Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - IMPEL NEUROPHARMA INC | d121817dex231.htm |

| EX-21.1 - EX-21.1 - IMPEL NEUROPHARMA INC | d121817dex211.htm |

| EX-10.11 - EX-10.11 - IMPEL NEUROPHARMA INC | d121817dex1011.htm |

| EX-10.10 - EX-10.10 - IMPEL NEUROPHARMA INC | d121817dex1010.htm |

| EX-10.9 - EX-10.9 - IMPEL NEUROPHARMA INC | d121817dex109.htm |

| EX-10.3 - EX-10.3 - IMPEL NEUROPHARMA INC | d121817dex103.htm |

| EX-10.2 - EX-10.2 - IMPEL NEUROPHARMA INC | d121817dex102.htm |

| EX-4.3 - EX-4.3 - IMPEL NEUROPHARMA INC | d121817dex43.htm |

| EX-4.2 - EX-4.2 - IMPEL NEUROPHARMA INC | d121817dex42.htm |

| EX-3.3 - EX-3.3 - IMPEL NEUROPHARMA INC | d121817dex33.htm |

| EX-3.1 - EX-3.1 - IMPEL NEUROPHARMA INC | d121817dex31.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 2, 2021

|

Registration No. 333- |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

IMPEL NEUROPHARMA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 2834 | 26-3058238 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

201 Elliott Avenue West, Suite 260

Seattle, WA 98119

(206) 568-1466

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Adrian Adams

President and Chief Executive Officer

Impel NeuroPharma, Inc.

201 Elliott Avenue West, Suite 260

Seattle, WA 98119

(206) 568-1466

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Alan C. Smith Amanda L. Rose Ryan Mitteness Fenwick & West LLP 1191 Second Avenue, Floor 10 Seattle, WA 98101 (206) 389-4510 |

Michael Nordtvedt Bryan D. King Tony Jeffries Wilson Sonsini Goodrich & Rosati, Professional Corporation 701 Fifth Avenue, Suite 5100 Seattle, WA 98104 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||

| Common Stock, par value $0.001 per share |

$75,000,000 | $8,183 | ||

|

| ||||

|

| ||||

| (1) | The proposed maximum aggregate offering price includes the offering price of additional shares that the underwriters have the option to purchase. |

| (2) | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PROSPECTUS (Subject to Completion) |

Dated April 2, 2021 |

Shares

Impel NeuroPharma, Inc.

Common Stock

This is an initial public offering of shares of our common stock. We are offering shares of our common stock. Prior to this offering, there has been no public market for our common stock. We will apply for listing of our common stock on The Nasdaq Global Market under the symbol “IMPL.” We expect that the public offering price will be between $ and $ per share.

We have granted the underwriters an option to purchase up to additional shares of our common stock at the initial public offering price, less underwriting discounts and commissions. We intend to apply to list our common stock on The Nasdaq Global Market under the symbol “IMPL.”

We are an “emerging growth company” under applicable Securities and Exchange Commission rules and will be subject to reduced public company reporting requirements for this prospectus and future filings.

Our business and an investment in our common stock involve significant risks. These risks are described under the caption “Risk Factors” beginning on page 14 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds, before expenses, to Impel NeuroPharma, Inc. |

$ | $ | ||||||

| (1) | See the section titled “Underwriting” for additional information regarding underwriting compensation. |

The underwriters may also purchase up to an additional shares from us at the public offering price, less underwriting discounts and commissions, within 30 days from the date of this prospectus to cover overallotments.

The underwriters expect to deliver the shares against payment in New York, New York on , 2021.

Joint Book-Running Managers

| Cowen | Guggenheim Securities |

Lead Manager

Wedbush PacGrow

, 2021

Table of Contents

| Page | ||||

| 1 | ||||

| 14 | ||||

| 65 | ||||

| 67 | ||||

| 68 | ||||

| 69 | ||||

| 70 | ||||

| 73 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

77 | |||

| 89 | ||||

| 134 | ||||

| 144 | ||||

| 156 | ||||

| 160 | ||||

| 163 | ||||

| 169 | ||||

| Material U.S. Federal Income Tax Consequences to Non-U.S. Holders |

172 | |||

| 177 | ||||

| 184 | ||||

| 184 | ||||

| 184 | ||||

| F-1 | ||||

We have not, and the underwriters have not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock.

Persons who come into possession of this prospectus and any applicable free writing prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus and any such free writing prospectus applicable to that jurisdiction.

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes and the information set forth under the sections titled “Risk Factors,” “Summary Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included in this prospectus. Some of the statements in this prospectus constitute forward-looking statements that involve risks and uncertainties. See the section titled “Special Note Regarding Forward-Looking Statements.” Unless the context otherwise requires, we use the terms “Impel,” “company,” “we,” “us” and “our” in this prospectus to refer to Impel NeuroPharma, Inc.

Overview

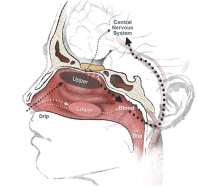

We are a late-stage pharmaceutical company focused on utilizing our proprietary technology to develop and commercialize transformative therapies for patients suffering from diseases with high unmet medical needs, with an initial focus on diseases of the central nervous system, or CNS. Our company was founded on the premise that the upper nasal cavity can be an optimal treatment entry point for CNS and other diseases where rapid vascular absorption can result in superior clinical outcomes. Our strategy is to pair our proprietary Precision Olfactory Delivery, or POD, upper nasal delivery technology with well-established therapeutics or other therapeutics where rapid vascular absorption is preferred to drive therapeutic benefit, improve patient outcomes, reduce drug development risk and expand the commercial opportunity within our target diseases. Since 2016, we have identified and advanced multiple product candidates, including TRUDHESATM (INP104) for the acute treatment of migraine and INP105 for the acute treatment of agitation and aggression in patients with Autism Spectrum Disorder, or ASD. Our pipeline of proprietary product candidates also includes INP107 for the treatment of OFF episodes in Parkinson’s Disease. In November 2020, we submitted an NDA for TRUDHESA, for the acute treatment of migraine headaches with or without aura in adult patients. The FDA has filed and accepted the new drug application, or NDA, for review and established a Prescription Drug User Fee Act, or PDUFA, goal date of September 6, 2021.

We have designed our proprietary POD technology to target the vascular-rich upper nasal cavity, and to provide rapid absorption, consistent drug biodistribution and ease of use for a patient, provider or caregiver. Our goal with our POD technology is to deliver injection-like clinical outcomes non-invasively. We believe that we are the first company to successfully harness the benefits of delivery to the upper nasal cavity to improve delivery and the pharmacologic potential of CNS therapies.

