Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - TC Bancshares, Inc. | d882215dex991.htm |

| EX-99.2 - EX-99.2 - TC Bancshares, Inc. | d882215dex992.htm |

| EX-23.3 - EX-23.3 - TC Bancshares, Inc. | d882215dex233.htm |

| EX-23.2 - EX-23.2 - TC Bancshares, Inc. | d882215dex232.htm |

| EX-21 - EX-21 - TC Bancshares, Inc. | d882215dex21.htm |

| EX-16.1 - EX-16.1 - TC Bancshares, Inc. | d882215dex161.htm |

| EX-10.1 - EX-10.1 - TC Bancshares, Inc. | d882215dex101.htm |

| EX-8 - EX-8 - TC Bancshares, Inc. | d882215dex8.htm |

| EX-5 - EX-5 - TC Bancshares, Inc. | d882215dex5.htm |

| EX-4 - EX-4 - TC Bancshares, Inc. | d882215dex4.htm |

| EX-3.2 - EX-3.2 - TC Bancshares, Inc. | d882215dex32.htm |

| EX-3.1 - EX-3.1 - TC Bancshares, Inc. | d882215dex31.htm |

| EX-2 - EX-2 - TC Bancshares, Inc. | d882215dex2.htm |

| EX-1.1 - EX-1.1 - TC Bancshares, Inc. | d882215dex11.htm |

| S-1 - FORM S-1 - TC Bancshares, Inc. | d882215ds1.htm |

Exhibit 99.3

FELDMAN FINANCIAL ADVISORS, INC.

8804 MIRADOR PLACE

MCLEAN, VA 22102

(202) 467-6862

|

TC Federal Bank

Thomasville, Georgia

Conversion Valuation Appraisal Report

Valued as of February 26, 2021

Prepared By

Feldman Financial Advisors, Inc. McLean, Virginia

|

FELDMAN FINANCIAL ADVISORS, INC.

8804 MIRADOR PLACE

MCLEAN, VA 22102

(202) 467-6862

February 26, 2021

Board of Directors

TC Federal Bank

131 South Dawson Street

Thomasville, Georgia 31792

Members of the Board of Directors:

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated pro forma market value of TC Federal Bank (the “Bank”) as of February 26, 2021 in conjunction with the Bank’s conversion (the “Conversion”) from the mutual to stock form of organization, issuance of all of its capital stock to a newly formed stock holding company known as TC Bancshares, Inc. (the “Company”), and offering for sale of the Company’s common stock to eligible depositors and borrowers of the Bank, the Bank’s employee stock ownership plan, and certain members of the general public in a subscription and community offering (the “Stock Offering”). The Appraisal is furnished pursuant to the filing by the Bank of applications with respect to the Conversion and the Stock Offering with the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, and the Georgia Department of Banking and Finance.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and advisory firm that specializes in valuations and analyses of business enterprises and securities in the thrift, banking, and mortgage industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of the Bank that included discussions with the Bank’s management, the Bank’s legal counsel, Bryan Cave Leighton Paisner LLP, and the Bank’s independent registered public accounting firm, Wipfli, LLP. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

We also reviewed, among other factors, the economy in the Bank’s primary market area and compared the Bank’s financial condition and operating performance with that of selected publicly traded thrift institutions. We reviewed conditions in the securities markets in general and in the market for thrift institution common stocks in particular.

The Appraisal is based on the Bank’s representation that the information in the Conversion applications and additional evidence furnished to us by the Bank and its independent auditor are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Bank and its independent accounting firm, nor did we independently value the assets or liabilities of the Bank. The Appraisal considers the Bank only as a going concern and should not be considered as an indication of the liquidation value of the Bank.

FELDMAN FINANCIAL ADVISORS, INC.

Board of Directors

TC Federal Bank

February 26, 2021

Page Two

It is our opinion that, as of February 26, 2021, the estimated pro forma market value of the Bank was within a range (the “Valuation Range”) of $39,950,000 to $54,050,000 with a midpoint of $47,000,000. The Valuation Range was based upon a 15% decrease from the midpoint to determine the minimum and a 15% increase from the midpoint to establish the maximum. Assuming an additional 15% increase above the maximum value would result in an adjusted maximum of $62,157,500. Based on an initial offering price of $10.00 per share, the shares to be sold in the Stock Offering from a minimum of 3,995,000 shares to a maximum of 5,405,000 shares with an adjusted maximum of 6,215,750 shares.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because the Appraisal is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Bank’s pro forma market value. Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws, and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The Valuation Range reported herein will be updated as appropriate. These updates will consider, among other factors, any developments or changes in the Bank’s operating performance, financial condition, or management policies, and current conditions in the securities markets for thrift institution common stocks. Should any such new developments or changes be material, in our opinion, to the valuation of the Bank, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in detail at that time.

| Respectfully submitted, |

| Feldman Financial Advisors, Inc. |

| /s/ Trent R. Feldman |

| Trent R. Feldman |

| President |

| /s/ Peter W. L. Williams |

| Peter W. L. Williams |

| Principal |

FELDMAN FINANCIAL ADVISORS, INC.

TABLE OF CONTENTS

| TAB |

PAGE | |||||

| INTRODUCTION |

1 | |||||

| I. |

CHAPTER ONE – BUSINESS OF TC FEDERAL BANK | |||||

| General Overview |

3 | |||||

| Financial Condition |

12 | |||||

| Income and Expense Trends |

24 | |||||

| Interest Rate Risk Management |

32 | |||||

| Asset Quality |

37 | |||||

| Office Facilities |

40 | |||||

| Market Area |

41 | |||||

| Summary Outlook |

56 | |||||

| II. |

CHAPTER TWO – COMPARISONS WITH PUBLICLY TRADED COMPANIES | |||||

| General Overview |

58 | |||||

| Selection Criteria |

59 | |||||

| Recent Financial Comparisons |

63 | |||||

| III. |

CHAPTER THREE – MARKET VALUE ADJUSTMENTS | |||||

| General Overview |

75 | |||||

| Earnings Prospects |

76 | |||||

| Financial Condition |

77 | |||||

| Market Area |

78 | |||||

| Management |

79 | |||||

| Dividend Payments |

80 | |||||

| Liquidity of the Issue |

81 | |||||

| Subscription Interest |

81 | |||||

| Recent Acquisition Activity |

83 | |||||

| Effect of Banking Regulations and Regulatory Reform |

83 | |||||

| Stock Market Conditions |

85 | |||||

| Adjustments Conclusion |

92 | |||||

| Valuation Approach |

92 | |||||

| Valuation Conclusion |

96 | |||||

| IV. |

APPENDIX – EXHIBITS | |||||

| I |

Background of Feldman Financial Advisors, Inc. |

I-1 | ||||

| II-1 |

Balance Sheets |

II-1 | ||||

| II-2 |

Income Statements |

II-2 | ||||

| II-3 |

Loan Portfolio Composition |

II-3 | ||||

| II-4 |

Net Lending Activity |

II-4 | ||||

| II-5 |

Cash and Investments Composition |

II-5 | ||||

| II-6 |

Deposit Account Composition |

II-6 | ||||

| II-7 |

Borrowed Funds Composition |

II-7 | ||||

| II-8 |

Office Properties |

II-8 | ||||

| III |

Financial and Market Data for All Public Thrifts |

III-1 | ||||

| IV-1 |

Pro Forma Assumptions for the Stock Offering |

IV-1 | ||||

| IV-2 |

Pro Forma Conversion Valuation Range |

IV-2 | ||||

| IV-3 |

Pro Forma Conversion Analysis at the Midpoint Value |

IV-3 | ||||

| IV-4 |

Comparative Valuation Ratio Analysis |

IV-4 | ||||

i

FELDMAN FINANCIAL ADVISORS, INC.

