license number 850.011/2006 and 851.867/1995 to 851.921/1995 and

851.252/1995 to 851.265/1995 and 851.273/1995 to 851.276/1995 by the Brazilian

National department of Mineral Production DNPM - Departamento Nacional de

Produção Mineral, and expires in 2012. The area covering the property has since

been incorporated into the Brazilian government land management scheme which

restricts all mining activity. We have since not carried on our

commitments to the property.

Option

Agreement

The Ouro

Mil option agreement allowed us to perform geological surveys and assessment

work necessary to ascertain the existence of possible mineral deposits which may

be economically mined and to earn a 100% interest in the Ouro Mil property

mineral rights via structured cash payments.

The total

option agreement payments for the license were structured as

follows:

|

January

20, 2006

|

–

USD $30,000 (paid);

|

|

July

20, 2006

|

–

USD $70,000 (paid R$15,000, approximately USD $8,481 at 12/31/2007 and

terminated option agreement);

|

|

July

20, 2007

|

–

USD $120,000;

|

|

July

20, 2008

|

–

USD $180,000;

|

|

July

20, 2009

|

–

USD $1,500,000

|

|

Total

of USD $1,900,000.

|

|

The

vendor would have a 1.5% Net Smelter Royalty. The Royalty payment could be

purchased at any time upon written notice to the vendor and payment in Reals

(Brazilian currency) of the equivalent of USD $1,000,000.The option agreement

could be terminated at any time upon written notice to the vendor and we would

have been free of any and all payment commitments yet to be due.

In

October 2006 we decided not to follow up our preliminary exploration program on

the Ouro Mil property and have decided not to exercise our option to acquire the

property and cancelled the option agreement.

Geology

The Ouro

Mil property is situated within a north west trending part of the Creporizao

Intrusive Suite along an E-NE shear subordinate to the NW trending regional

shear of the area. The western margin of this portion of the

Creporizao Intrusive Suite is in a NW faulted contact with the Pararui Intrusive

Suite, and similarly the eastern margin is in a NW faulted contact with the

Cuiu-Cuiu Complex.

Previous

mining at Ouro Mil property, via water canon and a sluice of surficial oxides,

recovered 600kg of gold. The area is dominated by a quartz vein stock

work system in weathered porphyritic granite. A moderately to

well-developed laterite profile exists and is exposed in previous mining areas

around the property.

21

Santa

Isabel – agreement cancelled

Location

and access

The Santa

Isabel property is located in the mid southern area of the Southern Tapajos gold

province. The Santa Isabel property area is accessed by a private

airstrip, and seasonal boat access via a tributary of the Rio Nova, which

eventually empties into the Tapajos River. Road access is by the

Trans Garimpeiro Highway via the Trans Amazon highway and ferry river

crossings.

Tenure

The

project covers an area of 3.650 hectares and was granted in 1994 and 1997 as

exploration license number 850.624/1994 to 850.666/1994 and 854.717/1997 to

854.738/1997 by the Brazilian National department of Mineral Production DNPM -

Departamento Nacional de Produção Mineral, and expires in 2012.

Option

Agreement

The Santa

Isabel option agreement allowed us to perform geological surveys and assessment

work necessary to ascertain the existence of possible mineral deposits which may

be economically mined and to earn a 100% interest in the Santa Isabel property

mineral rights via structured cash payments.

The total

option agreement payments for the license were structured as

follows:

|

February

7, 2006

|

–

USD $25,000 (paid);

|

|

July

21, 2006

|

–

USD $60,000 (paid, Option agreement cancelled)

|

|

July

21, 2007

|

–

USD $80,000;

|

|

July

21, 2008

|

–

USD $100,000;

|

|

July

21, 2009

|

–

USD $1,500,000

|

|

Total

of USD $1,765,000.

|

|

The

vendor would have a 1.5% Net Smelter Royalty. The Royalty payment could be

purchased at any time upon written notice to the vendor and payment in Reals

(Brazilian currency) of the equivalent of USD $1,000,000. The option agreement

could be terminated at any time upon written notice to the vendor and we would

have been free of any and all payment commitments yet to be due.

In March

2007 we decided not to follow up our preliminary exploration program on the

Santa Isabel property and have decided not to exercise our option to acquire the

property and the option agreement was cancelled.

Geology

The

property area is located approximately 50 km south of the São Domingos property

area. The principal property area is situated within the Pararui

Intrusive Suite. To the immediate west the Pararui Suite is in

faulted contact with the later Maloquinha Intrusive Suite, and the Maloquinha

Intrusive suite is in faulted contact with the Creporizao Intrusive Suite,

further to the west. The Pararui Suite and the Creporizao Intrusive

Suite play host to the vast majority of hard rock gold deposits and occurrences

within the Tapajos gold Province.

The

property area is dominated by a series of regional N to NNW trending regional

faults, and these orientations are also noted at mine scale as seen in the

mineralized quartz veins within the property area.

