Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - SkyWater Technology, Inc | d26688dex231.htm |

| EX-10.24 - EX-10.24 - SkyWater Technology, Inc | d26688dex1024.htm |

| EX-10.23 - EX-10.23 - SkyWater Technology, Inc | d26688dex1023.htm |

| EX-10.22 - EX-10.22 - SkyWater Technology, Inc | d26688dex1022.htm |

| EX-10.7.1 - EX-10.7.1 - SkyWater Technology, Inc | d26688dex1071.htm |

| EX-10.7 - EX-10.7 - SkyWater Technology, Inc | d26688dex107.htm |

| EX-10.6 - EX-10.6 - SkyWater Technology, Inc | d26688dex106.htm |

| EX-4.1 - EX-4.1 - SkyWater Technology, Inc | d26688dex41.htm |

| EX-3.2 - EX-3.2 - SkyWater Technology, Inc | d26688dex32.htm |

| EX-3.1 - EX-3.1 - SkyWater Technology, Inc | d26688dex31.htm |

| EX-1.1 - EX-1.1 - SkyWater Technology, Inc | d26688dex11.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 12, 2021

Registration No. 333-254580

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

SkyWater Technology, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3674 | 37-1839853 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

2401 East 86th Street

Bloomington, Minnesota 55425

(952) 851-5200

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Thomas Sonderman

President and Chief Executive Officer

SkyWater Technology, Inc.

2401 East 86th Street

Bloomington, Minnesota 55425

(952) 851-5200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Kevin K. Greenslade William J. Curtin Hogan Lovells US LLP 555 Thirteenth Street, N.W. Washington, D.C. 20004 (703) 610-6189 |

Steve Manko Chief Financial Officer SkyWater Technology, Inc. 2401 East 86th Street Bloomington, Minnesota 55425 (952) 876-8504 |

Heidi E. Mayon Julia R. White Goodwin Procter LLP 601 Marshall Street Redwood City, California 94063 (650) 752-3100 |

Table of Contents

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| TITLE OF EACH CLASS OF SECURITIES TO BE REGISTERED |

AMOUNT TO BE REGISTERED (1) |

PROPOSED MAXIMUM OFFERING PRICE PER SHARE (2) |

PROPOSED MAXIMUM AGGREGATE OFFERING PRICE (1)(2) |

AMOUNT OF REGISTRATION FEE (3) | ||||

| Common stock, par value $0.01 per share |

6,670,000 | $14.00 | $93,380,000 | $10,188 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated pursuant to Rule 457(a) under the Securities Act. Includes the additional shares which the underwriters have the option to purchase to cover over-allotments of shares, if any. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act. |

| (3) | The registrant previously paid $8,183 of the registration fee in connection with the initial filing of this registration statement. In accordance with Rule 457(a) under the Securities Act, an additional registration fee of $2,005 is being paid with this amendment to the registration statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

Prior to the effectiveness of this registration statement, CMI Acquisition, LLC, a Delaware limited liability company, will convert into a Delaware corporation and change its name to SkyWater Technology, Inc., which we refer to as the Corporate Conversion. As a result of the Corporate Conversion, the members of CMI Acquisition, LLC will become holders of shares of common stock of SkyWater Technology, Inc. Except as otherwise disclosed in the accompanying prospectus, the consolidated financial statements and selected historical consolidated financial data and other financial information included in this registration statement are those of CMI Acquisition, LLC and its subsidiaries and do not give effect to the Corporate Conversion. Shares of common stock of SkyWater Technology, Inc. are being offered by the prospectus that forms a part of this registration statement.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated April 12, 2021

5,800,000 Shares

Common Stock

This is our initial public offering. We are offering 5,800,000 shares of our common stock.

We expect that the public offering price will be between $12.00 and $14.00 per share. No public market currently exists for the shares. We have applied to list our common stock on the Nasdaq Capital Market under the trading symbol “SKYT.”

Following this offering, Oxbow Industries, LLC and its affiliates will own approximately 76.0% of our outstanding common stock (or approximately 74.2% if the underwriters exercise their over-allotment option in full), and will therefore control more than a majority of the voting power of our outstanding common stock. As a result, we expect to be a “controlled company” for purposes of the marketplace rules of the Nasdaq Capital Market.

We are an “emerging growth company” under the federal securities laws and are eligible to comply with reduced disclosure requirements for this prospectus and our public company filings.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 14.

| PRICE TO PUBLIC |

UNDERWRITING DISCOUNTS AND COMMISSIONS (1) |

PROCEEDS TO SKYWATER TECHNOLOGY, INC. |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

| (1) | See “Underwriting” on page 120 for additional information regarding underwriting compensation. |

The underwriters have an option to purchase a maximum of 870,000 additional shares of common stock from us solely to cover over-allotments of shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Delivery of the shares of common stock will be made on or about , 2021.

| Jefferies | Cowen | |||

| Piper Sandler | ||||

The date of this prospectus is , 2021.

Table of Contents

| PAGE | ||||

| 1 | ||||

| 14 | ||||

| 36 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 43 | ||||

| 45 | ||||

| 47 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

51 | |||

| 63 | ||||

| 83 | ||||

| 90 | ||||

| 105 | ||||

| 107 | ||||

| 109 | ||||

| 114 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK |

116 | |||

| 120 | ||||

| 124 | ||||

| 124 | ||||

| 125 | ||||

| F-1 | ||||

Table of Contents

ABOUT THIS PROSPECTUS

You should rely only on the information contained in this prospectus or any related free writing prospectus we may authorize to be delivered to you. We have not, and the underwriters have not, authorized anyone to provide you with any information other than that contained or incorporated by reference in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. Neither we nor the underwriters take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of the time of delivery of this prospectus or any sale of shares of our common stock.

Through and including , 2021 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside the United States, neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus outside the United States.

Except as otherwise indicated herein or as the context otherwise requires, references in this prospectus to “SkyWater,” “we,” “us,” “our” and similar references refer, prior to the Corporate Conversion discussed elsewhere in this prospectus, to CMI Acquisition, LLC, a Delaware limited liability company, and its subsidiaries, taken as a whole, and after the Corporate Conversion, to SkyWater Technology, Inc., a Delaware corporation, and its subsidiaries, taken as a whole. We own various unregistered trademarks and servicemarks, including our corporate logo. The name “SkyWater Technology,” the SkyWater Technology logos and the other trade names, trademarks or service marks of SkyWater Technology appearing in this prospectus are the property of SkyWater Technology. Solely for convenience, the trademarks and trade names in this prospectus are referred to without the ® and ™ symbols, but such references should not be construed as any indicator that the owner of such trademarks and trade names will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend the use or display of other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

ii

Table of Contents

INDUSTRY AND MARKET DATA

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size, is based on information from various third-party sources, including reports from Gartner, Inc., or Gartner, Infiniti Research, AMA Research & Media LLP, or AMA, IC Insights, Inc., or IC Insights, Databeans, Inc., or Databeans, the U.S. Department of Defense, or DoD, Mind Commerce, Yole Développement SA, or Yole Développement, MarketsandMarkets Research Private Ltd., or MarketsandMarkets, Statista, Inc., or Statistica, and Semiconductor Equipment and Materials International, or SEMI, on assumptions we have made based on such data and other similar sources and on our knowledge of the markets for our solution. Industry surveys, publications and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We believe the data from such third-party sources to be reliable. While we are not aware of any misstatements regarding the market or industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the headings “Risk Factors,” “Special Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