LIST OF TABLES

| TAB |

PAGE | |||||

| I. | CHAPTER ONE – BUSINESS OF TC FEDERAL BANK | |||||

| Table 1 | Selected Financial Condition Data | 12 | ||||

| Table 2 | Relative Balance Sheet Concentrations | 13 | ||||

| Table 3 | Income Statement Summary | 25 | ||||

| Table 4 | Income Statement Ratios | 26 | ||||

| Table 5 | Yield and Cost Summary | 27 | ||||

| Table 6 | Net Interest Income Sensitivity | 34 | ||||

| Table 7 | Economic Value of Equity | 35 | ||||

| Table 8 | Non-performing Asset Summary | 38 | ||||

| Table 9 | Allowance for Loan Losses | 39 | ||||

| Table 10 | Largest Employers in Thomas County, Georgia | 42 | ||||

| Table 11 | Largest Employers in Leon County, Florida | 44 | ||||

| Table 12 | Selected Demographic Data | 45 | ||||

| Table 13 | Total Employment Force | 47 | ||||

| Table 14 | Map of Office Network | 48 | ||||

| Table 15 | Branch Office Deposit Data | 49 | ||||

| Table 16 | Deposit Market Share in Thomas County and Leon County | 51 | ||||

| Table 17 | Residential Lending Share in Thomas County, Florida | 53 | ||||

| Table 18 | Residential Lending Share in Leon County, Florida | 54 | ||||

| Table 19 | Residential Lending Share in Chatham County, Georgia | 55 | ||||

| II. | CHAPTER TWO – COMPARISONS WITH PUBLICLY TRADED COMPANIES | |||||

| Table 20 | Comparative Group Operating Summary | 62 | ||||

| Table 21 | Key Financial Comparisons | 64 | ||||

| Table 22 | General Operating Characteristics | 70 | ||||

| Table 23 | Summary Financial Performance Ratios | 71 | ||||

| Table 24 | Income and Expense Analysis | 72 | ||||

| Table 25 | Balance Sheet Composition | 73 | ||||

| Table 26 | Growth Rates, Credit Risk, and Loan Composition | 74 | ||||

| III. | CHAPTER THREE – MARKET VALUE ADJUSTMENTS | |||||

| Table 27 | Selected Demographic Data of Primary Market Areas | 79 | ||||

| Table 28 | Summary of Recent Georgia and Florida Acquisition Activity | 84 | ||||

| Table 29 | Comparative One-Year Stock Index Performance | 88 | ||||

| Table 30 | Comparative Three-Year Stock Index Performance | 89 | ||||

| Table 31 | Summary of Standard Conversion Stock Offerings | 90 | ||||

| Table 32 | Comparative Pro Forma Market Valuation Analysis | 97 | ||||

ii

FELDMAN FINANCIAL ADVISORS, INC.

INTRODUCTION

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated pro forma market value of TC Federal Bank (the “Bank”) as of February 26, 2021 in conjunction with the Bank’s conversion (the “Conversion”) from the mutual to stock form of organization, issuance of all of its capital stock to a newly formed stock holding company known as TC Bancshares, Inc. (“TC Bancshares” or the “Company”), and offering for sale of the Company’s common stock to eligible depositors and borrowers of the Bank, the Bank’s employee stock ownership plan (“ESOP”), and certain members of the general public in a subscription and community offering (the “Stock Offering”). The Appraisal is furnished pursuant to the filing by the Bank of applications with respect to the Conversion and the Stock Offering with the Office of the Comptroller of the Currency (“OCC”), the Board of Governors of the Federal Reserve System (“Federal Reserve Board”), and the Georgia Department of Banking and Finance.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and advisory firm that specializes in financial valuations and analyses of business enterprises and securities in the thrift, banking, and mortgage industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of the Bank that included discussions with the Bank’s management, the Bank’s legal counsel, Bryan Cave Leighton Paisner LLP, and the Bank’s independent registered public accounting firm, Wipfli, LLP. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

We also reviewed, among other factors, the economy in the Bank’s primary market area and compared the Bank’s financial condition and operating performance with that of selected

1

FELDMAN FINANCIAL ADVISORS, INC.

publicly traded thrift institutions. We reviewed conditions in the securities markets in general and in the market for thrift institution common stocks in particular.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because the Appraisal is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Bank’s pro forma market value. Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws, and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The Valuation Range reported herein will be updated as appropriate. These updates will consider, among other factors, any developments or changes in the Bank’s operating performance, financial condition, or management policies, and current conditions in the securities markets for thrift institution common stocks. Should any such new developments or changes be material, in our opinion, to the valuation of the Bank, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in detail at that time.

2

FELDMAN FINANCIAL ADVISORS, INC.

I. BUSINESS OF TC FEDERAL BANK

General Overview

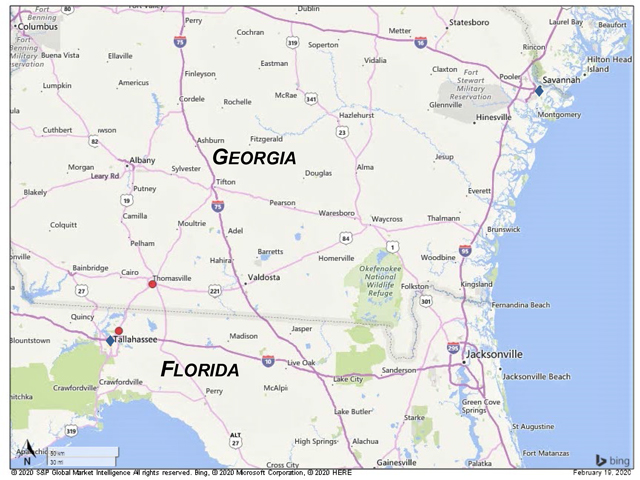

TC Federal Bank is a federally chartered mutual savings bank headquartered in Thomasville, Georgia. Thomas County Federal Savings & Loan Association was organized in 1934 and chartered in 1937 by the Federal Home Loan Bank Board as a mutual savings and loan association. Effective January 1, 2018, the Bank amended its corporate name to TC Federal Bank. The Bank conducts its business from its main office in Thomasville, Georgia, a branch office and a residential mortgage center in Tallahassee, Florida, and a commercial loan production office (“LPO”) in Savannah, Georgia. The Bank’s primary market area consists of Thomas County, Georgia and Leon County, Florida, and the surrounding counties.

The Bank’s business consists primarily of taking deposits from the general public and investing those deposits, together with funds generated from operations, in one- to four-family residential real estate loans, commercial and multi-family real estate loans, commercial business loans, construction and land loans, and consumer loans. The Bank expects to continue to focus on originating commercial real estate loans, commercial business loans, and construction loans. The Bank also invests in securities, which have historically consisted primarily of mortgage-backed securities issued by U.S. government-sponsored enterprises. In recent years, the Bank has originated single-family owner-occupied loans for sale into the secondary market and for its own portfolio. The Bank intends to continue this activity in the future in order to generate fee income. The Bank offers a variety of deposit accounts, including checking accounts, savings accounts, money market accounts, and certificates of deposit.

At December 31, 2020, the Bank had total assets of $349.9 million, total deposits of $294.1 million, and total equity of $39.9 million (measuring 11.39% of assets). The Bank reported net

3

FELDMAN FINANCIAL ADVISORS, INC.

income of approximately $308,000 for the year ended December 31, 2020. The Bank’s deposits are insured up to applicable limits by the Federal Deposit Insurance Corporation (“FDIC”). The Bank is subject to regulation, examination, and supervision primarily by the OCC and secondarily by the FDIC. The Bank is also a member of the Federal Home Loan Bank (“FHLB”) of Atlanta.

Historically, the Bank operated as a residential lender with a focus on managing growth and increasing its capital while relying heavily on certificate accounts as a funding source. At December 31, 1999, the Bank had total assets of $229.3 million and total equity of $29.1 million (12.70% of total assets), with residential mortgages composing approximately 72% of total loans. In the succeeding years, the Bank began to place more emphasis on diversifying its loan portfolio and increasing levels of commercial real estate, construction and development, and commercial business loans outstanding. By December 31, 2009, the Bank’s assets had expanded to $316.5 million, and its total equity had increased to $50.2 million (15.85% of total assets).

However, similar to many banks and thrifts operating in Georgia and Florida during the financial crisis (and other regions of the country as well), the Bank suffered a series of operating losses from 2010 to 2015 as a result of deteriorating asset quality. In an effort to protect its capital ratios, the Bank constricted its asset growth and turned its operating focus intently to resolving problem assets. Subsequently, its total assets declined to $246.4 million and total equity decreased to $29.9 million (12.14% of total assets) as of December 31, 2015. Following this period, the Bank’s asset quality stabilized and its capital erosion abated. Subsequently, the Bank returned to a position of expanding its balance sheet and pursuing selective growth opportunities.