1

Table of Contents

We have developed a pipeline of proprietary CNS product candidates built around our intellectual property and expertise in upper nasal cavity delivery. The following table summarizes our product candidates, each of which is wholly owned:

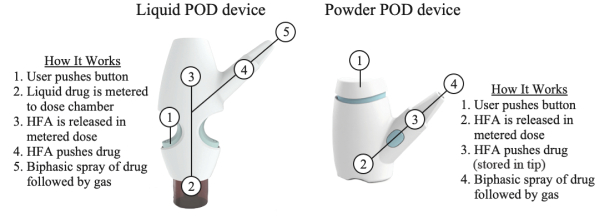

POD Technology

Using our proprietary POD technology, we have developed devices that deliver therapeutics directly to the upper nasal cavity. These devices are designed to offer several key benefits compared to traditional nasal delivery systems, including:

| ∎ | Rapid Onset. The precise spray plume and biphasic nature of delivery to the upper nasal cavity allows for superior dose deposition and rapid absorption into the systemic circulation as compared to traditional nasal delivery systems. |

| ∎ | Consistent Drug Bioavailability. Metered propellant dosing allows for more consistent blood levels than typically seen with traditional nasal sprays and are equivalent, or superior, to those achieved through intramuscular, or IM, injections. |

| ∎ | Improved Patient-Provider Experience. Our proprietary gas propulsion mechanism eliminates the need for coordination of breathing and enables delivery of a dosing in 1/10th of a second, enabling self- or provider-administration in a manner that improves patient comfort and compliance. |

| ∎ | Manufacturability. Separation of propellant and drug within the POD device helps streamline chemistry, manufacturing and controls, or CMC, development, as we are not constrained by the limits of co-formulating our therapeutics inside of a pressurized propellant canister. |

| ∎ | Formulation Versatility. The POD device is versatile and can deliver both liquid and powder formulations in order to potentially address a wide variety of indications across multiple therapeutic areas. |

| ∎ | Strong Intellectual Property Position. We believe that we have a strong global intellectual property position relating to our POD device and product candidates. We have four U.S. issued patents and 21 patents issued in ex-U.S. jurisdictions directed to our approach of drug delivery to the upper nasal cavity, including claims directed to a nasal device with separate drug and propellant compartments. Our patent portfolio is expected to provide patent protection ranging from 2032 to 2040. |

2

Table of Contents

We believe that our in-house technical and development expertise positions us to address unmet medical needs across multiple therapeutic areas by delivering well-established and novel drugs consistently, rapidly and non-invasively. Our technical and development expertise has allowed us to rapidly identify and develop our product candidates to their current state in under five years. For example, INP105 was advanced from lead candidate selection to development of more than 20 formulations, the completion of five nonclinical studies, and ultimately a proof-of-concept clinical trial, within 16 months. We have tested over 30 small molecules and biologics for suitability of nasal drug administration with our proprietary POD technology. This depth of knowledge and experience, along with our proprietary technology, creates a platform for rapid additional pipeline expansion. In addition to our technology and development expertise, our strong intellectual property portfolio protects multiple aspects of our approach to delivering drug to the upper nasal cavity. We believe that our apparatus, composition of matter and method of use intellectual property can provide strong exclusivity protection to our product candidates.

Our Product Candidates

TRUDHESA (Acute Treatment of Migraine)

We are currently developing our lead product candidate, TRUDHESA (INP104), as an upper nasal formulation of dihydroergotamine, or DHE, administered using our proprietary POD technology for the acute treatment of migraine. The brand name TRUDHESA has been conditionally approved by the FDA. Migraine is a growing market projected to triple in size to over $10 billion by 2028 with the introduction of multiple new product offerings and an expected increase in disease diagnosis. DHE is widely used as part of a standard of care for treatment of migraines, despite being limited by intravenous, or IV, and injection delivery or traditional nasal administration. IV and injection delivery require administration in physicians’ offices, migraine clinics and hospitals, and traditional nasal administration has been challenged by inconsistent efficacy.

In June 2020, we announced the following exploratory efficacy results of our STOP301 trial to evaluate the safety and tolerability of long-term, intermittent use of TRUDHESA as an acute treatment of migraine with or without aura in adult patients. In this trial, baseline results prior to trial initiation were based on migraine attacks where patients used their standard acute migraine medication. In the trial:

| ∎ | 38% of patients were pain free at two hours after their first dose of TRUDHESA. |

| ∎ | 52% of patients receiving TRUDHESA were free of their most bothersome migraine symptom at two hours. |

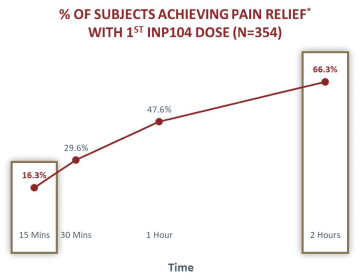

| ∎ | Patients treated with TRUDHESA also demonstrated improvement in pain relief: 16% of patients treated with TRUDHESA had pain relief within 15 minutes of treatment, and 66% had pain relief within two hours. |

The exploratory endpoints of the trial also included an assessment of the following long-term outcomes of TRUDHESA when patients were treated for six months:

| ∎ | 38% of patients treated with TRUDHESA remained pain free at two hours through three months of treatment and 34% of patients treated with TRUDHESA remained pain free at two hours through six months of treatment. |

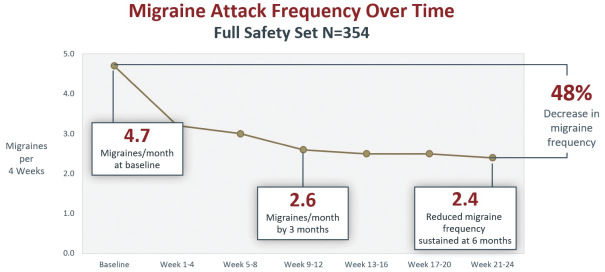

| ∎ | Patients who received TRUDHESA saw a 48% reduction in the frequency of their migraines compared to baseline during the six-month trial. |

| ∎ | 98% and 95% of patients achieving pain freedom at two hours on TRUDHESA did not suffer a relapse in migraine or require a rescue medication at 24 hours and 48 hours, respectively, by weeks 21 to 24. |

3

Table of Contents

| ∎ | Exposure Adjusted Event Rate, or EAER, data showed a meaningful reduction in the usage of healthcare resources by patients treated with TRUDHESA versus their baseline. Emergency room visits were reduced by approximately 73% and hospitalizations and urgent care visits were reduced by 100%. |

Although the trial was not powered to determine statistical significance of the exploratory efficacy endpoints, we believe these exploratory endpoints provide important data for evaluating the clinical benefit of TRUDHESA and showed consistency with the generally understood benefits of DHE for the acute treatment of migraines. The primary endpoints of the STOP301 trial were safety and tolerability of long-term, intermittent use. In this trial, TRUDHESA was generally well tolerated. There were a total of seven treatment emergent serious adverse events, or SAEs among five patients (1.4%) over the 52-week study. Three patients had one SAE each, consisting of one event each of ovarian mass, intestinal obstruction and miscarriage. Two patients had more than one SAE: one patient with a pulmonary embolism and visual impairment and one patient with clavicle and rib fractures. None of the SAEs were nasal-related and none of the SAEs, were determined by the investigator to be related to TRUDHESA or led to withdrawal from the trial. There were also no significant changes to sense of smell, and no significant abnormal findings from endoscopy examinations.

In November 2020, we submitted an NDA for TRUDHESA for the acute treatment of migraine headaches with or without aura in adult patients. The FDA has filed and accepted the NDA for review and established a PDUFA goal date of September 6, 2021. The brand name TRUDHESA has been conditionally approved by the FDA.

