Attached files

| file | filename |

|---|---|

| EX-99.1 - PPBI PRESS RELEASE SNL M&A SYMPOSIUM - PACIFIC PREMIER BANCORP INC | ppbi_8k-snlmaconfex991.htm |

| 8-K - PPBI 8-K PRESS RELEASE SNL M&A SYMPOSIUM - PACIFIC PREMIER BANCORP INC | ppbi_8k-snlmaconf.htm |

Exhibit 99.2

Pacific Premier Bancorp, Inc.

SNL M&A Conference

October 2013

Steven R. Gardner

President & Chief Executive Officer

2

Forward-Looking Statements and

Where to Find Additional Information

Where to Find Additional Information

The statements contained in this presentation that are not historical facts are forward-looking statements based on management’s current

expectations and beliefs concerning future developments and their potential effects on Pacific Premier Bancorp, Inc. (the “Company”). Such

statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the Company.

There can be no assurance that future developments affecting the Company will be the same as those anticipated by management. The Company

cautions readers that a number of important factors could cause actual results to differ materially from those expressed in, or implied or projected

by, such forward-looking statements. These risks and uncertainties include, but are not limited to, the following: the strength of the United States

economy in general and the strength of the local economies in which the Company conducts operations; the effects of, and changes in, trade,

monetary and fiscal policies and laws, including interest rate policies of the Board of Governors of the Federal Reserve System; inflation, interest rate,

market and monetary fluctuations; the timely development of competitive new products and services and the acceptance of these products and

services by new and existing customers; the willingness of users to substitute competitors’ products and services for the Company’s products and

services; the impact of changes in financial services policies, laws and regulations (including the Dodd-Frank Wall Street Reform and Consumer

Protection Act) and of governmental efforts to restructure the U.S. financial regulatory system; technological changes; the effect of acquisitions that

the Company has made or may make; changes in the level of the Company’s nonperforming assets and charge-offs; oversupply of inventory and

continued deterioration in values of California real estate, both residential and commercial; the effect of changes in accounting policies and practices,

as may be adopted from time-to-time by bank regulatory agencies, the Securities and Exchange Commission (“SEC”), the Public Company Accounting

Oversight Board, the Financial Accounting Standards Board or other accounting standards setters; possible other-than-temporary impairments of

securities held by the Company; changes in consumer spending, borrowing and savings habits; the effects of the Company’s lack of a diversified loan

portfolio, including the risks of geographic and industry concentrations; ability to attract deposits and other sources of liquidity; changes in the

financial performance and/or condition of the Company’s borrowers; changes in the competitive environment among financial and bank holding

companies and other financial service providers; unanticipated regulatory or judicial proceedings; and the Company’s ability to manage the risks

involved in the foregoing.

expectations and beliefs concerning future developments and their potential effects on Pacific Premier Bancorp, Inc. (the “Company”). Such

statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the Company.

There can be no assurance that future developments affecting the Company will be the same as those anticipated by management. The Company

cautions readers that a number of important factors could cause actual results to differ materially from those expressed in, or implied or projected

by, such forward-looking statements. These risks and uncertainties include, but are not limited to, the following: the strength of the United States

economy in general and the strength of the local economies in which the Company conducts operations; the effects of, and changes in, trade,

monetary and fiscal policies and laws, including interest rate policies of the Board of Governors of the Federal Reserve System; inflation, interest rate,

market and monetary fluctuations; the timely development of competitive new products and services and the acceptance of these products and

services by new and existing customers; the willingness of users to substitute competitors’ products and services for the Company’s products and

services; the impact of changes in financial services policies, laws and regulations (including the Dodd-Frank Wall Street Reform and Consumer

Protection Act) and of governmental efforts to restructure the U.S. financial regulatory system; technological changes; the effect of acquisitions that

the Company has made or may make; changes in the level of the Company’s nonperforming assets and charge-offs; oversupply of inventory and

continued deterioration in values of California real estate, both residential and commercial; the effect of changes in accounting policies and practices,

as may be adopted from time-to-time by bank regulatory agencies, the Securities and Exchange Commission (“SEC”), the Public Company Accounting

Oversight Board, the Financial Accounting Standards Board or other accounting standards setters; possible other-than-temporary impairments of

securities held by the Company; changes in consumer spending, borrowing and savings habits; the effects of the Company’s lack of a diversified loan

portfolio, including the risks of geographic and industry concentrations; ability to attract deposits and other sources of liquidity; changes in the

financial performance and/or condition of the Company’s borrowers; changes in the competitive environment among financial and bank holding

companies and other financial service providers; unanticipated regulatory or judicial proceedings; and the Company’s ability to manage the risks

involved in the foregoing.