In September 2017, TC Federal Bank opened a branch office in Tallahassee (Leon County), Florida. Leon County is adjacent to Thomas County and had long been a key lending market for the Bank. For several years prior to opening the branch office in Tallahassee, the Bank had

4

FELDMAN FINANCIAL ADVISORS, INC.

operated a loan office in the area. In an effort to enhance business development activity in the Tallahassee market and add depth to the management team, the Bank appointed Matt Brown as Tallahassee Market President in 2017. Mr. Brown has over 40 years of experience in serving financial institutions, including more than 20 years of executive officer leadership service to depository institutions. Also, during 2017, the Bank opened an LPO in Savannah, Georgia, where members of the management team had prior lending experience and the Bank recruited a commercial lender to serve that market specifically.

The Bank began to undertake an intensive review and analysis of its core operations in 2017, including efforts to improve profitability, enhance operating efficiency, revamp residential mortgage lending, upgrade its overall infrastructure, strengthen managerial proficiency, and reposition the Bank to serve broader customer segments of its market area. A rebranding of the Bank was considered necessary to facilitate geographic expansion beyond Thomas County into South Georgia and North Florida, and to reinforce marketing of the Bank’s product offerings beyond the traditional savings and loan model. The rebranding and name change to TC Federal Bank occurred during the first quarter of 2018.

TC Federal Bank has devoted considerable attention to improving the breadth and depth of its managerial team. In June 2018, the then-existing President and Chief Executive Officer (“CEO”) of the Bank resigned. In July 2018, Mr. Brown was promoted from Tallahassee Market President to serve as CEO of the Bank. Subsequently, Greg Eiford was named President and Senior Lending Officer of the Bank in August 2019, having served previously as Executive Vice President and Thomasville Market President since 2017 and Senior Lender since 2010. In December 2020, Mr. Brown retired from the Bank and Mr. Eiford assumed the additional position of CEO. Mr. Eiford has been employed with TC Federal Bank since October 2008 and has been

5

FELDMAN FINANCIAL ADVISORS, INC.

instrumental in managing numerous projects related to the Bank’s transition to a community bank platform. Linda Palmer was appointed Executive Vice President and Chief Financial Officer (“CFO”) of the Bank in May 2019. She previously served in a variety of leadership positions in community banks in her nearly 30-year career in community banking. Noel Ellis was named Executive Vice President and Chief Credit Officer in August 2016 and has served in the credit function at financial institutions for over 30 years. After beginning his career at the Bank in 2012 as a commercial lender and helping to establish the Tallahassee loan office, Nat Higdon was promoted to Tallahassee Market President in 2018. In January 2021, Mr. Higdon assumed the position of Executive Vice President and Senior Lending Officer.

The Bank has progressed significantly in recovering from its asset quality challenges of the prior decade. Its ratio of non-performing assets (excluding restructured loans) declined from 6.37% at December 31, 2014 to 0.59% at December 31, 2020. The Bank returned to profitable operations in 2015; however, the Bank’s core earnings have significantly lagged the industry’s level of profitability. In 2017 and 2018, the Bank benefited from income tax adjustments and the reversal of loan loss provisions to elevate reported earnings. The Bank’s historical operating focus on certificate accounts with limited transaction deposits contributed previously to its below-average net interest margin and below-average non-interest income levels. The Bank’s high efficiency ratio is reflective of its levels of above-average non-interest expense and below-average non-interest income.

In recent years, the Board of Directors (the “Board”) and senior management of TC Federal Bank have undertaken a thorough review of the Bank’s operations to identify opportunities for meaningful profit-improvement. In conjunction with revamping the senior management team, the Bank also utilized outside consultants to conduct an in-depth assessment of the Bank and

6

FELDMAN FINANCIAL ADVISORS, INC.

recommend a plan for earnings improvement and operating efficiency. The overall process was driven by the goal of transforming the Bank from a narrowly-focused thrift institution to a community banking organization capable of serving its markets in ways that would improve earnings and build loyalty with increased attention paid to retail banking, small businesses, and professionals.

Among the major initiatives that have been implemented in connection with the profit-improvement plan are (1) introducing a checking account marketing program to increase demand deposit accounts, fee income, and customer loyalty; (2) revamping residential mortgage lending and implementing a new loan origination software; (3) freezing the Bank’s pension plan and modifying certain other employee benefit and incentive plans; (4) outsourcing certain audit functions; (5) expanding lending activity through Small Business Administration (“SBA”) and U.S. Department of Agriculture (“USDA”) programs; (6) ensuring processes, policies, and procedures are in line with best practices, and (7) implementing plans to undertake a core system conversion from an outdated thrift system to a new and proven data processing platform that supports community banks. The core system conversion was completed in October 2020 and entailed a non-recurring expense of $1.1 million that impacted earnings for the year ended December 31, 2020.

The Bank believes that its community orientation is attractive to customers and distinguishes it from the larger banks that operate in the local market area. The Bank continues to stress high quality, personal customer service through an honest, straightforward, and upfront marketing approach and has developed a loyal customer base. The Bank relies on its experienced and committed staff to meet the needs of customers and effectively deliver banking products and services.

7

FELDMAN FINANCIAL ADVISORS, INC.

Going forward, the Bank’s operating goal is to provide long-term value to its stockholders, customers, employees, and the communities it serves by executing a prudent business strategy that produces increasing profitability. The Bank believes there is a significant opportunity for a community-focused bank to compete effectively in its primary market areas and that the increased capital it will have after the completion of the Stock Offering will facilitate this objective. The core elements of the Bank’s business strategy are outlined in more detail below:

| ● | Leverage the infrastructure of the Bank to create additional value for depositors, employees, customers, and the communities in which the Bank operates. The Bank seeks to improve its operating efficiency as it optimizes a new core processing system that was implemented in 2020 in order to enhance service features for both retail and business customers, and continue the process improvements implemented over the last two years. The Bank’s efficiency ratio improved from 100.8% in 2017 to 95.2% for 2018 and 85.9% for 2019, before regressing slightly to 91.2% in 2020 due to costs associated with the new core processing system. Based on the personnel and systems now in place, the Bank believes it can continue to improve its operational efficiency, particularly as it is able to utilize the capital raised in the Stock Offering and increase revenue. The Bank foresees the potential opportunity to add both an additional branch in Tallahassee, Florida and to expand its presence in the Savannah, Georgia market. |

| ● | Grow the loan portfolio prudently. The Bank intends to continue to maintain a diversified portfolio of loans, with an emphasis on commercial and multi-family real estate loans and residential mortgage loans. The capital raised in the Stock Offering will provide additional support for continued loan growth throughout the Bank’s market areas. The Bank also intends to seek to expand its commercial lending activities through government-sponsored loan programs, such as the SBA and USDA loan programs. Through its residential mortgage office in Tallahassee, the Bank will continue to seek to originate residential loans for its portfolio as well as for sale in the secondary market, using multiple correspondent relationships for the sale of residential mortgages on a servicing-released basis. |

| ● | Continue to increase core deposits. The Bank seeks to increase the proportion of the deposit base consisting of core deposits (non-certificate accounts) in order to provide a stable source of funds to support loan growth, at costs consistent with improving its net interest rate spread and margin. Historically, the Bank relied heavily on certificates of deposit, but recently has stressed the importance of building its core deposit base. As part of its focus on commercial loan growth, the Bank’s lenders are expected to source business checking accounts from borrowers. The Bank has begun reducing deposit costs to market |

8

FELDMAN FINANCIAL ADVISORS, INC.

| rates and placing greater emphasis on core deposits. As a result of these efforts and recognizing the impact of U.S. Government stimulus programs injecting liquidity and credit flow into the economy, core deposits increased by $42.3 million or 25.6% to $207.5 million at year-end 2020 from $165.2 million at year-end 2019. The Bank recently redesigned its checking account products and the related marketing program. Management will continue to emphasize the growth of both retail and commercial core deposits. |

| ● | Maintain credit standards while growing the balance sheet. The Bank believes strong asset quality is a critical key to its long-term financial success. The Bank’s strategy for credit risk management focuses on having an experienced team of credit professionals, well-defined policies and procedures, prudent loan underwriting criteria, and active credit monitoring. The Bank’s non-performing assets to total assets ratio was 0.59% at year-end 2020, 0.92% at year-end 2019, and 0.55% at year-end 2018. In anticipation of further growth, including as a result of the deployment of the capital raised in the Stock Offering, the Bank has invested in the enhancement of its credit function with experienced credit staff, upgraded internal and external credit review processes, and implemented new technology for underwriting processing and credit analysis. The Bank intends to maintain the high value of its credit culture, both in personnel as well as ancillary support systems, in order to be able to evaluate more complex loans and better manage credit risk, which will also support its intended loan growth, especially in the commercial loan market. |

| ● | Supplement organic growth through opportunistic bank or branch acquisitions. The Bank expects to consider acquisition opportunities that it believes would enhance the value of its franchise and yield potential financial benefits for its stockholders. The additional capital from the Stock Offering will provide the Bank the opportunity to acquire other institutions and financial services businesses located within reasonable proximity of its current market areas. The Bank believes that it is well positioned to take advantage of, and execute on, opportunities given the infrastructural improvements it has undertaken, including the upgrade of its core processing system and expanded management expertise. |

| ● | Enhance the sales, marketing, and service culture of the Bank. The Bank believes that loyalty is a key component of the success of community banks and intends to continue developing loyalty within its communities and from its customers. The Bank has emphasized creating a culture of accountability for its employee staff members, eliminating outdated and inefficient processes, raising employee capacity, expediting customer responsiveness, increasing customer retention and deposits, and enhancing fee income. The Bank believes that the new core processing system will allow it to improve the customer experience significantly and facilitate greater cross-selling opportunities. During 2021 and beyond, the Bank will continue to optimize the system for greater internal efficiencies and customer interactions and expand its digital banking capabilities. |