If approved, we believe we can successfully commercialize TRUDHESA in the United States with a specialty sales force beginning with approximately 60 representatives, and increasing to approximately 120 representatives, focusing in areas with increased demand. We intend to strategically pursue high value prescribers and early adopters, beginning with 8,000 of the highest volume migraine treatment prescribers. Based on recent migraine treatment product launches, such as ubrogepant and rimegepant, we believe this approach can be successful in accessing the concentrated prescriber bases in migraine. This target base includes approximately 4,000 neurologists and approximately 4,000 high prescribing primary care physicians and headache specialists who have significant experience with prescribing DHE. These groups make up 35% of the migraine treatment prescriptions written in 2020 in the United States. In particular, neurologist prescription productivity has grown an average of approximately 15% per year over the last two years, a growth figure aided by an increase in the number of patients seeking treatment from neurologists and primary care physicians for migraine. The planned scale up to 120 representatives is intended to allow us to target an additional 8,000 high prescribing physicians that we believe will enable us to expand coverage to 45% of all migraine treatment prescriptions in the United States. We intend to build a commercial infrastructure focused on distribution, access, promotion, education and customer support. Our market research indicates that over 70% of migraine sufferers are seeking better treatments, and physicians are willing to prescribe and payors support access at profitable price and rebate points. With approximately 72% of migraine prescriptions paid by commercial payors, we believe this market presents an attractive payor mix. We anticipate using a robust sample program to ensure trial with TRUDHESA for patients seeking better treatments and outcomes. Also, as part of our commercialization strategy, we plan to educate healthcare practitioners and patients, partner with national associations and actively support advocacy groups in the migraine market. These efforts will be supplemented with non-personal promotion to all targeted and non-targeted medium value physicians. To capture the maximum commercial opportunity of TRUDHESA, we may also selectively seek partners to commercialize the product outside of our target markets, including additional penetration within the broader primary care setting, as well as in geographies outside of the United States.

4

Table of Contents

INP105 (Acute Treatment of Agitation and Aggression in Autism Spectrum Disorder)

We are currently developing our second product candidate, INP105, as an upper nasal formulation of olanzapine administered using our proprietary POD technology for the treatment of agitation and aggression associated with ASD. ASD is a neurodevelopmental disorder affecting approximately 3.5 million children and adults in the United States and characterized by persistent difficulties in social communication and social interaction, coupled with restricted, repetitive patterns of behavior and higher aggression rates. Agitation and aggression are frequent and difficult to manage symptoms, and associated with negative outcomes for patients with ASD and their caregivers, including decreased quality of life, increased stress levels, and reduced availability of educational and social support. Based on a study of emergency room usage in Canada, which found that 18% of individuals with ASD aged 12 and up had visited the emergency room within the past year, and that approximately 34% of such visits were for mental health issues, we estimate that approximately 220,000 patients with ASD in the United States seek emergency room care due to mental health issues annually. Current treatment strategies include functional behavioral assessment, reinforcement strategies, functional communication training, and the use of second-generation antipsychotics. With an increasing rate of ASD diagnosis, we believe that the development of effective therapeutic and pharmacologic methods for preventing and treating aggression are essential to improving outcomes in this disorder. Currently, there is no approved treatment for patients living with ASD once there is onset of agitation leading to aggression, and we believe that INP105 has the potential to be an on-demand therapy in this indication.

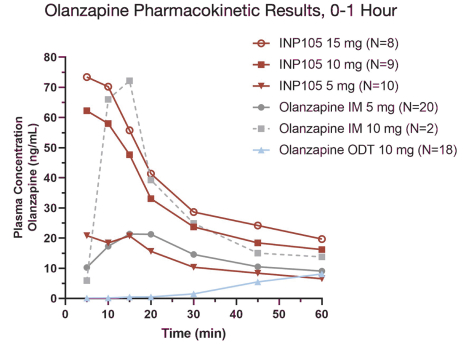

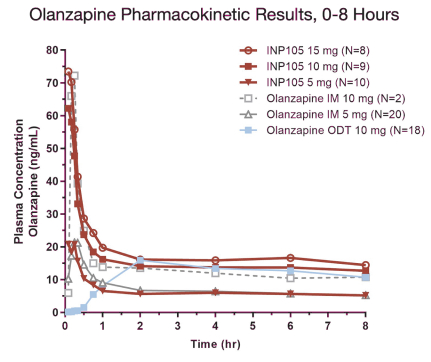

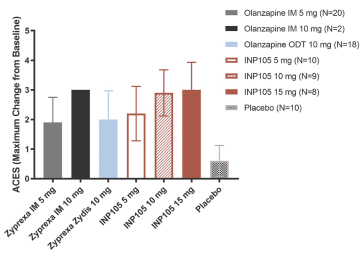

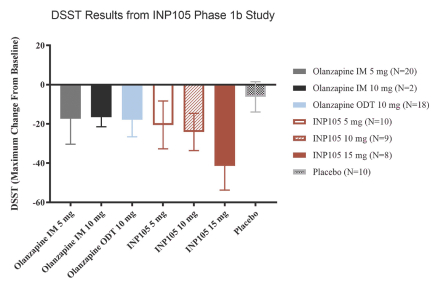

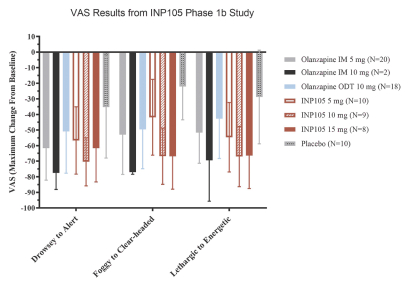

In a double-blind, placebo-controlled, single ascending dose Phase 1 clinical trial in 40 healthy adults conducted in Australia, we observed similar bioavailability for INP105 compared to equivalent doses of olanzapine delivered through IM administration, as measured by the area under the plasma drug concentration-time curve, or AUC, which reflects the actual body exposure to the drug after administration of a drug dose, and the maximum drug concentration, or Cmax, and achieved time to maximum drug concentration, or Tmax, 25-22% faster than that of IM olanzapine.

Based on its pharmacokinetic profile and method of administration, we believe INP105, if approved, has the potential to treat acute agitation and aggression events in this under-served population and in patients’ homes, potentially reducing visits to the emergency department and limiting the need to call in reinforcements to help caregivers. We plan to initiate a double-blind, placebo-controlled Phase 2 proof-of-concept clinical trial of INP105 in adolescents with ASD in the United States by the end of 2021 and expect to report topline results in the second half of 2022.

INP107 (Treatment of OFF Episodes in Parkinson’s Disease)

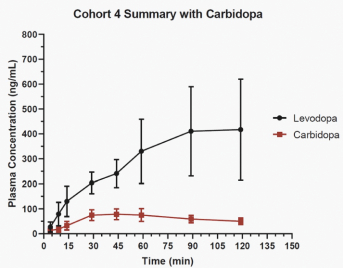

We are also currently developing INP107 as an upper nasal formulation of carbidopa/levodopa administered using our proprietary POD technology for the treatment of OFF episodes in Parkinson’s Disease, or Parkinson’s. The overall Parkinson’s market is expected to grow to over $8.4 billion by 2026, with emerging treatments for OFF episodes contributing to that growth. Current standard of care for the symptomatic treatment of Parkinson’s is oral levodopa; however when levodopa levels fall below their therapeutic range, patients may lose adequate control of motor symptoms, which are referred to as OFF episodes. Carbidopa is co-administered with levodopa to slow levodopa’s rapid absorption, thereby increasing the amount of levodopa available for the symptoms of Parkinson’s. INP107 is a self- or caregiver-administered, upper nasal therapy candidate designed to provide rapid delivery of levodopa to the brain for the treatment of OFF episodes. In 2019, we completed a Phase 2a clinical trial of INP107 and a levodopa-only formulation in Australia, which demonstrated an encouraging pharmacokinetic profile in Parkinson’s patients. Based on results of the Phase 2a clinical trial, we expect to further develop the formulation of INP107 prior to advancing into additional clinical trials. We expect to initiate a Phase 1 pharmacokinetic and tolerability trial in Australia or the United States in 2022 for dose selection for additional clinical development of INP107.

