Attached files

| file | filename |

|---|---|

| EX-99 - PDF - FIRST MIDWEST BANCORP INC | exhibit99.pdf |

| 8-K - FORM 8-K - FIRST MIDWEST BANCORP INC | nov108k.htm |

Sandler O’Neill

East Coast Financial Services Conference

Aventura, FL

November 10, 2011

2011 First Midwest Bancorp, Inc.

2

Forward Looking Statements &

Additional Information

Additional Information

This presentation may contain, and during this presentation our management may make statements that may

constitute “forward-looking statements” within the meaning of the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements are not historical facts but instead

represent only our beliefs regarding future events, many of which, by their nature, are inherently uncertain and

outside our control. Forward-looking statements include, among other things, statements regarding our

financial performance, business prospects, future growth and operating strategies, objectives and results.

Actual results, performance or developments could differ materially from those expressed or implied by these

forward-looking statements. Important factors that could cause actual results to differ from those in the forward-

looking statements include, among others, those discussed in our Annual Report on Form 10-K, the preliminary

prospectus supplement and other reports filed with the Securities and Exchange Commission, copies of which

will be made available upon request. With the exception of fiscal year end information previously included in the

audited financial statements in our Annual Report on Form 10-K, the information contained herein is unaudited.

Except as required by law, we undertake no duty to update the contents of this presentation after the date of

this presentation.

constitute “forward-looking statements” within the meaning of the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements are not historical facts but instead

represent only our beliefs regarding future events, many of which, by their nature, are inherently uncertain and

outside our control. Forward-looking statements include, among other things, statements regarding our

financial performance, business prospects, future growth and operating strategies, objectives and results.

Actual results, performance or developments could differ materially from those expressed or implied by these

forward-looking statements. Important factors that could cause actual results to differ from those in the forward-

looking statements include, among others, those discussed in our Annual Report on Form 10-K, the preliminary

prospectus supplement and other reports filed with the Securities and Exchange Commission, copies of which

will be made available upon request. With the exception of fiscal year end information previously included in the

audited financial statements in our Annual Report on Form 10-K, the information contained herein is unaudited.

Except as required by law, we undertake no duty to update the contents of this presentation after the date of

this presentation.

The Company’s accounting and reporting policies conform to U.S. generally accepted accounting principles

(“GAAP”) and general practice within the banking industry. As a supplement to GAAP, the Company has

provided non-GAAP performance results. The Company believes that these non-GAAP financial measures are

useful because they allow investors to assess the Company’s operating performance. Although the non-GAAP

financial measures are intended to enhance investors’ understanding of the Company’s business and

performance, these non-GAAP financial measures should not be considered an alternative to GAAP.

(“GAAP”) and general practice within the banking industry. As a supplement to GAAP, the Company has

provided non-GAAP performance results. The Company believes that these non-GAAP financial measures are

useful because they allow investors to assess the Company’s operating performance. Although the non-GAAP

financial measures are intended to enhance investors’ understanding of the Company’s business and

performance, these non-GAAP financial measures should not be considered an alternative to GAAP.