22

Historically

the Santa Isabel property focused mining activities on the alluvial deposits

within the many tributaries, and progressed to include saprolite host rock and

out cropping quartz veins.

São

Domingos

Location

and access

The Sao

Domingos property lies in the Tapajos Province of Para State, Brazil. It is

situated approximately 250 km SE of Itaituba, the regional centre, and includes

an area of nearly 8000 ha. Small aircraft service

Itaituba daily and on this occasion flights were sourced via Manaus. Access from

Itaituba to site is by small aircraft or unsealed road of average to poor

quality. The road is subject to seasonal closures and as the visit was at the

end of the ‘wet’ season site access was granted via light aircraft utilizing the

local airstrip.

Tenure

The

project covers an area of 6.100 hectares and was granted in 1995 as exploration

license number 859.587/1995 and 850.990/1995 to 851.019/1995 by the Brazilian

National department of Mineral Production DNPM - Departamento Nacional de

Produção Mineral, and expires in 2012. These licenses were

restructured by adding further applications and reductions of some areas under

option. Currently the Company has tenure over Processo Nos

850.782/2005, 850.119/2006, 850.684/2006, 859.1995/1995. For ease of

reference please see the map below.

23

Option

Agreement

The São

Domingos option agreement allowed us to perform geological surveys and

assessment work necessary to ascertain the existence of possible mineral

deposits which may be economically mined and to earn a 100% interest in the São

Domingos property mineral rights via structured cash payments. The

Company has since returned the portions of the license under the option

agreement and now has 4 license agreements free from further option

payments.

The

total option agreement payments for the license are structured as

follows:

|

February

7, 2006

|

–

USD $40,500 (paid);

|

|

July

30, 2006

|

–

USD $67,500 (paid);

|

|

July

30, 2007

|

–

USD $112,500 (to be paid on transference of license to

us);

|

|

July

30, 2008

|

–

USD $139,500; (to be paid on transference of license to

us);

|

|

December

30, 2008

|

–

USD $675,000: (to be paid on transference of license to

us);

|

|

Total

of USD $1,035,000.

|

|

The

vendor will have a 2.0% Net Smelter Royalty. The Royalty payment can be

purchased at any time upon written notice to the vendor and payment in Reals of

the equivalent of USD $500,000. The option agreement can be terminated at any

time upon written notice to the vendor and we will be free of any and all

payment commitments yet to be due.

Geology

The

geology of the Sao Domingos property is predominantly composed of

paleo-proterozoic Parauari Granites that play host to a number of gold deposits

in the Tapajos Basin. Typical Granites of the younger Maloquinha Intrusive Suite

have been noticed in the vicinity of Molly Gold Target, and basic rocks

considered to be part of the mesoproterozoic Cachoeira Seca Intrusive Suite

occur around the Esmeril target area.

The São

Domingos property was a previous large alluvial operation, and the property area

covers numerous areas of workings. The Company has outlined four (4) prime

targets, Atacadao, Esmeril, Molly Gold Target and Cachoeira for the São Domingos

drilling project. All targets are located around a series of regional

brittle and ductile structures trending NW, NE and NNW within the Parauari

Intrusive Suite and adjacent to the later Cachoelra (Gabbroic) Intrusive

Suite. The Parauari Intrusive Suite has proven to host the vast

majority of gold deposits elsewhere within the Tapajos Gold

Province. This area has also previously been the focus of large-scale

alluvial workings.

Preliminary

investigation of all four (4) target areas has confirmed the existence of

mineralized quartz veins and stockwork systems within these Intrusive Granite

Suites.

The

Atacadao area is an alluvial system and is the result of gold being shed from

the surrounding granitic topographic highs. These hills are part of

the Pararui Intrusive Suite, and locally contain well-developed mineralized

stock work quartz veins. Numerous production shafts are located on

the flanks of the hills, trending along a major property scale east/west fault

and we are confident of the potential for further mineralisation at depth.

Preliminary investigations proved the local topographic highs to be part of the

Parauari Intrusive Suite with well-developed stock work

quartz. Initial inspection of the quartz veins showed them to be

clearly mineralized and final results of initial sampling confirmed high grades

of gold, up to 42.56g/t Gold with 20g/t silver within the quartz stock

works. Locally, previous shallow, up to 10 meter production shafts

focused on an E-W sub-vertical, project scale brittle structure, which can be

traced for several hundreds of meters, and is thought to link up to the high

grade occurrences at the Molly Gold Target project a distance of approximately 5

km.

24

Esmeril

was the centre of recent mining activity targeting the highly oxidised fraction

of the porphyritic host rock. The stockwork veins, exposed by

previous workers, show boxwork and fresh sulphides and generally associated with

ferruginous staining of both the veins and the enclosing country

rock.

The Molly

Gold Target area was also the centre of a large-scale development of both the

alluvials and oxidised host rocks, using the common water canon and sluice

method. This area is also located on an East - West structure and

further investigations are underway to test if this structure forms part of the

East - West system leading from Atacadao giving a strike potential of several

km. Property scale dominant structures are all generally East

-West.