The Gartner content described herein, “Semiconductor Forecast Database, Worldwide, 2Q20 Update,” Ben Lee, et al., 30 June 2020 (the Gartner Content), represents research opinions or viewpoints published, as part of a syndicated subscription service, by Gartner, and are not representations of fact. The Gartner Content speaks as of its original publication date (and not as of the date of this prospectus) and the opinions expressed in the Gartner Content are subject to change without notice.

iii

Table of Contents

This summary highlights information presented elsewhere in this prospectus and is qualified in its entirety by such information. This summary does not contain all of the information you should consider before investing in our common stock. Before you decide whether to invest in our common stock, you should read and carefully consider the entire prospectus, including our consolidated financial statements and the related notes thereto appearing elsewhere in this prospectus and the matters discussed in the sections in this prospectus entitled “Risk Factors,” “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Some of the statements in this prospectus constitute forward-looking statements that involve risks and uncertainties, as discussed under “Special Note Regarding Forward-Looking Statements.”

SKYWATER TECHNOLOGY, INC.

Our Business

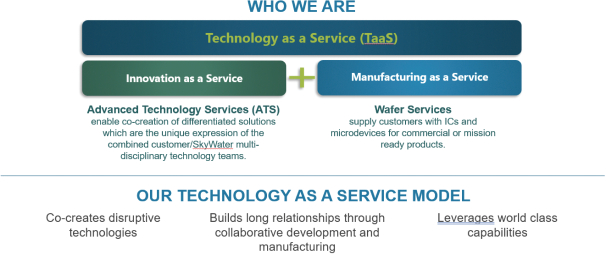

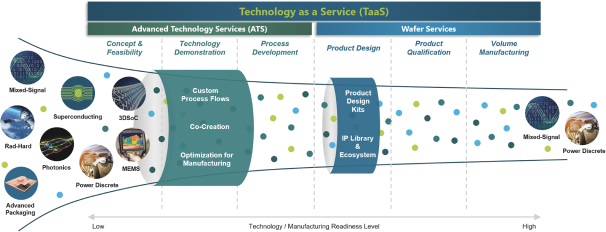

We are a U.S. investor-owned, independent, pure-play technology foundry that offers advanced semiconductor development and manufacturing services from our fabrication facility, or fab, in Minnesota and advanced packaging services from our Florida facility. In our technology as a service model, we leverage a strong foundation of proprietary technology to co-develop process technology IP with our customers that enables disruptive concepts through our Advanced Technology Services for diverse microelectronics (integrated circuits, or ICs) and related micro- and nanotechnology applications. In addition to differentiated technology development services, we support customers with volume production of ICs for high-growth markets through our Wafer Services.

The combination of semiconductor development and manufacturing services we provide our customers is not available to them from a conventional fab. In addition, following this offering, our status as a publicly-traded, U.S.-based, U.S. investor-owned pure-play technology foundry with Defense Microelectronics Activity, or DMEA, Category 1A accreditation from the U.S. Department of Defense, or DoD, is expected to position us well to provide distinct, competitive advantages to our customers. These advantages include the benefits of enhanced IP security and easy access to a U.S. domestic supply chain. In September 2019, we entered into a contract with the DoD to receive up to $170 million to expand and upgrade our manufacturing capabilities, specifically to build next-generation radiation hardened, or rad-hard, wafer solutions for the aerospace and defense sector which will have significant benefits for other commercial markets. Our fab expansion supporting this project began operations in October 2020. In January 2021, we entered into an agreement with Osceola County, Florida to take over operation of the Center for NeoVation facility in Kissimmee, Florida to accelerate pure-play advanced packaging services for differentiated technologies.

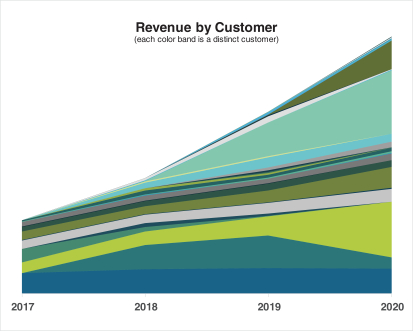

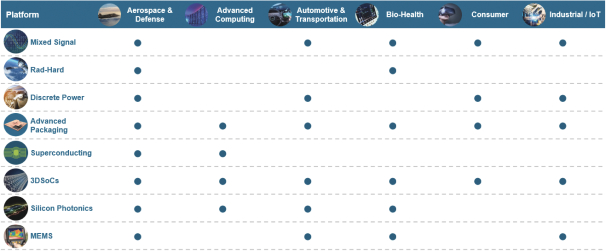

We primarily focus on serving diversified, high-growth, end users in numerous vertical markets, including (1) advanced computation, (2) aerospace and defense, or A&D, (3) automotive and transportation, (4) bio-health, (5) consumer and (6) industrial/internet of things, or IoT. By housing both development and manufacturing in a single operation, we rapidly and efficiently transition newly-developed processes to high-yielding volume production, eliminating the time it would otherwise take to transfer production to a third-party fab. Through our Advanced Technology Services, we specialize in co-creating with our customers advanced solutions that directly serve our end markets, such as superconducting ICs for quantum computing, integrated photonics, carbon nanotube technologies, or CNTs, microelectromechanical systems, or MEMS, technologies for biomedical and imaging applications, and advanced packaging. Our Wafer Services include the manufacture of silicon-based analog and mixed-signal ICs for our end markets. Our focus on the differentiated analog and mixed-signal and complementary metal-oxide-semiconductor, or CMOS, markets supports long product life-cycles and requirements that value performance over cost-efficiencies, and leverages our portfolio of IP. Our Advanced Technology Services and Wafer Services customers total 36 active accounts, and include Infineon, D-Wave, L3Harris, Leonardo DRS, Microsoft, MGI and Steifpower, compared to 11 customers in 2014.

1

Table of Contents

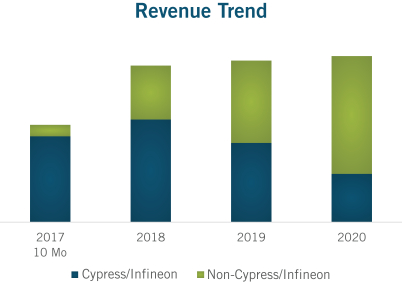

Before we began independent operations, our fab was owned and operated by Cypress Semiconductor Corporation, or Cypress, as a captive manufacturing facility for 20 years. We have leveraged the Cypress system, manufacturing technology and process development capabilities to advance our product offerings. We became an independent company in March 2017 when we were acquired by Oxbow Industries, LLC, or Oxbow, as part of a divestiture from Cypress. Our multi-year Foundry Services Agreement, or FSA, with Cypress, which ended in June 2020, created a runway for us to operate the foundry at a high utilization rate while continuing to expand and diversify the customer base transferred by Cypress.