Additional factors that could cause actual results to differ materially from those expressed in the forward-looking statements are discussed in the

Company’s 2012 Annual Report on Form 10-K, as amended, filed with the SEC and other filings made by the Company with the SEC. The Company

specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-looking statements

included herein to reflect future events or developments.

Company’s 2012 Annual Report on Form 10-K, as amended, filed with the SEC and other filings made by the Company with the SEC. The Company

specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-looking statements

included herein to reflect future events or developments.

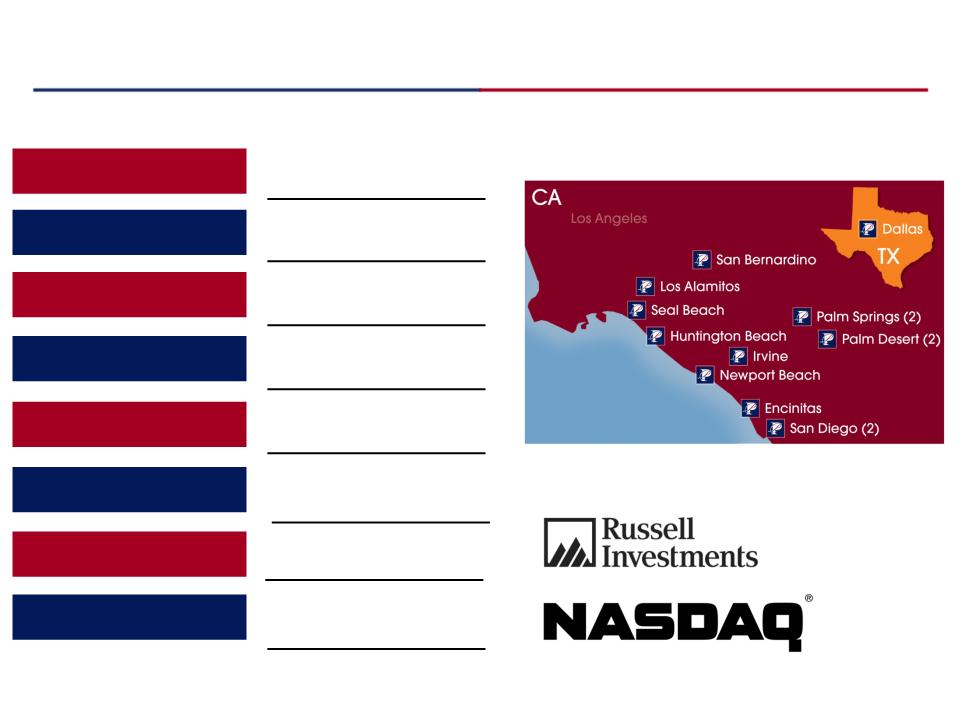

3

13 Full-Service

Branch Locations

Company Profile

Exchange / Listing

NASDAQ: PPBI

Focus

Small & Mid-Market

Businesses

Businesses

Total Assets

$1.6 Billion

Branch Network

Note: Financial information as of the quarter ending 6/30/2013

Note: Market data as of 7/25/2013

Pacific Premier Footprint

Headquarters

Irvine, CA

# of Research Analysts

5 Analysts

Market Cap

$220.5 Million

Avg. Daily Volume

95,231 Shares

4

Where We’ve Been and Where We’re Going

Strategic Plan -

Pre 2008 Stage

• Conversion from a thrift to a commercial banking platform

• Improve deposit base - diversify loan portfolio

• Regimented approach to credit management

Strategic Plan -

Current Stage

• Organic growth driven by high performing sales culture

• Geographic and product expansion through disciplined acquisitions

• Canyon National Bank (CNB) - $209 million in assets at closing on 2/11/2011 (FDIC-Assisted)

• Palm Desert National Bank (PDNB) - $121 million in assets at closing on 4/27/2012 (FDIC-Assisted)

• First Associations Bank (FAB) - $394 million in assets at closing on 3/15/2013 (Whole Bank)

• San Diego Trust Bank (SDTB) - $201 million in assets at closing on 6/25/2013 (Whole Bank)