5

Table of Contents

Our Team

We have assembled a team of scientific, clinical and business leaders with deep expertise in neuroscience and a track record of building, growing and transacting pharmaceutical companies. Our Chief Executive Officer, Adrian Adams, has over 25 years of pharmaceutical experience with an emphasis on commercialization and strategic execution. Our co-founder and Chief Scientific Officer, John Hoekman, Ph.D., has over 15 years of experience in investigating upper nasal drug delivery and nose-to-brain delivery, is an inventor of our proprietary POD technology, is widely recognized as a pioneer in upper nasal cavity drug delivery and has evaluated over 30 CNS targeting compounds with over six different modalities including small molecules, proteins, peptides and antibodies as opportunities for upper nasal cavity delivery. Our Chief Financial Officer, John Leaman, M.D., has over 15 years of pharmaceutical experience with an emphasis on public company financial oversight, corporate strategy and business development. Our Chief Medical Officer, Stephen Shrewsbury, M.B. ChB., has over 30 years of experience in developing pulmonary and nasal drug delivery and CNS therapies at pharmaceutical companies including GlaxoSmithKline, Aquinox Pharmaceuticals, AVI Biopharma and MAP Pharmaceuticals, where he led the development of Levadex. Our Chief Commercial Officer, Leonard S. Paolillo, has nearly 20 years of experience with various companies in the healthcare and pharmaceutical industries, including Warner Chilcott and Kyowa Kirin. Our Senior Vice President of Regulatory Affairs, Lynn Gold, has over 30 years of experience of leading regulatory activities for pharmaceutical companies, including at Warner Chilcott, Pharmacia and Camargo Pharmaceutical Services, and has been involved in over 40 NDA submissions, with expertise in drug devices and delivery. We are supported by our board of directors, scientific advisory boards and a group of leading biotechnology-focused investors, including KKR Iris Investors LLC, or KKR Iris, which is owned by investment funds and other entities affiliated with Kohlberg Kravis Roberts & Co. L.P., Norwest Venture Partners, 5AM Venture Management, LLC, venBio and Vivo Capital.

Our Strategy

Our goal is to deliver transformative therapies, harnessing the benefits of delivery to the upper nasal cavity, to patients suffering from CNS diseases and other diseases with high unmet medical needs. The key tenets of our strategy to accomplish this goal include:

| ∎ | Successfully commercialize TRUDHESA for the acute treatment of migraine after potential regulatory approval. |

| ∎ | Rapidly advance INP105 through clinical development for the acute treatment of agitation and aggression associated with ASD. |

| ∎ | Maximize the therapeutic and commercial potential of our proprietary POD technology platform. |

| ∎ | Expand applications of our existing product candidates. |

| ∎ | Independently develop and commercialize product candidates in indications and geographies where we believe we can maximize value. |

Risks Affecting Us

Our business is subject to risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this prospectus summary. These risks include, among others, the following:

| ∎ | We are a late-stage pharmaceutical company with a limited operating history and have incurred net losses since our inception. We anticipate that we will continue to incur substantial operating losses for the foreseeable future and we may never achieve or sustain profitability. |

| ∎ | We will require substantial additional financing to achieve our goals, and a failure to obtain this necessary capital when needed could force us to delay, limit, reduce or terminate our product development or commercialization efforts. |

6

Table of Contents

| ∎ | Raising additional capital may cause dilution to our stockholders, restrict our operations or require us to relinquish rights to our technologies or product candidates on unfavorable terms to us. |

| ∎ | The development and commercialization of pharmaceutical products is subject to extensive regulation, and we may not obtain regulatory approvals for TRUDHESA, INP105, INP107 or any other product candidates. |

| ∎ | Our future commercial success depends upon attaining significant market acceptance of our product candidates, if approved, among physicians, patients, health care payors and others in the medical community necessary for commercial success. |

| ∎ | Clinical failure may occur at any stage of clinical development, and we may never succeed in developing marketable product candidates or generating product revenue. |

| ∎ | Delays in the commencement, enrollment or completion of clinical trials of our product candidates, or in the acceptance of foreign clinical trial data, could result in increased costs to us as well as a delay or failure in obtaining regulatory approval, or prevent us from commercializing our product candidates on a timely basis, or at all. |

| ∎ | The outbreak of COVID-19, or similar public health crises, could have a material adverse impact on our business, financial condition and results of operations, including through disruption to our planned clinical trials, supply chains, business operations and commercialization efforts, or through delay in the FDA’s approval of our NDA for TRUDHESA. |

| ∎ | We rely entirely on third parties for the manufacturing of product candidates that we develop for nonclinical studies and clinical trials and expect to continue to do so for commercialization. If we encounter difficulties in negotiating manufacturing and supply agreements with third-party manufacturers and suppliers of our POD device and the active ingredients in TRUDHESA, INP105, and INP107, our ability to commercialize our product candidates, if approved, would be impaired. |

| ∎ | If we are not able to obtain and enforce patent protection for our technologies or product candidates, development and commercialization of our technology and product candidates may be adversely affected. |

| ∎ | We may encounter difficulties in managing our growth and expanding our operations successfully. |

| ∎ | If we fail to attract and keep senior management and key scientific personnel, we may be unable to successfully develop and commercialize our product candidates. |

Corporate Information

We were incorporated under the laws of the State of Delaware in July 2008. Our principal executive offices are located at 201 Elliott Avenue West, Suite 260, Seattle, Washington 98119, and our telephone number is (206) 568-1466. Our website address is www.impelnp.com. The information contained on, or that can be accessed through, our website is not part of, and is not incorporated by reference into, this prospectus. Investors should not rely on any such information in deciding whether to purchase our common stock.

The marks “IMPEL,” “POD,” “TRUDHESA,” “IMPELPOD” and the Impel NeuroPharma logo and our other registered or common law trade names, trademarks or service marks appearing in this prospectus are the property of Impel. All other service marks, trademarks and trade names appearing in this prospectus are the property of their respective owners. Solely for convenience, the trademarks and tradenames referred to in this prospectus appear without the ® and ™ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights, or the right of the applicable licensor, to these trademarks and tradenames.

7

Table of Contents

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

| ∎ | being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus; |

| ∎ | not being required to comply with the auditor attestation requirements on the effectiveness of our internal controls over financial reporting; |

| ∎ | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (auditor discussion and analysis); |

| ∎ | reduced disclosure obligations regarding executive compensation arrangements; and |

| ∎ | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We may use these provisions until the last day of our fiscal year following the fifth anniversary of the completion of this offering or such earlier time when we no longer qualify as an emerging growth company. We will cease to be an emerging growth company upon the earliest of (i) the end of the fiscal year following the fifth anniversary of this offering; (ii) the last day of the fiscal year during which our annual gross revenues are $1.07 billion or more; (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt securities; and (iv) the end of any fiscal year in which the market value of our common stock held by non-affiliates exceeded $700.0 million as of the end of the second quarter of that fiscal year.