Our Industry

Semiconductor designs require sophisticated manufacturing expertise and large capital investments for fab build-outs. This had led to the creation of pure-play technology foundries, which focus exclusively on providing semiconductor manufacturing based on processes and technologies that are developed for other semiconductor companies to utilize. Pure-play technology foundries neither offer nor design their own semiconductor products, and spread the cost of the fab across multiple customers.

We seek to help meet the growing and significant demand for specialty ICs. Electronics have become increasingly sophisticated and connected, increasing demand for analog and mixed-signal and specialty microelectronics, such as rad-hard, discrete power devices, superconducting, photonics, MEMS, carbon nanotubes and silicon interposers/advanced packaging solutions. These semiconductors and specialty microelectronics require higher levels of customization and are produced in lower volumes than other electronics. Traditional pure-play foundries generally have been unwilling or unable to manufacture these products either for financial reasons or because they do not possess the necessary IP. Security and IP protection also have become important as governments focus on developing their domestic supply chains.

The demand for these specialty ICs continues to grow due to demand from advanced computing, A&D, automotive and transportation, bio-health, consumer and industrial/IoT markets.

| ∎ | Advanced Computing. The volume of data produced globally is growing at a 35% compound annual growth rate, or CAGR, as the IoT landscape develops. Statistica projects that the volume of data produced by IoT connections worldwide in 2025 will be 79 zettabytes or 2,500 terabytes per second. New solutions such as chip accelerators, optical computing and transmission technologies and quantum computing are being explored to handle the new data volume requirements. We believe our superconducting process flows, silicon interposers and advanced packaging, 3-dimensional system on a chip technology, or 3DSoC, and silicon photonics and Advanced Technology Services are well-suited to enable these new solutions. |

| ∎ | Aerospace & Defense. Microelectronics provide critical capabilities for avionics, communications, space and weapon systems that support national security objectives. Domestic sourcing has become important as security and assured access needs have become U.S. governmental priorities. Rad-hard capabilities are required to successfully operate in extreme environments. We believe that, following this offering, our status as a publicly-traded, U.S.-based, U.S. investor-owned pure-play technology foundry with DMEA Category 1A accreditation through the DoD and our Advanced Technology Services and Wafer Services will enable us to deliver the next-generation capabilities needed for applications operating in extreme environments. |

| ∎ | Automotive & Transportation. According to IC Insights, the automotive and transportation market for integrated circuits in 2019 was $35 billion and is forecasted to grow at 8.5% annually for the next five years, with the analog sub-category growing 10.2% annually over the same period. Growth will be driven by the increasing amounts of customer-specific semiconductor content per vehicle to enable trends in connectivity, electrification, advanced driver-assistance systems concepts and autonomous driving. We believe our analog and mixed-signal CMOS, discrete power devices, silicon photonics, MEMS solutions and Advanced Technology Services are better suited for delivering customer-specific requirements faster to market than offerings by traditional pure-play foundries. |

2

Table of Contents

| ∎ | Bio-Health. The bio-health industry is rapidly adopting new technologies to improve healthcare outcomes, including enhancing integration between sensing and microelectronics to enable new diagnostic and intervention therapies. According to MarketsandMarkets, the market for microelectronics in the biomedical market for implants was $24.8 billion in 2016 and is forecasted to grow 9.8% annually through 2025. We believe our analog and mixed-signal CMOS, rad-hard CMOS, MEMS and Advanced Technology Services enable us to address the evolving technological needs within the bio-health industry. |

| ∎ | Consumer. The consumer industry has evolved towards connected, smart devices that require low-power battery systems and wireless connectivity to support product requirements for wearables, gaming, extended reality, voice assistants and other convenience and entertainment-oriented applications. We believe our analog and mixed-signal CMOS, discrete power devices and Advanced Technology Services provide better opportunities for consumer product companies to accelerate time-to-market to maintain product differentiation. |

| ∎ | Industrial/IoT. The 5G infrastructure roll-out and industrial IoT wave are driving demand for sensing, device connectivity, communications and edge computing applications. Companies have raced to develop solutions focused on reducing network latency and increasing data throughput. According to IC Insights, the industrial and communications market for ICs in 2019 was $175 billion. We believe our analog and mixed-signal CMOS, discrete power devices, MEMS and Advanced Technology Services can deliver faster time-to-market capabilities than offerings by traditional pure-play foundries. |

Our Competitive Strengths

We are a leader in technology innovation services, and believe that we have significant points of differentiation that will enable us to continue to succeed in the pure-play technology foundry industry. Our core strengths include the following:

| ∎ | Following this offering, our status as a publicly-traded, U.S.-based, U.S. investor-owned pure-play technology foundry with DMEA Category 1A accreditation from the DoD. We believe that our status following this offering as a publicly-traded U.S.-based, U.S. investor-owned pure-play technology foundry will provide us with a strong position to service the aerospace and defense market. Our current and potential aerospace and defense customers are required to comply with a range of information security protocols for protecting sensitive device IP with national security implications. The DoD established the Trusted Foundry Program in 2007 to provide secure access to leading-edge semiconductor technology and to ensure a trusted microelectronics supply chain for sensitive government programs with national security interests. As of March 5, 2021, there were 58 suppliers designated as “Trusted” under this program by the U.S. Government. Of those suppliers, we are one of only seven wafer fabs that have DMEA Category 1A accreditation through the DoD. In addition, there are other end markets, such as automotive and medical, that value working with a supplier operating within the United States, which offers a high level of protection for IP rights, or that value the convenience and branding advantage of services and products made in the United States. |

| ∎ | Unique IP model that offers customers an end-to-end solution for microelectronics and next-wave technology needs. We believe our pure-play technology foundry model combines the integrated process technology development services and manufacturing capability and expertise needed to address the high levels of customization specified by our customers. By combining our development lab capabilities in an advanced volume production fab, we are able to leverage our Advanced Technology Services to accelerate our customers’ time-to-market. We work alongside our customers to co-create customized ICs to meet or exceed stringent semiconductor requirements. By providing a full-scale semiconductor technology and manufacturing ecosystem, with substantial process flow integration and customized solutions, we are able to continually attract and retain customers. As of January 3, 2021, we had 34 Advanced Technology Services customers, including five Fortune 300 companies. |

