Attached files

| file | filename |

|---|---|

| EX-99.6 - EX-99.6 - Magyar Bancorp, Inc. | d132199dex996.htm |

| EX-99.2 - EX-99.2 - Magyar Bancorp, Inc. | d132199dex992.htm |

| EX-99.1 - EX-99.1 - Magyar Bancorp, Inc. | d132199dex991.htm |

| EX-23.6 - EX-23.6 - Magyar Bancorp, Inc. | d132199dex236.htm |

| EX-23.2 - EX-23.2 - Magyar Bancorp, Inc. | d132199dex232.htm |

| EX-10.14 - EX-10.14 - Magyar Bancorp, Inc. | d132199dex1014.htm |

| EX-10.11 - EX-10.11 - Magyar Bancorp, Inc. | d132199dex1011.htm |

| EX-10.10 - EX-10.10 - Magyar Bancorp, Inc. | d132199dex1010.htm |

| EX-8.2 - EX-8.2 - Magyar Bancorp, Inc. | d132199dex82.htm |

| EX-8.1 - EX-8.1 - Magyar Bancorp, Inc. | d132199dex81.htm |

| EX-5 - EX-5 - Magyar Bancorp, Inc. | d132199dex5.htm |

| EX-3.3 - EX-3.3 - Magyar Bancorp, Inc. | d132199dex33.htm |

| EX-2 - EX-2 - Magyar Bancorp, Inc. | d132199dex2.htm |

| EX-1.2 - EX-1.2 - Magyar Bancorp, Inc. | d132199dex12.htm |

| EX-1.1 - EX-1.1 - Magyar Bancorp, Inc. | d132199dex11.htm |

| S-1 - S-1 - Magyar Bancorp, Inc. | d132199ds1.htm |

Exhibit 99.3

| PRO FORMA VALUATION REPORT SECOND-STEP CONVERSION |

| Magyar Bancorp, Inc. | New Brunswick, New Jersey

HOLDING COMPANY FOR: Magyar Bank | New Brunswick, New Jersey |

Dated as of February 5, 2021

1311-A Dolley Madison Boulevard

Suite 2A

McLean, Virginia 22101

703.528.1700

rpfinancial.com

February 5, 2021

Boards of Directors

Magyar Bancorp, MHC

Magyar Bancorp, Inc.

Magyar Bank

400 Somerset Street

New Brunswick, New Jersey 08901

Members of the Boards of Directors:

At your request, we have completed and hereby provide an independent appraisal (“Appraisal”) of the estimated pro forma market value of the common stock which is to be issued in connection with the mutual-to-stock conversion transaction described below.

This Appraisal is furnished pursuant to the requirements stipulated in the Code of Federal Regulations and has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings and Loan Associations Converting from Mutual to Stock Form of Organization” of the Office of Thrift Supervision (“OTS”) and accepted by the Federal Reserve Board (“FRB”), the Office of the Comptroller of the Currency (“OCC”), the Federal Deposit Insurance Corporation (“FDIC”) and the New Jersey Department of Banking and Insurance (the “Department”), and applicable regulatory interpretations thereof.

Description of Plan of Conversion

On February 26, 2021, the Board of Directors of Magyar Bancorp MHC (the “MHC”) and the Board of Directors of Magyar Bancorp, Inc. (“MGYR”) and Magyar Bank adopted a plan of conversion. As a result of the conversion, the MHC will be merged into MGYR and as a result the MHC will cease to exist. As part of the conversion, the 55.08% ownership interest of the MHC in MGYR will be offered for sale in the offering. When the conversion is completed, MGYR will continue to own all of the outstanding common stock of Magyar Bank and public stockholders will own all of the outstanding common stock of Magyar Bancorp. For purposes of this document, the existing consolidated entity will hereinafter also be referred to as Magyar Bancorp or the Company, unless otherwise identified as MGYR. As of December 31, 2020, the MHC had a majority ownership interest in, and its principal asset consisted of, 55.08% of the common stock (the “MHC Shares”) of MGYR. The remaining 44.92% of MGYR’s common stock is owned by public stockholders.

It is our understanding that Magyar Bancorp will offer its stock, representing the majority ownership interest held by the MHC, in a subscription offering to Eligible Account Holders, Tax-Qualified Plans including the Bank’s employee stock ownership plan (the “ESOP”) and Supplemental Eligible Account Holders and Other Depositors, as such terms are defined for purposes of applicable federal regulatory requirements governing mutual-to-stock conversions.

| 1311-A Dolley Madison Boulevard, Suite 2A | Telephone: (703) 528-1700 | |

| McLean, VA 22101 | Fax No.: (703) 528-1788 | |

| www.rpfinancial.com | Toll-Free No.: (866) 723-0594 | |

| E-mail: mail@rpfinancial.com |

Boards of Directors

February 5, 2021

Page 2

To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to the public at large in a community offering and a syndicated offering or firm commitment underwritten offering. Upon completing the mutual-to-stock conversion and stock offering (the “second-step conversion”), the Company will be 100% owned by public shareholders, the publicly-held shares of MGYR will be exchanged for shares in the Company at a ratio that retains their ownership interest at the time the conversion is completed and the MHC assets will be consolidated with the Company.

RP® Financial, LC.

RP® Financial, LC. (“RP Financial”) is a financial consulting firm serving the financial services industry nationwide that, among other things, specializes in financial valuations and analyses of business enterprises and securities, including the pro forma valuation for savings institutions converting from mutual-to-stock form. The background and experience of RP Financial is detailed in Exhibit V-1. We believe that, except for the fee we will receive for the Appraisal, we are independent of the Company, the Bank, the MHC and the other parties engaged by the Bank or the Company to assist in the stock conversion process.

Valuation Methodology

In preparing our Appraisal, we have reviewed the regulatory applications of the Company, the Bank and the MHC, including the prospectus as filed with the FRB, the FDIC, the Department and the Securities and Exchange Commission (“SEC”). We have conducted a financial analysis of the Company, the Bank and the MHC that has included a review of audited financial information for the years ended September 30, 2016 through September 30, 2020 and for the three month period ended December 31, 2020, a review of various unaudited information and internal financial reports through December 31, 2020, and due diligence related discussions with the Company’s management; RSM US LLP, the Company’s independent auditor; Luse Gorman, PC, the Company’s conversion counsel and Keefe Bruyette & Woods, Inc., the Company’s marketing advisor in connection with the stock offering. All assumptions and conclusions set forth in the Appraisal were reached independently from such discussions. In addition, where appropriate, we have considered information based on other available published sources that we believe are reliable. While we believe the information and data gathered from all these sources are reliable, we cannot guarantee the accuracy and completeness of such information.

We have investigated the competitive environment within which Magyar Bancorp operates and have assessed Magyar Bancorp’s relative strengths and weaknesses. We have kept abreast of the changing regulatory and legislative environment for financial institutions and analyzed the potential impact on Magyar Bancorp and the industry as a whole. We have analyzed the potential effects of the stock conversion on Magyar Bancorp’s operating characteristics and financial performance as they relate to the pro forma market value of Magyar Bancorp. We have analyzed the assets held by the MHC, which will be consolidated with Magyar Bancorp’s assets and equity pursuant to the completion of the second-step conversion. We have reviewed the economic and demographic characteristics of the Company’s primary market area. We have compared Magyar Bancorp’s financial performance and condition with selected publicly-traded thrifts in accordance with the Valuation Guidelines, as well as all publicly-traded thrifts and thrift holding companies. We have reviewed the current conditions in the securities markets in general and the market for thrift stocks in particular, including the market for existing thrift issues, initial public offerings by thrifts and thrift holding companies, and second-step conversion offerings. We have excluded from such analyses thrifts subject to announced or rumored acquisition, and/or institutions that exhibit other unusual characteristics.

Boards of Directors

February 5, 2021

Page 3

The Appraisal is based on Magyar Bancorp’s representation that the information contained in the regulatory applications and additional information furnished to us by Magyar Bancorp and its independent auditor, legal counsel and other authorized agents are truthful, accurate and complete. We did not independently verify the financial statements and other information provided by Magyar Bancorp, or its independent auditor, legal counsel and other authorized agents nor did we independently value the assets or liabilities of Magyar Bancorp. The valuation considers Magyar Bancorp only as a going concern and should not be considered as an indication of Magyar Bancorp’s liquidation value.

Our appraised value is predicated on a continuation of the current operating environment for Magyar Bancorp and for all thrifts and their holding companies. Changes in the local, state and national economy, the legislative and regulatory environment for financial institutions and mutual holding companies, the stock market, interest rates, and other external forces (such as natural disasters or significant world events) may occur from time to time, often with great unpredictability and may materially impact the value of thrift stocks as a whole or the value of Magyar Bancorp’s stock alone. It is our understanding that there are no current plans for selling control of Magyar Bancorp following completion of the second-step conversion. To the extent that such factors can be foreseen, they have been factored into our analysis.