We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards, until those standards apply to private companies. We have elected to take advantage of the benefits of this extended transition period and, therefore, we will not be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards. Until the date that we are no longer an emerging growth company or affirmatively and irrevocably opt out of the exemption provided by Section 7(a)(2)(B) of the Securities Act of 1933, as amended, upon issuance of a new or revised accounting standard that applies to our financial statements and that has a different effective date for public and private companies, we will disclose the date on which adoption is required for non-emerging growth companies and the date on which we will adopt the recently issued accounting standard.

8

Table of Contents

Smaller Reporting Company

Additionally, we are a “smaller reporting company” as defined in Item 10(f)(1) of Regulation S-K. Smaller reporting companies may take advantage of certain reduced disclosure obligations, including, among other things, providing only two years of audited financial statements. We will remain a smaller reporting company as long as either (i) the market value of our common stock held by non-affiliates is less than $250 million as of the prior June 30, or (ii) our annual revenues is less than $100 million during such completed fiscal year and the market value of our common stock held by non-affiliates is less than $700 million as of the prior June 30.

9

Table of Contents

THE OFFERING

| Common stock offered |

shares |

| Option to purchase additional shares |

We have granted the underwriters an option, exercisable for 30 days after the date of this prospectus, to purchase up to an additional shares from us. See the section of this prospectus titled “Underwriting.” |

| Common stock to be outstanding immediately after this offering |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

| Use of proceeds |

We estimate that the net proceeds from this offering will be approximately $ million (or approximately $ million if the underwriters exercise their option to purchase additional shares in full), based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses. |

| We intend to use the net proceeds that we receive in this offering as follows: approximately $ million to fund the regulatory approval process and initial commercial launch of TRUDHESA; approximately $ million to initiate a clinical proof-of-concept trial for INP105 in patients with ASD; and any remaining amounts to fund working capital and general corporate purposes. See the section titled “Use of Proceeds.” |

| Risk factors |

You should read the section titled “Risk Factors” in this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Listing |

We intend to apply to list our shares of common stock on The Nasdaq Global Market under the symbol “IMPL.” |

The number of shares of our common stock to be outstanding after this offering is based on shares of our common stock outstanding as of December 31, 2020, which gives effect to (i) the automatic conversion of all outstanding shares of our redeemable convertible preferred stock as of December 31, 2020 into an aggregate of 206,399,763 shares of common stock immediately prior to the completion of this offering, (ii) the automatic exchange of a warrant held by Avenue Venture Opportunities Fund, L.P., or Avenue, into 1,762,810 shares upon completion of this offering, (iii) the

10

Table of Contents

issuance of shares of common stock pursuant to the net exercise of warrants to purchase 1,987,348 shares of redeemable convertible preferred stock outstanding as of December 31, 2020, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, (iv) the automatic conversion of convertible notes we issued in March 2021 into shares of common stock immediately prior to the completion of this offering and (v) the issuance of shares of common stock that we expect to issue, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, and excludes:

| ∎ | 39,983,012 shares of common stock issuable upon the exercise of options outstanding as of December 31, 2020, with a weighted-average exercise price of $0.32 per share; |

| ∎ | shares of our common stock issuable upon the exercise of stock options granted after December 31, 2020, with a weighted-average exercise price of $ per share; and |

| ∎ | shares of common stock reserved for future issuance under our stock-based compensation plans, consisting of (i) 5,639,902 shares of common stock reserved for future issuance under our 2018 Equity Incentive Plan as of December 31, 2020, (ii) shares of common stock reserved for future issuance under our 2021 Equity Incentive Plan, which will become effective on the date immediately prior to the date of this prospectus and (iii) shares of common stock reserved for future issuance under our 2021 Employee Stock Purchase Plan, which will become effective on the date of this prospectus. Upon completion of this offering, any remaining shares available for issuance under our 2018 Equity Incentive Plan will be added to the shares reserved under our 2021 Equity Incentive Plan and we will cease granting awards under our 2018 Equity Incentive Plan. Our 2021 Equity Incentive Plan and 2021 Employee Stock Purchase Plan also provide for automatic annual increases in the number of shares reserved under the plans each year, as more fully described in “Executive Compensation—Equity Compensation Plans and Other Benefit Plans.” |

Except as otherwise indicated, all information in this prospectus assumes or gives effect to:

| ∎ | the automatic conversion of all outstanding shares of our redeemable convertible preferred stock into an aggregate of 206,399,763 shares of common stock immediately prior to the completion of this offering; |

| ∎ | the automatic exchange of a warrant held by Avenue into 1,762,810 shares upon completion of this offering; |

| ∎ | the net exercise immediately prior to the completion of this offering of outstanding warrants to purchase 1,987,348 shares of redeemable convertible preferred stock that would otherwise terminate upon completion of this offering, which will result in the issuance of shares of common stock, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus; |

| ∎ | the automatic conversion of $7.5 million aggregate principal amount of convertible notes issued in March 2021 into shares of common stock immediately prior to the completion of this offering; |

| ∎ | a -for- reverse stock split, which will become effective on ; |

| ∎ | the effectiveness of our restated certificate of incorporation and restated bylaws in connection with the completion of this offering; |

| ∎ | no exercise of outstanding options or warrants after December 31, 2020, other than as described in the second and third bullets above; and |

| ∎ | no exercise of the underwriters’ option to purchase up to additional shares of our common stock. |

11

Table of Contents

Summary Consolidated Financial Data

The following tables set forth our summary consolidated statements of operations and consolidated balance sheet data. The summary consolidated statements of operations data presented below for the years ended December 31, 2019 and 2020 and the summary consolidated balance sheet data as of December 31, 2020 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The following summary consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in any future period. The summary consolidated financial data in this section are not intended to replace the consolidated financial statements and are qualified in their entirety by the consolidated financial statements and related notes included elsewhere in this prospectus.

| Year ended December 31, | ||||||||

| 2019 | 2020 | |||||||

| (in thousands, except share and per share data) |

||||||||

| Statement of Operations Data: |

||||||||

| Operating expenses: |

||||||||

| Research and development |

$ | 28,812 | $ | 27,285 | ||||

| General and administrative |

12,754 | 18,049 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

41,566 | 45,334 | ||||||

|

|

|

|

|

|||||

| Loss from operations |

(41,566 | ) | (45,334 | ) | ||||

| Interest income (expense), net |

417 | (55 | ) | |||||

| Other expense, net |

(680 | ) | (408 | ) | ||||

|

|

|

|

|

|||||

| Loss before income taxes |

(41,829 | ) | (45,797 | ) | ||||

| Provision for income taxes |

(30 | ) | (1 | ) | ||||

|

|

|

|

|

|||||

| Net loss and comprehensive loss |

$ | (41,859 | ) | $ | (45,798 | ) | ||

| Accretion on redeemable convertible preferred stock |

(505 | ) | (518 | ) | ||||

|

|

|

|

|

|||||

| Net loss attributable to common stockholders |

$ | (42,364 | ) | $ | (46,316 | ) | ||

|

|

|

|

|

|||||

| Per share information: |

||||||||

| Net loss per share attributable to common stockholders, basic and diluted(1) |

$ | (7.46 | ) | $ | (5.56 | ) | ||

|

|

|

|

|

|||||

| Weighted-average shares used in computing net loss per share attributable to common stockholders, basic and diluted(1) |