3

Table of Contents

| ∎ | Accelerated time-to-market advantage for our customers. Our integration of development and manufacturing into a single ecosystem enables our customers’ products to be designed for manufacturing robustness without sacrificing the unique customization needed for differentiation. In addition, our wafer fab offers rapid prototyping and validation and accommodates small lot manufacturing, making our facility an optimal size for providing a complete solution for our customers and allowing them the opportunity to access the market more quickly than with other semiconductor foundries. |

| ∎ | A seasoned engineering team that leverages our extensive IP portfolio to support the development of emerging technologies in a fully integrated lab-to-fab environment. Our team of over 100 engineers employs IP created over decades, and our fab is specially geared toward managing the complexity of developing emerging technologies alongside manufacturing, with world-class excellence. Through direct collaboration with our customers, our team of engineers can leverage existing wafer process technology and process flow options to create custom fabrication processes that best serve our customers’ needs for high-performance analog and mixed-signal ICs. We also specialize in developing advanced processes for emerging technologies such as silicon photonics, superconducting and quantum computing, CMOS image sensing and DNA sequencing, among others. Our Advanced Technology Services provide us with a competitive advantage by offering significant technical expertise and customized engineering practices required for the creation and delivery of scalable specialty applications. The technological capabilities of our foundry shorten design cycles to create an expedited path for our customers’ products to reach the market. |

| ∎ | Optimized manufacturing environment for highly-engineered projects. Customers in our end markets value high performance and are willing to pay a premium for the Advanced Technology Services needed for the development of specialized products. Many of our customers are focused on high-margin specialty applications, which typically involve a smaller volume of production. We believe such customers are underserved by our competitors, which primarily focus on higher-volume opportunities. Our high-mix foundry automation and manufacturing systems are geared to handle high levels of customization, making smaller volume projects more economical than for competitive fabs. Our right-sized fab provides opportunities for us to leverage our manufacturing scale and expertise for customized processes and to realize higher margins for the significant engineering effort required by these complicated projects. |

| ∎ | Expertise in highly customized projects in a low-volume research and development environment. We specialize in, and have the equipment and process expertise necessary to deliver, effective and cost-efficient solutions while co-creating next-generation technology with our customers. We couple our Advanced Technology Services with existing process design kits, or PDKs, that leverage proven IP acquired in our divestiture from Cypress to allow our customers to co-create tailored product offerings. Our technical experience enables us to either modify existing processes or develop new, innovative solutions that are tailored to our customer’s needs. The ability of our competitors to engage in highly customized process development activities within their large-scale manufacturing operations is difficult without the significant IP and capital expenditures required to retrofit the larger operations for the high-mix and logistically complex requirements of the technology foundry model. Our 200 mm manufacturing lines deliver a degree of agility that allows us to efficiently respond to customer demands without significant lead-times or capital investment, and provides us with the ability to complete rapid prototyping that can quickly translate to volume production. With substantial experience in complex high-mix, mid-market manufacturing, we have deployed our ability through deployment of our Advanced Technology Services to excel in customer programs that require specialty knowledge and expertise. |

4

Table of Contents

Our Growth Strategy

We intend to become a prominent U.S.-based foundry by leveraging our core competencies in specialty process development and advanced manufacturing, while expanding our customer base and presence in high-margin end markets. To achieve this goal, we intend to pursue the following key strategies:

| ∎ | Diversify our customer base, grow our presence in existing markets, and expand into new end markets. Our Trusted Foundry designation, various industry accreditations and broad range of capabilities and services have established our presence in high-growth specialty applications. We have reduced our revenue concentration from Cypress/Infineon to approximately 29% of our revenues for the year ended January 3, 2021 from approximately 100% of our revenues from the period of acquisition to July 1, 2017. As of January 3, 2021, since divesting from Cypress in March 2017, we have added four new customers to our Wafer Services business and 21 new customers to our Advanced Technology Services business. We intend to continue to build upon our success in the advanced computation, A&D, automotive and transportation, bio-health, consumer and industrial/IoT markets while expanding into new markets over time. Our technology foundry services, coupled with our Trusted Foundry designation and various industry accreditations, offer unique value to our customers that we plan to leverage as we expand our presence across both current and new end markets. |

| ∎ | Leverage our Trusted Foundry status and find U.S. Government investments to add to our capabilities and expand our markets. We are one of only seven wafer fabrication facilities that have DMEA Category 1A accreditation through the DoD. We believe most foundries are not positioned to partner with the U.S. Government because of the Trusted Foundry’s security requirements, stringent government contract provisions and small lot manufacturing typical of government contracts. We have extensive experience working with highly-sensitive government projects that enable new capabilities and subsequently re-applying those capabilities to expand our offerings, such as the atomic layer deposition tool which was later used for other U.S. Government-funded programs and prototyping on typical engagements. In August 2018, the Defense Advanced Research Projects Agency, or DARPA, awarded the largest contract in the first round of DARPA’s Electronics Resurgence Initiative, or ERI, program to a team consisting of SkyWater, the Massachusetts Institute of Technology, or MIT, and Stanford University, to focus on developing microelectronics using carbon nanotube technology. We will continue to evaluate these government opportunities as the U.S. Government invests to regain global technology leadership in the semiconductor industry by optimizing and securing its IC manufacturing supply chain. |

| ∎ | Expand in the microelectronics value chain and champion U.S.-based pure-play advanced packaging foundry services. As our industry evolves into a post-Moore’s Law reality, we believe 2.5D, 3D, and SiP advanced packaging concepts will be adopted broadly and our domestic offering for development and manufacturing of solutions in this space will be in high demand. Furthermore, our strategy is to make these services available not only to our customers developing highly differentiated and disruptive front-end technologies but also to advanced packaging services that may source chips from other foundries and seek our support for onshore heterogeneous integration solutions. In addition, as interest grows within the federal government to enhance domestic infrastructure in this area, we feel we are well positioned to lead efforts to position the U.S. as a leader in advanced packaging technology. |

| ∎ | Expand in the rad-hard market. There are increasing uses for various radiation-hardened applications across multiple industries. In September 2019, we received a DoD contract for up to $170 million to build a next-generation rad-hard chip manufacturing capability, with volume production beginning in 2021. We believe our fab’s lower capital requirements will provide an attractive opportunity for future projects of this nature. |

| ∎ | Co-develop next-generation technologies with our customers, and grow our Advanced Technology Services. We intend to continue to engage in advanced development opportunities and leverage technologies developed to broaden our portfolio of semiconductor solutions. Access to our engineering team, production-grade technology and equipment, verified IP and trade secrets developed over |

5

Table of Contents

| several decades enable us to provide customized process development and Advanced Technology Services. We believe that investing in these capabilities will enable us to maintain our market leadership and attract customers that require lower volumes and intricate engineering specifications. |

| ∎ | Invest in design block IP development and enable third-party creation of IP. The foundation of a PDK-driven foundry offering for wafer services is a comprehensive library of silicon-proven, well-characterized design IP blocks. We will continue to invest in IP blocks organically, through targeted external investments, by encouraging IP design companies to offer their blocks for use with customer-paid royalties. |

| ∎ | Expand our capabilities through cost-effective capital management, including seeking M&A opportunities to drive growth. We will continue to invest in additional manufacturing capacity and evaluate growth opportunities through acquisitions of other businesses and operations, including, with respect to (1) other foundries, (2) larger foundries looking to divest existing low-volume programs, (3) low-cost manufacturing capacity that increases our scale and (4) adjacent markets such as advanced packaging, or AP, and bond/assembly/test, or BAT. We also may expand our current facility or convert existing spaces into clean rooms to add to our contaminant-free manufacturing environment. We believe acquiring low-cost U.S.-based facilities will expand our scale and customer base while maintaining our domestic competitive advantage without disrupting current operations. |

Our Customers

We serve a diverse array of customers across our Advanced Technology Services and Wafer Services businesses, ranging from designers producing near-commodity volume chips to those requiring highly-specialized next-wave technology solutions. Through our Wafer Services, we support customers producing ICs and devices either on our standard process or on a co-developed process that was produced using our Advanced Technology Services. Customers of our Advanced Technology Service develop chips with a wide range of special processing needs, ranging from light customizations to next-generation technologies. As of January 3, 2021, we had 36 customers.