Strategic Plan -

Next Stage

• Continue to build out commercial banking franchise

• Focus on producing quality EPS growth

• Increase revenue from recurring fee income - government guaranteed lending

• Increase non-interest bearing deposit accounts to over 35% of deposit base

• Balance of organic growth and acquisitive growth

5

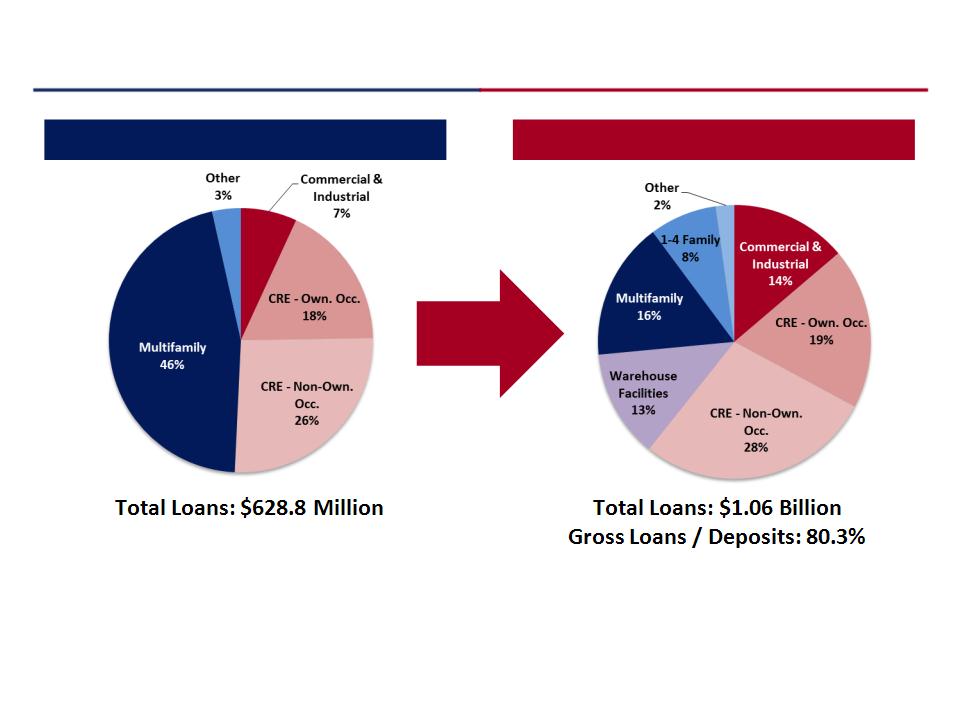

Commercial Bank Transformation - Loan Composition

Loan Composition - 12/31/2008

Loan Composition - 6/30/2013

• Management has significantly transformed the loan portfolio from one with significant real estate

exposure to a more balanced and well-diversified portfolio

exposure to a more balanced and well-diversified portfolio

• Total business loans represent 46% of total loans

Gross Loans / Deposits: 137.5%

6

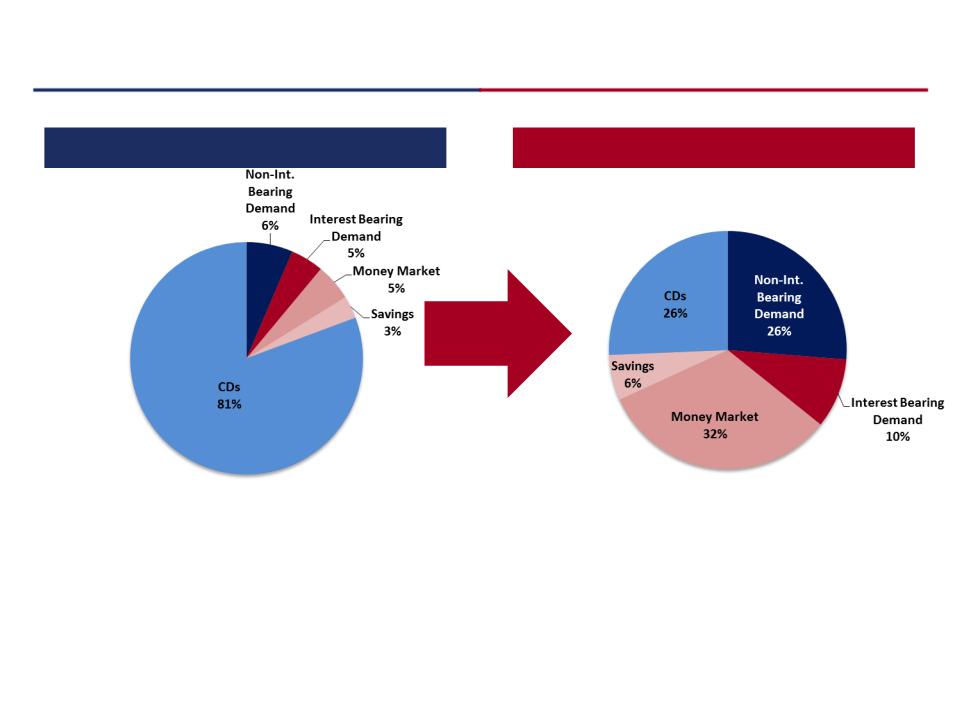

Commercial Bank Transformation - Deposit Composition

Deposit Composition - 12/31/2008

Deposit Composition - 6/30/2013

• 74% of deposits are non-CD deposits

• 26% of deposit balances are non-interest bearing deposits

Total Deposits: $457.1 Million

Cost of Deposits: 3.51%

Total Deposits: $1.3 Billion

Cost of Deposits: 0.35%

7

Acquisition & Integration Strategy

General Acquisition Criteria

Integration Strategy

• Look for strategic, financially compelling and

culturally compatible organizations

culturally compatible organizations

• Favorable markets / demographics

• Business line diversification / cross-sell

opportunity

opportunity

• Disciplined approach to analysis, pricing and

structuring of each transaction

structuring of each transaction

• Realistic cost savings assumptions

• Core customer retention

• Keeping franchise value intact

• Immediately accretive to EPS

• Minimum 15% internal rate of return

• Maximum 10% dilution to tangible book value

per share (Earn-back period of 4 years or less)