The estimated pro forma market value is defined as the price at which Magyar Bancorp’s common stock, immediately upon completion of the second-step stock offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

In preparing the pro forma pricing analysis we have taken into account the pro forma impact of the MHC’s net assets (i.e., unconsolidated equity) that will be consolidated with the Company and thus will slightly increase equity. After accounting for the impact of the MHC’s net assets, the public shareholders’ ownership interest was reduced by 0.0073%. Accordingly, for purposes of the Company’s pro forma valuation, the public shareholders’ pro forma ownership interest was reduced from 44.9219% to 44.9146% and the MHC’s ownership interest was increased from 55.0781 to 55.0854%.

Valuation Conclusion

It is our opinion that, as of February 5, 2021, the estimated aggregate pro forma valuation of the shares of the Company to be issued and outstanding at the end of the conversion offering – including (1) newly-issued shares representing the MHC’s current ownership interest in the Company and (2) exchange shares issued to existing public shareholders of MGYR – was $61,722,340 at the midpoint, equal to 6,172,234 shares at $10.00 per share. The resulting range of value and pro forma shares, all based on $10.00 per share, are as follows: $52,463,990 or 5,246,399 shares at the minimum and $70,980,700 or 7,098,070 shares at the maximum.

Based on this valuation and taking into account the ownership interest represented by the shares owned by the MHC, the midpoint of the offering range is $34,000,000 equal to 3,400,000 shares at $10.00 per share. The resulting offering range and offering shares, all based on $10.00 per share, are as follows: $28,900,000 or 2,890,000 shares at the minimum and $39,100,000 or 3,910,000 shares at the maximum.

Boards of Directors

February 5, 2021

Page 4

Establishment of the Exchange Ratio

The conversion regulations provide that in a conversion of a mutual holding company, the minority stockholders are entitled to exchange the public shares for newly issued shares in the fully converted company. The Board of Directors of the MHC and the Board of Directors of MGYR and the Bank have independently determined the exchange ratio, which has been designed to preserve the current aggregate percentage ownership in the Company (adjusted for the dilution resulting from the consolidation of the MHC’s unconsolidated net assets into the Company). The exchange ratio to be received by the existing minority shareholders of the Company will be determined at the end of the offering, based on the total number of shares sold in the offering and the final appraisal. Based on the valuation conclusion herein, the resulting offering value and the $10.00 per share offering price, the indicated exchange ratio at the midpoint is 1.0620 shares of the Company’s stock for every one share held by public shareholders. Furthermore, based on the offering range of value, the indicated exchange ratio is 0.9027 at the minimum and 1.2213 at the maximum. RP Financial expresses no opinion on the proposed exchange of newly issued Company shares for the shares held by the public stockholders or on the proposed exchange ratio.

Limiting Factors and Considerations

The valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the common stock. Moreover, because such valuation is determined in accordance with applicable regulatory guidelines and is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion offering, or prior to that time, will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the estimated pro forma market value thereof. The appraisal reflects only a valuation range as of this date for the pro forma market value of Magyar Bancorp immediately upon issuance of the stock and does not take into account any trading activity with respect to the purchase and sale of common stock in the secondary market on the date of issuance of such securities or at anytime thereafter following the completion of the second-step conversion.

RP Financial’s valuation was based on the financial condition, operations and shares outstanding of Magyar Bancorp as of December 31, 2020, the date of the financial data included in the prospectus. The proposed exchange ratio to be received by the current public stockholders of MGYR and the exchange of the public shares for newly issued shares of Magyar Bancorp’s common stock as a full public company was determined independently by the Board of Directors of the MHC and the Board of Directors of MGYR and the Bank. RP Financial expresses no opinion on the proposed exchange ratio to public stockholders or the exchange of public shares for newly issued shares.

RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its client institutions.

Boards of Directors

February 5, 2021

Page 5

This valuation will be updated as provided for in the conversion regulations and guidelines. These updates will consider, among other things, any developments or changes in the financial performance and condition of Magyar Bancorp, management policies, and current conditions in the equity markets for thrift shares, both existing issues and new issues. These updates may also consider changes in other external factors which impact value including, but not limited to: various changes in the legislative and regulatory environment for financial institutions, the stock market and the market for thrift stocks, and interest rates. Should any such new developments or changes be material, in our opinion, to the valuation of the shares, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in the update at the date of the release of the update. The valuation will also be updated at the completion of Magyar Bancorp’s stock offering.

| Respectfully submitted, |

| RP® FINANCIAL, LC. |

|

| William E. Pommerening |

| CEO and Managing Director |

|

| James J. Oren |

| Director |

| RP® Financial, LC. | TABLE OF CONTENTS | |

| i |

TABLE OF CONTENTS

Magyar Bancorp, Inc.

New Brunswick, New Jersey

| DESCRIPTION |

PAGE NUMBER |

|||||

| CHAPTER ONE |

OVERVIEW AND FINANCIAL ANALYSIS | |||||

| Introduction |

I.1 | |||||

| Plan of Reorganization |

I.1 | |||||

| Strategic Overview |

I.2 | |||||

| Balance Sheet Trends |

I.4 | |||||

| Income and Expense Trends |

I.7 | |||||

| Interest Rate Risk Management |

I.10 | |||||

| Lending Activities and Strategy |

I.11 | |||||

| Loan Originations, Purchases and Sales |

I.15 | |||||

| Asset Quality |

I.15 | |||||

| Funding Composition and Strategy |

I.16 | |||||

| Subsidiary Operations |

I.16 | |||||

| Legal Proceedings |

I.17 | |||||

| CHAPTER TWO |

MARKET AREA | |||||

| Introduction |

II.1 | |||||

| National Economic Factors |

II.1 | |||||

| Interest Rate Environment |

II.5 | |||||

| Primary Market Area |

II.6 | |||||

| Demographic and Economic Trends |

II.7 | |||||

| Economic Sectors |

II.9 | |||||

| Market Area Largest Employers |

II.10 | |||||

| Market Area Unemployment Data |

II.10 | |||||

| Deposit Trends |

II.12 | |||||

| Competition |

II.13 | |||||

| CHAPTER THREE |

PEER GROUP ANALYSIS |

|||||

| Peer Group Selection |

III.1 | |||||

| Financial Condition |

III.5 | |||||

| Income and Expense Components |

III.8 | |||||

| Loan Composition |

III.10 | |||||

| Credit Risk |

III.12 | |||||

| Interest Rate Risk |

III.14 | |||||

| Summary |

III.14 | |||||

| RP® Financial, LC. | TABLE OF CONTENTS | |

| ii |

TABLE OF CONTENTS

Magyar Bancorp, Inc.

New Brunswick, New Jersey

(continued)

| DESCRIPTION |

PAGE NUMBER |

|||||

| CHAPTER FOUR |

VALUATION ANALYSIS | |||||

| Introduction |

IV.1 | |||||

| Appraisal Guidelines |

IV.1 | |||||

| RP Financial Approach to the Valuation |

IV.1 | |||||

| Valuation Analysis |

IV.2 | |||||

| 1. Financial Condition |

IV.2 | |||||

| 2. Profitability, Growth and Viability of Earnings |

IV.4 | |||||

| 3. Asset Growth |

IV.6 | |||||

| 4. Primary Market Area |

IV.6 | |||||

| 5. Dividends |

IV.7 | |||||

| 6. Liquidity of the Shares |

IV.8 | |||||

| 7. Marketing of the Issue |

IV.8 | |||||

| A. The Public Market |

IV.9 | |||||

| B. The New Issue Market |

IV.14 | |||||

| C. The Acquisition Market |

IV.16 | |||||

| D. Trading in MGYR’s Stock |

IV.16 | |||||

| 8. Management |

IV.17 | |||||

| 9. Effect of Government Regulation and Regulatory Reform |

IV.17 | |||||

| Summary of Adjustments |

IV.17 | |||||

| Valuation Approaches: |

IV.18 | |||||

| 1. Price-to-Earnings (“P/E”) |

IV.20 | |||||

| 2. Price-to-Book (“P/B”) |

IV.20 | |||||

| 3. Price-to-Assets (“P/A”) |

IV.22 | |||||

| Comparison to Recent Offerings |

IV.22 | |||||

| Valuation Conclusion |

IV.22 | |||||

| Establishment of the Exchange Ratio |

IV.23 | |||||

| RP® Financial, LC. | TABLE OF CONTENTS | |

| iii |

LIST OF TABLES

Magyar Bancorp, Inc.