Corporate Conversion

Prior to the effectiveness of the registration statement of which this prospectus is a part, we intend to change our form of business organization by converting from a Delaware limited liability company to a Delaware corporation and to change our name from CMI Acquisition, LLC to SkyWater Technology, Inc. In connection with these changes, which we refer to as the Corporate Conversion, all of the outstanding limited liability company interests of CMI Acquisition, LLC, which we refer to as units and which are comprised of Class B preferred units and common units, will automatically be converted into shares of our common stock. In connection with the Corporate Conversion, each Class B preferred unit and common unit will convert into a number of shares of common stock determined by dividing (1) the amount that would have been distributed in respect of each such unit in accordance with CMI Acquisition, LLC’s operating agreement if all assets of CMI Acquisition, LLC had been sold for a cash amount equal to the pre-offering value of CMI Acquisition, LLC, as such value is determined by CMI Acquisition, LLC’s board of managers based on the fair value of each share of our common stock (net of any underwriting discounts, fees and expenses), by (2) such per share fair value. As discussed more fully in the section titled “Corporate Conversion,” the amounts that would have been distributed for this purpose in respect of Class B preferred units and common units are determined by reference to the terms of CMI Acquisition, LLC’s operating agreement, with different values applicable to each series of units. For purposes of the Corporate Conversion, pre-offering “per share fair value” will be determined taking into account the assumed initial public offering price of our common stock.

Accordingly, and taking into account an assumed initial public offering price of $13.00 per share of common stock, which is the midpoint of the price range set forth on the cover page of this prospectus, our outstanding units will be converted as follows:

| ∎ | holders of Class B preferred units will receive an aggregate of 27,995,374 shares of our common stock; and |

6

Table of Contents

| ∎ | holders of our common units will receive an aggregate of 3,060,355 shares of our common stock. |

Risks Associated With Our Business

Our business is subject to a number of risks that you should be aware of before making a decision to invest in our common stock. These risks are discussed more fully in the section titled “Risk Factors” and include, among others:

| ∎ | If our sole semiconductor foundry in Minnesota is damaged or becomes inoperable, we will be unable to develop or produce wafers in a timely manner, if at all, and our business would be materially adversely affected. |

| ∎ | Our industry has experienced rapid technological changes, and new technologies may prove difficult to commercialize or may not gain market acceptance by our customers, which may have a material adverse effect on demand for our products and service offerings. |

| ∎ | Defects or performance problems in our products could result in loss of customers, reputational damage and decreased revenue, and we may face warranty, indemnity and product liability claims arising from defective products. |

| ∎ | If we do not achieve satisfactory yields or quality, our reputation and customer relationships could be harmed. |

| ∎ | Our customers may cancel their orders, change production quantities or delay production, and if we fail to forecast demand accurately, we may incur supply shortages or lose revenue. |

| ∎ | A material decrease in demand for products that contain semiconductors may decrease the demand for our services and products, and a decrease in the selling prices of our customers’ products may significantly affect our business, financial results and financial position. |

| ∎ | We have a finite amount of production capacity, and to the extent customer demand exceeds our capacity we may lose customers and potential revenues. |

| ∎ | We have a limited operating history as a standalone company, and we may have difficulty accurately predicting our future revenue for the purpose of appropriately budgeting and adjusting our expenses. |

| ∎ | A significant portion of our sales comes from one customer, the loss of which would adversely affect our financial results. |

| ∎ | We may not be able to successfully diversify our customer base and penetrate new markets which would negatively impact our growth strategy. |

| ∎ | We depend on successful parts and materials procurement for our foundry and a shortage, or an increase in the price, of these raw materials could interrupt our operations and result in a decline in revenues. |

| ∎ | A breach of our security systems or a cyber-attack that disrupts our operations or results in the breach of confidential information about us, our technology or our customers could harm our business and expose us to costly regulatory enforcement and other liability. |

| ∎ | We operate in the highly cyclical semiconductor industry, which is subject to significant downturns that may negatively impact our results of operations. |

| ∎ | Because the markets in which we compete are highly competitive and many of our competitors have greater resources than us, we may not be able to compete successfully, and we may lose or be unable to gain market share. |

| ∎ | The effects of the coronavirus disease 2019, or COVID-19, pandemic could adversely affect our business, results of operations and financial condition. |

| ∎ | We are a party to several significant U.S. Government contracts, which are subject to unique risks. |

| ∎ | Changes to DoD business practices could have a material effect on the DoD’s procurement process and adversely impact our current programs and potential new awards. |

| ∎ | We depend on IP to succeed in our business, and any failure or inability to obtain, preserve, enforce, defend and protect our technologies or IP rights could harm our business and financial condition. |

7

Table of Contents

| ∎ | Our collaboration with others regarding the development of technologies and IP may result in disputes regarding ownership of or rights to use or enforce IP rights, which could harm our business and financial condition. |

| ∎ | We have elected to take advantage of the controlled company exemption from certain corporate governance requirements, which could make our common stock less attractive to some investors or otherwise adversely affect its trading price. |

| ∎ | A limited number of stockholders will have the ability to influence the outcome of director elections and other matters requiring stockholder approval. |

Corporate Information

Our principal executive offices are located at 2401 East 86th Street, Bloomington, Minnesota 55425. Our telephone number at that address is (952) 851-5200. Our website is www.skywatertechnology.com. Information appearing on, or that can be accessed through, our website is not a part of this prospectus.

We were originally formed on October 3, 2016 as a Delaware limited liability company under the name CMI Acquisition, LLC. We are a holding company that conducts operations through our wholly-owned subsidiaries, SkyWater Technology Foundry, Inc., which we refer to as SkyWater Technology Foundry, SkyWater Federal, LLC, which we refer to as SkyWater Federal, and SkyWater Florida, Inc., which we refer to as SkyWater Florida. SkyWater Technology Foundry is our principal operating subsidiary through which we provide our custom design and development services and wafer manufacturing. SkyWater Federal was established to bid on specific procurement contracts and operate as a prime contractor for the U.S. Government. Once approved, SkyWater Federal will coordinate support services for our U.S. Government contract-related activities within SkyWater Technology Foundry. SkyWater Florida was established to operate a center for technological research and development, including certain semiconductor manufacturing equipment, and an advanced water treatment facility in Osceola County, Florida.

Our operations were acquired in March 2017 as part of a divestiture from Cypress. In our current corporate structure, CMI Oxbow Partners, LLC, which we refer to as CMI Oxbow, a Delaware limited liability company affiliated with Oxbow Industries, LLC, owns all of our outstanding voting interests. Before the closing of this offering, we will convert into a Delaware corporation and change our name to SkyWater Technology, Inc. as described above under “Corporate Conversion.”