3

First Midwest Presentation Index

Who We Are

Operating Performance

Credit And Capital

Opportunities and Focus

Going Forward

4

Who We Are

5

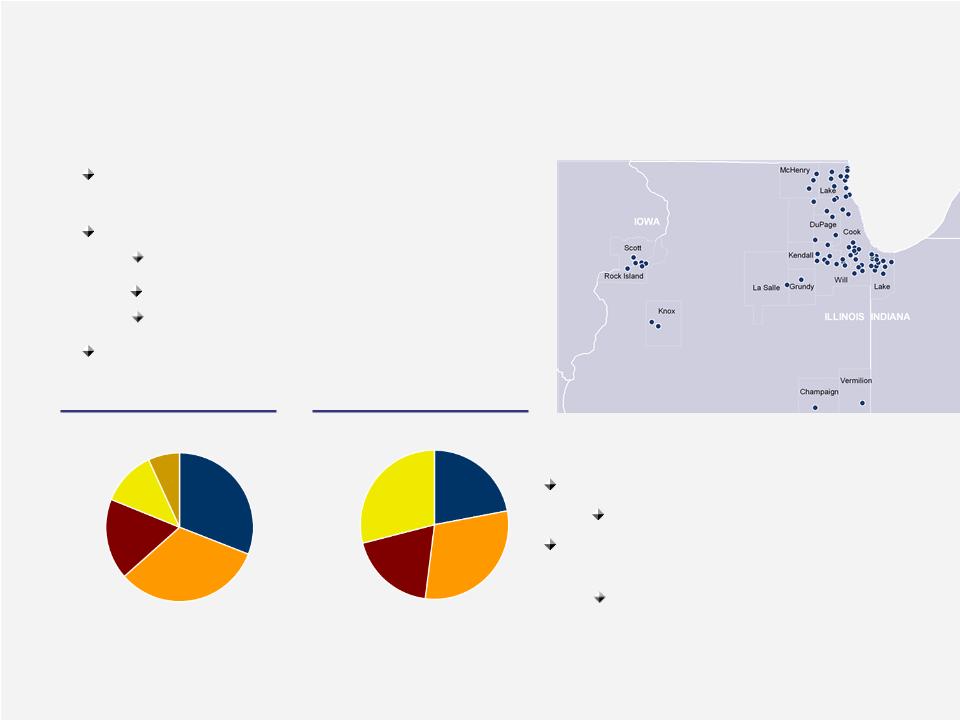

Overview Of First Midwest

Headquartered In Suburban

Chicago

Chicago

$8.4bn Assets

$5.4bn Loans (3)

$6.6bn Deposits

74% Transactional

$4.3bn Trust Assets

Loan Mix

Deposit Mix 2

Highly Efficient Platform

$69mm Of Deposits Per Branch

Leading Market Share In Non-

Downtown Chicago MSA 1

Downtown Chicago MSA 1

#9 In Market Share

$5.4bn

$6.6bn

Note: Information as of 30-September-11.

1 Source: SNL Financial. Non-downtown ranking and market share based on total deposits in Chicago MSA less deposits in the city of Chicago. Data as of 31-Dec-10.

2 Based on quarterly average deposit mix as of 30-Sept-11.

3 Includes $290mm in covered loans stemming from three FDIC-assisted transactions since 30-Sept-09.

Consumer

12%

Commercial

& Industrial

& Industrial

32%

Non Owner

- Occupied

CRE

CRE

32%

Savings &

NOW

NOW

31%

Demand

22%

Money

Market

Market

19%

Time

Deposits

28%

28%

Covered Loans

6%

Owner -

Occupied

CRE 18%

Occupied

CRE 18%

Top 100 Employer, #7 Of 20 Largest

(Only Financial Institution)