5,682,463 | 8,328,911 | ||||||

|

|

|

|

|

|||||

| Pro forma net loss per share attributable to common stockholders, basic and diluted (unaudited)(2) |

$ | |||||||

|

|

|

|||||||

| Weighted-average shares used in computing pro forma net loss per share attributable to common stockholders, basic and diluted (unaudited)(2) |

||||||||

|

|

|

|||||||

| (1) | See Note 13 to our audited financial statements included elsewhere in this prospectus for an explanation of the method used to calculate basic and diluted net loss per share and basic and diluted weighted-average number of shares of common stock used in the computation of the per share amounts. |

| (2) | See the subsection titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations–Unaudited Pro Forma Information” for an explanation of the calculations of our basic and diluted pro forma net loss per share attributable to common stockholders, and the weighted-average number of shares outstanding used in the computation of the per share amounts. |

12

Table of Contents

| As of December 31, 2020 | ||||||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2) |

||||||||||

| (in thousands) | ||||||||||||

| Balance Sheet Data: |

||||||||||||

| Cash |

$ | 7,095 | $ | $ | ||||||||

| Working capital (deficit)(3) |

(2,354 | ) | ||||||||||

| Total assets |

12,059 | |||||||||||

| Redeemable convertible preferred stock warrant liabilities |

2,622 | |||||||||||

| Long-term debt, current and noncurrent |

8,411 | |||||||||||

| Total redeemable convertible preferred stock |

127,039 | |||||||||||

| Total stockholders’ (deficit) equity |

(133,500 | ) | ||||||||||

| (1) | Pro forma amounts give effect to (i) the automatic conversion of all outstanding shares of our redeemable convertible preferred stock as of December 31, 2020 into an aggregate of 206,399,763 shares of our common stock immediately prior to the completion of this offering, (ii) the automatic exchange of a warrant held by Avenue into 1,762,810 shares upon completion of this offering, (iii) the issuance of shares of common stock pursuant to the net exercise of warrants to purchase 1,987,348 shares of redeemable convertible preferred stock outstanding as of December 31, 2020 that would otherwise expire upon completion of this offering, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, (iv) $7.5 million in proceeds from the convertible notes we issued in March 2021 and their conversion into shares of common stock immediately prior to the completion of this offering at 90% of the offering price and (v) the effectiveness of our restated certificate of incorporation in connection with the completion of this offering. |

| (2) | Pro forma as adjusted amounts reflect pro forma adjustments described in footnote (1) as well as the sale of shares of our common stock in this offering, based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. The pro forma as adjusted information is illustrative only, and will change based on the actual initial public offering price and other terms of this offering determined at pricing. A $1.00 increase (decrease) in the assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover of this prospectus, would increase (decrease) the pro forma as adjusted amount of each of cash, working capital, total assets and total stockholders’ equity by $ million, assuming that the number of shares offered by us, as set forth on the cover of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. Similarly, each increase (decrease) of 1.0 million in the number of shares offered by us in this offering would increase (decrease) the pro forma as adjusted amount of each of cash, working capital, total assets and total stockholders’ equity by $ million, assuming the assumed initial offering price remains the same and after deducting estimated underwriting discounts and commissions. |

| (3) | We define working capital (deficit) as current assets less current liabilities. |

13

Table of Contents

Investing in our common stock involves a high degree of risk. Before making your decision to invest in shares of our common stock, you should carefully consider the risks described below, together with the other information contained in this prospectus, including our consolidated financial statements and the related notes appearing at the end of this prospectus. We cannot assure you that any of the events discussed below will not occur. Any of these events could have a material and adverse impact on our business, financial condition, results of operations and prospects. If that were to happen, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Related to Our Financial Position and Need for Additional Capital

We are a late-stage pharmaceutical company and have incurred net losses since our inception. We anticipate that we will continue to incur substantial operating losses for the foreseeable future and we may never achieve or sustain profitability.

We are a late-stage pharmaceutical company formed in 2008. Since inception, we have devoted substantially all of our financial resources to research and development, including our clinical and nonclinical development activities. To date, we have financed our operations primarily through the sale and issuance of redeemable convertible preferred stock, convertible notes and warrants.

We have incurred significant net losses since our inception. Our net losses were $41.9 million and $45.8 million for the years ended December 31, 2019 and 2020, respectively. As of December 31, 2020, we had an accumulated deficit of $138.3 million. We cannot predict when or whether we will become profitable. To date, we have not generated any product revenues, and we may never be able to develop or commercialize a marketable product. Our losses have resulted principally from costs incurred in our product candidate discovery and development activities. We expect to incur net losses for the foreseeable future.

Our financial position will depend, in part, on the rate of our future expenditures and our ability to obtain funding through equity or debt financings, strategic collaborations, or additional grants. If we are required by the U.S. Food and Drug Administration, or FDA, or any equivalent foreign regulatory authority to perform clinical trials or studies in addition to those we currently expect to conduct, including if foreign clinical trial data are not accepted by the FDA, or if there are any delays in completing the clinical trials of our product candidates, our expenses could increase substantially. Although we have submitted an NDA for TRUDHESA, we may not receive approval for commercialization and even if approved, the resulting revenue may not enable us to achieve profitability. Even if we obtain regulatory approval to market a product candidate, our future revenues will depend upon the size of any markets in which our product candidates have received approval, and our ability to achieve sufficient market acceptance, reimbursement from third-party payors and adequate market share for our product candidates in those markets.

We expect our expenses and net losses to increase significantly as we prepare to potentially commercialize TRUDHESA, continue our development of, and seek regulatory approvals for, our other product candidates, and begin to commercialize other approved products, if any, as well as hire additional personnel, protect our intellectual property and incur additional costs associated with operating as a public company. Our net losses may fluctuate significantly from quarter to quarter and year to year, depending on the timing of our clinical studies and trials, associated manufacturing needs, commercialization activities if our product candidates are approved and our expenditures on other research and development activities.

14

Table of Contents

To become and remain profitable, we must successfully develop product candidates, obtain regulatory approval for them, and manufacture, market and sell those product candidates for which we may obtain regulatory approval. We may not succeed in these activities and we may never generate revenue from product sales that are significant enough to achieve profitability. Even if we achieve profitability in the future, we may not be able to sustain profitability in subsequent periods. We may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors that may adversely affect our business for any reason, including as a result of the COVID-19 pandemic. The size of our future net losses will depend, in part, on the rate of future growth of our expenses and our ability to generate revenue. Our prior losses and expected future losses have had and will continue to have an adverse effect on our stockholders’ equity and working capital. Our failure to become or remain profitable would depress our market value and could impair our ability to raise capital, expand our business, discover or develop other product candidates or continue our operations. A decline in the value of our business could cause you to lose all or part of your investment.

We will require substantial additional financing to achieve our goals and a failure to obtain this necessary capital when needed could force us to delay, limit, reduce or terminate our product development or commercialization efforts.