9

FELDMAN FINANCIAL ADVISORS, INC.

| ● | Expand the employee base to support future growth. The additional capital from the Stock Offering will provide the Bank with the ability to expand its employee base opportunistically. The Bank intends to continue to build depth and expertise as needed with increases in the Bank’s asset size and complexity. The potential to offer equity awards in the future following the Stock Offering will also allow the Bank to be more competitive when hiring and retaining experienced banking personnel. |

While its equity level is solid at 11.39% of total assets as of December 31, 2020, the Bank believes it must raise additional capital in order to facilitate its growth objectives and loan generation activity, and provide a greater cushion in response to the risk profile associated with continued expansion and future economic conditions. Over the past three years, the Bank’s total equity increased from $37.6 million at year-end 2017 to $39.9 million at year-end 2020. However, the ratio of total equity to assets declined from 13.76% at year-end 2017 to 11.39% at year-end 2020 as the Bank’s asset growth outpaced its capital formation, which in the Bank’s current mutual form of ownership is reliant primarily upon earnings generation. As a stock organization upon completion of the Conversion, the Bank will be organized in the ownership form used by commercial banks, most major businesses, and a large number of thrift institutions. The ability to raise new equity capital through the issuance and sale of capital stock will allow the Bank the flexibility to increase its equity capital position more rapidly than by accumulating earnings.

The Bank also believes that the ability to attract new capital also will help address the needs of the communities it serves and enhance its ability to expand or to make acquisitions. After the Conversion, the Bank will have an increased ability to merge with or acquire other financial institutions or business enterprises; however, there are no current arrangements, understandings, or agreements regarding any such acquisition opportunities. Finally, the Bank expects to benefit from its employees and directors having stock ownership in its business, since that is viewed as an

10

FELDMAN FINANCIAL ADVISORS, INC.

effective performance incentive and a means of attracting, retaining, and compensating employees and directors.

In summary, the Bank’s primary reasons for implementing the Conversion and undertaking the Stock Offering are to:

| ● | Increase the capital base to support future growth and profitability, although the Bank currently has capital well in excess of all applicable regulatory requirements. |

| ● | Compete more effectively in the financial services marketplace. |

| ● | Offer the Bank’s depositors, employees, management, and directors an equity ownership interest in TC Bancshares, the proposed stock holding company, and thereby an economic interest in the potential future success of the Bank and TC Bancshares. |

| ● | Attract and retain qualified personnel by establishing stock-based benefit plans. |

| ● | Increase the Bank’s flexibility to structure and finance the expansion of its operations, including potential acquisitions of other financial service businesses and establishing de novo branches or new loan production offices. |

The remainder of Chapter I examines in more detail the trends addressed in this section, including the impact of changes in TC Federal Bank’s economic and competitive environment, and recent strategic initiatives. The discussion is supplemented by the exhibits in the Appendix. Exhibit II-1 summarizes the Bank’s audited balance sheets as of December 31, 2018 to 2020. Exhibit II-2 presents the Bank’s audited income statements for the years ended December 31, 2018 to 2020.

11

FELDMAN FINANCIAL ADVISORS, INC.

Financial Condition

Table 1 presents selected data concerning the Bank’s financial position as of December 31, 2017 to 2020. Table 2 displays relative balance sheet concentrations as of similar year-end dates.

Table 1

Selected Financial Condition Data

As of December 31, 2017 to 2020

(Dollars in Thousands)

| December 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | |||||||||||||

| Total assets |

$ | 349,927 | $ | 321,762 | $ | 297,181 | $ | 273,412 | ||||||||

| Cash and cash equivalents (1) |

47,528 | 33,036 | 25,127 | 32,827 | ||||||||||||

| Investment securities available-for-sale |

15,917 | 22,107 | 27,114 | 21,500 | ||||||||||||

| Federal Home Loan Bank stock |

714 | 400 | 379 | 456 | ||||||||||||

| Total loans, net (2) |

265,301 | 246,399 | 235,321 | 210,109 | ||||||||||||

| Premises and equipment, net |

3,444 | 3,339 | 3,485 | 2,621 | ||||||||||||

| Bank-owned life insurance |

10,883 | 10,583 | - | - | ||||||||||||

| Total deposits |

294,100 | 273,604 | 250,348 | 224,096 | ||||||||||||

| Federal Home Loan Bank advances |

9,515 | 2,825 | 2,992 | 5,510 | ||||||||||||

|

Total equity |

39,858 | 39,788 | 38,019 | 37,609 | ||||||||||||

| (1) | Includes federal funds sold and certificates of deposit with other banks. |

| (2) | Includes mortgage loans held for sale. |

Source: TC Federal Bank, financial statements.

Asset Composition

The Bank’s total assets amounted to $349.9 million at December 31, 2020, reflecting an 8.8% or $28.1 million increase from total assets of $321.8 million at December 31, 2019. In the prior year, the Bank’s total assets increased by 8.3% or $24.6 million from $297.2 million at December 31, 2018 to $321.8 million at December 31, 2019. The recent expansion of total assets was primarily attributable to increases in the holdings of loans, cash and cash equivalents, and bank-owned life insurance (“BOLI”).

12

FELDMAN FINANCIAL ADVISORS, INC.

Table 2

Relative Balance Sheet Concentrations

As of December 31, 2017 to 2020

(Percent of Total Assets)

| December 31, | ||||||||||||||||||||||||||

| 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||

| Cash and cash equivalents (1) |

13.58 | % | 10.27 | % | 8.46 | % | 12.01 | % | ||||||||||||||||||

| Investment securities available-for-sale |

4.55 | 6.87 | 9.12 | 7.86 | ||||||||||||||||||||||

| Federal Home Loan Bank stock |

0.20 | 0.12 | 0.13 | 0.17 | ||||||||||||||||||||||

| Total loans, net (2) |

75.82 | 76.58 | 79.18 | 76.85 | ||||||||||||||||||||||

| Premises and equipment, net |

0.98 | 1.04 | 1.17 | 0.96 | ||||||||||||||||||||||

| Bank-owned life insurance |

3.11 | 3.29 | - | - | ||||||||||||||||||||||

| Other assets |

1.75 | 1.83 | 1.94 | 2.16 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total assets |

100.00 | % | 100.00 | % | 100.00 | % | 100.00 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total deposits |

84.05 | % | 85.03 | % | 84.24 | % | 81.96 | % | ||||||||||||||||||

| Federal Home Loan Bank advances |

2.72 | 0.88 | 1.01 | 2.02 | ||||||||||||||||||||||

| Other liabilities |

1.84 | 1.72 | 1.96 | 2.27 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total liabilities |

88.61 | 87.63 | 87.21 | 86.24 | ||||||||||||||||||||||

| Total equity |

11.39 | 12.37 | 12.79 | 13.76 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total liabilities and equity |

100.00 | % | 100.00 | % | 100.00 | % | 100.00 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

||||||||||||||||||||||||||

| (1) | Includes federal funds sold and certificates of deposit with other banks. |

| (2) | Includes mortgage loans held for sale. |

Source: TC Federal Bank, financial statements.