New Brunswick, New Jersey

| TABLE |

DESCRIPTION |

PAGE | ||||

| 1.1 | Historical Balance Sheets |

I.5 | ||||

| 1.2 | Historical Income Statements |

I.8 | ||||

| 2.1 | Summary Demographic/Economic Data |

II.8 | ||||

| 2.2 | Primary Market Area Employment Sectors |

II.10 | ||||

| 2.3 | Market Area Largest Employers |

II.11 | ||||

| 2.4 | Unemployment Trends |

II.12 | ||||

| 2.5 | Deposit Summary |

II.13 | ||||

| 2.6 | Market Area Deposit Competitors – As of June 30, 2020 |

II.15 | ||||

| 3.1 | Peer Group of Publicly-Traded Thrifts |

III.3 | ||||

| 3.2 | Balance Sheet Composition and Growth Rates |

III.6 | ||||

| 3.3 | Income as a Pct. of Avg. Assets and Yields, Costs, Spreads |

III.9 | ||||

| 3.4 | Loan Portfolio Composition and Related Information |

III.11 | ||||

| 3.5 | Interest Rate Risk Measures and Net Interest Income Volatility |

III.13 | ||||

| 3.6 | Credit Risk Measures and Related Information |

III.15 | ||||

| 4.1 | Peer Group Market Area Unemployment Rates |

IV.7 | ||||

| 4.2 | Pricing Characteristics and After-Market Trends |

IV.15 | ||||

| 4.3 | Public Market Pricing Versus Peer Group |

IV.21 | ||||

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.1 |

I. OVERVIEW AND FINANCIAL ANALYSIS

Introduction

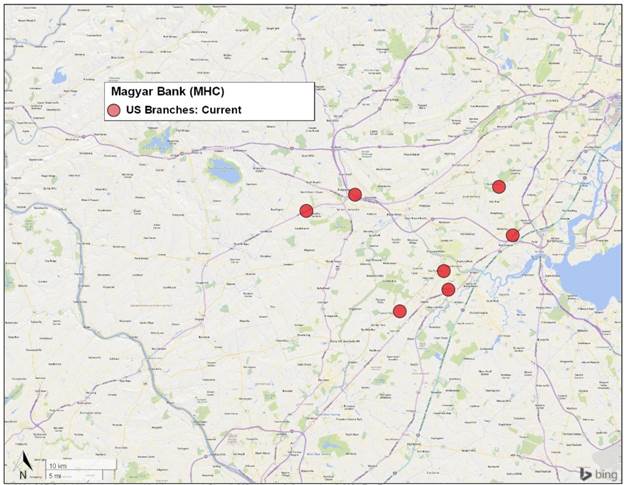

Magyar Bank is a New Jersey-chartered stock savings bank originally organized in 1922. Magyar Bank is headquartered in the city of New Brunswick, Middlesex County, New Jersey, in east central New Jersey. The Bank operates a community banking business through its headquarters office, five branch offices in Middlesex County, and two branch offices in Somerset County, New Jersey, located northwest of Middlesex County. While the market area for deposit gathering is concentrated in the local communities in which a branch office is maintained, the Bank also conducts lending operations over a somewhat wider area, defined as Central and Northern portions of New Jersey. A map of the Bank’s office locations is included as Exhibit I-1. The Bank is a member of the Federal Home Loan Bank (“FHLB”) system, and its deposits are insured up to the regulatory maximums by the Deposit Insurance Fund of the Federal Deposit Insurance Corporation (“FDIC”). Magyar Bank is subject to regulatory oversight and examination by the New Jersey Department of Banking and Insurance (the NJDOBI”) as its chartering agency and by the FDIC for deposit insurance purposes.

Magyar Bancorp, Inc. (“MGYR”) is the federally chartered mid-tier holding company of the Bank. MGYR owns 100% of the outstanding common stock of the Bank. Since its formation in 2006, MGYR has been engaged primarily in the business of holding the common stock of the Bank. MGYR completed its initial public offering on January 24, 2006, pursuant to which it sold 2,618,820 shares or 44.2% of its outstanding common stock to the public and issued 3,200,450 shares or 55.8% of its common stock outstanding to Magyar Bancorp, MHC (the “MHC”), the mutual holding company parent of MGYR. The MHC and MGYR are subject to supervision and regulation by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board” or the “FRB”). At December 31, 2020, MGYR had total consolidated assets of $741.8 million, deposits of $612.1 million and equity of $58.2 million or 7.85% of total assets. MGYR’s tangible equity was equal to reported equity given there are no intangibles. MGYR’s audited financial statements for the most recent period are included by reference as Exhibit I-2.

Plan of Reorganization

The boards of directors of Magyar Bancorp, MHC and Magyar Bancorp have approved the plan of conversion. Pursuant to the plan of conversion, the organization will convert from the mutual holding company form of organization to the fully stock form. Magyar Bancorp, MHC will

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.2 |

be merged into Magyar Bancorp and as a result Magyar Bancorp, MHC will cease to exist. As part of the conversion, the 55.1% ownership interest of Magyar Bancorp, MHC in Magyar Bancorp will be offered for sale in the offering. When the conversion is completed, Magyar Bancorp will continue to own all of the outstanding common stock of Magyar Bank and public stockholders will own all of the outstanding common stock of Magyar Bancorp. For purposes of this document, the existing consolidated entity will also hereinafter be also referred to as Magyar Bancorp or the Company, unless otherwise identified as MGYR.

Magyar Bancorp will offer its common stock in a subscription offering to Eligible Account Holders, Tax-Qualified Plans, Supplemental Eligible Account Holders and Other Depositors as such terms are defined for purposes of applicable regulatory guidelines governing stock offerings by mutual institutions. To the extent that shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to members of the general public in a community offering and a syndicated or firm commitment offering. Upon completing the mutual-to-stock conversion and stock offering (the “second-step conversion”), the Company will be 100% owned by public shareholders, the publicly-held shares of MGYR will be exchanged for shares in the Company at a ratio that retains their ownership interest at the time the conversion is completed and the MHC assets will be consolidated with the Company.

Strategic Overview

Magyar Bank has been serving Middlesex County and the related central New Jersey marketplace as a locally-owned and operated financial institution since its founding in 1922. For many years Magyar Bank operated as a traditional thrift institution, originating for portfolio long-term fixed rate residential loans funded with certificates of deposit. In recent years, the Bank has strived to diversify the loan portfolio into multifamily and commercial real estate mortgage loans, home equity loans and lines of credit, commercial business loans and construction loans. An additional benefit of this strategy has been an increase in lower cost core deposit accounts, related to the commercial lending activities. The Bank’s products and services are focused on the lending and investment needs of the local retail and commercial customer base as well as households in the market area. Based on the operating history and growth of the Bank since its founding, the Bank has established, to certain degree, its name recognition and overall reputation in the central New Jersey area. In addition, the Bank views itself as an integral part of the local communities served, and thus has historically strongly supported the retail customer base through providing residential loan products.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.3 |

The equity from the stock offering will increase the Bank’s liquidity, lending capacity, leverage and growth capacity and the overall financial strength. Magyar Bank’s higher equity position resulting from the infusion of stock proceeds is anticipated to reduce interest rate risk through enhancing the interest-earning assets to interest-bearing liabilities (“IEA/IBL”) ratio. The increased equity is expected to reduce overall funding costs for the asset base. The Bank will be better positioned to pursue growth and revenue diversification. The projected use of proceeds is highlighted below.

| • | The Company. The Company is expected to retain up to 50% of the net offering proceeds. At present, funds at the Company level, net of the loan to the ESOP, are expected to be primarily invested initially into liquid funds, in which some or all may be held as a deposit at the Bank. Over time, the funds may be utilized for various corporate purposes, possibly including acquisitions, infusing additional equity into the Bank, repurchases of common stock and the payment of cash dividends. |

| • | The Bank. A minimum of 50% of the net conversion proceeds will be infused into the Bank as cash and equity. Cash proceeds (i.e., net proceeds less deposits withdrawn to fund stock purchases) infused into the Bank are expected to be deposited as an interest-earning deposit, providing additional funds for reinvestment in earning assets. |

With the Bank’s enhanced equity position, following the completion of the offering, Magyar Bank intends to continue to pursue the following strategies in order to operate as a well-capitalized and profitable community bank focused on meeting the needs of individuals, small businesses, and community organizations in Middlesex County and the related regional market area:

| • | Continue to grow the loan portfolio, with a focus primarily on commercial real estate and to a lesser extent, commercial business lending, with a continued emphasis on 1-4 family residential mortgage loans originated and held in portfolio. |

| • | Operate as a community oriented financial institution, focusing on service and a local customer base; |

| • | Focus on secure technological innovation to increase convenience to customers while at the same time improve efficiencies; |

| • | Increase core deposits, with an emphasis on low cost demand deposits in order to provide a source of funds for lending activities while improving the interest rate spread and net interest margin; |

| • | Manage credit risk to maintain a low level of nonperforming assets through a strict and disciplined credit culture. |

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.4 |

Balance Sheet Trends

Table 1.1 presents the Company’s historical balance sheet data for the most recent five fiscal years and as of December 31, 2020. Over this period, Magyar Bancorp’s total assets have increased at a 5.8% annual rate, with loans receivable, representing the majority of the asset base, increasing at an 6.7% annual rate, a higher rate than assets over the same time period.