Emerging Growth Company Status

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, or the JOBS Act. For so long as we remain an emerging growth company, we are permitted and currently intend to rely on the following provisions of the JOBS Act that contain exceptions from disclosure and other requirements that otherwise are applicable to companies that conduct initial public offerings and file periodic reports with the SEC. The JOBS Act provisions:

| ∎ | permit us to include only two years of selected financial data in this prospectus; |

| ∎ | provide an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley Act; |

| ∎ | provide an extended transition period for complying with new or revised accounting standards; |

| ∎ | permit us to include reduced disclosure regarding executive compensation in this prospectus and our filings with the Securities and Exchange Commission, or SEC, as a public company; and |

| ∎ | provide an exemption from the requirement to hold a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute arrangements not previously approved. |

8

Table of Contents

We will remain an emerging growth company until:

| ∎ | the first to occur of the last day of the fiscal year (1) which follows the fifth anniversary of the completion of this offering, (2) in which we have total annual gross revenue of at least $1.07 billion or (3) in which the market value of our capital stock held by non-affiliates was $700 million or more as of the last business day of the preceding second fiscal quarter; or |

| ∎ | if it occurs before any of the foregoing dates, the date on which we have issued more than $1 billion in non-convertible debt over a three-year period. |

Even after we no longer qualify as an emerging growth company, we may still qualify as a “smaller reporting company” (as we do as of the date of this prospectus), which would allow us to take advantage of many of the same exemptions from disclosure requirements, including reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements.

Recent Developments

Preliminary Estimated Financial Results for the Three Months Ended April 4, 2021

Our preliminary estimated net sales and cost of sales for the three months ended April 4, 2021 are set forth below. We have provided a range for these preliminary financial results because our closing procedures for our fiscal quarter ended April 4, 2021 are not yet complete. Our preliminary estimates of the financial results set forth below are based solely on information available to us as of the date of this prospectus and are inherently uncertain and subject to change. Our preliminary estimates contained in this prospectus are forward-looking statements. Our actual results remain subject to the completion of management’s final review and our other closing procedures. These preliminary estimates are not a comprehensive statement of our financial results for the three months ended April 4, 2021 and should not be viewed as a substitute for full financial statements prepared in accordance with GAAP. In addition, these preliminary estimates for the three months ended April 4, 2021 are not necessarily indicative of the results to be achieved in any future period. Accordingly, you should not place undue reliance on these preliminary financial results. See “Risk Factors,” “Special Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of certain factors that could result in differences between the preliminary estimated financial results reported below and the actual results. Our actual financial statements and related notes as of and for the three months ended April 4, 2021 are not expected to be filed with the SEC until after this offering is completed.

The preliminary estimated financial results included in this prospectus have been prepared by, and are the responsibility of, our management. Our independent registered public accounting firm, Deloitte & Touche LLP, has not audited, reviewed, compiled or performed any procedures with respect to the preliminary financial results. Accordingly, Deloitte & Touche LLP does not express an opinion or any other form of assurance with respect thereto.

Our fiscal quarter ends on the Sunday closest to the end of the calendar month. We refer to the three-month period ended April 4, 2021 as the three months 2021, which contained 13 weeks.

For the three months 2021, we estimate that our net sales will range from $45 million to $47 million. We anticipate that our net sales for the three months 2021 will be driven by strong demand in Wafer Services as well as continued momentum in sales of our Advanced Technology Services. We expect Wafer Services sales of $9 million to $10 million, principally driven by continued demand in the automotive and transportation market. We expect Advanced Technology Services sales of $36 million to $37 million, which includes $15 million of sales related to services we provide to qualify customer funded tool technologies, as our customers invest in our capabilities to expand our technology platforms, principally within the aerospace and defense and advanced computing markets.

For the three months 2021, we estimate that our cost of sales will range from $37 million to $39 million. We expect our cost of sales to be impacted by the high costs we incur related to qualification of customer funded tool technologies, additional depreciation from property and equipment that was placed into service in the fourth quarter of 2020 and increased direct costs as we expand our workforce in both Minnesota and Florida.

9

Table of Contents

THE OFFERING

| Issuer |

SkyWater Technology, Inc. |

| Common stock offered by us |

5,800,000 shares |

| Common stock offered by us pursuant to the underwriters’ over-allotment option to purchase additional shares |

870,000 shares |

| Common stock to be outstanding after this offering |

36,855,729 shares (or 37,725,729 shares, if the underwriters exercise their over-allotment option in full) |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $66.2 million, or approximately $76.7 million if the underwriters exercise their over-allotment option in full, at an assumed initial public offering price of $13.00 per share, which is the midpoint of the estimated price range set forth on the cover page of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. |

| We intend to use the net proceeds we receive from this offering for working capital and other general corporate purposes, including financing our growth and funding capital expenditures. We may use a portion of the proceeds from this offering for acquisitions or strategic investments in businesses or technologies, although we do not currently have any plans or commitments for any such acquisitions or investments. For information about our proposed use of proceeds, see “Use of Proceeds.” |

| Risk factors |

You should read the “Risk Factors” section of this prospectus and the other information in this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Proposed Nasdaq Capital Market symbol |

“SKYT” |

Unless otherwise indicated, the number of shares of our common stock that will be outstanding immediately after this offering as stated in this prospectus gives effect to the Corporate Conversion, and excludes:

| ∎ | 5,000,000 shares of our common stock reserved for future issuance under our 2021 Equity Incentive Plan, or the 2021 Plan, which will become effective following the Corporate Conversion, including 1,899,774 shares of our common stock issuable pursuant to grants of restricted stock units and stock options to be made before the closing of this offering, based on the assumed initial public offering price of $13.00 per share; |

| ∎ | 700,000 shares of our common stock reserved for issuance under our 2021 Employee Stock Purchase Plan, or the ESPP; and |

| ∎ | 2,328,886 shares of our common stock reserved for issuance pursuant to outstanding restricted stock units held by certain of our employees. |

10

Table of Contents

Except as otherwise indicated, all information in this prospectus reflects and assumes the following:

| ∎ | the completion of the Corporate Conversion, as a result of which all of the outstanding limited liability company interests of CMI Acquisition, LLC will automatically be converted into an aggregate of 31,055,729 shares of our common stock; |

| ∎ | the filing of our certificate of incorporation in the State of Delaware and the adoption of our bylaws, each of which will be in effect prior to the closing of this offering; and |

| ∎ | no exercise by the underwriters of their over-allotment option to purchase additional shares of our common stock. |

In connection with this offering, we expect to grant restricted stock units with an aggregate fixed dollar value of $9.2 million and stock options with an exercise price equal to the initial public offering price and an aggregate fair value of $5.9 million. Based on an assumed initial public offering price of $13.00 per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, we will grant 705,997 restricted stock units and options to purchase 1,193,777 shares of our common stock. A $1.00 decrease in the initial public offering price will increase the aggregate number of shares underlying the restricted stock units and stock options by 158,315 shares. A $1.00 increase in the initial public offering price will decrease the aggregate number of shares underlying the restricted stock units and stock options by 135,698 shares.