6

7

8

Operating Performance

9

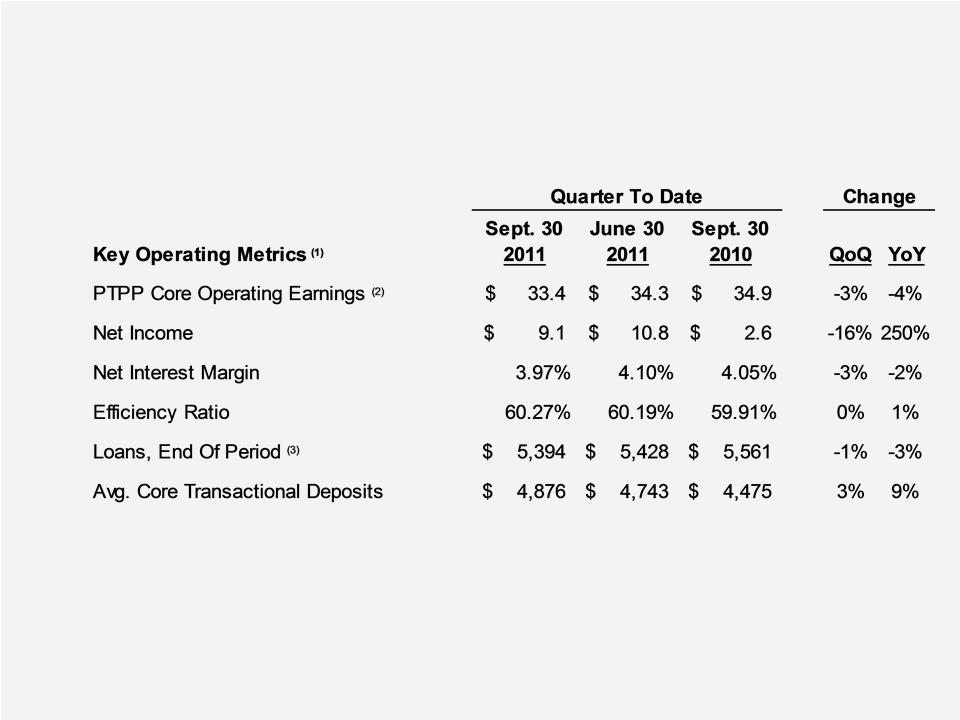

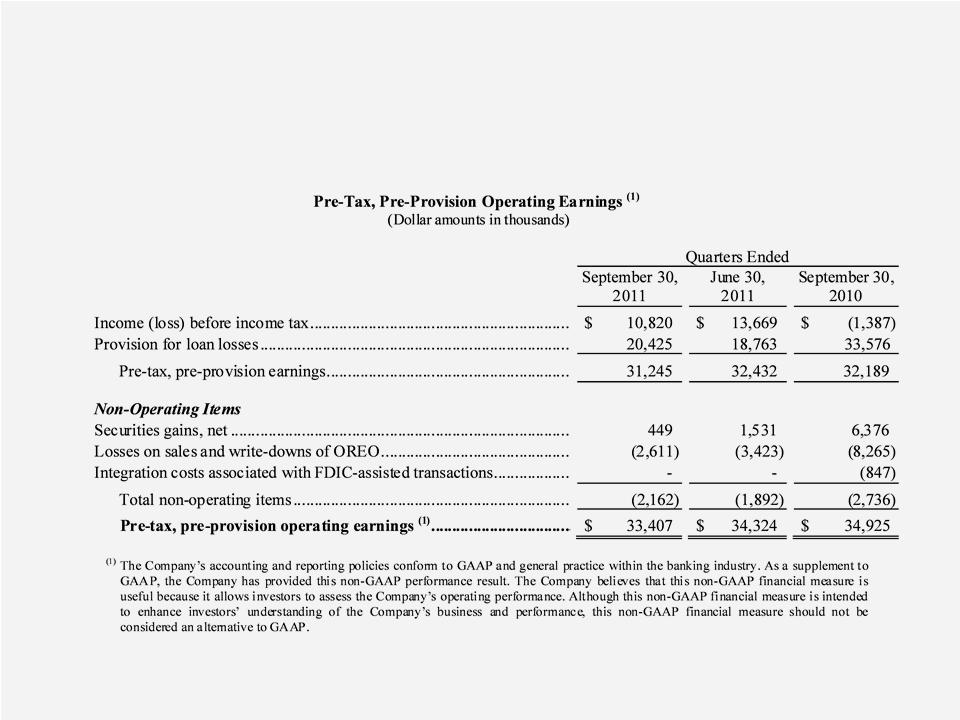

Third Quarter Results

1 Dollar amounts in millions.

2 PTPP represents Pre-Tax, Pre-Provision earnings, which is a non-GAAP financial measure. For reconciliation to GAAP measure, please refer to the appendix.

3 Includes covered loans acquired from FDIC-assisted transactions totaling $290 million, $315 million, and 396 million as of 30-Sept-11, 30-June-11, and 30-Sept-10, respectively.

Stable Earnings, Efficiency, Loans

Notable Growth In Low Cost Deposits

10

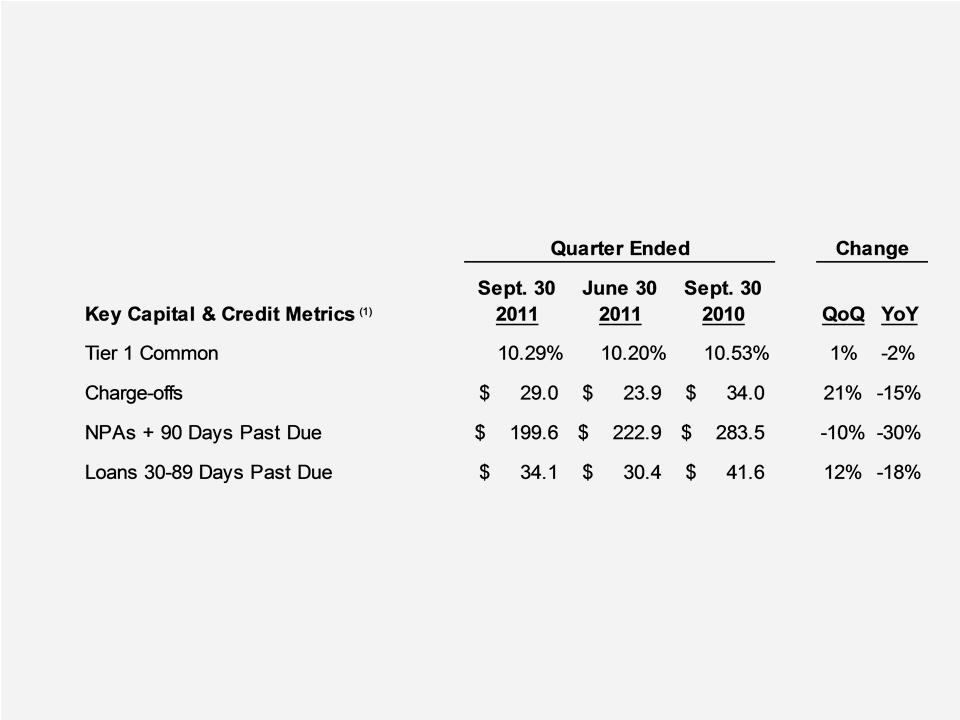

Third Quarter Highlights

Strong Capital Position

Credit Metrics Elevated But Improving

1 Dollar amounts in millions.

11

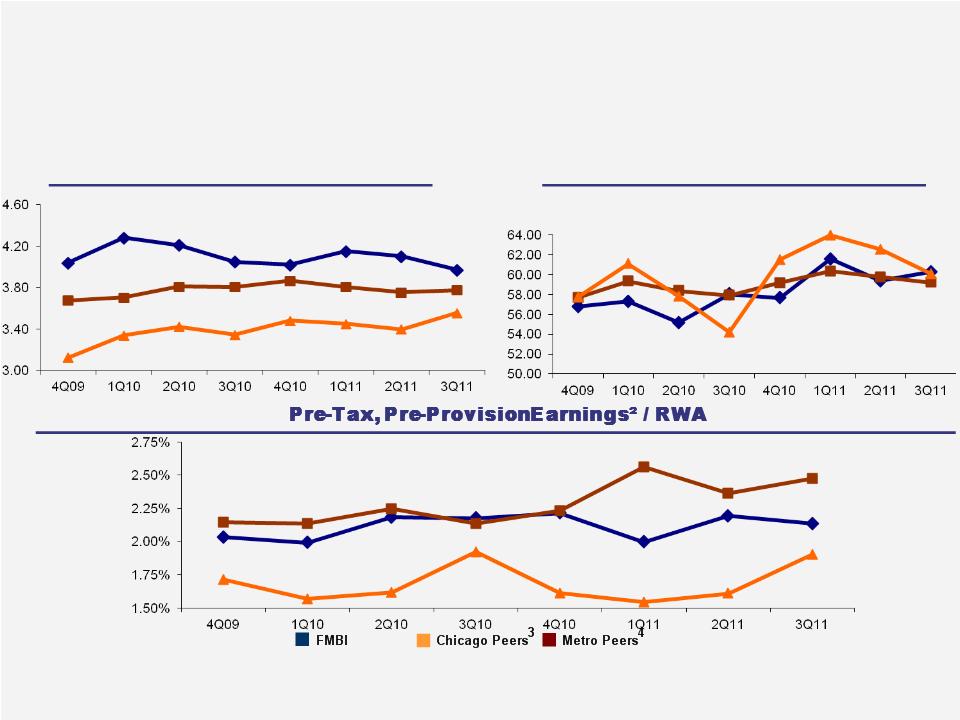

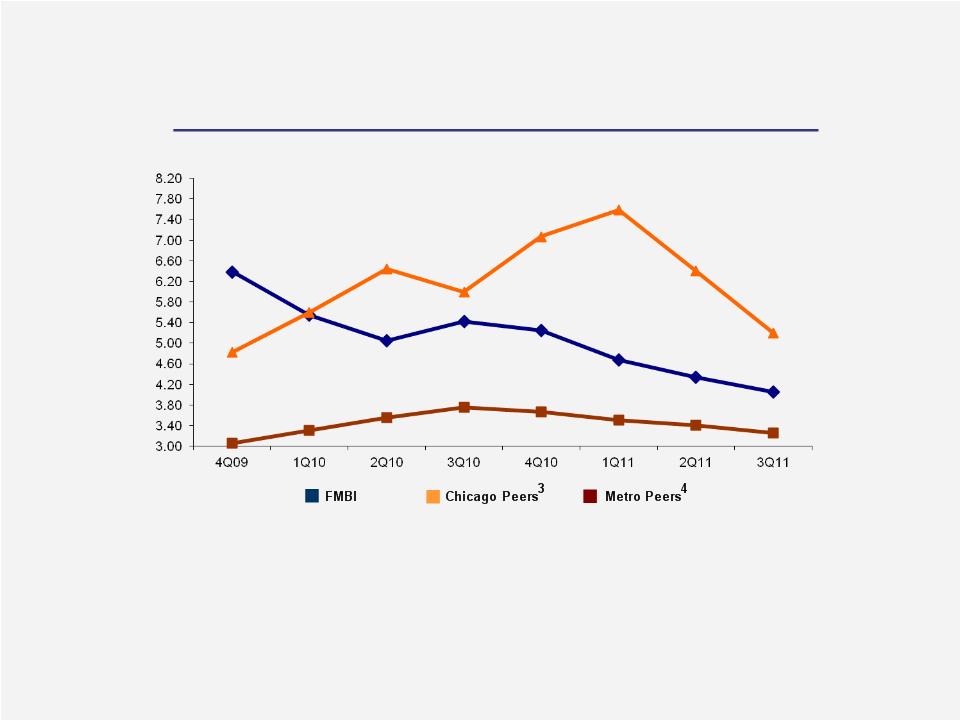

Core Business Is Solid

Source: FMBI based on internal data; peer data from SNL Financial.

¹ Equal to non-interest expense divided by fully taxable equivalent (FTE) net interest income and non-interest income. Excludes nonrecurring items; items sourced from SNL.

² This is a non-GAAP financial measure. For reconciliation to GAAP measure, please refer to the appendix.

³ Chicago Peers based on median of MBFI, OSBC, PVTB, TAYC and WTFC.

4 Metro Peers based on median of CATY, CBSH, CFR, FCF, FMER, FULT, MBFI, ONB, PVTB, SUSQ, UMPQ, VLY, WTFC, and TRMK.

Efficiency Ratio % ¹

Net Interest Margin %

12

Credit & Capital

13

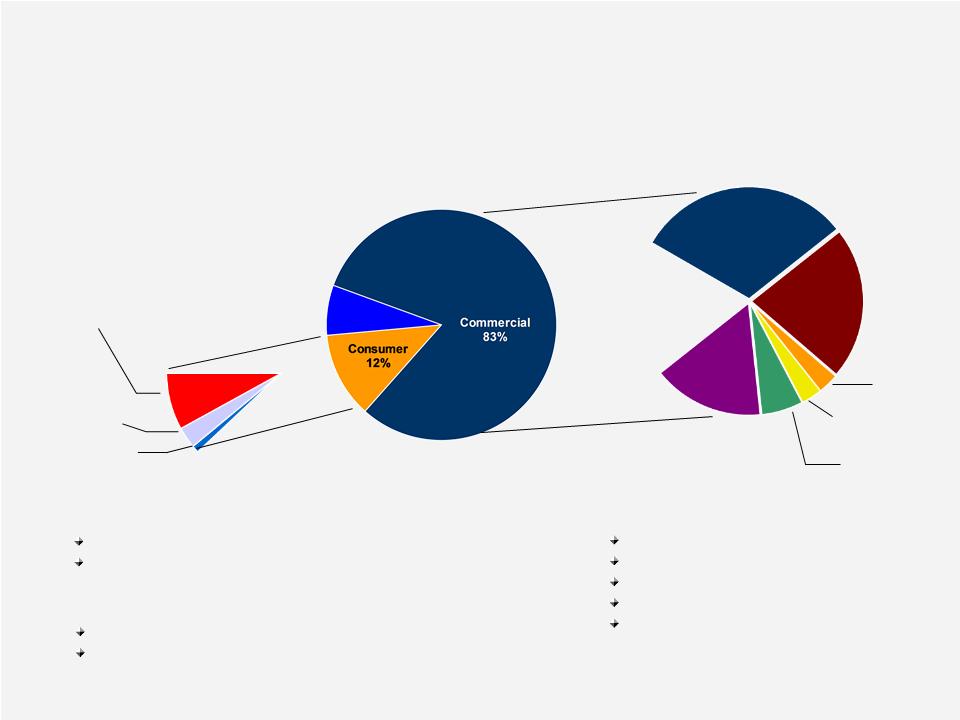

Loan Portfolio Overview

Branch originated

Home equity dominated

~95% in footprint

83% of portfolio, 51% CRE

Diversified + granular

Most have personal guarantees

35% of CRE is owner-occupied

Consumer Loans = $658mm

Home Equity

8%

8%

Other

Consumer

1%

Consumer

1%

C&I

32%

32%

Office,

Retail &

Industrial

24%

Retail &

Industrial

24%

Residential

Construction

2%

Construction

2%

Commercial

Construction &

Land 3%

Construction &

Land 3%

Multi-family

6%

6%

Other CRE

16%

16%

Commercial Loans = $4.74bn

Real Estate - 1- 4

Family

3%

Family

3%

Total Loans = $5.4bn

Note: Loan data as of 30-Sept-11.

Covered 5%

Covered Loans = $290 mm

Performing Better Than Originally Expected

Losses Mitigated By Loss-Share

14

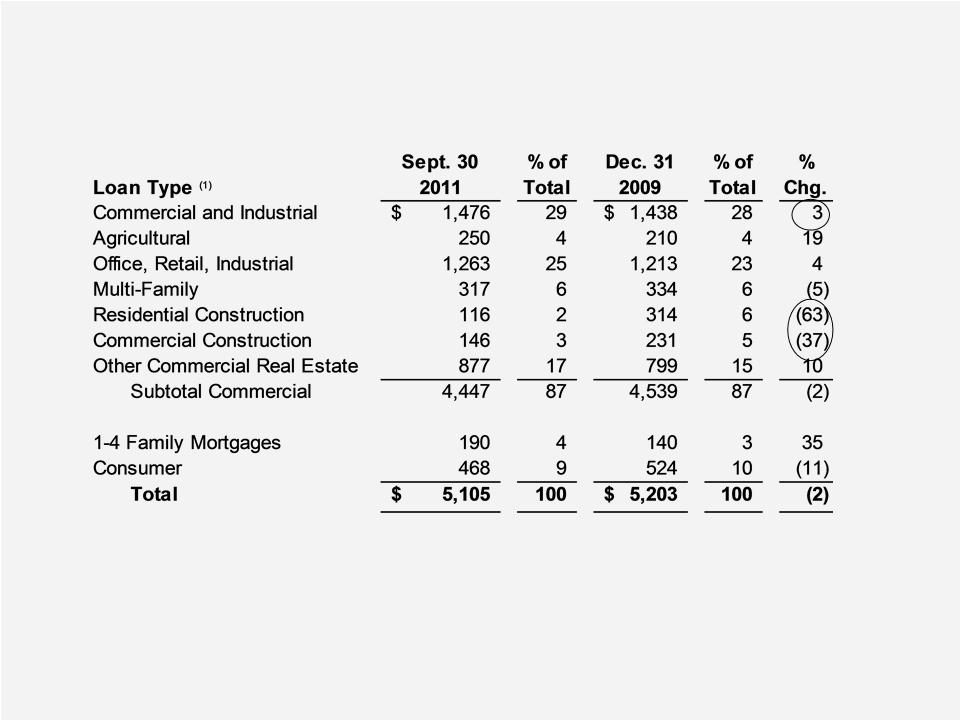

Changing Loan Mix

Note: Excludes covered loans acquired in FDIC-assisted transactions.

Greater Commercial And Owner-Occupied CRE

Reduced Construction, Re-entry To 1-4 Family

1 Dollar amounts in millions.

Non-Performing Asset Trends (1) (2)

Reflects Steady Progress, Influenced

By Disposition Strategy And Market

15

Source: SNL Financial.

¹ Non-performing asset trends are represented as Nonperforming Assets (NPAs) + 90 days past due loans divided by loans plus Real Estate Owned (REO).

² Graph represents problem non-performing asset (NPA) percentage.

³ Chicago Peers based on median of MBFI, OSBC, PVTB, TAYC and WTFC.

4 Metro Peers based on median of CATY, CBSH, CFR, FCF, FMER, FULT, MBFI, ONB, PVTB, SUSQ, UMPQ, VLY, WTFC, and TRMK.

NPA %

16

Addressing Reality of Credit Cycle

Conditions Slowly Improving

Real Estate Lagging

C&D Remains Stressed, Lower Exposure

Continued Focus On Reducing NPA Levels

Adverse Rated Credits Declining

Adjusting Carrying Values To Facilitate Disposition

Pursuing Multiple Strategies

Cash-Flowing Properties Offer Greater Alternatives

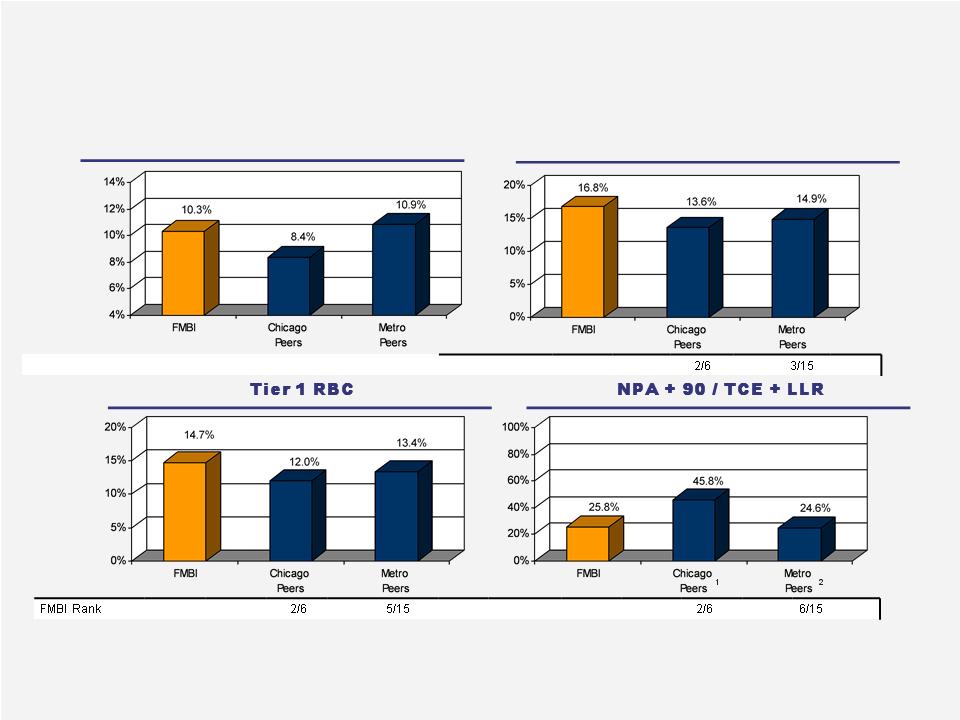

Leading Capital Foundation

First Midwest vs. Peers

First Midwest vs. Peers

Source: Company data and SNL Financial. FMBI as of 30-Sept-11.

1 Chicago Peers based on median of MBFI, OSBC, PVTB, TAYC and WTFC.

2 Metro Peers based on median of CATY, CBSH, CFR, FCF, FMER, FULT, MBFI, ONB, PVTB, SUSQ, UMPQ, VLY, WTFC, and TRMK.

Tier 1 Common

Total Capital

|

FMBI Rank

|

|

|

2/6

|

4/15

|

|

|

1

1

1

2

2

2

17

TARP Redemption

Overview and Rationale

Overview and Rationale

U.S. Treasury, in consultation with our regulators, has approved

redemption of all $193mm of TARP preferred stock

redemption of all $193mm of TARP preferred stock

Expect to fund redemption with cash on hand and proceeds from potential

debt offering(s)

debt offering(s)

Redemption of TARP capital is consistent with strategic priorities and will

allow continued focus on growing core franchise

allow continued focus on growing core franchise

Reflects strong capital position and significant improvement in credit trends

Pro forma for redemption, capital ratios will exceed current and projected

well-capitalized guidelines on standalone basis and under stress scenarios

well-capitalized guidelines on standalone basis and under stress scenarios

18

19

Opportunities & Focus

20

Continued Business Investment

Strengthening Sales

Asset-Based Lending

Mortgage Sales Platform

Wealth Management

Cash Management

Retail Product Offering

Expanding Distribution And Reach

Market Entry

Downtown Chicago, DuPage

Upgrading Internet Platform

Targeting Efficiency

Market Disruption

Environment Creates Opportunities

In Greater Chicago Area

~ 30 Failures Since Start Of 2009

Well Positioned To Benefit

Strong Capital Position

Solid Reputation: In Marketplace 70+ Years

Tenured Sales Force

Experienced Management

Successful Acquisition Growth(1)

Strategically and Financially Accretive

|

|

Date

|

Deposits (2)

|

Core (3)

|

Loans (2)

|

|

First DuPage

|

4Q09

|

$ 232

|

26%

|

$ 212

|

|

Peotone Bank And Trust

|

2Q10

|

84

|

73%

|

53

|

|

Palos Bank And Trust

|

3Q10

|

462

|

47%

|

297

|

|

Total

|

|

$ 778

|

|

$ 562

|

(1) Information as of acquisition date

(2) Dollars in millions

(3) Core comprised of demand, NOW, money market, and savings

(4) As of 30-Sept-11

In Total, Added 8 Locations, 25,000 Households,

Generated Pre-Tax Gain of $17 Million,

Retained Over 90% of Core Deposits (4)

22

23

Acquisition Opportunities

Selective Criteria

Ability To Strengthen The Company

Leverages Our Skills

Local Market Knowledge

Core Competency

Experienced And Successful Acquirer

7 Deals, $2.7bn Since 2003

FDIC-Assisted Deals Becoming More Competitive

Deals Likely Smaller

Eventual Shift From Assisted To Unassisted

24

Deposit-Only Acquisition

$185 Million In Deposits, 50% Core

In-Market Acquisition

Single Branch

Deal Price

Set At Close

Core Deposits Only

December 2011 Close

25

Going Forward

26

Positioning For Long-Term Success

Investing In Sales Organization

Lending Platform

Wealth Management

Market Expansion

Increasing Efficiency

Transitioning To Improved Credit

Investing In And Leveraging Technology

Improving Credit, Significant Capital

27

Why First Midwest

Premier Community Banking Franchise

Working Through Cycle

Solid Capital; Liquidity

Experienced Management Team

Market Opportunities Available

Positioned For Long-term Success

28

Questions?

29

30

Appendix

31

Reconciliation of Non-GAAP Measures