Within

the project area the main structures strike NE-SW to E-W. Nearly all documented

quartz veins and vein rock zones run parallel to this general tectonic trend

suggesting the mineralisation is frequently related to the fracturing of the

host rocks. Gold, silver, sphalerite, galena, pyrite, chalcopyrite, millerite,

malachite and azurite are common minerals found within the rocks of the project

area.

The Molly

Gold Target lies NNE of Sao Domingos. It consists of a water filled pit that was

created by artisanal miners exploiting an E-W striking qtz vein and adjacent

stockwork system. Water ingress and poor wall stability have beaten local miners

and mining has ceased except for the re-washing of old stockpiles. For this

reason no in-situ samples of vein rocks and alteration envelopes could be taken.

Mineralized rocks of Molly Gold Target are also anomalous in copper and oxidised

specimens show abundant azurite and malachite. Stockpile rock and tailings

samples have yielded gold grades ranging from 2 g/t to 20 g/t.

Diamond

drilling has defined an E-W striking qtz vein over approximately 300m strike

length. It appears that this structure, which is in the order of 0.5 to 1m wide

and hosted within the Parauari Granites, is the core of the mineralized zone at

Molly Gold Target. Around the ‘high grade’ core of qtz veining associated

sulphides and weakly developed stockwork is a ‘low grade’ alteration halo at

Molly Gold Target the degree of mineralization seems to be a direct function of

vein intensity and as the stockwork is poorly developed the associated

mineralization is extremely variable.

São

João – Samba Minerals farm in agreement

In May

2008 the Company signed an agreement with Samba Minerals Limited (“Samba”),

which was subsequently amended in August 2008, whereby Samba can earn up to an

80% participating interest in the São João project by funding exploration

expenditures to completion of a feasibility study on the property. Upon

completion of a feasibility study, the Company will immediately transfer an 80%

participation interest in the property to Samba and enter into a formal joint

venture agreement to govern the development and production of minerals from the

property. Samba can terminate its participation by providing the Company 30 days

notice in writing. Upon withdrawal from its participation, Samba would forfeit

to the Company all of its rights in relation to the project and would be free of

any and all payment commitments yet to be due. Samba will be the manager of the

São João project. A feasibility study has not been completed as of December 31,

2008 and thus no joint venture has been formed as of that date.

Location

and access

The Sao

Joao property is located in the central portion of the Southern Tapajos basin

and is accessed by light aircraft from the regional centre of

Itaituba. Access is also possible by unsealed roads linking up to the

Transgarimpeiro highway and by a purpose cut heavy vehicle access track linking

Sao Joao to the exploration centre at the primary project at Sao

Domingo.

25

Tenure

The

project covers an area of 5.160 hectares and was granted in 1994 and 2005 as

exploration license number 851.533/1994 to 851.592/1994 and 850.091/2005 by

the

Brazilian National department of Mineral Production DNPM - Departamento

Nacional de Produção Mineral, and expires in 2010.

Option

Agreement

The São

João option agreement allows us to perform geological surveys and assessment

work necessary to ascertain the existence of possible mineral deposits which may

be economically mined and to earn a 100% interest in the São João property

mineral rights via structured cash payments.

The total

option agreement payments for the license are structured as

follows:

|

April

12, 2006

|

–

USD $20,000 (paid);

|

|

September

12, 2006

|

–

USD $25,000 (paid);

|

|

September

12, 2007

|

–

USD $60,000 (paid);

|

|

September

12, 2008

|

–

USD $80,000; (paid by Samba Minerals as part of farm in

agreement)

|

|

September

12, 2009

|

–

USD $1,250,000

|

|

Total

of USD $1,435,000.

|

|

The

vendor will have a 1.5% Net Smelter Royalty. The Royalty payment can be

purchased at any time upon written notice to the vendor and payment in Reals

(Brazilian currency) of the equivalent of USD $1,000,000. The option agreement

can be terminated at any time upon written notice to the vendor and we will be

free of any and all payment commitments yet to be due.

Geology

The prime

targets for the São João property are located around and on the intersection of

regional NW and NNW faults within the Pararui Intrusive Suite and this area has

been the focus of large-scale alluvial workings. The Pararui

Intrusive Suite has proven to host the vast majority of gold deposits elsewhere

within the Tapajos Gold Province. We conducted a rock chip program over an area

currently being excavated for gold in quartz systems via shallow underground

workings. The sample results have demonstrated that the quartz vein

systems are highly mineralized and considered continuous for at least

200m. We are confident that the quartz vein systems are much more

extensive and are currently planning to increase the sample density of rock and

soil sampling over, and adjacent to, the current workings to locate further

mineralized vein systems, and to drill test their depth extensions in the near

future.

Previous

mining activity over a number of years focused on the alluvial deposits within

its many tributaries, and has now progressed to include the saprolite host rock

and out cropping quartz veins.

Comandante