Net total loans (including loans held for sale) increased by 7.7% or $18.9 million from $246.4 million at year-end 2019 to $265.3 million at year-end 2020, spurred mainly by commercial business loans increasing $20.4 million from $9.2 million at year-end 2019 to $29.6 million at year-end 2020. In March 2020, Congress passed the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) to provide economic relief for the country, including the Small Business Administration (“SBA”) Paycheck Protection Program (“PPP”) to fund short-term loans for small businesses. The Bank experienced significant growth in commercial business loans in 2020 due to the origination of $25.1 million in PPP loans. The Bank had $17.9 million of PPP

13

FELDMAN FINANCIAL ADVISORS, INC.

loans outstanding as of December 31, 2020. PPP loans originated by the Bank in 2020 generally have a term of two years or five years and earn interest at 1.0% plus fees. PPP loans are expected to primarily be repaid via forgiveness provisions (under the CARES Act) from the SBA. These loans are fully guaranteed as to principal and interest by the SBA.

The balance sheet value of BOLI increased from zero at year-end 2018 to $10.6 million at December 31, 2019 and $10.9 million at December 31, 2020. In connection with adopting Supplemental Executive Retirement Plans (“SERPs”) for certain of its officers as a result of freezing the pension plan, the Bank purchased single-premium BOLI during 2019 to fund the benefit obligations created by the SERPs. The cash surrender value of these policies was $10.9 million as of December 31, 2020.

Largely as a result of the increase in and cash and cash equivalents and BOLI, the ratio of net total loans to total assets declined from 79.2% at December 31, 2018 to 75.8% at December 31, 2020. Cash and cash equivalents increased from $25.1 million at December 31, 2018 to $47.5 million at December 31, 2020, reflecting a buildup of liquidity from deposit inflows. Total deposits increased from $250.3 million at December 31, 2018 to $294.1 million at December 31, 2020, largely as a result of the Bank emphasizing core deposit growth. In addition, core deposits were elevated by PPP loan funds and other stimulus liquidity deposited into customer accounts. Total deposits increased by 9.3% or $23.3 million from $250.3 million at year-end 2018 to $273.6 million at year-end 2019, and then increased by 7.5% or $17.5 million to $294.1 million at year-end 2020. The Bank’s ratio of net total loans to total deposits decreased from 94.0% at December 31, 2018 to 90.2% at December 31, 2020.

Lending is the principal business activity of the Bank, and its loan portfolio constitutes the largest portion of its assets and is the predominant source of its income. The largest segment of

14

FELDMAN FINANCIAL ADVISORS, INC.

the Bank’s loan portfolio comprises real estate mortgage loans, consisting primarily of residential mortgage loans, commercial real estate and multi-family mortgage loans, and construction and land development loans. The Bank’s collateralized real estate loans are overwhelmingly secured by properties located in the Bank’s primary lending markets and other nearby areas.

The Bank’s primary lending market is Thomas County, Georgia, and the adjacent Georgia counties of Grady, Colquitt, Brooks, and Mitchell. In Florida, the Bank’s primary market area includes Leon County and the adjacent Florida counties of Gadsden, Wakulla, Jefferson, and Liberty. The Bank’s lending market also includes Chatham County, Georgia, where it operates an LPO in Savannah, and the adjacent Georgia counties of Liberty, Bryan, and Effingham along with the Hilton Head Island-Bluffton-Beaufort metropolitan area in South Carolina.

As presented in Exhibit II-3, the Bank’s current loan portfolio is composed mainly of real estate loans. At December 31, 2020, real estate loans comprised $232.6 million or 86.9% of the gross loan portfolio and consisted of residential loans (including one- to four-family mortgages and home equity lines of credit) and non-residential real estate loans (comprising loans secured by commercial and multi-family real estate and construction and land development loans). Non-real estate loans chiefly comprised commercial business loans and a limited amount of consumer loans. Along with residential lending, the Bank intends to continue to emphasize commercial real estate, commercial business, and construction lending in an effort to diversify its overall loan portfolio, increase the overall yield earned on loans, and assist in managing interest rate risk.

Exhibit II-4 details the Bank’s recent lending activity for its own portfolio. For the year ended December 31, 2020, the Bank originated $86.0 million of loans for portfolio, including $29.8 million of commercial business loans, $21.3 million of residential mortgages, and $19.7 million of commercial and multi-family real estate loans. For the year ended December 31, 2019,

15

FELDMAN FINANCIAL ADVISORS, INC.

the Bank originated $51.9 million of loans, including $17.6 million of commercial and multi-family real estate loans, $16.6 million of residential mortgages, and $11.0 million of construction and land loans. In addition to orginating loans for its own portfolio, the Bank also originates loan for sale to generate fee income. During 2020, the Bank sold $65.6 million of residential mortgage loans, all on a servicing-released basis, and generated $1.2 million in gains on sale of loans. This level of mortgage banking activity reflected an increase from $20.7 million of residential mortgage loan sales in 2019, which resulted in $380,000 in gains on sale of loans.

At December 31, 2020, the Bank had $105.8 million in residential mortgage loans, which represented 39.6% of total loans. Of the $105.8 million, $39.0 million consisted of non-owner occupied mortgage loans with the remaining $66.8 million in owner-occupied loans. Residential loans decreased by 3.4% or $3.8 million in 2020 after decreasing by 5.2% or $6.0 million in 2019. As noted above, the Bank has also originated single-family, owner-occupied residential loans for sale in the secondary market and it intends to continue this activity to generate fee income. Adjustable-rate loans comprise a majority of the residential mortgage loans in portfolio. Currently, the Bank generally only originates fixed-rate, owner-occupied residential mortgages for sale into the secondary market. The Bank’s residential real estate loans typically have terms of up to 30 years and are generally underwritten pursuant to Fannie Mae documentation guidelines.

The Bank generally limits the loan-to-value (“LTV”) ratios of its residential mortgage loans to 85% of the purchase price or appraised value, whichever is lower. In addition, the Bank occasionally makes residential mortgage loans with LTV ratios in excess of 85% of the purchase price or appraised value, whichever is less, if the borrower obtains private mortgage insurance. The Bank’s adjustable-rate residential mortgage loans typically have fixed interest rate periods for five to ten years and then adjust annually with amortization terms of up to 30 years. The Bank

16

FELDMAN FINANCIAL ADVISORS, INC.

does not offer “interest only” mortgage loans on permanent residential mortgage loans, and also does not offer residential mortgage loans that provide for negative amortization of principal or contain any other subprime loan characteristics.

At December 31, 2020, the Bank had $87.9 million in commercial real estate and multi-family real estate loans, which represented 32.8% of its total loan portfolio. Of this aggregate total, the Bank’s commercial real estate loans amounted to $72.7 million and multi-family real estate loans amounted to $15.1 million at year-end 2020. The Bank’s commercial real estate lending activity is consistent with its strategy to diversify the loan portfolio and increase the overall portfolio yield. The Bank’s commercial real estate loans are secured by a variety of properties in the Bank’s market areas, including office buildings, farms, retail and mixed-use properties, churches, warehouses, and restaurants. The Bank’s multi-family real estate loans are secured by apartment buildings, mobile home parks, and other multi-family properties. The Bank’s commercial real estate loans are generally originated as balloon loans with an initial term of five to seven years and a 20-year amortization period, although the Bank does originate loans that fully amortize over 20 years with certain financial covenants. The maximum LTV ratio of the Bank’s commercial real estate loans is generally 80%.

The Bank’s commercial real estate loans (including multi-family loans) increased from $71.0 million (33.2% of gross total loans) at year-end 2017 to $90.4 million (37.9%) at year-end 2018 and $95.2 million (38.3%) at year-end 2019, before decreasing to $87.9 million (32.8%) at year-end 2020. Four years ago, the Bank initiated a policy to manage concentration risk, whereas it would limit its total exposure to a single parcel of collateral property to $3.0 million and its aggregate debt exposure to related entities to $5.0 million. The Bank has a few legacy loans outstanding that exceed these current limits, and one loan has been originated that exceeded the

17

FELDMAN FINANCIAL ADVISORS, INC.

limit to an individual property since implementation of the current policy. This loan is an SBA loan that carries an LTV ratio of less than 55%.

At December 31, 2020, the Bank had $30.0 million in construction and land development loans, which represented 11.2% of its overall loan portfolio, and included $5.0 million in land loans. Construction and development loans increased from $18.2 million at year-end 2018 to $23.4 million at year-end 2019 and $30.0 million at year-end 2020. These loans consist primarily of loans to individuals for the construction of their primary or secondary residences or commercial structures, as well as loans to contractors and builders of single-family homes. The Bank also makes a limited amount of land loans to complement its construction lending activities, as such loans are generally secured by lots that will be used for residential development. The Bank also originates construction loans for commercial development projects, including retail buildings, churches, small industrial facilities, hotels, and office buildings. Most of the Bank’s construction loans are interest-only loans that provide for the payment of interest during the construction phase, which is usually up to 12 months. At the end of the construction phase, the loan may convert to a permanent mortgage loan or the loan may be repaid in full.