As of December 31, 2020, we had $7.1 million of cash. We believe that we will continue to expend substantial resources for the foreseeable future as we continue clinical trials, pursue product commercialization, in particular as we prepare for potential commercialization of TRUDHESA and develop additional product candidates. In addition, other unanticipated costs may arise. Because the outcome of our planned and anticipated clinical trials are highly uncertain, we cannot reasonably estimate the actual amounts necessary to successfully complete the development and commercialization of our product candidates. Our costs will increase if we suffer any delays in our planned clinical trials for our current product candidates. Following this offering, we expect to incur additional costs associated with operating as a public company, hiring additional personnel and potentially expanding our facilities.

We believe that the net proceeds from this offering, together with our existing cash, will fund our projected operating requirements through at least the next 12 months. Our forecast of the period of time through which our financial reserves will adequately support our operations is a forward-looking statement and involves risks and uncertainties, and actual results could vary as a result of a number of factors, including the factors discussed elsewhere in this “Risk Factors” section. We have based this estimate on assumptions that may prove to be wrong, and we could utilize our available capital resources sooner than we currently expect.

Our future capital requirements will depend on many factors, including:

| ∎ | the timing of, and the costs involved in, obtaining regulatory approvals for TRUDHESA and our other product candidates if clinical trials are successful; |

| ∎ | the cost of commercialization activities for TRUDHESA, if approved, or any other approved product, including marketing, sales and distribution costs; |

| ∎ | the scope, progress, results and costs of developing and advancing our product candidates through clinical trials and researching and discovering new product candidates; |

| ∎ | our ability to establish and maintain strategic partnerships, licensing or other arrangements and the financial terms of such agreements; |

| ∎ | the cost of manufacturing our product candidates for clinical trials in preparation for regulatory approval and in preparation for commercialization; |

| ∎ | our ability to generate revenue from approved product candidates, if any; and |

| ∎ | the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including litigation costs and the outcome of such litigation. |

15

Table of Contents

We will need to raise additional funds to address our goals. Additional funds may not be available when we need them on terms that are acceptable to us, or at all. Until we can generate sufficient revenue to finance our cash requirements, which we may never do, we expect to finance our future cash needs through a combination of public or private equity offerings, debt financings, collaborations, strategic alliances, licensing arrangements, and other marketing or distribution arrangements. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, reduce or terminate nonclinical studies, clinical trials or other development activities for one or more of our product candidates or delay, limit, reduce or terminate our establishment of sales and marketing capabilities or other activities that may be necessary to commercialize our product candidates if approved.

We have disclosed that there is substantial doubt about our ability to continue as a going concern.

As a result of our net losses from operations, accumulated deficit and need for substantial additional capital, our independent registered public accounting firm included an explanatory paragraph in its report on our financial statements as of, and for the year ended, December 31, 2020 that raises substantial doubt about our ability to continue as a going concern. The conditions giving rise to this uncertainty and our plan with respect to this uncertainty are disclosed in Note 1 to our consolidated financial statements appearing at the end of this prospectus. If we are unable to obtain sufficient funding, we could be forced to delay, reduce or eliminate all of our research and development programs, future research and development efforts and ongoing preclinical studies and clinical trials, and our financial condition and results of operations will be materially and adversely affected and we may be unable to continue as a going concern. After the completion of this offering, future financial statements may continue to disclose substantial doubt about our ability to continue as a going concern. If we seek additional financing to fund our business activities in the future and there remains substantial doubt about our ability to continue as a going concern, investors or other financing sources may be unwilling to provide additional funding to us on commercially reasonable terms or at all.

Raising additional capital may cause dilution to our stockholders, restrict our operations or require us to relinquish rights to our technologies or product candidates on unfavorable terms to our business.

We may seek additional capital through a variety of means, including through private and public equity offerings and debt financings. To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms of such equity or convertible debt securities may include liquidation or other preferences that are senior to or otherwise adversely affect your rights as a stockholder. Debt financing, if available, may involve agreements that include covenants limiting or restricting our ability to take certain actions, such as incurring additional debt, making capital expenditures, declaring dividends or encumbering our assets to secure future indebtedness. For example, our debt and equity financing agreement with Avenue is secured by a lien on substantially all of our assets, including our intellectual property and following this offering will be secured by a lien on substantially all of our assets, excluding our intellectual property. If we raise additional funds through strategic partnerships with third parties, we may have to relinquish valuable rights to our technologies or product candidates, or grant licenses on terms that are not favorable to us. If we are unable to raise additional funds through equity or debt financing when needed, we may be required to delay, limit, reduce or terminate our product development or commercialization efforts for our product candidates, or grant rights to third parties to develop and market product candidates that we would otherwise prefer to develop and market ourselves.

16

Table of Contents

Our quarterly operating results may fluctuate significantly or may fall below the expectations of investors or securities analysts, each of which may cause our stock price to fluctuate or decline.

We expect our operating results to be subject to quarterly fluctuations. Our net loss and other operating results will be affected by numerous factors, including:

| ∎ | variations in the level of expense related to the ongoing development of our product candidates or future development programs; |

| ∎ | results of nonclinical and clinical trials, or the addition or termination of clinical trials or funding support by us, or existing or future collaborators or licensing partners; |

| ∎ | our execution of any additional collaboration, licensing or similar arrangements, and the timing of payments we may make or receive under existing or future arrangements or the termination or modification of any such existing or future arrangements; |

| ∎ | any intellectual property infringement lawsuit or opposition, interference or cancellation proceeding in which we may become involved; |

| ∎ | additions and departures of key personnel; |

| ∎ | strategic decisions by us or our competitors, such as acquisitions, divestitures, spin-offs, joint ventures, strategic investments or changes in business strategy; |

| ∎ | if any of our product candidates receive regulatory approval, the terms of such approval and market acceptance and demand for such product candidates; |

| ∎ | if any of our product candidates receive regulatory approval, variation in the level of expense related to the commercialization of such product candidates and quarterly fluctuations in any future product sales; |

| ∎ | regulatory developments affecting our product candidates or those of our competitors; and |

| ∎ | changes in general market and economic conditions. |

If our quarterly operating results fall below the expectations of investors or securities analysts, the price of our common stock could decline substantially. Furthermore, any quarterly fluctuations in our operating results may, in turn, cause the price of our common stock to fluctuate substantially. We believe that quarterly comparisons of our financial results should not be relied upon as an indication of our future performance.

Risks Related to Regulatory Review and Approval of Our Product Candidates

The development and commercialization of pharmaceutical products is subject to extensive regulation, and we may not obtain regulatory approvals for TRUDHESA, INP105, INP107 or any other product candidates.

The clinical development, manufacturing, labeling, packaging, storage, recordkeeping, advertising, promotion, export, import, marketing, distribution, adverse event reporting, including the submission of safety and other post-marketing information and reports, and other possible activities relating to TRUDHESA and INP105, which are our furthest advanced product candidates under clinical development, as well as INP107 and any other product candidate that we may develop in the future, are subject to extensive regulation. Marketing approval of drugs in the United States requires the submission of an NDA to the FDA, and we are not permitted to market any product candidate in the United States until we obtain approval from the FDA of the NDA for that product. An NDA must be supported by extensive clinical and preclinical data, as well as extensive information regarding pharmacology, CMC, and current good manufacturing practices, or cGMP, at the manufacturing facilities. Further, our product candidates must be approved by comparable regulatory authorities in other jurisdictions where we intend to market our product candidates prior to commercialization.