11

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables set forth a summary of our historical consolidated financial data as of and for the periods indicated. The summary consolidated statements of operations data for the years ended January 3, 2021 and December 29, 2019 and the summary consolidated balance sheet data as of January 3, 2021 and December 29, 2019 have been derived from our audited consolidated financial statements and related notes thereto included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results to be expected in the future. When you read this summary consolidated financial data, it is important that you read it together with the historical consolidated financial statements and the related notes thereto included elsewhere in this prospectus, which qualify this summary consolidated financial data in their entirety, as well as the sections of this prospectus titled “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Our consolidated statements of operations for the years ended January 3, 2021 and December 29, 2019 contain 53 and 52 weeks, respectively.

| YEAR ENDED JANUARY 3, 2021 |

YEAR ENDED DECEMBER 29, 2019 |

|||||||

| (in thousands, except unit and per unit data) | ||||||||

| Consolidated Statement of Operations Data: |

||||||||

| Net sales |

$ | 140,438 | $ | 136,725 | ||||

| Cost of sales |

117,746 | 111,379 | ||||||

|

|

|

|

|

|||||

| Gross profit |

22,692 | 25,346 | ||||||

| Selling and marketing expenses |

7,778 | 4,326 | ||||||

| Research and development |

4,208 | 6,330 | ||||||

| General and administrative expenses |

17,254 | 14,390 | ||||||

| Change in fair value of contingent consideration |

2,094 | 9,271 | ||||||

|

|

|

|

|

|||||

| Operating loss |

(8,642 | ) | (8,971 | ) | ||||

| Other income (expense): |

||||||||

| Change in fair value of warrant liability |

780 | (4,460 | ) | |||||

| Loss on debt modification and extinguishment |

(1,434 | ) | — | |||||

| Interest expense |

(5,499 | ) | (6,547 | ) | ||||

|

|

|

|

|

|||||

| Total other income (expense) |

(6,153 | ) | (11,007 | ) | ||||

|

|

|

|

|

|||||

| Loss before income taxes |

(14,795 | ) | (19,978 | ) | ||||

| Income tax expense (benefit) |

4,919 | (3,559 | ) | |||||

|

|

|

|

|

|||||

| Net loss |

(19,714 | ) | (16,419 | ) | ||||

| Less: net income attributable to non-controlling interests |

903 | — | ||||||

|

|

|

|

|

|||||

| Net loss attributable to CMI Acquisition, LLC |

$ | (20,617 | ) | $ | (16,419 | ) | ||

|

|

|

|

|

|||||

| Net loss per unit attributable to CMI Acquisition, LLC, basic and diluted (1) |

$ | (1.15 | ) | $ | (0.91 | ) | ||

| Weighted average units used in computing net loss per unit, basic and diluted |

18,000,000 | 18,000,000 | ||||||

| (1) | Pro forma net loss per unit giving effect to the Corporate Conversion has not been presented as we believe such conversion will not result in a material reduction to net loss per unit. |

12

Table of Contents

| (in thousands) |

JANUARY 3, 2021 |

DECEMBER 29, 2019 |

||||||

| Consolidated Balance Sheet Data: |

||||||||

| Cash and cash equivalents |

$ | 7,436 | $ | 4,605 | ||||

| Working capital (deficit) (1) |

$ | (9,755 | ) | $ | 37,946 | |||

| Total assets |

$ | 263,209 | $ | 190,435 | ||||

| Long-term debt (2) |

$ | 71,824 | $ | 49,720 | ||||

| Total liabilities |

$ | 264,793 | $ | 166,268 | ||||

| Total members’ equity (deficit) |

$ | (1,584 | ) | $ | 24,167 | |||

| (1) | Working capital (deficit) is defined as current assets minus current liabilities. |

| (2) | Long-term debt represents the long-term portion of the term loan (for 2019), line of credit (for 2019), amended and restated revolving credit agreement, financing agreement, paycheck protection loan and contingent consideration, inclusive of debt issuance costs. |

| (in thousands) |

YEAR ENDED JANUARY 3, 2021 |

YEAR ENDED DECEMBER 29, 2019 |

||||||

| Non-GAAP Financial Data: |

||||||||

| Adjusted EBITDA (1) |

$ | 13,500 | $ | 21,879 | ||||

| (1) | We define adjusted EBITDA as net income before interest expense, income tax provision (benefit), depreciation and amortization, equity-based compensation and certain other items that we do not view as indicative of our ongoing performance, including fair value changes in contingent consideration, equity-based compensation, fair value changes in warrants and management fees. Adjusted EBITDA is a financial measure that is not required by, or presented in accordance with generally accepted accounting principles in the United States, or GAAP. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measure” for our reasons for presenting non-GAAP financial measures and for a reconciliation to the most directly comparable GAAP measure. |

13

Table of Contents

An investment in our common stock involves a high degree of risk. You should carefully read and consider the risks described below, together with all of the other information in this prospectus, including our consolidated financial statements and the related notes thereto and the section of this prospectus entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding to purchase shares of our common stock. The following risks could materially and adversely affect our business, financial condition, results of operation or cash flows. In any such case, the trading price of shares of our common stock could decline and you could lose all or part of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations.

Risks Relating to Our Business and Our Industry

If our sole semiconductor foundry is damaged or becomes inoperable, we will be unable to develop or produce wafers in a timely manner, if at all, and our business would be materially adversely affected.

We currently perform all of our manufacturing services and most of our design services at our foundry in Bloomington, Minnesota. Our foundry operation and the equipment we use to manufacture wafers would be costly to replace and could require substantial lead time to repair or replace. Our foundry may be harmed or rendered inoperable by physical damage from fire, floods, tornadoes, power loss, telecommunications failures, break-ins and similar events, which may render it difficult or impossible for us to produce or test products for a considerable period of time. If any of the foregoing events occur, we may incur significant additional costs including, among other things, loss of profits due to unplanned temporary or permanent shutdowns of our foundry, cleanup costs, liability for damages or injuries, legal expenses and reconstruction expenses, which would harm our results of operations and financial condition. In addition, because any substitute facility must hold any required licensures or certifications, we may be limited in our ability to rely on a third-party to perform interim design and manufacturing services or testing processes. We cannot assure you that we would be able to find another semiconductor foundry that is capable or willing to design and produce wafers in compliance with applicable specifications, or that such a substitute foundry would be willing to produce wafers for us on commercially reasonable terms. A substitute foundry may not have rights to intellectual property of others that is necessary to design, manufacture, and test products for us, and we may not be permitted to extend our license rights to a substitute foundry. Any unexpected constraints on our foundry’s ability to design, manufacture or test products could result in the loss of customers or harm our reputation, and we may be unable to regain those customers in the future, all of which would materially adversely affect our business.

Our industry has experienced rapid technological changes, and new technologies may prove difficult to commercialize or may not gain market acceptance by our customers, which may have a material adverse effect on demand for our products and service offerings.

The industry in which we operate is subject to constant technological change, industry standards and technological obsolescence. Our future success will depend on our ability to appropriately respond to changing technologies, including significant developments in wafer production, and changes in function of products and quality in a timely and cost-effective basis. If we adopt products and technologies that are not attractive to customers, we may not be successful in capturing or retaining our share of the market. If we fail to adopt enhanced technologies or processes, we could experience product obsolescence, loss of competitiveness of our products, decreased revenue and a loss of market share to competitors. In addition, some new technologies are relatively untested and unperfected and may not perform as expected or as desired, in which event our adoption of such products or technologies may cause us to lose money.