Assets have mostly steadily increased since fiscal 2016 as a result of efforts and strategies put into place by directors and management. Funding for such growth consisted of both deposits and borrowings, as the Company has made use of available low-cost borrowings. Newly added funds were directed to various categories within the asset base, including the loan portfolio, which has increased from 78% of assets in FY2016 to 81% of assets as of December 31, 2020. Cash and investments have been maintained at sufficient levels for liquidity purposes, while some funds have been placed into bank owned life insurance (“BOLI”). Equity reached $58.2 million at December 31, 2020 or 7.85% of assets. A summary of Magyar Bancorp’s key operating ratios for the past five years is presented in Exhibit I-3.

A key long-term business strategy of Magyar Bancorp is to increase the investment in whole loans receivable. As such, the Company’s loan portfolio totaled $598.5 million, or 80.7% of assets at December 31, 2020, an increase from $455.0 million, or 77.9% of assets as of September 30, 2016. The combination of the increase in loans receivable as a percent of assets and the additional use of deposits to fund assets resulted in the loan/deposit ratio increasing from 92.4% at September 30, 2016 to 97.8% at December 31, 2020.

Magyar Bancorp‘s investment in loans reflects the Company’s historical level of diversified lending activities which include traditional long-term fixed rate 1-4 family residential loans, along with commercial lending. The 1-4 family residential loan portfolio comprised approximately 34% of total loans as of December 31, 2020, down slightly from 38% of loans in FY2016. The Company has continued to pursue additional lending in the areas of commercial real estate, construction/land and commercial and industrial loans, with commercial and industrial loans recording the largest increase in proportion of loans. The commercial real estate/multifamily lending activities represent a primary part of the Company’s business strategy to maximize revenue (in terms of yield on portfolio loans) and provide benefits in areas such as interest rate risk. Second position home equity lines of credit and consumer loans have historically been limited to small amounts of the overall loan portfolio.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.5 |

Table 1.1

Magyar Bancorp, Inc.

Historical Balance Sheet Data

| As of September 30, | As of: December 31, 2020 |

9/30/2016- 12/31/2020 Annual Growth Rate |

||||||||||||||||||||||||||||||||||||||||||||||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Pct | ||||||||||||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | (%) | ||||||||||||||||||||||||||||||||||||||||

| Total Amount of: |

||||||||||||||||||||||||||||||||||||||||||||||||||||

| Assets |

$ | 584,377 | 100.00 | % | $ | 603,044 | 100.00 | % | $ | 623,968 | 100.00 | % | $ | 630,328 | 100.00 | % | $ | 753,997 | 100.00 | % | $ | 741,784 | 100.00 | % | 5.77 | % | ||||||||||||||||||||||||||

| Loans Receivable (net) |

455,031 | 77.87 | % | 470,693 | 78.05 | % | 508,430 | 81.48 | % | 518,217 | 82.21 | % | 603,110 | 79.99 | % | 598,530 | 80.69 | % | 6.66 | % | ||||||||||||||||||||||||||||||||

| Cash and Equivalents |

21,806 | 3.73 | % | 22,334 | 3.70 | % | 15,368 | 2.46 | % | 21,469 | 3.41 | % | 61,726 | 8.19 | % | 52,070 | 7.02 | % | 22.73 | % | ||||||||||||||||||||||||||||||||

| Investment Securities |

60,407 | 10.34 | % | 65,185 | 10.81 | % | 58,278 | 9.34 | % | 48,406 | 7.68 | % | 46,985 | 6.23 | % | 49,272 | 6.64 | % | -4.68 | % | ||||||||||||||||||||||||||||||||

| Fixed Assets |

18,084 | 3.09 | % | 17,567 | 2.91 | % | 16,990 | 2.72 | % | 16,172 | 2.57 | % | 14,746 | 1.96 | % | 14,607 | 1.97 | % | -4.90 | % | ||||||||||||||||||||||||||||||||

| BOLI |

11,257 | 1.93 | % | 11,550 | 1.92 | % | 11,843 | 1.90 | % | 13,647 | 2.17 | % | 13,971 | 1.85 | % | 14,049 | 1.89 | % | 5.35 | % | ||||||||||||||||||||||||||||||||

| Other Real Estate Owned |

12,082 | 2.07 | % | 11,056 | 1.83 | % | 8,586 | 1.38 | % | 7,528 | 1.19 | % | 2,594 | 0.34 | % | 2,072 | 0.28 | % | -33.96 | % | ||||||||||||||||||||||||||||||||

| Other Assets |

5,710 | 0.98 | % | 4,659 | 0.77 | % | 4,473 | 0.72 | % | 4,889 | 0.78 | % | 10,865 | 1.44 | % | 11,184 | 1.51 | % | 17.14 | % | ||||||||||||||||||||||||||||||||

| Depos its |

$ | 492,650 | 84.30 | % | $ | 515,201 | 85.43 | % | $ | 530,137 | 84.96 | % | $ | 530,075 | 84.10 | % | $ | 618,330 | 82.01 | % | $ | 612,064 | 82.51 | % | 5.24 | % | ||||||||||||||||||||||||||

| FHLB Advances |

36,040 | 6.17 | % | 31,905 | 5.29 | % | 35,524 | 5.69 | % | 36,189 | 5.74 | % | 67,410 | 8.94 | % | 60,260 | 8.12 | % | 12.86 | % | ||||||||||||||||||||||||||||||||

| Other Liabilities |

7,962 | 1.36 | % | 6,481 | 1.07 | % | 6,945 | 1.11 | % | 9,413 | 1.49 | % | 11,407 | 1.51 | % | 11,259 | 1.52 | % | 8.49 | % | ||||||||||||||||||||||||||||||||

| Stockholders’ Equity |

$ | 47,725 | 8.17 | % | $ | 49,457 | 8.20 | % | $ | 51,362 | 8.23 | % | $ | 54,651 | 8.67 | % | $ | 56,850 | 7.54 | % | $ | 58,201 | 7.85 | % | 4.78 | % | ||||||||||||||||||||||||||

| Tangible Stockholders’ Equity |

$ | 47,725 | 8.17 | % | $ | 49,457 | 8.20 | % | $ | 51,362 | 8.23 | % | $ | 54,651 | 8.67 | % | $ | 56,850 | 7.54 | % | $ | 58,201 | 7.85 | % | 4.78 | % | ||||||||||||||||||||||||||

| Net Unrealized Gain/(Loss) on Investment/MBS Available for Sale |

($ | 1,159 | ) | -0.20 | % | ($ | 1,004 | ) | -0.17 | % | ($ | 1,474 | ) | -0.24 | % | ($ | 1,330 | ) | -0.21 | % | ($ | 1,357 | ) | -0.18 | % | ($ | 1,393 | ) | -0.19 | % | — | |||||||||||||||||||||

| Public Shares Outstanding |

2,620,296 | 45.02 | % | 2,620,296 | 45.02 | % | 2,620,296 | 45.02 | % | 2,620,296 | 45.02 | % | 2,610,296 | 44.92 | % | 2,610,296 | 44.92 | % | — | |||||||||||||||||||||||||||||||||

| MHC Shares Outstanding |

3,200,450 | 54.98 | % | 3,200,450 | 54.98 | % | 3,200,450 | 54.98 | % | 3,200,450 | 54.98 | % | 3,200,450 | 55.08 | % | 3,200,450 | 55.08 | % | — | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

| Total Shares Outstanding |

5,820,746 | 100.00 | % | 5,820,746 | 100.00 | % | 5,820,746 | 100.00 | % | 5,820,746 | 100.00 | % | 5,810,746 | 100.00 | % | 5,810,746 | 100.00 | % | — | |||||||||||||||||||||||||||||||||

| Tangible Book Value per Share |

$ | 8.20 | — | $ | 8.50 | — | $ | 8.82 | — | $ | 9.39 | $ | 9.78 | $ | 10.02 | — | ||||||||||||||||||||||||||||||||||||

| Loans/Deposits |

92.36 | % | 91.36 | % | 95.91 | % | 97.76 | % | 97.54 | % | 97.79 | % | ||||||||||||||||||||||||||||||||||||||||

| Offices Open |

6 | 7 | 7 | 7 | 7 | 7 | ||||||||||||||||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of ending assets. |

Source: Preliminary Prospectus; RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.6 |

The intent of the Company’s cash and investment policy is to provide adequate liquidity and to generate a favorable return within the context of supporting Magyar Bancorp’s cash operating needs and credit and interest rate risk objectives. Historically, the level of cash and equivalents has fluctuated in the range of 2.5% to 8.2% based on the operating environment and cash needs. The ratio equaled 7.0% as of December 31, 2020.

Regarding the investment securities portfolio, as of December 31, 2020 the Company held investments both as available for sale (“AFS”) and as held to maturity (“HTM”), and the portfolio is managed in concert with the overall asset/liability management policy guidance and to maximize revenue. As of December 31, 2020, securities classified as HTM and AFS equaled 69% and 31% of total investments, respectively. The investment portfolio consisted of several investment types, including mortgage backed securities, US government agency debt bonds and corporate bonds, with mortgage-backed securities comprising 68% of total securities. The only other investment security consisted of the required equity investment of FHLB of New York of $2.0 million. The level of cash and investments is anticipated to increase initially following the stock offering, pending gradual redeployment into higher yielding loans. Details of the Company’s investment securities portfolio are presented in Exhibit I-4.

Magyar Bancorp owns the headquarters office in New Brunswick, New Jersey and one other office and lease the remaining five branch offices. Details of the investment in fixed assets by branch are presented in Exhibit II-2. The investment in fixed assets has decreased in recent periods as depreciation expense has exceeded an additional investment in fixed assets.

Reflecting in improvement in asset quality, Magyar Bancorp has recorded a substantial decline in the balances of other real estate owned (“OREO”) over the period from 2016 to 2020. The OREO in 2016 consisted of a variety of property types, including construction/land, 1-4 family properties and commercial real estate/multifamily. The Company has successfully reduced the OREO balance through efforts to resolve the problem assets through workouts and sales and more stringent lending activities that have reduced new OREO properties.

Magyar Bancorp maintains an investment in bank-owned life insurance (“BOLI”) policies, as a source of funding for employee benefit expenses and to provide tax-advantaged income. As of December 31, 2020, the cash surrender value of the Company’s BOLI equaled $14.0 million or 1.89% of assets.

As shown in Table 1.1, since September 30, 2016 Magyar Bancorp’s funding needs have been provided by retail deposits, borrowings and retained earnings. The balance of the

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.7 |

Company’s deposits has increased at a slightly slower pace than assets since 2016, recording an annualized growth rate of 5.24%. Borrowings have increased at a higher rate, in particular in more recent periods, mostly due to the participation in the Paycheck Protection Program (“PPP”), as non-PPP loans have declined. Borrowings use is generally based on the indicated cost of these funds in comparison to deposits, and the respective term for interest rate risk management purposes, along with the ability to obtain such funds in a timely manner to support the lending and overall growth objectives. As a result of the relative growth in assets, the proportion of assets funded with deposits has decreased slightly from 84% to 83% since fiscal 2016. The Company maintains a notable level of core deposit accounts in checking and savings accounts, which comprised 51% of deposits at December 31, 2020, with this ratio increasing from 44% as of September 30, 2016.

The balance of equity increased between fiscal 2016 and December 31, 2020 as Magyar Bancorp recorded consistent profitable operations. Reflecting the combination of this increase in equity and the increase in assets over that time period, the equity-to-assets ratio has remained in the range of 7.50% to 8.75% of assets over that time period, and equaled 7.85% at December 31, 2020. All of the Company’s equity is tangible, and the Company maintained surpluses relative to all of its regulatory capital requirements at December 31, 2020. The pro forma return on equity (“ROE”) is expected to initially decline given the increased equity position.

Income and Expense Trends

Table 1.2 presents the Company’s income and expense trends over the past five fiscal years and for the 12 months ended December 31, 2020. The table reveals the Company has recorded consistently profitable operations over the time period, and profitability has averaged 0.33% of average assets since fiscal 2016. Non-operating items have been substantially limited and consisted of gains on the sale of investment securities.

Magyar Bancorp’s net interest income to average assets ratio has reflected the impact of market interest rate trends and internal asset investment and funding strategies over the time period shown in Table 1.2. Net interest income as a percent of average assets increased through FY2019, reflecting the higher interest rate environment at that time, with the asset yields supported by the increasing investment in commercial, construction and other loans. The noted rise and then fall of funding costs in Table 1.2 reflects the interest rate environment and also has been impacted by the increase in lower cost core deposit from the lending diversification, along

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.8 |

Table 1.2

Magyar Bancorp, Inc.

Historical Income Statements

| For the Year Ended September 30, | 12 Mths ended, December 31, 2020 |

|||||||||||||||||||||||||||||||||||||||||||||||

| 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||

| Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | Amount | Pct(1) | |||||||||||||||||||||||||||||||||||||

| ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||||||||||

| Interest Income |

$ | 20,451 | 3.56 | % | $ | 21,978 | 3.71 | % | $ | 24,350 | 3.96 | % | $ | 27,103 | 4.25 | % | $ | 26,927 | 3.93 | % | $ | 27,156 | 3.82 | % | ||||||||||||||||||||||||

| Interest Expense |

(3,532 | ) | -0.62 | % | (3,773 | ) | -0.64 | % | (4,649 | ) | -0.76 | % | (6,710 | ) | -1.05 | % | (5,513 | ) | -0.81 | % | (4,827 | ) | -0.68 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net Interest Income |

$ | 16,919 | 2.95 | % | $ | 18,205 | 3.07 | % | $ | 19,701 | 3.20 | % | $ | 20,393 | 3.20 | % | $ | 21,414 | 3.13 | % | $ | 22,329 | 3.14 | % | ||||||||||||||||||||||||

| Provision for Loan Losses |

(1,366 | ) | -0.24 | % | (1,343 | ) | -0.23 | % | (997 | ) | -0.16 | % | (668 | ) | -0.10 | % | (1,666 | ) | -0.24 | % | (2,096 | ) | -0.29 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net Interest Income after Provisions |

$ | 15,553 | 2.71 | % | $ | 16,862 | 2.84 | % | $ | 18,704 | 3.04 | % | $ | 19,725 | 3.09 | % | $ | 19,748 | 2.89 | % | $ | 20,233 | 2.85 | % | ||||||||||||||||||||||||

| Gain(Loss) on Sale of Loans |

$ | 625 | 0.11 | % | $ | 324 | 0.05 | % | $ | 493 | 0.08 | % | $ | 193 | 0.03 | % | $ | 317 | 0.05 | % | $ | 554 | 0.08 | % | ||||||||||||||||||||||||

| Other Income |

1,448 | 0.25 | % | 1,675 | 0.28 | % | 1,521 | 0.25 | % | 1,826 | 0.29 | % | 1,331 | 0.19 | % | 1,915 | 0.27 | % | ||||||||||||||||||||||||||||||

| Operating Expense |

(15,943 | ) | -2.78 | % | (16,444 | ) | -2.77 | % | (17,323 | ) | -2.82 | % | (17,600 | ) | -2.76 | % | (18,353 | ) | -2.68 | % | (18,544 | ) | -2.61 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net Operating Income |

$ | 1,683 | 0.29 | % | $ | 2,417 | 0.41 | % | $ | 3,394 | 0.55 | % | $ | 4,144 | 0.65 | % | $ | 3,043 | 0.44 | % | $ | 4,158 | 0.59 | % | ||||||||||||||||||||||||

| Non-Operating Income/Expense |

||||||||||||||||||||||||||||||||||||||||||||||||

| Gain(Loss) on Sale/Impair of Investments |

$ | 72 | 0.01 | % | $ | 0 | 0.00 | % | $ | 107 | 0.02 | % | $ | 117 | 0.02 | % | $ | 68 | 0.01 | % | $ | 68 | 0.01 | % | ||||||||||||||||||||||||

| Income/(Loss) Before Tax |

$ | 1,755 | 0.31 | % | $ | 2,417 | 0.41 | % | $ | 3,501 | 0.57 | % | $ | 4,261 | 0.67 | % | $ | 3,111 | 0.45 | % | $ | 4,226 | 0.59 | % | ||||||||||||||||||||||||

| Income Tax Provision (Benefit) |

(664 | ) | -0.12 | % | (994 | ) | -0.17 | % | (1,471 | ) | -0.24 | % | (1,265 | ) | -0.20 | % | (921 | ) | -0.13 | % | (1,252 | ) | -0.18 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net Income (Loss) |

$ | 1,091 | 0.19 | % | $ | 1,423 | 0.24 | % | $ | 2,030 | 0.33 | % | $ | 2,996 | 0.47 | % | $ | 2,190 | 0.32 | % | $ | 2,974 | 0.42 | % | ||||||||||||||||||||||||

| Adjusted Earnings |

||||||||||||||||||||||||||||||||||||||||||||||||

| Net Income |

$ | 1,091 | 0.19 | % | $ | 1,423 | 0.24 | % | $ | 2,030 | 0.33 | % | $ | 2,996 | 0.47 | % | $ | 2,190 | 0.32 | % | $ | 2,974 | 0.42 | % | ||||||||||||||||||||||||

| Deduct: Net Gain on Sale/Impair of Invests |

(72 | ) | -0.01 | % | 0 | 0.00 | % | (107 | ) | -0.02 | % | ($ | 117 | ) | -0.02 | % | ($ | 68 | ) | -0.01 | % | ($ | 68 | ) | -0.01 | % | ||||||||||||||||||||||

| Addback: Federal Tax Law Impact |

0 | 0.00 | % | 0 | 0.00 | % | 0 | 0.00 | % | — | 0.00 | % | — | 0.00 | % | — | 0.00 | % | ||||||||||||||||||||||||||||||

| Tax Effect (2) |

24 | 0.00 | % | 0 | 0.00 | % | 36 | 0.01 | % | 25 | 0.00 | % | 14 | 0.00 | % | 14 | 0.00 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Adjusted Earnings |

$ | 1,043 | 0.18 | % | $ | 1,423 | 0.24 | % | $ | 1,959 | 0.32 | % | $ | 2,904 | 0.46 | % | $ | 2,136 | 0.31 | % | $ | 2,920 | 0.41 | % | ||||||||||||||||||||||||

| Diluted Weighted Avg. Shares Outst. |

5,820,563 | 5,820,746 | 5,820,746 | 5,820,746 | 5,817,480 | 5,814,980 | ||||||||||||||||||||||||||||||||||||||||||

| Diluted Earnings Per Share |

$ | 0.19 | $ | 0.24 | $ | 0.35 | $ | 0.51 | $ | 0.38 | $ | 0.51 | ||||||||||||||||||||||||||||||||||||

| Diluted Adjusted Earnings Per Share |

$ | 0.18 | $ | 0.24 | $ | 0.34 | $ | 0.50 | $ | 0.37 | $ | 0.50 | ||||||||||||||||||||||||||||||||||||

| Expense Coverage Ratio (3) |

106.1 | % | 110.7 | % | 113.7 | % | 115.9 | % | 116.7 | % | 120.4 | % | ||||||||||||||||||||||||||||||||||||

| Efficiency Ratio (4) |

83.9 | % | 81.4 | % | 79.8 | % | 78.5 | % | 79.6 | % | 74.8 | % | ||||||||||||||||||||||||||||||||||||

| Effective Tax Rate Cost (Benefit) |

-37.8 | % | -41.1 | % | -42.0 | % | -29.7 | % | -29.6 | % | -29.6 | % | ||||||||||||||||||||||||||||||||||||

| Return on Equity |

2.28 | % | 2.90 | % | 3.95 | % | 5.47 | % | 3.85 | % | 5.28 | % | ||||||||||||||||||||||||||||||||||||

| (1) | Ratios are as a percent of average assets. |

| (2) | Assumes a 34% effective tax rate, federal tax law change is not tax-affected through 2017 and 21% federal rate thereafter. |

| (3) | Expense coverage ratio calculated as net interest income before provisions for loan losses divided by operating expenses. |

| (4) | Efficiency ratio calculated as op. exp. divided by the sum of net int. inc. before prov. for loan losses plus other income (excluding net gains). |

Source: Audited financial statements, internal financial statements; RP Financial calculations.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.9 |

with the increased borrowings used in recent periods. Both the interest income and interest expense ratios have followed the same trend, with such rates rising through FY2019 and then declining thereafter. This is indicative of the Company’s continued focus on interest rate risk management and the benefits of the diversified lending away from long-term fixed rate residential loans. The Company’s interest rate spreads and yields and costs for the past three and one-quarter years are set forth in Exhibits I-3 and I-5.

Non-interest operating income has historically been a modest contributor to the Company’s income statement and averaged 0.26% of average assets for the most recent five and one quarter fiscal years and equaled 0.27% of average assets for the most recent 12-month period. Most of this income is gained from deposit account fees and the BOLI investment income.

Magyar Bancorp sells loans to third parties as a strategy to assist in interest rate risk and realize gains on the sale of such loans. The Company sells the guaranteed portion of a portion of Small Business Administration (“SBA”) loans that are originated and also has occasionally sold long-term fixed rate residential loans into the secondary market, mostly on a servicing retained basis. Thus, the Company has recorded some income on gains on sale of loans sold. Such gains on sale totaled $554,000, or 0.08% of average assets for the 12 months ended December 31, 2020. As of December 31, 2020, the Company was servicing $23.4 million of SBA loans and $4.1 million of residential loans serviced for others portfolio and maintained a corresponding capitalized mortgage servicing rights of $8,000.

Operating expenses represent the other major component of the Company’s income statement, and as shown in Table 1.2, such expenses have declined somewhat as a percent of average assets and have increased in dollar amount since 2016. Total operating expenses equaled $18.5 million, or 2.61% of average assets during the 12 months ended December 31, 2020. The increase in the dollar amount of operating expenses since 2016 reflects the overall growth of the Company’s operations, continued focus on lending diversification, general inflation costs and the overall costs of operations and increases in compensation/benefits for employees to staff the various operating departments of the Company. Upward pressure will be placed on the Company’s expense ratio following the stock offering, due to expenses associated with operating as a publicly-traded company, including expenses related to the stock benefit plans, auditing and legal costs.

The trends in the net interest income (including the gains on sale of loans) and operating expense ratios since fiscal 2016 have caused the expense coverage ratio (net interest

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.10 |

income/gains on sale divided by operating expenses) to trend upward within the range of 106% to 120% since FY2016. Also reflecting a similar trend, Magyar Bancorp’s efficiency ratio (operating expenses as a percent of the sum of net interest income and other operating income, including mortgage banking income) has trended lower from 84% for fiscal 2016 to 75% for the 12 months ended December 31, 2020.

As noted earlier, loan loss provisions have had a modest impact on the income statement as Magyar Bancorp has recorded improved asset quality ratios and recorded a declining level of asset charge offs since 2016, while growth in the loan portfolio has required some additional reserves. Loan loss provisions have averaged $1.4 million, or 0.21% of average assets from FY2016 to the most recent 12-month period. As of December 31, 2020, the ALLL equaled $7.1million, or 71.0% of non-performing loans and 1.17% of total loans receivable. Exhibit I-6 sets forth the Company’s allowance for loan loss activity during the past two years and three months.

As noted earlier, non-operating items have had a minimal impact on the Company’s income statement since fiscal 2016 and have consisted of small amounts of gains on the sale of securities.

Magyar Bancorp has recorded income tax rates of approximately 30% since fiscal 2019, and tax rates of approximately 40% in prior years, based on the prevailing federal and state corporate tax rates.

Interest Rate Risk Management

Magyar Bancorp’s balance sheet is asset-sensitive in the shorter-term and, thus, the net interest margin will typically be favorably affected during periods of rising and higher interest rates. Magyar Bancorp measures its interest rate risk exposure by examining the change in net interest income under the assumed instantaneous changes in the U.S. treasury yield curve. Utilizing figures as of December 31, 2020, based on a 2.0% instantaneous and sustained increase in interest rates, the net interest income model indicates that the Bank’s net interest income would increase by 0.49% in year 1 and by 0.85% in year two (see Exhibit I-7).

The Company pursues strategies to manage interest rate risk, particularly with respect to seeking to limit the repricing mismatch between interest rate sensitive assets and liabilities. The Company manages interest rate risk from the asset side of the balance sheet by retaining in portfolio fewer fixed rate residential loans and by originating and retaining adjustable rate loans

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.11 |

in the residential, construction and commercial portfolios, all of which have shorter terms to repricing or maturity, and generally carry higher interest rates. On the liability side of the balance sheet, management of interest rate risk has been pursued through attempting to retain the balance of deposits in lower cost and less interest rate sensitive transaction and savings accounts, along with increasing the balance of money market accounts, which offer a variable rate based on market indications. The Company has also utilized advances from the FHLB of New York to “match-fund” certain longer-term loans. Core deposits, which consist of transaction and savings accounts, comprised 80.6% of the Bank’s deposits at December 31, 2020. As of September 30, 2020, of the Bank’s total loans due after September 30, 2021, ARM loans comprised 61.3% of those loans (see Exhibit I-8). In addition, the Bank maintains a notable balance of cash and cash equivalents, which provide for short-term to maturity funds on the balance sheet. Finally, the Bank maintains an equity position of almost 8% of assets, representing interest-free funds that can be used to fund earning assets. The infusion of stock proceeds will serve to further limit the Bank’s interest rate risk exposure, as most of the net proceeds will be redeployed into interest-earning assets and the increase in the Bank’s equity will lessen the proportion of interest rate sensitive liabilities funding assets.

There are numerous limitations inherent in interest rate risk analyses such as the credit risk of the Company’s loans pursuant to changing interest rates. Additionally, such analyses do not measure the impact of changing spread relationships, as interest rates among various asset and liability accounts rarely move in tandem, as the shape of the yield curve for various types of assets and liabilities is constantly changing in response to investor perceptions and economic events and circumstances.

Lending Activities and Strategy

Magyar Bancorp operates a diversified lending strategy, with active lending operations in 1-4 family residential, commercial real estate, commercial business and construction/land lending. The overall lending strategy is to diversify its overall loan portfolio, shorten the term-to-maturity or repricing, and increase the overall yield earned on loans. Details of the Bank’s loan portfolio composition are shown in Exhibit I-9, while Exhibit I-10 provides details of the Bank’s loan portfolio by contractual maturity date.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.12 |

Residential Real Estate Lending

Magyar Bancorp’s historical lending focus has included the origination of first position 1-4 family residential real estate loans. As of December 31, 2020, residential first and second position mortgage loans equaled $228.2 million, or 37.6% of total loans, with adjustable rate loans totaling approximately 39% of total residential mortgage loans. As shown in Exhibit I-9, the balance of residential mortgage loans (first and second position) has increased since September 30, 2016, while the proportion of such loans has declined from 42.6% to 37.6%. The Company generally retains most originations of conforming fixed-rate one- to four-family residential real estate loans.

Magyar Bancorp’s first mortgage loans are generally underwritten to Freddie Mac origination guidelines and thus are deemed to be “conforming” loans with terms of 10 to 30 years. Most of the 1-4 family mortgage loans are secured by residences in the central and northern New Jersey market. Loan-to-value ratios (“LTV”) of mortgage loans are generally limited to an 80% LTV, or up to 95% if the loans carry private mortgage insurance. Adjustable rate loans have an initial fixed interest rate period of one to ten years, followed by annual adjustments to the interest rate, with a 2% period cap on changes in interest rates and a 5% lifetime interest adjustment rate cap. Magyar Bancorp does not offer “interest only”, “negative amortization”, subprime or Alt-A loans, which have higher risk underwriting characteristics. The Company also offers low- to moderate income residential mortgage loans originated using Freddie Mac guidelines.

Commercial Real Estate/Multi-Family Lending

As of December 31, 2020, commercial real estate/multi-family loans totaled $260.3 million, or 42.9% of the total loan portfolio, versus $199.5 million, or 43.6% of loans as of September 30, 2016. The balances of these loans have been trending upward in recent years due to the Company’s focus to diversify its loan portfolio and increase yield. These types of loans are attractive credits given the higher yields, larger balances, shorter duration and prospective relationship potential.

Commercial real estate loans are generally secured by five-or-more-unit apartment buildings, industrial properties and properties used for business purposes such as small office buildings and retail facilities. Adjustable-rate commercial real estate loans are originated with a maximum term of 25 years with adjustable rate periods every five years. The maximum LTV for commercial real estate loans is 75%, based on the appraised value of the property.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.13 |

These loans are generally priced at a higher rate of interest, have larger balances and involve a greater risk profile than 1-4 residential mortgage loans. Often the payments on commercial real estate loans are dependent on successful operations and management of the property. When originating commercial real estate loans, the Company evaluates the qualifications and financial condition of the borrower, as well as the value and condition of the property securing the loan. The Company will also generally require and obtain personal guarantees from the principals and generally requires a debt service coverage ratio of at least 120%. At December 31, 2020, the Company’s largest commercial real estate loan was $6.1 million to refinance a 21,000 square foot building consisting of office, retail, and storage units in Summit, New Jersey. The loan was performing in accordance with its repayment terms at December 31, 2020.

Construction Loans

Construction loans represent an area of lending diversification for Magyar Bancorp, and such loans totaled $23.4 million, or 3.9% of loans as of December 31, 2020. Construction loans are generally offered to experienced local developers operating in the primary market area and to individuals for the construction of their personal residences. Construction loans for both residential and commercial properties usually have a maximum term of 24 months. At the end of the construction phase, the loan generally converts to a permanent real estate mortgage loan, but in some cases it may be payable in full. Loans can be made with a maximum loan-to-value ratio of 75% of the appraised market value upon completion of the project. The Company provides financing for land acquisition and site improvement. Land acquisition loans are limited to an LTV of 50% to 75% of the sale price of the land. At December 31, 2020, the largest outstanding construction loan was a $2.8 million loan to finance the construction of single-family home in Colts Neck, New Jersey.

Construction loans generally involve greater credit risk than improved owner-occupied real estate lending. Magyar Bancorp reviews and inspects each property before disbursement of loan funds, and also requires detailed cost estimates to complete the construction project and an appraisal of the property.

Commercial Business Loans

As part of the strategy of diversifying the loan portfolio, Magyar Bancorp originates commercial business loans and lines of credit on non-real estate commercial business assets.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.14 |

The Company originates commercial business loans to small businesses and professionals located in its market area. As of December 31, 2020, the Company had $91.2 million of commercial business loans in portfolio, equal to 15.0% of total loans. Magyar Bancorp encourages the borrowers to maintain their primary deposit accounts with the Bank. The Company also originates Small Business Administration (“SBA”) 7(a) loans, on which the SBA provides guarantees of up to 90% of the principal balance. The Company generally sells the guaranteed portions of the SBA loan into the secondary market. Included in the December 31, 2020 balance was $46.0 million of loans originated through the SBA’s Paycheck Protection Program (“PPP”). The PPP loans are part of the Company’s actions to support its customers and the local communities. The PPP loans have terms of either two or five years and a 1.0% interest rate. The Company also received approximately $2.0 million in fees during 2020.

Commercial business loans are generally lines of credit with terms of up to 25 years and are generally used for longer-term working capital purposes. Commercial business loans are originated with either fixed for adjustable rates of interest. Lines of credit typically carry variable interest rates tied to the prime rate of interest that adjust annually or are tied to an index. Commercial business loans have greater credit risk compared to 1-4 family residential real estate loans, because the availability of funds for the repayment of commercial business loans are dependent on the success of the business and the general economic environment of the Company’s market area. The Company generally considers the financial statements, debt service capabilities, cash flows and the Company’s history of the borrower, and generally required a loan-to-value ratio of no more than 75%.

Consumer Lending (including HELOCs)

Magyar Bancorp originates personal consumer loans to individuals who reside or work in the Company’s market area, including loans secured by home equity lines of credit and personal consumer loans. Consumer loans have greater risk compared to mortgage loans, due to their dependence on the borrower’s continuing financial stability.

At December 31, 2020, home equity lines of credit totaled $19.8 million in outstanding balances. The underwriting standards utilized for home equity lines of credit include a determination of the applicant’s credit history, an assessment of the applicant’s ability to meet existing obligations and payments on the proposed loan and the value of the collateral securing the loan. Home equity lines of credit are offered with a loan-to-value ratio up to 80%. Our home equity lines of credit are generally 10-year balloon loans. Our home equity lines of credit have adjustable rates of interest which are indexed to the prime rate of interest and terms of up to 25 years.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.15 |

The Company also originates stock-secured loans, secured by the common stock of publicly-traded companies, provided the company is listed on the New York Stock Exchange or the NASDAQ Stock Market. These loans are interest only with terms of up to 12 months and for adjustable rates of interest indexed to the prime rate. The LTV is limited to 70% of the value of the stock securing the loan at any time. These loans totaled $3.8 million as of December 31, 2020, with a limit of 15% of the Bank’s capital, with the exception of Johnson & Johnson, a larger local employer, for which the limit is 150% of the Bank’s capital.

Loan Originations, Purchases and Sales

All lending activities are conducted by bank personnel located at the office locations, underwritten pursuant to bank policies and procedures. Loan sources typically include loan officers, marketing efforts, the existing customer base, walk-in customers and referrals from real estate brokers, builders and attorneys.

Generally, the Company retains in portfolio substantially all loans that are originated, as historically the Company has not originated a significant number of loans for the purpose of resale into the secondary market. Any loans that are sold are sold on a servicing retained basis. These sales provide benefits in terms of interest rate risk management and also provide for current period income in the form of gains on the sale of loans.

Magyar Bancorp has also periodically purchased or sold participation loans from or with other financial institutions in the market area. Such loans are underwritten according to the Bank’s underwriting criteria and procedures. At December 31, 2020 the outstanding balances of purchased loan participations totaled $19.8 million, while the balance of sold participations equaled $16.9 million. All such loans were performing as of December 31, 2020. Magyar Bancorp has not historically purchased residential mortgage loans, except for loans to low-income borrowers as part of the Community Reinvestment Act program.

Asset Quality

Magyar Bancorp’s lending operations include originations of commercial real estate/multi-family, commercial business, construction/land and consumer loans for portfolio, all of which carry a higher risk profile than traditional 1-4 family mortgage lending. In recent years the Company

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.16 |

has maintained a moderate level of non-performing assets (“NPAs”), consisting of non-accruing loans, real estate owned and performing troubled debt restructured loans (“TDRs”). Exhibit I-11 presents a history of NPAs for the Company since 2016. NPAs reached a high of $16.3 million as of September 30, 2016, and since then have been reduced to $12.3 million as of December 31, 2020, consisting of non-accruing loans of $10.0 million, real estate owned of $2.1 million and accruing troubled debt restructured loans of $218,000. The non-accruing loans and real estate owned were comprised of 1-4 family residential, commercial real estate, construction and commercial business loans.

To track the Company’s asset quality and the adequacy of valuation allowances, Magyar Bancorp has established detailed asset classification policies and procedures which are consistent with regulatory guidelines. Detailed asset classifications are reviewed quarterly by senior management and the Board. Pursuant to these procedures, when needed, the Company establishes additional valuation allowances to cover anticipated losses in classified or non-classified assets. As of December 31, 2020, the Company maintained an allowance for loan losses of $7.13 million, equal to 1.17% of total loans receivable and 71.0% of non-performing loans.

Funding Composition and Strategy

Magyar Bank has traditionally utilized both deposits and borrowings as funding sources. At December 31, 2020, deposits equaled $612.1 million. Exhibit I-12 sets forth the Bank’s deposit composition since September 30, 2018 and Exhibit I-13 provides the maturity composition of the certificate of deposit (“CD”) portfolio at December 31, 2020 for all uninsured CDs in excess of $100,000 in balance. Money Market Accounts constitute the largest portion of the deposit base, totaling 29.4% of deposits at December 31, 2020 versus 31.6% of deposits as of September 30, 2018. Checking and savings accounts equaled $313.1 million, or 51.2% of total deposits as of December 31, 2020, versus $232.5 million, or 43.9% of total deposits at September 30, 2018. A portion of the checking account balances include certain funds from the PPP lending program instituted in 2020.

Magyar Bank has historically utilized borrowed funds as a funding source, and such borrowings totaled $60.3 million as of December 31, 2020 with the funds used to support lending activities and liquidity. Of the borrowed funds, $29.8 million were borrowed under the recent Paycheck Protection Program Liquidity Facility. Additional detail of the borrowings portfolio is presented in Exhibit I-14, indicating a weighted average rate of 1.23% as of December 31, 2020. The remaining borrowings consisted of FHLB of New York advances.

| RP® Financial, LC. | OVERVIEW AND FINANCIAL ANALYSIS | |

| I.17 |

Subsidiary Operations

The Bank is the only subsidiary of Magyar Bancorp. Magyar Bank has three subsidiaries as follows: Magyar Investment Company, which holds investment securities for certain state income tax benefits; Hungaria Urban Renewal, LLC which holds the Company’s main office facility (land and building); and Magyar Service Corp., which offers bank customers a range of non-deposit investment products and financial planning services, including insurance products, fixed and variable annuities, and retirement planning for individual and commercial customers.

Legal Proceedings

Magyar Bancorp is not involved in any pending legal proceedings other than routine legal proceedings occurring in the ordinary course of business which, in the aggregate, are believed by management to be immaterial to the financial condition of the Company.

| RP® Financial, LC. | OPERATING ENVIRONMENT AND MARKET AREA | |

| Page II.1 |

II. OPERATING ENVIRONMENT AND MARKET AREA

Introduction

Magyar Bank is headquartered in the city of New Brunswick, Middlesex County, New Jersey, in east central New Jersey. The Bank operates a community banking business through its headquarters office five branch offices in Middlesex County, and two branch offices in Somerset County, New Jersey, located northwest of Middlesex County. While the market area for deposit gathering is concentrated in the local communities in which a branch office is maintained, the Bank also conducts lending operations over a somewhat wider area, defined as Central and Northern portions of New Jersey. A map of the Bank’s office locations is included as Exhibit I-1.

The Bank focuses on providing personal service while meeting the needs of its business and retail customer base, emphasizing personalized banking services to retail customers and full service activities for business customers. Deposit services offered include demand deposits, business accounts, regular savings accounts, money market deposits, certificates of deposit and individual retirement accounts. Recent strategic actions have focused on continuing the historical growth trends, and maintaining a diversified lending program in the areas of residential, commercial and construction lending.

Future business and growth opportunities for the Bank depend on the future growth trends of the local and regional economy, demographic growth trends and the nature and intensity of the competitive environment. These factors have been briefly examined to help determine the growth potential that exists for the Bank, the relative economic health of the Bank’s market area, and the resultant impact on value.

National Economic Factors

After expanding for over 10 years, the longest on record, the national economic expansion came to an end in the second quarter of 2020 as a result of the COVID-19 pandemic and related shutdown of businesses and economic activity on both a personal and business basis. Through December 2020, the worldwide impact of COVID-19 has caused a substantial change in current and go-forward expectations in many economic performance factors, including the United States GDP growth. Following annual GDP growth in the range of 1.0% to 3.0% during the most recent economic expansion, the United States GDP declined by 3.5% for calendar year 2021, with a

| RP® Financial, LC. | OPERATING ENVIRONMENT AND MARKET AREA | |

| Page II.2 |

sharp decline in the second quarter (31.4%) and strong growth in the third quarter (33.4%) as a result of the implementation of federal assistance payments. Based on the most recent Wall Street Journal (“WSJ”) economists’ forecast, GDP is projected to increase by 4.2% for all of 2021, indicating a welcome return to economic growth. This growth, however, would be achieved through substantial public spending and related increase in the federal debt, as the fiscal 2020 budget deficit totaled $3.1 trillion, and expectations are that substantial deficits will continue based on pre-COVID deficit levels and that additional COVID-related spending will be required.

The economy has recorded job growth in recent years, with an average of 2.4 million jobs added annually over the 2015-2019 time period, indicating a steady and notable growth period. As was the case with GDP performance noted above, United States job growth turned negative in March 2020, with the labor force contracting by 1.4 million in March and 20.8 million in April 2020, reflecting an unprecedented deterioration in the employment sector of the economy. During the May-November 2020 time period, a total of 12.5 million jobs were added to the workforce, reflecting a recovery of a portion of the prior losses. However, the December 2020 jobs report indicated a net loss of 140,000 jobs, indicating a continued weakness to the economy. Near-term expectations for employment gains are for a gradual improvement, particularly as the daily impacts of COVID-19 diminish, with quarterly average job growth of 419,000 as estimated by the WSJ economists forecast.

For 2020, the annualized national inflation rate was 1.33%, compared to 2.11% for CY19 and 2.44% for CY18, indicating inflation has been kept under control, which is a focus of the Federal Reserve policy. The 2020 inflation rate was impacted substantially by the COVID-19 crisis, reflecting the reduced demand for products and services nationwide and therefore lower inflation. The Federal Reserve has recently indicated that it intends to manage inflation and interest rates differently, effectively allowing prices to run higher in order to accelerate growth and bring down unemployment. For example, instead of targeting a two percent inflation level and raising rates to head off price pressure, the Federal Reserve would aim for an average of two percent over time, which would let inflation briefly run higher.

Economists have been focused in recent periods on the national unemployment rate, which prior to 2020 had been at levels considered to be “full employment” for the last year and a half. From highs reached during the national recession of 2008-2009 in the range of 10%, the unemployment rate steadily declined and equaled 3.5% as of December 2019, the lowest rate in 2019. In calendar year 2020, the unemployment rate remained below 4.0% through February

| RP® Financial, LC. | OPERATING ENVIRONMENT AND MARKET AREA | |

| Page II.3 |