per share (Earn-back period of 4 years or less)

• Aggressive approach to timely and effective

integration

integration

• Identify key players that fit into our culture

and who can add value to the organization

and who can add value to the organization

• Immediately meet with new customer base to

begin cross-selling products and services

begin cross-selling products and services

• Aggressive approach to disposition of any

problem assets inherited in a transaction

problem assets inherited in a transaction

• Diligent approach to acquisitive growth and business integration

8

|

|

Canyon

National Bank

|

Palm Desert

National Bank

|

|

Date

|

Feb. 2011

|

Apr. 2012

|

|

|

||

|

Assets (millions)

|

$209

|

$121

|

|

|

||

|

Loans (millions)

|

$150

|

$64

|

|

|

|

|

|

Deposits (millions)

|

$205

|

$116

|

|

|

|

|

|

Bid Discount (millions)

|

($27,920)

|

($32,200)

|

|

|

|

|

|

Bargain purchase gain (millions)

|

$4.2

|

$5.3

|

|

|

||

|

Number of branches

|

3

|

1

|

|

|

||

|

Loss Share

|

No

|

No

|

Acquisition History

The table below presents key metrics of our FDIC assisted deals at each acquisition date.

9

FAB - Business Line Acquisition

• Niche depository focused business model serving HOA management companies

• Substantial synergies with FAB’s deposit platform and PPBI’s commercial banking

model

model

• Liquidity from FAB’s long-term, low-cost core deposits will fund future loan growth

and replace high rate CD runoff

and replace high rate CD runoff

• Minimal credit risk

• Key members of FAB management team retained

• Effective use of capital, enhancing both profitability and shareholder value

10

Transaction Overview - FAB

•Accretive to EPS beginning in 2013

•Tangible book value payback period approximately 2 years (1)

•Internal rate of return (IRR) exceeds cost of capital (>20%) (1)

• Definitive Agreement October 15, 2012

• Regulatory Approval November 30, 2012

• SEC Acceptance of S-4 February 7, 2012

• Transaction Closed March 15, 2013

• $53.2 million payable to FAB common shareholders consisting of approximately

70% cash / 30% PPBI common stock

70% cash / 30% PPBI common stock

• $37.2 million in cash

• $15.9 million in PPBI common stock

• $3.5 million in cash payable to FAB option and warrant holders

• PPB entered into an amendment to FAB’s current Depository Services Agreement

with Associa providing for a five (5) year term

with Associa providing for a five (5) year term

•Price / tangible book value of 117.0% (1)

•Core deposit premium of 2.55% (1)

•Price / earnings (last twelve months, tax adjusted) (1) of 17.2x

(1) As of the transaction announcement on October 15, 2012

Transaction Value:

Consideration Detail:

Significant Dates:

Other Considerations:

Pro Forma Impact:

11

SDTB - Geographic Expansion

• New market entry into San Diego County

• Further improves PPBI’s deposit mix with low-cost core deposits

• Acquiring a profitable and clean bank - minimal credit risk

• Combining PPBI’s product offering with SDBK’s existing customer relationships

• Key bankers of SDBK team retained

12

Transaction Overview - SDTB

Transaction Value:

Consideration Detail:

Significant Dates:

Pro Forma Impact:

•Price / tangible book value 119.0% ( 1)

•Core deposit premium 2.66% (1)

•Price / earnings (last twelve months) (1) 16.9x

•Accretive to earnings per share (EPS) beginning in 2013 (1)

•Tangible book value payback period approximately 2.3 years (1)

•IRR of approximately 15% (1)

• Definitive Agreement March 6, 2013

• Regulatory Approval April 23, 2013

• SEC Approval of S-4 May 8, 2013

• Transaction Closed June 25, 2013

• $29.1 million payable to FAB common shareholders consisting of approximately

50% cash / 50% PPBI common stock

50% cash / 50% PPBI common stock

• $14.4 million in cash

• $14.7 million in PPBI common stock

• $1.8 million in cash payable to SDTB option holders

Other Considerations:

• Strong pro forma capital ratios

(1) As of the transaction announcement on March 6, 2012