At December 31, 2020, the Bank had $29.6 million in commercial business loans, which represented 11.1% of its total loan portfolio. Commercial business loans outstanding have increased from $2.3 million, $3.7 million, $7.7 million, $7.5 million, and $9.2 million at year-end 2015, 2016, 2017, 2018, and 2019, respectively. The Bank’s commercial business loans include loans to a variety of professionals, sole proprietorships, and small businesses operating in the Bank’s market area. As noted previously, the expansion of the commercial business loan portfolio in 2020 was driven by the origination of PPP loans. The Bank originated $25.1 million of PPP loans during 2020 and had $17.9 million of PPP loans outstanding as of December 31, 2020.

18

FELDMAN FINANCIAL ADVISORS, INC.

As part of its relationship-driven focus, the Bank encourages its commercial borrowers to maintain their primary deposit accounts with the Bank, which helps to improve the Bank’s overall interest rate spread. The Bank’s commercial business loans include term loans and revolving lines of credit and are made with either adjustable or fixed rates of interest. Adjustable interest rates are based on the prime rate or the U.S Treasury constant maturity rate, plus a margin. Commercial business loans are generally secured by business assets of the respective borrowers, and the bank may support this collateral with junior liens on real property. Depending on the collateral used to secure the loans, commercial business loans are made in amounts of up to 75% of the collateral securing the loans.

The Bank had $8.9 million of home equity loans and lines of credit as of December 31, 2020, representing 3.3% of total loans. The Bank offers home equity loans and lines of credit, which are multi-purpose loans used to finance various home or personal needs, where a primary or secondary residence serves as collateral. The Bank’s home equity lines of credit either feature a 10-year term with an interest-only option or a 15-year term that requires a principal payment of 1% of the outstanding balance plus interest. These loans are limited mainly to being collateralized by borrowers’ personal primary residences and to those customers who reside within the Bank’s primary market area with acceptable credit ratings. These loans can be secured either by a first or second lien position. Home equity lines of credit are tied to the prime rate. A conversion option allows for the borrower to convert to a fixed-rate, fully amortizing loan with a 10-year term.

At December 31, 2020, the Bank’s consumer loans amounted to $5.4 million, representing 2.0% of total loans. The Bank offers a limited range of consumer loans, principally to customers residing in its primary market areas who maintain other relationships with the Bank and have

19

FELDMAN FINANCIAL ADVISORS, INC.

acceptable credit ratings. The Bank’s consumer loans generally consist of loans secured by deposit accounts, loans on new and used automobiles, and unsecured personal loans.

Exhibit II-5 presents a summary of the Bank’s portfolio of cash, liquidity, and investments as of December 31, 2018 to 2020. The Bank’s primary investment objectives include the following: (1) provide and maintain liquidity to meet deposit withdrawal and loan funding needs; (2) help mitigate interest rate and market risk; (3) diversify the Bank’s assets; (4) provide collateral for pledging requirements, and (5) generate a reasonable rate of return on funds within the context of the Bank’s interest rate and credit risk objectives.

The Bank’s Board of Directors is responsible for adopting and reviewing annually the investment policy of TC Federal Bank. The Bank’s Asset/Liability Management Committee (“ALCO”) is responsible for implementing the Bank’s investment policy. The Bank’s ALCO consists of the President/CEO, CFO, Chief Credit Officer, members of the Board, and other members of senior management. The Bank’s CFO, or designee as approved by the ALCO, acts as the Bank’s investment manager and is responsible for executing portfolio strategy as set by the ALCO. All of the Bank’s investment securities are currently classified as available-for-sale.

The Bank implemented a securities portfolio restructuring during 2019 in an effort to improve investment returns across changing interest rate cycles. The Bank had sales of investment securities for total proceeds of approximately $10.9 million, resulting in gains on sale of $67,000. Collateralized mortgage obligations were added to the investment portfolio in 2019 and amounted to $9.7 million at year-end 2019 and $9.1 million at year-end 2020.

At December 31, 2020, the Bank’s cash and investments amounted to $55.5 million or 17.3% of total assets. Cash and cash equivalents (including federal funds sold and certificates of deposit in other financial institutions) amounted to $47.5 million or 74.1% of the Bank’s total cash

20

FELDMAN FINANCIAL ADVISORS, INC.

and investments as of December 31, 2020. Cash and cash equivalents increased by $14.5 million from year-end 2019 to year-end 2020, largely resulting from the buildup of liquidity related to increased customer deposit inflows. The Bank’s available-for-sale securities portfolio totaled $15.9 million at December 31, 2020 and was composed of $15.4 million in U.S. Government-sponsored enterprises obligations (including residential mortgage-backed securities and collateralized mortgage obligations) and $501,000 in corporate debt obligations. The Bank’s available-for-sale investment securities portfolio had a weighted average yield of 1.70% at December 31, 2020. The Bank also owned $714,000 of stock in the FHLB of Atlanta as of December 31, 2020.

Liability Composition

Deposits are the Bank’s primary external source of funds for lending and other investment purposes. The Bank has also utilized borrowings to supplement deposits as a funding source. Exhibit II-6 presents a summary of the Bank’s deposit composition as of December 31, 2018 to 2020. Total deposits amounted to $294.1 million or 84.0% of total assets and 94.9% of total liabilities at December 31, 2020. Total deposits increased by 7.5% or $20.5 million from $273.6 million at December 31, 2019 to $294.1 million at December 31, 2020. Recent deposit growth has largely been concentrated in the Bank’s interest-bearing checking accounts and savings accounts. The Bank’s recent deposit expansion has been accelerated by the establishment of its Tallahassee branch office (which opened in September 2017), the emphasis on core deposit accounts, and the inflow of PPP loan proceeds and Government stimulus-related liquidity into customer accounts.

TC Federal Bank relies on personalized customer service, longstanding relationships with customers, and the favorable image of the Bank in its primary market area to attract and retain deposits. Deposit account terms vary according to the minimum balance required, the time period

21

FELDMAN FINANCIAL ADVISORS, INC.

that funds must remain on deposit, and the interest rate, among other factors. In determining the rates and terms of its deposit accounts, the Bank considers the rates offered by competitors, liquidity needs, growth objectives, current operating strategies, and customer preferences and concerns. The Bank’s deposit pricing strategy has generally been to offer competitive rates, while generally not providing the highest rates in the market.

The Bank has placed a concerted emphasis on attracting core (non-certificate) deposit accounts, which tend to represent lower cost and more stable funding sources. Core deposits composed 70.6% or $207.5 million of total deposits at December 31, 2020, which reflected an increase from 52.2% of total deposits or $106.0 million at December 31, 2015. In 2020, the Bank’s weighted average cost of interest-bearing core deposits was 0.48%, the weighted average cost of certificate accounts was 1.53%, and the overall weighted average cost of interest-bearing deposits was 0.80%, reflecting a decline from the corresponding overall cost of 1.16% in 2019.

As a member of the FHLB of Atlanta, the Bank may obtain FHLB borrowings based upon the security of FHLB capital stock owned and certain of the Bank’s real estate mortgage loans. The Bank uses FHLB advances to provide short-term or intermediate-term funding as a supplement to its deposits. As of December 31, 2020, the Bank had $9.5 million in FHLB advances outstanding, which amounted to 2.7% of total assets. The Bank had approximately $19.2 million in available borrowing capacity from the FHLB of Atlanta at December 31, 2020. The Bank could access additional advances if it purchased additional FHLB of Atlanta capital stock. The Bank also had available borrowing capacity through the Federal Reserve Bank of Atlanta and for overnight borrowing under unsecured federal funds lines of credit through correspondent banks. There were no outstanding borrowings against these credit facilities as of December 31, 2020.

22

FELDMAN FINANCIAL ADVISORS, INC.

Equity Capital

The Bank has historically maintained solid capital levels. The Bank’s total equity amounted to $39.9 million or 11.39% of total assets at December 31, 2020. The total equity to assets ratio decreased from 13.76% at December 31, 2017 to 11.39% at December 31, 2020 as the rate of asset expansion outpaced the rate of capital formation. Over the three-year period from December 31, 2017 to December 31, 2020, the Bank’s total equity increased at a compound annual growth rate of 1.3%, while its total assets increased by a compound annual growth rate of 8.5%.