17

Table of Contents

FDA approval of an NDA is not guaranteed, and review and approval is an expensive and uncertain process that may take several years. Of the large number of drugs in development in the United States, only a small percentage will successfully complete the FDA regulatory approval process and will be commercialized. Accordingly, there can be no assurance that any of our product candidates will receive regulatory approval in the United States, or other jurisdictions. The FDA also has substantial discretion in the approval process. The number and types of preclinical studies and clinical trials that will be required for NDA approval varies depending on the product candidate, the disease or the condition that the product candidate is designed to treat and the regulations applicable to any particular product candidate. We have submitted an NDA for TRUDHESA through the Section 505(b)(2) regulatory pathway and intend to seek FDA approval for our other product candidates through the Section 505(b)(2) regulatory pathway. If the FDA does not agree that the 505(b)(2) regulatory pathway is appropriate or scientifically justified for one or more of our product candidates, we may need to conduct additional clinical trials, provide additional data and information and meet additional standards for regulatory approval. Additionally, if CMC information in the NDA is found to be deficient, if the FDA disagrees with our interpretation or analysis of clinical data, or identifies any deficiency in our clinical data, we may fail to obtain approval of TRUDHESA or approval may be delayed. CMC issues that could be found to be deficient to the FDA include our investigation of increased levels of impurities in some vials of certain drug lots used in the STOP301 trial, or the use of certain drug lots for our primary stability data because the FDA concludes that the manufacturing process has not been in a state of control at the time of their manufacture.

Clinical trial failure may result from a multitude of factors including flaws in trial design, dose selection, placebo effect, patient enrollment criteria and failure to demonstrate favorable safety or efficacy traits, and failure in clinical trials can occur at any stage. Companies in the pharmaceutical industry frequently suffer setbacks in the advancement of clinical trials due to lack of efficacy or adverse safety profiles, notwithstanding promising results in earlier trials. Based upon negative or inconclusive results, we may decide, or regulators may require us, to conduct additional clinical trials or preclinical studies. In addition, data obtained from clinical trials are susceptible to varying interpretations, and regulators may not interpret our data as favorably as we do, which may further delay, limit or prevent marketing approval.

The FDA could delay, limit or deny approval of a product candidate for many reasons, including because the FDA:

| ∎ | may not deem our product candidate to be safe and effective; |

| ∎ | determines that the product candidate does not have an acceptable benefit-risk profile; |

| ∎ | determines in the case of an NDA seeking accelerated approval that the NDA does not provide evidence that the product candidate represents a meaningful advantage over available therapies; |

| ∎ | determines that the objective response rate, or ORR, and duration of response are not clinically meaningful; |

| ∎ | may not agree that the data collected from preclinical studies and clinical trials are acceptable or sufficient to support the submission of an NDA or other submission or to obtain regulatory approval, and may impose requirements for additional preclinical studies or clinical trials; |

| ∎ | may determine that adverse events experienced by participants in our clinical trials represent an unacceptable level of risk; |

| ∎ | may determine that population studied in the clinical trial may not be sufficiently broad or representative to assure safety in the full population for which we seek approval; |

| ∎ | may disagree regarding the formulation, labeling and/or the specifications; |

| ∎ | may not approve the manufacturing processes associated with our product candidate or may determine that a manufacturing facility does not have an acceptable compliance status; |

18

Table of Contents

| ∎ | may conclude there are CMC issues that preclude approval of the NDA; |

| ∎ | may conclude that the drug substance or drug product manufacturing process is not in a state of control or does not meet cGMPs or all the regulatory requirements; |

| ∎ | may not be able to timely conduct the necessary pre-approval inspection or devote sufficient resources to NDA review on a timely basis due to the COVID-19 pandemic; |

| ∎ | may change approval policies or adopt new regulations; or |

| ∎ | may not file a submission due to, among other reasons, the content or formatting of the submission. |

We have not obtained FDA approval for any of our product candidates. This lack of experience may impede our ability to obtain FDA approval in a timely manner, if at all, for our clinical product candidates.

If we experience delays in obtaining approval or if we fail to obtain approval of TRUDHESA, INP105 or INP107, our commercial prospects will be harmed and our ability to generate revenues will be materially impaired which would adversely affect our business, prospects, financial condition and results of operations.

Clinical failure may occur at any stage of clinical development, and we may never succeed in developing marketable product candidates or generating product revenue.

Before obtaining marketing approval from regulatory authorities for the sale of any product candidate, we must complete preclinical development and then conduct clinical trials to demonstrate the safety and efficacy of our product candidates in humans. Clinical testing is expensive, difficult to design and implement, can take many years to complete and is uncertain as to outcome. A failure of one or more clinical trials can occur at any stage of testing. Although our NDA for TRUDHESA for the acute treatment of migraine headaches with or without aura in adult patients has been accepted for filing, the FDA may reject this NDA or require additional clinical testing prior to approval.

Although the active ingredients in our product candidates, TRUDHESA, INP105, and INP107, are approved or commonly used as treatments for migraine, agitation associated with ASD, and Parkinson’s, respectively, they have not previously been approved or demonstrated to be safe for chronic use over an extended period of time using an upper nasal cavity drug delivery. Our NDA submission for TRUDHESA proposes to bridge TRUDHESA to two Listed Drugs, or LDs, for which we have conducted a comparative bioavailability study, and conducted a long-term safety study to evaluate local toxicity on the nasal and olfactory epithelia. Our prior clinical results for our product candidates are not necessarily indicative of our ability to bridge to LD, as there can be significant variability in results between different clinical trials due to numerous factors, including changes in trial procedures, differences in the size and type of patient populations, including across geographies, changes in and adherence to the clinical trial protocols, and the rate of dropout among clinical trial participants. If we are not able to establish a bridge between a product candidate and each LD upon which they rely to demonstrate that such reliance is justified, we may be required to show safety and efficacy through one or more clinical trials. In addition, the long-term safety studies we are conducting or plan to conduct may reveal safety concerns, including with regard to nasal mucosa or olfactory function. If either or both of these outcomes occur, we may be prevented or delayed in obtaining marketing approval.

We may be required to perform additional or unanticipated clinical trials to obtain approval or be subject to additional post-marketing testing requirements to maintain regulatory approval. In addition, regulatory authorities may withdraw their approval of a product or impose restrictions on our distribution, such as in the form of a Risk Evaluation and Mitigation Strategy, or REMS. The failure to obtain timely regulatory approval of product candidates, any product marketing limitations or a product

19

Table of Contents

withdrawal would materially and adversely affect our business, results of operations and financial condition.

Delays in the commencement, enrollment or completion of clinical trials of our product candidates could result in increased costs to us as well as a delay or failure in obtaining regulatory approval, or prevent us from commercializing our product candidates on a timely basis, or at all.

We plan to initiate a Phase 2 trial of a double-blind placebo-controlled single dose of INP105 study in adolescents with ASD by the end of 2021. Any of our future clinical trials may not be conducted as planned or completed on schedule, if at all. A failure of one or more clinical trials can occur at any stage. Events that may prevent successful or timely commencement, enrollment or completion of clinical development include: