Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FLUSHING FINANCIAL CORP | ffic-20210506x8k.htm |

Exhibit 99.1

| “Small Enough To Know You. Large Enough To Help You.” D.A. Davidson Investor Presentation May 6, 2021 “Small Enough To Know You. Large Enough To Help You.” |

| Safe Harbor Statement “Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995: Statements in this Presentation relating to plans, strategies, economic performance and trends, projections of results of specific activities or investments and other statements that are not descriptions of historical facts may be forward- looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking information is inherently subject to risks and uncertainties, and actual results could differ materially from those currently anticipated due to a number of factors, which include, but are not limited to, risk factors discussed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2020 and in other documents filed by the Company with the Securities and Exchange Commission from time to time. Forward- looking statements may be identified by terms such as “may”, “will”, “should”, “could”, “expects”, “plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”, “forecasts”, “goals”, “potential” or “continue” or similar terms or the negative of these terms. Although we believe that the expectations reflected in the forward- looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. The Company has no obligation to update these forward-looking statements. 2 |

| Key Messages Conservative Underwriting with History of Solid Value Creation 3 |

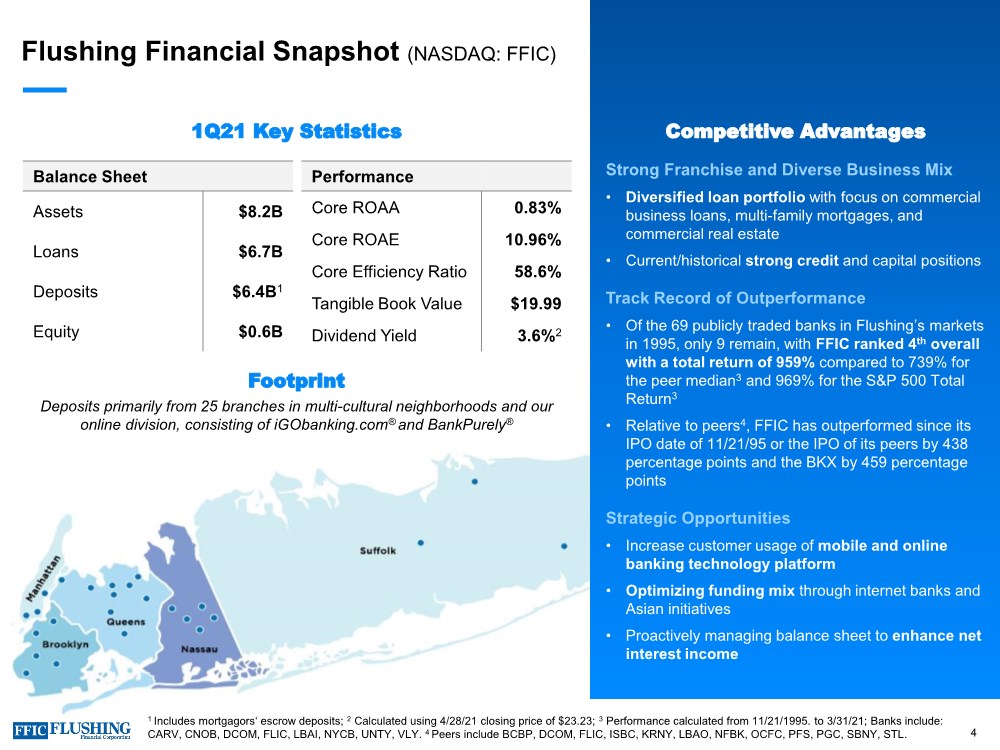

| Flushing Financial Snapshot (NASDAQ: FFIC) Competitive Advantages Balance Sheet Assets $8.2B Loans $6.7B Deposits $6.4B1 Equity $0.6B Performance Core ROAA 0.83% Core ROAE 10.96% Core Efficiency Ratio 58.6% Tangible Book Value $19.99 Dividend Yield 3.6%2 1Q21 Key Statistics Footprint Deposits primarily from 25 branches in multi-cultural neighborhoods and our online division, consisting of iGObanking.com® and BankPurely® 1 Includes mortgagors‘ escrow deposits; 2 Calculated using 4/28/21 closing price of $23.23; 3 Performance calculated from 11/21/1995. to 3/31/21; Banks include: CARV, CNOB, DCOM, FLIC, LBAI, NYCB, UNTY, VLY. 4 Peers include BCBP, DCOM, FLIC, ISBC, KRNY, LBAO, NFBK, OCFC, PFS, PGC, SBNY, STL. 4 Strong Franchise and Diverse Business Mix • Diversified loan portfolio with focus on commercial business loans, multi-family mortgages, and commercial real estate • Current/historical strong credit and capital positions Track Record of Outperformance • Of the 69 publicly traded banks in Flushing’s markets in 1995, only 9 remain, with FFIC ranked 4th overall with a total return of 959% compared to 739% for the peer median3 and 969% for the S&P 500 Total Return3 • Relative to peers4, FFIC has outperformed since its IPO date of 11/21/95 or the IPO of its peers by 438 percentage points and the BKX by 459 percentage points Strategic Opportunities • Increase customer usage of mobile and online banking technology platform • Optimizing funding mix through internet banks and Asian initiatives • Proactively managing balance sheet to enhance net interest income |

| 13% of Total Deposits $28.3B Market Potential (~3% Market Share) 7.0% FFIC 5 Year CAGR vs 5.7% for the Comparable Asian Markets Asian Communities – Total Loans $690MM and Deposits $850M Multilingual Branch Staff Serves Diverse Customer Base in NYC Metro Area Growth Aided by the Asian Advisory Board Sponsorships of Cultural Activities Support New and Existing Opportunities Strong Asian Banking Market Focus 5 |

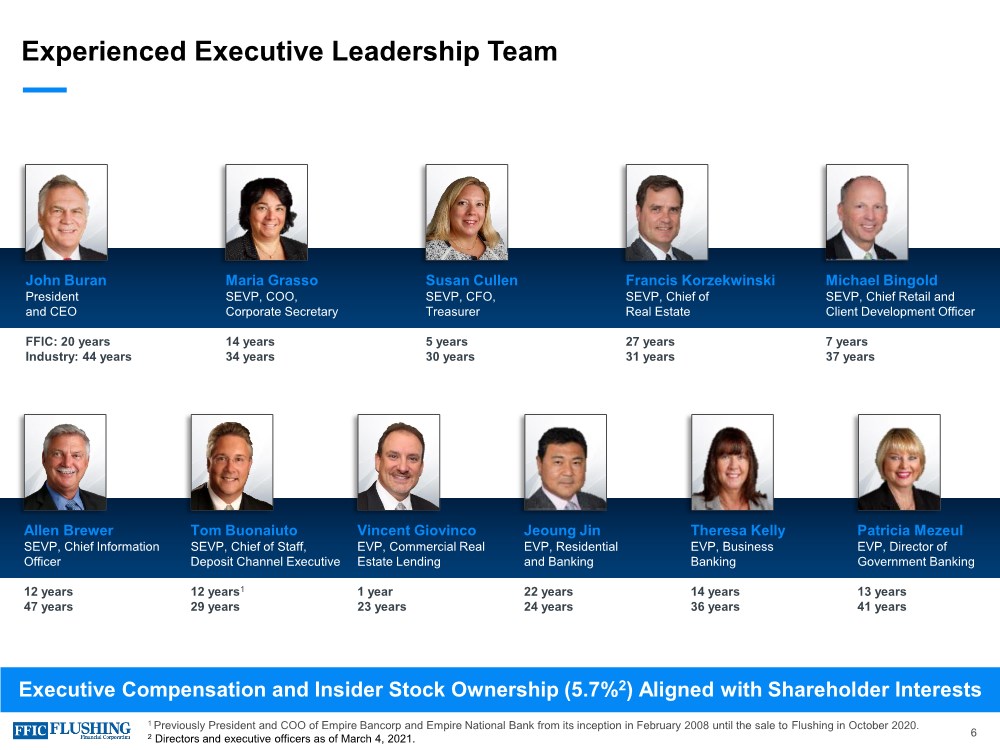

| Experienced Executive Leadership Team Executive Compensation and Insider Stock Ownership (5.7%2) Aligned with Shareholder Interests John Buran President and CEO Maria Grasso SEVP, COO, Corporate Secretary Susan Cullen SEVP, CFO, Treasurer Francis Korzekwinski SEVP, Chief of Real Estate Michael Bingold SEVP, Chief Retail and Client Development Officer FFIC: 20 years Industry: 44 years 14 years 34 years 5 years 30 years 27 years 31 years 7 years 37 years Allen Brewer SEVP, Chief Information Officer Tom Buonaiuto SEVP, Chief of Staff, Deposit Channel Executive Vincent Giovinco EVP, Commercial Real Estate Lending Jeoung Jin EVP, Residential and Banking Theresa Kelly EVP, Business Banking Patricia Mezeul EVP, Director of Government Banking 12 years 47 years 12 years1 29 years 1 year 23 years 22 years 24 years 14 years 36 years 13 years 41 years 1 Previously President and COO of Empire Bancorp and Empire National Bank from its inception in February 2008 until the sale to Flushing in October 2020. 2 Directors and executive officers as of March 4, 2021. 6 |

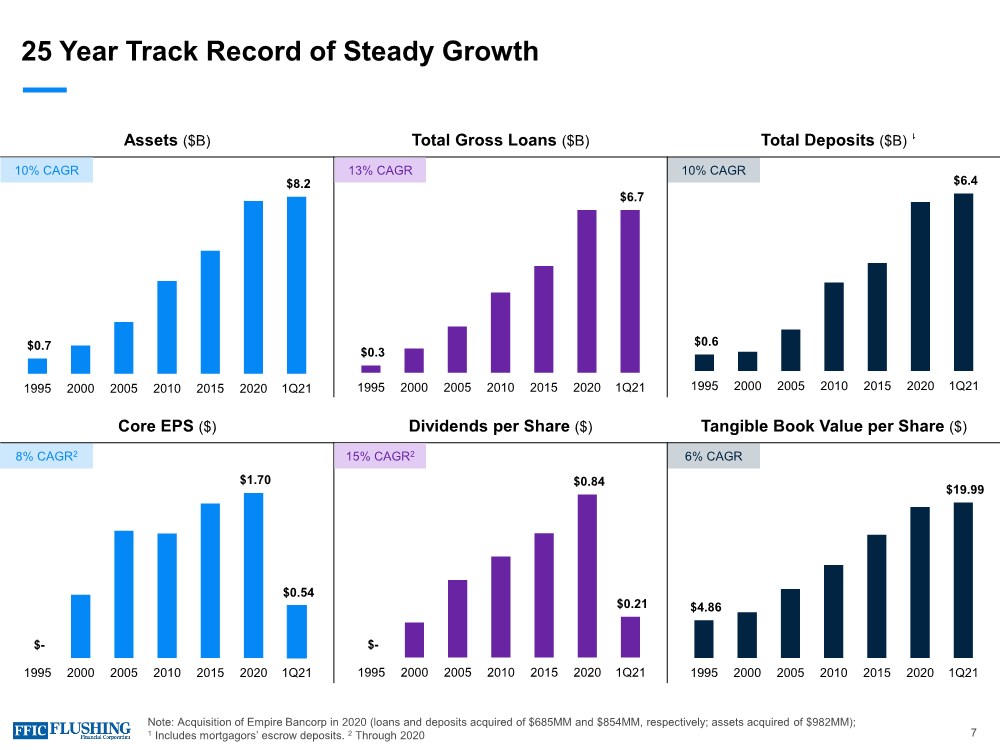

| Core EPS ($) Dividends per Share ($) Tangible Book Value per Share ($) Assets ($B) Total Gross Loans ($B) Total Deposits ($B) $- $0.84 $0.21 1995 2000 2005 2010 2015 2020 1Q21 $- $1.70 $0.54 1995 2000 2005 2010 2015 2020 1Q21 $0.6 $6.4 1995 2000 2005 2010 2015 2020 1Q21 $0.3 $6.7 1995 2000 2005 2010 2015 2020 1Q21 $0.7 $8.2 1995 2000 2005 2010 2015 2020 1Q21 10% CAGR 10% CAGR 25 Year Track Record of Steady Growth Note: Acquisition of Empire Bancorp in 2020 (loans and deposits acquired of $685MM and $854MM, respectively; assets acquired of $982MM); 1 Includes mortgagors’ escrow deposits. 2 Through 2020 1 13% CAGR 8% CAGR2 15% CAGR2 $4.86 $19.99 1995 2000 2005 2010 2015 2020 1Q21 6% CAGR 7 |

| Continued Strong Execution in 1Q21 • Core EPS up 184% YoY ‒ Fourth Consecutive Quarter of Record NII ‒ Core NIM expansion of 3 bps QoQ ‒ Core PPNR rose 79% YoY; 6% QoQ ‒ 11% Core ROAE • Loan Growth from PPP; Pipeline Increases ‒ 2.6% annualized loan growth in 1Q21; PPP loan balances of $251 million ‒ $123 million of PPP originations and assisting customers on nearly $50 million of lifetime PPP forgiveness ‒ Loan pipeline rose 15.9% YoY to $376MM • Solid Credit Quality Continues ‒ Flat NPA QoQ; Criticized and classified assets decrease 12% QoQ ‒ NCOs of 17 bps, 16 bps from charge-off of remaining taxi medallion portfolio ‒ Coverage ratio over 200% • Strong Deposit Growth; Mix Improves ‒ Average deposits rose 23% YoY; approximately 8% excluding Empire ‒ Average non-interest bearing deposits rose 91% YoY ‒ Core deposits 83% of average deposits (including escrow deposits) • Tangible Book Value of $19.99 with a 3.6%1 Dividend Yield 1 Calculated using 4/28/21 closing price of $23.23. 8 |

| Strategic Objectives ENSURE appropriate risk- adjusted returns for loans while optimizing cost of funds MAINTAIN strong historical loan growth ENHANCE core earnings power by improving scalability and efficiency MANAGE Asset quality with consistently disciplined underwriting 1 2 3 4 9 |

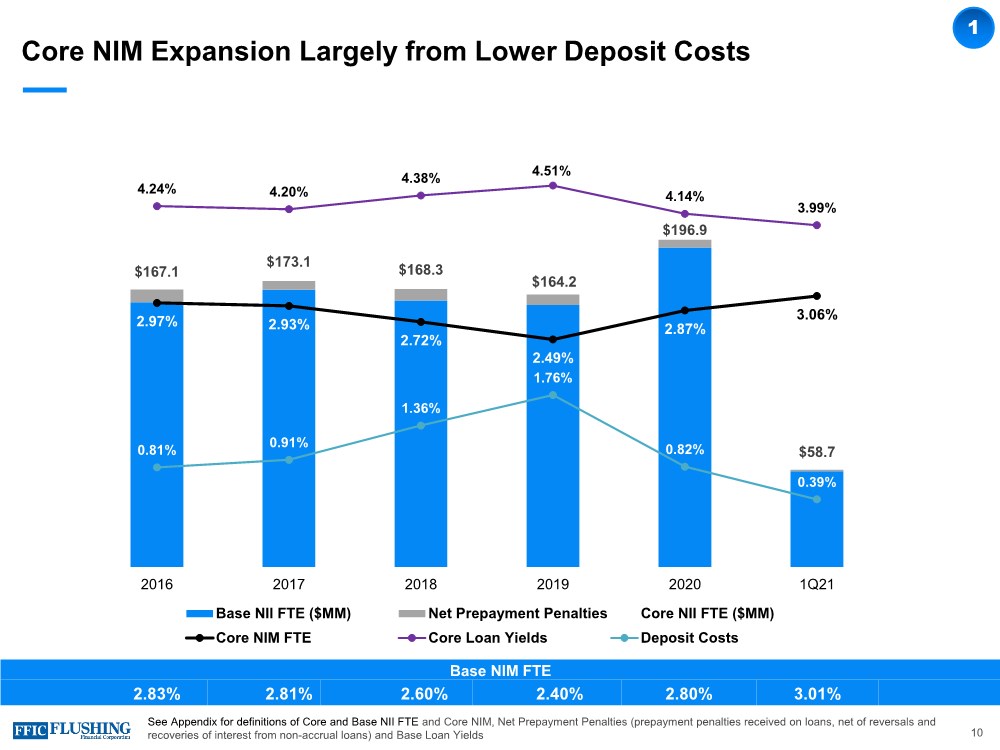

| Core NIM Expansion Largely from Lower Deposit Costs 10 1 See Appendix for definitions of Core and Base NII FTE and Core NIM, Net Prepayment Penalties (prepayment penalties received on loans, net of reversals and recoveries of interest from non-accrual loans) and Base Loan Yields Base NIM FTE 2.83% 2.81% 2.60% 2.40% 2.80% 3.01% $167.1 $173.1 $168.3 $164.2 $196.9 $58.7 2.97% 2.93% 2.72% 2.49% 2.87% 3.06% 4.24% 4.20% 4.38% 4.51% 4.14% 3.99% 0.81% 0.91% 1.36% 1.76% 0.82% 0.39% -0.50% 0.50% 1.50% 2.50% 3.50% 4.50% 5.50% $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 2016 2017 2018 2019 2020 1Q21 Base NII FTE ($MM) Net Prepayment Penalties Core NII FTE ($MM) Core NIM FTE Core Loan Yields Deposit Costs |

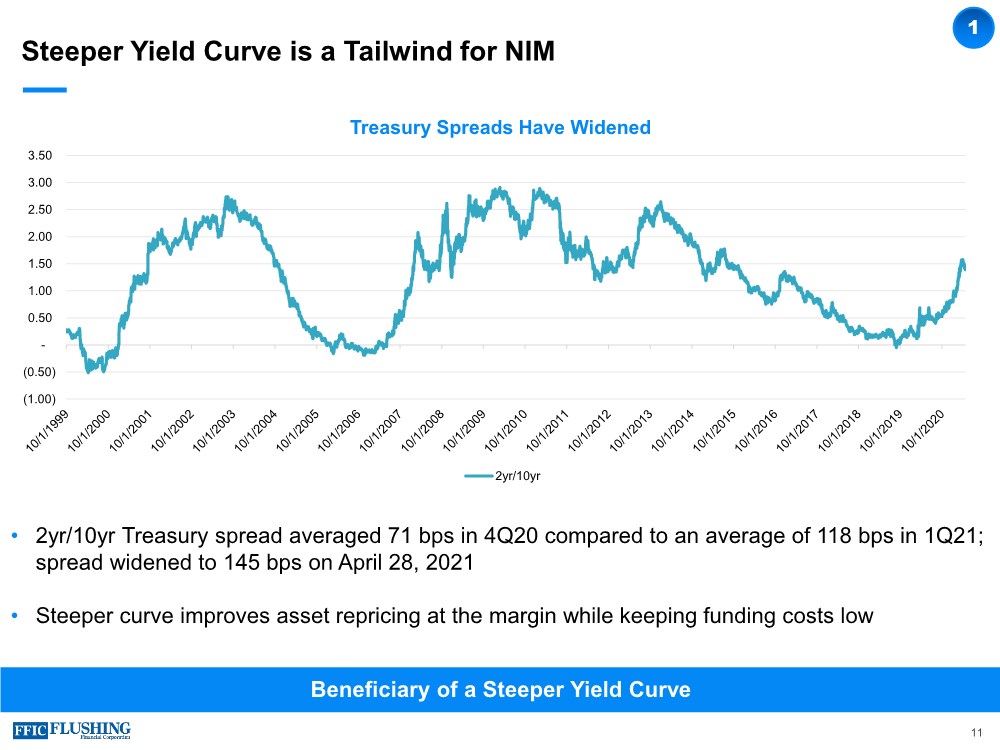

| Steeper Yield Curve is a Tailwind for NIM 1 11 Beneficiary of a Steeper Yield Curve (1.00) (0.50) - 0.50 1.00 1.50 2.00 2.50 3.00 3.50 Treasury Spreads Have Widened 2yr/10yr • 2yr/10yr Treasury spread averaged 71 bps in 4Q20 compared to an average of 118 bps in 1Q21; spread widened to 145 bps on April 28, 2021 • Steeper curve improves asset repricing at the margin while keeping funding costs low |

| We Have Tools to Manage Short-term Increases in Rates 1 12 Forward Starting Swaps To Help Protect NIM From Rising Short Rates • Duration of our assets is greater than the duration of our liabilities • Our balance sheet naturally improves over the next two years without any actions and we can take, or have already taken, the following actions: ‒ $480MM of forward starting pay fixed (0.73%), receive floating swaps on our wholesale funding replacing existing Federal Home Loan Bank advances yield (inclusive of existing swaps) of 2.33% in 1Q21 ‒ On average the forward starting swaps begin in early 4Q22, which is ahead of the Fed’s timing on rate increases in 2023 ‒ Extending the duration of liabilities to better match our assets; we will take further actions opportunistically ‒ Continue to grow C&I portfolio and use back-to-back loan swap program to add shorter duration loans |

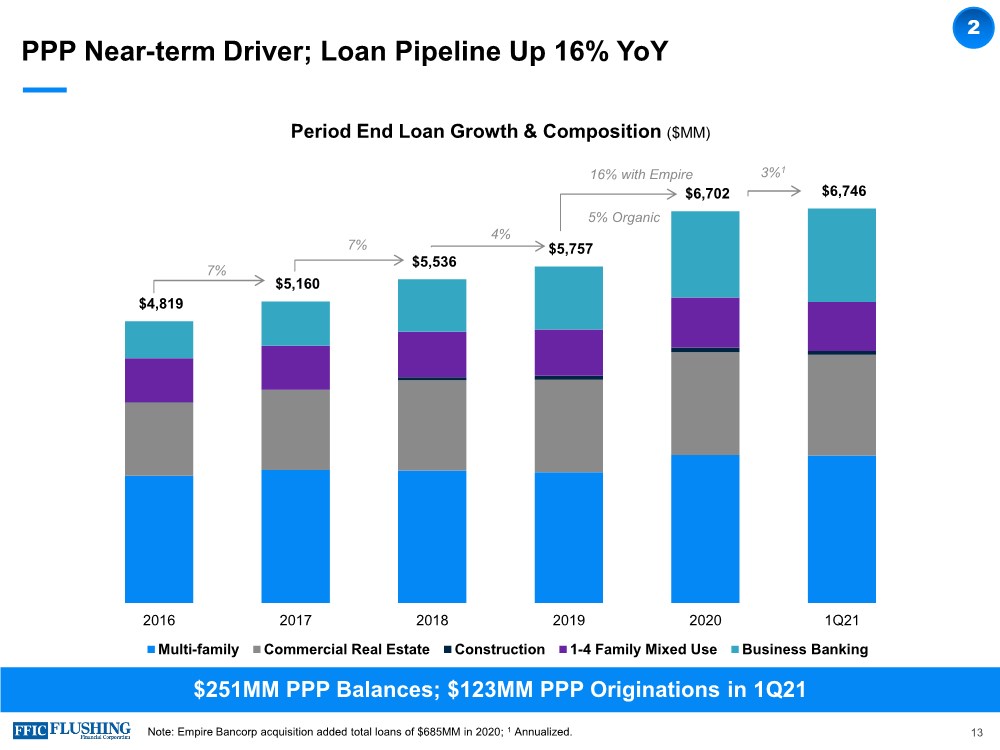

| PPP Near-term Driver; Loan Pipeline Up 16% YoY 2 $4,819 $5,160 $5,536 $5,757 $6,702 $6,746 $- $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $- $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 2016 2017 2018 2019 2020 1Q21 Multi-family Commercial Real Estate Construction 1-4 Family Mixed Use Business Banking 5% Organic 3%1 Period End Loan Growth & Composition ($MM) 7% 7% 4% 16% with Empire 13 $251MM PPP Balances; $123MM PPP Originations in 1Q21 Note: Empire Bancorp acquisition added total loans of $685MM in 2020; 1 Annualized. |

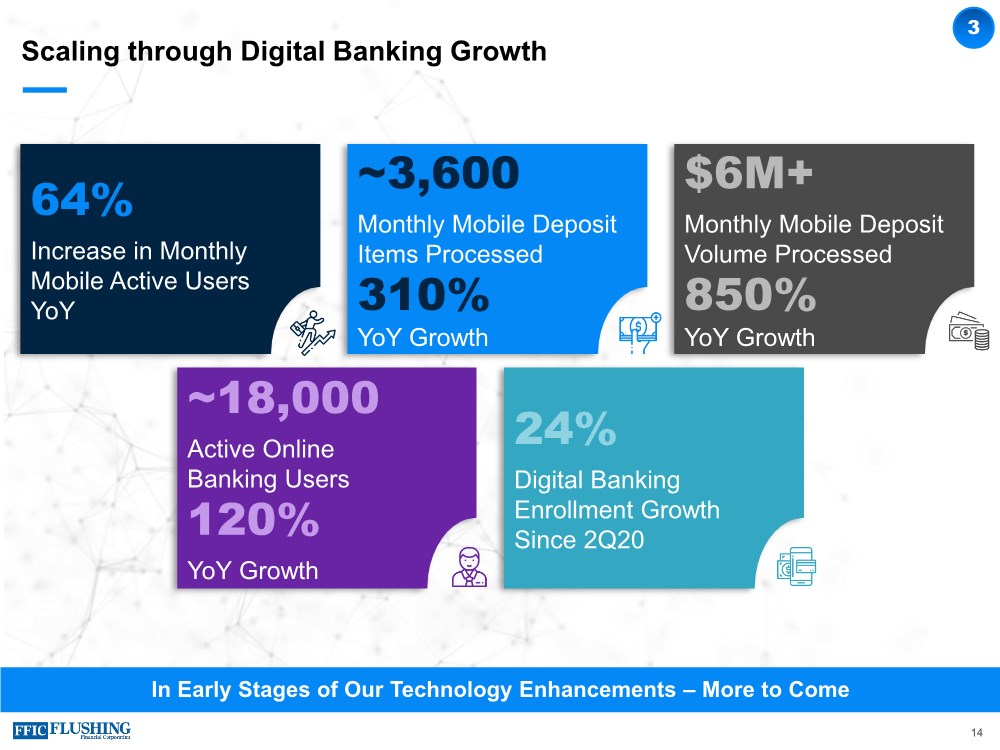

| In Early Stages of Our Technology Enhancements – More to Come 64% Increase in Monthly Mobile Active Users YoY ~3,600 Monthly Mobile Deposit Items Processed 310% YoY Growth $6M+ Monthly Mobile Deposit Volume Processed 850% YoY Growth 24% Digital Banking Enrollment Growth Since 2Q20 ~18,000 Active Online Banking Users 120% YoY Growth Scaling through Digital Banking Growth 14 3 |

| Achieving Synergies from Empire Transaction • $982MM asset bank with $685MM loans and $854MM deposits • $7MM after-tax cost saves expected in 2021 ‒ Cost savings recognized in 1Q21 consistent with projections ‒ Systems conversion completed in November 2020 ‒ Essentially all cost saves in the 1Q21 run rate • Branch Deposit growth of 14% since close • 15-20% of our marketing budget will be spent in Suffolk County • Ramping community service/sponsorships ‒ Delivered food to 6 local Suffolk County hospitals ‒ Identified 7 sponsorship opportunities to date Deal in Line with Expectations; Confident in Achieving 20% Earnings Accretion in 2021 3 Closed Transaction on October 30, 2020 15 |

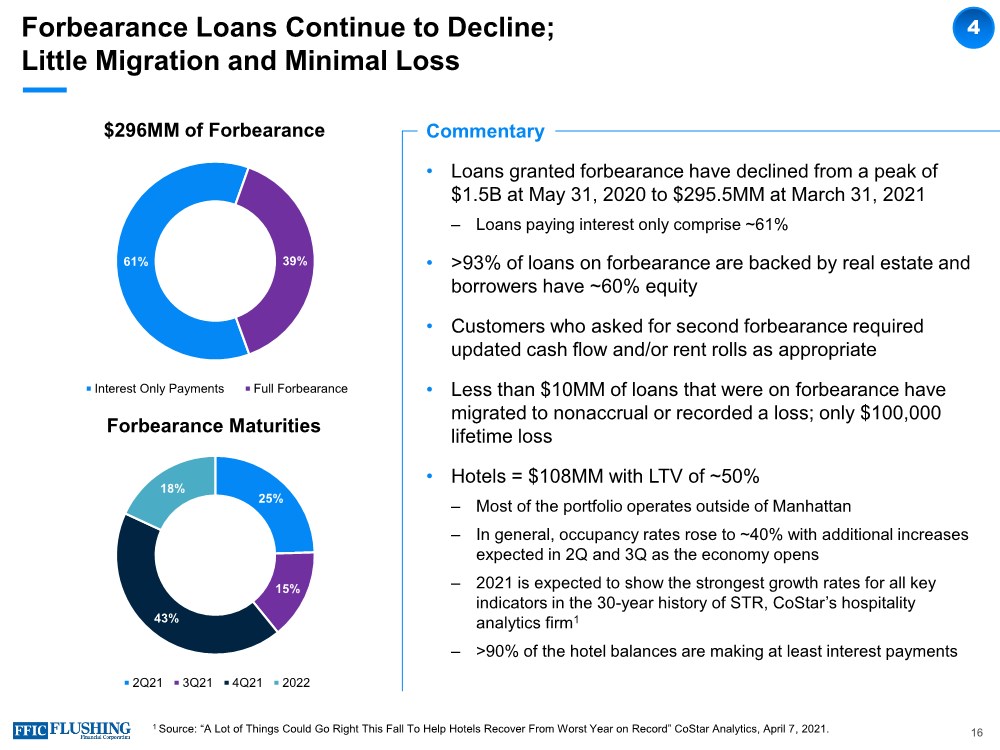

| Forbearance Loans Continue to Decline; Little Migration and Minimal Loss Commentary • Loans granted forbearance have declined from a peak of $1.5B at May 31, 2020 to $295.5MM at March 31, 2021 ‒ Loans paying interest only comprise ~61% • >93% of loans on forbearance are backed by real estate and borrowers have ~60% equity • Customers who asked for second forbearance required updated cash flow and/or rent rolls as appropriate • Less than $10MM of loans that were on forbearance have migrated to nonaccrual or recorded a loss; only $100,000 lifetime loss • Hotels = $108MM with LTV of ~50% ‒ Most of the portfolio operates outside of Manhattan ‒ In general, occupancy rates rose to ~40% with additional increases expected in 2Q and 3Q as the economy opens ‒ 2021 is expected to show the strongest growth rates for all key indicators in the 30-year history of STR, CoStar’s hospitality analytics firm1 ‒ >90% of the hotel balances are making at least interest payments 4 16 1 Source: “A Lot of Things Could Go Right This Fall To Help Hotels Recover From Worst Year on Record” CoStar Analytics, April 7, 2021. 25% 15% 43% 18% Forbearance Maturities 2Q21 3Q21 4Q21 2022 61% 39% $296MM of Forbearance Interest Only Payments Full Forbearance |

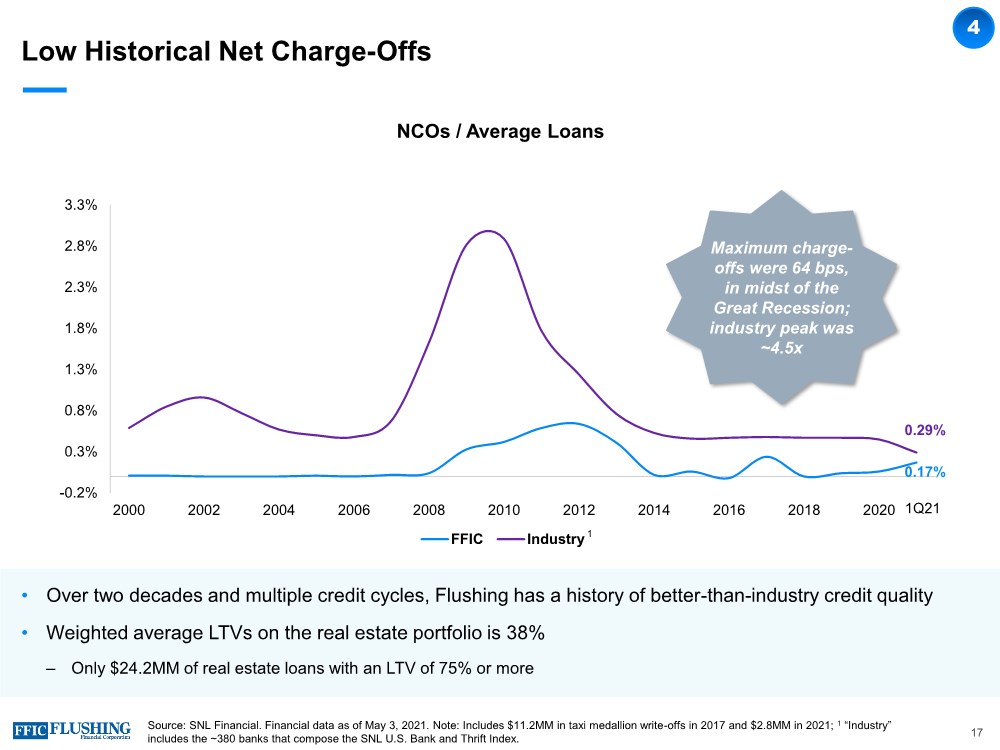

| Low Historical Net Charge-Offs • Over two decades and multiple credit cycles, Flushing has a history of better-than-industry credit quality • Weighted average LTVs on the real estate portfolio is 38% ‒ Only $24.2MM of real estate loans with an LTV of 75% or more Source: SNL Financial. Financial data as of May 3, 2021. Note: Includes $11.2MM in taxi medallion write-offs in 2017 and $2.8MM in 2021; 1 “Industry” includes the ~380 banks that compose the SNL U.S. Bank and Thrift Index. NCOs / Average Loans 0.17% 0.29% -0.2% 0.3% 0.8% 1.3% 1.8% 2.3% 2.8% 3.3% 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 FFIC Industry Maximum charge- offs were 64 bps, in midst of the Great Recession; industry peak was ~4.5x 1Q21 1 4 17 |

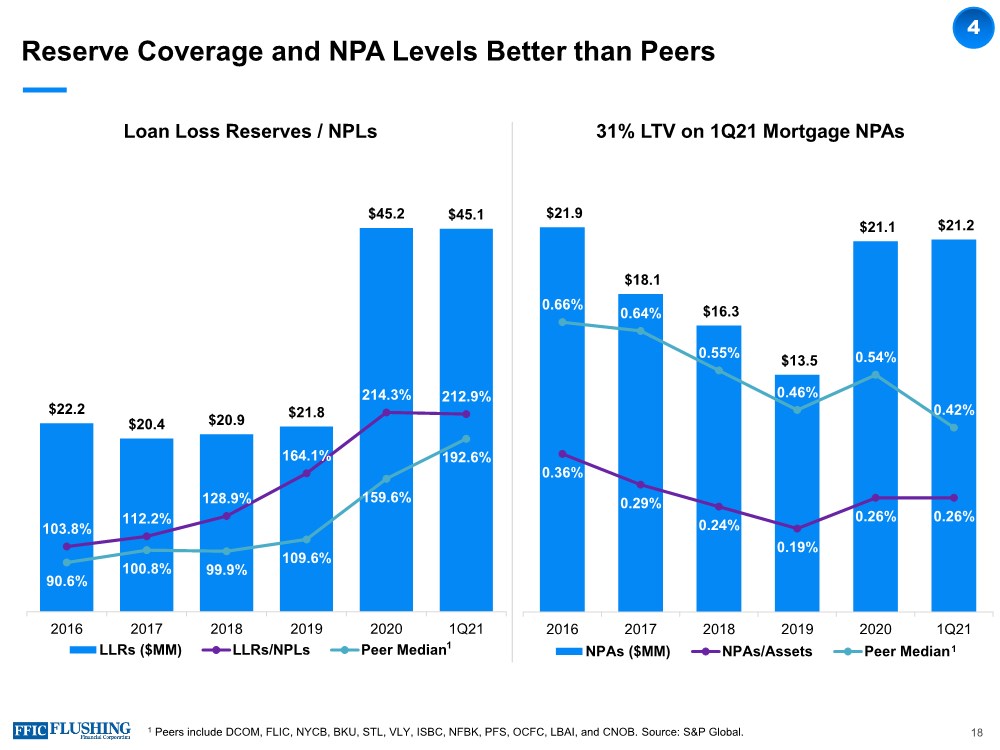

| Reserve Coverage and NPA Levels Better than Peers Loan Loss Reserves / NPLs 31% LTV on 1Q21 Mortgage NPAs $21.9 $18.1 $16.3 $13.5 $21.1 $21.2 0.36% 0.29% 0.24% 0.19% 0.26% 0.26% 0.66% 0.64% 0.55% 0.46% 0.54% 0.42% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 2016 2017 2018 2019 2020 1Q21 $- $5.0 $10.0 $15.0 $20.0 $25.0 NPAs ($MM) NPAs/Assets Peer Median1 4 18 1 Peers include DCOM, FLIC, NYCB, BKU, STL, VLY, ISBC, NFBK, PFS, OCFC, LBAI, and CNOB. Source: S&P Global. $22.2 $20.4 $20.9 $21.8 $45.2 $45.1 103.8% 112.2% 128.9% 164.1% 214.3% 212.9% 90.6% 100.8% 99.9% 109.6% 159.6% 192.6% 50.0% 100.0% 150.0% 200.0% 250.0% 300.0% 350.0% 400.0% 2016 2017 2018 2019 2020 1Q21 0 5 10 15 20 25 30 35 40 45 50 LLRs ($MM) LLRs/NPLs Peer Median1 |

| Outlook Benefitting from steeper yield curve; positioning for higher rates ‒ Steeper yield curve helps asset repricing and keeps funding pressures low ‒ Starting to extend liability duration to help protect from rising short term rates ‒ Continue to build out Commercial lending portfolio and shorten asset duration ‒ $480MM forward starting swaps on wholesale funding More optimistic about operating environment ‒ Accelerated vaccine roll out to have a positive impact on the economy ‒ Asian franchise to become more active as pandemic recedes; more outreach and community events planned ‒ Using some of the benefit from the steeper yield curve to make investments in the business ‒ Digital enhancements are planned with new offerings and business opportunities • Loan pipelines are solid and should translate to better non-PPP loan growth • Empire synergies are underway; costs savings targets on track; working on revenue enhancements; confident in 20% EPS accretion in 2021 Remain very comfortable with our credit profile On right path to reach through-the-cycle goals: ROA ≥1% and ROE ≥10% 19 |

| Appendix |

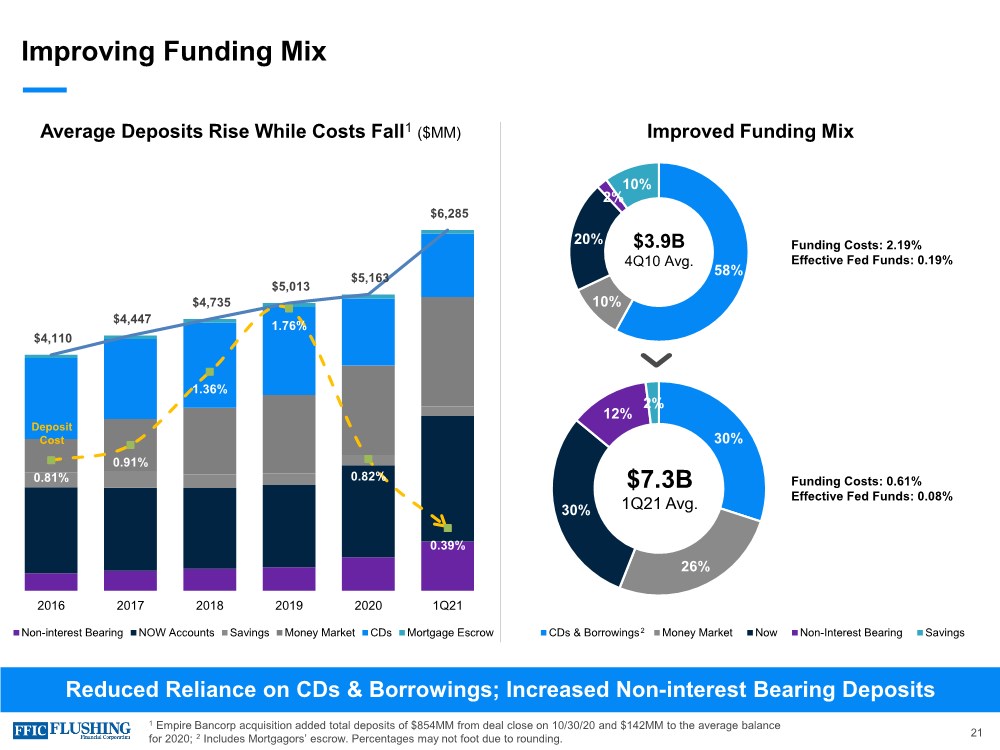

| Improving Funding Mix Reduced Reliance on CDs & Borrowings; Increased Non-interest Bearing Deposits Average Deposits Rise While Costs Fall1 ($MM) Improved Funding Mix $4,110 $4,447 $4,735 $5,013 $5,163 $6,285 0.81% 0.91% 1.36% 1.76% 0.82% 0.39% - 1,000 2,000 3,000 4,000 5,000 6,000 7,000 2016 2017 2018 2019 2020 1Q21 Non-interest Bearing NOW Accounts Savings Money Market CDs Mortgage Escrow Deposit Cost 1 Empire Bancorp acquisition added total deposits of $854MM from deal close on 10/30/20 and $142MM to the average balance for 2020; 2 Includes Mortgagors’ escrow. Percentages may not foot due to rounding. 58% 10% 20% 2% 10% 30% 26% 30% 12% 2% Funding Costs: 2.19% Effective Fed Funds: 0.19% Funding Costs: 0.61% Effective Fed Funds: 0.08% $3.9B 4Q10 Avg. $7.3B 1Q21 Avg. CDs & Borrowings Money Market Now Non-Interest Bearing Savings 2 21 |

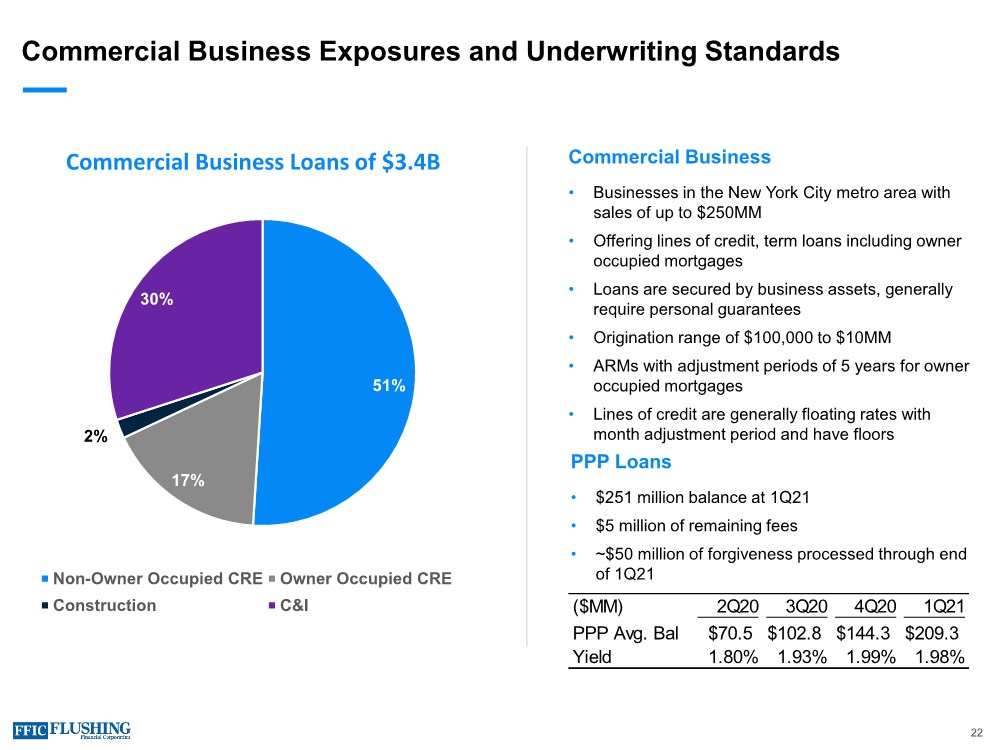

| Commercial Business Exposures and Underwriting Standards Commercial Business • Businesses in the New York City metro area with sales of up to $250MM • Offering lines of credit, term loans including owner occupied mortgages • Loans are secured by business assets, generally require personal guarantees • Origination range of $100,000 to $10MM • ARMs with adjustment periods of 5 years for owner occupied mortgages • Lines of credit are generally floating rates with month adjustment period and have floors 22 PPP Loans • $251 million balance at 1Q21 • $5 million of remaining fees • ~$50 million of forgiveness processed through end of 1Q21 ($MM) 2Q20 3Q20 4Q20 1Q21 PPP Avg. Bal $70.5 $102.8 $144.3 $209.3 Yield 1.80% 1.93% 1.99% 1.98% 51% 17% 2% 30% Non-Owner Occupied CRE Owner Occupied CRE Construction C&I Commercial Business Loans of $3.4B |

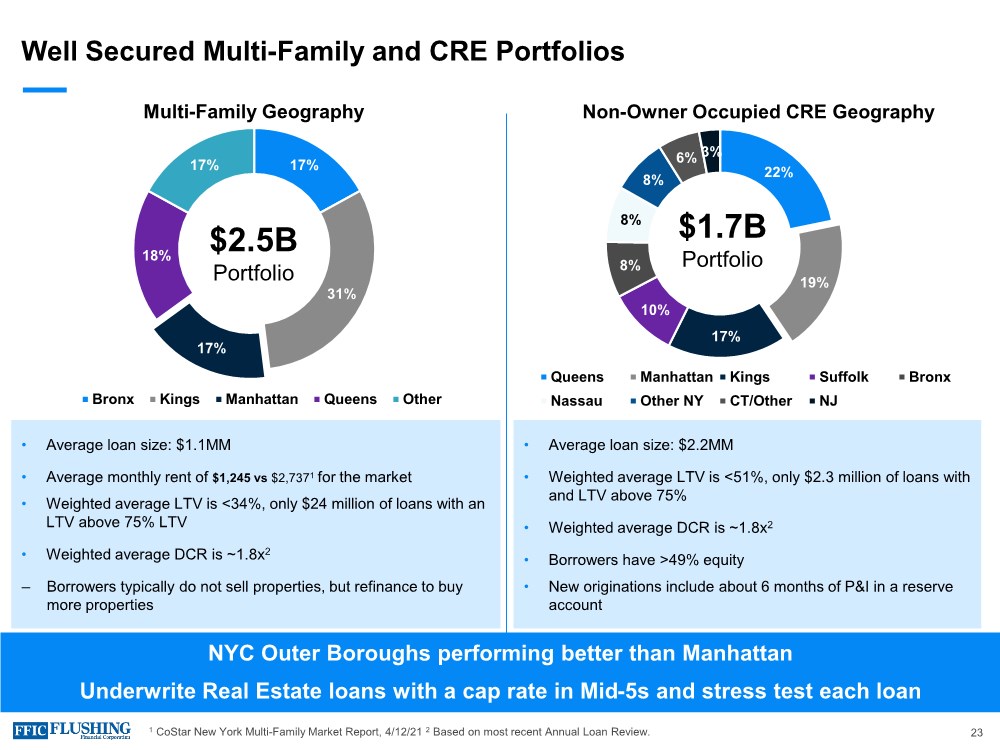

| Well Secured Multi-Family and CRE Portfolios Multi-Family Geography 17% 31% 17% 18% 17% Bronx Kings Manhattan Queens Other 1 CoStar New York Multi-Family Market Report, 4/12/21 2 Based on most recent Annual Loan Review. 23 $2.5B Portfolio • Average loan size: $1.1MM • Average monthly rent of $1,245 vs $2,7371 for the market • Weighted average LTV is <34%, only $24 million of loans with an LTV above 75% LTV • Weighted average DCR is ~1.8x2 ‒ Borrowers typically do not sell properties, but refinance to buy more properties • Average loan size: $2.2MM • Weighted average LTV is <51%, only $2.3 million of loans with and LTV above 75% • Weighted average DCR is ~1.8x2 • Borrowers have >49% equity • New originations include about 6 months of P&I in a reserve account Non-Owner Occupied CRE Geography 22% 19% 17% 10% 8% 8% 8% 6% 3% Queens Manhattan Kings Suffolk Bronx Nassau Other NY CT/Other NJ $1.7B Portfolio NYC Outer Boroughs performing better than Manhattan Underwrite Real Estate loans with a cap rate in Mid-5s and stress test each loan |

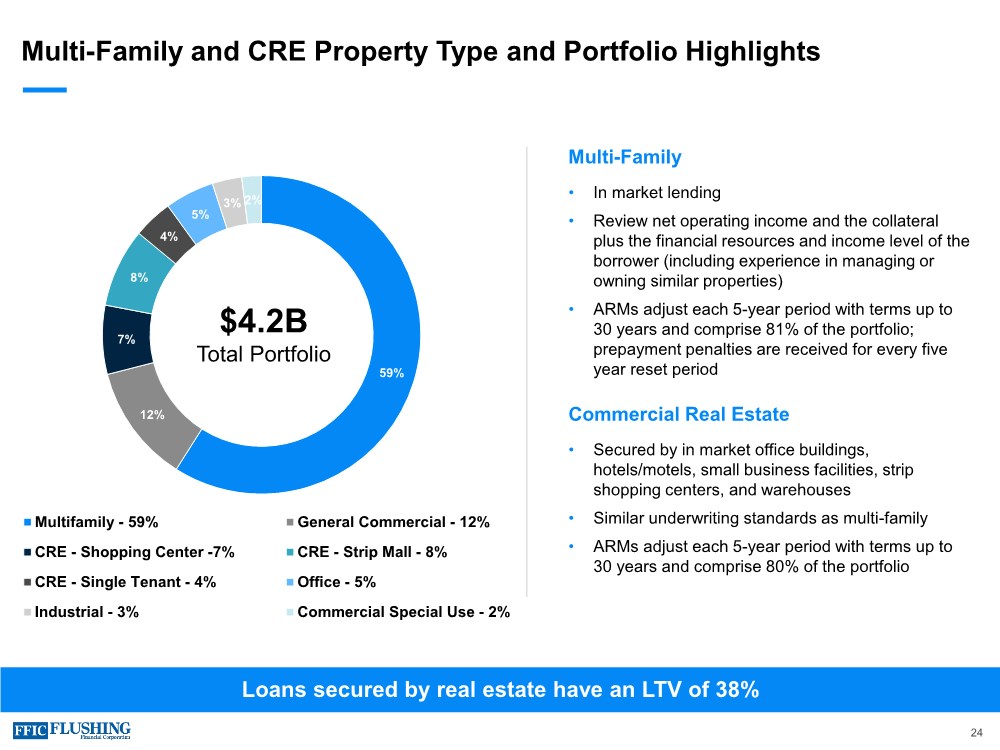

| Loans secured by real estate have an LTV of 38% Multi-Family and CRE Property Type and Portfolio Highlights Multi-Family • In market lending • Review net operating income and the collateral plus the financial resources and income level of the borrower (including experience in managing or owning similar properties) • ARMs adjust each 5-year period with terms up to 30 years and comprise 81% of the portfolio; prepayment penalties are received for every five year reset period Commercial Real Estate • Secured by in market office buildings, hotels/motels, small business facilities, strip shopping centers, and warehouses • Similar underwriting standards as multi-family • ARMs adjust each 5-year period with terms up to 30 years and comprise 80% of the portfolio 59% 12% 7% 8% 4% 5% 3% 2% Multifamily - 59% General Commercial - 12% CRE - Shopping Center -7% CRE - Strip Mall - 8% CRE - Single Tenant - 4% Office - 5% Industrial - 3% Commercial Special Use - 2% $4.2B Total Portfolio 24 |

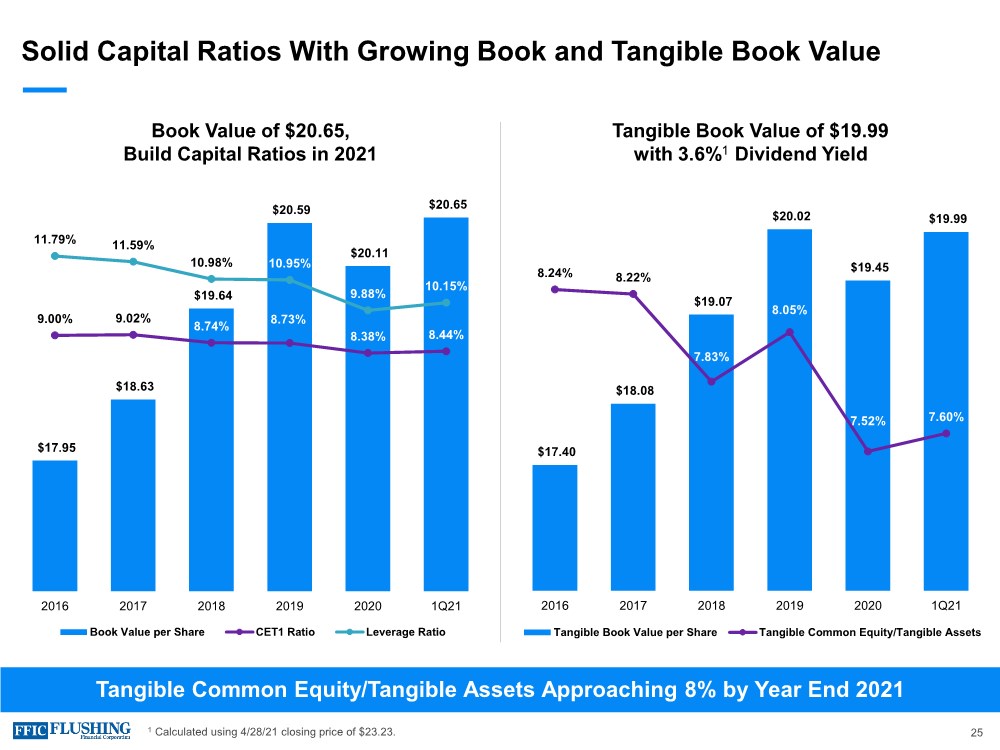

| Solid Capital Ratios With Growing Book and Tangible Book Value Tangible Common Equity/Tangible Assets Approaching 8% by Year End 2021 Book Value of $20.65, Build Capital Ratios in 2021 Tangible Book Value of $19.99 with 3.6%1 Dividend Yield $17.40 $18.08 $19.07 $20.02 $19.45 $19.99 8.24% 8.22% 7.83% 8.05% 7.52% 7.60% 6.90% 7.10% 7.30% 7.50% 7.70% 7.90% 8.10% 8.30% 8.50% 8.70% $16.00 $16.50 $17.00 $17.50 $18.00 $18.50 $19.00 $19.50 $20.00 $20.50 2016 2017 2018 2019 2020 1Q21 Tangible Book Value per Share Tangible Common Equity/Tangible Assets $17.95 $18.63 $19.64 $20.59 $20.11 $20.65 9.00% 9.02% 8.74% 8.73% 8.38% 8.44% 11.79% 11.59% 10.98% 10.95% 9.88% 10.15% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% $16.50 $17.00 $17.50 $18.00 $18.50 $19.00 $19.50 $20.00 $20.50 $21.00 2016 2017 2018 2019 2020 1Q21 Book Value per Share CET1 Ratio Leverage Ratio 1 Calculated using 4/28/21 closing price of $23.23. 25 |

| Reconciliation of GAAP Earnings and Core Earnings Non-cash Fair Value Adjustments to GAAP Earnings The variance in GAAP and core earnings is partly driven by the impact of non-cash net gains and losses from fair value adjustments. These fair value adjustments relate primarily to swaps designated to protect against rising rates and borrowing carried at fair value under the fair value option. As the swaps get closer to maturity, the volatility in fair value adjustments will dissipate. In a declining interest rate environment, the movement in the curve exaggerates our mark-to-market loss position. In a rising interest rate environment or a steepening of the yield curve, the loss position would experience an improvement. Core Net Income, Core Diluted EPS, Core ROAE, Core ROAA, Pre-provision Pre-tax Net Revenue, Core Net Interest Income FTE, Core Net Interest Margin FTE, Base Net Interest Income FTE, Base Net Interest Margin FTE, Core Interest Income and Yield on Total Loans, Base Interest Income and Yield on Total Loans, Core Non-interest Income, Core Non-interest Expense and tangible book value per common share are each non- GAAP measures used in this presentation.A reconciliation to the most directly comparable GAAP financial measures appears below in tabular form. The Company believes that these measures are useful for both investors and management to understand the effects of certain interest and non-interest items and provide an alternative view of the Company's performance over time and in comparison to the Company's competitors. These measures should not be viewed as a substitute for net income. The Company believes that tangible book value per common share is useful for both investors and management as these are measures commonly used by financial institutions, regulators and investors to measure the capital adequacy of financial institutions. The Company believes these measures facilitate comparison of the quality and composition of the Company's capital over time and in comparison to its competitors. These measures should not be viewed as a substitute for total shareholders' equity. These non-GAAP measures have inherent limitations, are not required to be uniformly applied and are not audited. They should not be considered in isolation or as a substitute for analysis of results reported under GAAP. These non-GAAP measures may not be comparable to similarly titled measures reported by other companies. 26 |

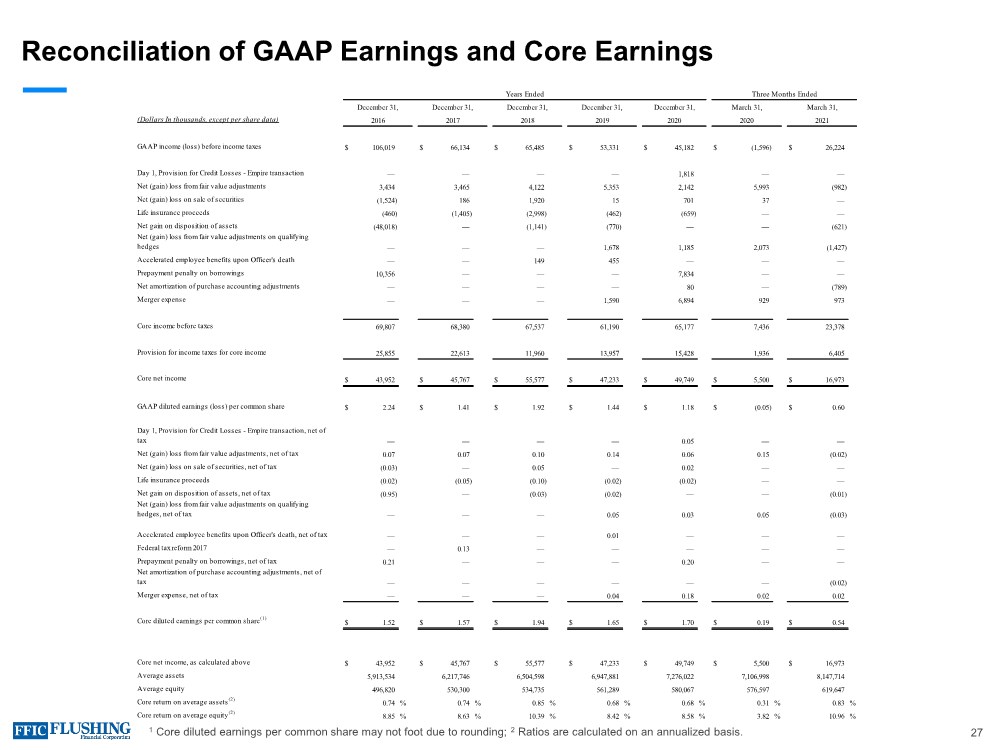

| Reconciliation of GAAP Earnings and Core Earnings 1 Core diluted earnings per common share may not foot due to rounding; 2 Ratios are calculated on an annualized basis. 27 (Dollars In thousands, except per share data) GAAP income (loss) before income taxes $ 106,019 $ 66,134 $ 65,485 $ 53,331 $ 45,182 $ (1,596) $ 26,224 Day 1, Provision for Credit Losses - Empire transaction — — — — 1,818 — — Net (gain) loss from fair value adjustments 3,434 3,465 4,122 5,353 2,142 5,993 (982) Net (gain) loss on sale of securities (1,524) 186 1,920 15 701 37 — Life insurance proceeds (460) (1,405) (2,998) (462) (659) — — Net gain on disposition of assets (48,018) — (1,141) (770) — — (621) Net (gain) loss from fair value adjustments on qualifying hedges — — — 1,678 1,185 2,073 (1,427) Accelerated employee benefits upon Officer's death — — 149 455 — — — Prepayment penalty on borrowings 10,356 — — — 7,834 — — Net amortization of purchase accounting adjustments — — — — 80 — (789) Merger expense — — — 1,590 6,894 929 973 Core income before taxes 69,807 68,380 67,537 61,190 65,177 7,436 23,378 Provision for income taxes for core income 25,855 22,613 11,960 13,957 15,428 1,936 6,405 Core net income $ 43,952 $ 45,767 $ 55,577 $ 47,233 $ 49,749 $ 5,500 $ 16,973 GAAP diluted earnings (loss) per common share $ 2.24 $ 1.41 $ 1.92 $ 1.44 $ 1.18 $ (0.05) $ 0.60 Day 1, Provision for Credit Losses - Empire transaction, net of tax — — — — 0.05 — — Net (gain) loss from fair value adjustments, net of tax 0.07 0.07 0.10 0.14 0.06 0.15 (0.02) Net (gain) loss on sale of securities, net of tax (0.03) — 0.05 — 0.02 — — Life insurance proceeds (0.02) (0.05) (0.10) (0.02) (0.02) — — Net gain on disposition of assets, net of tax (0.95) — (0.03) (0.02) — — (0.01) Net (gain) loss from fair value adjustments on qualifying hedges, net of tax — — — 0.05 0.03 0.05 (0.03) Accelerated employee benefits upon Officer's death, net of tax — — — 0.01 — — — Federal tax reform 2017 — 0.13 — — — — — Prepayment penalty on borrowings, net of tax 0.21 — — — 0.20 — — Net amortization of purchase accounting adjustments, net of tax — — — — — — (0.02) Merger expense, net of tax — — — 0.04 0.18 0.02 0.02 Core diluted earnings per common share(1) $ 1.52 $ 1.57 $ 1.94 $ 1.65 $ 1.70 $ 0.19 $ 0.54 Core net income, as calculated above $ 43,952 $ 45,767 $ 55,577 $ 47,233 $ 49,749 $ 5,500 $ 16,973 Average assets 5,913,534 6,217,746 6,504,598 6,947,881 7,276,022 7,106,998 8,147,714 Average equity 496,820 530,300 534,735 561,289 580,067 576,597 619,647 Core return on average assets(2) 0.74 % 0.74 % 0.85 % 0.68 % 0.68 % 0.31 % 0.83 % Core return on average equity(2) 8.85 % 8.63 % 10.39 % 8.42 % 8.58 % 3.82 % 10.96 % December 31, December 31, December 31, December 31, December 31, Three Months Ended 2016 2017 2018 2019 2020 Years Ended March 31, 2020 March 31, 2021 |

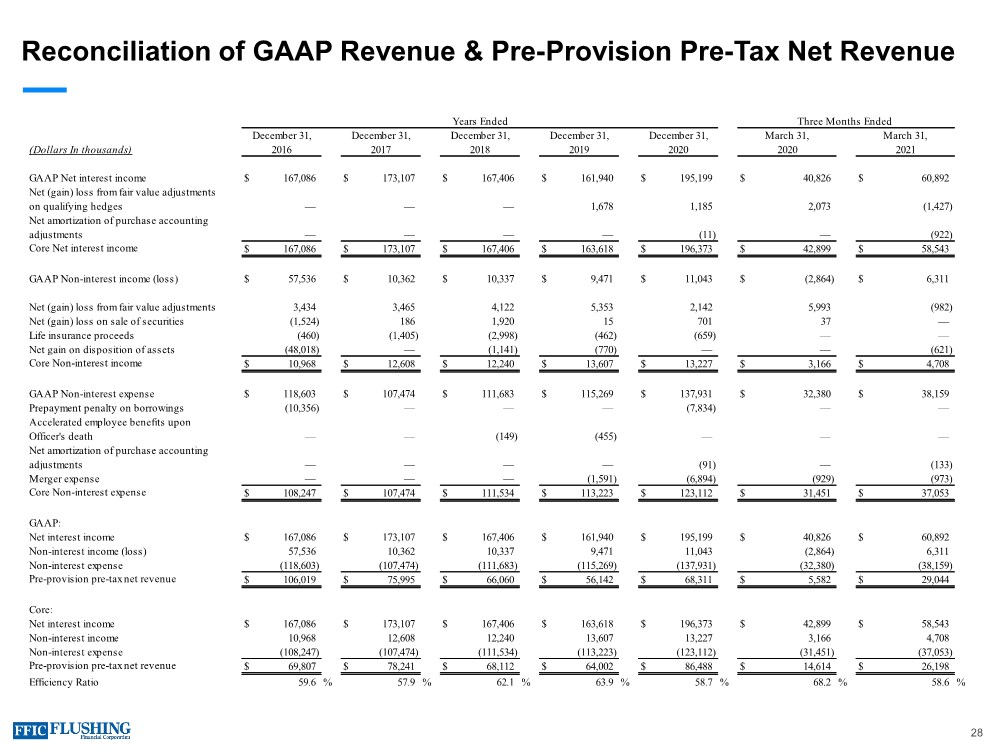

| Reconciliation of GAAP Revenue & Pre-Provision Pre-Tax Net Revenue 28 (Dollars In thousands) GAAP Net interest income $ 167,086 $ 173,107 $ 167,406 $ 161,940 $ 195,199 $ 40,826 $ 60,892 Net (gain) loss from fair value adjustments on qualifying hedges — — — 1,678 1,185 2,073 (1,427) Net amortization of purchase accounting adjustments — — — — (11) — (922) Core Net interest income $ 167,086 $ 173,107 $ 167,406 $ 163,618 $ 196,373 $ 42,899 $ 58,543 GAAP Non-interest income (loss) $ 57,536 $ 10,362 $ 10,337 $ 9,471 $ 11,043 $ (2,864) $ 6,311 Net (gain) loss from fair value adjustments 3,434 3,465 4,122 5,353 2,142 5,993 (982) Net (gain) loss on sale of securities (1,524) 186 1,920 15 701 37 — Life insurance proceeds (460) (1,405) (2,998) (462) (659) — — Net gain on disposition of assets (48,018) — (1,141) (770) — — (621) Core Non-interest income $ 10,968 $ 12,608 $ 12,240 $ 13,607 $ 13,227 $ 3,166 $ 4,708 GAAP Non-interest expense $ 118,603 $ 107,474 $ 111,683 $ 115,269 $ 137,931 $ 32,380 $ 38,159 Prepayment penalty on borrowings (10,356) — — — (7,834) — — Accelerated employee benefits upon Officer's death — — (149) (455) — — — Net amortization of purchase accounting adjustments — — — — (91) — (133) Merger expense — — — (1,591) (6,894) (929) (973) Core Non-interest expense $ 108,247 $ 107,474 $ 111,534 $ 113,223 $ 123,112 $ 31,451 $ 37,053 GAAP: Net interest income $ 167,086 $ 173,107 $ 167,406 $ 161,940 $ 195,199 $ 40,826 $ 60,892 Non-interest income (loss) 57,536 10,362 10,337 9,471 11,043 (2,864) 6,311 Non-interest expense (118,603) (107,474) (111,683) (115,269) (137,931) (32,380) (38,159) Pre-provision pre-tax net revenue $ 106,019 $ 75,995 $ 66,060 $ 56,142 $ 68,311 $ 5,582 $ 29,044 Core: Net interest income $ 167,086 $ 173,107 $ 167,406 $ 163,618 $ 196,373 $ 42,899 $ 58,543 Non-interest income 10,968 12,608 12,240 13,607 13,227 3,166 4,708 Non-interest expense (108,247) (107,474) (111,534) (113,223) (123,112) (31,451) (37,053) Pre-provision pre-tax net revenue $ 69,807 $ 78,241 $ 68,112 $ 64,002 $ 86,488 $ 14,614 $ 26,198 Efficiency Ratio 59.6 % 57.9 % 62.1 % 63.9 % 58.7 % 68.2 % 58.6 % Years Ended December 31, December 31, December 31, December 31, December 31, 2016 2017 2018 2019 2020 March 31, 2021 March 31, 2020 Three Months Ended |

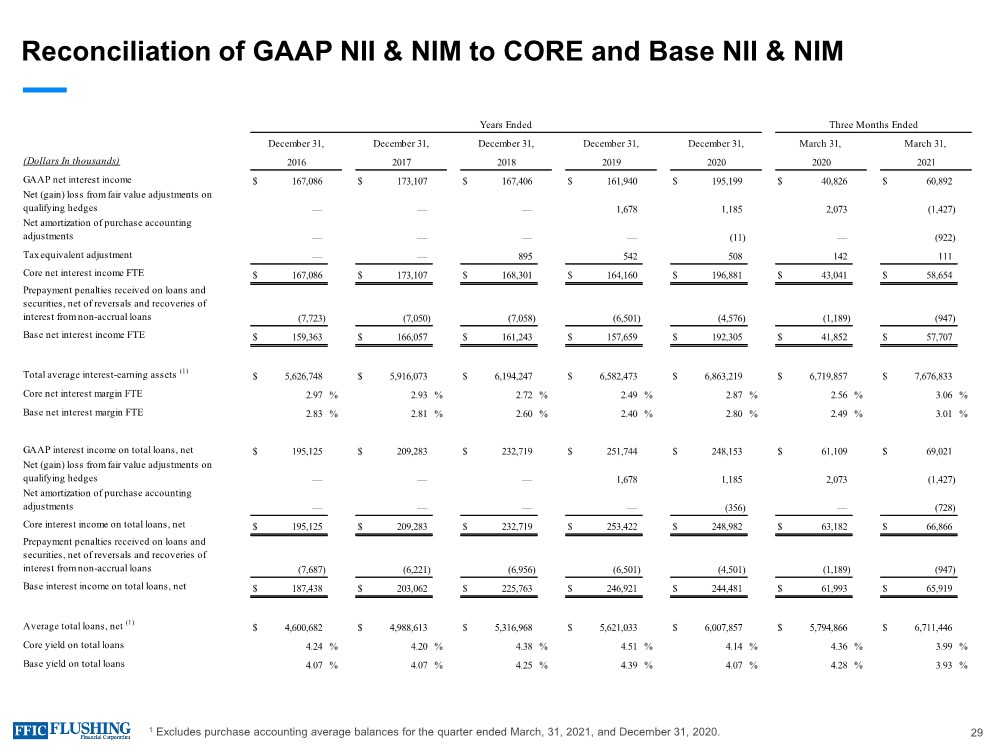

| Reconciliation of GAAP NII & NIM to CORE and Base NII & NIM 1 Excludes purchase accounting average balances for the quarter ended March, 31, 2021, and December 31, 2020. 29 (Dollars In thousands) GAAP net interest income $ 167,086 $ 173,107 $ 167,406 $ 161,940 $ 195,199 $ 40,826 $ 60,892 Net (gain) loss from fair value adjustments on qualifying hedges — — — 1,678 1,185 2,073 (1,427) Net amortization of purchase accounting adjustments — — — — (11) — (922) Tax equivalent adjustment — — 895 542 508 142 111 Core net interest income FTE $ 167,086 $ 173,107 $ 168,301 $ 164,160 $ 196,881 $ 43,041 $ 58,654 Prepayment penalties received on loans and securities, net of reversals and recoveries of interest from non-accrual loans (7,723) (7,050) (7,058) (6,501) (4,576) (1,189) (947) Base net interest income FTE $ 159,363 $ 166,057 $ 161,243 $ 157,659 $ 192,305 $ 41,852 $ 57,707 Total average interest-earning assets (1) $ 5,626,748 $ 5,916,073 $ 6,194,247 $ 6,582,473 $ 6,863,219 $ 6,719,857 $ 7,676,833 Core net interest margin FTE 2.97 % 2.93 % 2.72 % 2.49 % 2.87 % 2.56 % 3.06 % Base net interest margin FTE 2.83 % 2.81 % 2.60 % 2.40 % 2.80 % 2.49 % 3.01 % GAAP interest income on total loans, net $ 195,125 $ 209,283 $ 232,719 $ 251,744 $ 248,153 $ 61,109 $ 69,021 Net (gain) loss from fair value adjustments on qualifying hedges — — — 1,678 1,185 2,073 (1,427) Net amortization of purchase accounting adjustments — — — — (356) — (728) Core interest income on total loans, net $ 195,125 $ 209,283 $ 232,719 $ 253,422 $ 248,982 $ 63,182 $ 66,866 Prepayment penalties received on loans and securities, net of reversals and recoveries of interest from non-accrual loans (7,687) (6,221) (6,956) (6,501) (4,501) (1,189) (947) Base interest income on total loans, net $ 187,438 $ 203,062 $ 225,763 $ 246,921 $ 244,481 $ 61,993 $ 65,919 Average total loans, net (1) $ 4,600,682 $ 4,988,613 $ 5,316,968 $ 5,621,033 $ 6,007,857 $ 5,794,866 $ 6,711,446 Core yield on total loans 4.24 % 4.20 % 4.38 % 4.51 % 4.14 % 4.36 % 3.99 % Base yield on total loans 4.07 % 4.07 % 4.25 % 4.39 % 4.07 % 4.28 % 3.93 % March 31, 2021 Three Months Ended 2016 2017 2018 2019 2020 March 31, 2020 Years Ended December 31, December 31, December 31, December 31, December 31, |

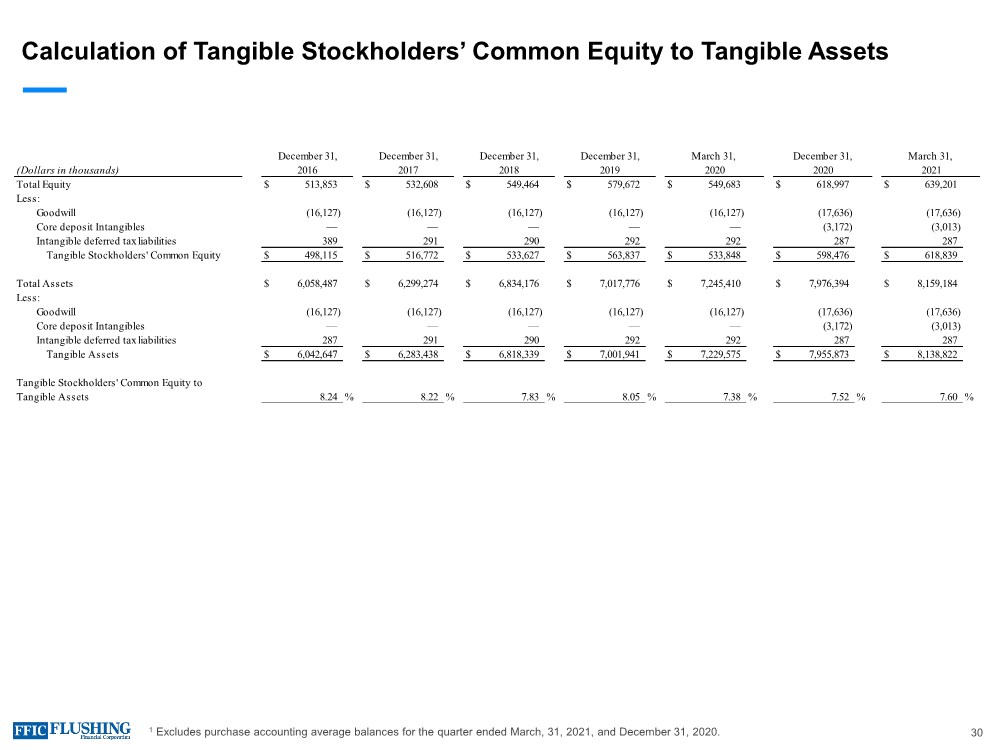

| Calculation of Tangible Stockholders’ Common Equity to Tangible Assets 1 Excludes purchase accounting average balances for the quarter ended March, 31, 2021, and December 31, 2020. 30 (Dollars in thousands) Total Equity $ 513,853 $ 532,608 $ 549,464 $ 579,672 $ 549,683 $ 618,997 $ 639,201 Less: Goodwill (16,127) (16,127) (16,127) (16,127) (16,127) (17,636) (17,636) Core deposit Intangibles — — — — — (3,172) (3,013) Intangible deferred tax liabilities 389 291 290 292 292 287 287 Tangible Stockholders' Common Equity $ 498,115 $ 516,772 $ 533,627 $ 563,837 $ 533,848 $ 598,476 $ 618,839 Total Assets $ 6,058,487 $ 6,299,274 $ 6,834,176 $ 7,017,776 $ 7,245,410 $ 7,976,394 $ 8,159,184 Less: Goodwill (16,127) (16,127) (16,127) (16,127) (16,127) (17,636) (17,636) Core deposit Intangibles — — — — — (3,172) (3,013) Intangible deferred tax liabilities 287 291 290 292 292 287 287 Tangible Assets $ 6,042,647 $ 6,283,438 $ 6,818,339 $ 7,001,941 $ 7,229,575 $ 7,955,873 $ 8,138,822 Tangible Stockholders' Common Equity to Tangible Assets 8.24 % 8.22 % 7.83 % 8.05 % 7.38 % 7.52 % 7.60 % March 31, 2020 March 31, 2021 December 31, December 31, December 31, December 31, December 31, 2016 2017 2018 2019 2020 |

| Contact Details Susan K. Cullen SEVP, CFO & Treasurer Phone: (718) 961-5400 Email: susan.cullen@flushingbank.com Al Savastano Director of Investor Relations Phone: (516) 820-1146 Email: asavastano@flushingbank.com 31 |

|