The Bank’s equity capital increased by $70,000 or 0.2% from $39.8 million at year-end 2019 to $39.9 million at year-end 2020. Retained earnings of $308,000 added to the Bank’s equity for the year ended December 31, 2020. However, the Bank’s accumulated other comprehensive income (“AOCI”) declined by $238,000 during 2020. The Bank’s AOCI is affected mainly by unrealized gains or losses on available-for-sale securities and changes in post-retirement benefit obligations. The Bank’s equity increased by $331,000 due to increases in unrealized gains but was reduced by $569,000 due to changes in the funded status of post-retirement benefit obligations.

The Bank’s capital level remains strong in comparison to minimum regulatory requirements. The Bank’s regulatory capital ratios of tier 1 leverage capital, common equity tier 1 risk-based capital, tier 1 risk-based capital, and total risk-based capital were 11.73%, 16.47%, 16.47%, and 17.72%, respectively, as of December 31, 2019. In comparison, the minimum regulatory requirements under federal banking agency guidelines were 4.00%, 4.50%, 6.00%, and 8.00%, and the threshold requirements for regulatory “well capitalized” levels under prompt corrective action provisions were 5.00%, 6.50%, 8.00%, and 10.00%, respectively. Based on these regulatory capital ratios and requirements, the Bank was considered well capitalized for regulatory purposes as of December 31, 2020.

23

FELDMAN FINANCIAL ADVISORS, INC.

Income and Expense Trends

Table 3 displays the main components of the Bank’s earnings performance for the years ended December 31, 2018 to 2020. Table 4 displays the Bank’s principal income and expense ratios as a percent of average assets for the corresponding periods. Table 5 displays the Bank’s weighted average yields on interest-earning assets and weighted average costs of interest-bearing liabilities for the years ended December 31, 2018 to 2020.

General Overview

Over recent years, the Bank has exhibited a record of low to moderate profitability from core operations (excluding non-recurring items). The Bank’s net income amounted to $308,000 for 2020, $1.2 million for 2019, and $679,000 in 2018. The Bank reported a return on average assets (“ROA”) of 0.24%, 0.39%, and 0.09% for 2018, 2019, and 2020, respectively. The Bank reported a return on average equity (“ROE”) of 1.80%, 3.06%, and 0.76% for 2018, 2019, and 2020, respectively. The Bank’s profitability in 2020 was impacted by several non-recurring items, including data processing conversion costs and expenses associated with a delayed capital offering.

Compared to its asset size peer group of federally insured savings institutions, the Bank’s ROA of 0.24% in 2018 lagged the corresponding peer group average of 0.60% and its ROA of 0.39% in 2019 trailed the peer group average of 0.71%. Similarly, the Bank’s ROA of 0.09% in 2020 was below the peer group average of 0.66%. Compared to its regulatory peer group on a historical basis, the Bank’s profitability trends can be characterized by below-average non-interest income ratios and above-average non-interest expense ratios. However, the Bank’s net interest margin in 2020 at 3.38% exceeded the peer group average of 3.02%. While the peer group experienced a decline in its average net interest margin in recent years, the Bank has been able to reverse this trend by generating steady asset growth and increasing its core deposit base.

24

FELDMAN FINANCIAL ADVISORS, INC.

Table 3

Income Statement Summary

For the Years Ended December 31, 2018 to 2020

(Dollars in Thousands)

| Year Ended December 31, | |||||||||||||||

| 2020 | 2019 | 2018 | |||||||||||||

| Interest income |

$ | 13,088 | $ | 12,556 | $ | 11,374 | |||||||||

| Interest expense |

2,365 | 3,101 | 2,110 | ||||||||||||

|

|

|

|

|

|

|

||||||||||

| Net interest income |

10,723 | 9,455 | 9,264 | ||||||||||||

| Provision for (reduction in) loan losses |

780 | - | (551 | ) | |||||||||||

|

|

|

|

|

|

|

||||||||||

| Net interest income after provision |

9,943 | 9,455 | 9,815 | ||||||||||||

| Service charges on deposit account |

472 | 513 | 420 | ||||||||||||

| Gain on sale of mortgage loans |

1,236 | 380 | 187 | ||||||||||||

| Gain on sale of available-for-sale securities |

- | 67 | - | ||||||||||||

| Other income |

323 | 300 | - | ||||||||||||

|

|

|

|

|

|

|

||||||||||

| Total non-interest income |

2,031 | 1,260 | 607 | ||||||||||||

| Salaries and employee benefits |

6,444 | 5,327 | 5,499 | ||||||||||||

| Occupany equipment |

754 | 658 | 629 | ||||||||||||

| Other real estate owned expense, net |

(13 | ) | 11 | (4 | ) | ||||||||||

| Data processing conversion costs |

1,132 | - | - | ||||||||||||

| Expenses of delayed stock offering |

506 | - | - | ||||||||||||

| Other expense |

2,803 | 3,145 | 3,271 | ||||||||||||

|

|

|

|

|

|

|

||||||||||

| Total non-interest income |

11,626 | 9,141 | 9,395 | ||||||||||||

| Income before income taxes |

348 | 1,574 | 1,027 | ||||||||||||

| Income tax expense |

40 | 367 | 348 | ||||||||||||

|

|

|

|

|

|

|

||||||||||

| Net income |

$ | 308 | $ | 1,207 | $ | 679 | |||||||||

|

|

|

|

|

|

|

||||||||||

Source: TC Federal Bank, financial statements.

Years Ended December 31, 2019 and 2020

Net income declined to $308,000 in 2020 from $1.2 million in 2019, a decrease of $899,000 or 74.5%. The decrease was caused by increases of $2.5 million in non-interest expense and $780,000 in the loan loss provision, offset partially by increases of $1.3 million in net interest income and $771,000 in non-interest income. Net interest income increased from $9.5 million in 2019 to $10.7 million in 2020, due mainly to an increase in interest-earning assets in 2020 and an increase in the net interest spread from 3.07% in 2019 to 3.23% in 2020. The yield on interest-earning assets declined by 20 basis points from 4.32% in 2019 to 4.12% in 2020, while, the cost of interest-bearing liabilities declined by 36 basis points from 1.25% in 2019 to 0.89% in 2020.

25

FELDMAN FINANCIAL ADVISORS, INC.

Table 4

Income Statement Ratios

For the Years Ended December 31, 2018 to 2020

(Percent of Average Assets)

| Year Ended December 31, | ||||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||||

| Interest income |

3.90 | % | 4.11 | % | 4.01 | % | ||||||||||||

| Interest expense |

0.70 | 1.00 | 0.74 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Net interest income |

3.19 | 3.09 | 3.26 | |||||||||||||||

| Provision for (reduction in) loan losses |

0.23 | 0.00 | (0.19 | ) | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Net interest income after provision |

2.96 | 3.09 | 3.46 | |||||||||||||||

| Service charges on deposit account |

0.14 | 0.17 | 0.15 | |||||||||||||||

| Gain on sale of mortgage loans |

0.37 | 0.12 | 0.07 | |||||||||||||||

| Gain on sale of available-for-sale securities |

- | 0.02 | - | |||||||||||||||

| Other income |

0.10 | 0.10 | 0.00 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Total non-interest income |

0.60 | 0.41 | 0.21 | |||||||||||||||

| Salaries and employee benefits |

1.92 | 1.74 | 1.94 | |||||||||||||||

| Occupany equipment |

0.22 | 0.22 | 0.22 | |||||||||||||||

| Other real estate owned expense, net |

(0.00 | ) | 0.00 | (0.00 | ) | |||||||||||||

| Data processing conversion costs |

0.34 | - | - | |||||||||||||||

| Expenses of delayed stock offering |

0.15 | - | - | |||||||||||||||

| Other expense |

0.83 | 1.03 | 1.15 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Total non-interest income |

3.46 | 2.99 | 3.31 | |||||||||||||||

| Income before income taxes |

0.10 | 0.50 | 0.36 | |||||||||||||||

| Income tax expense |

0.01 | 0.12 | 0.12 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

| Net income |

0.09 | 0.39 | 0.24 | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||

Source: TC Federal Bank, financial statements; Feldman Financial calculations.

The provision for loan losses was increased from zero in 2019 to $780,000 for 2020. The Bank’s ratio of non-performing assets to total assets declined from 0.92% at December 31, 2019 to 0.59% at December 31, 2020. The Bank increased the provision in 2020 to reflect the continued growth of the loan portfolio along with the uncertain economic impact of the coronavirus pandemic. The allowance for loan losses increased from $3.1 million at December 31, 2019 to $4.1 million at December 31, 2020. The ratio of the allowance for loan losses to gross total loans (including loans held for sale) increased from 1.23% at year-end 2019 to 1.51% at year-end 2020. The Bank incurred net loan charge-offs of $121,000 in 2019, and realized net recoveries of $241,000 for 2020.

26

FELDMAN FINANCIAL ADVISORS, INC.

Table 5

Yield and Cost Summary

For the Years Ended December 31, 2018 to 2020

| Year Ended December 31, |

||||||||||||

| 2020 | 2019 | 2018 | ||||||||||

| Weighted Average Yields |

||||||||||||

| Loans receivable |

4.61 | % | 4.69 | 4.57 | % | |||||||

| Investment securities |

2.09 | 2.95 | 3.07 | |||||||||

| Interest-earning deposits |

0.92 | 1.87 | 1.28 | |||||||||

| Other interest-earning assets |

4.62 | 6.33 | 6.62 | |||||||||

| Total interest-earning assets |

4.12 | 4.32 | 4.11 | |||||||||

| Weighted Average Costs |

||||||||||||

| Savings and money market accounts |

0.63 | 0.99 | 0.79 | |||||||||

| Interest-bearing checking accounts |

0.07 | 0.24 | 0.18 | |||||||||

| Certificates of deposit |

1.53 | 1.82 | 1.24 | |||||||||

| Total interest-bearing deposits |

0.88 | 1.24 | 0.90 | |||||||||

| Borrowed funds |

1.14 | 2.48 | 2.61 | |||||||||

| Total interest-bearing liabilities |

0.89 | 1.25 | 0.92 | |||||||||

| Net interest rate spread (1) |

3.23 | 3.07 | 3.19 | |||||||||

| Net interest margin (2) |

3.38 | 3.26 | 3.35 | |||||||||

| (1) | Weighted average yield on interest-earning assets less the weighted average cost of interest-bearing liabilities. |

| (2) | Net interest income divided by average total interest-earning assets. |

Source: TC Federal Bank, financial data.

The Bank’s non-interest income primarily comprises service charges on deposit accounts, gains on sale of mortgage loans, gains on sale of securities, and BOLI income. The Bank’s non-interest income increased by $771,000 or 61.2% from $1.3 million in 2019 to $2.0 million in 2020. Gains on sale of securities decreased from $67,000 in 2019 to zero in 2020. BOLI income increased moderately by 1.7% from $296,000 in 2019 to $301,000 in 2020. As a result of the increased level of non-interest income, the ratio of non-interest income to average assets increased from 0.41% in 2019 to 0.60% for 2020.

27

FELDMAN FINANCIAL ADVISORS, INC.

Non-interest expense increased by $2.5 million or 27.2% from $9.1 million in 2019 to $11.6 million in 2020. The significant increase was due primarily to the impact of non-recurring items. The Bank experienced $1.1 million in expenses related to the conversion of the Bank’s core data processor to a new system. In addition, the Bank recognized $506,000 in previously deferred expenses associated with its delayed capital offering. In February 2020, the Bank adopted plans to pursue a minority stock offering under a mutual holding company structure. Due to market conditions being impacted by the coronavirus pandemic, the Bank decided to delay implementation of its capital until later in 2020 or 2021. Ultimately, the Bank elected to restructure its capital offering as a standard mutual-to-stock transaction and is currently pursuing implementation of the Stock Offering in 2021. Because of the delay in the capital offering, the expenses incurred earlier in 2020 were required to be charged to operations (instead of being deferred and deducted from the gross proceeds of the capital offering).

Salaries and employee benefits increased by $1.1 million or 21.0% from $5.3 million in 2019 to $6.4 million in 2020, primarily reflecting expansion of the Bank’s staff personnel. The number of full-time equivalent employees increased from 45 at December 31, 2019 to 54 at December 31, 2020. The increase in salaries and employee benefits was also related to the increased variable compensation paid to mortgage lenders as a result of increased lending volume in 2020. The ratio of non-interest expense to average assets increased from 2.99% for 2019 to 3.46% for 2020. Excluding the data processing conversion costs and expenses of the delayed capital offering, the Bank’s adjusted non-interest expense ratio would have measured 2.97% of average assets in 2020.

As discussed earlier, the Bank has placed considerable emphasis on enhancing operating efficiency and improving its historically high efficiency ratio. Although the Bank’s efficiency

28

FELDMAN FINANCIAL ADVISORS, INC.

ratio remains high in comparison to peers, it improved from 100.8% in 2017 to 95.2% in 2018 and 85.9% in 2019, before increasing to 91.2% because of the non-recurring items. (The efficiency ratio represents non-interest expense divided by the sum of net interest income and non-interest income exclusive of securities gains.) Operating expenses in prior years had been elevated by the opening of new offices, severance benefits, and increased expenses for professional services related to outside consultants and for checking account marketing programs. Excluding the impact of the data processing conversions costs and expenses of the delayed stock offering, the Bank’s adjusted efficiency ratio would have measured 78.3% in 2020.

The provision for income taxes decreased from $367,000 for the year ended December 31, 2019 to $40,000 for the year ended December 31, 2020. The effective income tax rate was approximately 23.3% and 11.4% for the years ended December 31, 2019 and 2020, respectively. The decline in the effective tax rate was due in part to the recognition of tax-exempt BOLI income offsetting the much lower level of pre-tax income in 2020.

Years Ended December 31, 2018 and 2019

Net income was $1.2 million for the year ended December 31, 2019, compared to net income of $679,000 for the year ended December 31, 2018, an increase of $528,000 or 77.8%. The increase was due to a $191,000 increase in net interest income, a $653,000 increase in non-interest income, and a $254,000 decrease in non-interest expense, offset partially by a change in the credit for loan losses from $551,000 in 2018 to zero in 2019. Net interest income increased by $181,000 from $9.3 million in 2018 to $9.5 million in 2019. This increase was due to an increase in the balance of interest-earning assets in 2019 versus 2018, offset by a decrease in the net interest rate spread to 3.07% for 2019 from 3.19% in 2018 and a decrease in the net interest margin to 3.26% for 2019 from 3.35% in 2018.

29

FELDMAN FINANCIAL ADVISORS, INC.

The decrease in the net interest rate spread and the net interest margin was primarily due to the increase in the average balance of interest-bearing liabilities from $224.9 million for the year ended December 31, 2018 to $247.2 million for the year ended December 31, 2019 and an increase in the weighted average rate paid on interest-bearing liabilities from 0.92% for the year ended December 31, 2018 to 1.25% for the year ended December 31, 2019. This decrease was partially offset by an increase in the average balances and yields on interest-earning assets. The Bank’s loan portfolio yield increased by 12 basis points from 4.57% in 2018 to 4.69% in 2019, while the securities portfolio yield decreased by 12 basis points from 3.07% in 2018 to 2.95% in 2019. The Bank’s yield on interest-earning deposits increased by 49 basis points from 1.28% in 2018 to 1.87% in 2019, reflecting higher market interest rates. As a result, the overall yield on total interest-earning assets increased by 21 basis points from 4.11% in 2018 to 4.32% in 2018.

While the Bank’s weighted average yield on interest-earning assets increased by 22 basis points from 4.11% in 2018 to 4.33% in 2019, the weighted average cost of interest-bearing liabilities increased further by 33 basis points from 0.92% to 1.25%. The Bank’s cost of interest-bearing deposits increased by 34 basis points from 0.90% in 2018 to 1.24% in 2019, primarily due to increases in rates paid on certificate accounts. The Bank’s cost of borrowings decreased by 13 basis points from 2.61% in 2018 to 2.48% in 2019, mainly due to the maturity of certain high-cost FHLB advances in 2018.

Based on management’s analysis of the allowance for loan losses, the Bank did not record a provision for loan losses for the year ended December 31, 2019 and credited the provision expense in an amount of $551,000 for the year ended December 31, 2018. The Bank’s allowance for loan losses was $3.1 million at December 31, 2019 as compared to $3.2 million at December 31, 2018. The ratio of the allowance for loan losses to total loans decreased to 1.23% at December

30

FELDMAN FINANCIAL ADVISORS, INC.

31, 2019 from 1.33% at December 31, 2018, and the ratio the allowance for loan losses to non-performing loans decreased to 118.3% at December 31, 2019 from 247.7% at December 31, 2018.