Defects or performance problems in our products could result in loss of customers, reputational damage and decreased revenue, and we may face warranty, indemnity and product liability claims arising from defective products.

Although our products are tested to meet our stringent quality requirements, they may contain undetected errors or defects, especially when first introduced or when new generations are released. Errors, defects or poor performance can arise due to design flaws, defects in raw materials or components or manufacturing errors or difficulties, which can affect both the quality and the yield of the product. Any actual or perceived errors, defects or poor performance in our products could result in the replacement or recall of our products, shipment delays, rejection of our products,

14

Table of Contents

damage to our reputation, lost revenue, diversion of our engineering personnel from our product development efforts and increases in customer service and support costs, all of which could have a material adverse effect on our business, financial condition and results of operations. We typically provide a one year warranty on the operability of the products we design and manufacture. Defective components may give rise to warranty, indemnity or product liability claims against us that exceed any revenue or profit we receive from the affected products.

If we do not achieve satisfactory yields or quality, our reputation and customer relationships could be harmed.

The fabrication of wafers is a complex and technically demanding process. Minor deviations in the manufacturing process can cause substantial decreases in yields and, in some cases, cause production to be suspended. Our foundry could, from time to time, experience manufacturing defects and reduced manufacturing yields. Changes in manufacturing processes or the inadvertent use of defective or contaminated materials could result in lower than anticipated production yields or unacceptable performance of our wafers. Many of these problems are difficult to detect at an early stage of the manufacturing process and may be time-consuming and expensive to correct. We also may experience manufacturing problems in achieving acceptable yields as a result of, among other things, transferring production to other facilities, upgrading or expanding existing facilities or changing our process technologies. Poor production or defects, integration issues or other performance problems in our solutions could significantly harm our customer relationships and financial results and give rise to financial or other damages to our customers.

Our customers may cancel their orders, change production quantities or delay production, and if we fail to forecast demand accurately, we may incur supply shortages or lose revenue.

We generally do not obtain firm, long-term purchase commitments from our customers. Because production lead times often exceed the amount of time required to fulfill orders, we often must build our products in advance of orders, relying on an imperfect demand forecast to optimize use of our manufacturing capacity.

Our demand forecast accuracy can be adversely affected by a number of factors, including inaccurate forecasting by our customers, changes in market conditions, and demand for our customers’ products. Even after an order is received, our customers may cancel these orders or request a decrease in production quantities. Any such cancellation or decrease subjects us to a number of risks, most notably that our projected sales will not materialize on schedule or at all, leading to unanticipated revenue shortfalls and excess manufacturing capacity. Either underestimating or overestimating demand could lead to insufficient, excess or obsolete inventory, which could harm our operating results, cash flow and financial condition, as well as our relationships with our customers.

A material decrease in demand for products that contain semiconductors may decrease the demand for our services and products, and a decrease in the selling prices of our customers’ products may significantly affect our business, financial results and financial position.

Our customers generally use the semiconductors produced in our fab in a wide variety of applications. Any significant decrease in the demand for end-market devices or products may decrease the demand for our services and products. In addition, if the average selling prices of key end-market devices or products decline significantly, we may be pressured to reduce our selling prices, which may reduce our revenues and margins significantly. As demonstrated in the past by downturns in demand for high technology products, market conditions can change rapidly, without warning or advance notice. In such instances, our customers may experience inventory buildup or difficulties in selling their products and, in turn, may reduce or cancel orders for wafers from us, which may harm our business and profitability. The timing, severity and recovery of these downturns cannot be predicted. In order for demand for our wafer fabrication services to increase, the markets for the end products utilizing the integrated circuits that we manufacture must develop and expand. Because our services may be used in many new applications, it is difficult to forecast demand. If demand is lower than expected, we may have excess capacity and our revenue may not be sufficient to cover all our costs and serve all our debt, which may adversely affect our financial results and financial position.

We have a finite amount of production capacity, and to the extent customer demand exceeds our capacity we may lose customers and potential revenues.

In periods during which demand for our foundry services exceeds our capacity and manufacturing capabilities, we may be unable to (1) fulfill customer demand in whole or in part, in a timely manner or at all, (2) assure production of customers’ next-generation products or (3) provide additional capacity through transfer of process technologies, or ensure successful implementation. However, we could lose one or more of our current or potential customers, which may adversely affect our revenues, profitability and business.

15

Table of Contents

We have a limited operating history as a standalone company, and we may have difficulty accurately predicting our future revenues for the purpose of appropriately budgeting and adjusting our expenses.

We were divested from Cypress in 2017. Our limited operating experience as a standalone company, the dynamic and rapidly evolving market in which we sell our products, our dependence on a limited number of customers, as well as numerous other factors beyond our control, may impede our ability to forecast quarterly and annual revenues accurately. As a result, we could experience budgeting and cash flow management problems, unexpected fluctuations in our results of operations and other difficulties, any of which could make it difficult for us to gain and maintain profitability and could increase the volatility of the market price of our common stock.

A significant portion of our sales comes from five customers, the loss of which would adversely affect our financial results.

Cypress, which was acquired in April 2020 by Infineon Technologies AG, accounted for approximately 29% and 48% of our revenue for the fiscal years ended January 3, 2021 and December 29, 2019, respectively. Four of our non-Cypress customers accounted for 30%, 20%, 19% and 18% of our outstanding accounts receivable as of January 3, 2021, and two of our non-Cypress customers represent 16% and 14% of our revenues for the year ended January 3, 2021. If we were to lose these key customers or experience a significant decrease in volume or sales prices, our financial results would be adversely affected. We currently sell to a relatively small number of customers in total, and we expect our operating results will likely continue to depend on sales to a relatively small number of customers for the foreseeable future. We cannot be certain that these customers will generate significant revenue for us in the future or if these customer relationships will continue to develop. If our relationships with our other customers do not continue to develop, we may not be able to expand our customer base or maintain or increase our revenue. In addition, the loss or reduction in volume or sales price, whether due to their insolvency, or their unwillingness or inability to perform their obligations under their respective relationships with us, or if we are unable to renew or engagements with them in commercially reasonable terms, or attract new customers to replace such lost business, may materially negatively impact our overall business. This is exacerbated by our current manufacturing constraints which limit our ability to sell to other customers. In addition, our business is affected by competition in the market for the end products that our customers sell, and any decline in their business could harm our business and cause our revenue to decline.

We may not be able to successfully diversify our customer base and penetrate new markets which would negatively impact our growth strategy.

Our growth strategy depends on our ability to diversify our customer base and penetrate new markets. Our ability to add new customers to our Advanced Technology Services and Wafer Services businesses is subject to various elements outside of our control, such as fluctuations in demand for discrete components in both commodity and differentiated categories. If we are unable to attract new customers our customer revenue could remain highly concentrated. In addition, even if we add new customers, they may not require high levels of production, negatively impacting our growth strategy. Our growth strategy may also be adversely affected if we are unable to enter new markets, such as rad-hard electronic markets. Because we face competition from companies with substantially greater production and marketing resources than we have, we may not be able to penetrate these new markets successfully.

Our expansion strategy carries inherent risks.